Comprehensive Financial Analysis of GSK Plc's Dividend Policy

VerifiedAdded on 2021/01/03

|18

|4960

|450

Report

AI Summary

This report undertakes a detailed analysis of dividend policies, commencing with an introduction to their significance in enhancing shareholder wealth. Part A explores the dividend irrelevance theory, including its assumptions and implications, contrasting it with the dividend relevance theory and its various models, such as the Walter model, and the Signal and Clientele Effect theories. A comparative summary of these theories is provided. Part B focuses on the financial performance of GlaxoSmithKline (GSK) Plc, employing key financial indicators to evaluate profitability, liquidity, and solvency over a five-year period. The report assesses GSK's debt capacity and identifies financial and business risks. It culminates in recommendations for an optimal mix of debt and equity for GSK Plc. The report concludes with a synthesis of the findings and references cited.

Dividend Policy and Financial

Analysis

Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

PART A ..........................................................................................................................................3

A. Explaining the dividend irrelevancy theory and its assumption............................................3

B. Explaining the dividend relevant theory.................................................................................4

C. Summary based on comparison among theories....................................................................6

PART B............................................................................................................................................7

A) Financial performance of company using indicators.............................................................7

B) Assessing debt capacity of organisation..............................................................................11

C) Financial and business risks of organization........................................................................13

(D) Recommendation for purpose of optimal mix for GSK Plc...............................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

PART A ..........................................................................................................................................3

A. Explaining the dividend irrelevancy theory and its assumption............................................3

B. Explaining the dividend relevant theory.................................................................................4

C. Summary based on comparison among theories....................................................................6

PART B............................................................................................................................................7

A) Financial performance of company using indicators.............................................................7

B) Assessing debt capacity of organisation..............................................................................11

C) Financial and business risks of organization........................................................................13

(D) Recommendation for purpose of optimal mix for GSK Plc...............................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Dividend policies are to be implemented in effective manner so that shareholders' wealth

can be increased. Present report deals with various dividend theory such as irrelevance and

relevance theory and models are discussed. On the other part, GSK Plc's financial performance

over last five years is analysed and ratio analysis is conducted. Moreover, capital structure of

organisation is made and mix of debt and equity is analysed. Recommendations to improve

capital structure are also provided along with business and financial risks are evaluated in a

better way. Hence, complete financial health analysis of company is done in effective manner.

PART A

A. Explaining the dividend irrelevancy theory and its assumption

It is a theory in which investors have no worry whether adequate dividend policy is

implemented by the company or not. It is because option is provided to them to sell off shares

held by them and as a result, cash is provided. This dividend policy is useful the firm as price

and cost of capital is not affected. This theory identifies that dividend policy is independent on

value and market price of shares. Assumption is made by the theory that markets are perfect and

stockholders' can build their policy by selling or purchasing stock in the markets (Jabbouri and

Attar, 2018). The theory indicates that if shareholders need the cash they can sell their shares,

and if they do not want in cash they can hold up their share with them. Brokerage fees are

exempted and the same is treated if capital gains are involved in this irrelevance theory.

Modigliani and Miller proposed that the dividend policy implemented by organization is

independent and do not influence share prices of organization. In this irrelevance theory of the

dividend MM proposed that when a shareholder attains dividend in excess than he has the option

to again invest the company's share in relation to cash flow (Kaur and Saraf, 2014). On contrary

to this, if dividend is small, it can be sold. In both the cases, investors are relevance. In both the

cases it is irrelevant because investors are creating their own cash.

Assumptions of the dividend irrelevant theory are as-

All sort of taxes is ignored (personal taxes, corporate taxes)

There is no flotation cost or transaction cost at the time when company is taking decision

of cost.

There is no impact on dividend policy, when a firm decides in capital budgeting.

All the investors have all the information about firm’s future

Dividend policies are to be implemented in effective manner so that shareholders' wealth

can be increased. Present report deals with various dividend theory such as irrelevance and

relevance theory and models are discussed. On the other part, GSK Plc's financial performance

over last five years is analysed and ratio analysis is conducted. Moreover, capital structure of

organisation is made and mix of debt and equity is analysed. Recommendations to improve

capital structure are also provided along with business and financial risks are evaluated in a

better way. Hence, complete financial health analysis of company is done in effective manner.

