Griffin Ltd: Consolidated Financial Statement Analysis Report

VerifiedAdded on 2022/11/24

|9

|1585

|50

Report

AI Summary

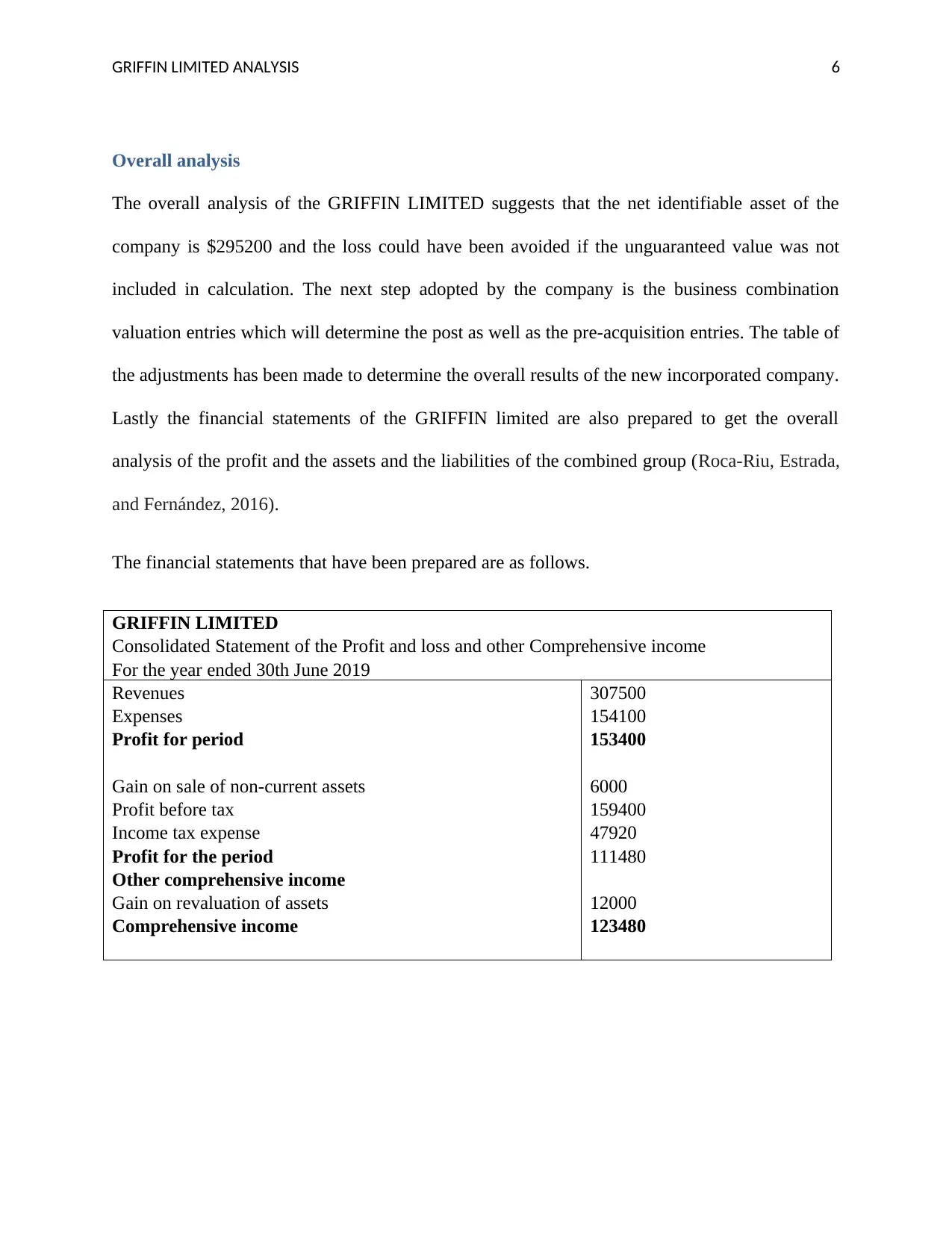

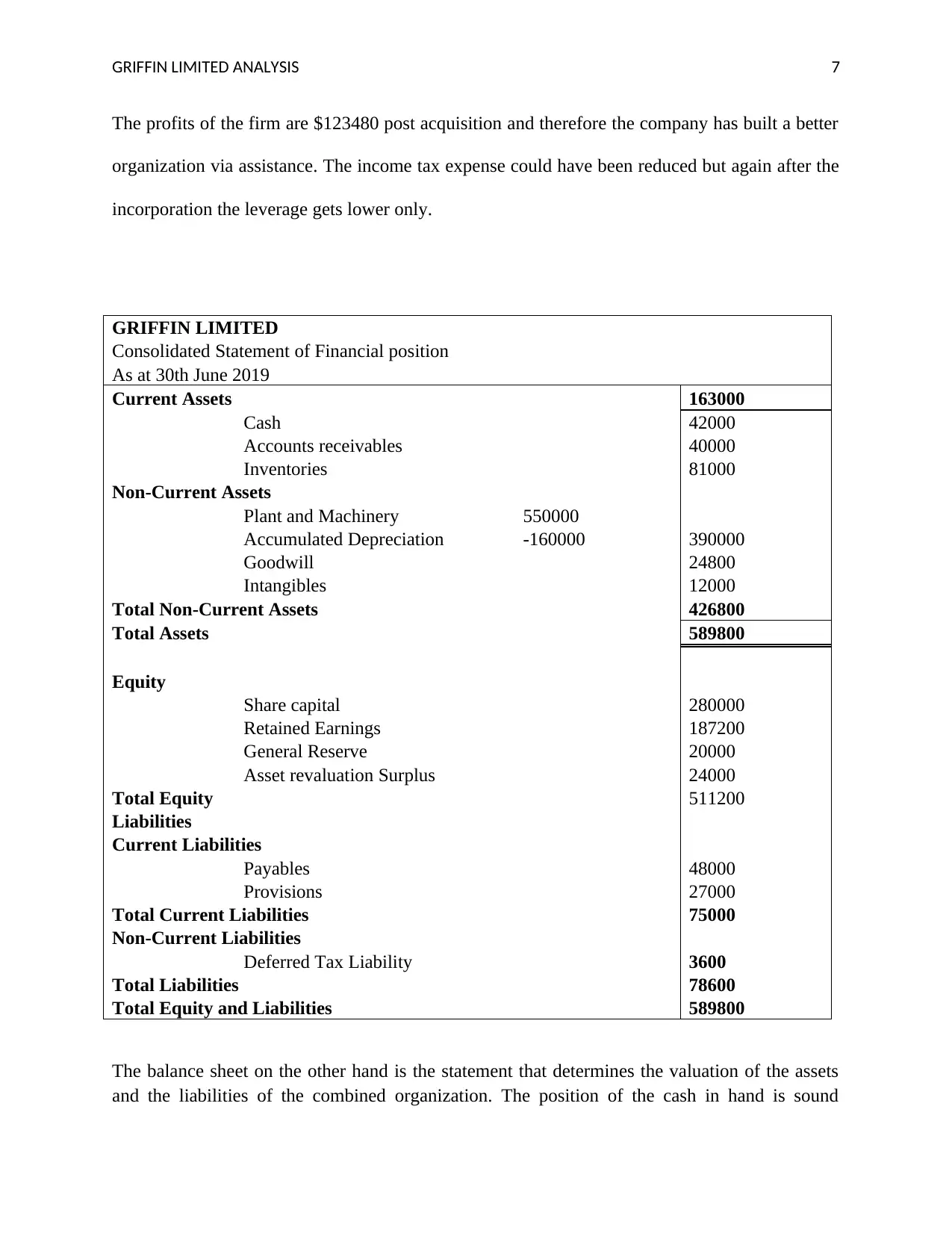

This report provides a comprehensive analysis of Griffin Ltd's acquisition of Frank Ltd, focusing on the financial implications and consolidation processes. The acquisition, completed on July 1, 2016, involved Griffin Ltd acquiring all issued shares of Frank Ltd. The report details the interpretation of the acquisition analysis, including the application of US GAAP and IFRS in preparing consolidated financial statements. It identifies the assumptions made during the consolidation process, such as the sale of land and inventory, and the valuation of assets and liabilities at fair market value. The report explores the complexities of acquisition analysis, highlighting the time-consuming nature of adjusting and integrating the financial records of both companies. It also outlines the purpose of the acquisition, emphasizing the potential for increased value, synergies, and reduced financial risk for Griffin Ltd. The overall analysis includes a calculation of the net identifiable assets and the preparation of consolidated financial statements, including the statement of profit and loss and other comprehensive income, and the consolidated statement of financial position. These statements reveal the financial performance and position of the combined group, including revenues, expenses, profit, assets, liabilities, and equity. The report concludes by highlighting the benefits of the acquisition, such as improved profitability and a stronger balance sheet for Griffin Ltd.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.