Evaluating Business Strategies for Green Motor Ltd's Success

VerifiedAdded on 2020/05/04

|11

|2579

|54

AI Summary

Green Motor Ltd has experienced significant sales declines due to increased competition in the automobile parts sector. To address this challenge, the company is evaluating various financial and operational strategies. The assignment includes a detailed analysis of the company's current situation, focusing on fixed versus variable costs, pricing adjustments, profit maximization techniques, and performance measurement systems. A comprehensive review of the first half-year data reveals insights into sales patterns, profitability, and cost structures, while proposals for strategic improvements are suggested to enhance Green Motor Ltd’s market position. The study emphasizes the importance of adapting cost management strategies in response to fluctuating market dynamics and leveraging performance metrics to drive decision-making processes.

11/7/2017

Student Name

Performance Management - Green Motor Ltd

Student Name

Performance Management - Green Motor Ltd

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction......................................................................................................................................1

How the Economist’s and Accountant’s breakeven charts differ....................................................1

Economist’s breakeven chart.......................................................................................................1

Accountants Breakeven Chart......................................................................................................1

Defining period of time, relevant range and fixed cost...................................................................2

Breakeven Point and Margin of Safety of the company..................................................................2

Recommendation to the Managing Director on Selecting Proposal................................................3

Proposal analysis..........................................................................................................................4

Proposal 1.....................................................................................................................................4

Proposal 2.....................................................................................................................................4

The Better Proposal......................................................................................................................4

Conclusion.......................................................................................................................................5

Introduction......................................................................................................................................1

How the Economist’s and Accountant’s breakeven charts differ....................................................1

Economist’s breakeven chart.......................................................................................................1

Accountants Breakeven Chart......................................................................................................1

Defining period of time, relevant range and fixed cost...................................................................2

Breakeven Point and Margin of Safety of the company..................................................................2

Recommendation to the Managing Director on Selecting Proposal................................................3

Proposal analysis..........................................................................................................................4

Proposal 1.....................................................................................................................................4

Proposal 2.....................................................................................................................................4

The Better Proposal......................................................................................................................4

Conclusion.......................................................................................................................................5

Introduction

It is critical for any new business to undertake a performance management evaluation to

determine the businesses and identify a position at which the business is likely to break even on

its investment and begin registering profits. This helps determine the number of products and

time Green Motor Ltd needs to sell before it begins registering profits. It also helps determine

how long the business will take to repay loans or capital invested into the business. This makes it

critical for any new business to evaluate performance and undertake analysis so as to secure this

data which can be used to improve the on areas of weakness (Bacal, 2012).

How the Economist’s and Accountant’s breakeven charts differ

It is important to understand predicted economists breakeven chart differs from the accountant's

break-even charts but both must be analysed together to help deliver a clear vision linked to

breaking even analysis (Media, 2017).

Economist’s breakeven chart

The Economist’s breakeven chart is based on theoretical figures which are estimated and fixed.

These results in delivering fixed expenses on an average between the markets high and low. This

chart does not include variables and is limited to a single predictable line graph which is

consistent and flows predictably. Timelines are have fixed flexibility delivered on a variable

percentage of the predicted timeline which results in the chart being generalized and not very

accurate when compared to the practical output of the projects performance and reporting

schedule (Scarlett, 2005, p.168). This chart is usually developed as a guideline during the

business planning process but will from the accountant's break-even chart when compared after

X duration.

It is critical for any new business to undertake a performance management evaluation to

determine the businesses and identify a position at which the business is likely to break even on

its investment and begin registering profits. This helps determine the number of products and

time Green Motor Ltd needs to sell before it begins registering profits. It also helps determine

how long the business will take to repay loans or capital invested into the business. This makes it

critical for any new business to evaluate performance and undertake analysis so as to secure this

data which can be used to improve the on areas of weakness (Bacal, 2012).

How the Economist’s and Accountant’s breakeven charts differ

It is important to understand predicted economists breakeven chart differs from the accountant's

break-even charts but both must be analysed together to help deliver a clear vision linked to

breaking even analysis (Media, 2017).

Economist’s breakeven chart

The Economist’s breakeven chart is based on theoretical figures which are estimated and fixed.

These results in delivering fixed expenses on an average between the markets high and low. This

chart does not include variables and is limited to a single predictable line graph which is

consistent and flows predictably. Timelines are have fixed flexibility delivered on a variable

percentage of the predicted timeline which results in the chart being generalized and not very

accurate when compared to the practical output of the projects performance and reporting

schedule (Scarlett, 2005, p.168). This chart is usually developed as a guideline during the

business planning process but will from the accountant's break-even chart when compared after

