Detailed Analysis of Goodman Group: Focusing on Equity and Tax Aspects

VerifiedAdded on 2024/04/26

|9

|2570

|87

Report

AI Summary

This report provides a detailed analysis of Goodman Group's financial statements, focusing on changes in equity capital, tax expenses, deferred tax assets and liabilities, and current tax payable. The analysis covers the fiscal years 2016 and 2017, examining the differences between reported tax expenses and calculated tax liabilities based on prevailing tax rates. The report also delves into the reasons for discrepancies, such as profits allocated to unitholders and non-assessable items. Furthermore, it addresses the management's approach to recognizing deferred taxes on assets and liabilities, including investment properties and receivables. The report also discusses the critical aspects of the annual statements, including credit and liquidity risk management. The income tax presented in the cash flow statement is reconciled with the income tax expense and current tax payable, highlighting the components contributing to the variance. Desklib provides students access to similar solved assignments and past papers.

Table of Contents

Introduction.................................................................................................................................................2

Content of the project.................................................................................................................................2

Part 1 – Analysis of changes in equity capital.........................................................................................2

Tax expenses stated by the business........................................................................................................4

Tax rates as stated by the business...........................................................................................................4

Deferred tax asset and liabilities..............................................................................................................5

Current tax payable by the management..................................................................................................6

Income tax in cash flow statement...........................................................................................................7

Critical aspects from the annual statements.............................................................................................7

Conclusion...................................................................................................................................................8

References...................................................................................................................................................9

Introduction.................................................................................................................................................2

Content of the project.................................................................................................................................2

Part 1 – Analysis of changes in equity capital.........................................................................................2

Tax expenses stated by the business........................................................................................................4

Tax rates as stated by the business...........................................................................................................4

Deferred tax asset and liabilities..............................................................................................................5

Current tax payable by the management..................................................................................................6

Income tax in cash flow statement...........................................................................................................7

Critical aspects from the annual statements.............................................................................................7

Conclusion...................................................................................................................................................8

References...................................................................................................................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The main theme of the given project is to read briefly the annual report of a chosen company and

analyse in detail the various financial terms like the equity of the company, tax expenses paid by

the firm to the government, the tax rate applied, status on the deferred tax towards key assets and

liabilities the method implemented by the management in reognising such deferred taxes, if there

is any income tax payable by the company towards the government and to breifly attempt the key

understanding of the financial statements which is presented to the stakeholders. The company

which is considered for this analysis is Goodman group staples. The firms is founded in the year

1929, the firm is mainly involved in real estate which covers the range of large sized warehouse

facilities, logistics aspects, business complext, office parks etc. therefore they are mainly

categorised as the commercial real estate developers. The company was listed in the ASX in

1995, in 2000 there was a merger between the companies of Goodman and Macquaire, in 2007

the company was named as Goodman group and currently it is the largest builders and providers

of industrial property and other commercial spaces for many in the world, the company has

slowly expanded into various countries in Asia, Americas and the Europe. This was achieved

through clear organic growth of the company and the acquisitions. The company owns more than

450 properties in nearly 15 countries, also the company is having nearly 50 properties under

development, the business has generated more than $2 billion annually and the net profits is

nearly $650 million. It should be noted that the Goodman group is split into three different

divisions: Goodman limited, Goodman trust and Goodman logistis, this assignment is focused on

Goodman group which covers all three divisions.

Content of the project

Part 1 – Analysis of changes in equity capital

The first part of the project is to analyse in detail the current capital structure of the company and

to compare with the previous years, the current year is considered as 2017 and the previous year

is stated as 2016.

The main theme of the given project is to read briefly the annual report of a chosen company and

analyse in detail the various financial terms like the equity of the company, tax expenses paid by

the firm to the government, the tax rate applied, status on the deferred tax towards key assets and

liabilities the method implemented by the management in reognising such deferred taxes, if there

is any income tax payable by the company towards the government and to breifly attempt the key

understanding of the financial statements which is presented to the stakeholders. The company

which is considered for this analysis is Goodman group staples. The firms is founded in the year

1929, the firm is mainly involved in real estate which covers the range of large sized warehouse

facilities, logistics aspects, business complext, office parks etc. therefore they are mainly

categorised as the commercial real estate developers. The company was listed in the ASX in

1995, in 2000 there was a merger between the companies of Goodman and Macquaire, in 2007

the company was named as Goodman group and currently it is the largest builders and providers

of industrial property and other commercial spaces for many in the world, the company has

slowly expanded into various countries in Asia, Americas and the Europe. This was achieved

through clear organic growth of the company and the acquisitions. The company owns more than

450 properties in nearly 15 countries, also the company is having nearly 50 properties under

development, the business has generated more than $2 billion annually and the net profits is

nearly $650 million. It should be noted that the Goodman group is split into three different

divisions: Goodman limited, Goodman trust and Goodman logistis, this assignment is focused on

Goodman group which covers all three divisions.

Content of the project

Part 1 – Analysis of changes in equity capital

The first part of the project is to analyse in detail the current capital structure of the company and

to compare with the previous years, the current year is considered as 2017 and the previous year

is stated as 2016.

