Monash Uni - BFF5300: Groupe Ariel S.A. Case Study Finance Analysis

VerifiedAdded on 2022/09/07

|13

|2337

|26

Case Study

AI Summary

This document provides a detailed solution to the Groupe Ariel S.A. case study, focusing on international corporate finance. The analysis begins by computing the Net Present Value (NPV) of Ariel-Mexico's recycling equipment in pesos and translating it into Euros, considering inflation rates. It then calculates the NPV in Euros by translating peso cash flows at expected future exchange rates, comparing the two approaches. The solution explores the impact of changes in Mexican inflation rates on NPV calculations and examines the effect of a real depreciation of the peso against the Euro on the NPV under different approaches. The document includes calculations using the International Fisher Effect and addresses the implications for investment decisions, providing a comprehensive understanding of cross-border valuation and the application of parity conditions.

INTERNATIONAL CORPORATE FINANCE

Study Case: Groupe Ariel S.A. – Parity Conditions and Cross-Border Valuation

Study Case: Groupe Ariel S.A. – Parity Conditions and Cross-Border Valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

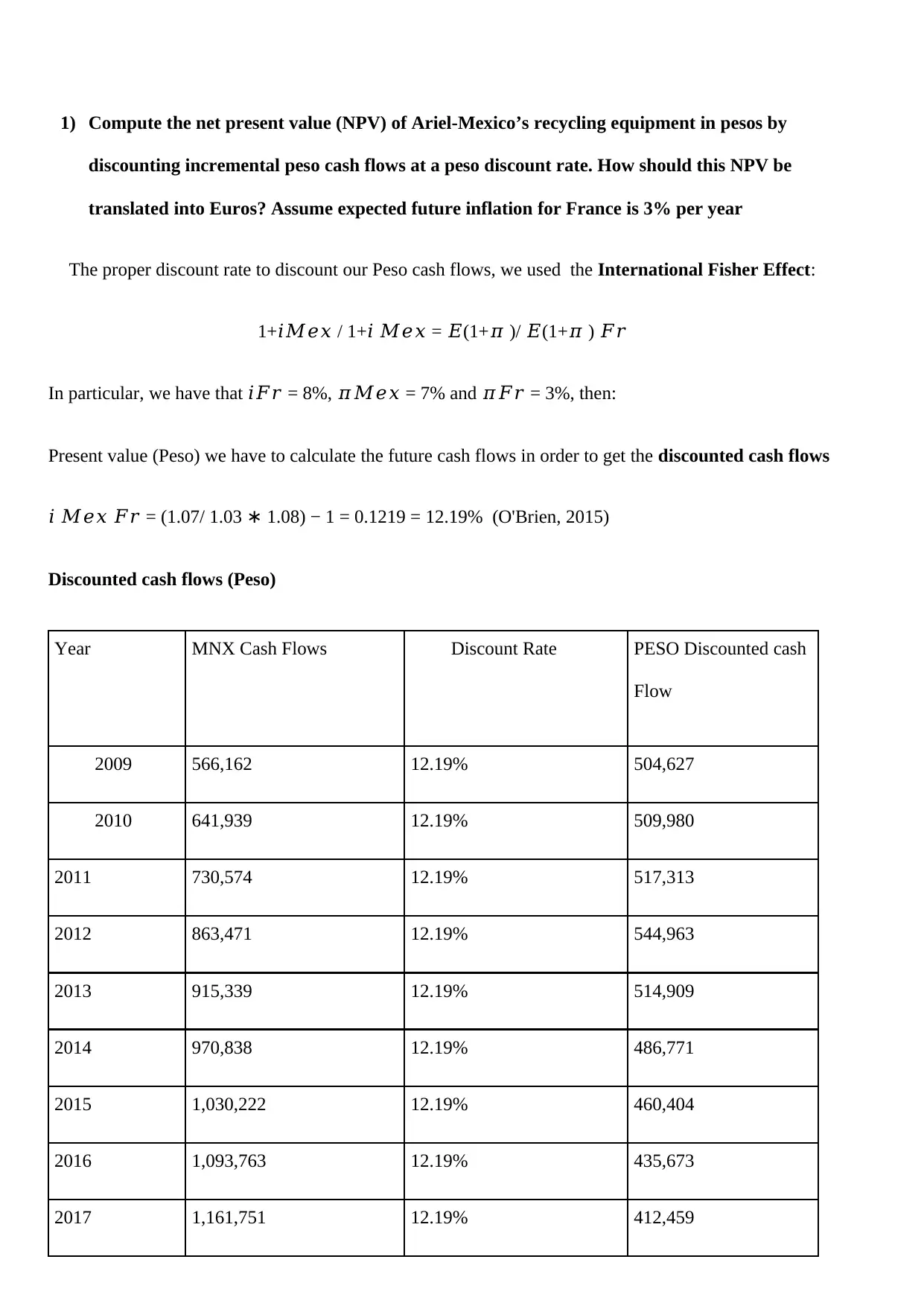

1) Compute the net present value (NPV) of Ariel-Mexico’s recycling equipment in pesos by

discounting incremental peso cash flows at a peso discount rate. How should this NPV be

translated into Euros? Assume expected future inflation for France is 3% per year

The proper discount rate to discount our Peso cash flows, we used the International Fisher Effect:

1+𝑖𝑀𝑒𝑥 / 1+𝑖 𝑀𝑒𝑥 = 𝐸(1+𝜋 )/ 𝐸(1+𝜋 ) 𝐹𝑟

In particular, we have that 𝑖𝐹𝑟 = 8%, 𝜋𝑀𝑒𝑥 = 7% and 𝜋𝐹𝑟 = 3%, then:

Present value (Peso) we have to calculate the future cash flows in order to get the discounted cash flows

𝑖 𝑀𝑒𝑥 𝐹𝑟 = (1.07/ 1.03 ∗ 1.08) − 1 = 0.1219 = 12.19% (O'Brien, 2015)

Discounted cash flows (Peso)

Year MNX Cash Flows Discount Rate PESO Discounted cash

Flow

2009 566,162 12.19% 504,627

2010 641,939 12.19% 509,980

2011 730,574 12.19% 517,313

2012 863,471 12.19% 544,963

2013 915,339 12.19% 514,909

2014 970,838 12.19% 486,771

2015 1,030,222 12.19% 460,404

2016 1,093,763 12.19% 435,673

2017 1,161,751 12.19% 412,459

discounting incremental peso cash flows at a peso discount rate. How should this NPV be

translated into Euros? Assume expected future inflation for France is 3% per year

The proper discount rate to discount our Peso cash flows, we used the International Fisher Effect:

1+𝑖𝑀𝑒𝑥 / 1+𝑖 𝑀𝑒𝑥 = 𝐸(1+𝜋 )/ 𝐸(1+𝜋 ) 𝐹𝑟

In particular, we have that 𝑖𝐹𝑟 = 8%, 𝜋𝑀𝑒𝑥 = 7% and 𝜋𝐹𝑟 = 3%, then:

Present value (Peso) we have to calculate the future cash flows in order to get the discounted cash flows

𝑖 𝑀𝑒𝑥 𝐹𝑟 = (1.07/ 1.03 ∗ 1.08) − 1 = 0.1219 = 12.19% (O'Brien, 2015)

Discounted cash flows (Peso)

Year MNX Cash Flows Discount Rate PESO Discounted cash

Flow

2009 566,162 12.19% 504,627

2010 641,939 12.19% 509,980

2011 730,574 12.19% 517,313

2012 863,471 12.19% 544,963

2013 915,339 12.19% 514,909

2014 970,838 12.19% 486,771

2015 1,030,222 12.19% 460,404

2016 1,093,763 12.19% 435,673

2017 1,161,751 12.19% 412,459

2018 1,234,499 12.19% 390,650

4,777,749

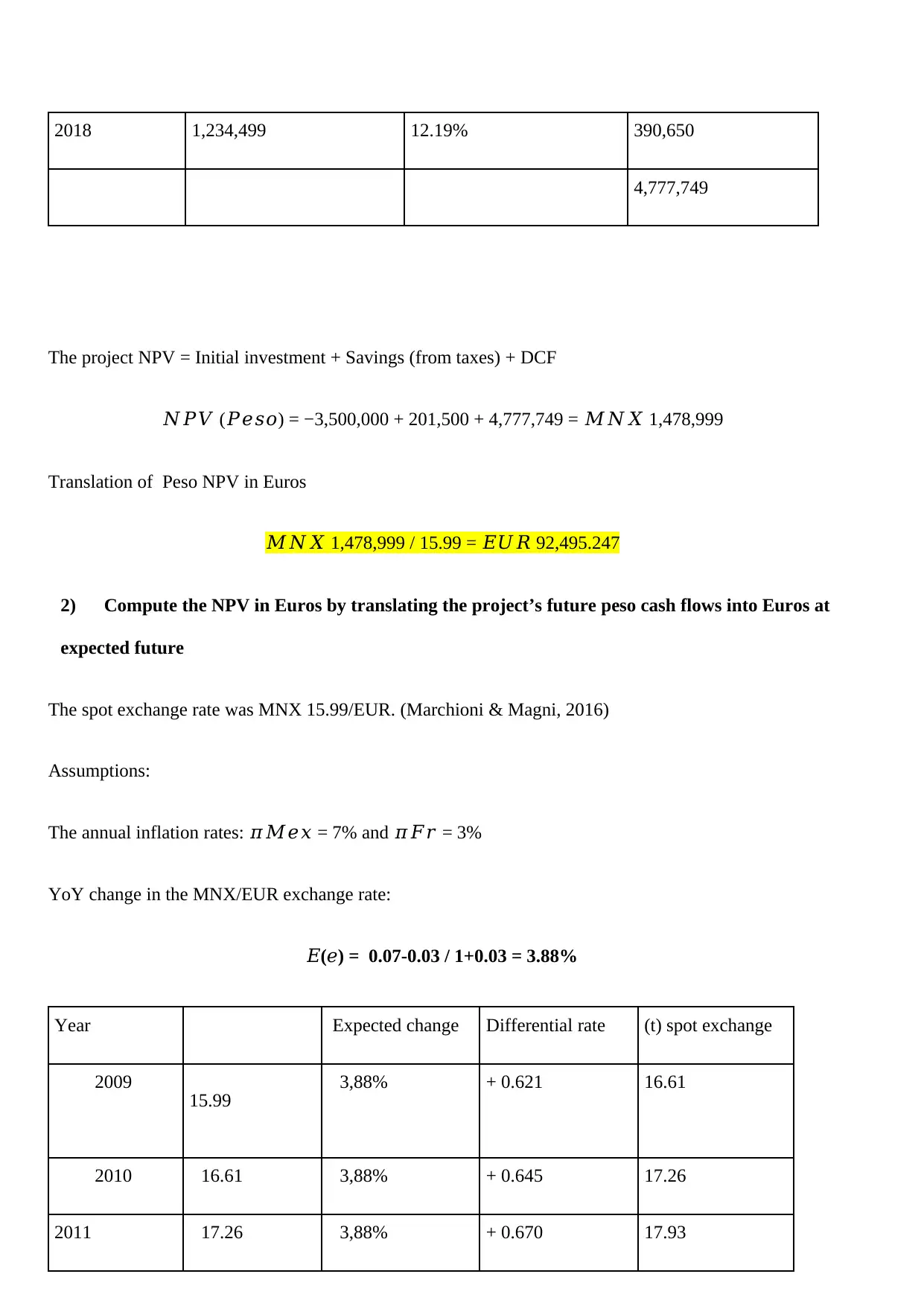

The project NPV = Initial investment + Savings (from taxes) + DCF

𝑁𝑃𝑉 (𝑃𝑒𝑠𝑜) = −3,500,000 + 201,500 + 4,777,749 = 𝑀𝑁𝑋 1,478,999

Translation of Peso NPV in Euros

𝑀𝑁𝑋 1,478,999 / 15.99 = 𝐸𝑈𝑅 92,495.247

2) Compute the NPV in Euros by translating the project’s future peso cash flows into Euros at

expected future

The spot exchange rate was MNX 15.99/EUR. (Marchioni & Magni, 2016)

Assumptions:

The annual inflation rates: 𝜋𝑀𝑒𝑥 = 7% and 𝜋𝐹𝑟 = 3%

YoY change in the MNX/EUR exchange rate:

𝐸(𝑒) = 0.07-0.03 / 1+0.03 = 3.88%

Year Expected change Differential rate (t) spot exchange

2009 15.99 3,88% + 0.621 16.61

2010 16.61 3,88% + 0.645 17.26

2011 17.26 3,88% + 0.670 17.93

4,777,749

The project NPV = Initial investment + Savings (from taxes) + DCF

𝑁𝑃𝑉 (𝑃𝑒𝑠𝑜) = −3,500,000 + 201,500 + 4,777,749 = 𝑀𝑁𝑋 1,478,999

Translation of Peso NPV in Euros

𝑀𝑁𝑋 1,478,999 / 15.99 = 𝐸𝑈𝑅 92,495.247

2) Compute the NPV in Euros by translating the project’s future peso cash flows into Euros at

expected future

The spot exchange rate was MNX 15.99/EUR. (Marchioni & Magni, 2016)

Assumptions:

The annual inflation rates: 𝜋𝑀𝑒𝑥 = 7% and 𝜋𝐹𝑟 = 3%

YoY change in the MNX/EUR exchange rate:

𝐸(𝑒) = 0.07-0.03 / 1+0.03 = 3.88%

Year Expected change Differential rate (t) spot exchange

2009 15.99 3,88% + 0.621 16.61

2010 16.61 3,88% + 0.645 17.26

2011 17.26 3,88% + 0.670 17.93

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2012 17.93 3,88% + 0.696 18.62