PART A

A. Explaining the dividend irrelevancy theory and its assumption

It is a theory in which investors have no worry whether adequate dividend policy is

implemented by the company or not. It is because option is provided to them to sell off shares

held by them and as a result, cash is provided. This dividend policy is useful the firm as price

and cost of capital is not affected. This theory identifies that dividend policy is independent on

value and market price of shares. Assumption is made by the theory that markets are perfect and

stockholders' can build their policy by selling or purchasing stock in the markets (Jabbouri and

Attar, 2018). The theory indicates that if shareholders need the cash they can sell their shares,

and if they do not want in cash they can hold up their share with them. Brokerage fees are

exempted and the same is treated if capital gains are involved in this irrelevance theory.

Modigliani and Miller proposed that the dividend policy implemented by organization is

independent and do not influence share prices of organization. In this irrelevance theory of the

dividend MM proposed that when a shareholder attains dividend in excess than he has the option

to again invest the company's share in relation to cash flow (Kaur and Saraf, 2014). On contrary

to this, if dividend is small, it can be sold. In both the cases, investors are relevance. In both the

cases it is irrelevant because investors are creating their own cash.

Assumptions of the dividend irrelevant theory are as-

All sort of taxes is ignored (personal taxes, corporate taxes)

There is no flotation cost or transaction cost at the time when company is taking decision

of cost.

There is no impact on dividend policy, when a firm decides in capital budgeting.

All the investors have all the information about firm’s future

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Zero impact of leverage has on the cost of capital of the company (Baker and Jabbouri,

2016).

Argument in favor of the dividend irrelevant theory

This theory allows the perfect markets as it believes existence of it. Kaur and Saraf,

(2014) stated that investors behave rationally and as such, complete access with relation to

information is provided. Furthermore, flotation costs do not prevail. Both capital gains and

dividends are taxed at same rate due to absence of tax. In addressing this, investment policy is

fixed and no changes are made in it. Shareholders are certain regarding market price of shares in

the future. However, Jabbouri and Attar, (2018) argued that perfect market do not exist.

According to them in this theory, no difference is observed in between external and internal

funding. Therefore, it is uncertain to consider the flotation cost of new issues. They argued that

this theory believes that the wealth of company's shareholder does not affect dividends.

However, there are flotation cost prevails in relation to sell of shares to generate cash inflow.

They also object the no certainty is unrealistic. The theory holds mix empirical evidences and

proper conclusions are not drawn yet. This is because in real business scenario, organization

makes budget by taking into account dividends to be paid in more or less same manner which

they do for cash outflow like capital expenses, future need of cash, requirements for debt

services etc. Hence, constructive conclusions are yet to be drawn.

B. Explaining the dividend relevant theory

The Walter models

In accordance with the approaches based on this theory it can be said that there are no

differences in the dividend and investment policies. It identifies a clear relationship among the

cost of capital, internal rate of return and the return on investments. Therefore, it has the impacts

over the overall performance in firm as well as impacts over the market value.

Following are the assumption of Walter model:

There will be funding through retained earning expect various other external sources.

There will be consistency in the rate of return and the costs of capital in any investment. Consistency in various asset value of firm such as EPS and DPS.

Argument in favor of the dividend relevant theory

As per the views of Rafique and Javaid, (2017), Organization develops the policies and

procedure of making payments of dividends among the shareholders of the firm. Therefore, the

2016).

Argument in favor of the dividend irrelevant theory

This theory allows the perfect markets as it believes existence of it. Kaur and Saraf,

(2014) stated that investors behave rationally and as such, complete access with relation to

information is provided. Furthermore, flotation costs do not prevail. Both capital gains and

dividends are taxed at same rate due to absence of tax. In addressing this, investment policy is

fixed and no changes are made in it. Shareholders are certain regarding market price of shares in

the future. However, Jabbouri and Attar, (2018) argued that perfect market do not exist.

According to them in this theory, no difference is observed in between external and internal

funding. Therefore, it is uncertain to consider the flotation cost of new issues. They argued that

this theory believes that the wealth of company's shareholder does not affect dividends.

However, there are flotation cost prevails in relation to sell of shares to generate cash inflow.

They also object the no certainty is unrealistic. The theory holds mix empirical evidences and

proper conclusions are not drawn yet. This is because in real business scenario, organization

makes budget by taking into account dividends to be paid in more or less same manner which

they do for cash outflow like capital expenses, future need of cash, requirements for debt

services etc. Hence, constructive conclusions are yet to be drawn.