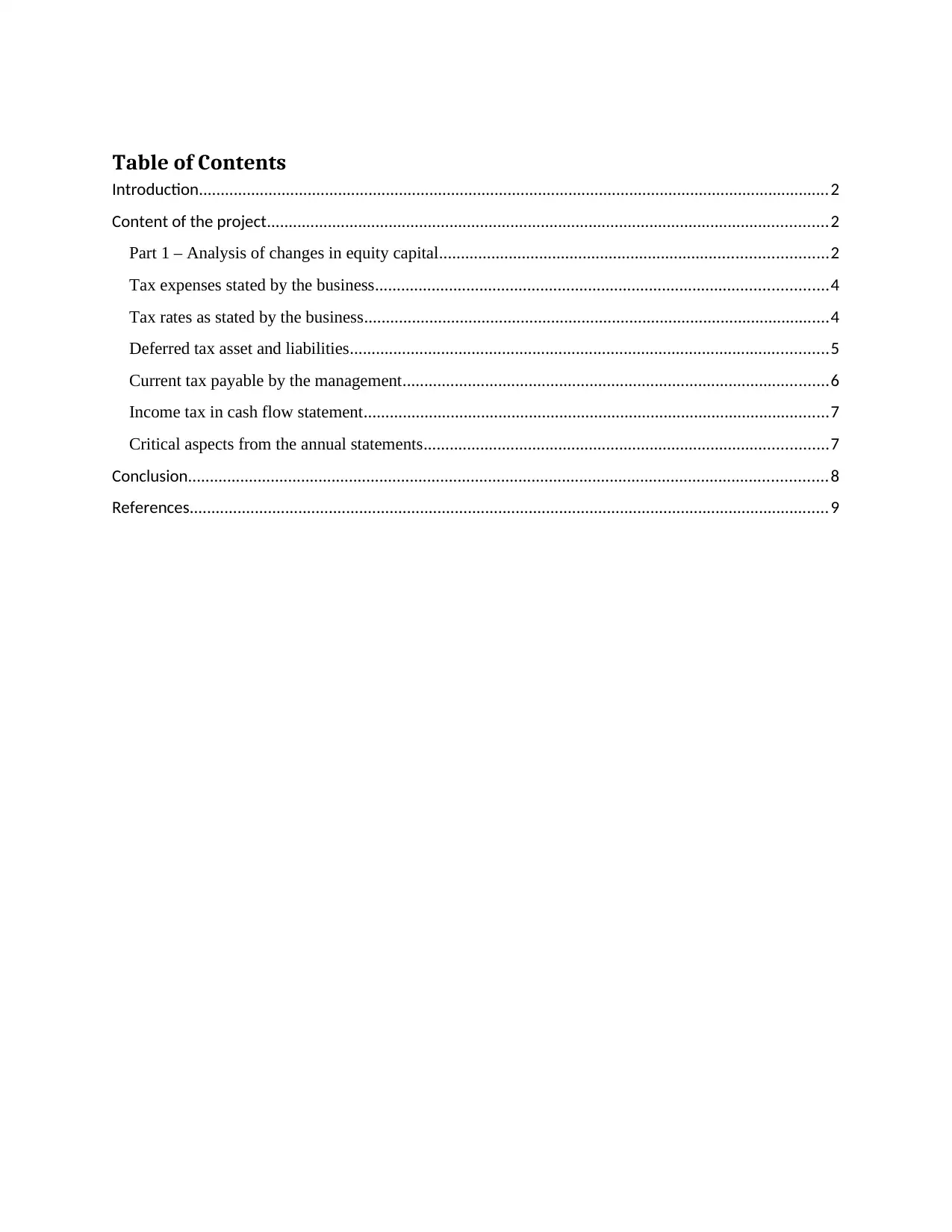

Based on the annual report of the company it is identified that the total equity of the group is

shown as 8.6 billion in 2017 whereas in the previous year the total equity is stated as 8.3 billion,

which shows that there is an increase of nearly 300 million between the years. The toal equty of

the limited company has reduced due to the increase in the acumulated loss, however the equity

of the trust company and the logistics company has incrased which resulted in increase in the

total equity of Goodman group. (Goodman, 2017)

From the Notes to the annual report 16(a) it is identified that the issued capital of the group

remains the same, with the total issued capital is 8.03 billion and the total number of securities

issued stood at 1.78 billion.

The notes also mentions the meaning of stapled security, which states tha 1 share of stapled

security is a combinatio of 1 unit of shares in Trust company and 1 unit of CDI unit over the

logistics units, the shareholders of the stapled are permitted to get the dividends as declared by

the management and is also entitled to vote in the AGM, during the time of liquidation of the

company, the security holders will get the proceedings at the last. The total equity of the capital

is mainly contributed by the issued capital, reserves of the business unit and the retained earnings

of the firm after distributing the profits to the shareholders.

shown as 8.6 billion in 2017 whereas in the previous year the total equity is stated as 8.3 billion,

which shows that there is an increase of nearly 300 million between the years. The toal equty of

the limited company has reduced due to the increase in the acumulated loss, however the equity

of the trust company and the logistics company has incrased which resulted in increase in the

total equity of Goodman group. (Goodman, 2017)

From the Notes to the annual report 16(a) it is identified that the issued capital of the group

remains the same, with the total issued capital is 8.03 billion and the total number of securities

issued stood at 1.78 billion.

