Goodwill and Consolidation: Patagonia Ltd and Salto Ltd

VerifiedAdded on 2023/04/21

|5

|887

|279

Homework Assignment

AI Summary

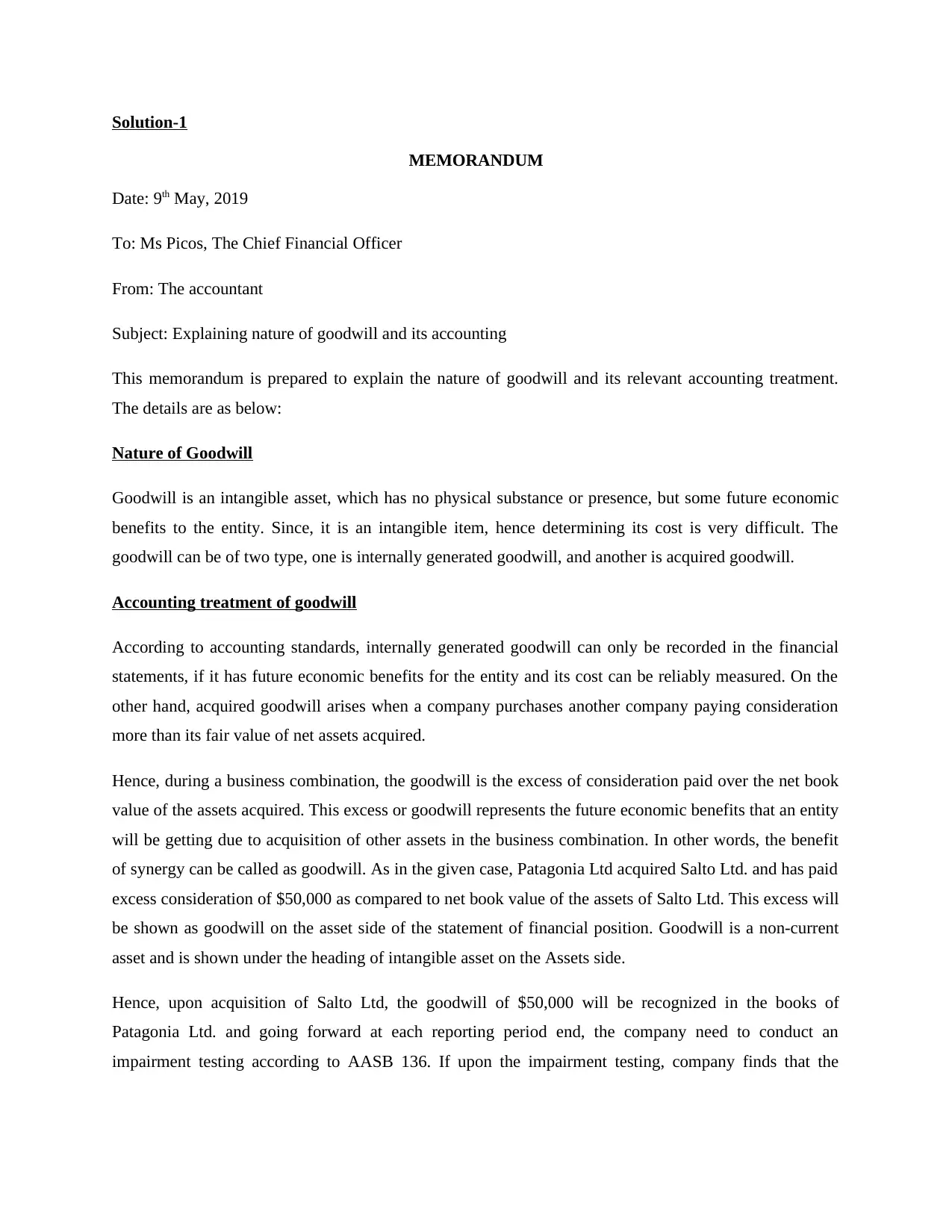

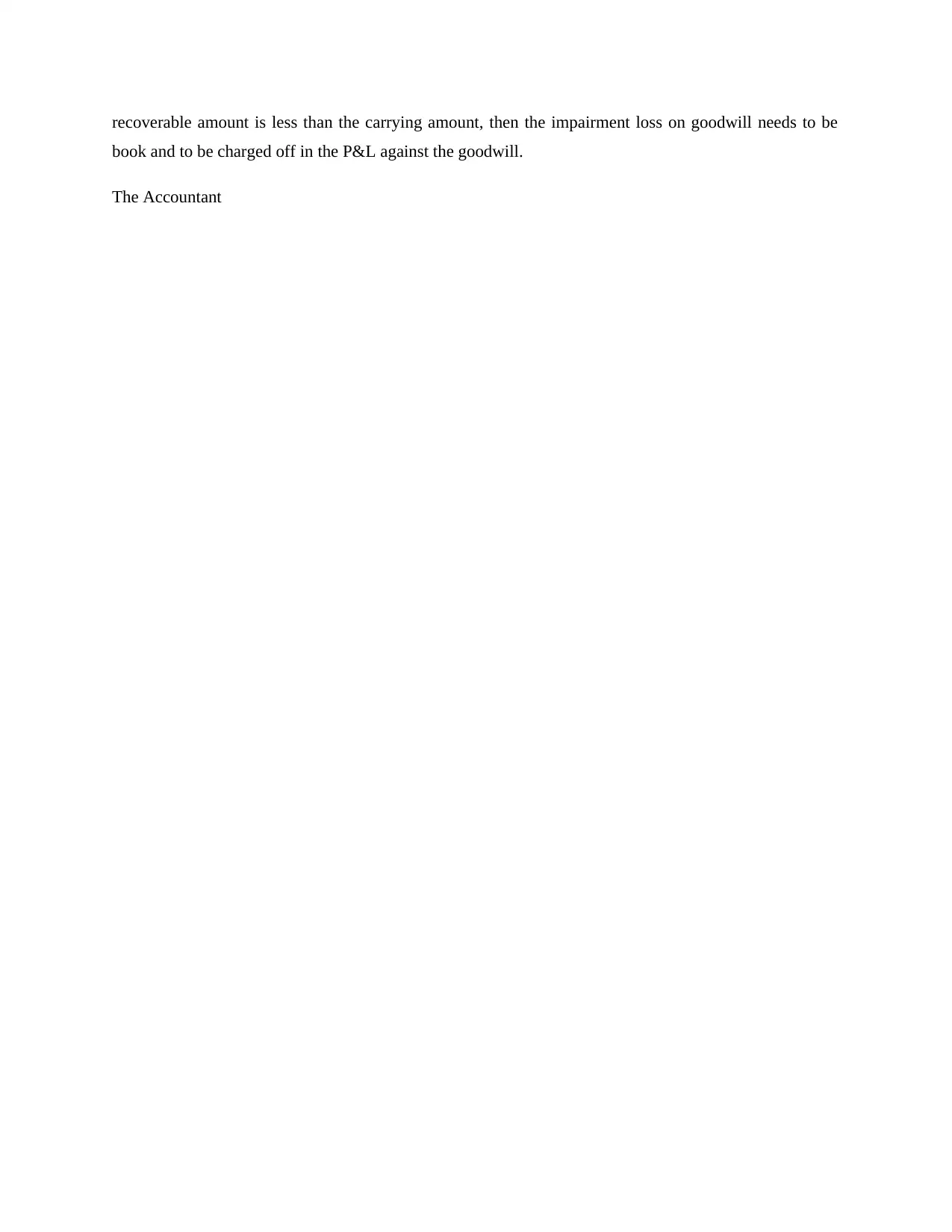