B. Explaining the dividend relevant theory

The Walter models

In accordance with the approaches based on this theory it can be said that there are no

differences in the dividend and investment policies. It identifies a clear relationship among the

cost of capital, internal rate of return and the return on investments. Therefore, it has the impacts

over the overall performance in firm as well as impacts over the market value.

Following are the assumption of Walter model:

There will be funding through retained earning expect various other external sources.

There will be consistency in the rate of return and the costs of capital in any investment. Consistency in various asset value of firm such as EPS and DPS.

Argument in favor of the dividend relevant theory

As per the views of Rafique and Javaid, (2017), Organization develops the policies and

procedure of making payments of dividends among the shareholders of the firm. Therefore, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

payment made by an organization to its shareholders will be in the form of cash. Therefore, these

are the plans which will be based on making the payments to investors on the basis of money

kept in firm and being used later. Similarly, as per analyzing the issues relevant with the facts

which insists that there have been changes in the dividend policies which in tur have the impacts

over the valuations. Thus, the investors do not find company profitable as the dividend payable

by them is not up to the satisfactory level. According to Ardalan, (2017), there have been

variations in the valuation as well as capital structure of the firm which will be balanced and

managed by the professionals in terms of making appropriate operational changes.

Signal and Clientele Effect theories:

This theory is based on variation in the market value of the organization with

consideration of the reforms held in taxation policies. Thus, the demands and aims of

shareholders will be based in the changing policies by government in relation with taxation.

Impacts of reforms in the company policies will have impacts over the changes in investors

perception and phenomenon regarding stock holdings, purchase and sale of the assets.

On the other side, analyzing assumption-based ion signaling theory which insists that the

dividends act as signal to perform the transactional activities in the industry and the in the capital

market (Hartanto, Paramita and Fathoni, 2018). However, the changes in the tax rates and

addition of various new policies will have impacts over the investors perception and thinking

relevant with the projects. Considering the impacts of Signaling theory which states that the rise

in the payout ratio of firm which benefits in estimating the rise in performance as well as the

value of common stock in the future. Reciprocate, if the reduction in the payouts which indicates

the downfall of performance and stock value as well. For example, Fisher Investments had been

affected in respect with fall in the dividend payouts which has created the market risk regarding

investment of stock (John, Okelo and Chesang, 2017).

Similarly, Clientele effects had been seen by organization Winn-Dixie Stores Inc. which

announces to slash its 1.02 annual dividends. Therefore, there are various impacts incurred which

creates the changes in the operations.

Assumptions of Signal and Clientele Effect:

It has been assumed here that the government variation in the taxation polices will have

impacts on the market value of firm.

are the plans which will be based on making the payments to investors on the basis of money

kept in firm and being used later. Similarly, as per analyzing the issues relevant with the facts

which insists that there have been changes in the dividend policies which in tur have the impacts

over the valuations. Thus, the investors do not find company profitable as the dividend payable

by them is not up to the satisfactory level. According to Ardalan, (2017), there have been

variations in the valuation as well as capital structure of the firm which will be balanced and

managed by the professionals in terms of making appropriate operational changes.

Signal and Clientele Effect theories:

This theory is based on variation in the market value of the organization with

consideration of the reforms held in taxation policies. Thus, the demands and aims of

shareholders will be based in the changing policies by government in relation with taxation.

Impacts of reforms in the company policies will have impacts over the changes in investors

perception and phenomenon regarding stock holdings, purchase and sale of the assets.

On the other side, analyzing assumption-based ion signaling theory which insists that the

dividends act as signal to perform the transactional activities in the industry and the in the capital

market (Hartanto, Paramita and Fathoni, 2018). However, the changes in the tax rates and

addition of various new policies will have impacts over the investors perception and thinking

relevant with the projects. Considering the impacts of Signaling theory which states that the rise

in the payout ratio of firm which benefits in estimating the rise in performance as well as the

value of common stock in the future. Reciprocate, if the reduction in the payouts which indicates

the downfall of performance and stock value as well. For example, Fisher Investments had been

affected in respect with fall in the dividend payouts which has created the market risk regarding

investment of stock (John, Okelo and Chesang, 2017).

Similarly, Clientele effects had been seen by organization Winn-Dixie Stores Inc. which

announces to slash its 1.02 annual dividends. Therefore, there are various impacts incurred which

creates the changes in the operations.

