GSB003 Managing Financial Resources: Billabong International Analysis

VerifiedAdded on 2023/06/11

|21

|4235

|423

Report

AI Summary

This report provides an in-depth financial statement analysis of Billabong International Limited, an Australian clothing retailer. It covers the company's financial performance, key financial issues, and a global overview of its market position. The analysis includes a comparison of average prices with competitors, an examination of branding and market position events, and an assessment of the impact of the Global Financial Crisis (GFC). Critical factors for financial viability are identified, and a comprehensive ratio analysis is performed, including liquidity, asset management, profitability, and leverage ratios. The report concludes with a summary of the findings, offering insights into Billabong's financial health and strategic direction. Desklib provides access to similar past papers and solved assignments for students.

Running Head: FINANCIAL STATEMNET ANALYSIS 0

Billabong International Limited

Financial Statement Analysis

Billabong International Limited

Financial Statement Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMNET ANALYSIS 1

Executive Summary

The below report provides an overview about an Australian Company Billabong International

which deals in clothing segment of the industry. An in depth analysis of the financial

performance of the company has been done along with the ratio analysis. Further, the global

review is also done to view the market position of the company in terms of its competitors.

Also the impact of the global financial crisis has been undertaken and the list of events that

lead to this kind of financial position has also been discussed relevantly.

Executive Summary

The below report provides an overview about an Australian Company Billabong International

which deals in clothing segment of the industry. An in depth analysis of the financial

performance of the company has been done along with the ratio analysis. Further, the global

review is also done to view the market position of the company in terms of its competitors.

Also the impact of the global financial crisis has been undertaken and the list of events that

lead to this kind of financial position has also been discussed relevantly.

FINANCIAL STATEMNET ANALYSIS 2

Table of Contents

Introduction................................................................................................................................2

Financial Performance...............................................................................................................2

Financial issues.......................................................................................................................3

Global Overview........................................................................................................................3

Average Price Comparison........................................................................................................4

Events Branding and Market position........................................................................................5

Impact of GFC........................................................................................................................6

Critical Factors of financial viability......................................................................................7

Ratio Analysis............................................................................................................................7

Liquidity ratios.......................................................................................................................7

Assets management ratio........................................................................................................9

Fixed asset ratio..................................................................................................................9

Profitability Ratios................................................................................................................11

Profit Margin.....................................................................................................................12

Return on Assets...............................................................................................................13

Return on Capital Employed.............................................................................................13

Leverage Ratios....................................................................................................................14

Debt to Equity Ratio.........................................................................................................15

Asset to Equity Ratio........................................................................................................15

Debt to EBITDA...............................................................................................................16

Conclusion................................................................................................................................16

References................................................................................................................................17

Table of Contents

Introduction................................................................................................................................2

Financial Performance...............................................................................................................2

Financial issues.......................................................................................................................3

Global Overview........................................................................................................................3

Average Price Comparison........................................................................................................4

Events Branding and Market position........................................................................................5

Impact of GFC........................................................................................................................6

Critical Factors of financial viability......................................................................................7

Ratio Analysis............................................................................................................................7

Liquidity ratios.......................................................................................................................7

Assets management ratio........................................................................................................9

Fixed asset ratio..................................................................................................................9

Profitability Ratios................................................................................................................11

Profit Margin.....................................................................................................................12

Return on Assets...............................................................................................................13

Return on Capital Employed.............................................................................................13

Leverage Ratios....................................................................................................................14

Debt to Equity Ratio.........................................................................................................15

Asset to Equity Ratio........................................................................................................15

Debt to EBITDA...............................................................................................................16

Conclusion................................................................................................................................16

References................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL STATEMNET ANALYSIS 3

Introduction

Billabong Australia is a surf company, primarily a clothing retailer which is also involved in

the businesses of wide range of accessories such as backpacks, skate boards and products

related to snowboard. This company came into existence on 1973 by Rena merchant and

Gordan and was founded in the Gold coast, Queensland. On 11th of August 2000, the

company was first traded on the Australian Securities Exchange. The name of the company

was derived from the word “bilaban” which means a creek that is operating only in the rainy

season. The most prominent and futuristic brands owned by the company billabong are Von

Zipper and Element.

Financial Performance

EBITDA of the brand Billabong escalated by $7.5 million globally in contrast to the sales

which want down by 0.8%. This reflects the contraction of the plan in the Europe and to

deliver the whole attention on key accounts and revenue shall be not only quantity wise but

also shall account for quality. Outside Australia the market coverage of the Billabong grew

by 13.2% (Annual reports, 2018).

For RVCA the investment was heavy and high in the area of marketing to drive the growth of

the product globally. Though the EBITDA rise by only $0.5 million yet the initiative led to

sales grew by 12.8% outside the region (Annual reports, 2018). Also in Asia pacific region

the sales were above by 30%.

