Analysis of Contemporary Accounting Issues in GrainCorp Limited

VerifiedAdded on 2023/06/15

|11

|2099

|415

Report

AI Summary

This report provides an analysis of GrainCorp Limited's financial statements, focusing on their adherence to the Australian Accounting Standards Board (AASB) regulations and the International Financial Reporting Standards (IFRS). It examines the conceptual framework underlying the statements, the recognition criteria used, and the fundamental qualitative enhancing features of the financial reporting. The analysis confirms that GrainCorp Limited effectively complies with AASB guidelines, ensuring the reliability and faithfulness of its financial statements. The report concludes that GrainCorp Limited's financial reporting presents a true and fair view of the company's financial position and performance, making it a valuable resource for stakeholders and investors. Desklib provides similar solved assignments and past papers for students.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author Note

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Conceptual framework and its reporting....................................................................................3

Recognition Criteria...................................................................................................................5

Fundamental Qualitative Enhancing characteristics of financial reporting...............................7

Conclusion..................................................................................................................................8

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................3

Conceptual framework and its reporting....................................................................................3

Recognition Criteria...................................................................................................................5

Fundamental Qualitative Enhancing characteristics of financial reporting...............................7

Conclusion..................................................................................................................................8

References................................................................................................................................10

2CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The primary logic behind this study is to determine if the accounting statements

prepared by an organization adhere to the guidelines and principles laid down by the

regulating bodies. Through this study, an understanding of the basic concepts of accounts and

the regulatory standards of constructing the major accounting statements has been aimed at.

The company chosen for the purpose of this examination is GrainCorp Limited.

GrainCorp Limited is an Australian leading agribusiness company that deals in grain

activities. For analyzing the accounting statements, the annual report for the financial year of

2016 of the company has been chosen.

Abstract

The primary logic behind this study is to determine if the accounting statements

prepared by an organization adhere to the guidelines and principles laid down by the

regulating bodies. Through this study, an understanding of the basic concepts of accounts and

the regulatory standards of constructing the major accounting statements has been aimed at.

The company chosen for the purpose of this examination is GrainCorp Limited.

GrainCorp Limited is an Australian leading agribusiness company that deals in grain

activities. For analyzing the accounting statements, the annual report for the financial year of

2016 of the company has been chosen.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The most important reference while measuring the financial performance of a

company are its accounting statements which have been prepared by the administration of the

concerned entity. This is done in accordance to the policies and regulations set by the

financial institutions. Therefore, the adherence to the financial and other criteria or standards

is very important in order to produce the accounting statements that reflect a real and fair

image of the firm. This particular study analyzes the annual report of GrainCorp Limited and

provides an overview as to whether the construction of the accounting statements has been

done in compliance to the laid down policies and regulations (Loyeung et al., 2016).

Conceptual framework and its reporting

The term conceptual framework refers to a framework that in particular deals with the

fundamental financial reporting issues that range from the utilization of the financial

statements to the to the objectives of such statements, their characteristics and other

associated features that enhance the usefulness of such statements and make them simple to

understand and analyze by its users .

The general objectives of a regulating body, for instance, the Australian Accounting

Standards Board state that the framework has been framed in order to support the regulating

body to promote the harmonization of the already set regulations, assist the auditors in

making their opinions and also assist the users in the efficient utilization of the financial

statements.

GrainCorp Limited states in its annual report for the current accounting year of 2016

that the accounting statements were constructed in compliance with the Australian

Accounting Standards and other authoritative pronouncements of the Australian Accounting

Introduction

The most important reference while measuring the financial performance of a

company are its accounting statements which have been prepared by the administration of the

concerned entity. This is done in accordance to the policies and regulations set by the

financial institutions. Therefore, the adherence to the financial and other criteria or standards

is very important in order to produce the accounting statements that reflect a real and fair

image of the firm. This particular study analyzes the annual report of GrainCorp Limited and

provides an overview as to whether the construction of the accounting statements has been

done in compliance to the laid down policies and regulations (Loyeung et al., 2016).

Conceptual framework and its reporting

The term conceptual framework refers to a framework that in particular deals with the

fundamental financial reporting issues that range from the utilization of the financial

statements to the to the objectives of such statements, their characteristics and other

associated features that enhance the usefulness of such statements and make them simple to

understand and analyze by its users .

The general objectives of a regulating body, for instance, the Australian Accounting

Standards Board state that the framework has been framed in order to support the regulating

body to promote the harmonization of the already set regulations, assist the auditors in

making their opinions and also assist the users in the efficient utilization of the financial

statements.