The notes also mentions the meaning of stapled security, which states tha 1 share of stapled

security is a combinatio of 1 unit of shares in Trust company and 1 unit of CDI unit over the

logistics units, the shareholders of the stapled are permitted to get the dividends as declared by

the management and is also entitled to vote in the AGM, during the time of liquidation of the

company, the security holders will get the proceedings at the last. The total equity of the capital

is mainly contributed by the issued capital, reserves of the business unit and the retained earnings

of the firm after distributing the profits to the shareholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

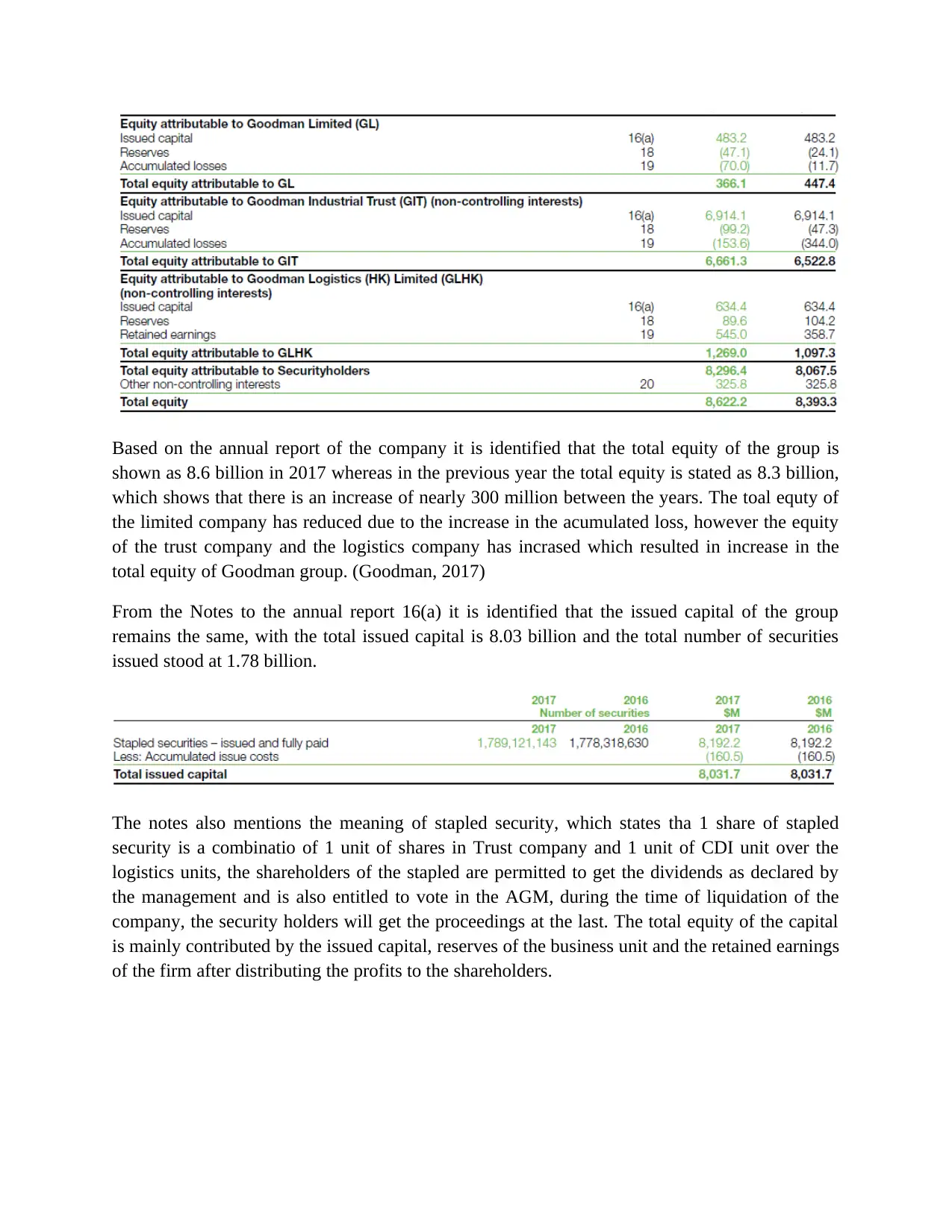

The total reserves of the company for the year 2017 is -56 million whereas in 2016 the reserves

were a positive 32 million, the main reason is the loss in the foreign currency reserve with 149

million, also other reserves like asset revaluation, cash flow hedge and defined benefit funds also

possess loss. The only positive generated reserve is the employee compensation reserve of the

company.

Tax expenses stated by the business

Based on the financial statement of 2017, it is idetntified that the tax expense which is projected

for the year 2017 is 54 million, however the net profit before tax is stated as 851 million,

similarly for the year 2016 the tax expense is stated as 75.6 million for the net profit before tax

value of 1,370 million.

This shows that the tax expense of the compay has reduced significantly in 2017 when compared

with 2016, this is due to the decrease in the profit before tax values.

Tax rates as stated by the business

With the prevailing tax rate stated by the government it is noted that the rate is 30% on the

profits before tax, as per the consolidated financial statement the profit before tax for the year

2017 is 851.2 million, so with the applicable tax rate the income tax expense needs to be

= 851.2 x 30 / 100 = 255.36 million

Similarly for the year 2016 the profit before tax is 1,370.3 million by applying the same rate the

tax should be computed as

= 1,370.3 x 30 / 100 = 411.09 million

However, the financial statement has projected the tax expense as 54 milion for 2017 and 75.6

million for 2016. The reason is stated as follows:

were a positive 32 million, the main reason is the loss in the foreign currency reserve with 149

million, also other reserves like asset revaluation, cash flow hedge and defined benefit funds also

possess loss. The only positive generated reserve is the employee compensation reserve of the

company.

