Ethics and Governance in Depreciation Policy: A Comprehensive Analysis

VerifiedAdded on 2020/02/19

|12

|2474

|50

Report

AI Summary

This report provides a comprehensive analysis of depreciation policies, focusing on the ethical and governance aspects within financial reporting. It begins with an executive summary and an introduction to depreciation, defining its meaning and uses in accounting. The report then delves into the ethical implications of changing depreciation methods, considering stakeholder perspectives and compliance with accounting standards, particularly AASB 116. It explores various depreciation methods, including straight-line, diminishing balance, sum-of-years' digit, and units of production, evaluating their advantages and disadvantages. A decision analysis is included, comparing the buy versus lease options for machinery using IRR calculations. Furthermore, the report analyzes the depreciation practices of Wesfarmers, examining their reporting of property, plant, and equipment. The conclusion emphasizes the importance of ethical conduct and compliance with accounting standards in depreciation practices. The report includes depreciation schedules, references to accounting standards and relevant literature, and provides a detailed examination of depreciation's role in financial statements and decision-making.

ETHICS AND GOVERNANCE IN DEPRECIATION POLICY

Student Name

Student ID

8/31/2017

Student Name

Student ID

8/31/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY:

The accounting policies play a very important role in the presentation of the financial statements

of the company. The main aim of this report is to analyze the different methods of calculation of

depreciation and how the financial statements are presented when the change has been made in

the method of calculating the depreciation during the year under concern. The second major aim

that has been shown in the report is the importance of the accounting standard and how the

company complies with the provisions of the accounting standards even after changing the

method of depreciation. With this aim the report has been framed and prepared with different

headings.

2

The accounting policies play a very important role in the presentation of the financial statements

of the company. The main aim of this report is to analyze the different methods of calculation of

depreciation and how the financial statements are presented when the change has been made in

the method of calculating the depreciation during the year under concern. The second major aim

that has been shown in the report is the importance of the accounting standard and how the

company complies with the provisions of the accounting standards even after changing the

method of depreciation. With this aim the report has been framed and prepared with different

headings.

2

Contents

EXECUTIVE SUMMARY:................................................................................................................................2

INTRODUCTION:..........................................................................................................................................4

MEANING OF DEPRECIATION AND ITS USES................................................................................................4

ETHICS AND GIVERNANCE - CHANGING DEPRECIATION..............................................................................5

Stakeholders:...........................................................................................................................................5

Ethical Issues:..........................................................................................................................................5

Objective of the Company Met by Change in Method............................................................................6

Marion’s Action Compliance....................................................................................................................6

DECISION ANALYSIS – DEPRECIATION OF MACHINERY................................................................................7

Depreciation Schedules...........................................................................................................................7

Advantages and Disadvantages of Each depreciation Method................................................................8

BUY OR LEASE..........................................................................................................................................8

ANALYSIS - WEFARMERS...........................................................................................................................10

Reporting of Property Plant and Equipment..........................................................................................10

Composition of Property Plant and Equipment.....................................................................................10

Methods of Depreciation Used..............................................................................................................10

Rates of Depreciation or Useful Life of an Asset....................................................................................10

Amount of Depreciation for Current and Previous Year........................................................................10

Purchases and Treatment of Borrowing Costs.......................................................................................10

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................11

3

EXECUTIVE SUMMARY:................................................................................................................................2

INTRODUCTION:..........................................................................................................................................4

MEANING OF DEPRECIATION AND ITS USES................................................................................................4

ETHICS AND GIVERNANCE - CHANGING DEPRECIATION..............................................................................5

Stakeholders:...........................................................................................................................................5

Ethical Issues:..........................................................................................................................................5

Objective of the Company Met by Change in Method............................................................................6

Marion’s Action Compliance....................................................................................................................6

DECISION ANALYSIS – DEPRECIATION OF MACHINERY................................................................................7

Depreciation Schedules...........................................................................................................................7

Advantages and Disadvantages of Each depreciation Method................................................................8

BUY OR LEASE..........................................................................................................................................8

ANALYSIS - WEFARMERS...........................................................................................................................10

Reporting of Property Plant and Equipment..........................................................................................10

Composition of Property Plant and Equipment.....................................................................................10

Methods of Depreciation Used..............................................................................................................10

Rates of Depreciation or Useful Life of an Asset....................................................................................10

Amount of Depreciation for Current and Previous Year........................................................................10

Purchases and Treatment of Borrowing Costs.......................................................................................10

CONCLUSION.............................................................................................................................................11

REFERENCES..............................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION:

The financial statements are prepared in accordance with the conceptual framework of

accounting embedded with the accounting standards and the generally accepted accounting

principles. In the given case study, emphasis has been placed on depreciation part of the

accounting. In the first case, the change in the method of depreciation from Straight Line Method

to Sum of year digit method has been discussed with compliance to the Australian Accounting

Standard 116. In the second case, the depreciation has been calculated with different methods

and the advantages and the disadvantages of each depreciation method have been provided. In

the third case, the consolidated financial statements of the Wesfarmers Company has been

analysed in regard to the depreciation if the valuation of the property, plant and equipment. The

report is then ended up with the conclusion and recommendation.