Lastly the Element brand was also playing a vital role in reshaping the position of the

organisation. EBITDA was up by $3 million and on the contrary the sales were down 9.7%.

However, element’s covered the largest market, were up 5.6% (Annual reports, 2018).

Introduction

Billabong Australia is a surf company, primarily a clothing retailer which is also involved in

the businesses of wide range of accessories such as backpacks, skate boards and products

related to snowboard. This company came into existence on 1973 by Rena merchant and

Gordan and was founded in the Gold coast, Queensland. On 11th of August 2000, the

company was first traded on the Australian Securities Exchange. The name of the company

was derived from the word “bilaban” which means a creek that is operating only in the rainy

season. The most prominent and futuristic brands owned by the company billabong are Von

Zipper and Element.

Financial Performance

EBITDA of the brand Billabong escalated by $7.5 million globally in contrast to the sales

which want down by 0.8%. This reflects the contraction of the plan in the Europe and to

deliver the whole attention on key accounts and revenue shall be not only quantity wise but

also shall account for quality. Outside Australia the market coverage of the Billabong grew

by 13.2% (Annual reports, 2018).

For RVCA the investment was heavy and high in the area of marketing to drive the growth of

the product globally. Though the EBITDA rise by only $0.5 million yet the initiative led to

sales grew by 12.8% outside the region (Annual reports, 2018). Also in Asia pacific region

the sales were above by 30%.

Lastly the Element brand was also playing a vital role in reshaping the position of the

organisation. EBITDA was up by $3 million and on the contrary the sales were down 9.7%.

However, element’s covered the largest market, were up 5.6% (Annual reports, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMNET ANALYSIS 4

The financial results of the company after the Net Profit after Tax for the full year to 30th

June were $4.2 million, compared to $233.7 million loss for the previous year entirely. It was

almost a surprise for the company as it returned to full year EBITDA after the year 2008. The

overall result which was derived after eliminating certain items and discounted business the

value amounted to $65.7 million. Also when compared to the previous year the result was up

by 8.9% (Corporate Finance Institute, 2016).

Financial issues

Due to the initial recovery of the company the dividend was not allocated for the year 2015.

For the year 2016-2017 the EBITDA was of $10.8 million for as compared to $21.8 million

of the previous year. If the performance is reviewed from the regional side than the EBITDA

of $11.9 million for the Asia Pacific was highest. EBITDA was $4.8 million for the American

region and $1.3 million for the European region (Annual reports, 2018). On the contrary in

terms of the revenue, the revenue of the American region was highest 1.1% higher, otherwise

for both the European region and Asia pacific region the revenue was 6.5% lower and 3.7%

lower respectively (Sarlin, 2015).

Global Overview

Strong second half lifts EBITDA to $51.1 million up by 2.8%. The results mark a

turning point for the company to build itself for long term.

Europe also rebounded after facing the tough market conditions.

Totals sales are of $974.7 million exclusive of Tigerlily and Sector 9.

Particulars Asia Pacific American European

Bricks and

Comparable Store

0.8% higher 0.7% higher 2.3% down

The financial results of the company after the Net Profit after Tax for the full year to 30th

June were $4.2 million, compared to $233.7 million loss for the previous year entirely. It was

almost a surprise for the company as it returned to full year EBITDA after the year 2008. The

overall result which was derived after eliminating certain items and discounted business the

value amounted to $65.7 million. Also when compared to the previous year the result was up

by 8.9% (Corporate Finance Institute, 2016).

Financial issues

Due to the initial recovery of the company the dividend was not allocated for the year 2015.

For the year 2016-2017 the EBITDA was of $10.8 million for as compared to $21.8 million

of the previous year. If the performance is reviewed from the regional side than the EBITDA

of $11.9 million for the Asia Pacific was highest. EBITDA was $4.8 million for the American

region and $1.3 million for the European region (Annual reports, 2018). On the contrary in

terms of the revenue, the revenue of the American region was highest 1.1% higher, otherwise

for both the European region and Asia pacific region the revenue was 6.5% lower and 3.7%

lower respectively (Sarlin, 2015).

Global Overview

Strong second half lifts EBITDA to $51.1 million up by 2.8%. The results mark a

turning point for the company to build itself for long term.

Europe also rebounded after facing the tough market conditions.

Totals sales are of $974.7 million exclusive of Tigerlily and Sector 9.