GrainCorp Limited states in its annual report for the current accounting year of 2016

that the accounting statements were constructed in compliance with the Australian

Accounting Standards and other authoritative pronouncements of the Australian Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

Standards Board and the Corporations Act 2001. It has been further stated that the accounting

statements have been constructed on a going concern basis. A going concern, according to the

regulating body of the Australian Accounting Standards Board, is essentially a standard

which normally assumes that the firm is very effectively a going concern and shall resume its

operations through the days to come (Wee, Tarca and Chang 2014). Hence, it is further

assumed that the entity has no intention to liquidate its assets or be insolvent in the near

future. A company in order to qualify as a going concern should have to maintain a stable

business without the need to curtail materiality.

Figure: Basis of preparation

Source: GrainCorp Limited, Annual Report, 2016

Standards Board and the Corporations Act 2001. It has been further stated that the accounting

statements have been constructed on a going concern basis. A going concern, according to the

regulating body of the Australian Accounting Standards Board, is essentially a standard

which normally assumes that the firm is very effectively a going concern and shall resume its

operations through the days to come (Wee, Tarca and Chang 2014). Hence, it is further

assumed that the entity has no intention to liquidate its assets or be insolvent in the near

future. A company in order to qualify as a going concern should have to maintain a stable

business without the need to curtail materiality.

Figure: Basis of preparation

Source: GrainCorp Limited, Annual Report, 2016

5CONTEMPORARY ISSUES IN ACCOUNTING

It is further stated, in the financial report of the entity that the accounting statements

have in all probabilities been constructed complying to the International Financial Reporting

Standards (IFRS).

This can be understood by the fact that the company has provided relevant disclosures

in the accounting statements. Moreover, the company has prepared the income statement,

balance sheet, cash flow statements and statement of changes in equity, which effectively

complies with the requirements of AASB. Further, it has been stated in the annual report that

the certain comparative accounts have been reclassified to align with current period

presentation. Moreover, each and every financial component that has been included in the

accounting statements, have been referred to in the disclosures to financial reporting as

proper disclosures that has made it easier to understand (Lovell 2014).

Therefore, the management of GrainCorp Limited in the preparation construction of

the accounting statements has effectively adhered to the conceptual framework laid down by

the Australian Accounting Standards Board (AASB).

Recognition Criteria

The recognition criteria is an important criteria on the basis of which the company

aims to prepare its financial statements. There are two methods laid down by AASB

according to which a particular company may prepare its financial statements. These are

accounting statements prepared on the basis of cash received and accounting statements

constructed occurrence basis. The accounting statements prepared on cash basis recognize an

asset or liability or a loss or gain at the exact moment when cash or capital in actual flows in

or out of business. On the other hand, accounting statements prepared on the basis of

occurrence, records a certain transaction or an asset or liability or revenue or expenditure at

the time when it occurs or is intended by business.

It is further stated, in the financial report of the entity that the accounting statements

have in all probabilities been constructed complying to the International Financial Reporting

Standards (IFRS).

This can be understood by the fact that the company has provided relevant disclosures

in the accounting statements. Moreover, the company has prepared the income statement,

balance sheet, cash flow statements and statement of changes in equity, which effectively

complies with the requirements of AASB. Further, it has been stated in the annual report that

the certain comparative accounts have been reclassified to align with current period

presentation. Moreover, each and every financial component that has been included in the

accounting statements, have been referred to in the disclosures to financial reporting as

proper disclosures that has made it easier to understand (Lovell 2014).

Therefore, the management of GrainCorp Limited in the preparation construction of

the accounting statements has effectively adhered to the conceptual framework laid down by

the Australian Accounting Standards Board (AASB).

Recognition Criteria

The recognition criteria is an important criteria on the basis of which the company

aims to prepare its financial statements. There are two methods laid down by AASB

according to which a particular company may prepare its financial statements. These are

accounting statements prepared on the basis of cash received and accounting statements

constructed occurrence basis. The accounting statements prepared on cash basis recognize an

asset or liability or a loss or gain at the exact moment when cash or capital in actual flows in

or out of business. On the other hand, accounting statements prepared on the basis of

occurrence, records a certain transaction or an asset or liability or revenue or expenditure at

the time when it occurs or is intended by business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