MEANING OF DEPRECIATION AND ITS USES

The term depreciation is referred to as the amount set aside from the value of the asset regularly

every year on account of the normal loss, wear and tear of the assets of the company. The

depreciation is the non cash item and is charged to the Statement of Income.

Its major use is that the company will be able to match the cost of the assets with the benefits that

the company has derived from the asset over the period of time. Apart from this matching

concept, the company will be able to report the value of the assets in the true and fair manner.

The third use of the depreciation is that it helps the company in saving the tax component as the

4

The financial statements are prepared in accordance with the conceptual framework of

accounting embedded with the accounting standards and the generally accepted accounting

principles. In the given case study, emphasis has been placed on depreciation part of the

accounting. In the first case, the change in the method of depreciation from Straight Line Method

to Sum of year digit method has been discussed with compliance to the Australian Accounting

Standard 116. In the second case, the depreciation has been calculated with different methods

and the advantages and the disadvantages of each depreciation method have been provided. In

the third case, the consolidated financial statements of the Wesfarmers Company has been

analysed in regard to the depreciation if the valuation of the property, plant and equipment. The

report is then ended up with the conclusion and recommendation.

MEANING OF DEPRECIATION AND ITS USES

The term depreciation is referred to as the amount set aside from the value of the asset regularly

every year on account of the normal loss, wear and tear of the assets of the company. The

depreciation is the non cash item and is charged to the Statement of Income.

Its major use is that the company will be able to match the cost of the assets with the benefits that

the company has derived from the asset over the period of time. Apart from this matching

concept, the company will be able to report the value of the assets in the true and fair manner.

The third use of the depreciation is that it helps the company in saving the tax component as the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tax laws provides that the depreciation is the allowable expenditure while calculating the taxable

income (AASB, 2011 and 2014).

ETHICS AND GIVERNANCE - CHANGING DEPRECIATION

Stakeholders:

Stakeholders are the persons who are vital to the survival of the company. Stakeholder includes

shareholders, employees, government authorities, financial institutions and the customers. In the

given situation, the first stakeholder is the shareholder of the company (Fontaine, Haarman and

Schmid, 2016). Shareholders have invested in the company in order to have the dividends and

the increase wealth. Since in the given case, the profit has been deferred from year 2016 and

2017 to the year 2018 and 2019, the return on the investment of the shareholders has been

declined.

Another major stakeholder is the taxation authorities as less tax will be paid by the company on

the declared profits of the year 2016 and 2017.

Ethical Issues:

Ethics are the rules and principles comprised of the moral beliefs which conduct the behavior of

the individuals involved in the working of an organization like employees, top management

officials, etc (Andrews, 2011). Following are the ethical issues which is present:

- Financial Statements of the company has been misrepresented by deferring the profit of

the company. Thus, ethics in Finance has been violated.

- The decision has been made with the consent of employees. Thus, ethics in personnel

have been violated (Harsen, 2004).

- The professional, Marion, has agreed in order to save his professional engagement with

the company.

- The change in method of depreciation has been done without informing shareholders of

the company and other stakeholders (Arjoon and Gopal, 2003).

5

income (AASB, 2011 and 2014).

ETHICS AND GIVERNANCE - CHANGING DEPRECIATION

Stakeholders:

Stakeholders are the persons who are vital to the survival of the company. Stakeholder includes

shareholders, employees, government authorities, financial institutions and the customers. In the

given situation, the first stakeholder is the shareholder of the company (Fontaine, Haarman and

Schmid, 2016). Shareholders have invested in the company in order to have the dividends and

the increase wealth. Since in the given case, the profit has been deferred from year 2016 and

2017 to the year 2018 and 2019, the return on the investment of the shareholders has been

declined.

Another major stakeholder is the taxation authorities as less tax will be paid by the company on

the declared profits of the year 2016 and 2017.

Ethical Issues:

Ethics are the rules and principles comprised of the moral beliefs which conduct the behavior of

the individuals involved in the working of an organization like employees, top management

officials, etc (Andrews, 2011). Following are the ethical issues which is present:

- Financial Statements of the company has been misrepresented by deferring the profit of

the company. Thus, ethics in Finance has been violated.

- The decision has been made with the consent of employees. Thus, ethics in personnel

have been violated (Harsen, 2004).

- The professional, Marion, has agreed in order to save his professional engagement with

the company.

- The change in method of depreciation has been done without informing shareholders of

the company and other stakeholders (Arjoon and Gopal, 2003).

5

- Non compliance with the requirement of the accounting standards as the company has not

disclosed the fact of change in the method of depreciation in the notes to the financial

statements of the company (Badaracco, 2005 and Longstaff , 2008).