Particulars Asia Pacific American European

Bricks and

Comparable Store

0.8% higher 0.7% higher 2.3% down

FINANCIAL STATEMNET ANALYSIS 5

Gross Margin 120 basis point 110 basis point 100 basis point

Ecommerce 28.7% growth Grew by19.5% A growth of 15.1%

Revenue 6.6% lower 1.15% higher 3.7% lower

Income Tax Expense $2.2 million $2.8 million $2.1 million

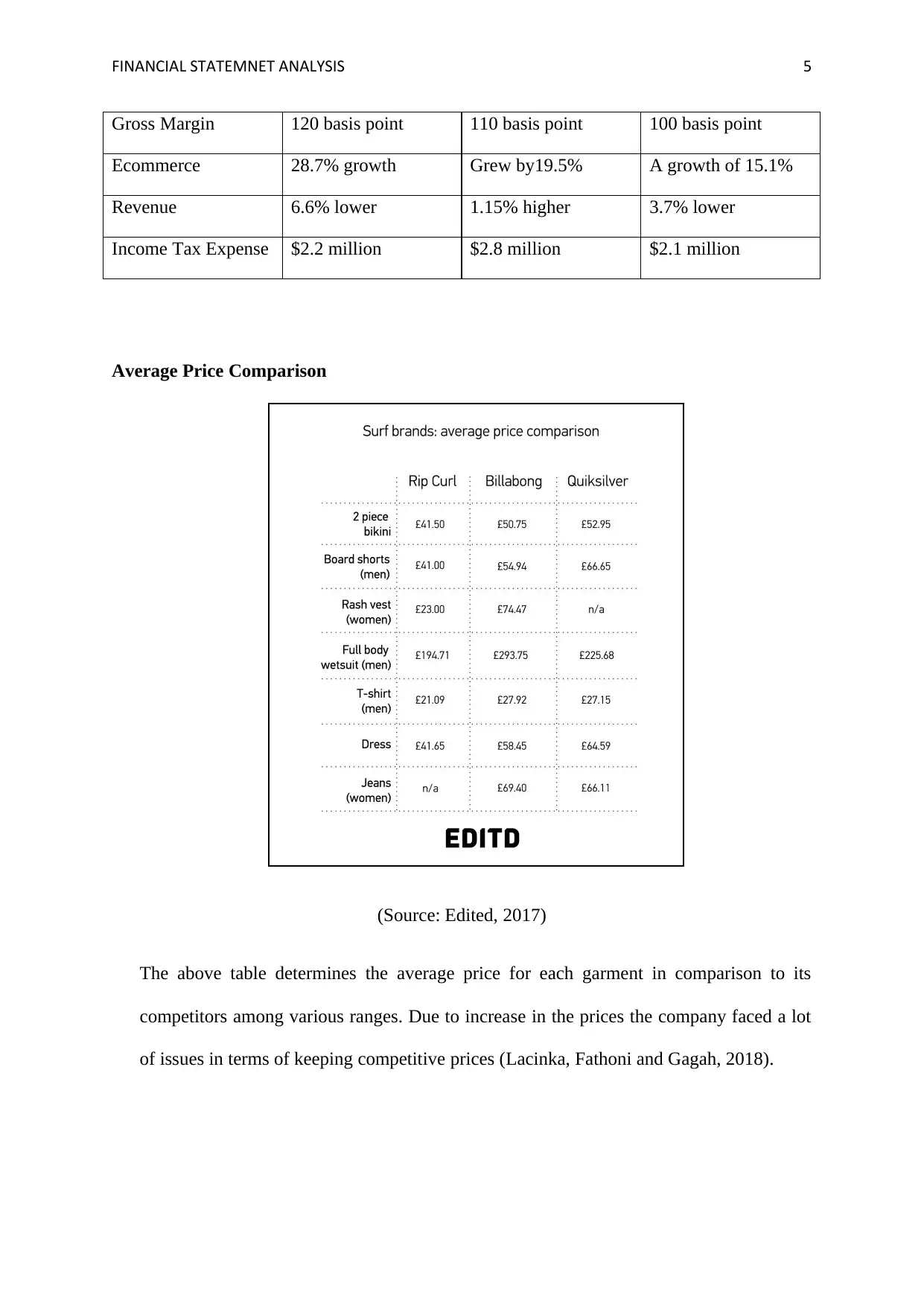

Average Price Comparison

(Source: Edited, 2017)

The above table determines the average price for each garment in comparison to its

competitors among various ranges. Due to increase in the prices the company faced a lot

of issues in terms of keeping competitive prices (Lacinka, Fathoni and Gagah, 2018).

Gross Margin 120 basis point 110 basis point 100 basis point

Ecommerce 28.7% growth Grew by19.5% A growth of 15.1%

Revenue 6.6% lower 1.15% higher 3.7% lower

Income Tax Expense $2.2 million $2.8 million $2.1 million

Average Price Comparison

(Source: Edited, 2017)

The above table determines the average price for each garment in comparison to its

competitors among various ranges. Due to increase in the prices the company faced a lot

of issues in terms of keeping competitive prices (Lacinka, Fathoni and Gagah, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL STATEMNET ANALYSIS 6

Events Branding and Market position

These events provide a wide range of platform through which the company can take

challenge itself for revamping the business to support our world class brands. The year 2014-

2015 has been year of the rebuilding because of the fact that the company was returning to its

original profit state after 2011 (Annual reports, 2018). The performance was achieved

specially by having a team which is focused globally and uniformly. The company had strong

collaborations and relations both within the region as well as in the brands (Sarlin, 2015).

