Stewardship and Governance: Theories, Contributions, and Applications

VerifiedAdded on 2022/11/25

|13

|3137

|181

Report

AI Summary

This report delves into the critical aspects of stewardship and governance, offering a comprehensive analysis of its significance within various organizational structures. It begins by introducing the concept of corporate governance and its importance, particularly in environments with multiple stakeholders. The report then explores key corporate governance theories, including agency theory, stakeholder theory, resource dependency theory, and, most importantly, stewardship theory. It examines the contributions of stewardship theory to effective governance, focusing on its application in both non-profit and profit organizations. The report highlights how stewardship theory promotes accountability, shared decision-making, and the prioritization of organizational goals over self-interest, making it a valuable framework for leaders and managers. Furthermore, it discusses the roles of committees, trustees, and board members in ensuring that organizations fulfill their objectives, especially in the context of non-profit entities. Finally, it explores the governance structure of profit-oriented organizations, emphasizing how the principles of stewardship theory can be applied to enhance corporate performance and accountability. The report provides a well-rounded understanding of stewardship and governance, offering valuable insights for students of leadership and management.

Stewardship and Governance

Running Head: Stewardship and Governance

0

6 / 8 / 2 0 1 9

Students Name

Running Head: Stewardship and Governance

0

6 / 8 / 2 0 1 9

Students Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stewardship and Governance 1

Contents

Introduction......................................................................................................................................2

Corporate Governance Theories......................................................................................................3

Contributions of Stewardship theory...............................................................................................6

Non-Profit Organization 7

Profit Origination 8

Leader’s values and effective governance.......................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Contents

Introduction......................................................................................................................................2

Corporate Governance Theories......................................................................................................3

Contributions of Stewardship theory...............................................................................................6

Non-Profit Organization 7

Profit Origination 8

Leader’s values and effective governance.......................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Stewardship and Governance 2

Introduction

Management is an important part of each organization as the same is the ultimate

authority that decides the matter of an organization and develops plan and procedures for the

same. Corporate governance is a system or a mechanism by that an entity is regulated, directed,

and controlled (Davoren, 2019). It helps management to inform what practices are required to

adopt for the development of the whole organization. In this manner, this would not be wrongful

to state that corporate governance helps the management of the company to act in an efficient

manner and provides guidelines to the same. In the present era where changes are very frequent

in organizations, corporate governance has its unique significance. In a situation where an

organization has many stakeholders by that the same get affected, managers of the business need

guidance as it becomes very difficult to manage different situations at the same time considering

other aspects such as ethics and goodness of all the stakeholders. Corporate governance includes

business managers, the board of directors, ethics committees, and every other party that is liable

to ensure good governance in the organization (Walls, Berrone, & Phan, 2012). In order to

discuss the scope of corporate governance, this is to state that the same has a wider scope and it

includes external factors in addition to internal ones. Mainly corporate governance is about

fairness, accountability, and transparency.

In other words, this is to state that corporate governance prescribes the manner in which

governance should be performed by the management. Different scholars have provided different

theories on corporate governance, that provides different principles and focus on different

aspects (Abid, Khan, Rafiq, & Ahmad, 2014).. In the presented report, the corporate governance

theories related to nonprofit organizations will be discussed. In addition to this, the manner in

Introduction

Management is an important part of each organization as the same is the ultimate

authority that decides the matter of an organization and develops plan and procedures for the

same. Corporate governance is a system or a mechanism by that an entity is regulated, directed,

and controlled (Davoren, 2019). It helps management to inform what practices are required to

adopt for the development of the whole organization. In this manner, this would not be wrongful

to state that corporate governance helps the management of the company to act in an efficient

manner and provides guidelines to the same. In the present era where changes are very frequent

in organizations, corporate governance has its unique significance. In a situation where an

organization has many stakeholders by that the same get affected, managers of the business need

guidance as it becomes very difficult to manage different situations at the same time considering

other aspects such as ethics and goodness of all the stakeholders. Corporate governance includes

business managers, the board of directors, ethics committees, and every other party that is liable

to ensure good governance in the organization (Walls, Berrone, & Phan, 2012). In order to

discuss the scope of corporate governance, this is to state that the same has a wider scope and it

includes external factors in addition to internal ones. Mainly corporate governance is about

fairness, accountability, and transparency.