2013 18.62 3,88% +0.723 19.35

2014 19.35 3,88% + 0.751 20.10

2015 20.10 3,88% + 0.780 20.88

2016 20.88 3,88% + 0.811 21.69

2017 21.69 3,88% +0.842 22.53

2018 22.52 3,88% +0.875 23.41

EURO cash flows with the required rate 8%

Yea

r

MNX Expected EUR Cash

Flows

Discount EUR

Discounted

Cashflows Exchange Rate Cashflows

Rate

2009 566,162 16.61 34,083.63 8% 31,558.9166

2010 641,939 17.26 37,200.8 8% 31,893.6926

2011 730,574 17.93 40,754.58 8% 32,352.2962

2012 863,471 18.62 46,367.46 8% 34,081.4654

2013 915,339 19.35 47,315.23 8% 32,201.9502

2014 970,838 20.10 48,308.01 8% 30,442.2418

2013 18.62 3,88% +0.723 19.35

2014 19.35 3,88% + 0.751 20.10

2015 20.10 3,88% + 0.780 20.88

2016 20.88 3,88% + 0.811 21.69

2017 21.69 3,88% +0.842 22.53

2018 22.52 3,88% +0.875 23.41

EURO cash flows with the required rate 8%

Yea

r

MNX Expected EUR Cash

Flows

Discount EUR

Discounted

Cashflows Exchange Rate Cashflows

Rate

2009 566,162 16.61 34,083.63 8% 31,558.9166

2010 641,939 17.26 37,200.8 8% 31,893.6926

2011 730,574 17.93 40,754.58 8% 32,352.2962

2012 863,471 18.62 46,367.46 8% 34,081.4654

2013 915,339 19.35 47,315.23 8% 32,201.9502

2014 970,838 20.10 48,308.01 8% 30,442.2418

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

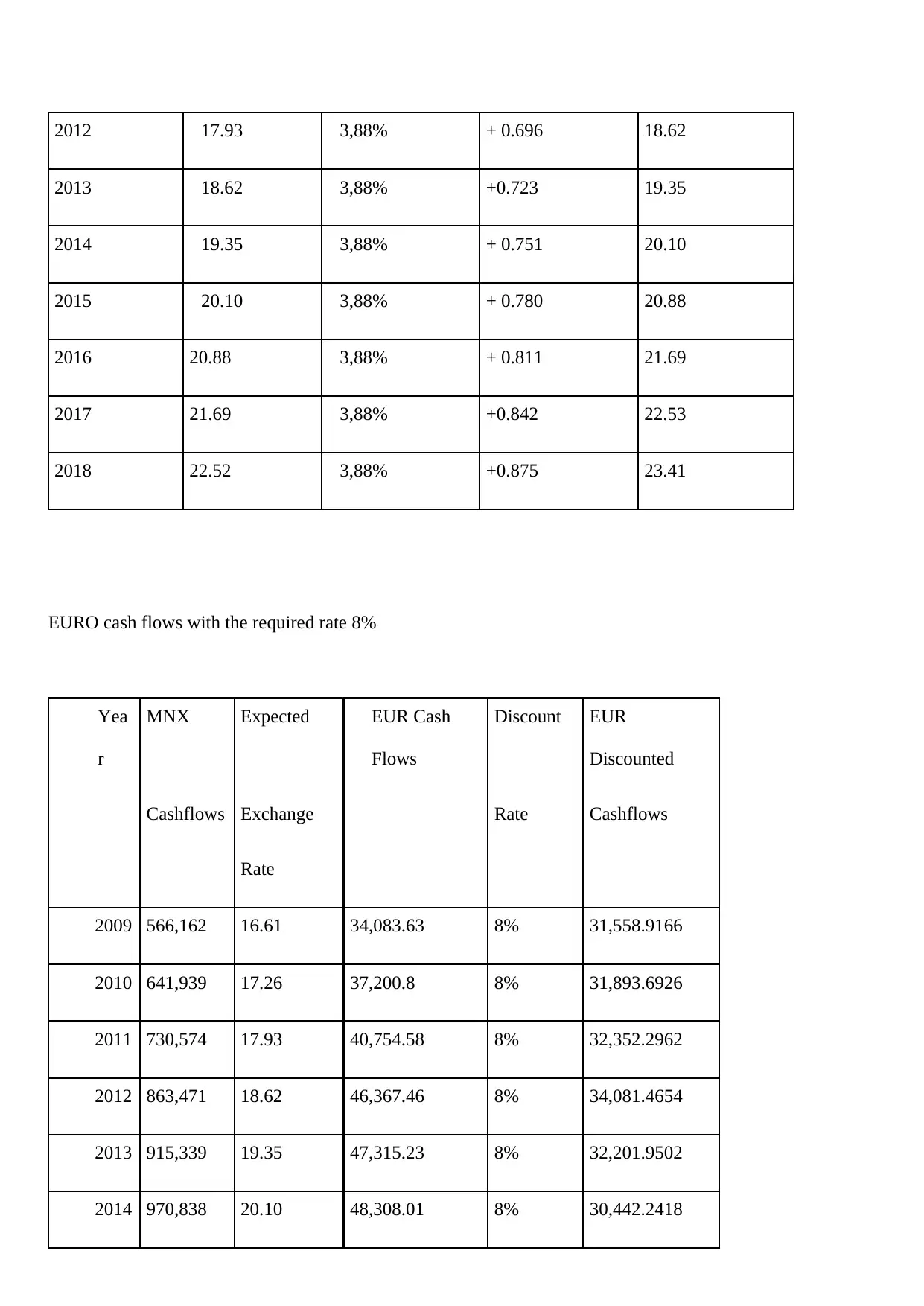

2015 1,030,222 20.88 49,346.53 8% 28,793.2286

2016 1,093,763 21.69 50,431.56 8% 27,246.6025

2017 1,161,751 22.53 51,563.89 8% 25,794.7837

2018 1,234,499 23.41 52,744.43 8% 24,430.8758

298,796

.05

("Euro Depreciation and Its Impact on Trade with the US - Market Realist", 2020)

The initial cost of the project = EUR 220,000.

The Exchange rate is 15.99 MNX/EUR

The initial cost of the project EUR 218,887.80.

The value of Savings (from taxes) is now:

MNX 201,250 / 15.99 = EUR 12,585.9912

3) Compare the two sets of study calculations and the corresponding NPVs. Do they differ?

Why? Which approach should Arnaud Martin use?

Results from the two counts are the equivalent. This is because the two methodologies join

indistinguishable suspicions about interest rates and inflation rates. ("Ariel | Team & Leadership

Training", 2020) This implies if the IRP, PPP and the International Fisher Effect hold, Arnaud Martin

will be detached in picking which is the best way to deal with use to play out his DCF investigation.

(Jacobs, 2014)

4) Suppose Mexican inflation is projected at 3% instead of 7% per year (assume French inflation

remains at 3%). How does this affect NPV calculations?