After an in depth analysis the company sold the interest in SurfStitch and the completely

owned Swell in September 2014. Due to this step the transactions were retrieved and entire

control was given to the company. The previously licensed websites which were allocated for

the SurfStithc also retains the supply agreements in bulk (Annual reports, 2018).

The second move was towards the mono brand focus and in particular the major attention

was on three big brands namely Billabong, RVCA, Element are the key drivers in improving

the overall performance of the business (My Accounting Course, 2017).

Consistently following an old logo, the new mantra for success was “fewer, bigger, better”. A

heavy load of the projects were segregated among the four major projects which are given

priority namely Omni-channel, distribution and transportation, customer the cream and

sourcing and chain of supply (Kaur, Aggarwal and Gupta, 2017). These four projects were

provided more evaluation and attention and eventually they helped in accelerating the volume

globally.

The reduction in the distribution costs by $10 million per annum is now an initiative of sober

implementation. The group worked on the closure of the Canadian Warehouse and also

transitioned the third party logistics.

Events Branding and Market position

These events provide a wide range of platform through which the company can take

challenge itself for revamping the business to support our world class brands. The year 2014-

2015 has been year of the rebuilding because of the fact that the company was returning to its

original profit state after 2011 (Annual reports, 2018). The performance was achieved

specially by having a team which is focused globally and uniformly. The company had strong

collaborations and relations both within the region as well as in the brands (Sarlin, 2015).

After an in depth analysis the company sold the interest in SurfStitch and the completely

owned Swell in September 2014. Due to this step the transactions were retrieved and entire

control was given to the company. The previously licensed websites which were allocated for

the SurfStithc also retains the supply agreements in bulk (Annual reports, 2018).

The second move was towards the mono brand focus and in particular the major attention

was on three big brands namely Billabong, RVCA, Element are the key drivers in improving

the overall performance of the business (My Accounting Course, 2017).

Consistently following an old logo, the new mantra for success was “fewer, bigger, better”. A

heavy load of the projects were segregated among the four major projects which are given

priority namely Omni-channel, distribution and transportation, customer the cream and

sourcing and chain of supply (Kaur, Aggarwal and Gupta, 2017). These four projects were

provided more evaluation and attention and eventually they helped in accelerating the volume

globally.

The reduction in the distribution costs by $10 million per annum is now an initiative of sober

implementation. The group worked on the closure of the Canadian Warehouse and also

transitioned the third party logistics.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMNET ANALYSIS 7