In other words, this is to state that corporate governance prescribes the manner in which

governance should be performed by the management. Different scholars have provided different

theories on corporate governance, that provides different principles and focus on different

aspects (Abid, Khan, Rafiq, & Ahmad, 2014).. In the presented report, the corporate governance

theories related to nonprofit organizations will be discussed. In addition to this, the manner in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stewardship and Governance 3

which Stewardship theory contributes to effective governance in a non-profit organization will

also be discussed.

Corporate Governance Theories

As mentioned above, theories of corporate governance are different concepts. These

theories provide a different basis that business managementis required to consider while decision

making. Further, these theories prescribe the relationship of stakeholders in mutual. Agency,

Stewardship, resource dependence are some the major theories of corporate governance that are

applicable to profit as well as to nonprofit organizations and the same are discussed below in

detail.

Agency Theory: - As the name implies, this theory defines the relationship between agent

and principals. In the context of an organization, directors are the agent where

shareholders play the role of principals (Fooladi & Chaleshtori, 2011). As per this theory,

these principal employ agents to work on behalf of principals. The principal of business

hire agents to run the business. Demsetz and Alchain introduced this theory as an

economic concept and afterward the same has been introduced as in governance as well

as in leadership. The theory highlights the role of governing bodies of an organization

such as the board of directors and members of the managing committee. Shareholder

often expects that agents of the organization will work in the best interest of principals

but it is not necessary that they always do. In actual agents may act in their self-interest

and can fail to fulfill the expectations of shareholders by not acting in the best interest of

the principals (Wan Yusoff, 2012). If to talk about the main feature of this theory, this is

to state that the same is a difference between ownership and management. In a

which Stewardship theory contributes to effective governance in a non-profit organization will

also be discussed.

Corporate Governance Theories

As mentioned above, theories of corporate governance are different concepts. These

theories provide a different basis that business managementis required to consider while decision

making. Further, these theories prescribe the relationship of stakeholders in mutual. Agency,

Stewardship, resource dependence are some the major theories of corporate governance that are

applicable to profit as well as to nonprofit organizations and the same are discussed below in

detail.

Agency Theory: - As the name implies, this theory defines the relationship between agent

and principals. In the context of an organization, directors are the agent where

shareholders play the role of principals (Fooladi & Chaleshtori, 2011). As per this theory,

these principal employ agents to work on behalf of principals. The principal of business

hire agents to run the business. Demsetz and Alchain introduced this theory as an

economic concept and afterward the same has been introduced as in governance as well

as in leadership. The theory highlights the role of governing bodies of an organization

such as the board of directors and members of the managing committee. Shareholder

often expects that agents of the organization will work in the best interest of principals

but it is not necessary that they always do. In actual agents may act in their self-interest

and can fail to fulfill the expectations of shareholders by not acting in the best interest of

the principals (Wan Yusoff, 2012). If to talk about the main feature of this theory, this is

to state that the same is a difference between ownership and management. In a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stewardship and Governance 4

summarized way this is to say that as per the agency theory, agents i.e. directors and

managers must work in the best interest of principals i.e. Shareholders.

Stakeholder Theory: - Freeman has developed this theory by introducing corporate

responsibility and accountability to a broad range of stakeholders. This theory develops

the focus on stakeholders and not the shareholders only. In order to discuss the concept of

this theory, this is to state that every stakeholder is important for the organization. No

doubt, shareholders play their significant role when it comes to the capital and funding,

but the role of other stakeholders cannot be ignored for this reason (Dennehy, 2012).