X duration.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

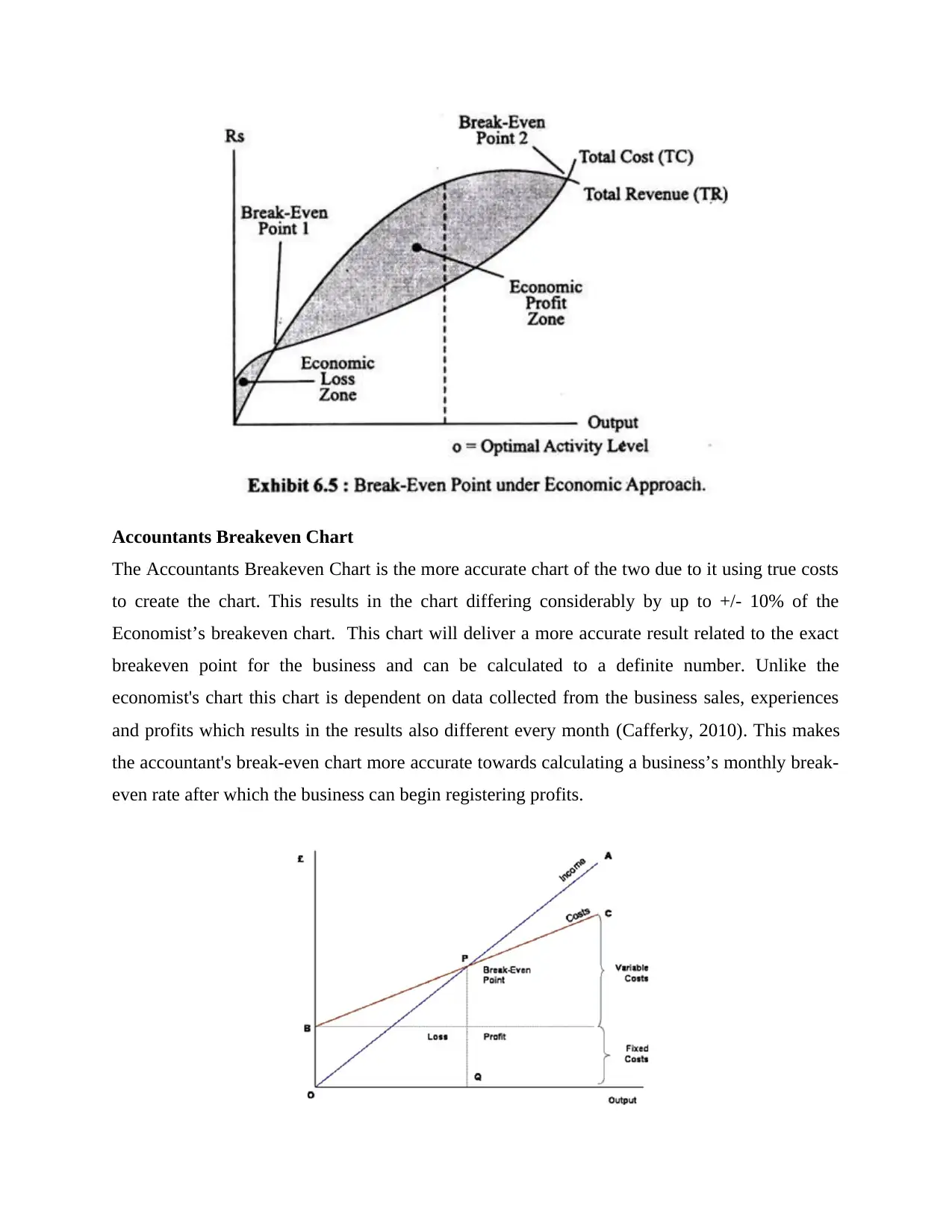

Accountants Breakeven Chart

The Accountants Breakeven Chart is the more accurate chart of the two due to it using true costs

to create the chart. This results in the chart differing considerably by up to +/- 10% of the

Economist’s breakeven chart. This chart will deliver a more accurate result related to the exact

breakeven point for the business and can be calculated to a definite number. Unlike the

economist's chart this chart is dependent on data collected from the business sales, experiences

and profits which results in the results also different every month (Cafferky, 2010). This makes

the accountant's break-even chart more accurate towards calculating a business’s monthly break-

even rate after which the business can begin registering profits.

The Accountants Breakeven Chart is the more accurate chart of the two due to it using true costs

to create the chart. This results in the chart differing considerably by up to +/- 10% of the

Economist’s breakeven chart. This chart will deliver a more accurate result related to the exact

breakeven point for the business and can be calculated to a definite number. Unlike the

economist's chart this chart is dependent on data collected from the business sales, experiences

and profits which results in the results also different every month (Cafferky, 2010). This makes

the accountant's break-even chart more accurate towards calculating a business’s monthly break-

even rate after which the business can begin registering profits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Both charts differ considerably due to one's dependency on projected statistics while the other is

uses practical expenses but both charts must be used alongside each other as they both deliver

important statistics linked to how a business is projected to perform so as to register profits.

These analyses can also be done for individual product sales on a monthly basis or to determine

the businesses long-term breakeven point which allows the business owner to project a timeline

at which the business can be expected to repay investment or loans used as capital.

Defining period of time, relevant range, and fixed cost

Fixed cost refers to costs which remain stable and predictable over a fixed period of time. A

business does not have any fixed costs over the long term perspective but the costs can be fixed

for a period of time. The long-term fixed cost in this situation refers to costs which remain stable

for a period of 12 months or more. Costs such as Salaries, rent, loan instalments, depreciation

rates, insurance, interest all for all under fixed costs (Khan & Jain, 2013).

Fixed costs must be paid despite the businesses having registered a profit or loss thus the

business will need to dig into its profits and saving during periods which the sales targets may

not be met. The business must, therefore, plan its sales and marketing plans carefully to cater for

the lean season which attracts very low sales so as to help the business break even rather than

register a loss. It is critical for the business to measure calculate the break-even costs for both the

high and low seasons thus allowing them to determine the number of sales which must be

achieved to keep the business profitable.