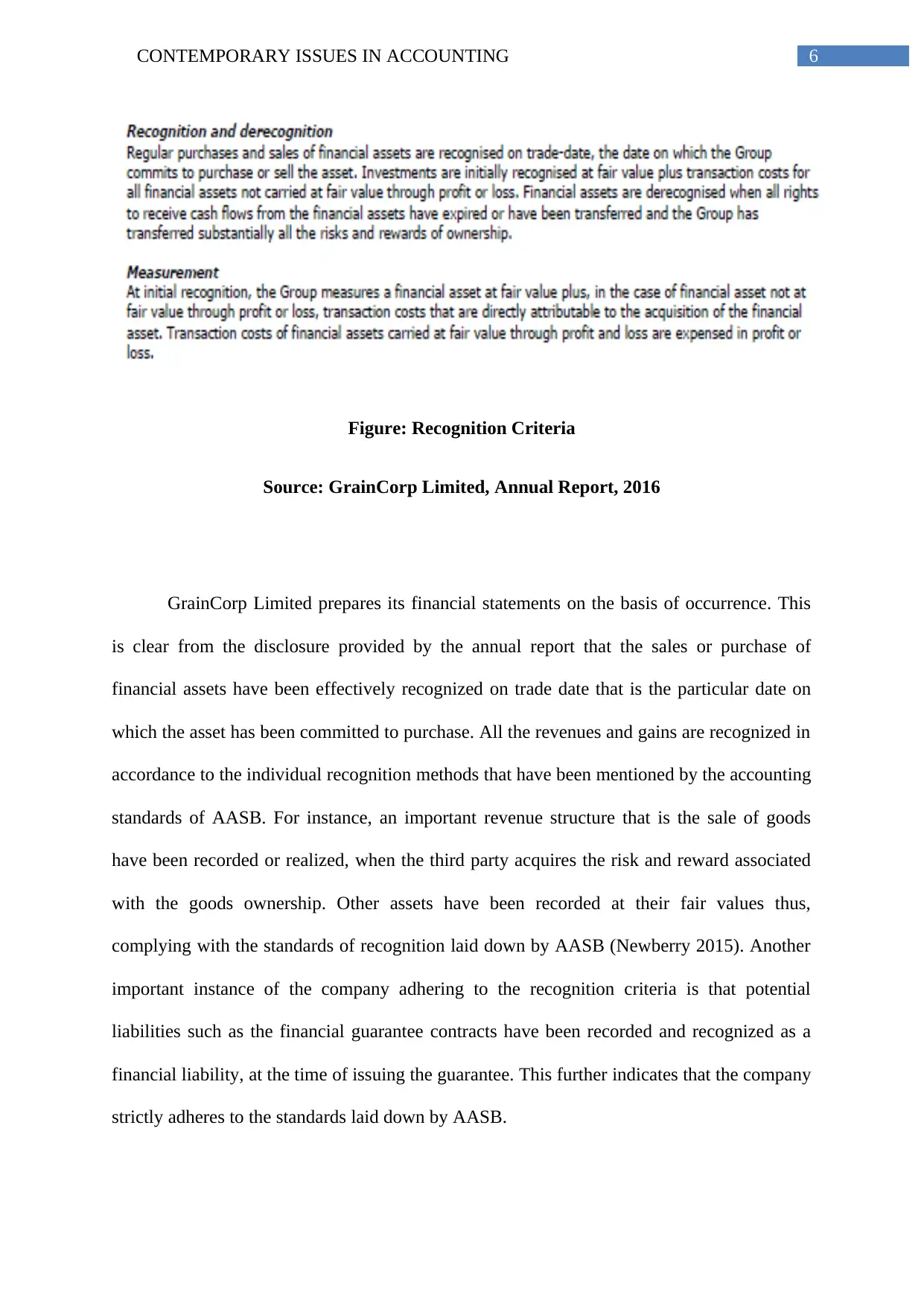

Figure: Recognition Criteria

Source: GrainCorp Limited, Annual Report, 2016

GrainCorp Limited prepares its financial statements on the basis of occurrence. This

is clear from the disclosure provided by the annual report that the sales or purchase of

financial assets have been effectively recognized on trade date that is the particular date on

which the asset has been committed to purchase. All the revenues and gains are recognized in

accordance to the individual recognition methods that have been mentioned by the accounting

standards of AASB. For instance, an important revenue structure that is the sale of goods

have been recorded or realized, when the third party acquires the risk and reward associated

with the goods ownership. Other assets have been recorded at their fair values thus,

complying with the standards of recognition laid down by AASB (Newberry 2015). Another

important instance of the company adhering to the recognition criteria is that potential

liabilities such as the financial guarantee contracts have been recorded and recognized as a

financial liability, at the time of issuing the guarantee. This further indicates that the company

strictly adheres to the standards laid down by AASB.