Clients, suppliers, customers, employees are few internal as well as external stakeholders

that are influenced by the activities of the entity. An entity while doing anything or while

taking decisions must ensure the interest of all the stakeholders. In this manner, it

becomes a special responsibility of management to ensure that all the stakeholders are

getting a fair return in respect to their stake. It was argued by Sundaram & Inkpen (2004)

that the stakeholder theory tries to state that every stakeholder's group deserves to be in

the attention of management. The theory can be better understand by having a look at the

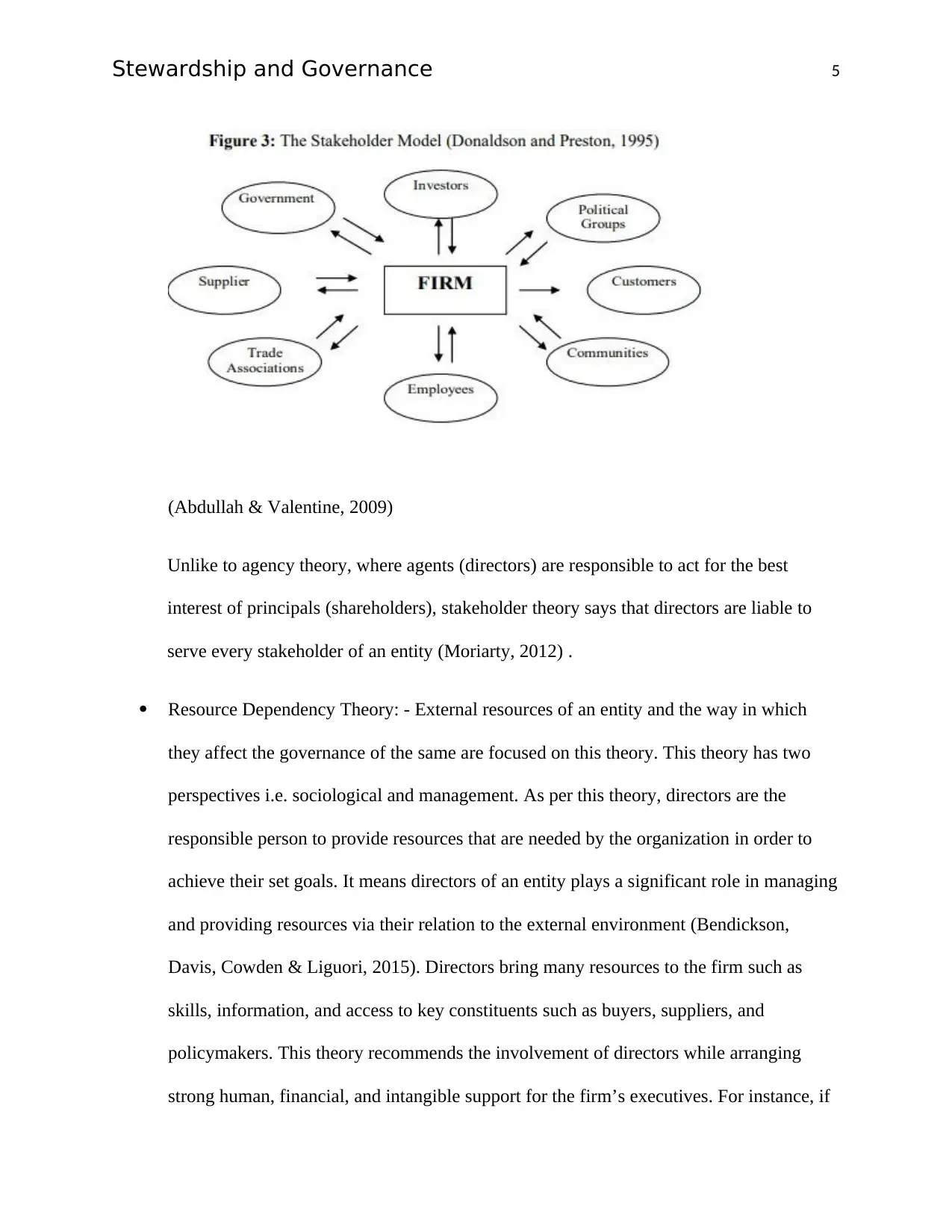

following diagram:-

summarized way this is to say that as per the agency theory, agents i.e. directors and

managers must work in the best interest of principals i.e. Shareholders.