Objective of the Company Met by Change in Method

The company has been advised by Marion to change the accounting method from the straight

line method to Sum of Years digit method.

In the straight line method, equal amount is charged over the useful life of an asset whereas

under the sum of year’s digit method, the higher depreciation is charged in the nearer periods and

the lower depreciation is charged in the future periods (Australian government official website,

2014).

By changing the depreciation method the company will be able to generate lower profits in the

earlier years and higher profits in the future years and thus in this way the change in method of

depreciation has been able to meet the objective.

Marion’s Action Compliance

The International Accounting Standard 16 and Australian Accounting Standard 116 provide that

the company shall disclose all the facts relating to the assets of the company that has happened

during the year (EC Europa, 2009). This standard prescribes that the following shall be

disclosed:

- Carrying amount of asset

- Depreciation method

- Useful life of an asset

- Value of Impairment Loss and

- Reconciliation statement showing each head of the Property Plant and Equipment (IFRS

Official Website, 2012)

Also as per the accounting standard 108, the company is required to disclose the change in

method of depreciation as the change in an accounting estimate.

6

disclosed the fact of change in the method of depreciation in the notes to the financial

statements of the company (Badaracco, 2005 and Longstaff , 2008).

Objective of the Company Met by Change in Method

The company has been advised by Marion to change the accounting method from the straight

line method to Sum of Years digit method.

In the straight line method, equal amount is charged over the useful life of an asset whereas

under the sum of year’s digit method, the higher depreciation is charged in the nearer periods and

the lower depreciation is charged in the future periods (Australian government official website,

2014).

By changing the depreciation method the company will be able to generate lower profits in the

earlier years and higher profits in the future years and thus in this way the change in method of

depreciation has been able to meet the objective.

Marion’s Action Compliance

The International Accounting Standard 16 and Australian Accounting Standard 116 provide that

the company shall disclose all the facts relating to the assets of the company that has happened

during the year (EC Europa, 2009). This standard prescribes that the following shall be

disclosed:

- Carrying amount of asset

- Depreciation method

- Useful life of an asset

- Value of Impairment Loss and

- Reconciliation statement showing each head of the Property Plant and Equipment (IFRS

Official Website, 2012)

Also as per the accounting standard 108, the company is required to disclose the change in

method of depreciation as the change in an accounting estimate.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