A) For the case of NPV in pesos

2016 1,093,763 21.69 50,431.56 8% 27,246.6025

2017 1,161,751 22.53 51,563.89 8% 25,794.7837

2018 1,234,499 23.41 52,744.43 8% 24,430.8758

298,796

.05

("Euro Depreciation and Its Impact on Trade with the US - Market Realist", 2020)

The initial cost of the project = EUR 220,000.

The Exchange rate is 15.99 MNX/EUR

The initial cost of the project EUR 218,887.80.

The value of Savings (from taxes) is now:

MNX 201,250 / 15.99 = EUR 12,585.9912

3) Compare the two sets of study calculations and the corresponding NPVs. Do they differ?

Why? Which approach should Arnaud Martin use?

Results from the two counts are the equivalent. This is because the two methodologies join

indistinguishable suspicions about interest rates and inflation rates. ("Ariel | Team & Leadership

Training", 2020) This implies if the IRP, PPP and the International Fisher Effect hold, Arnaud Martin

will be detached in picking which is the best way to deal with use to play out his DCF investigation.

(Jacobs, 2014)

4) Suppose Mexican inflation is projected at 3% instead of 7% per year (assume French inflation

remains at 3%). How does this affect NPV calculations?

A) For the case of NPV in pesos

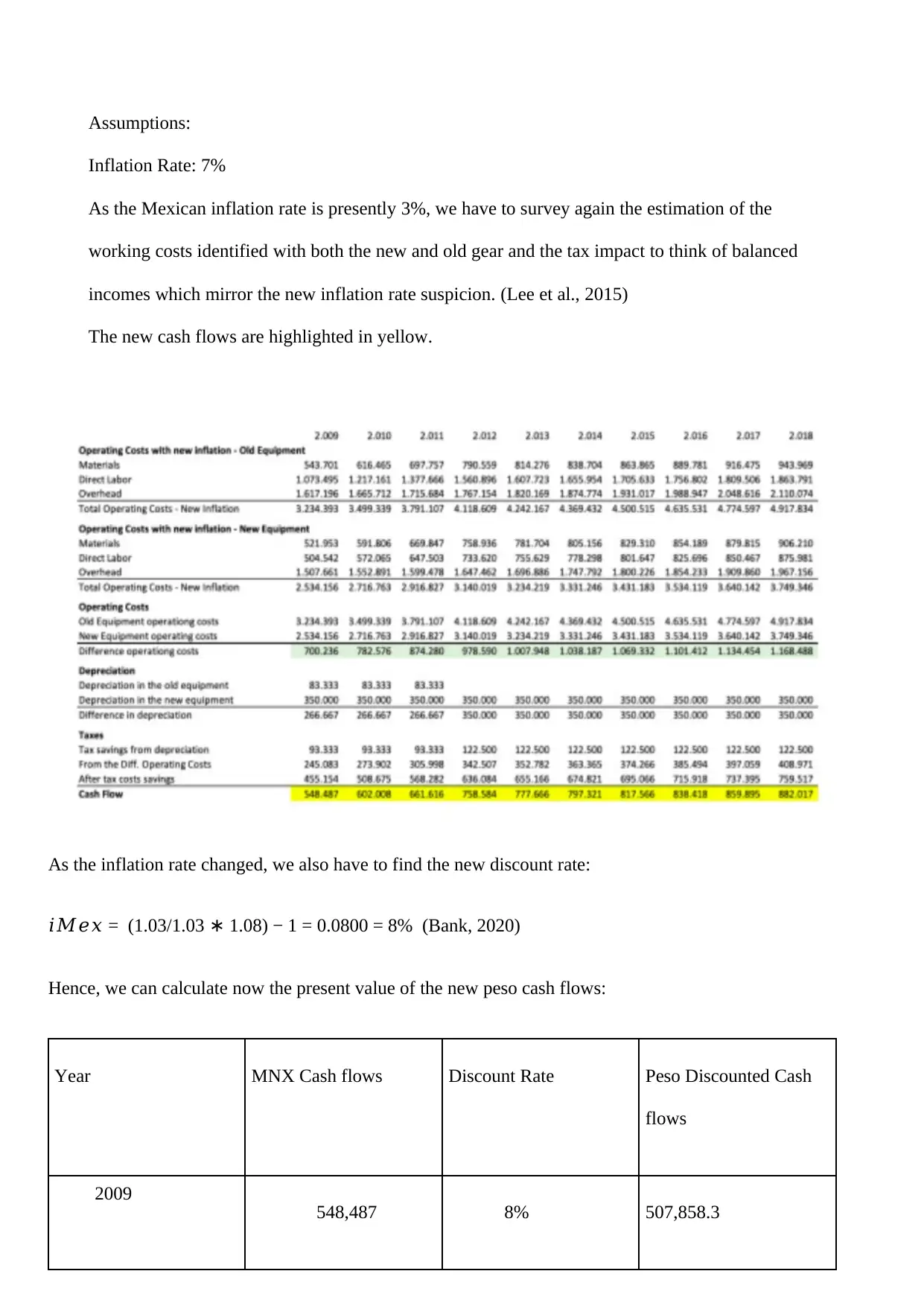

Assumptions:

Inflation Rate: 7%

As the Mexican inflation rate is presently 3%, we have to survey again the estimation of the

working costs identified with both the new and old gear and the tax impact to think of balanced

incomes which mirror the new inflation rate suspicion. (Lee et al., 2015)

The new cash flows are highlighted in yellow.

As the inflation rate changed, we also have to find the new discount rate:

𝑖𝑀𝑒𝑥 = (1.03/1.03 ∗ 1.08) − 1 = 0.0800 = 8% (Bank, 2020)

Hence, we can calculate now the present value of the new peso cash flows:

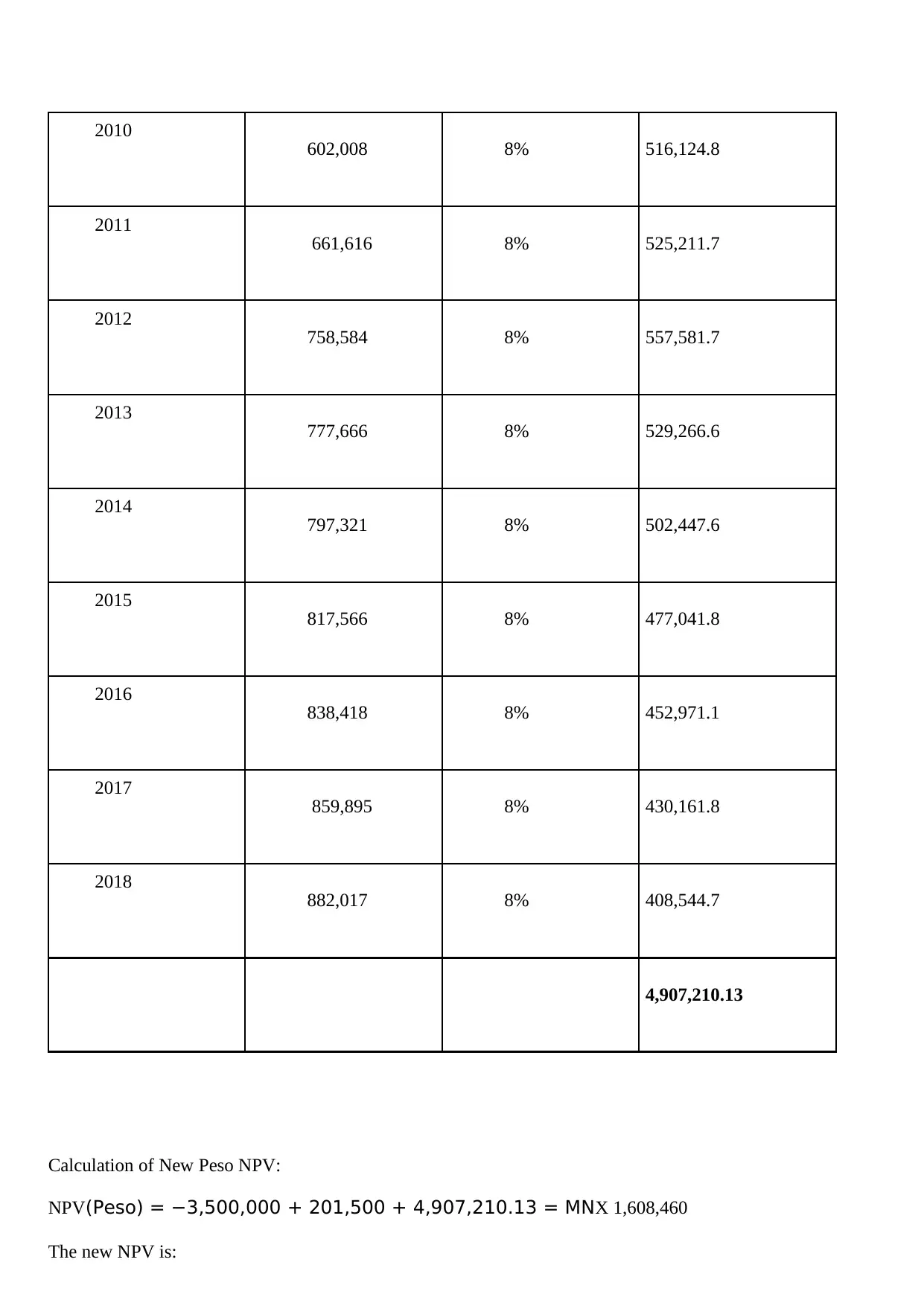

Year MNX Cash flows Discount Rate Peso Discounted Cash

flows

2009 548,487 8% 507,858.3

Inflation Rate: 7%

As the Mexican inflation rate is presently 3%, we have to survey again the estimation of the

working costs identified with both the new and old gear and the tax impact to think of balanced

incomes which mirror the new inflation rate suspicion. (Lee et al., 2015)

The new cash flows are highlighted in yellow.

As the inflation rate changed, we also have to find the new discount rate:

𝑖𝑀𝑒𝑥 = (1.03/1.03 ∗ 1.08) − 1 = 0.0800 = 8% (Bank, 2020)

Hence, we can calculate now the present value of the new peso cash flows:

Year MNX Cash flows Discount Rate Peso Discounted Cash

flows

2009 548,487 8% 507,858.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2010 602,008 8% 516,124.8

2011 661,616 8% 525,211.7

2012 758,584 8% 557,581.7

2013 777,666 8% 529,266.6

2014 797,321 8% 502,447.6

2015 817,566 8% 477,041.8

2016 838,418 8% 452,971.1

2017 859,895 8% 430,161.8

2018 882,017 8% 408,544.7

4,907,210.13

Calculation of New Peso NPV:

NPV(Peso) = −3,500,000 + 201,500 + 4,907,210.13 = MNX 1,608,460

The new NPV is:

2011 661,616 8% 525,211.7

2012 758,584 8% 557,581.7

2013 777,666 8% 529,266.6

2014 797,321 8% 502,447.6

2015 817,566 8% 477,041.8

2016 838,418 8% 452,971.1

2017 859,895 8% 430,161.8

2018 882,017 8% 408,544.7

4,907,210.13

Calculation of New Peso NPV:

NPV(Peso) = −3,500,000 + 201,500 + 4,907,210.13 = MNX 1,608,460

The new NPV is:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

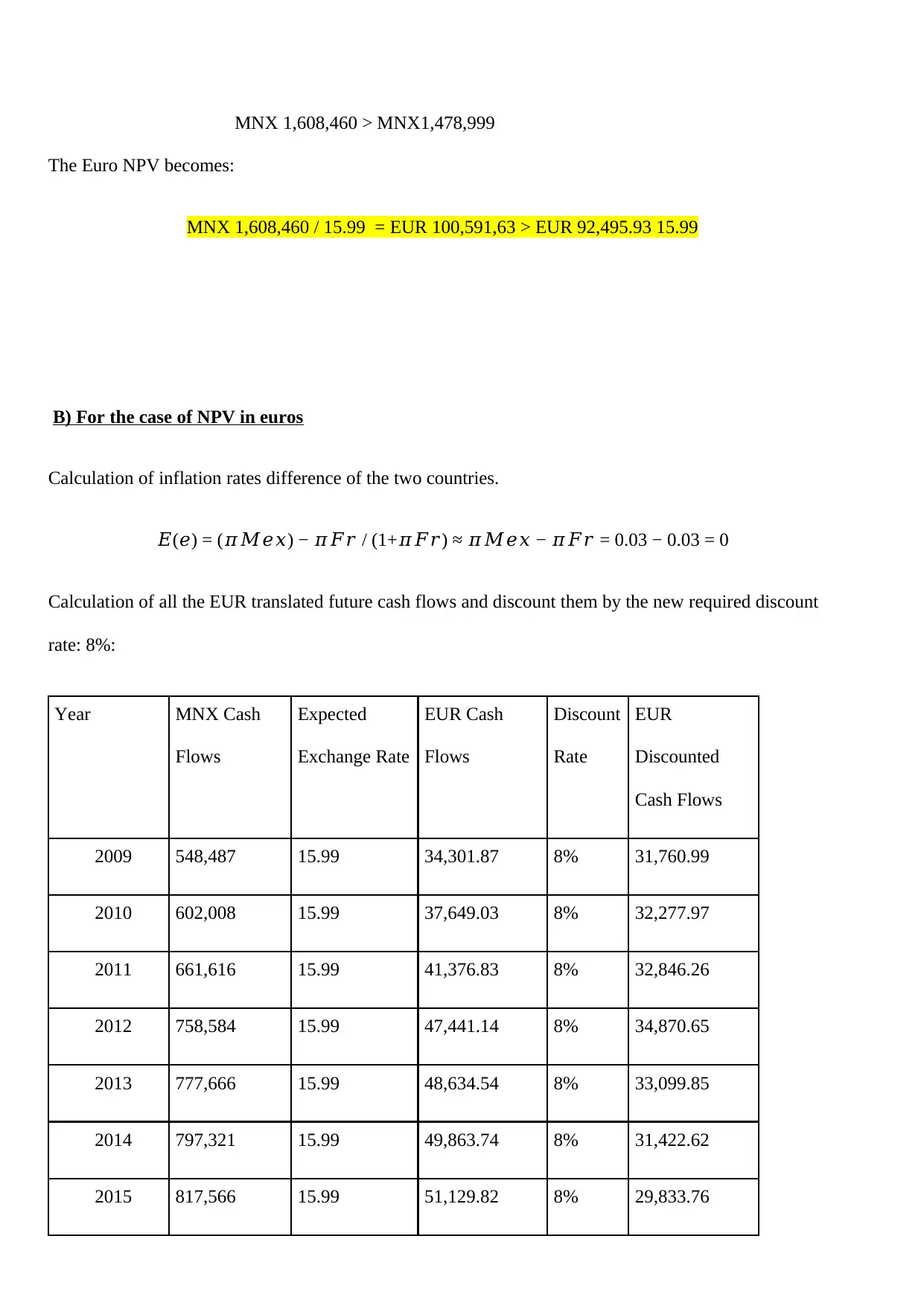

MNX 1,608,460 > MNX1,478,999

The Euro NPV becomes:

MNX 1,608,460 / 15.99 = EUR 100,591,63 > EUR 92,495.93 15.99

B) For the case of NPV in euros

Calculation of inflation rates difference of the two countries.

𝐸(𝑒) = (𝜋𝑀𝑒𝑥) − 𝜋𝐹𝑟 / (1+𝜋𝐹𝑟) ≈ 𝜋𝑀𝑒𝑥 − 𝜋𝐹𝑟 = 0.03 − 0.03 = 0

Calculation of all the EUR translated future cash flows and discount them by the new required discount

rate: 8%:

Year MNX Cash

Flows

Expected

Exchange Rate

EUR Cash

Flows

Discount

Rate

EUR

Discounted

Cash Flows

2009 548,487 15.99 34,301.87 8% 31,760.99

2010 602,008 15.99 37,649.03 8% 32,277.97

2011 661,616 15.99 41,376.83 8% 32,846.26

2012 758,584 15.99 47,441.14 8% 34,870.65

2013 777,666 15.99 48,634.54 8% 33,099.85

2014 797,321 15.99 49,863.74 8% 31,422.62

2015 817,566 15.99 51,129.82 8% 29,833.76

The Euro NPV becomes:

MNX 1,608,460 / 15.99 = EUR 100,591,63 > EUR 92,495.93 15.99

B) For the case of NPV in euros

Calculation of inflation rates difference of the two countries.

𝐸(𝑒) = (𝜋𝑀𝑒𝑥) − 𝜋𝐹𝑟 / (1+𝜋𝐹𝑟) ≈ 𝜋𝑀𝑒𝑥 − 𝜋𝐹𝑟 = 0.03 − 0.03 = 0

Calculation of all the EUR translated future cash flows and discount them by the new required discount

rate: 8%:

Year MNX Cash

Flows

Expected

Exchange Rate

EUR Cash

Flows

Discount

Rate

EUR

Discounted

Cash Flows

2009 548,487 15.99 34,301.87 8% 31,760.99

2010 602,008 15.99 37,649.03 8% 32,277.97

2011 661,616 15.99 41,376.83 8% 32,846.26

2012 758,584 15.99 47,441.14 8% 34,870.65

2013 777,666 15.99 48,634.54 8% 33,099.85

2014 797,321 15.99 49,863.74 8% 31,422.62

2015 817,566 15.99 51,129.82 8% 29,833.76

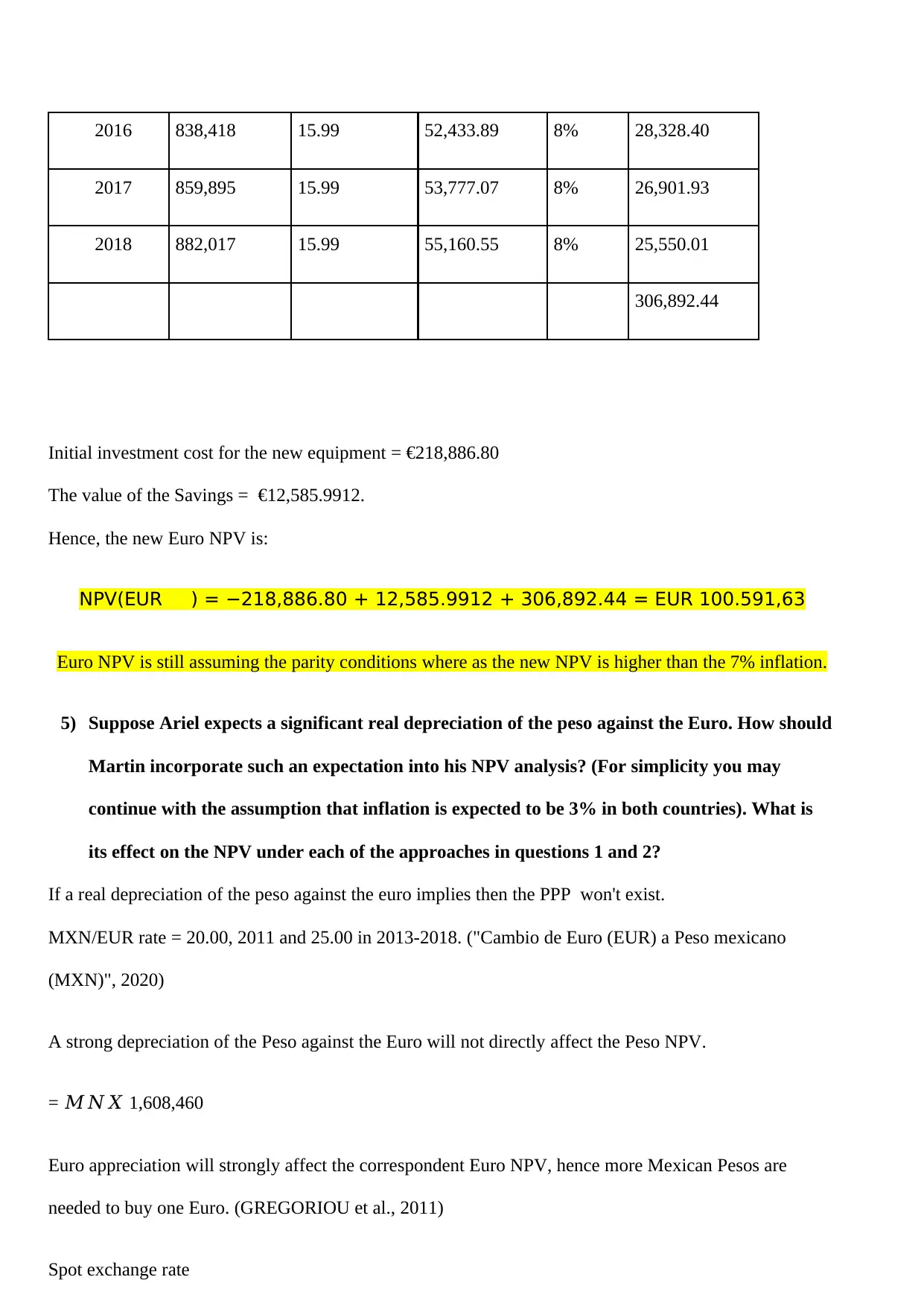

2016 838,418 15.99 52,433.89 8% 28,328.40

2017 859,895 15.99 53,777.07 8% 26,901.93

2018 882,017 15.99 55,160.55 8% 25,550.01

306,892.44

Initial investment cost for the new equipment = €218,886.80

The value of the Savings = €12,585.9912.