Figure: Recognition Criteria

Source: GrainCorp Limited, Annual Report, 2016

GrainCorp Limited prepares its financial statements on the basis of occurrence. This

is clear from the disclosure provided by the annual report that the sales or purchase of

financial assets have been effectively recognized on trade date that is the particular date on

which the asset has been committed to purchase. All the revenues and gains are recognized in

accordance to the individual recognition methods that have been mentioned by the accounting

standards of AASB. For instance, an important revenue structure that is the sale of goods

have been recorded or realized, when the third party acquires the risk and reward associated

with the goods ownership. Other assets have been recorded at their fair values thus,

complying with the standards of recognition laid down by AASB (Newberry 2015). Another

important instance of the company adhering to the recognition criteria is that potential

liabilities such as the financial guarantee contracts have been recorded and recognized as a

financial liability, at the time of issuing the guarantee. This further indicates that the company

strictly adheres to the standards laid down by AASB.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

Therefore, it is evidently proved that the company complies to the principle of

recognition criteria as laid down by the Australian Accounting Standards Board and strictly

adheres to it.

Fundamental Qualitative Enhancing features of financial reporting

The qualitative enhancing features of the financial statements of the company

essentially refer to the quality of the information provided in the accountingl statements of a

particular organization. This means that the primary objective of the financial statements is

that the external users of the statements may get an idea about the financial condition and the

performance of the company. This can only be achieved when the statements are prepared

provide information that is understandability, comparability, timeliness and verifiability.

GrainCorp Limited adheres to the first criteria that is understandability of the

accounting statements completely. The administration of the company provides enough scope

to the user of the financial statements to understand and scrutinize the performance and

condition of the company (Saha and Roy 2017).

Secondly, it prepares its accounting statement complying to the generally accepted

accounting principles that provides common standards of measurement and judgment. This

makes comparison of the financial performance of GrainCorp Limited with its fellow

competitors easier to execute and understand. The explanation of each financial component in

the accounting disclosures of the financial report gives an excellent view into the financial

condition by the company.

Thirdly, the timeliness of the information disclosed in the accounting statements also

appears to be accurate. Even the carrying value of any account or an asset or liability has

Therefore, it is evidently proved that the company complies to the principle of

recognition criteria as laid down by the Australian Accounting Standards Board and strictly

adheres to it.

Fundamental Qualitative Enhancing features of financial reporting

The qualitative enhancing features of the financial statements of the company

essentially refer to the quality of the information provided in the accountingl statements of a

particular organization. This means that the primary objective of the financial statements is

that the external users of the statements may get an idea about the financial condition and the

performance of the company. This can only be achieved when the statements are prepared

provide information that is understandability, comparability, timeliness and verifiability.

GrainCorp Limited adheres to the first criteria that is understandability of the

accounting statements completely. The administration of the company provides enough scope

to the user of the financial statements to understand and scrutinize the performance and

condition of the company (Saha and Roy 2017).

Secondly, it prepares its accounting statement complying to the generally accepted

accounting principles that provides common standards of measurement and judgment. This

makes comparison of the financial performance of GrainCorp Limited with its fellow

competitors easier to execute and understand. The explanation of each financial component in

the accounting disclosures of the financial report gives an excellent view into the financial

condition by the company.

Thirdly, the timeliness of the information disclosed in the accounting statements also

appears to be accurate. Even the carrying value of any account or an asset or liability has

8CONTEMPORARY ISSUES IN ACCOUNTING

been properly disclosed revealing that the financial statements have accurately met the aspect

of timeliness (Jin, Shan and Taylor 2015).

The aspect of verifiability can be confirmed by the auditor’s report. The auditor’s

report mentions that the accounting particulars have been prepared in compliance to the

Corporations Act 300A further revealing that there has been no issue of materiality in the

books of accounts. Moreover, the accounting standards in all probabilities reveal a real and

fair image of the firm thus enhancing verifiability of the financial statements. Therefore,

GrainCorp Limited has very effectively adhered to the fundamental qualitative enhancing of

financial reporting (Morris 2017).

The faithfulness of the accounting statements have been proved by the auditor’s

opinion. Moreover, the company seem to be in a healthy financial position without the need

to curtail materiality. This means that there has been no occurrence of material misstatement

in the books of accounts either deliberately or by mistake further revealing and confirming

the genuineness of the information disclosed in the accounting statements of the company.