Tax expenses stated by the business

Based on the financial statement of 2017, it is idetntified that the tax expense which is projected

for the year 2017 is 54 million, however the net profit before tax is stated as 851 million,

similarly for the year 2016 the tax expense is stated as 75.6 million for the net profit before tax

value of 1,370 million.

This shows that the tax expense of the compay has reduced significantly in 2017 when compared

with 2016, this is due to the decrease in the profit before tax values.

Tax rates as stated by the business

With the prevailing tax rate stated by the government it is noted that the rate is 30% on the

profits before tax, as per the consolidated financial statement the profit before tax for the year

2017 is 851.2 million, so with the applicable tax rate the income tax expense needs to be

= 851.2 x 30 / 100 = 255.36 million

Similarly for the year 2016 the profit before tax is 1,370.3 million by applying the same rate the

tax should be computed as

= 1,370.3 x 30 / 100 = 411.09 million

However, the financial statement has projected the tax expense as 54 milion for 2017 and 75.6

million for 2016. The reason is stated as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

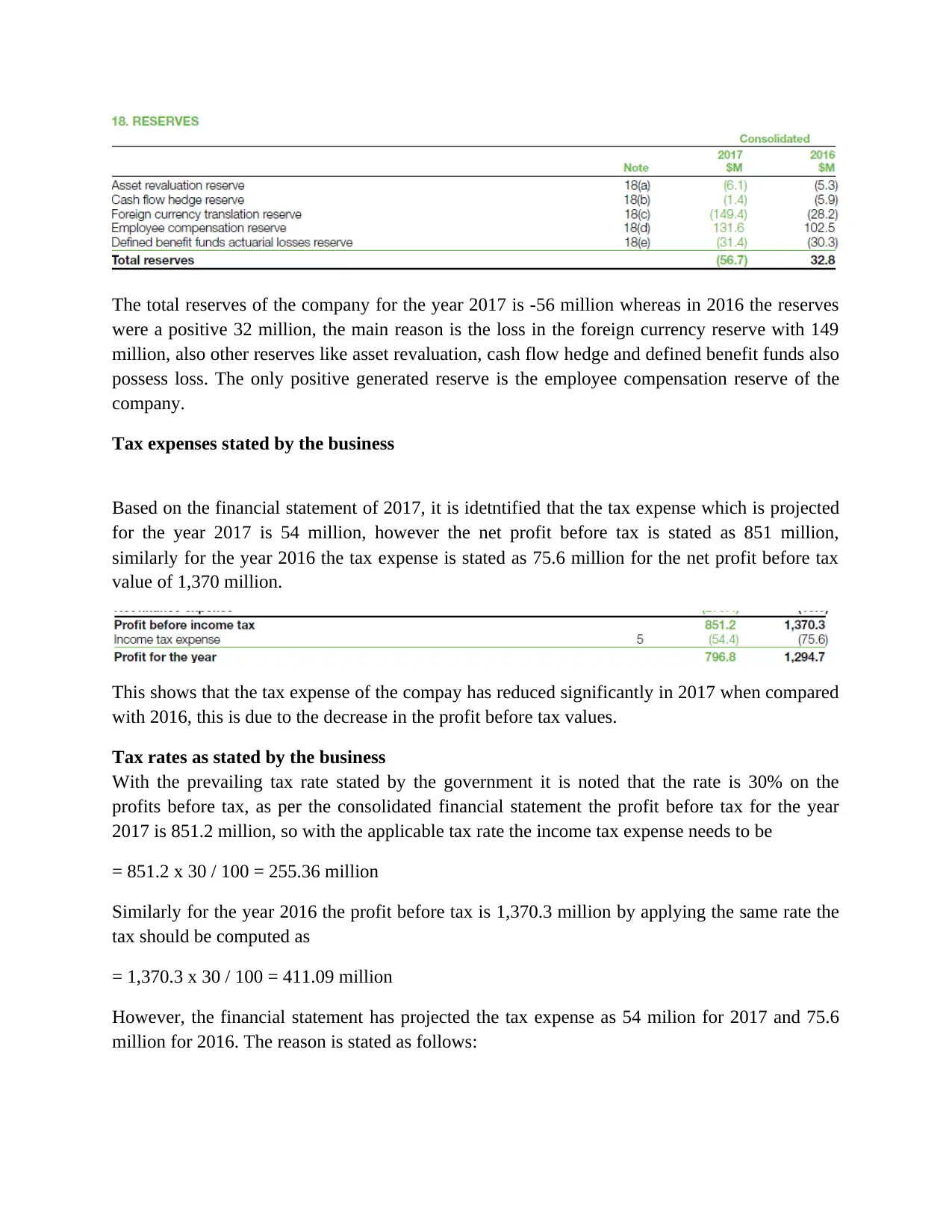

The adjustment is mainly attributed due to the profit which needs to be allocated to the

unitholders, the non-assessable item included in the financial statement and unrecognised tax

losses etc. has made the tax expense to be lower than the actual computation. Therefore the

estimated tax expense to the company for the year 2017 is stated as 54.4 million and similarly for

the year 2016 it is attributed to be 75.6 million. (Goodman, 2017)