Assumptions of Signal and Clientele Effect:

It has been assumed here that the government variation in the taxation polices will have

impacts on the market value of firm.

There will be variation in the investors’ perceptions regarding company’s dividend

policies.

Gordon Model

Bird in the hand theory is provided by Gorden / Lintner which states that dividend and

organization's value are interdependent. It means that value of firm is affected when lower

dividends are paid and vice-versa. He postulated that cost of equity which is financed by

organization is nothing but has to be paid to shareholders on perpetuity basis. Annual increment

of dividends and share price on current basis.

Assumptions of theory are as follows-

The firm has no debt in its capital structure.

To finance any expansion of the business, consequently retained earnings are used and no

external information is available. Investment's marginal efficiency does not take into account constant return on

investment.

Argument in favour of the dividend relevant theory

Oyinlola and Ajeigbe, (2014) assessed in their study that the relevance theory has the

benefits as this theory restricts the debt. The theory assumes that the company is an all equity

company, with no proportion of debt in the capital structure. In this no external finance is

required all the investment made with the help of retained earnings, it provides the constant

internal rate of return by ignoring the diminishing marginal efficiency of the investment. The

cost of capital is also constant. The relevant theory provides the perpetual earnings. Rafique and

Javaid, (2017) criticized that the constant internal rate of return, they say that this model is

inaccurate in assuming that r and k always remain constant. Constant of rate means in that the

wealth of the shareholders is not optimized. They also argued for the no external financing, as

they believed that this reflects the sub-optimum investment and dividend policies.

C. Summary based on comparison among theories

Comparing both the theories such as relevance and irrelevance theories on dividend

policies on which it can be said that in irrelevant theories there will be appropriate ascertainment

of the operations which are consists of the thinking is that there is no affect of dividend polices

ion the decision making of the professionals as well as resining the market share of entity. On the

policies.

Gordon Model

Bird in the hand theory is provided by Gorden / Lintner which states that dividend and

organization's value are interdependent. It means that value of firm is affected when lower

dividends are paid and vice-versa. He postulated that cost of equity which is financed by

organization is nothing but has to be paid to shareholders on perpetuity basis. Annual increment

of dividends and share price on current basis.

Assumptions of theory are as follows-

The firm has no debt in its capital structure.

To finance any expansion of the business, consequently retained earnings are used and no

external information is available. Investment's marginal efficiency does not take into account constant return on

investment.

Argument in favour of the dividend relevant theory

Oyinlola and Ajeigbe, (2014) assessed in their study that the relevance theory has the

benefits as this theory restricts the debt. The theory assumes that the company is an all equity

company, with no proportion of debt in the capital structure. In this no external finance is

required all the investment made with the help of retained earnings, it provides the constant

internal rate of return by ignoring the diminishing marginal efficiency of the investment. The

cost of capital is also constant. The relevant theory provides the perpetual earnings. Rafique and

Javaid, (2017) criticized that the constant internal rate of return, they say that this model is

inaccurate in assuming that r and k always remain constant. Constant of rate means in that the

wealth of the shareholders is not optimized. They also argued for the no external financing, as

they believed that this reflects the sub-optimum investment and dividend policies.

C. Summary based on comparison among theories

Comparing both the theories such as relevance and irrelevance theories on dividend

policies on which it can be said that in irrelevant theories there will be appropriate ascertainment

of the operations which are consists of the thinking is that there is no affect of dividend polices

ion the decision making of the professionals as well as resining the market share of entity. On the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other side, as per considering the relevant theories where the Walter model insist that there will

be impacts over firm’s value as per the plans and polices planned by the professionals.

PART B

A) Financial performance of company using indicators

Company background:

Analysing the financial performance of the organisation on which analysing its various

efficiencies based on profitability, liquidity, efficiencies and solvency will be addressed. Glaxo

Smith Kline is the most successful pharmaceutical business of UK which serves and produces

various medicines or drugs that helps patients in overcoming with the life-threatening diseases. It

has the net income as per the survey 2017 as 2.169 billion pounds (Qiu and Scrivens, 2018). It

served the drugs all over the world which brings the suitable revenue generation to the entity. It

will be helpful or attractive to investors as per analysing the financial stability of the organisation

in the due period.