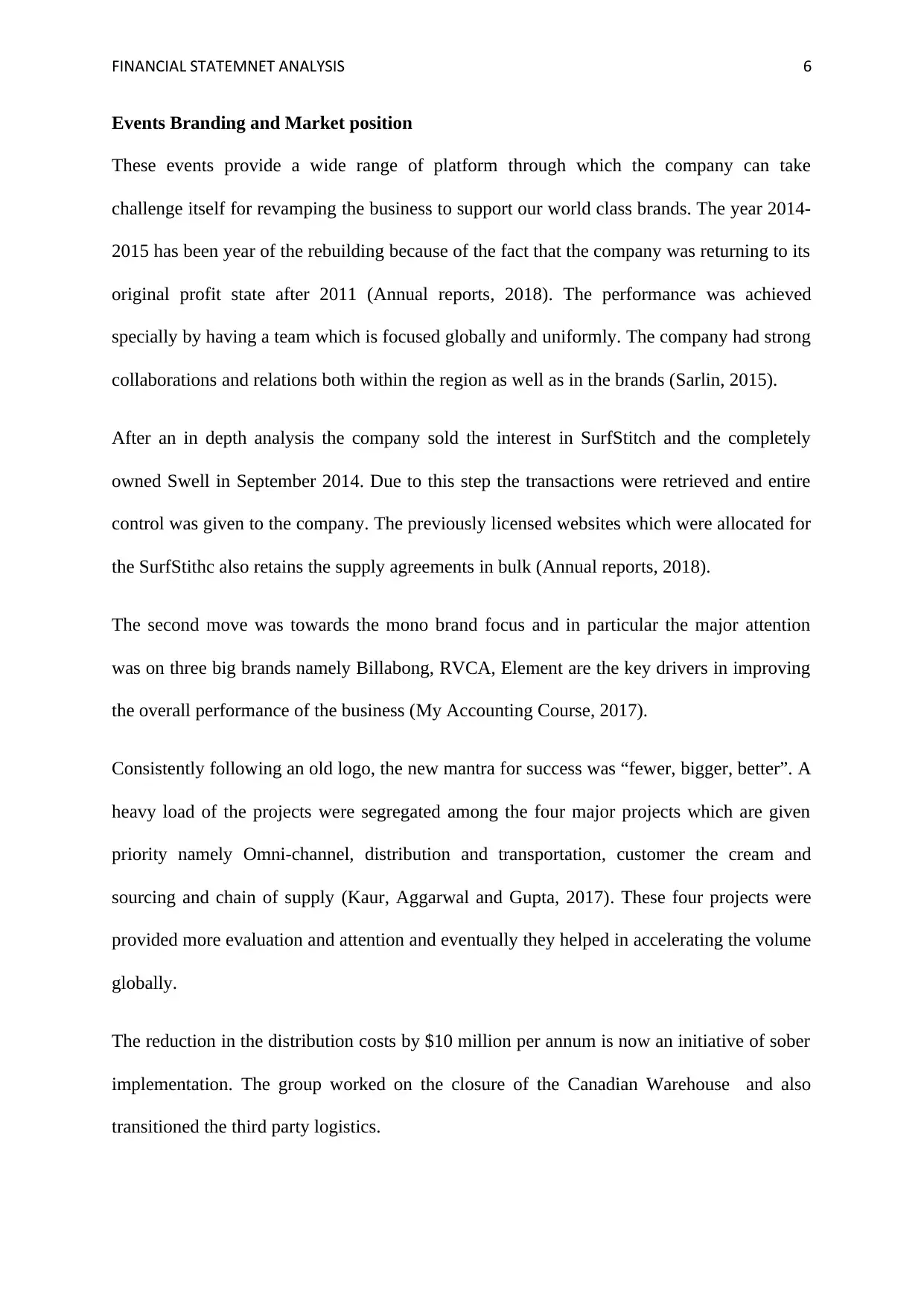

(Source: Edited, 2017).

The above picture depicts the market position of the company among the other similar

companies.

Impact of GFC

The global financial crisis made a square pit for the Billabong International to test itself on

account of performance in the emerging retail operations with a wider wholesale account

base. The Australian dollar stays at US92c and the net profit is down by 6%, excluding the

prior year’s impairment change if there is any fluctuation in the rate as what is recorded. The

overall impact was held on the net profit after tax attributable to the shareholders which

amounted to $152.8 after a drop by more than 13%.

(Source: Edited, 2017).

The above picture depicts the market position of the company among the other similar

companies.

Impact of GFC

The global financial crisis made a square pit for the Billabong International to test itself on

account of performance in the emerging retail operations with a wider wholesale account

base. The Australian dollar stays at US92c and the net profit is down by 6%, excluding the

prior year’s impairment change if there is any fluctuation in the rate as what is recorded. The

overall impact was held on the net profit after tax attributable to the shareholders which

amounted to $152.8 after a drop by more than 13%.

FINANCIAL STATEMNET ANALYSIS 8

Critical Factors of financial viability

Global sourcing of the products and the services

The preferred vendors are included in the new initiatives and the schemes

To convert the losses into at par profits through the highly strategic moves and

transformational methods.

To improve the gross margin is also one of the critical factors for the future

sustainability.

To continue to gain the effective cost in the productivity of the company.

To keep the top line inventory cautiously.

Ratio Analysis

Ratio analysis is the quantitative analysis of the financial statements which is used to evaluate

the various aspects of the company such as efficiency, liquidity, solvency and profitability.

This type of comparison is particularly useful for many users of the financial statements both

within the organisation as well as outside it. The investors, shareholders, suppliers, customers

and employees majorly take decisions on the basis of the ratio analysis (Alin-Eliodor, 2014).

There are majorly four types of ratios liquidity, Asset Management Ratio, Profitability and

Leverage Ratios.

Liquidity ratios

A liquidity ratio is an indicator in which it can be determined that how much of the current

assets are sufficient to pay back the company’s obligations as and when they become due. It

is also known as the acid test ratio (Entwistle, 2015). Under the liquidity ratio there are

majorly three ratios which are current ratio, quick ratio and working capital ratio.

Critical Factors of financial viability

Global sourcing of the products and the services

The preferred vendors are included in the new initiatives and the schemes

To convert the losses into at par profits through the highly strategic moves and

transformational methods.

To improve the gross margin is also one of the critical factors for the future

sustainability.

To continue to gain the effective cost in the productivity of the company.

To keep the top line inventory cautiously.

Ratio Analysis

Ratio analysis is the quantitative analysis of the financial statements which is used to evaluate

the various aspects of the company such as efficiency, liquidity, solvency and profitability.

This type of comparison is particularly useful for many users of the financial statements both

within the organisation as well as outside it. The investors, shareholders, suppliers, customers

and employees majorly take decisions on the basis of the ratio analysis (Alin-Eliodor, 2014).