The term period of the term refers to the duration of time the cost remains fixed. In most

situations, a business will enter into agreement with the stakeholders to deliver their services, be

hired or supply the business with raw materials for a fixed cost over a 12 month period. This

duration is classified as the fixed cost period of time in which a business can predict the cost it

would incur. On the other hand, in many of the same contracts or agreement, the business will

also state the amount of increment the service provider or supplier can expect on completion of

the period. The rate differs and can be calculated by considering inflation, and raw materials and

production costs. The business will in most situation state a range within which the service

provider or supplier can expect an increment which is termed as the relevant range of increment

after competition of the fixed period.

uses practical expenses but both charts must be used alongside each other as they both deliver

important statistics linked to how a business is projected to perform so as to register profits.

These analyses can also be done for individual product sales on a monthly basis or to determine

the businesses long-term breakeven point which allows the business owner to project a timeline

at which the business can be expected to repay investment or loans used as capital.

Defining period of time, relevant range, and fixed cost

Fixed cost refers to costs which remain stable and predictable over a fixed period of time. A

business does not have any fixed costs over the long term perspective but the costs can be fixed

for a period of time. The long-term fixed cost in this situation refers to costs which remain stable

for a period of 12 months or more. Costs such as Salaries, rent, loan instalments, depreciation

rates, insurance, interest all for all under fixed costs (Khan & Jain, 2013).

Fixed costs must be paid despite the businesses having registered a profit or loss thus the

business will need to dig into its profits and saving during periods which the sales targets may

not be met. The business must, therefore, plan its sales and marketing plans carefully to cater for

the lean season which attracts very low sales so as to help the business break even rather than

register a loss. It is critical for the business to measure calculate the break-even costs for both the

high and low seasons thus allowing them to determine the number of sales which must be

achieved to keep the business profitable.

The term period of the term refers to the duration of time the cost remains fixed. In most

situations, a business will enter into agreement with the stakeholders to deliver their services, be

hired or supply the business with raw materials for a fixed cost over a 12 month period. This

duration is classified as the fixed cost period of time in which a business can predict the cost it

would incur. On the other hand, in many of the same contracts or agreement, the business will

also state the amount of increment the service provider or supplier can expect on completion of

the period. The rate differs and can be calculated by considering inflation, and raw materials and

production costs. The business will in most situation state a range within which the service

provider or supplier can expect an increment which is termed as the relevant range of increment

after competition of the fixed period.