Stakeholder Theory: - Freeman has developed this theory by introducing corporate

responsibility and accountability to a broad range of stakeholders. This theory develops

the focus on stakeholders and not the shareholders only. In order to discuss the concept of

this theory, this is to state that every stakeholder is important for the organization. No

doubt, shareholders play their significant role when it comes to the capital and funding,

but the role of other stakeholders cannot be ignored for this reason (Dennehy, 2012).

Clients, suppliers, customers, employees are few internal as well as external stakeholders

that are influenced by the activities of the entity. An entity while doing anything or while

taking decisions must ensure the interest of all the stakeholders. In this manner, it

becomes a special responsibility of management to ensure that all the stakeholders are

getting a fair return in respect to their stake. It was argued by Sundaram & Inkpen (2004)

that the stakeholder theory tries to state that every stakeholder's group deserves to be in

the attention of management. The theory can be better understand by having a look at the

following diagram:-

Stewardship and Governance 5

(Abdullah & Valentine, 2009)

Unlike to agency theory, where agents (directors) are responsible to act for the best

interest of principals (shareholders), stakeholder theory says that directors are liable to

serve every stakeholder of an entity (Moriarty, 2012) .

Resource Dependency Theory: - External resources of an entity and the way in which

they affect the governance of the same are focused on this theory. This theory has two

perspectives i.e. sociological and management. As per this theory, directors are the

responsible person to provide resources that are needed by the organization in order to

achieve their set goals. It means directors of an entity plays a significant role in managing

and providing resources via their relation to the external environment (Bendickson,

Davis, Cowden & Liguori, 2015). Directors bring many resources to the firm such as

skills, information, and access to key constituents such as buyers, suppliers, and

policymakers. This theory recommends the involvement of directors while arranging

strong human, financial, and intangible support for the firm’s executives. For instance, if

(Abdullah & Valentine, 2009)

Unlike to agency theory, where agents (directors) are responsible to act for the best

interest of principals (shareholders), stakeholder theory says that directors are liable to

serve every stakeholder of an entity (Moriarty, 2012) .

Resource Dependency Theory: - External resources of an entity and the way in which

they affect the governance of the same are focused on this theory. This theory has two

perspectives i.e. sociological and management. As per this theory, directors are the

responsible person to provide resources that are needed by the organization in order to

achieve their set goals. It means directors of an entity plays a significant role in managing

and providing resources via their relation to the external environment (Bendickson,

Davis, Cowden & Liguori, 2015). Directors bring many resources to the firm such as

skills, information, and access to key constituents such as buyers, suppliers, and

policymakers. This theory recommends the involvement of directors while arranging

strong human, financial, and intangible support for the firm’s executives. For instance, if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stewardship and Governance 6

professional members are there on the board of the company then the same can use

his/her expertise, knowledge, and experience to train other executives. The theory is

significant to study here as it has been argued that the provisions of resources increase

firm’s functioning, its performance, and survival. Depending on the provisions of

resources, directors may be classified into four categories that are as follow:-

Insiders

Business Experts

Support Specialist and

Community influential

Stewardship Theory: _ According to Davis, Schoorman & Donaldson (1997), steward

safeguards and maximizes the wealth of shareholders by firm performance as by doing so

utility functions of steward are maximized. In this manner, stewards are organizational

executives that work for the benefit of shareholders. The theory focuses on the role of top

management as steward by incorporating and integrating their goals as part of the

organization. It discourse practice of self-interest. Further, the theory believes that

stewards are satisfied when an organization attains its goals. The model of this theory

mainly includes two parties which are managers and owners of the organization.