There are majorly four types of ratios liquidity, Asset Management Ratio, Profitability and

Leverage Ratios.

Liquidity ratios

A liquidity ratio is an indicator in which it can be determined that how much of the current

assets are sufficient to pay back the company’s obligations as and when they become due. It

is also known as the acid test ratio (Entwistle, 2015). Under the liquidity ratio there are

majorly three ratios which are current ratio, quick ratio and working capital ratio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL STATEMNET ANALYSIS 9

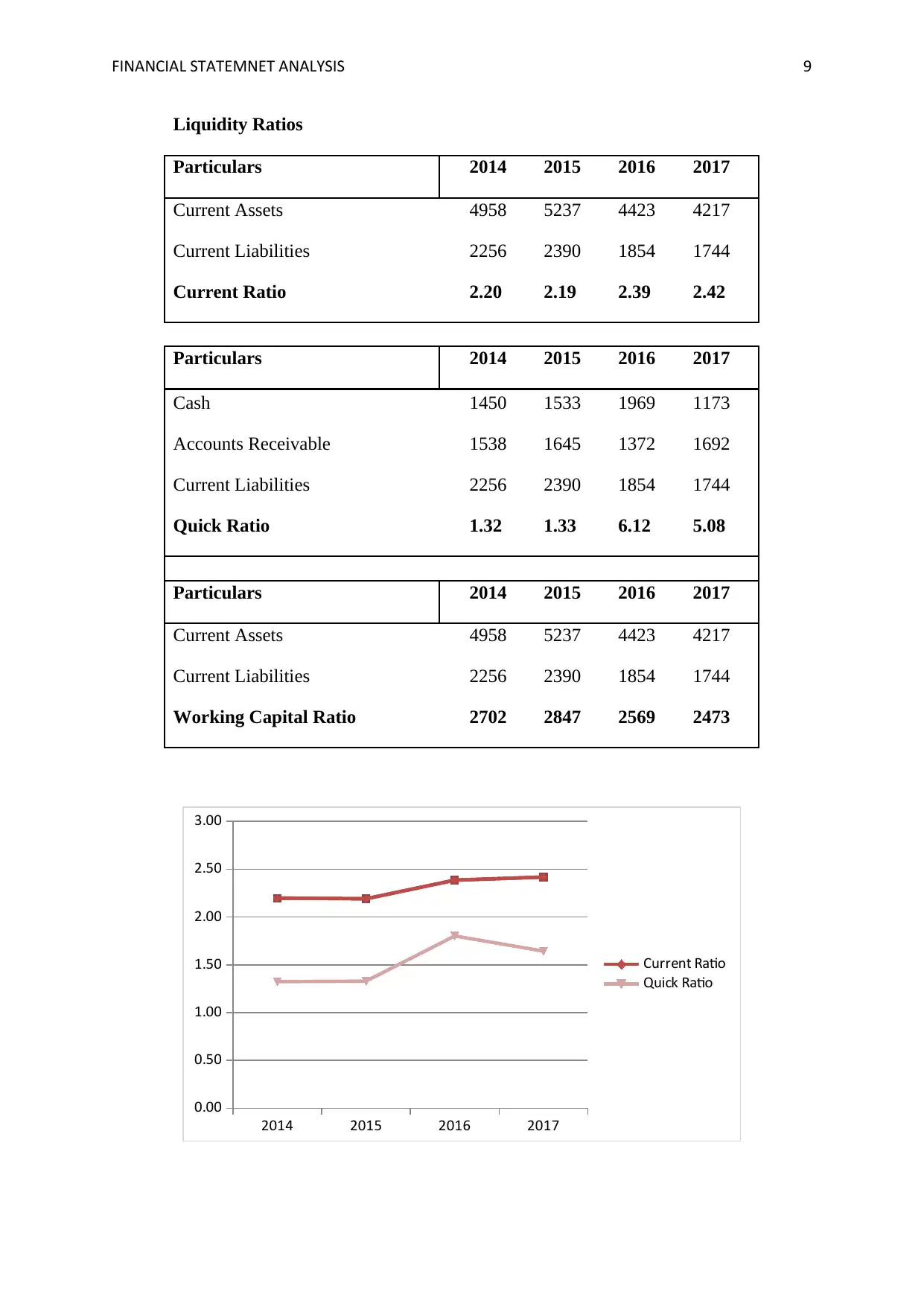

Liquidity Ratios

Particulars 2014 2015 2016 2017

Current Assets 4958 5237 4423 4217

Current Liabilities 2256 2390 1854 1744

Current Ratio 2.20 2.19 2.39 2.42

Particulars 2014 2015 2016 2017

Cash 1450 1533 1969 1173

Accounts Receivable 1538 1645 1372 1692

Current Liabilities 2256 2390 1854 1744

Quick Ratio 1.32 1.33 6.12 5.08

Particulars 2014 2015 2016 2017

Current Assets 4958 5237 4423 4217

Current Liabilities 2256 2390 1854 1744

Working Capital Ratio 2702 2847 2569 2473

2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Current Ratio

Quick Ratio

Liquidity Ratios

Particulars 2014 2015 2016 2017

Current Assets 4958 5237 4423 4217

Current Liabilities 2256 2390 1854 1744

Current Ratio 2.20 2.19 2.39 2.42

Particulars 2014 2015 2016 2017

Cash 1450 1533 1969 1173

Accounts Receivable 1538 1645 1372 1692

Current Liabilities 2256 2390 1854 1744

Quick Ratio 1.32 1.33 6.12 5.08

Particulars 2014 2015 2016 2017

Current Assets 4958 5237 4423 4217

Current Liabilities 2256 2390 1854 1744

Working Capital Ratio 2702 2847 2569 2473

2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Current Ratio

Quick Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL STATEMNET ANALYSIS 10

(Source: By author)

From the above graph it can be analysed that the current ratio of the Billabong International is

consistently within the rule of the ideal ratio. The ideal ratio is 2:1. However as can be seen

from the above calculations the current ratio is more than 2:1 in all the four years.

The quick ratio of the company is also consistent around 1.5, whereas the ideal ratio is 1:1. A

higher quick ratio shows the company’s ability to liquidate its assets to pay back the

obligations (Flammer, 2015).

And lastly the working capital ratio will determine how much of the current assets are

available against the current liabilities.