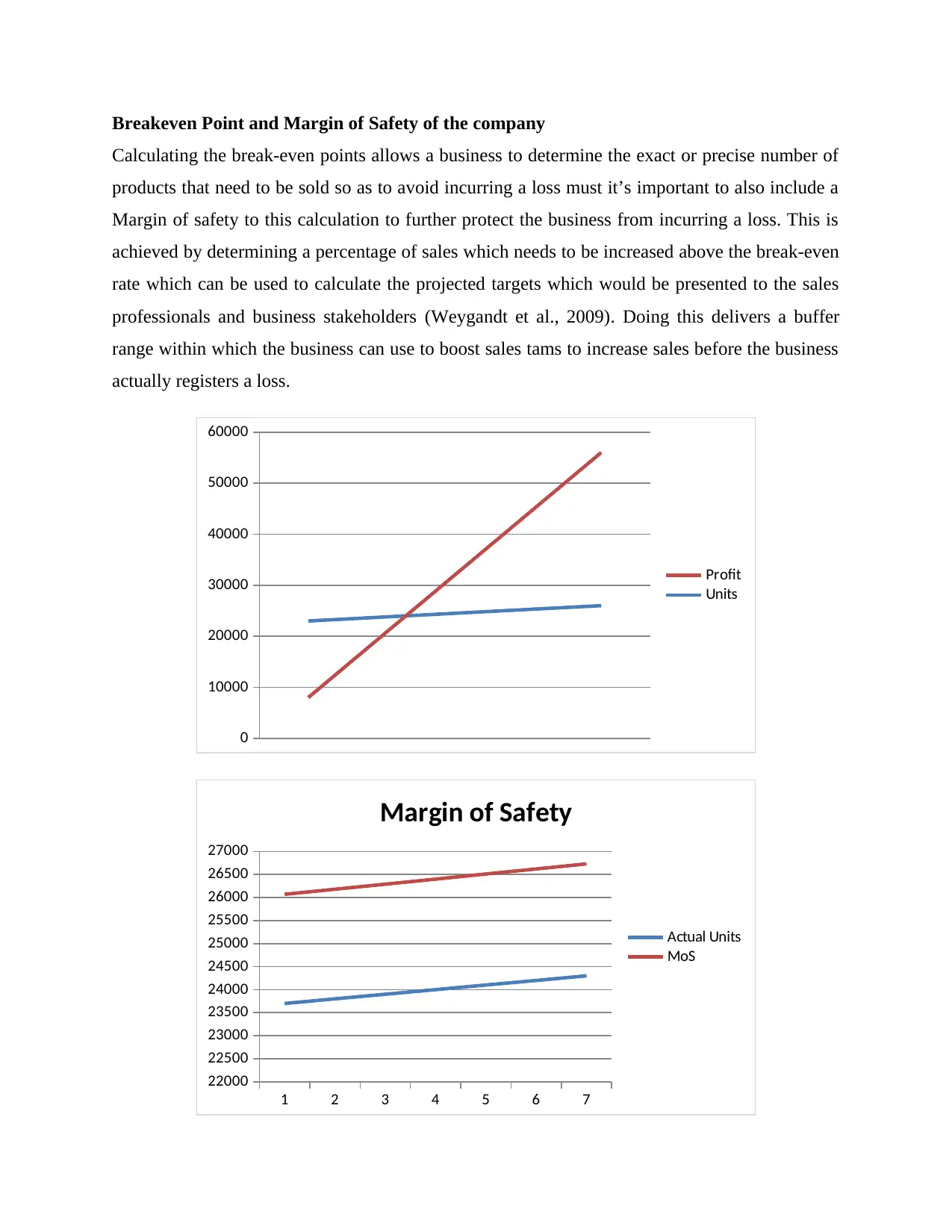

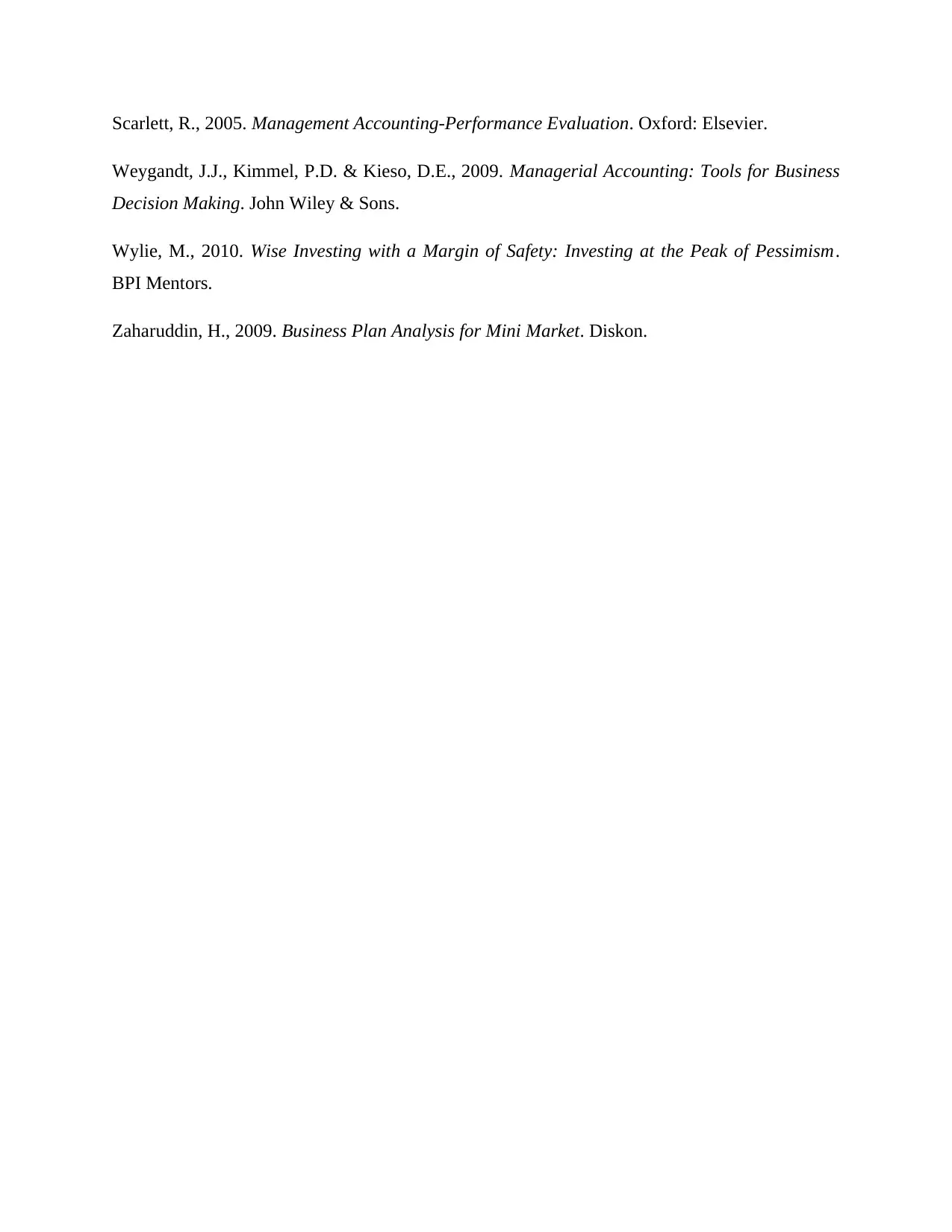

Breakeven Point and Margin of Safety of the company

Calculating the break-even points allows a business to determine the exact or precise number of

products that need to be sold so as to avoid incurring a loss must it’s important to also include a

Margin of safety to this calculation to further protect the business from incurring a loss. This is

achieved by determining a percentage of sales which needs to be increased above the break-even

rate which can be used to calculate the projected targets which would be presented to the sales

professionals and business stakeholders (Weygandt et al., 2009). Doing this delivers a buffer

range within which the business can use to boost sales tams to increase sales before the business

actually registers a loss.

0

10000

20000

30000

40000

50000

60000

Profit

Units

1 2 3 4 5 6 7

22000

22500

23000

23500

24000

24500

25000

25500

26000

26500

27000

Margin of Safety

Actual Units

MoS

Calculating the break-even points allows a business to determine the exact or precise number of

products that need to be sold so as to avoid incurring a loss must it’s important to also include a

Margin of safety to this calculation to further protect the business from incurring a loss. This is

achieved by determining a percentage of sales which needs to be increased above the break-even

rate which can be used to calculate the projected targets which would be presented to the sales

professionals and business stakeholders (Weygandt et al., 2009). Doing this delivers a buffer

range within which the business can use to boost sales tams to increase sales before the business

actually registers a loss.