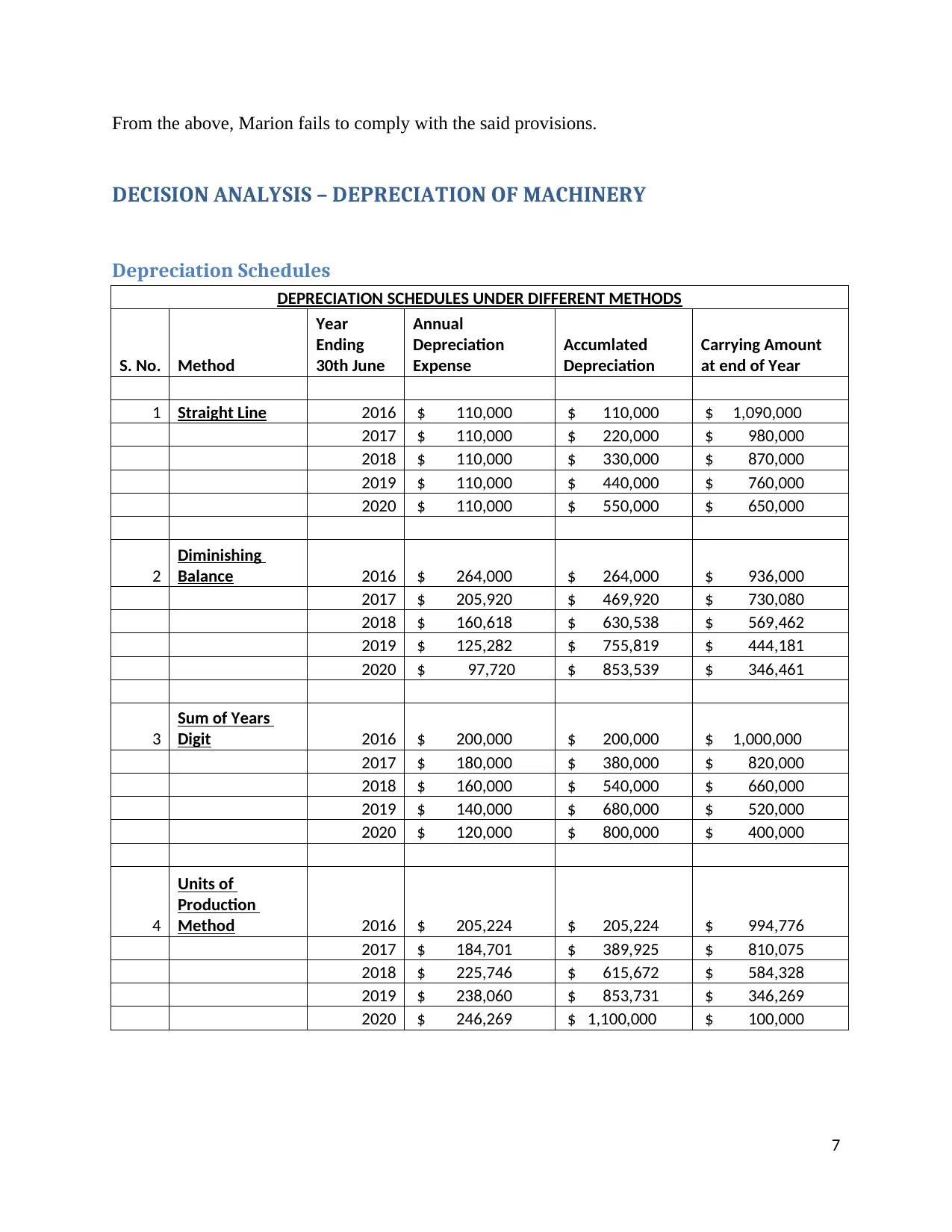

From the above, Marion fails to comply with the said provisions.

DECISION ANALYSIS – DEPRECIATION OF MACHINERY

Depreciation Schedules

DEPRECIATION SCHEDULES UNDER DIFFERENT METHODS

S. No. Method

Year

Ending

30th June

Annual

Depreciation

Expense

Accumlated

Depreciation

Carrying Amount

at end of Year

1 Straight Line 2016 $ 110,000 $ 110,000 $ 1,090,000

2017 $ 110,000 $ 220,000 $ 980,000

2018 $ 110,000 $ 330,000 $ 870,000

2019 $ 110,000 $ 440,000 $ 760,000

2020 $ 110,000 $ 550,000 $ 650,000

2

Diminishing

Balance 2016 $ 264,000 $ 264,000 $ 936,000

2017 $ 205,920 $ 469,920 $ 730,080

2018 $ 160,618 $ 630,538 $ 569,462

2019 $ 125,282 $ 755,819 $ 444,181

2020 $ 97,720 $ 853,539 $ 346,461

3

Sum of Years

Digit 2016 $ 200,000 $ 200,000 $ 1,000,000

2017 $ 180,000 $ 380,000 $ 820,000

2018 $ 160,000 $ 540,000 $ 660,000

2019 $ 140,000 $ 680,000 $ 520,000

2020 $ 120,000 $ 800,000 $ 400,000

4

Units of

Production

Method 2016 $ 205,224 $ 205,224 $ 994,776

2017 $ 184,701 $ 389,925 $ 810,075

2018 $ 225,746 $ 615,672 $ 584,328

2019 $ 238,060 $ 853,731 $ 346,269

2020 $ 246,269 $ 1,100,000 $ 100,000

7

DECISION ANALYSIS – DEPRECIATION OF MACHINERY

Depreciation Schedules

DEPRECIATION SCHEDULES UNDER DIFFERENT METHODS

S. No. Method

Year

Ending

30th June

Annual

Depreciation

Expense

Accumlated

Depreciation

Carrying Amount

at end of Year

1 Straight Line 2016 $ 110,000 $ 110,000 $ 1,090,000

2017 $ 110,000 $ 220,000 $ 980,000

2018 $ 110,000 $ 330,000 $ 870,000

2019 $ 110,000 $ 440,000 $ 760,000

2020 $ 110,000 $ 550,000 $ 650,000

2

Diminishing

Balance 2016 $ 264,000 $ 264,000 $ 936,000

2017 $ 205,920 $ 469,920 $ 730,080

2018 $ 160,618 $ 630,538 $ 569,462

2019 $ 125,282 $ 755,819 $ 444,181

2020 $ 97,720 $ 853,539 $ 346,461

3

Sum of Years

Digit 2016 $ 200,000 $ 200,000 $ 1,000,000

2017 $ 180,000 $ 380,000 $ 820,000

2018 $ 160,000 $ 540,000 $ 660,000

2019 $ 140,000 $ 680,000 $ 520,000

2020 $ 120,000 $ 800,000 $ 400,000

4

Units of

Production

Method 2016 $ 205,224 $ 205,224 $ 994,776

2017 $ 184,701 $ 389,925 $ 810,075

2018 $ 225,746 $ 615,672 $ 584,328

2019 $ 238,060 $ 853,731 $ 346,269

2020 $ 246,269 $ 1,100,000 $ 100,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

