UK Tax System: Tax Gap, Avoidance, Evasion, and Government Response

VerifiedAdded on 2020/12/29

|7

|1278

|438

Report

AI Summary

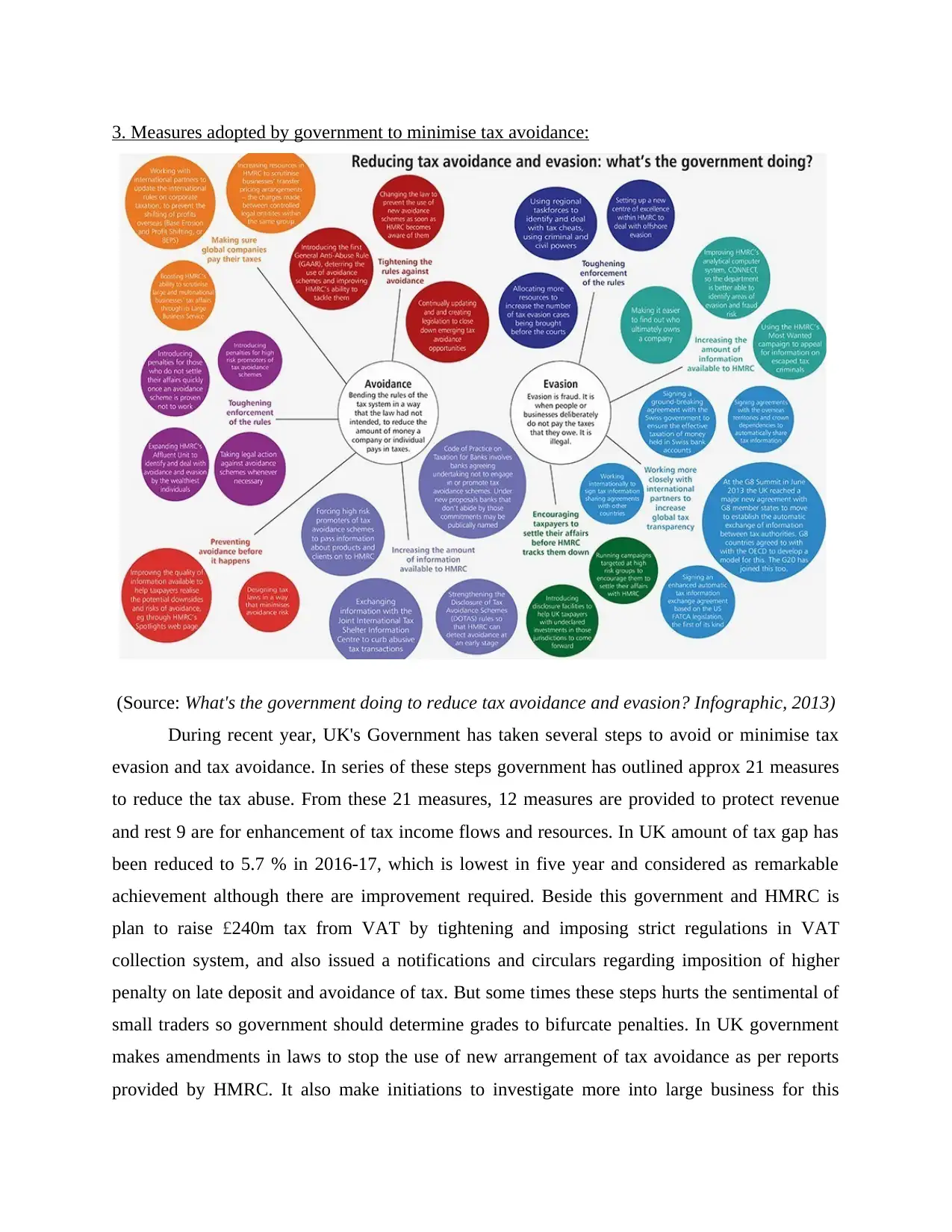

This report provides an overview of tax-related concepts in the UK, focusing on the tax gap, tax avoidance, and tax evasion. It explains the differences between tax avoidance, which involves legal methods to minimize tax liability, and tax evasion, which involves illegal methods. The report details aggressive tax avoidance schemes and arrangements used by taxpayers, such as offshore accounts and VAT supply splitting. It also outlines the measures adopted by the UK government and HMRC to minimize tax avoidance and evasion, including legislative amendments, increased scrutiny of large businesses, and international agreements. The report concludes that while the government has taken effective steps, there is a need for continuous improvement to make these steps more taxpayer-friendly. The report references key sources including academic journals and government publications.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.