0

10000

20000

30000

40000

50000

60000

Profit

Units

1 2 3 4 5 6 7

22000

22500

23000

23500

24000

24500

25000

25500

26000

26500

27000

Margin of Safety

Actual Units

MoS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This can be observed on the above Margin of safety chart where the margin of safety has been

calculated at 10% of the actual breakeven point which shows a 10% increment in the number of

sales the sales team need to target achieving on a monthly basis. The main reason for delivering a

Margin of Safety is to ensure the business sales targets remain above the actual requirement thus

helping avert losses which may occur due to the lack of meeting targets (Wylie, 2010). Having

this margin of safety also provided the business at a fixed percentage of flexibility which the

business can use make modification and changes to their marketing strategy before the business

begins registering actual losses. The margin of safety can be calculated on any range of the

business sales and profits thus delivers additional flexibility linked to the business's performance.

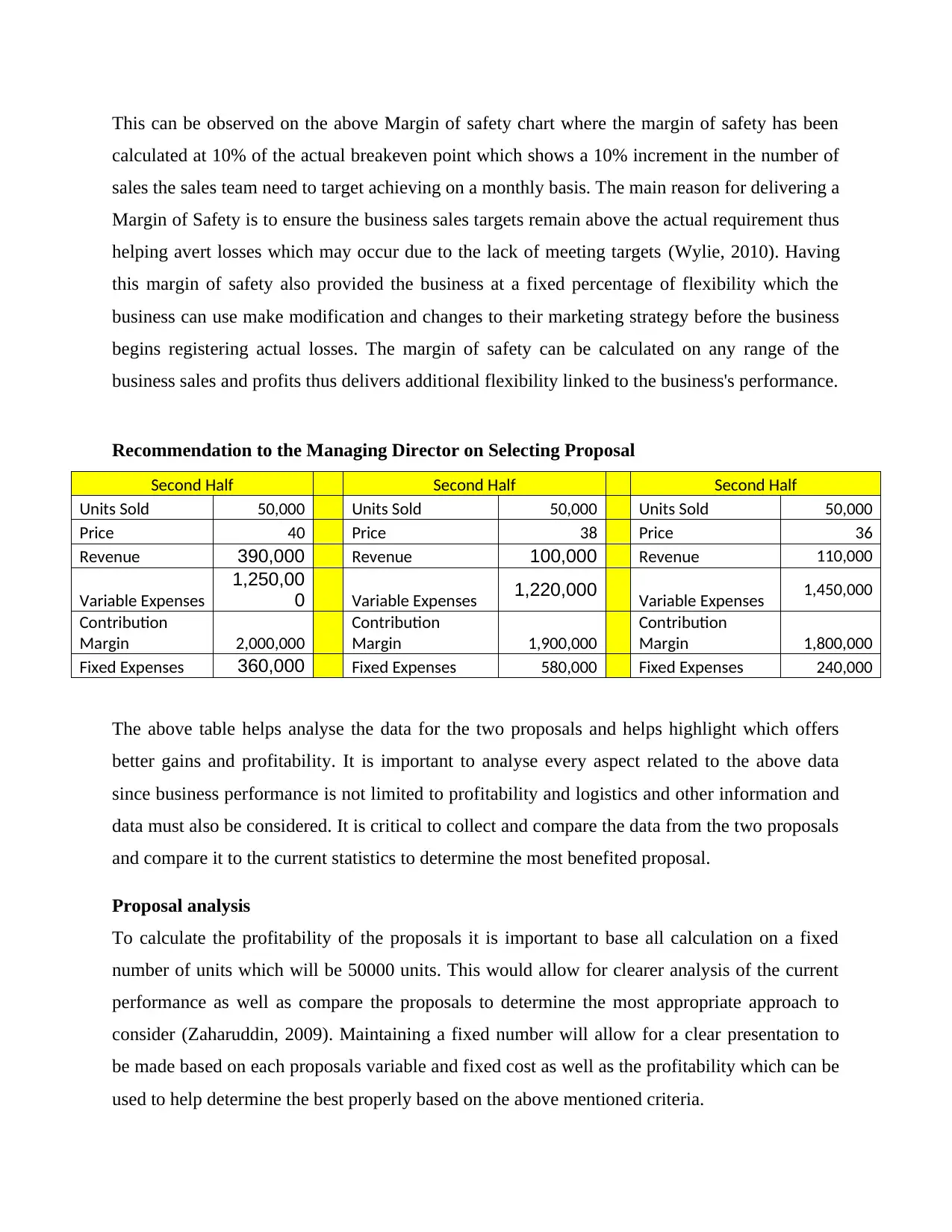

Recommendation to the Managing Director on Selecting Proposal

Second Half Second Half Second Half

Units Sold 50,000 Units Sold 50,000 Units Sold 50,000

Price 40 Price 38 Price 36

Revenue 390,000 Revenue 100,000 Revenue 110,000

Variable Expenses

1,250,00

0 Variable Expenses 1,220,000 Variable Expenses 1,450,000

Contribution

Margin 2,000,000

Contribution

Margin 1,900,000

Contribution

Margin 1,800,000

Fixed Expenses 360,000 Fixed Expenses 580,000 Fixed Expenses 240,000

The above table helps analyse the data for the two proposals and helps highlight which offers

better gains and profitability. It is important to analyse every aspect related to the above data

since business performance is not limited to profitability and logistics and other information and

data must also be considered. It is critical to collect and compare the data from the two proposals

and compare it to the current statistics to determine the most benefited proposal.