Deferred tax asset and liabilities

The complete details of the deferred tax attributed by the management on the assets and

liabilities are briefly stated as under:

The major aspect of the deferred tax on assets / liabilities is recognised based on the provisional

variations among the carrying value of such items and the amount which is mainly applied for

taxation purpose. The following categories are not recognised in deferred tax as they tend to be

tested for impairment. Balance sheet items like goodwill; recognition of assets / liabilties which

may not impact the profit for taxation purpose; differences pertaining to the overall investments

in the controlled entities. It is noted in the annual report that the deferred tax towards the assets /

liabilities is mainly attributed to the receivavbles of the firm, properties, payables by the

management to their creditors and provisions. The value of the deferred tax is mainly based on

the expected aspect of such realisation or the settlement made by the management on the

carrying value of the stated assets / liabilities. The major contributor of the deferred tax assets is

the investment properties, therefore the management applies the fair value recognition of such

assets. They are mainly computed based on the assumption that such carrying value tend to be

recognised through the overall sale of such assets, the deferred tax on such assets is recognised

based on the future profits which is compared against the asset utilised by the management. Also

unitholders, the non-assessable item included in the financial statement and unrecognised tax

losses etc. has made the tax expense to be lower than the actual computation. Therefore the

estimated tax expense to the company for the year 2017 is stated as 54.4 million and similarly for

the year 2016 it is attributed to be 75.6 million. (Goodman, 2017)

Deferred tax asset and liabilities

The complete details of the deferred tax attributed by the management on the assets and

liabilities are briefly stated as under:

The major aspect of the deferred tax on assets / liabilities is recognised based on the provisional

variations among the carrying value of such items and the amount which is mainly applied for

taxation purpose. The following categories are not recognised in deferred tax as they tend to be

tested for impairment. Balance sheet items like goodwill; recognition of assets / liabilties which

may not impact the profit for taxation purpose; differences pertaining to the overall investments

in the controlled entities. It is noted in the annual report that the deferred tax towards the assets /

liabilities is mainly attributed to the receivavbles of the firm, properties, payables by the

management to their creditors and provisions. The value of the deferred tax is mainly based on

the expected aspect of such realisation or the settlement made by the management on the

carrying value of the stated assets / liabilities. The major contributor of the deferred tax assets is

the investment properties, therefore the management applies the fair value recognition of such

assets. They are mainly computed based on the assumption that such carrying value tend to be

recognised through the overall sale of such assets, the deferred tax on such assets is recognised

based on the future profits which is compared against the asset utilised by the management. Also