Assets management ratio

Asset Management Ratios are available to measure the firm's success in managing its assets

to generate volume of sales (Uechi, et al 2015). For example, these ratios can provide insight

into the success of the firm's credit policy and inventory management. These ratios are also

termed as Activity or Turnover Ratios.

Fixed asset ratio

It is the ratio of sales to the net asset of the company which is very important for knowing

how much the asset of the company are contributing towards the sales of the company. A

positive ratio tells the assets are contributing in the required manner and negative means

declining ratio explains that the assets are not in the favour of sales that is required for the

company. It is the magnitude relation of sales to cyber web plus of the corporate that is

incredibly vital for knowing what proportion the plus of the corporate square measure

(Source: By author)

From the above graph it can be analysed that the current ratio of the Billabong International is

consistently within the rule of the ideal ratio. The ideal ratio is 2:1. However as can be seen

from the above calculations the current ratio is more than 2:1 in all the four years.

The quick ratio of the company is also consistent around 1.5, whereas the ideal ratio is 1:1. A

higher quick ratio shows the company’s ability to liquidate its assets to pay back the

obligations (Flammer, 2015).

And lastly the working capital ratio will determine how much of the current assets are

available against the current liabilities.

Assets management ratio

Asset Management Ratios are available to measure the firm's success in managing its assets

to generate volume of sales (Uechi, et al 2015). For example, these ratios can provide insight

into the success of the firm's credit policy and inventory management. These ratios are also

termed as Activity or Turnover Ratios.

Fixed asset ratio

It is the ratio of sales to the net asset of the company which is very important for knowing

how much the asset of the company are contributing towards the sales of the company. A

positive ratio tells the assets are contributing in the required manner and negative means

declining ratio explains that the assets are not in the favour of sales that is required for the

company. It is the magnitude relation of sales to cyber web plus of the corporate that is

incredibly vital for knowing what proportion the plus of the corporate square measure