Proposal analysis

To calculate the profitability of the proposals it is important to base all calculation on a fixed

number of units which will be 50000 units. This would allow for clearer analysis of the current

performance as well as compare the proposals to determine the most appropriate approach to

consider (Zaharuddin, 2009). Maintaining a fixed number will allow for a clear presentation to

be made based on each proposals variable and fixed cost as well as the profitability which can be

used to help determine the best properly based on the above mentioned criteria.

calculated at 10% of the actual breakeven point which shows a 10% increment in the number of

sales the sales team need to target achieving on a monthly basis. The main reason for delivering a

Margin of Safety is to ensure the business sales targets remain above the actual requirement thus

helping avert losses which may occur due to the lack of meeting targets (Wylie, 2010). Having

this margin of safety also provided the business at a fixed percentage of flexibility which the

business can use make modification and changes to their marketing strategy before the business

begins registering actual losses. The margin of safety can be calculated on any range of the

business sales and profits thus delivers additional flexibility linked to the business's performance.

Recommendation to the Managing Director on Selecting Proposal

Second Half Second Half Second Half

Units Sold 50,000 Units Sold 50,000 Units Sold 50,000

Price 40 Price 38 Price 36

Revenue 390,000 Revenue 100,000 Revenue 110,000

Variable Expenses

1,250,00

0 Variable Expenses 1,220,000 Variable Expenses 1,450,000

Contribution

Margin 2,000,000

Contribution

Margin 1,900,000

Contribution

Margin 1,800,000

Fixed Expenses 360,000 Fixed Expenses 580,000 Fixed Expenses 240,000

The above table helps analyse the data for the two proposals and helps highlight which offers

better gains and profitability. It is important to analyse every aspect related to the above data

since business performance is not limited to profitability and logistics and other information and

data must also be considered. It is critical to collect and compare the data from the two proposals

and compare it to the current statistics to determine the most benefited proposal.

Proposal analysis

To calculate the profitability of the proposals it is important to base all calculation on a fixed

number of units which will be 50000 units. This would allow for clearer analysis of the current

performance as well as compare the proposals to determine the most appropriate approach to

consider (Zaharuddin, 2009). Maintaining a fixed number will allow for a clear presentation to

be made based on each proposals variable and fixed cost as well as the profitability which can be

used to help determine the best properly based on the above mentioned criteria.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