Managers perform their job in the interest of owners and in this manner; there is a clear

structure of governance. Both of these groups are benefited if success is attained. As

mentioned above, the theory suggests that managers are the stewards of owners and both

groups share certain general and common goals. In this way, the board is not advised to

be too controlling as suggested under agency theory (Ebrary.net, 2019). The owners

professional members are there on the board of the company then the same can use

his/her expertise, knowledge, and experience to train other executives. The theory is

significant to study here as it has been argued that the provisions of resources increase

firm’s functioning, its performance, and survival. Depending on the provisions of

resources, directors may be classified into four categories that are as follow:-

Insiders

Business Experts

Support Specialist and

Community influential

Stewardship Theory: _ According to Davis, Schoorman & Donaldson (1997), steward

safeguards and maximizes the wealth of shareholders by firm performance as by doing so

utility functions of steward are maximized. In this manner, stewards are organizational

executives that work for the benefit of shareholders. The theory focuses on the role of top

management as steward by incorporating and integrating their goals as part of the

organization. It discourse practice of self-interest. Further, the theory believes that

stewards are satisfied when an organization attains its goals. The model of this theory

mainly includes two parties which are managers and owners of the organization.

Managers perform their job in the interest of owners and in this manner; there is a clear

structure of governance. Both of these groups are benefited if success is attained. As

mentioned above, the theory suggests that managers are the stewards of owners and both

groups share certain general and common goals. In this way, the board is not advised to

be too controlling as suggested under agency theory (Ebrary.net, 2019). The owners

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stewardship and Governance 7

outline their requirements and goals to managers and then managers have to balance such

requirements with the demands of other stakeholders of the company. In such a way,

owners empower the management despite controlling them under this theory. As per this

theory, the relationship of the board with executives involves training, shared decision

making and mentoring.

Contributions of Stewardship theory

This theory provides very important principals in the sector of corporate governance and

therefore keeps the significant place in every organization no matter whether they are a profitable

or non-profit organization. In the following discussion, the focus will be made on the

contribution of Stewardship theory to profit and nonprofit organization.

Non-Profit Organization

As the name implies, these are the organizations, which do not work to earn profits. Such

organizations are commonly formed in the form of charitable trust and have a specific mission in

society. Some individuals and groups make these organizations by collecting contributions to the

social people and the public owns these organizations. As mentioned earlier, non-profits

organizations do not a worker for profits and for this reasons income earned by them are

distributable for the purpose of the same. It means the income of the same is used to be used for

fulfilling the organization’s objectives. Although a particular or identified owner is missing, but

still the same consist of Stewardship leadership. Committees, trustees, or board of directors

operate and regulate these organizations and ensure that a nonprofit firm is fulfilling its

objectives. Trustees and management committee members are people who take care of the

outline their requirements and goals to managers and then managers have to balance such

requirements with the demands of other stakeholders of the company. In such a way,

owners empower the management despite controlling them under this theory. As per this

theory, the relationship of the board with executives involves training, shared decision

making and mentoring.

Contributions of Stewardship theory

This theory provides very important principals in the sector of corporate governance and

therefore keeps the significant place in every organization no matter whether they are a profitable

or non-profit organization. In the following discussion, the focus will be made on the

contribution of Stewardship theory to profit and nonprofit organization.