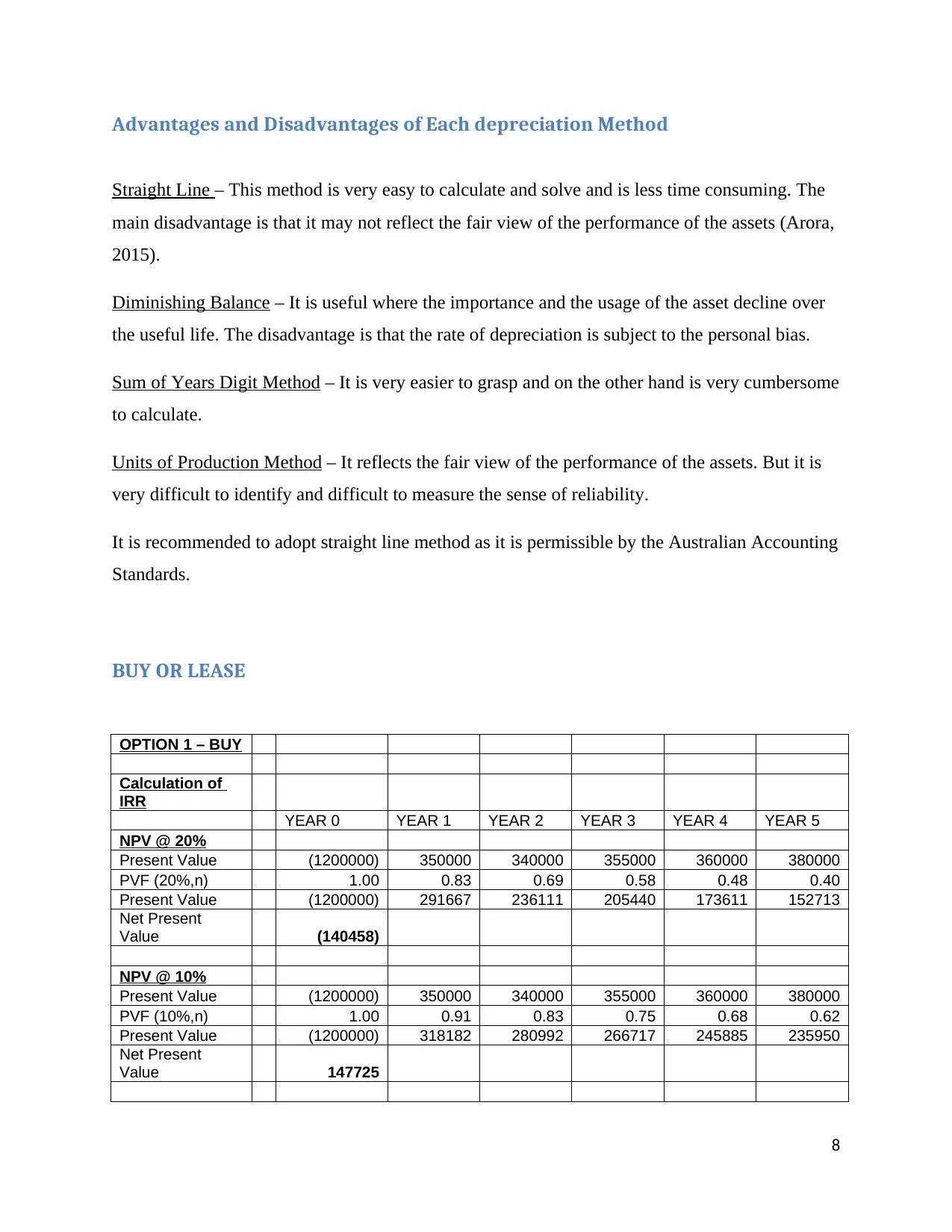

Advantages and Disadvantages of Each depreciation Method

Straight Line – This method is very easy to calculate and solve and is less time consuming. The

main disadvantage is that it may not reflect the fair view of the performance of the assets (Arora,

2015).

Diminishing Balance – It is useful where the importance and the usage of the asset decline over

the useful life. The disadvantage is that the rate of depreciation is subject to the personal bias.

Sum of Years Digit Method – It is very easier to grasp and on the other hand is very cumbersome

to calculate.

Units of Production Method – It reflects the fair view of the performance of the assets. But it is

very difficult to identify and difficult to measure the sense of reliability.

It is recommended to adopt straight line method as it is permissible by the Australian Accounting

Standards.

BUY OR LEASE

OPTION 1 – BUY

Calculation of

IRR

YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5

NPV @ 20%

Present Value (1200000) 350000 340000 355000 360000 380000

PVF (20%,n) 1.00 0.83 0.69 0.58 0.48 0.40

Present Value (1200000) 291667 236111 205440 173611 152713

Net Present

Value (140458)

NPV @ 10%

Present Value (1200000) 350000 340000 355000 360000 380000

PVF (10%,n) 1.00 0.91 0.83 0.75 0.68 0.62

Present Value (1200000) 318182 280992 266717 245885 235950

Net Present

Value 147725

8

Straight Line – This method is very easy to calculate and solve and is less time consuming. The

main disadvantage is that it may not reflect the fair view of the performance of the assets (Arora,

2015).