Therefore, it can be added that the degree of reliability of the accounting statements

produced in the annual report of the company are high and the stakeholders of business or

other third party investors making decision on the basis of such statements, will in all

probabilities lead to potentially good decisions.

Conclusion

The finding that is arrived at after the scrutiny of the financial statements of

GrainCorp Limited is that the company strictly adheres to the principles or regulations laid

down by the Australian Accounting Standards Board in terms of its financial reporting. The

conceptual framework that has acted as the foundation of the accounting statements has

been properly disclosed revealing that the financial statements have accurately met the aspect

of timeliness (Jin, Shan and Taylor 2015).

The aspect of verifiability can be confirmed by the auditor’s report. The auditor’s

report mentions that the accounting particulars have been prepared in compliance to the

Corporations Act 300A further revealing that there has been no issue of materiality in the

books of accounts. Moreover, the accounting standards in all probabilities reveal a real and

fair image of the firm thus enhancing verifiability of the financial statements. Therefore,

GrainCorp Limited has very effectively adhered to the fundamental qualitative enhancing of

financial reporting (Morris 2017).

The faithfulness of the accounting statements have been proved by the auditor’s

opinion. Moreover, the company seem to be in a healthy financial position without the need

to curtail materiality. This means that there has been no occurrence of material misstatement

in the books of accounts either deliberately or by mistake further revealing and confirming

the genuineness of the information disclosed in the accounting statements of the company.

Therefore, it can be added that the degree of reliability of the accounting statements

produced in the annual report of the company are high and the stakeholders of business or

other third party investors making decision on the basis of such statements, will in all

probabilities lead to potentially good decisions.

Conclusion

The finding that is arrived at after the scrutiny of the financial statements of

GrainCorp Limited is that the company strictly adheres to the principles or regulations laid

down by the Australian Accounting Standards Board in terms of its financial reporting. The

conceptual framework that has acted as the foundation of the accounting statements has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

strengthened the accounting base of the company by revealing its true image via the financial

statements that are the income statement, balance sheet and the cash flow statement. The

reliability of the information provided in the accounting statements is high as the books have

been prepared by following the guidelines of AASB. Thus, GainCorp Limited has

successfully adhered to all the criteria, that qualifies its financial statements as the statements

that reflect a real and fair image of the company.

strengthened the accounting base of the company by revealing its true image via the financial

statements that are the income statement, balance sheet and the cash flow statement. The

reliability of the information provided in the accounting statements is high as the books have

been prepared by following the guidelines of AASB. Thus, GainCorp Limited has

successfully adhered to all the criteria, that qualifies its financial statements as the statements

that reflect a real and fair image of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

References

Morris, R.D., 2017. Discussion of: The Phoenix Rises: The Australian Accounting Standards

Board and IFRS Adoption. Journal of International Accounting Research, 16(2), pp.155-157.

Saha, S.S. and Roy, M.N., 2017. Quality Control Procedure for Statutory Financial Audit: An

Empirical Study.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

Lovell, H., 2014. Climate change, markets and standards: the case of financial accounting.

Economy and Society, 43(2), pp.260-284.

Loyeung, A., Matolcsy, Z., Weber, J. and Wells, P., 2016. The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), pp.611-632.

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in Accounting,

31(1), pp.165-178.

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Wee, M., Tarca, A. and Chang, M., 2014. Disclosure incentives, mandatory standards and

firm communication in the IFRS adoption setting. Australian Journal of Management, 39(2),

pp.265-291.

References

Morris, R.D., 2017. Discussion of: The Phoenix Rises: The Australian Accounting Standards

Board and IFRS Adoption. Journal of International Accounting Research, 16(2), pp.155-157.

Saha, S.S. and Roy, M.N., 2017. Quality Control Procedure for Statutory Financial Audit: An

Empirical Study.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

Lovell, H., 2014. Climate change, markets and standards: the case of financial accounting.

Economy and Society, 43(2), pp.260-284.

Loyeung, A., Matolcsy, Z., Weber, J. and Wells, P., 2016. The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), pp.611-632.

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in Accounting,

31(1), pp.165-178.

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Wee, M., Tarca, A. and Chang, M., 2014. Disclosure incentives, mandatory standards and

firm communication in the IFRS adoption setting. Australian Journal of Management, 39(2),

pp.265-291.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.