RATIOS 2017

£

2016

£

2015

£

2014

£

2013

£

Net Profit

Margin

Net

Profit/Revenu

e

percentage

2,169/

30186

7.19%

1,062/

27889

3.80%

8,372/

23,923

35.0%

2,832/

23,006

12.31%

5,628/

26,505

21.23%

Current Ratio

Current

Assets/Curren

t Liabilities

15,907/

26569

0.60

16,711/

19,001

0.88

16,587/

13,417

1.24

14,678/

13,295

1.10

15,227/

13,667

1.11

Inventory

Turnover

Ratio

Cost of

Sales/Average

Inventory

10,342/

(5102+5557)/

2

1.9 times

9,290/

(4716+5102)/

2

1.89 times

8,853/

(4231+4716)/

2

1.98 times

7,323/

(3900+4231)/

2

1.80 times

8,585/

(3969+3900)/

2

2.18 times

be impacts over firm’s value as per the plans and polices planned by the professionals.

PART B

A) Financial performance of company using indicators

Company background:

Analysing the financial performance of the organisation on which analysing its various

efficiencies based on profitability, liquidity, efficiencies and solvency will be addressed. Glaxo

Smith Kline is the most successful pharmaceutical business of UK which serves and produces

various medicines or drugs that helps patients in overcoming with the life-threatening diseases. It

has the net income as per the survey 2017 as 2.169 billion pounds (Qiu and Scrivens, 2018). It

served the drugs all over the world which brings the suitable revenue generation to the entity. It

will be helpful or attractive to investors as per analysing the financial stability of the organisation

in the due period.

RATIOS 2017

£

2016

£

2015

£

2014

£

2013

£

Net Profit

Margin

Net

Profit/Revenu

e

percentage

2,169/

30186

7.19%

1,062/

27889

3.80%

8,372/

23,923

35.0%

2,832/

23,006

12.31%

5,628/

26,505

21.23%

Current Ratio

Current

Assets/Curren

t Liabilities

15,907/

26569

0.60

16,711/

19,001

0.88

16,587/

13,417

1.24

14,678/

13,295

1.10

15,227/

13,667

1.11

Inventory

Turnover

Ratio

Cost of

Sales/Average

Inventory

10,342/

(5102+5557)/

2

1.9 times

9,290/

(4716+5102)/

2

1.89 times

8,853/

(4231+4716)/

2

1.98 times

7,323/

(3900+4231)/

2

1.80 times

8,585/

(3969+3900)/

2

2.18 times

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EPS (Taken

from GSK

Annual

Report)

31.40 18.80 174.30 57.30 112.50

Debt to Equity

Ratio

Total

Debt/Equity

52,897/

3,489

15.16:1

54,118/

4,963

10.90:1

44,568/

8,878

5.02:1

35,715/

4,936

7.24:1

34,274/

7,812

4.39:1

Interest Cover

Ratio

Operating

Profit/Interest

Expense

4,087/

669

5.9 times

2,598/

664

4 times

10,322/

653

16 times

3,597/

659

5.5 times

7,028/

706

10 times

The above financial ratios are computed showing financial performance of GSK Plc in

the past financial years such as 2013, 2014, 2015, 2016 and 2017. Ratios are computed for

analysing profitability, liquidity, efficiency, investment in effective manner. These are required

to be computed so as to evaluate overall health of GSK Plc in the best possible manner ( Hamid

and Akhi, 2016).