Diminishing Balance – It is useful where the importance and the usage of the asset decline over

the useful life. The disadvantage is that the rate of depreciation is subject to the personal bias.

Sum of Years Digit Method – It is very easier to grasp and on the other hand is very cumbersome

to calculate.

Units of Production Method – It reflects the fair view of the performance of the assets. But it is

very difficult to identify and difficult to measure the sense of reliability.

It is recommended to adopt straight line method as it is permissible by the Australian Accounting

Standards.

BUY OR LEASE

OPTION 1 – BUY

Calculation of

IRR

YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5

NPV @ 20%

Present Value (1200000) 350000 340000 355000 360000 380000

PVF (20%,n) 1.00 0.83 0.69 0.58 0.48 0.40

Present Value (1200000) 291667 236111 205440 173611 152713

Net Present

Value (140458)

NPV @ 10%

Present Value (1200000) 350000 340000 355000 360000 380000

PVF (10%,n) 1.00 0.91 0.83 0.75 0.68 0.62

Present Value (1200000) 318182 280992 266717 245885 235950

Net Present

Value 147725

8

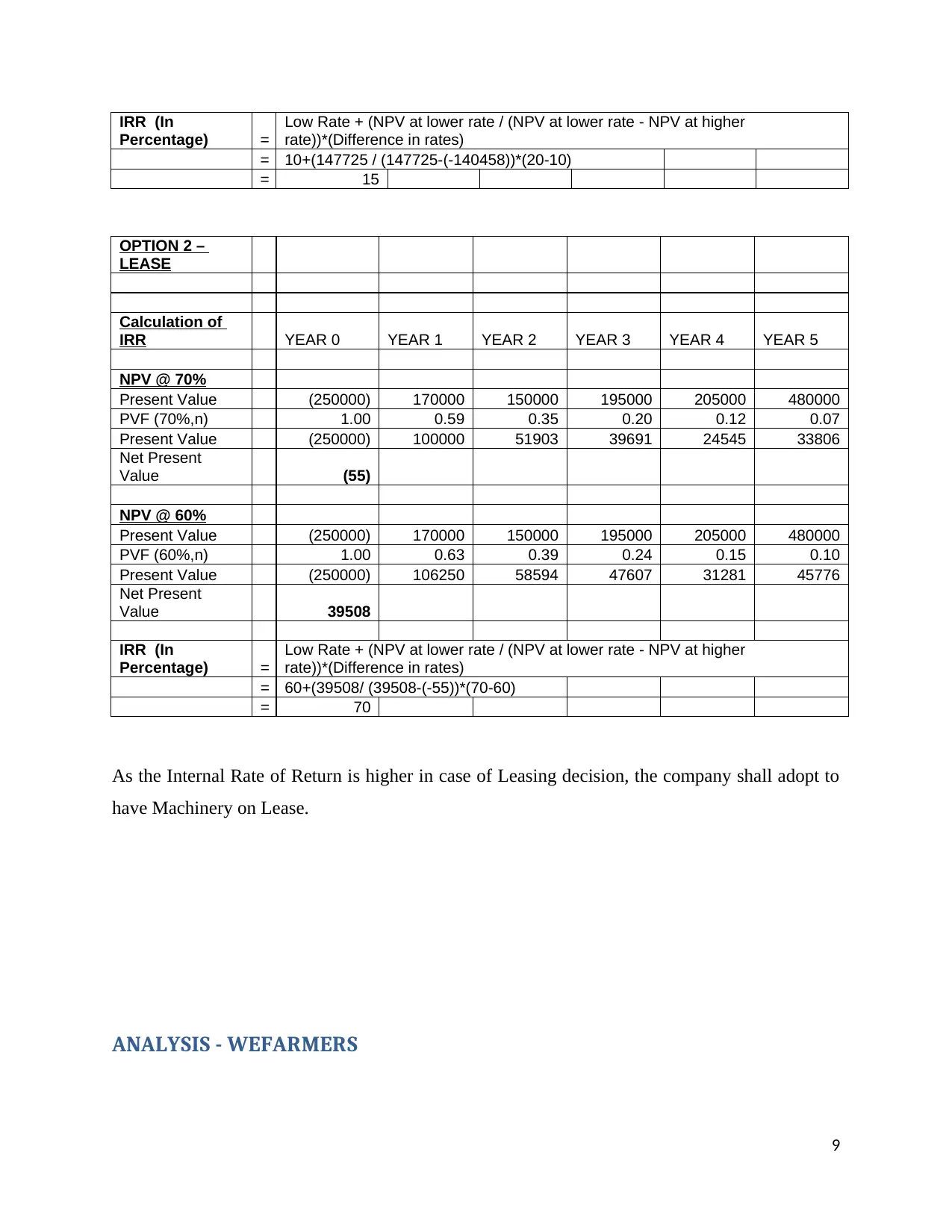

IRR (In

Percentage) =

Low Rate + (NPV at lower rate / (NPV at lower rate - NPV at higher

rate))*(Difference in rates)

