ECON 3: Federal, State, and Local Government Budget Comparison Report

VerifiedAdded on 2020/02/18

|12

|1840

|53

Report

AI Summary

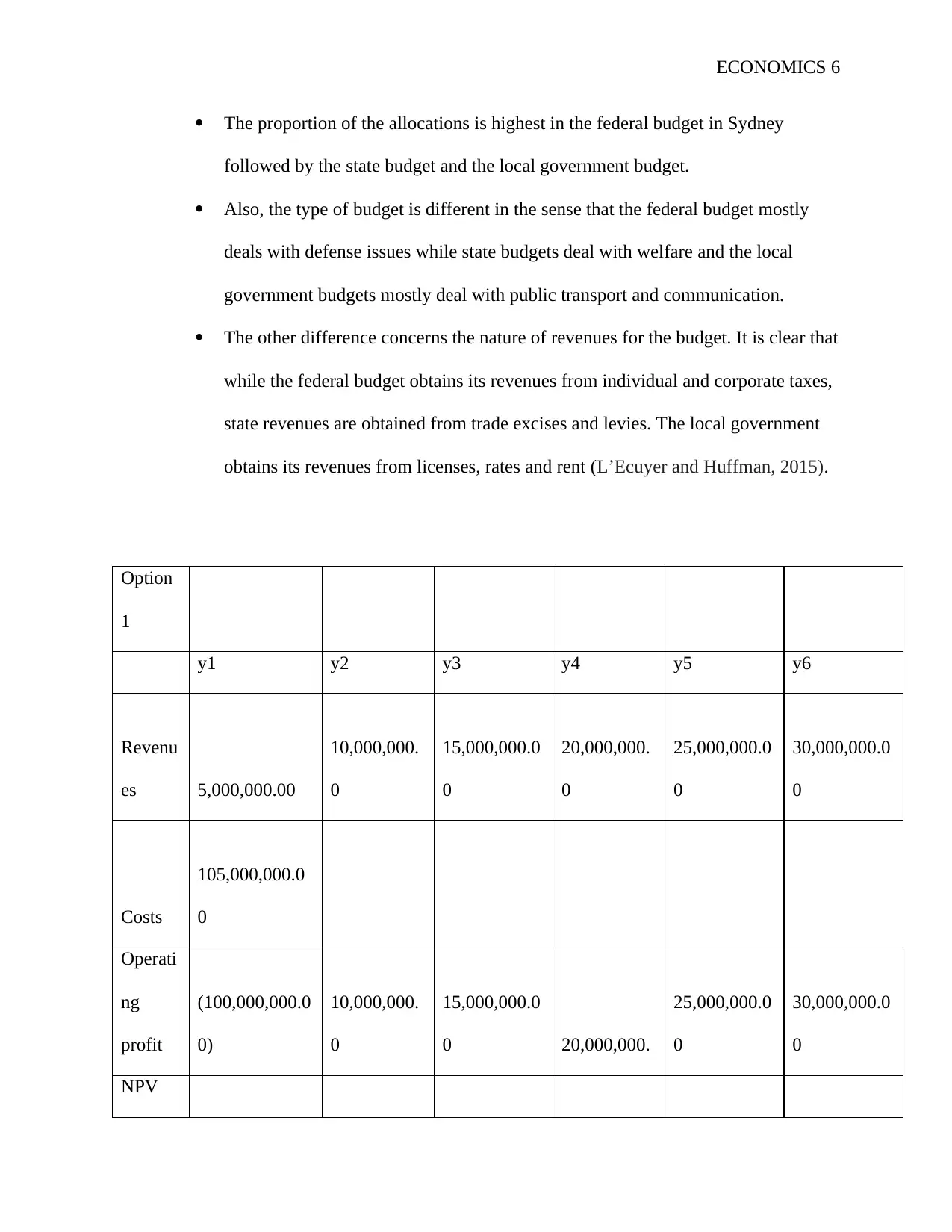

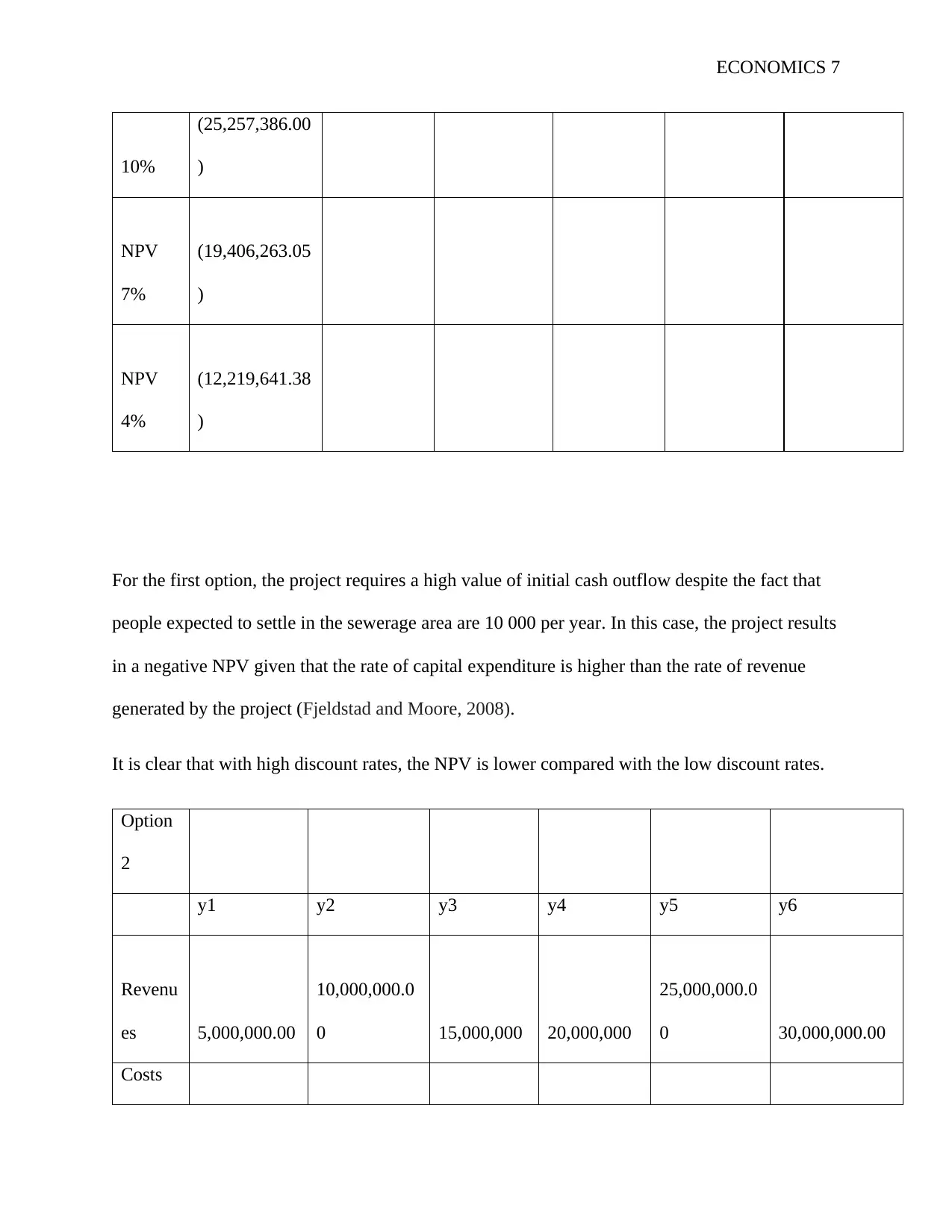

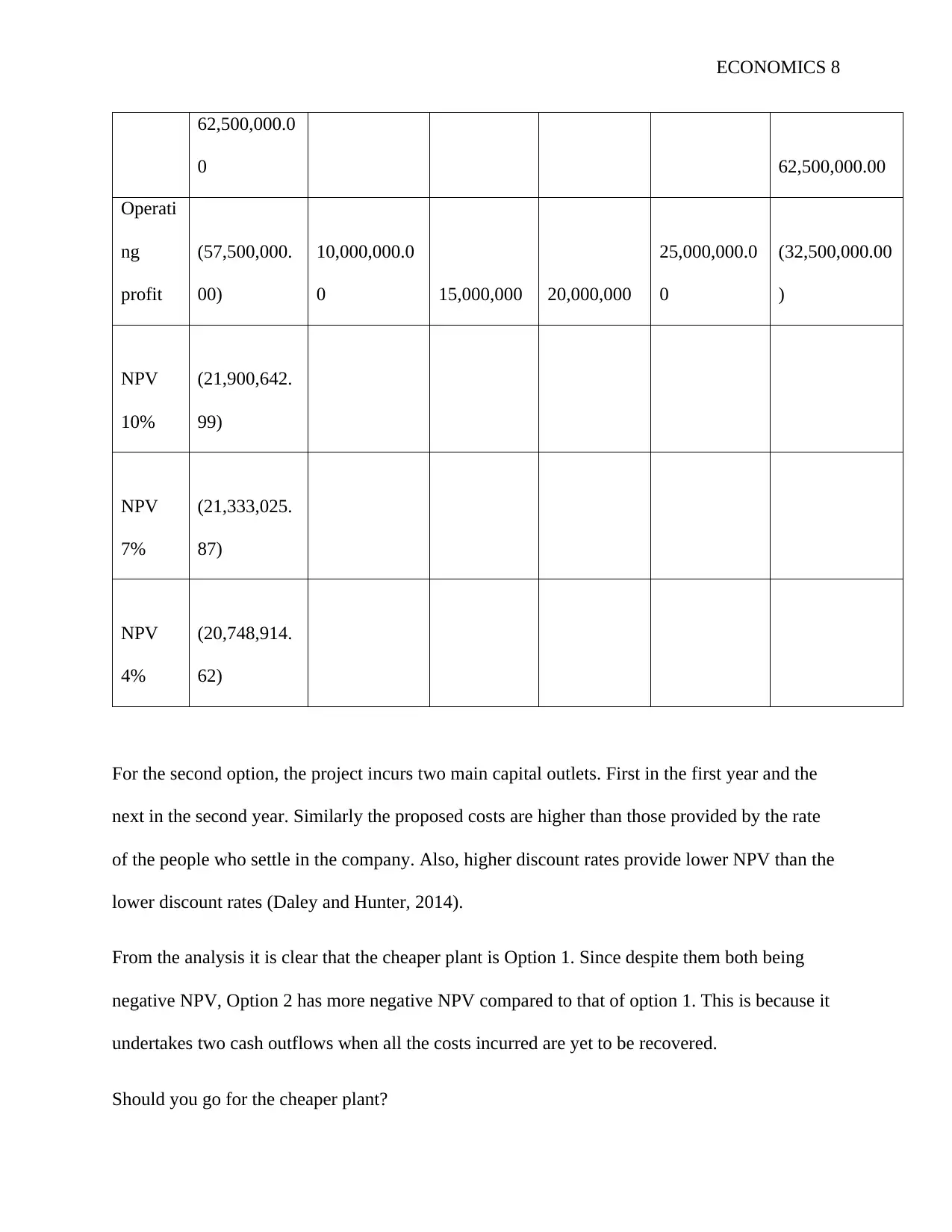

This report, prepared for an Economics 3 course, examines the budgetary differences between the federal, state, and local governments. It analyzes the allocation of funds, revenue sources (including taxes, levies, and licenses), and expenditure patterns of each level of government. The federal budget, primarily focused on defense and national programs, is contrasted with state budgets that emphasize social security, education, and health, and local government budgets which are focused on public transport and communication. The report highlights the varying proportions of allocations, revenue generation methods, and the implications of these differences. The analysis also includes a case study of two investment options, their pros and cons, and the decision-making process involved, considering factors like financial capacity and project feasibility. The report concludes by summarizing the key differences and providing references to support the analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.