ACCT 701, Centennial College Assignment 3: Transfer Pricing Analysis

VerifiedAdded on 2022/10/09

|5

|723

|394

Homework Assignment

AI Summary

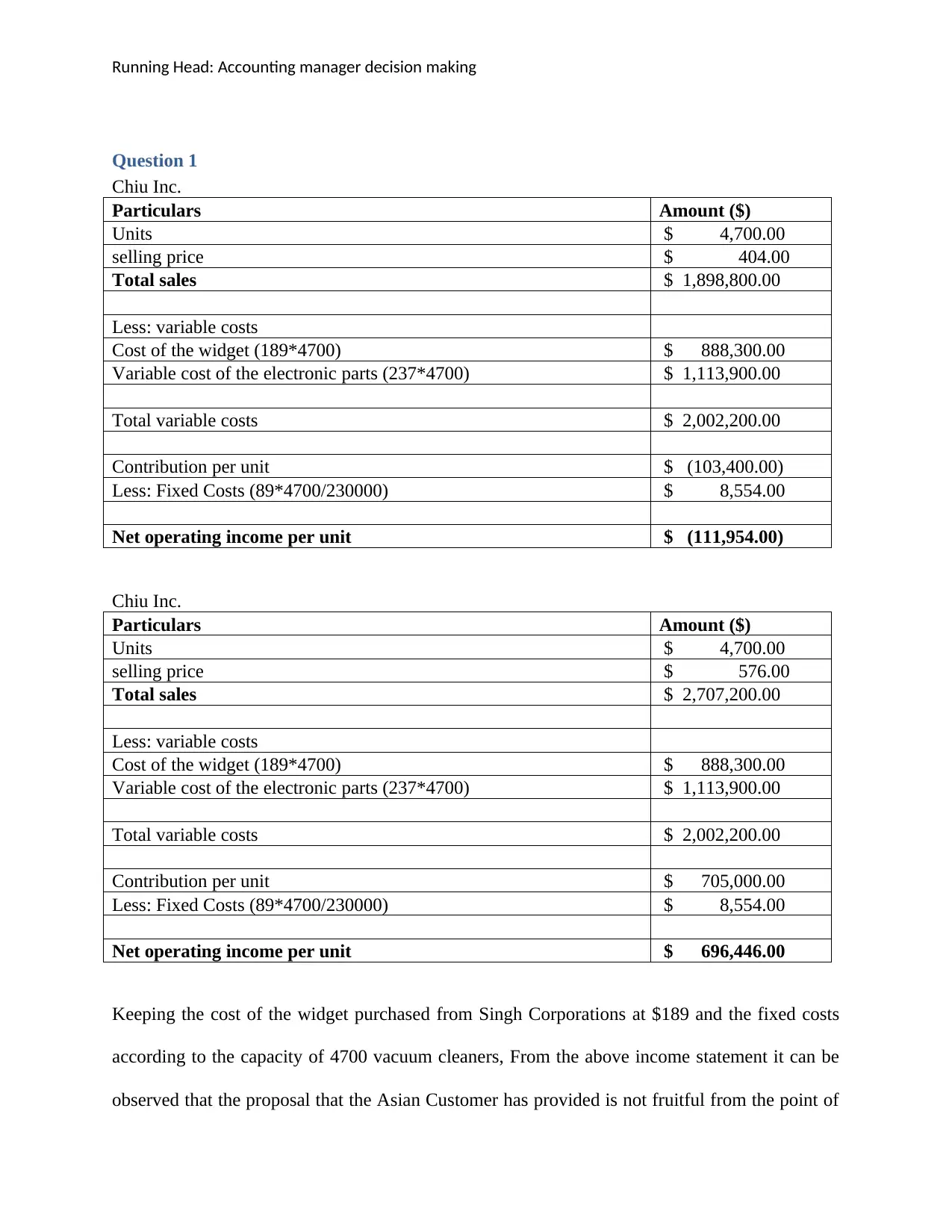

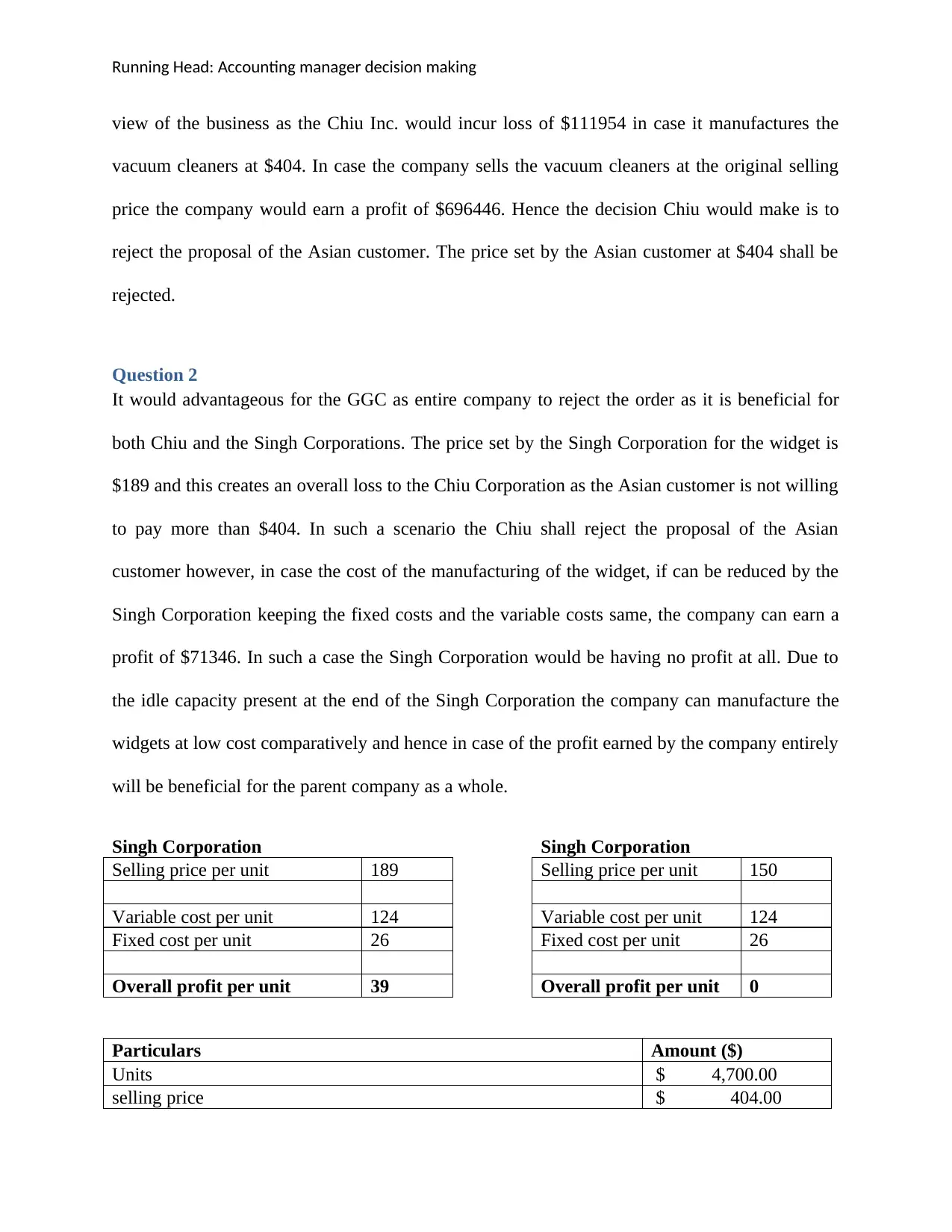

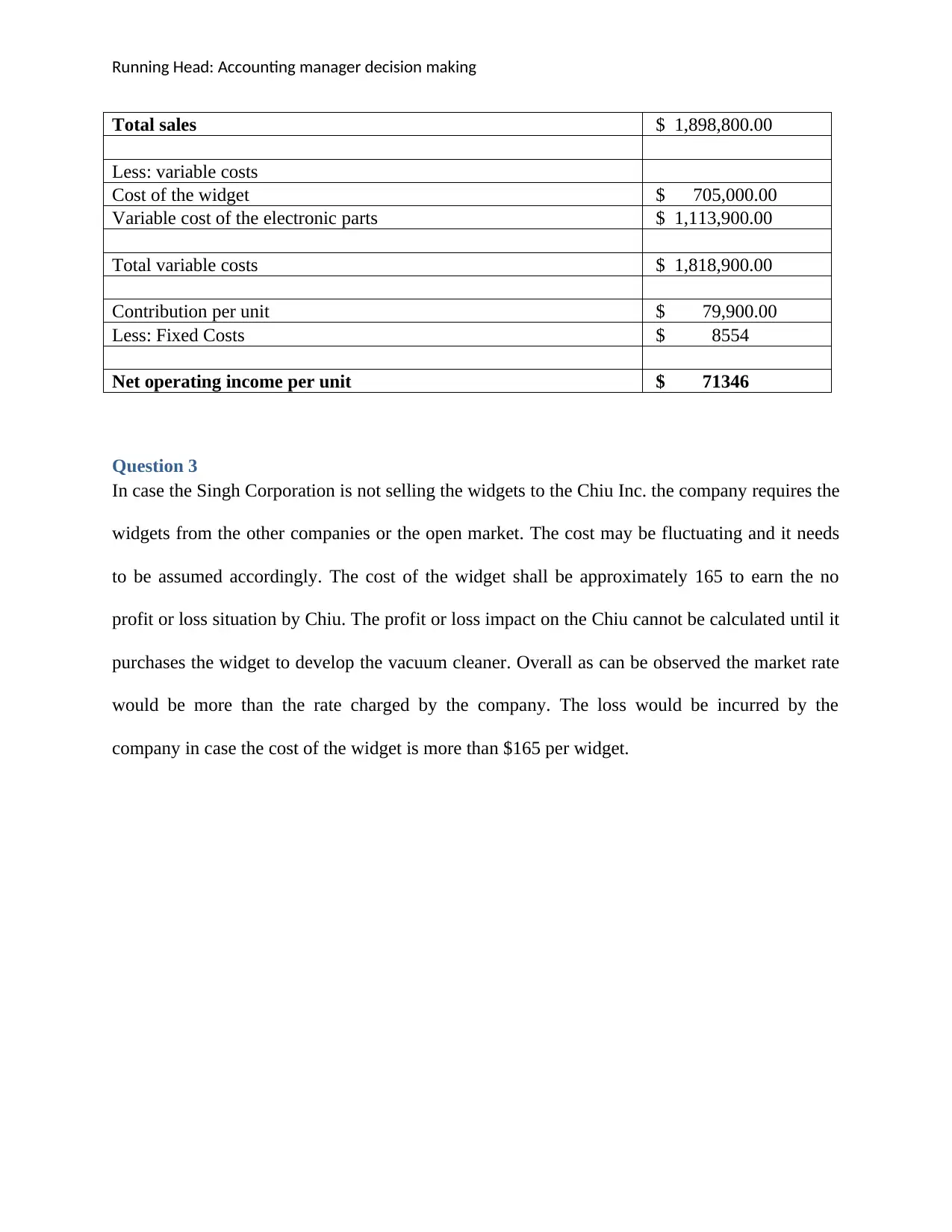

This document presents a solution to Assignment 3 for ACCT 701, focusing on transfer pricing within the Grecco Group of Companies. The assignment involves analyzing the costs and profitability of the Singh Corporation, which produces widgets used in vacuum cleaners. The solution includes an income statement analysis to determine the impact of a potential order from an Asian customer on Chiu Inc. The analysis considers variable and fixed costs, contribution margins, and net operating income to determine whether to accept or reject the customer's proposal. The solution also addresses the benefits of rejecting the order for both Chiu Inc. and the Singh Corporation, and explores the impact of varying widget costs on the company's profit or loss, considering market rates and the company's internal costs. The document provides detailed calculations and explanations to support the decision-making process related to transfer pricing and profitability.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.