Hence, the new Euro NPV is:

NPV(EUR ) = −218,886.80 + 12,585.9912 + 306,892.44 = EUR 100.591,63

Euro NPV is still assuming the parity conditions where as the new NPV is higher than the 7% inflation.

5) Suppose Ariel expects a significant real depreciation of the peso against the Euro. How should

Martin incorporate such an expectation into his NPV analysis? (For simplicity you may

continue with the assumption that inflation is expected to be 3% in both countries). What is

its effect on the NPV under each of the approaches in questions 1 and 2?

If a real depreciation of the peso against the euro implies then the PPP won't exist.

MXN/EUR rate = 20.00, 2011 and 25.00 in 2013-2018. ("Cambio de Euro (EUR) a Peso mexicano

(MXN)", 2020)

A strong depreciation of the Peso against the Euro will not directly affect the Peso NPV.

= 𝑀𝑁𝑋 1,608,460

Euro appreciation will strongly affect the correspondent Euro NPV, hence more Mexican Pesos are

needed to buy one Euro. (GREGORIOU et al., 2011)

Spot exchange rate

2017 859,895 15.99 53,777.07 8% 26,901.93

2018 882,017 15.99 55,160.55 8% 25,550.01

306,892.44

Initial investment cost for the new equipment = €218,886.80

The value of the Savings = €12,585.9912.

Hence, the new Euro NPV is:

NPV(EUR ) = −218,886.80 + 12,585.9912 + 306,892.44 = EUR 100.591,63

Euro NPV is still assuming the parity conditions where as the new NPV is higher than the 7% inflation.

5) Suppose Ariel expects a significant real depreciation of the peso against the Euro. How should

Martin incorporate such an expectation into his NPV analysis? (For simplicity you may

continue with the assumption that inflation is expected to be 3% in both countries). What is

its effect on the NPV under each of the approaches in questions 1 and 2?

If a real depreciation of the peso against the euro implies then the PPP won't exist.

MXN/EUR rate = 20.00, 2011 and 25.00 in 2013-2018. ("Cambio de Euro (EUR) a Peso mexicano

(MXN)", 2020)

A strong depreciation of the Peso against the Euro will not directly affect the Peso NPV.

= 𝑀𝑁𝑋 1,608,460

Euro appreciation will strongly affect the correspondent Euro NPV, hence more Mexican Pesos are

needed to buy one Euro. (GREGORIOU et al., 2011)

Spot exchange rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

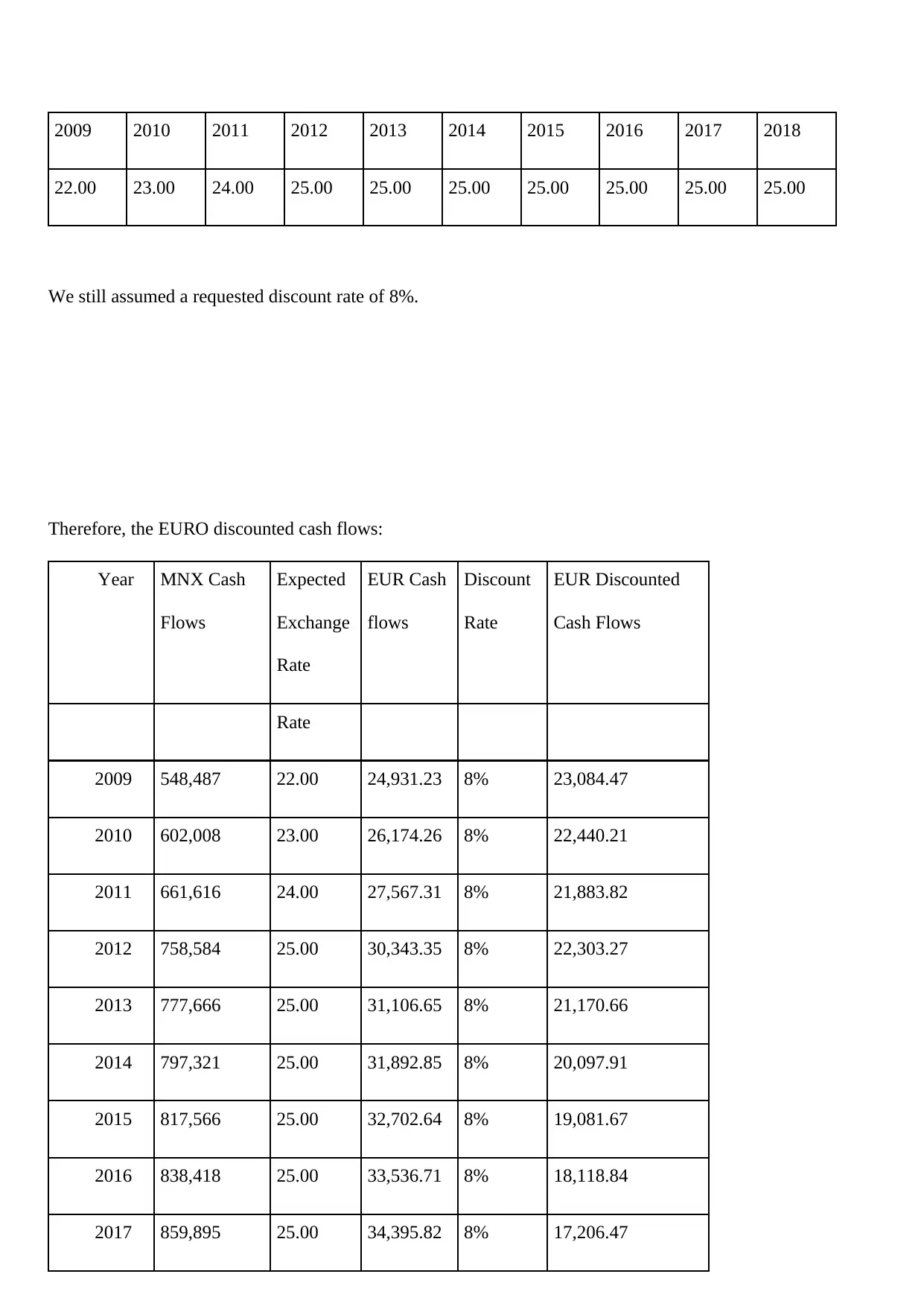

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

22.00 23.00 24.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00

We still assumed a requested discount rate of 8%.