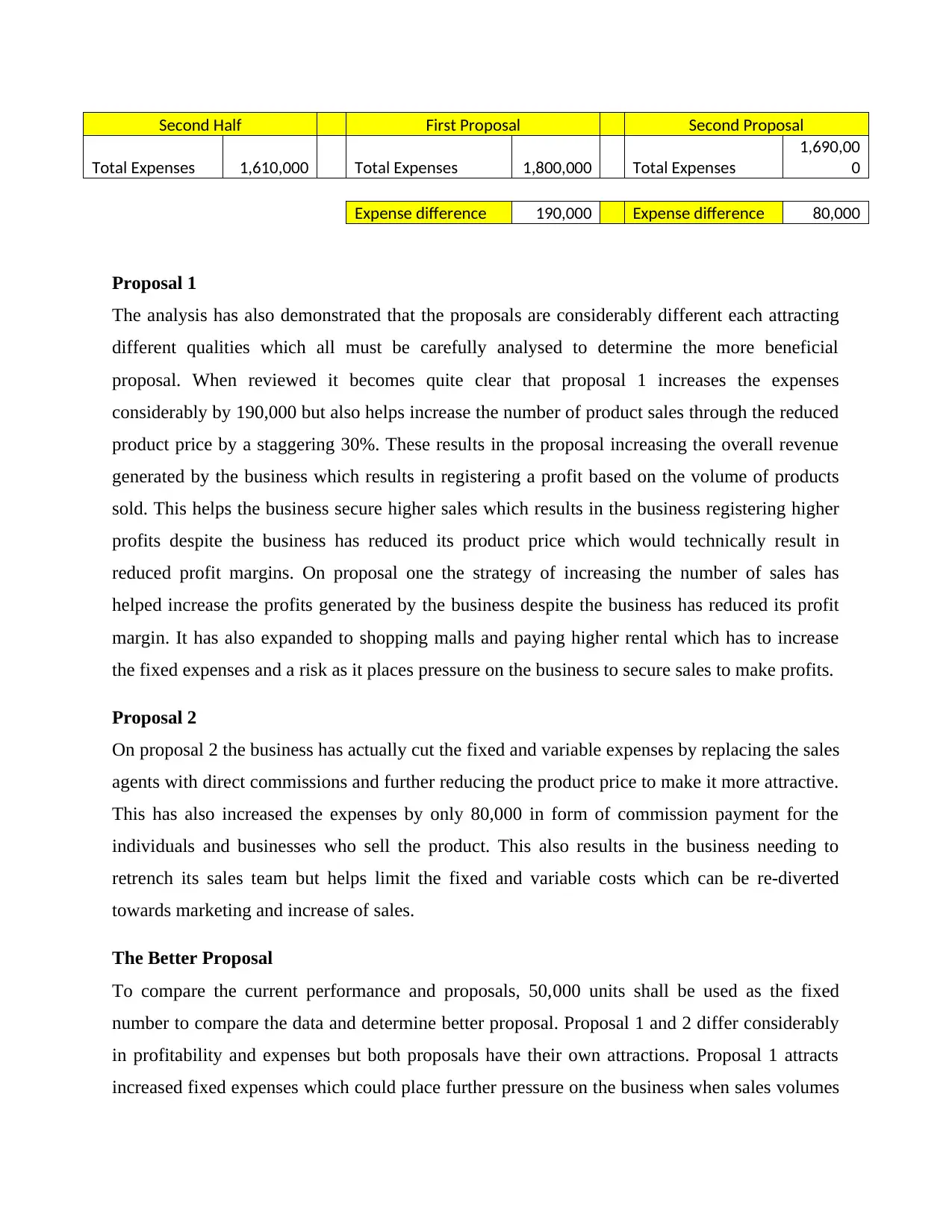

Second Half First Proposal Second Proposal

Total Expenses 1,610,000 Total Expenses 1,800,000 Total Expenses

1,690,00

0

Expense difference 190,000 Expense difference 80,000

Proposal 1

The analysis has also demonstrated that the proposals are considerably different each attracting

different qualities which all must be carefully analysed to determine the more beneficial

proposal. When reviewed it becomes quite clear that proposal 1 increases the expenses

considerably by 190,000 but also helps increase the number of product sales through the reduced

product price by a staggering 30%. These results in the proposal increasing the overall revenue

generated by the business which results in registering a profit based on the volume of products

sold. This helps the business secure higher sales which results in the business registering higher

profits despite the business has reduced its product price which would technically result in

reduced profit margins. On proposal one the strategy of increasing the number of sales has

helped increase the profits generated by the business despite the business has reduced its profit

margin. It has also expanded to shopping malls and paying higher rental which has to increase

the fixed expenses and a risk as it places pressure on the business to secure sales to make profits.

Proposal 2

On proposal 2 the business has actually cut the fixed and variable expenses by replacing the sales

agents with direct commissions and further reducing the product price to make it more attractive.

This has also increased the expenses by only 80,000 in form of commission payment for the

individuals and businesses who sell the product. This also results in the business needing to

retrench its sales team but helps limit the fixed and variable costs which can be re-diverted

towards marketing and increase of sales.

The Better Proposal

To compare the current performance and proposals, 50,000 units shall be used as the fixed

number to compare the data and determine better proposal. Proposal 1 and 2 differ considerably

in profitability and expenses but both proposals have their own attractions. Proposal 1 attracts

increased fixed expenses which could place further pressure on the business when sales volumes

Total Expenses 1,610,000 Total Expenses 1,800,000 Total Expenses

1,690,00

0

Expense difference 190,000 Expense difference 80,000

Proposal 1

The analysis has also demonstrated that the proposals are considerably different each attracting

different qualities which all must be carefully analysed to determine the more beneficial

proposal. When reviewed it becomes quite clear that proposal 1 increases the expenses

considerably by 190,000 but also helps increase the number of product sales through the reduced

product price by a staggering 30%. These results in the proposal increasing the overall revenue

generated by the business which results in registering a profit based on the volume of products

sold. This helps the business secure higher sales which results in the business registering higher

profits despite the business has reduced its product price which would technically result in

reduced profit margins. On proposal one the strategy of increasing the number of sales has

helped increase the profits generated by the business despite the business has reduced its profit

margin. It has also expanded to shopping malls and paying higher rental which has to increase

the fixed expenses and a risk as it places pressure on the business to secure sales to make profits.

Proposal 2

On proposal 2 the business has actually cut the fixed and variable expenses by replacing the sales

agents with direct commissions and further reducing the product price to make it more attractive.

This has also increased the expenses by only 80,000 in form of commission payment for the

individuals and businesses who sell the product. This also results in the business needing to

retrench its sales team but helps limit the fixed and variable costs which can be re-diverted

towards marketing and increase of sales.

The Better Proposal

To compare the current performance and proposals, 50,000 units shall be used as the fixed

number to compare the data and determine better proposal. Proposal 1 and 2 differ considerably

in profitability and expenses but both proposals have their own attractions. Proposal 1 attracts

increased fixed expenses which could place further pressure on the business when sales volumes

are low thus Proposal 2 seems to be the better option which delivers a fixed expanse rate based

on the sales volume. Reducing fixed expanses reduced the pressure on Green Motor Ltd in case

the business encounters an unexpected reduction in sales or competition. Maintaining

commission based expenses helps fix the costs associated to each products sale this allowing the

business to determine its expenses and limit overhead expenses. This helps relieve pressure from

the business with relation to the fixed and variable expenses and allow the business determine

the product expenses based on the sales volumes (SANT, 2012). The product price may increase

due to the commission being charged but the commission will also encourage the service

providers to sell the product which will help increase the sales volume without Green Motor Ltd

needing to invest on renting additional space and paying utility bills which all contribute towards

the businesses overall expenses.