FINANCIAL STATEMNET ANALYSIS 11

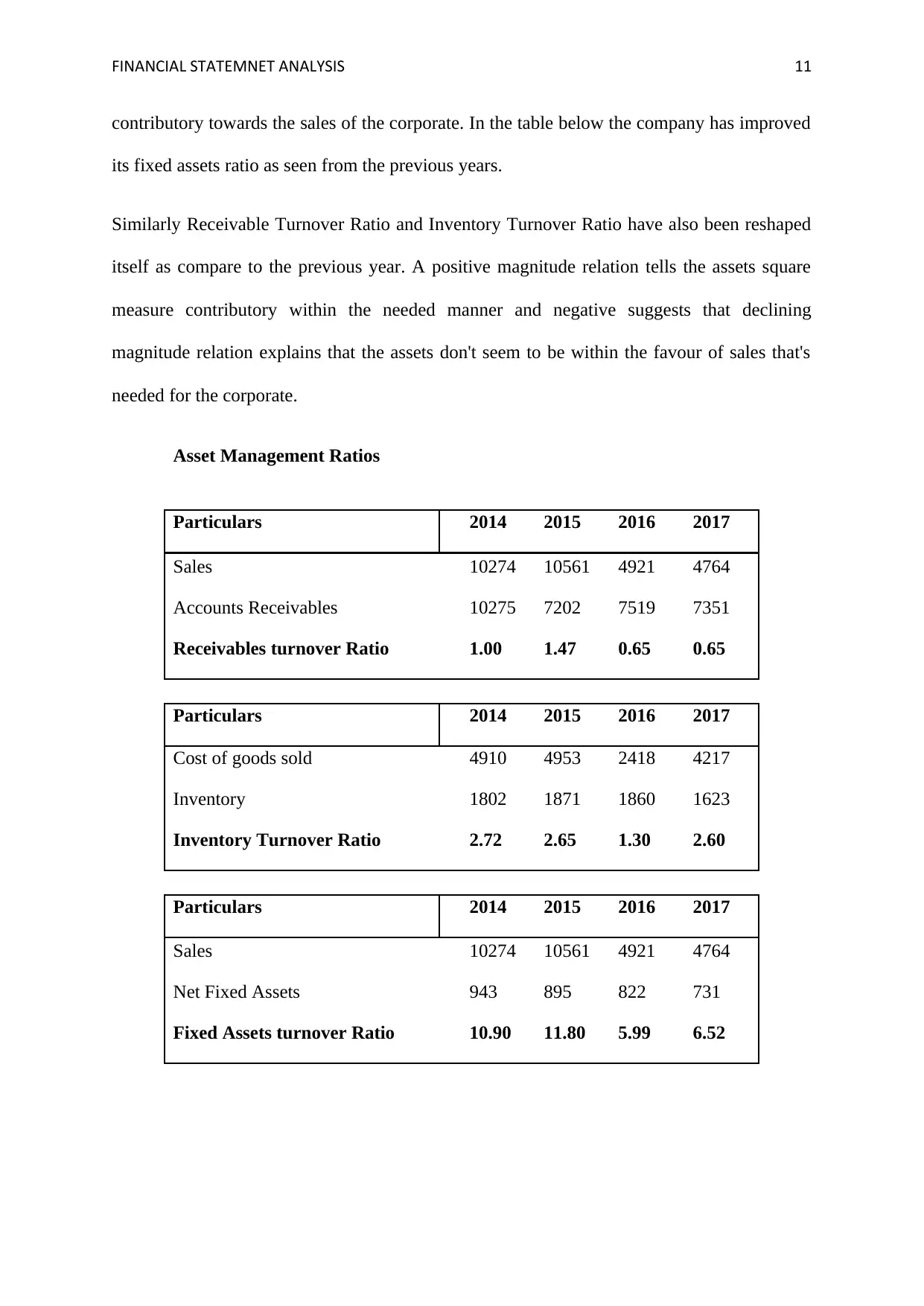

contributory towards the sales of the corporate. In the table below the company has improved

its fixed assets ratio as seen from the previous years.

Similarly Receivable Turnover Ratio and Inventory Turnover Ratio have also been reshaped

itself as compare to the previous year. A positive magnitude relation tells the assets square

measure contributory within the needed manner and negative suggests that declining

magnitude relation explains that the assets don't seem to be within the favour of sales that's

needed for the corporate.

Asset Management Ratios

Particulars 2014 2015 2016 2017

Sales 10274 10561 4921 4764

Accounts Receivables 10275 7202 7519 7351

Receivables turnover Ratio 1.00 1.47 0.65 0.65

Particulars 2014 2015 2016 2017

Cost of goods sold 4910 4953 2418 4217

Inventory 1802 1871 1860 1623

Inventory Turnover Ratio 2.72 2.65 1.30 2.60

Particulars 2014 2015 2016 2017

Sales 10274 10561 4921 4764

Net Fixed Assets 943 895 822 731

Fixed Assets turnover Ratio 10.90 11.80 5.99 6.52

contributory towards the sales of the corporate. In the table below the company has improved

its fixed assets ratio as seen from the previous years.

Similarly Receivable Turnover Ratio and Inventory Turnover Ratio have also been reshaped

itself as compare to the previous year. A positive magnitude relation tells the assets square

measure contributory within the needed manner and negative suggests that declining

magnitude relation explains that the assets don't seem to be within the favour of sales that's

needed for the corporate.

Asset Management Ratios

Particulars 2014 2015 2016 2017

Sales 10274 10561 4921 4764

Accounts Receivables 10275 7202 7519 7351

Receivables turnover Ratio 1.00 1.47 0.65 0.65

Particulars 2014 2015 2016 2017

Cost of goods sold 4910 4953 2418 4217

Inventory 1802 1871 1860 1623

Inventory Turnover Ratio 2.72 2.65 1.30 2.60

Particulars 2014 2015 2016 2017

Sales 10274 10561 4921 4764

Net Fixed Assets 943 895 822 731

Fixed Assets turnover Ratio 10.90 11.80 5.99 6.52

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.