Goodwill Impairment Loss Reversal: Analysis & Journal Entries

VerifiedAdded on 2023/06/07

|10

|1849

|210

Essay

AI Summary

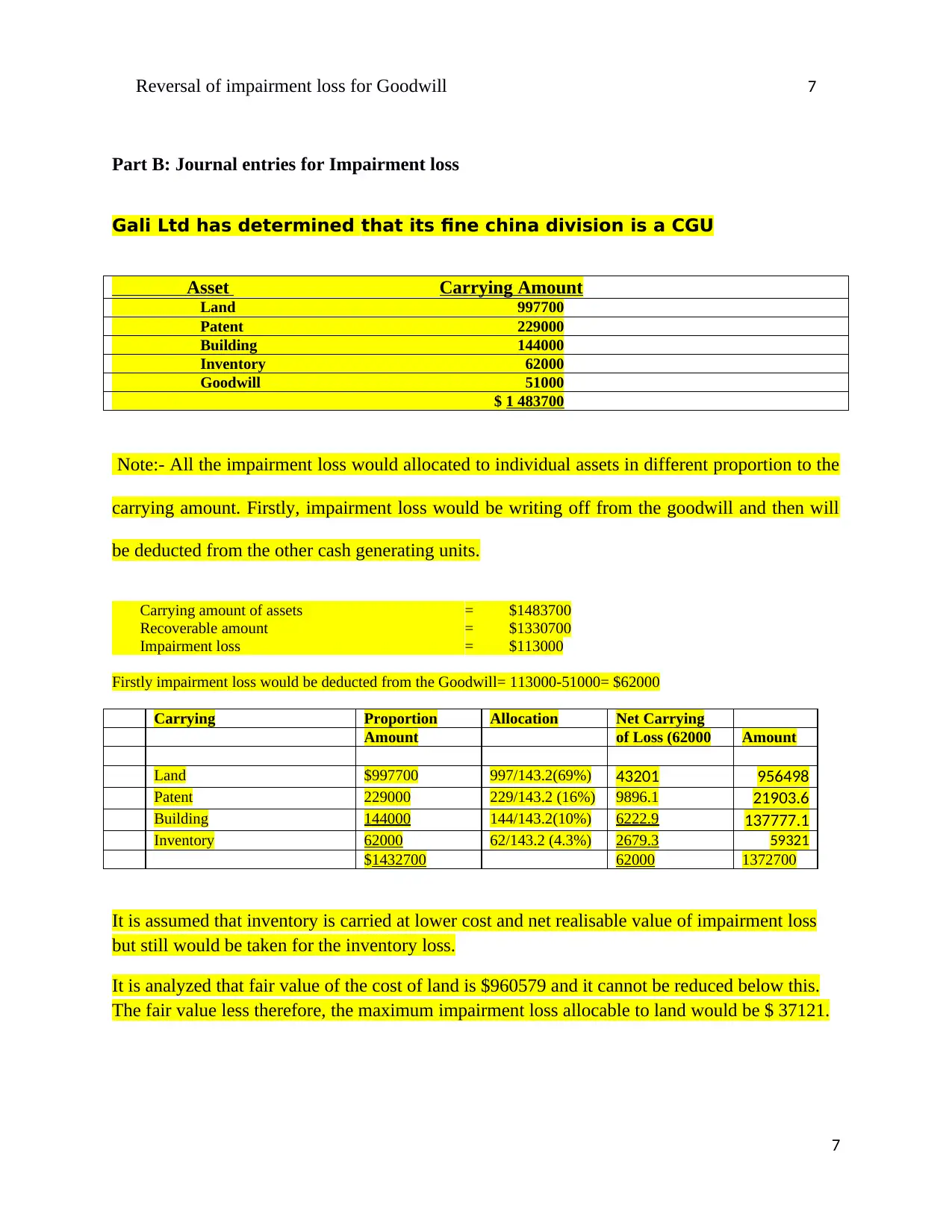

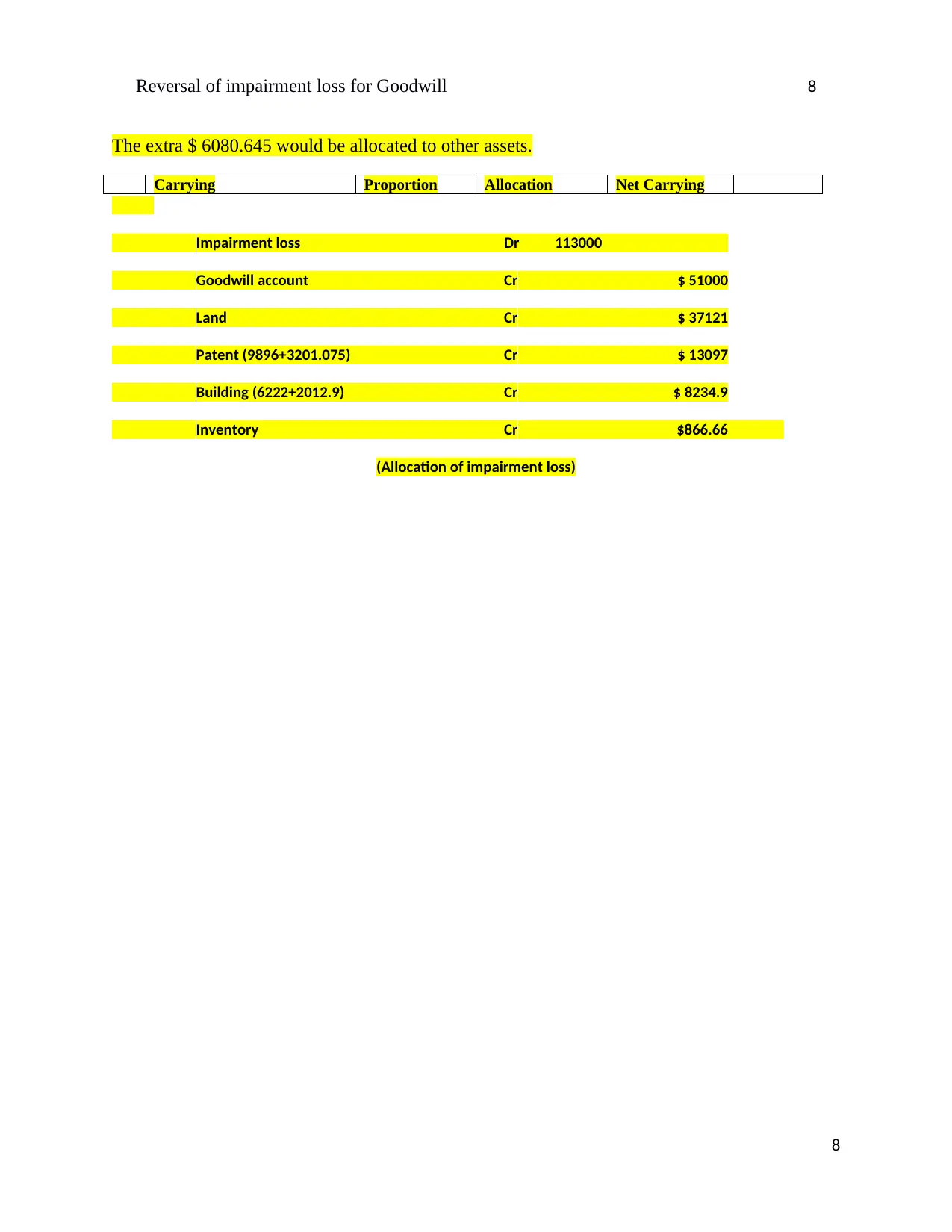

This assignment provides a detailed analysis of the reversal of impairment loss for goodwill, referencing AASB 136 and other relevant accounting standards. It explains the nature of impairment loss, its recognition as a revenue expenditure, and the conditions under which reversal can occur for cash-generating units (CGUs), but explicitly states that impairment losses for goodwill cannot be reversed. The assignment further includes a practical application involving Gali Ltd, demonstrating the calculation and journal entries for an impairment loss in a CGU, allocating the loss across various assets like land, patents, buildings, inventory, and goodwill, while adhering to the principle of first writing off the goodwill. The conclusion emphasizes the importance of proper disclosure in financial statements as per IAS 136 to maintain transparency for stakeholders. Desklib offers a wide range of solved assignments and past papers for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.