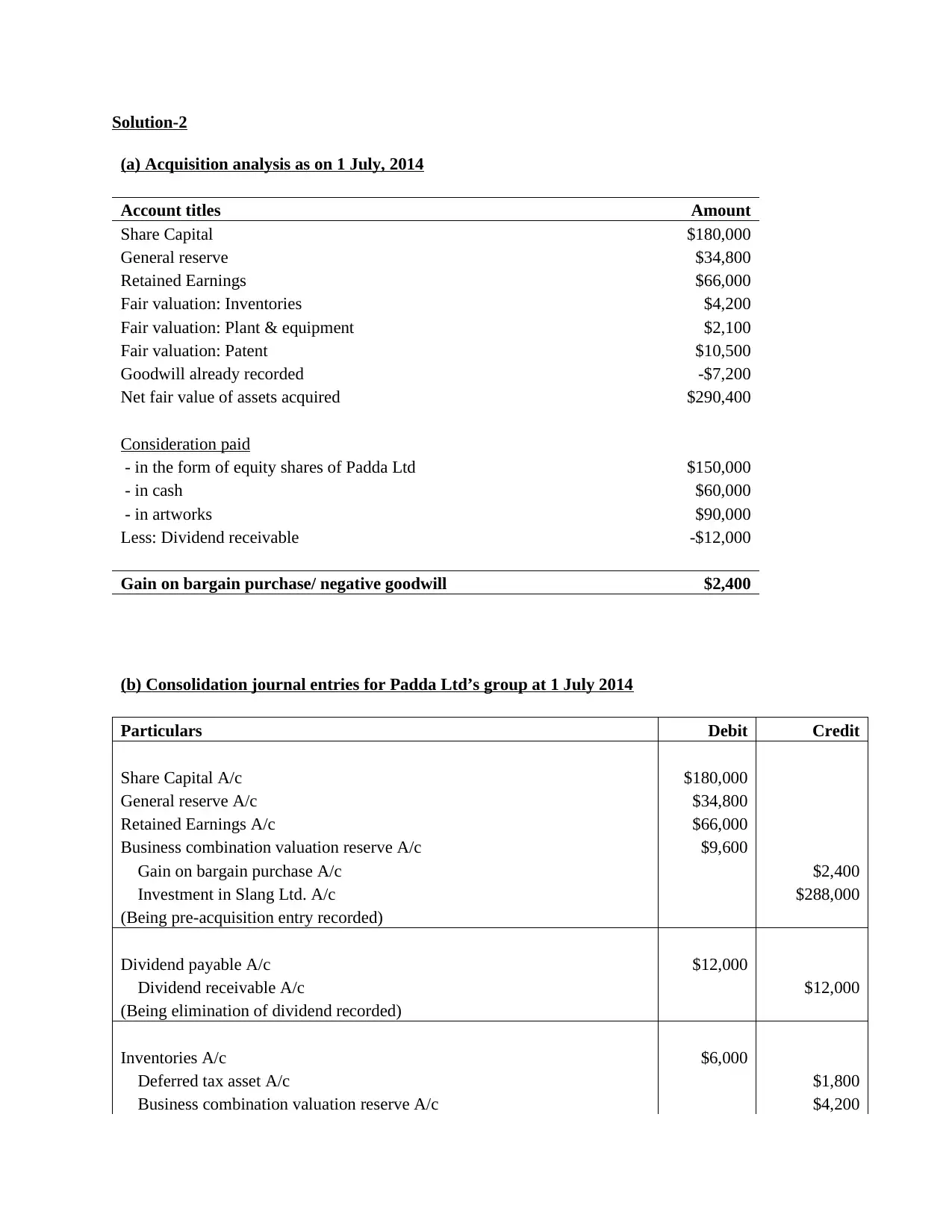

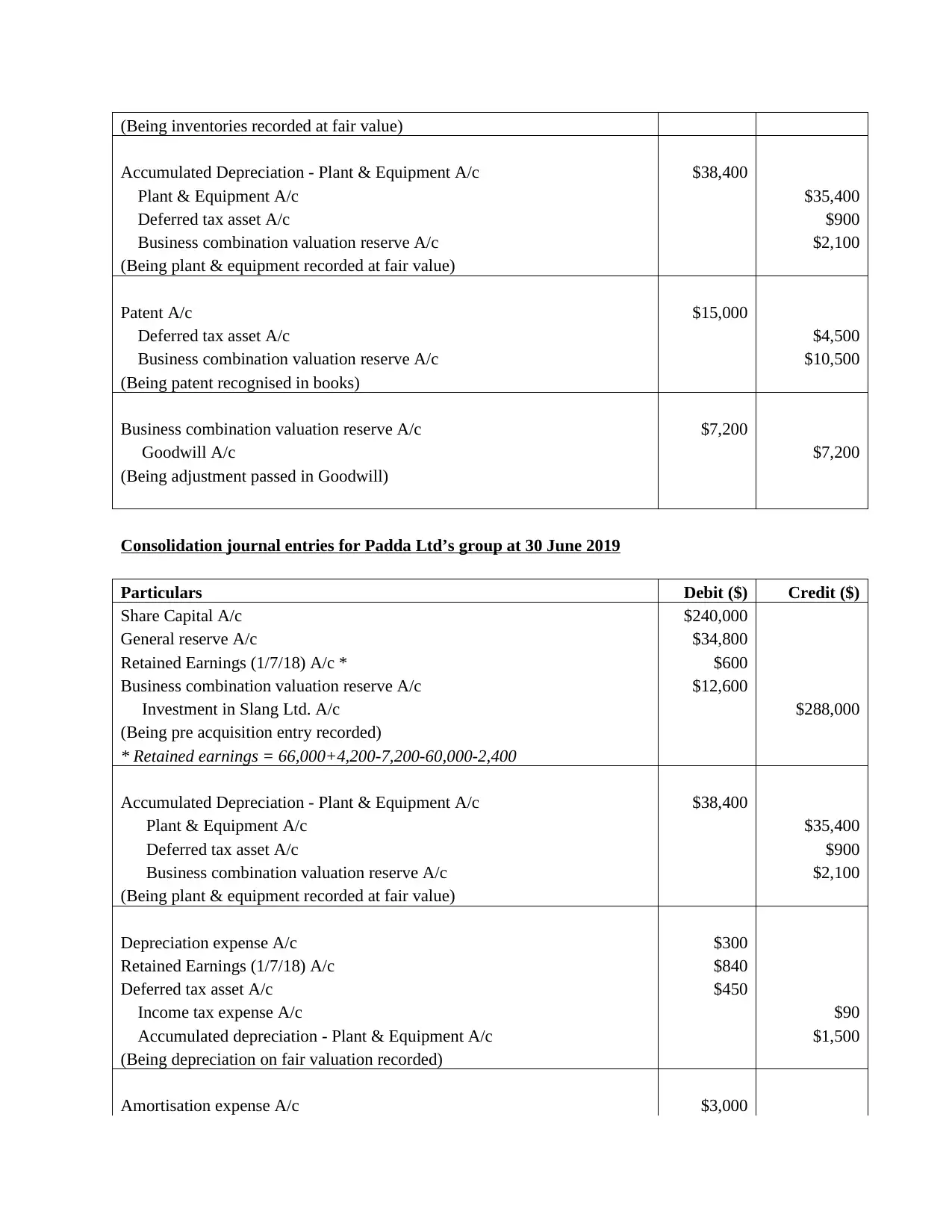

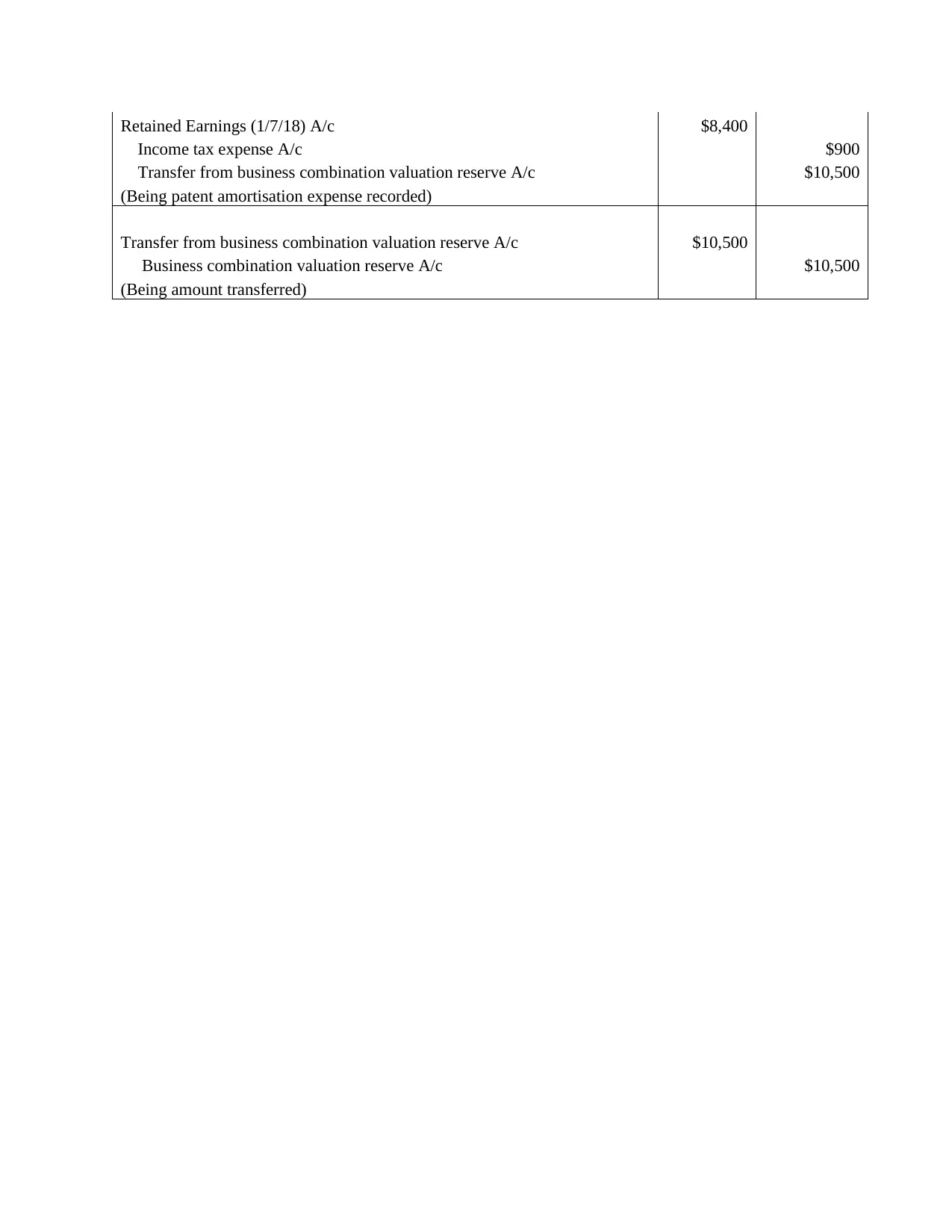

This document presents a memorandum explaining the nature of goodwill and its accounting treatment, including the distinction between internally generated and acquired goodwill. It details the recognition of goodwill in the financial statements, impairment testing, and the application of AASB 136. The document also provides acquisition analysis for Patagonia Ltd's acquisition of Salto Ltd, and Padda Ltd's acquisition of Slang Ltd. It includes journal entries for consolidation at different dates, demonstrating how to account for various items such as share capital, reserves, fair value adjustments, and bargain purchases. The solutions detail the accounting procedures for business combinations, including the handling of goodwill and other relevant financial aspects of the transactions.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.