Non-Profit Organization

As the name implies, these are the organizations, which do not work to earn profits. Such

organizations are commonly formed in the form of charitable trust and have a specific mission in

society. Some individuals and groups make these organizations by collecting contributions to the

social people and the public owns these organizations. As mentioned earlier, non-profits

organizations do not a worker for profits and for this reasons income earned by them are

distributable for the purpose of the same. It means the income of the same is used to be used for

fulfilling the organization’s objectives. Although a particular or identified owner is missing, but

still the same consist of Stewardship leadership. Committees, trustees, or board of directors

operate and regulate these organizations and ensure that a nonprofit firm is fulfilling its

objectives. Trustees and management committee members are people who take care of the

Stewardship and Governance 8

management of the organization and control the same. In this manner, controlling powers are not

limited to one or two people. Members are there that contribute their money to the organization

and takes shares in return. However, trustees and management committee has the right to dismiss

any member in case of misbehavior or other inappropriate conduct. As managers work in a group

hence it discourages the practice of self-interest. Here Stewardship theory applies. No member of

the management committee can think of self-interest or self-profits because decisions are used to

be made by all. It would not be wrong to mention that from the perspective of Stewardship

theory, no profit organizations are the owner and managers are stewards. Managers (members of

committees/trustees) are expected to fulfill and achieve the goals of the organization by serving

to the public (Coule, 2013). As Stewardship theory emphasis focuses on the accountability of

Stewards, this is to say that the board or management committee is responsible and accountable

on behalf of the organization. In general, such an organization shows there accountability by

furnishing their annual accounts to the public so that they can be ensured that the organization is

doing well to achieve its objectives. As giving back is a core concept of Stewardship theory, in

this manner, such an organization can engage the public through various means and can provide

better outcomes. For a nonprofit organization, the ultimate beneficiaries are public members and

therefore the entities must engage the public in the various activities and should ask for the

feedback. Board members of the nonprofit organization believe that their CEO will not pursue

the self-interest under Stewardship theory (Bernstein, Buse & Bilimoria, 2016).

Profit Origination

These organizations operate for a primary benefit to earn profits. Concept of Stewardship

theory is also present and applicable to this kind of organizations. In terms of ownership,

leadership and other aspects, such organizations are different from a non-profit organization. In

management of the organization and control the same. In this manner, controlling powers are not

limited to one or two people. Members are there that contribute their money to the organization

and takes shares in return. However, trustees and management committee has the right to dismiss

any member in case of misbehavior or other inappropriate conduct. As managers work in a group

hence it discourages the practice of self-interest. Here Stewardship theory applies. No member of

the management committee can think of self-interest or self-profits because decisions are used to

be made by all. It would not be wrong to mention that from the perspective of Stewardship

theory, no profit organizations are the owner and managers are stewards. Managers (members of

committees/trustees) are expected to fulfill and achieve the goals of the organization by serving

to the public (Coule, 2013). As Stewardship theory emphasis focuses on the accountability of

Stewards, this is to say that the board or management committee is responsible and accountable

on behalf of the organization. In general, such an organization shows there accountability by

furnishing their annual accounts to the public so that they can be ensured that the organization is

doing well to achieve its objectives. As giving back is a core concept of Stewardship theory, in

this manner, such an organization can engage the public through various means and can provide

better outcomes. For a nonprofit organization, the ultimate beneficiaries are public members and

therefore the entities must engage the public in the various activities and should ask for the

feedback. Board members of the nonprofit organization believe that their CEO will not pursue

the self-interest under Stewardship theory (Bernstein, Buse & Bilimoria, 2016).

Profit Origination

These organizations operate for a primary benefit to earn profits. Concept of Stewardship

theory is also present and applicable to this kind of organizations. In terms of ownership,

leadership and other aspects, such organizations are different from a non-profit organization. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stewardship and Governance 9

order to discuss the governance structure of this kind of organization, this is to state that mainly

two parties are there, one is the owner of the business, and another one is managers. These

managers play the role of Stewards. As the main purpose is to earn profits, hence, many

stakeholders are often engaged and structure of such organizations is more complicated. For

effective corporate governance in profit organizations, many concepts and principles of

Stewardship theory can apply. As managers are Steward, hence, they are accountable and their

professional success can be understood as the success of the organization. The other entire

workgroup such as founder, owner, and stakeholders review the performance of managers. Here

there is a risk that managers can misuse their position, can act for the self-interest, and can forget

the organizational goals. Stewardship models help here under which the performance of steward

can be evaluated. When managers act according to the stewardship model they consider the

interest of all and in this manner, stakeholders remain satisfied. When a manager ensure that

employees are satisfied, they work in a better way and feel like part of the organization. In this

manner, good governance can be ensured in profit organizations using stewardship model.