= 10+(147725 / (147725-(-140458))*(20-10)

= 15

OPTION 2 –

LEASE

Calculation of

IRR YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5

NPV @ 70%

Present Value (250000) 170000 150000 195000 205000 480000

PVF (70%,n) 1.00 0.59 0.35 0.20 0.12 0.07

Present Value (250000) 100000 51903 39691 24545 33806

Net Present

Value (55)

NPV @ 60%

Present Value (250000) 170000 150000 195000 205000 480000

PVF (60%,n) 1.00 0.63 0.39 0.24 0.15 0.10

Present Value (250000) 106250 58594 47607 31281 45776

Net Present

Value 39508

IRR (In

Percentage) =

Low Rate + (NPV at lower rate / (NPV at lower rate - NPV at higher

rate))*(Difference in rates)

= 60+(39508/ (39508-(-55))*(70-60)

= 70

As the Internal Rate of Return is higher in case of Leasing decision, the company shall adopt to

have Machinery on Lease.

ANALYSIS - WEFARMERS

9

Percentage) =

Low Rate + (NPV at lower rate / (NPV at lower rate - NPV at higher

rate))*(Difference in rates)

= 10+(147725 / (147725-(-140458))*(20-10)

= 15

OPTION 2 –

LEASE

Calculation of

IRR YEAR 0 YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5

NPV @ 70%

Present Value (250000) 170000 150000 195000 205000 480000

PVF (70%,n) 1.00 0.59 0.35 0.20 0.12 0.07

Present Value (250000) 100000 51903 39691 24545 33806

Net Present

Value (55)

NPV @ 60%

Present Value (250000) 170000 150000 195000 205000 480000

PVF (60%,n) 1.00 0.63 0.39 0.24 0.15 0.10

Present Value (250000) 106250 58594 47607 31281 45776

Net Present

Value 39508

IRR (In

Percentage) =

Low Rate + (NPV at lower rate / (NPV at lower rate - NPV at higher

rate))*(Difference in rates)

= 60+(39508/ (39508-(-55))*(70-60)

= 70

As the Internal Rate of Return is higher in case of Leasing decision, the company shall adopt to

have Machinery on Lease.

ANALYSIS - WEFARMERS

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reporting of Property Plant and Equipment

The property plant and equipment has been reported at the cost less depreciation and impairment

loss if any. The total carrying amount of Property plant and equipment for the year ending 30th

June 2016 is $9612 Million.

Composition of Property Plant and Equipment

Property Plant and Equipment is composed of Freehold Land, Building, Leasehold

Improvements, Plant, Vehicles and Equipment and Mineral Lease and Development

(Wesfarmers Official Website, 2016).

Methods of Depreciation Used

The depreciation has been calculated using straight line method in which cost has been

depreciated over the useful life of an asset.

Rates of Depreciation or Useful Life of an Asset

Yes the group has disclosed the useful life of an asset. These are mentioned below:

- Buildings 20 to 40 years

- Plant and Equipments Between 3 and 40 years

- Leasehold Improvements Leasehold period

Amount of Depreciation for Current and Previous Year

The amount of Depreciation charged in the current year is $1162 million and in the previous year

$1101 million.

Purchases and Treatment of Borrowing Costs

Yes, asset of $1738 million has been purchased during the year. Yes assets of $984 million are under

construction. Borrowing costs have been capitalized by the company in the assets. No the company does

not have any commitments for future expansions.

CONCLUSION

10

The property plant and equipment has been reported at the cost less depreciation and impairment

loss if any. The total carrying amount of Property plant and equipment for the year ending 30th

June 2016 is $9612 Million.

Composition of Property Plant and Equipment

Property Plant and Equipment is composed of Freehold Land, Building, Leasehold

Improvements, Plant, Vehicles and Equipment and Mineral Lease and Development

(Wesfarmers Official Website, 2016).

Methods of Depreciation Used

The depreciation has been calculated using straight line method in which cost has been

depreciated over the useful life of an asset.

Rates of Depreciation or Useful Life of an Asset

Yes the group has disclosed the useful life of an asset. These are mentioned below:

- Buildings 20 to 40 years

- Plant and Equipments Between 3 and 40 years

- Leasehold Improvements Leasehold period

Amount of Depreciation for Current and Previous Year

The amount of Depreciation charged in the current year is $1162 million and in the previous year

$1101 million.

Purchases and Treatment of Borrowing Costs

Yes, asset of $1738 million has been purchased during the year. Yes assets of $984 million are under

construction. Borrowing costs have been capitalized by the company in the assets. No the company does

not have any commitments for future expansions.

