Goodwill Impairment Analysis: GAAP, IFRS, and Corporate Practices

VerifiedAdded on 2023/05/31

|22

|1556

|92

Report

AI Summary

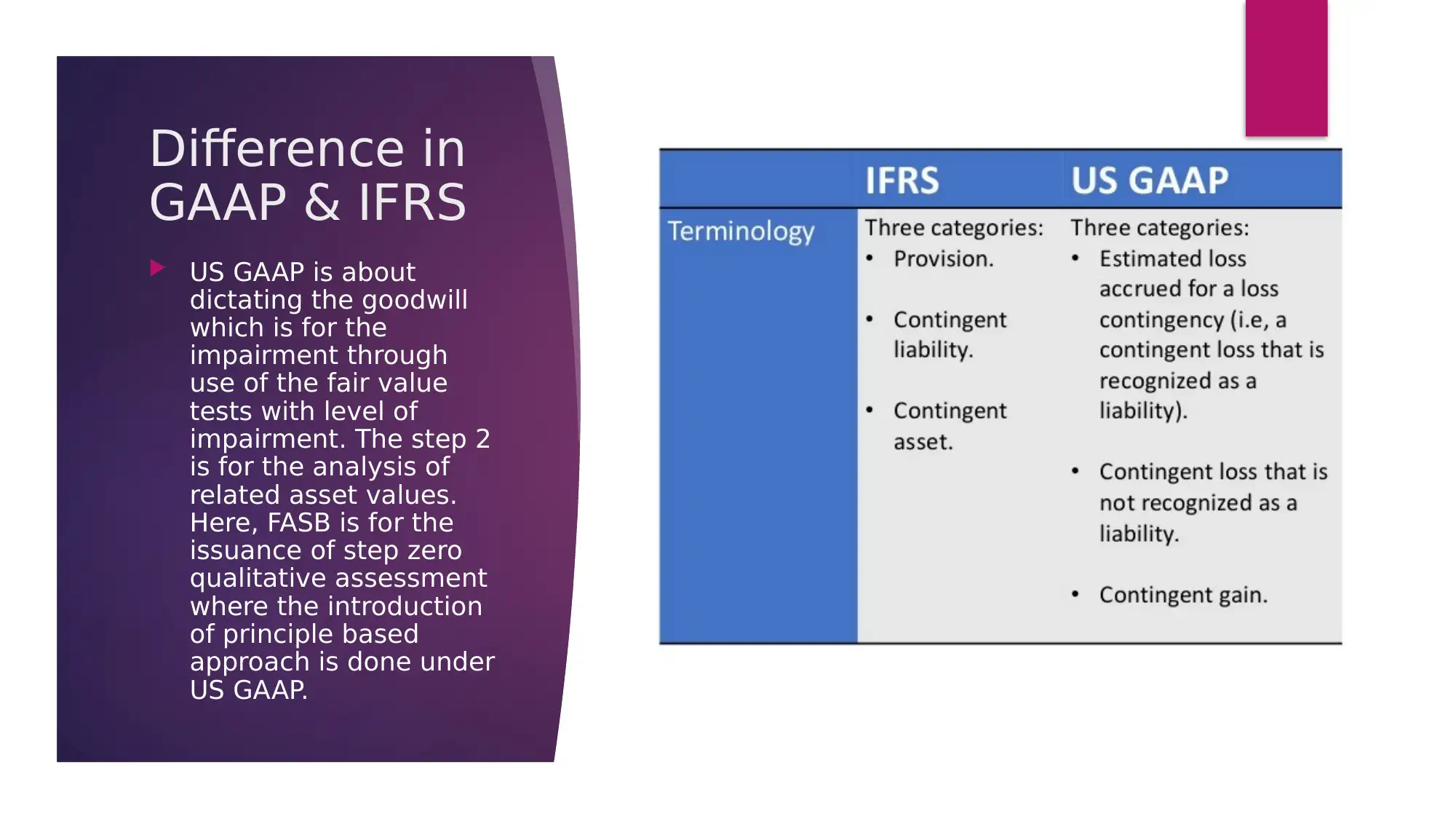

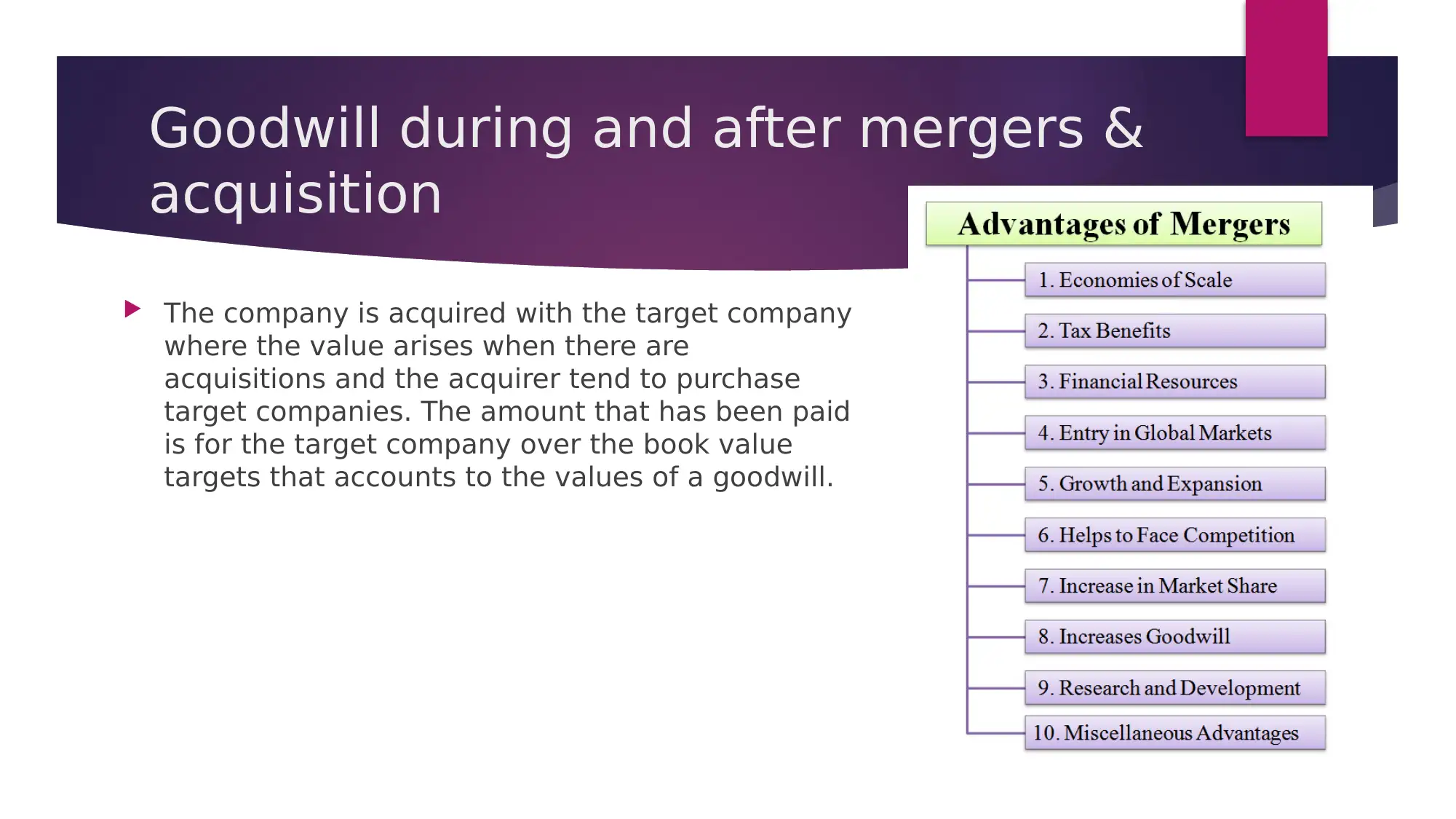

This report provides a detailed analysis of goodwill impairment, comparing and contrasting the Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). It explores the key differences in valuation methodologies and the challenges these differences pose for company management. The report examines the treatment of goodwill during and after various financial events, including mergers and acquisitions, transfers, and bankruptcies. It also investigates how companies balance goodwill in their financial statements, considering the specific requirements of GAAP and IFRS regarding balance sheets and income statements. Furthermore, the report includes case studies of companies like PwC and General Electric (GE), illustrating their approaches to managing goodwill impairment and navigating the complexities of accounting standards. The references include several research papers and studies that further support the analysis of goodwill impairment.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.