Leader’s values and effective governance

In the context of an organization, a leader is the one, which ensures corporate governance

and presences of all the ethical systems in place. Leadership is a manner in which leader deal

with the situations and people and similar to theories of corporate governance, leadership has

different theories. What leader thinks is directly reflected in the governance of the organization

and this is the reason that there is a direct relationship between the values of leader and

effectiveness of governance. Leaders should have a value of goodness of all and they should

adopt the principles of stewardship theory. As more good and efficient a leader will be, corporate

will have more good governance structure. Only adoption of different governance theory is not

order to discuss the governance structure of this kind of organization, this is to state that mainly

two parties are there, one is the owner of the business, and another one is managers. These

managers play the role of Stewards. As the main purpose is to earn profits, hence, many

stakeholders are often engaged and structure of such organizations is more complicated. For

effective corporate governance in profit organizations, many concepts and principles of

Stewardship theory can apply. As managers are Steward, hence, they are accountable and their

professional success can be understood as the success of the organization. The other entire

workgroup such as founder, owner, and stakeholders review the performance of managers. Here

there is a risk that managers can misuse their position, can act for the self-interest, and can forget

the organizational goals. Stewardship models help here under which the performance of steward

can be evaluated. When managers act according to the stewardship model they consider the

interest of all and in this manner, stakeholders remain satisfied. When a manager ensure that

employees are satisfied, they work in a better way and feel like part of the organization. In this

manner, good governance can be ensured in profit organizations using stewardship model.

Leader’s values and effective governance

In the context of an organization, a leader is the one, which ensures corporate governance

and presences of all the ethical systems in place. Leadership is a manner in which leader deal

with the situations and people and similar to theories of corporate governance, leadership has

different theories. What leader thinks is directly reflected in the governance of the organization

and this is the reason that there is a direct relationship between the values of leader and

effectiveness of governance. Leaders should have a value of goodness of all and they should

adopt the principles of stewardship theory. As more good and efficient a leader will be, corporate

will have more good governance structure. Only adoption of different governance theory is not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stewardship and Governance 10

enough, but values and beliefs of leader are also significant. When a leader is ethical and

understands the requirement of every stakeholder, the same practice good governance

considering the interest of all. On the other side, if the leader of an organization considers self-

interest then governance cannot be assumed to be effective. In this manner, this is to state that

what a leader thinks and believes highly affect the governance level and quality in the

organization.

Conclusion

In order to conclude the discussion on the governance theories, this is to state that these

theories provide different concepts and enlighten the path of management. Everyone knows that

governance should be good but how the same can be achieved is addressed by governance

theories. In the presented paper/report, different corporate governance theories have been

discussed namely Stakeholder Theory, Agency Theory, Resource Dependency Theory, and

Stewardship Theory. Stewardship Theory seems to be very significant out of them as the same

work in profit as well as in nonprofit organizations. Further, it is closely connected to other

theories such as agency and stakeholder theory. The manner in which the theory can be adopted

by profit, as well as the nonprofit organization, has also been discussed in the above-mentioned

discussion. At last, the relationship between a leader’s value and effectiveness of governance has

been discussed. This is to conclude that the management of every organization is required to set

aside self-interest while working on behalf of their organization and should consider the interest

of all stakeholders. If a leader would believe in such practices then the organization will be able

to attain a very good level of corporate governance.

enough, but values and beliefs of leader are also significant. When a leader is ethical and

understands the requirement of every stakeholder, the same practice good governance

considering the interest of all. On the other side, if the leader of an organization considers self-

interest then governance cannot be assumed to be effective. In this manner, this is to state that

what a leader thinks and believes highly affect the governance level and quality in the

organization.