Therefore, the EURO discounted cash flows:

Year MNX Cash

Flows

Expected

Exchange

Rate

EUR Cash

flows

Discount

Rate

EUR Discounted

Cash Flows

Rate

2009 548,487 22.00 24,931.23 8% 23,084.47

2010 602,008 23.00 26,174.26 8% 22,440.21

2011 661,616 24.00 27,567.31 8% 21,883.82

2012 758,584 25.00 30,343.35 8% 22,303.27

2013 777,666 25.00 31,106.65 8% 21,170.66

2014 797,321 25.00 31,892.85 8% 20,097.91

2015 817,566 25.00 32,702.64 8% 19,081.67

2016 838,418 25.00 33,536.71 8% 18,118.84

2017 859,895 25.00 34,395.82 8% 17,206.47

22.00 23.00 24.00 25.00 25.00 25.00 25.00 25.00 25.00 25.00

We still assumed a requested discount rate of 8%.

Therefore, the EURO discounted cash flows:

Year MNX Cash

Flows

Expected

Exchange

Rate

EUR Cash

flows

Discount

Rate

EUR Discounted

Cash Flows

Rate

2009 548,487 22.00 24,931.23 8% 23,084.47

2010 602,008 23.00 26,174.26 8% 22,440.21

2011 661,616 24.00 27,567.31 8% 21,883.82

2012 758,584 25.00 30,343.35 8% 22,303.27

2013 777,666 25.00 31,106.65 8% 21,170.66

2014 797,321 25.00 31,892.85 8% 20,097.91

2015 817,566 25.00 32,702.64 8% 19,081.67

2016 838,418 25.00 33,536.71 8% 18,118.84

2017 859,895 25.00 34,395.82 8% 17,206.47

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 882,017 25.00 35,280.69 8% 16,341.79

201,729.11

The initial investment cost = EUR 218,886.80

The new equipment = EUR 12,585.9912,

The Euro NPV is:

𝑁𝑃𝑉(𝐸𝑈𝑅) = −218,886.80 + 12,585.9912 + 201,729.11 = −EUR 4,571.70

6) Should Ariel approve the equipment purchase?

The organization ought to decide if to buy the new gear putting together its choice concerning the

undertaking NPV. Specifically, if 𝑁𝑃𝑉 > 0, at that point the venture will be a positive development

opportunity. (Demina et al., 2017)

As should be obvious from the Peso DCF assessment, subbing the old gear with the new robotized

process is by and large a wise venture opportunity (Peso NPV is constantly positive). Right now the

organization ought to enter the new speculation and will be detached whether to put resources into Euros

or Pesos. If rather, the Mexican Peso endures a solid devaluation (expecting equality conditions don't

hold any more), the Euro NPV of the undertaking might be negative, bringing about an awful venture

choice. ("International Capital Budgeting", 2020)

201,729.11

The initial investment cost = EUR 218,886.80

The new equipment = EUR 12,585.9912,

The Euro NPV is:

𝑁𝑃𝑉(𝐸𝑈𝑅) = −218,886.80 + 12,585.9912 + 201,729.11 = −EUR 4,571.70

6) Should Ariel approve the equipment purchase?

The organization ought to decide if to buy the new gear putting together its choice concerning the

undertaking NPV. Specifically, if 𝑁𝑃𝑉 > 0, at that point the venture will be a positive development

opportunity. (Demina et al., 2017)

As should be obvious from the Peso DCF assessment, subbing the old gear with the new robotized

process is by and large a wise venture opportunity (Peso NPV is constantly positive). Right now the

organization ought to enter the new speculation and will be detached whether to put resources into Euros

or Pesos. If rather, the Mexican Peso endures a solid devaluation (expecting equality conditions don't

hold any more), the Euro NPV of the undertaking might be negative, bringing about an awful venture

choice. ("International Capital Budgeting", 2020)

References

Lee, J., Faruqee, H., & Bayoumi, T. (2015). A Fair Exchange? Theory and Practice of Calculating

Equilibrium Exchange Rates. IMF Working Papers, 05(229),

https://doi.org/10.5089/9781451862485.001

Cambio de Euro (EUR) a Peso mexicano (MXN). Themoneyconverter.com. (2020). Retrieved 31 March

2020, from https://themoneyconverter.com/ES/EUR/MXN.

Marchioni, A., & Magni, C. (2016). Sensitivity Analysis and Investment Decisions: NPV-Consistency of

Rates of Return. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2797685

International Capital Budgeting. Xplaind.com. (2020). Retrieved 31 March 2020, from

https://xplaind.com/175889/international-npv-foreign-project.

Jacobs, J. (2014). Capital Budgeting: NPV v. IRR Controversy, Unmasking Common Assertions. SSRN

Electronic Journal. https://doi.org/10.2139/ssrn.981382

O'Brien, T. (2015). Foreign Exchange and Cross-Border Valuation. SSRN Electronic Journal.

https://doi.org/10.2139/ssrn.348462

Ariel | Team & Leadership Training. Ariel Group. (2020). Retrieved 1 April 2020, from

https://www.arielgroup.com/.

Demina, I., Larionova, E., & Chinaeva, T. (2017). Investments in fixed assets and depreciation of fixed

assets: theoretical and practical aspects of study and analysis. Statistics And Economics, (3), 71-79.

https://doi.org/10.21686/2500-3925-2017-3-71-79

Lee, J., Faruqee, H., & Bayoumi, T. (2015). A Fair Exchange? Theory and Practice of Calculating

Equilibrium Exchange Rates. IMF Working Papers, 05(229),

https://doi.org/10.5089/9781451862485.001

Cambio de Euro (EUR) a Peso mexicano (MXN). Themoneyconverter.com. (2020). Retrieved 31 March

2020, from https://themoneyconverter.com/ES/EUR/MXN.

Marchioni, A., & Magni, C. (2016). Sensitivity Analysis and Investment Decisions: NPV-Consistency of

Rates of Return. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2797685

International Capital Budgeting. Xplaind.com. (2020). Retrieved 31 March 2020, from

https://xplaind.com/175889/international-npv-foreign-project.

Jacobs, J. (2014). Capital Budgeting: NPV v. IRR Controversy, Unmasking Common Assertions. SSRN

Electronic Journal. https://doi.org/10.2139/ssrn.981382

O'Brien, T. (2015). Foreign Exchange and Cross-Border Valuation. SSRN Electronic Journal.

https://doi.org/10.2139/ssrn.348462

Ariel | Team & Leadership Training. Ariel Group. (2020). Retrieved 1 April 2020, from

https://www.arielgroup.com/.

Demina, I., Larionova, E., & Chinaeva, T. (2017). Investments in fixed assets and depreciation of fixed

assets: theoretical and practical aspects of study and analysis. Statistics And Economics, (3), 71-79.

https://doi.org/10.21686/2500-3925-2017-3-71-79

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.