Recommendation

Analysis of the 1st and 2nd half as well as the Proposal 1 and 2 reveals some important statistics

which can be used to improve the performance of Green Motor Ltd. With sales dropping due to

competition and the reduction is old prices minimizing fixed expenses is critical towards the

business managing its expenses. Thus it is recommended that proposal two be given priority as

this proposal helps the businesses limit overhead fixed costs. The proposal also increases the

price of the finished product due to the commissions being offered to the workshops and motor

engineers used to sell the product but this is critical towards the businesses limiting expenses. By

converting the majority of expenses to variable costs the business can limit overhead costs

incurred on a monthly basis thus allowing the businesses to manage its expenses even during

times of crisis. It also encourages the workshops, engineers and agents to sell more of the brands

products so as to secure more commissions thus helping boost the businesses overall sales.

Proposal 2 is there for the recommended choice for Green Motor Ltd to adopt as it will help limit

the expenses incurred by the businesses

Conclusion

Performance management required for a business to evaluate their previous and current

performance history so as to make a modification to their future targets. This is a critical

requirement for every business so as to retain its competitive edge which would allow the

business map its history and determines important areas which may require improvement. It also

on the sales volume. Reducing fixed expanses reduced the pressure on Green Motor Ltd in case

the business encounters an unexpected reduction in sales or competition. Maintaining

commission based expenses helps fix the costs associated to each products sale this allowing the

business to determine its expenses and limit overhead expenses. This helps relieve pressure from

the business with relation to the fixed and variable expenses and allow the business determine

the product expenses based on the sales volumes (SANT, 2012). The product price may increase

due to the commission being charged but the commission will also encourage the service

providers to sell the product which will help increase the sales volume without Green Motor Ltd

needing to invest on renting additional space and paying utility bills which all contribute towards

the businesses overall expenses.

Recommendation

Analysis of the 1st and 2nd half as well as the Proposal 1 and 2 reveals some important statistics

which can be used to improve the performance of Green Motor Ltd. With sales dropping due to

competition and the reduction is old prices minimizing fixed expenses is critical towards the

business managing its expenses. Thus it is recommended that proposal two be given priority as

this proposal helps the businesses limit overhead fixed costs. The proposal also increases the

price of the finished product due to the commissions being offered to the workshops and motor

engineers used to sell the product but this is critical towards the businesses limiting expenses. By

converting the majority of expenses to variable costs the business can limit overhead costs

incurred on a monthly basis thus allowing the businesses to manage its expenses even during

times of crisis. It also encourages the workshops, engineers and agents to sell more of the brands

products so as to secure more commissions thus helping boost the businesses overall sales.

Proposal 2 is there for the recommended choice for Green Motor Ltd to adopt as it will help limit

the expenses incurred by the businesses

Conclusion

Performance management required for a business to evaluate their previous and current

performance history so as to make a modification to their future targets. This is a critical

requirement for every business so as to retain its competitive edge which would allow the

business map its history and determines important areas which may require improvement. It also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps encourage contribution of new ideas which is critical towards the business securing new

and innovative approaches which can be used to improve the business's performance. The same

has been applied by Green Motor Ltd which experiences a major fluctuation in its sales volume

and profits thus allowing the business analysis important strategies it can adapt to improve its

performance, sales, and market position.

References:

Bacal, R., 2012. Performance Management 2/E. 2nd ed. McGraw Hill Professional.

Cafferky, M., 2010. Breakeven Analysis: The Definitive Guide to Cost-Volume-Profit Analysis.

New York: Business Expert Press.

Khan, M.Y. & Jain, P.K., 2013. Management Accounting : Text, Problems and Cases. Tata

McGraw-Hill Education.

Media, B.L., 2017. ACCA F5 Performance Management. Singapore: BPP Learning Media.

SANT, T., 2012. Persuasive Business Proposals: Writing to Win More Customers, Clients, and

Contracts. 3rd ed. AMACOM Div American Mgmt Assn.

and innovative approaches which can be used to improve the business's performance. The same

has been applied by Green Motor Ltd which experiences a major fluctuation in its sales volume

and profits thus allowing the business analysis important strategies it can adapt to improve its

performance, sales, and market position.

References:

Bacal, R., 2012. Performance Management 2/E. 2nd ed. McGraw Hill Professional.

Cafferky, M., 2010. Breakeven Analysis: The Definitive Guide to Cost-Volume-Profit Analysis.

New York: Business Expert Press.

Khan, M.Y. & Jain, P.K., 2013. Management Accounting : Text, Problems and Cases. Tata

McGraw-Hill Education.

Media, B.L., 2017. ACCA F5 Performance Management. Singapore: BPP Learning Media.

SANT, T., 2012. Persuasive Business Proposals: Writing to Win More Customers, Clients, and

Contracts. 3rd ed. AMACOM Div American Mgmt Assn.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Scarlett, R., 2005. Management Accounting-Performance Evaluation. Oxford: Elsevier.

Weygandt, J.J., Kimmel, P.D. & Kieso, D.E., 2009. Managerial Accounting: Tools for Business

Decision Making. John Wiley & Sons.

Wylie, M., 2010. Wise Investing with a Margin of Safety: Investing at the Peak of Pessimism.

BPI Mentors.

Zaharuddin, H., 2009. Business Plan Analysis for Mini Market. Diskon.

Weygandt, J.J., Kimmel, P.D. & Kieso, D.E., 2009. Managerial Accounting: Tools for Business

Decision Making. John Wiley & Sons.

Wylie, M., 2010. Wise Investing with a Margin of Safety: Investing at the Peak of Pessimism.

BPI Mentors.

Zaharuddin, H., 2009. Business Plan Analysis for Mini Market. Diskon.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.