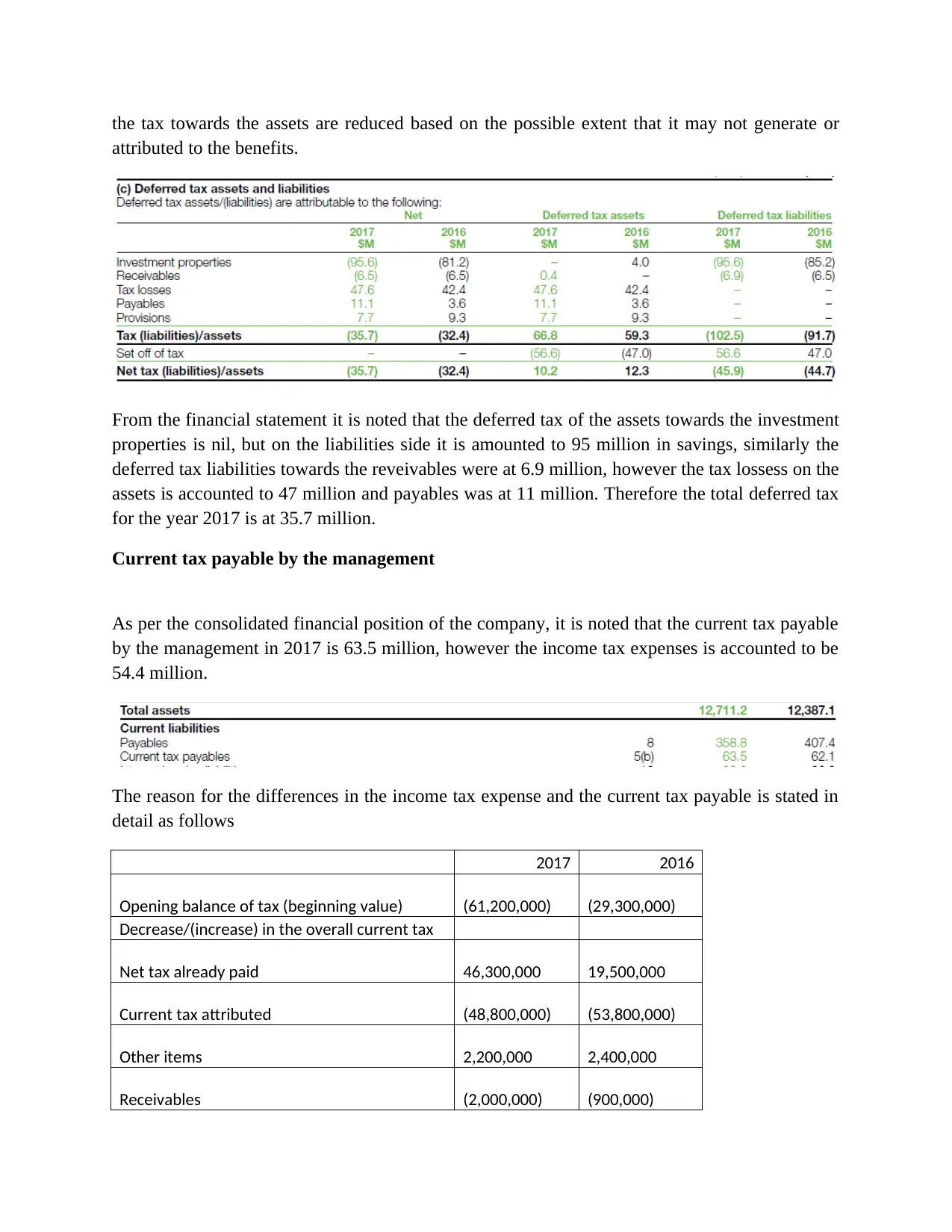

the tax towards the assets are reduced based on the possible extent that it may not generate or

attributed to the benefits.

From the financial statement it is noted that the deferred tax of the assets towards the investment

properties is nil, but on the liabilities side it is amounted to 95 million in savings, similarly the

deferred tax liabilities towards the reveivables were at 6.9 million, however the tax lossess on the

assets is accounted to 47 million and payables was at 11 million. Therefore the total deferred tax

for the year 2017 is at 35.7 million.

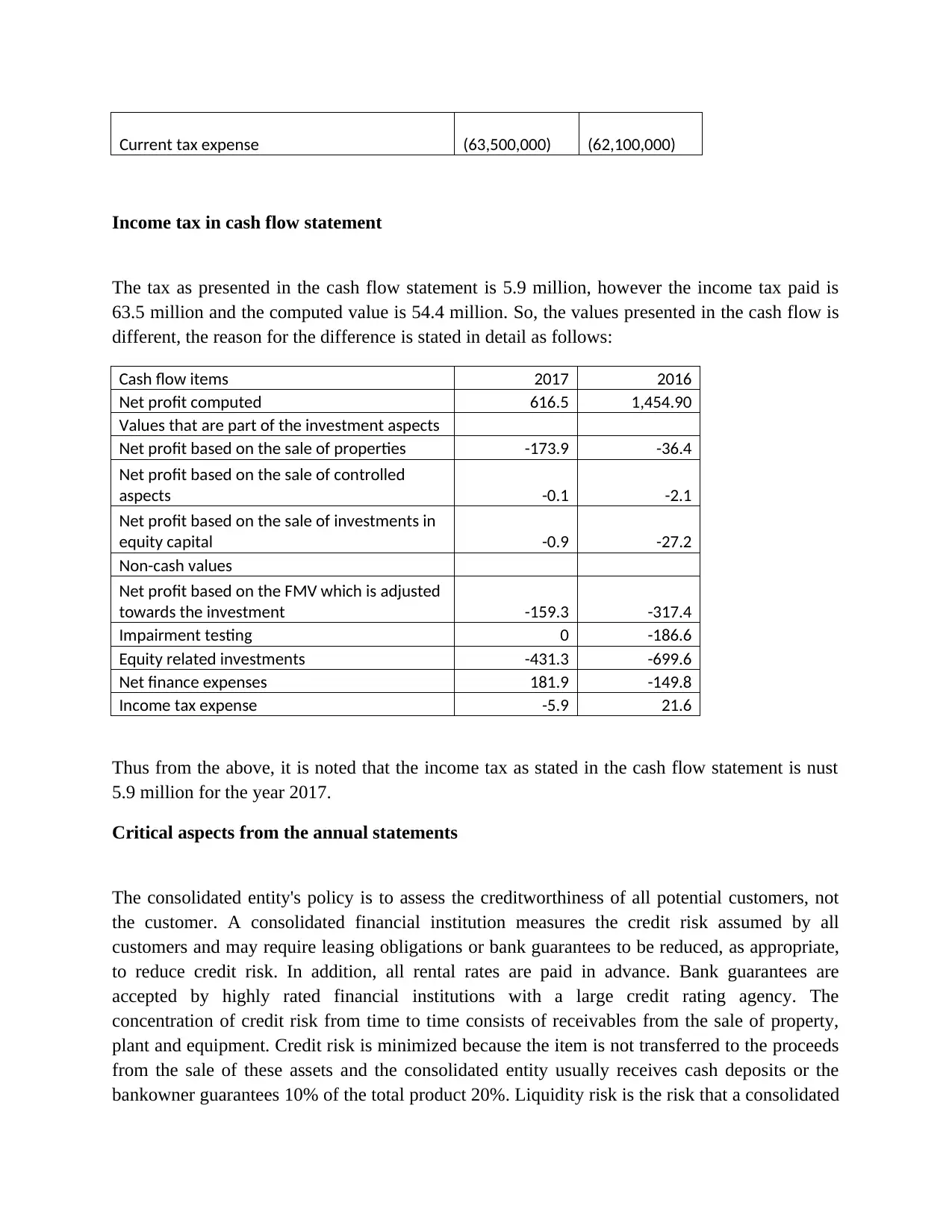

Current tax payable by the management

As per the consolidated financial position of the company, it is noted that the current tax payable

by the management in 2017 is 63.5 million, however the income tax expenses is accounted to be

54.4 million.