CONCLUSION

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depreciation has been the major part of the financial statements as it is directly related to the

assets of the company which is counted as the Net Worth of the company. Every company is

required to follow the guidelines of the accounting standards of the respective countries and also

the International Accounting Standards.

To conclude, every company shall follow the correct depreciation method and shall not in any

manner manipulate the financial statements of the company.

REFERENCES

AASB, (2011), “Depreciation” available on

http://www.aasb.gov.au/admin/file/content102/c3/AAS04_8-11.pdf accessed on

31/08/2017

AASB, (2014), “Complied AASB Standard – Property, Plant and Equipment” available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-

04_COMPjun14_07 -14.pdf accessed on 31/08/2017

Andrews K., (2011), “Ethics in Practice : Managing the Moral Corporation”, Harward Business

Review – School Press.

Arjoon S. , J. Gopal, (2003), “Ethical Orientation for Future Managers : The Case of Trinidad”,

Social and Economic Studies, pages 98-114.

Arora D. (2015), “Different Methods of Depreciation calculation” available on

http://scn.sap.com/docs/DOC-46210 accessed on 31/08/2017

Australian government official website, (2014), “Amendments to Australian Accounting

Standards – Clarification of Acceptable Methods of Depreciation and

Amortization”, available on https://www.legislation.gov.au/Details/F2014L01174

accessed on 31/08/2017

Badaracco T, (2005), “Business Ethics : A view from the Trenches”, California

Management Review, Pages 8-28.

Fontaine C, Haarman A. and Schmid S, (2016), “The Stakeholder Theory” available on

http://www.martonomily.com/sites/default/files/attach/Stakeholders

%20theory.pdf accessed on 31/08/2017

11

assets of the company which is counted as the Net Worth of the company. Every company is

required to follow the guidelines of the accounting standards of the respective countries and also

the International Accounting Standards.

To conclude, every company shall follow the correct depreciation method and shall not in any

manner manipulate the financial statements of the company.

REFERENCES

AASB, (2011), “Depreciation” available on

http://www.aasb.gov.au/admin/file/content102/c3/AAS04_8-11.pdf accessed on

31/08/2017

AASB, (2014), “Complied AASB Standard – Property, Plant and Equipment” available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-

04_COMPjun14_07 -14.pdf accessed on 31/08/2017

Andrews K., (2011), “Ethics in Practice : Managing the Moral Corporation”, Harward Business

Review – School Press.

Arjoon S. , J. Gopal, (2003), “Ethical Orientation for Future Managers : The Case of Trinidad”,

Social and Economic Studies, pages 98-114.

Arora D. (2015), “Different Methods of Depreciation calculation” available on

http://scn.sap.com/docs/DOC-46210 accessed on 31/08/2017

Australian government official website, (2014), “Amendments to Australian Accounting

Standards – Clarification of Acceptable Methods of Depreciation and

Amortization”, available on https://www.legislation.gov.au/Details/F2014L01174

accessed on 31/08/2017

Badaracco T, (2005), “Business Ethics : A view from the Trenches”, California

Management Review, Pages 8-28.

Fontaine C, Haarman A. and Schmid S, (2016), “The Stakeholder Theory” available on

http://www.martonomily.com/sites/default/files/attach/Stakeholders

%20theory.pdf accessed on 31/08/2017

11

EC Europa, (2009),”International Accounting Standard 16- Property, Plant and

Equipment”available at

http://ec.europa.eu/internal_market/accounting/docs/consolidated/ias16_en.pdf

accessed on 31/08/2017

.

Harsen (2004), “Business Ethics Platitude or Commitment ?” Centre for Business Ethics,

Bentley MA

IFRS Official Website, (2012), “IAS 16 Property, Plant and Equipment” available at

http://www.ifrs.org/Documents/IAS16.pdf accessed on 31/08/2017

Longstaff S., (2008) “The ethical dimension of Corporate Governance” available at

http://www.ethics.org.au/on-ethics/blog/december-2008/the-ethical-dimension-of

-corporate-governance accessed on 31/08/2017

Wesfarmers Official Website, (2016), “Annual Report 2016), available on

www.wesfarmers.com.au accessed on 31/08/2017.

12

Equipment”available at

http://ec.europa.eu/internal_market/accounting/docs/consolidated/ias16_en.pdf

accessed on 31/08/2017

.

Harsen (2004), “Business Ethics Platitude or Commitment ?” Centre for Business Ethics,

Bentley MA

IFRS Official Website, (2012), “IAS 16 Property, Plant and Equipment” available at

http://www.ifrs.org/Documents/IAS16.pdf accessed on 31/08/2017

Longstaff S., (2008) “The ethical dimension of Corporate Governance” available at

http://www.ethics.org.au/on-ethics/blog/december-2008/the-ethical-dimension-of

-corporate-governance accessed on 31/08/2017

Wesfarmers Official Website, (2016), “Annual Report 2016), available on

www.wesfarmers.com.au accessed on 31/08/2017.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.