Conclusion

In order to conclude the discussion on the governance theories, this is to state that these

theories provide different concepts and enlighten the path of management. Everyone knows that

governance should be good but how the same can be achieved is addressed by governance

theories. In the presented paper/report, different corporate governance theories have been

discussed namely Stakeholder Theory, Agency Theory, Resource Dependency Theory, and

Stewardship Theory. Stewardship Theory seems to be very significant out of them as the same

work in profit as well as in nonprofit organizations. Further, it is closely connected to other

theories such as agency and stakeholder theory. The manner in which the theory can be adopted

by profit, as well as the nonprofit organization, has also been discussed in the above-mentioned

discussion. At last, the relationship between a leader’s value and effectiveness of governance has

been discussed. This is to conclude that the management of every organization is required to set

aside self-interest while working on behalf of their organization and should consider the interest

of all stakeholders. If a leader would believe in such practices then the organization will be able

to attain a very good level of corporate governance.

Stewardship and Governance 11

References

Abdullah, H., & Valentine, B. (2009). Fundamental and ethics theories of corporate

governance. Middle Eastern Finance and Economics, 4(4), 88-96.

Abid, G. Khan, B. Rafiq, Z. and Ahmad, A. (2014).Theoretical Perspective of Corpornance.

Bulletin of Business and Economics, 3(4), 166-175.

Bendickson, J., Davis,P., Cowden, B., J. & Liguori, E., W. (2015). Why Small Firms Are

Different: Addressing Varying Needs From Boards Of Directors. Journal of small

business strategy, 25 (2)

Bernstein, R., Buse, K., & Bilimoria, D. (2016). Revisiting Agency and Stewardship

Theories. Nonprofit Management And Leadership, 26(4), 489-498. doi:

10.1002/nml.21199

Coule, T. (2013). Nonprofit Governance and Accountability. Nonprofit And Voluntary Sector

Quarterly, 44(1), 75-97. doi: 10.1177/0899764013503906

Davoren, J. (2019). Three Types of Corporate Governance Mechanisms. Retrieved From:

https://smallbusiness.chron.com/three-types-corporate-governance-mechanisms-

66711.html

Dennehy, E. (2012). Corporate governance - a stakeholder model. International Journal Of

Business Governance And Ethics, 7(2), 83. doi: 10.1504/ijbge.2012.047536

Ebrary.net. (2019). Governance Theories. Retrieved From:

https://ebrary.net/8636/business_finance/governance_theories

References

Abdullah, H., & Valentine, B. (2009). Fundamental and ethics theories of corporate

governance. Middle Eastern Finance and Economics, 4(4), 88-96.

Abid, G. Khan, B. Rafiq, Z. and Ahmad, A. (2014).Theoretical Perspective of Corpornance.

Bulletin of Business and Economics, 3(4), 166-175.

Bendickson, J., Davis,P., Cowden, B., J. & Liguori, E., W. (2015). Why Small Firms Are

Different: Addressing Varying Needs From Boards Of Directors. Journal of small

business strategy, 25 (2)

Bernstein, R., Buse, K., & Bilimoria, D. (2016). Revisiting Agency and Stewardship

Theories. Nonprofit Management And Leadership, 26(4), 489-498. doi:

10.1002/nml.21199

Coule, T. (2013). Nonprofit Governance and Accountability. Nonprofit And Voluntary Sector

Quarterly, 44(1), 75-97. doi: 10.1177/0899764013503906

Davoren, J. (2019). Three Types of Corporate Governance Mechanisms. Retrieved From:

https://smallbusiness.chron.com/three-types-corporate-governance-mechanisms-

66711.html

Dennehy, E. (2012). Corporate governance - a stakeholder model. International Journal Of

Business Governance And Ethics, 7(2), 83. doi: 10.1504/ijbge.2012.047536

Ebrary.net. (2019). Governance Theories. Retrieved From:

https://ebrary.net/8636/business_finance/governance_theories

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.