The reason for the differences in the income tax expense and the current tax payable is stated in

detail as follows

2017 2016

Opening balance of tax (beginning value) (61,200,000) (29,300,000)

Decrease/(increase) in the overall current tax

Net tax already paid 46,300,000 19,500,000

Current tax attributed (48,800,000) (53,800,000)

Other items 2,200,000 2,400,000

Receivables (2,000,000) (900,000)

attributed to the benefits.

From the financial statement it is noted that the deferred tax of the assets towards the investment

properties is nil, but on the liabilities side it is amounted to 95 million in savings, similarly the

deferred tax liabilities towards the reveivables were at 6.9 million, however the tax lossess on the

assets is accounted to 47 million and payables was at 11 million. Therefore the total deferred tax

for the year 2017 is at 35.7 million.

Current tax payable by the management

As per the consolidated financial position of the company, it is noted that the current tax payable

by the management in 2017 is 63.5 million, however the income tax expenses is accounted to be

54.4 million.

The reason for the differences in the income tax expense and the current tax payable is stated in

detail as follows

2017 2016

Opening balance of tax (beginning value) (61,200,000) (29,300,000)

Decrease/(increase) in the overall current tax

Net tax already paid 46,300,000 19,500,000

Current tax attributed (48,800,000) (53,800,000)

Other items 2,200,000 2,400,000

Receivables (2,000,000) (900,000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current tax expense (63,500,000) (62,100,000)

Income tax in cash flow statement

The tax as presented in the cash flow statement is 5.9 million, however the income tax paid is

63.5 million and the computed value is 54.4 million. So, the values presented in the cash flow is

different, the reason for the difference is stated in detail as follows:

Cash flow items 2017 2016

Net profit computed 616.5 1,454.90

Values that are part of the investment aspects

Net profit based on the sale of properties -173.9 -36.4

Net profit based on the sale of controlled

aspects -0.1 -2.1

Net profit based on the sale of investments in

equity capital -0.9 -27.2

Non-cash values

Net profit based on the FMV which is adjusted

towards the investment -159.3 -317.4

Impairment testing 0 -186.6

Equity related investments -431.3 -699.6

Net finance expenses 181.9 -149.8

Income tax expense -5.9 21.6

Thus from the above, it is noted that the income tax as stated in the cash flow statement is nust

5.9 million for the year 2017.

Critical aspects from the annual statements

The consolidated entity's policy is to assess the creditworthiness of all potential customers, not

the customer. A consolidated financial institution measures the credit risk assumed by all

customers and may require leasing obligations or bank guarantees to be reduced, as appropriate,

to reduce credit risk. In addition, all rental rates are paid in advance. Bank guarantees are

accepted by highly rated financial institutions with a large credit rating agency. The

concentration of credit risk from time to time consists of receivables from the sale of property,

plant and equipment. Credit risk is minimized because the item is not transferred to the proceeds

from the sale of these assets and the consolidated entity usually receives cash deposits or the

bankowner guarantees 10% of the total product 20%. Liquidity risk is the risk that a consolidated

Income tax in cash flow statement

The tax as presented in the cash flow statement is 5.9 million, however the income tax paid is

63.5 million and the computed value is 54.4 million. So, the values presented in the cash flow is

different, the reason for the difference is stated in detail as follows:

Cash flow items 2017 2016

Net profit computed 616.5 1,454.90

Values that are part of the investment aspects

Net profit based on the sale of properties -173.9 -36.4

Net profit based on the sale of controlled

aspects -0.1 -2.1

Net profit based on the sale of investments in

equity capital -0.9 -27.2

Non-cash values

Net profit based on the FMV which is adjusted

towards the investment -159.3 -317.4

Impairment testing 0 -186.6

Equity related investments -431.3 -699.6

Net finance expenses 181.9 -149.8

Income tax expense -5.9 21.6

Thus from the above, it is noted that the income tax as stated in the cash flow statement is nust

5.9 million for the year 2017.

Critical aspects from the annual statements

The consolidated entity's policy is to assess the creditworthiness of all potential customers, not

the customer. A consolidated financial institution measures the credit risk assumed by all

customers and may require leasing obligations or bank guarantees to be reduced, as appropriate,

to reduce credit risk. In addition, all rental rates are paid in advance. Bank guarantees are

accepted by highly rated financial institutions with a large credit rating agency. The

concentration of credit risk from time to time consists of receivables from the sale of property,

plant and equipment. Credit risk is minimized because the item is not transferred to the proceeds

from the sale of these assets and the consolidated entity usually receives cash deposits or the

bankowner guarantees 10% of the total product 20%. Liquidity risk is the risk that a consolidated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial unit will not be able to meet its financial obligations as they become receivables. The

Group Unit intends to maintain sufficient liquidity to finance working capital, capital costs,

investment opportunities, delays and dividends. This can be achieved by preparing a three-year

cash forecast each month to understand the use of funds and identify potential funding shortages.

