Goodwill Impairment Report: GAAP, IFRS, and Financial Implications

VerifiedAdded on 2021/11/19

|22

|1527

|54

Report

AI Summary

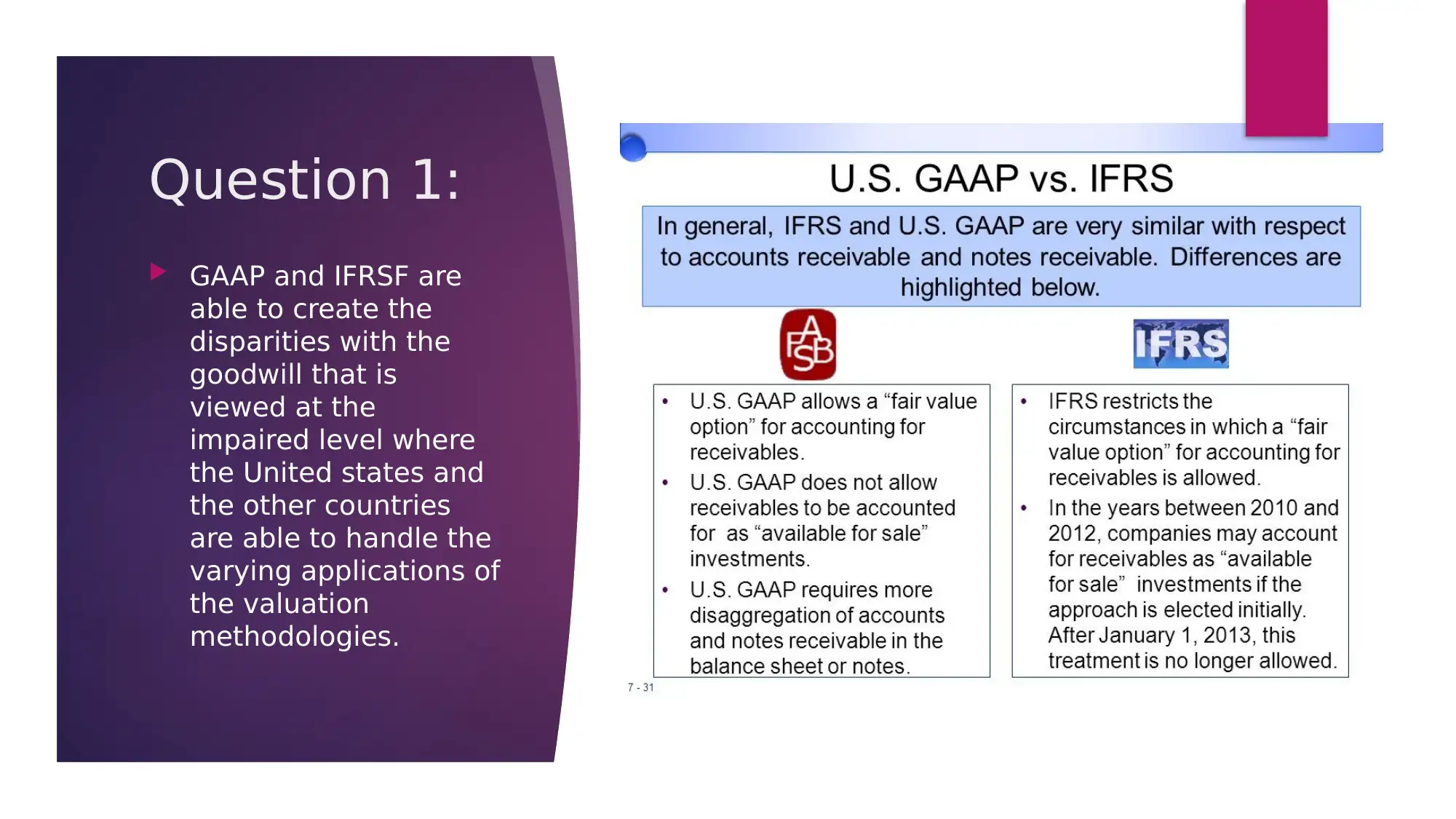

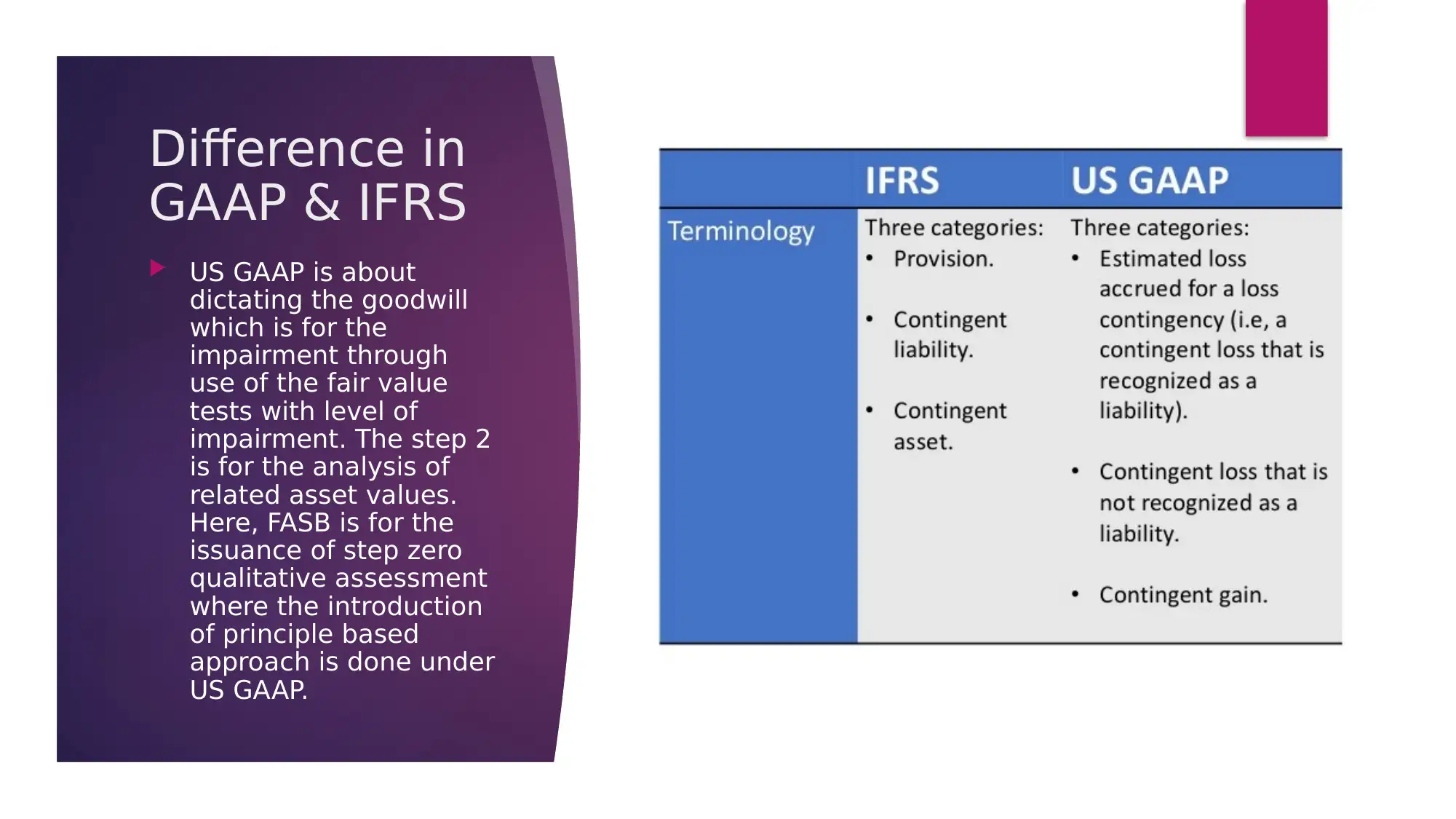

This report delves into the complexities of goodwill impairment, contrasting the approaches of Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS). It explores the disparities in valuation methodologies, highlighting the challenges companies face in adhering to these varying standards. The report examines goodwill impairment treatment, the impact of financial events, and the role of goodwill in mergers, acquisitions, and bankruptcies. It further analyzes how companies balance goodwill under GAAP and IFRS, considering differences in balance sheet layouts, income statements, and the handling of contingencies and employee benefits. The report also provides insights into how companies like PwC and GE manage goodwill, addressing accounting risks and currency transaction risks. The student report provides a comprehensive overview of the subject matter.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.