This allows the consolidated entity to plan renewal of credit facilities, credit negotiations, new

issues, including DRP and other possible funding sources. The Goodman Group's mandate is to

inform the Board of the details of delays at regular meetings. The mandate of Goodman Group is

also responsible for sending all information and records on the Board of Finance Agreements

reviewed and approved by the consolidated entity (consolidated). (Goodman, 2017)

Receivables include loans to related parties, accounts receivable and other receivables and are

reported at the time of formation, initially in the form of transaction costs, valued at fair value

and directly. After initial recognition, receivables are reported at accrued acquisition value using

the effective interest method less impairment losses. A consolidated company loses a claim when

its contractual cash flow rights cease or transfer the right to contractual cash flows from the

obligation to a transaction where the risk and benefit of all receivables are substantially

unavoidable. The carrying amount of receivables should be determined at each balance sheet

date to determine if there is any indication of impairment. If that is the case, the asset's present

value is reported of the estimated future cash flows discounted below the real interest rate. Write-

downs are recognized in the income statement during the period in which they are presented. The

recoverable amount of the Group company's receivables is calculated as the present value of the

estimated future cash flows discounted at amortized cost at the original effective interest rate (ie

the effective interest rate). the financial instruments calculated at the time of the introduction).

Short-term receivables are not reported. The external valuation estimates are usually not

dedicated to property development, but are directly attributable to the company, but estimates are

more likely to be determined by feasibility studies to support recent developments lvimento. The

final prices of feasibility studies are based on leverage conditions, rest periods and assumptions

of profit and risk-adjusted incentives on the relevant market. This profit and risk factor depends

on the business, location and size of growth, and generally ranges from 10 to 15%. In practice,

practice for determining fair value can be applied to the adequacy of growth . The interests of a

consolidated entity in partnership. However, some associations receive annual valuation

estimates for underlying investment in real estate.

Conclusion

Thus from the above a detailed analysis of key financial terms of Goodman group was discussed,

one of the critical element noted is on the income tax expense which is stated in different

statements like the consolidated income statement, cash flow statement etc.

Group Unit intends to maintain sufficient liquidity to finance working capital, capital costs,

investment opportunities, delays and dividends. This can be achieved by preparing a three-year

cash forecast each month to understand the use of funds and identify potential funding shortages.

This allows the consolidated entity to plan renewal of credit facilities, credit negotiations, new

issues, including DRP and other possible funding sources. The Goodman Group's mandate is to

inform the Board of the details of delays at regular meetings. The mandate of Goodman Group is

also responsible for sending all information and records on the Board of Finance Agreements

reviewed and approved by the consolidated entity (consolidated). (Goodman, 2017)

Receivables include loans to related parties, accounts receivable and other receivables and are

reported at the time of formation, initially in the form of transaction costs, valued at fair value

and directly. After initial recognition, receivables are reported at accrued acquisition value using

the effective interest method less impairment losses. A consolidated company loses a claim when

its contractual cash flow rights cease or transfer the right to contractual cash flows from the

obligation to a transaction where the risk and benefit of all receivables are substantially

unavoidable. The carrying amount of receivables should be determined at each balance sheet

date to determine if there is any indication of impairment. If that is the case, the asset's present

value is reported of the estimated future cash flows discounted below the real interest rate. Write-

downs are recognized in the income statement during the period in which they are presented. The

recoverable amount of the Group company's receivables is calculated as the present value of the

estimated future cash flows discounted at amortized cost at the original effective interest rate (ie

the effective interest rate). the financial instruments calculated at the time of the introduction).

Short-term receivables are not reported. The external valuation estimates are usually not

dedicated to property development, but are directly attributable to the company, but estimates are

more likely to be determined by feasibility studies to support recent developments lvimento. The

final prices of feasibility studies are based on leverage conditions, rest periods and assumptions

of profit and risk-adjusted incentives on the relevant market. This profit and risk factor depends

on the business, location and size of growth, and generally ranges from 10 to 15%. In practice,

practice for determining fair value can be applied to the adequacy of growth . The interests of a

consolidated entity in partnership. However, some associations receive annual valuation

estimates for underlying investment in real estate.

Conclusion

Thus from the above a detailed analysis of key financial terms of Goodman group was discussed,

one of the critical element noted is on the income tax expense which is stated in different

statements like the consolidated income statement, cash flow statement etc.

References

Brigham, E. F. (2010). Financial Management: Theory & Practice. 5th edition. Cengage

Learning.

Brooks, R. M. (2012). Financial Management. 4th edition. Prentice Hall.

Goodman Group (2017). Annual report of Goodman group

Kaplan, R. S., & Young, M. S. (2011). Management Accounting. 3rd edition. Prentice Hall.

Ray, G., & Eric, N. (2011). Managerial Accounting. McGraw-Hill/Irwin.

Titman, S. J. (2010). Financial Management. Prentice Hall.

Brigham, E. F. (2010). Financial Management: Theory & Practice. 5th edition. Cengage

Learning.

Brooks, R. M. (2012). Financial Management. 4th edition. Prentice Hall.

Goodman Group (2017). Annual report of Goodman group

Kaplan, R. S., & Young, M. S. (2011). Management Accounting. 3rd edition. Prentice Hall.

Ray, G., & Eric, N. (2011). Managerial Accounting. McGraw-Hill/Irwin.

Titman, S. J. (2010). Financial Management. Prentice Hall.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.