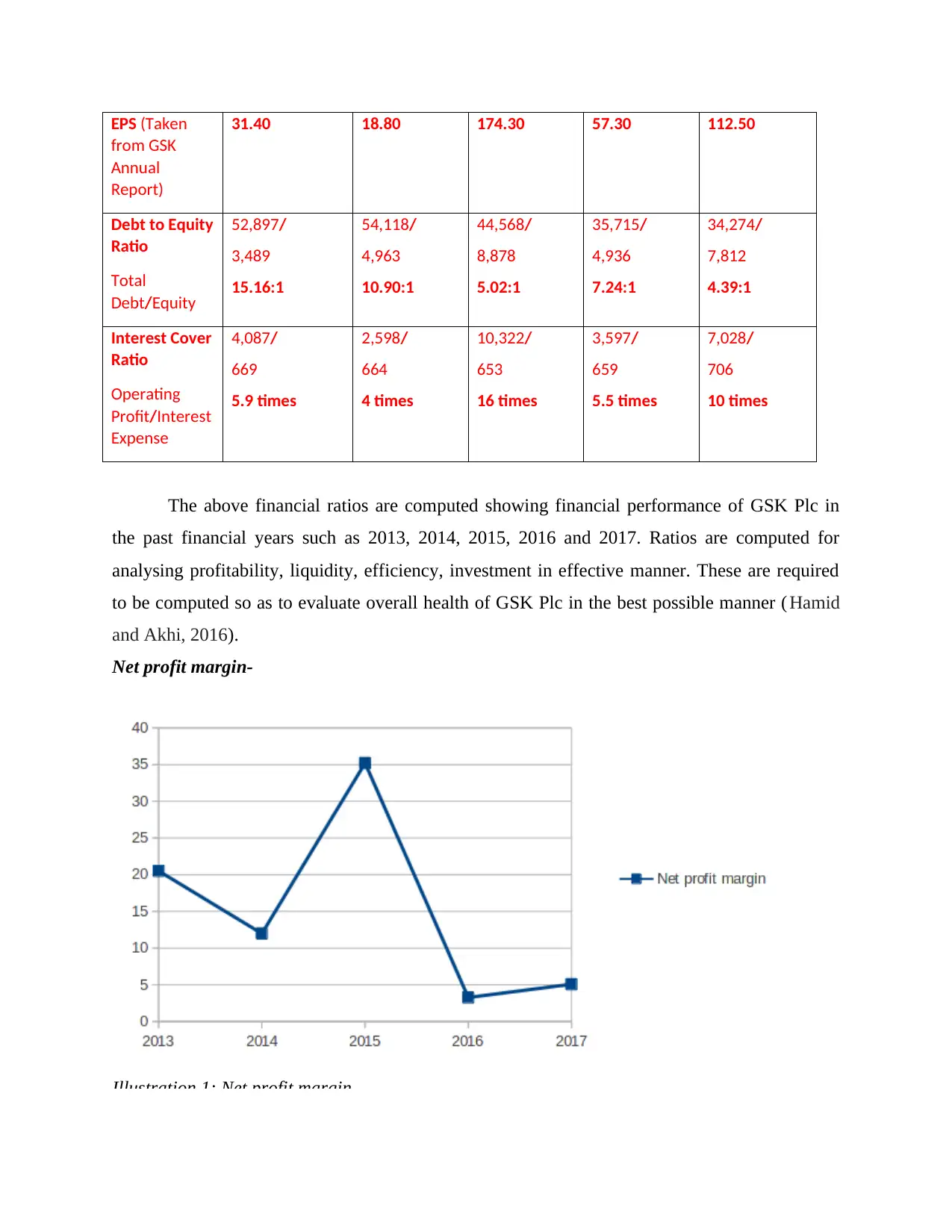

Net profit margin-

Illustration 1: Net profit margin

from GSK

Annual

Report)

31.40 18.80 174.30 57.30 112.50

Debt to Equity

Ratio

Total

Debt/Equity

52,897/

3,489

15.16:1

54,118/

4,963

10.90:1

44,568/

8,878

5.02:1

35,715/

4,936

7.24:1

34,274/

7,812

4.39:1

Interest Cover

Ratio

Operating

Profit/Interest

Expense

4,087/

669

5.9 times

2,598/

664

4 times

10,322/

653

16 times

3,597/

659

5.5 times

7,028/

706

10 times

The above financial ratios are computed showing financial performance of GSK Plc in

the past financial years such as 2013, 2014, 2015, 2016 and 2017. Ratios are computed for

analysing profitability, liquidity, efficiency, investment in effective manner. These are required

to be computed so as to evaluate overall health of GSK Plc in the best possible manner ( Hamid

and Akhi, 2016).

Net profit margin-

Illustration 1: Net profit margin

It can be analysed that profitability aspect such as net profit margin was 21.23% in 2013,

it decreased in 2014 as it came to 12.31%. However, trend in 2015 was good because net profit

increased to 35.0% which was all time for organization. It was high in 2015 because net profit

was much higher in the year as compared to other years. Furthermore, operational and non-

operational expenses are alleviated which had increased net profit and ratio was increased as

well. It significantly decreased in 2016 to 3.80% and furthermore, increased to 7.19% in 2017. It

can be interpreted that firm need to initiate control on operating and non-operating expenditures

so as to maximise earnings (Annual Report GSK. 2017).

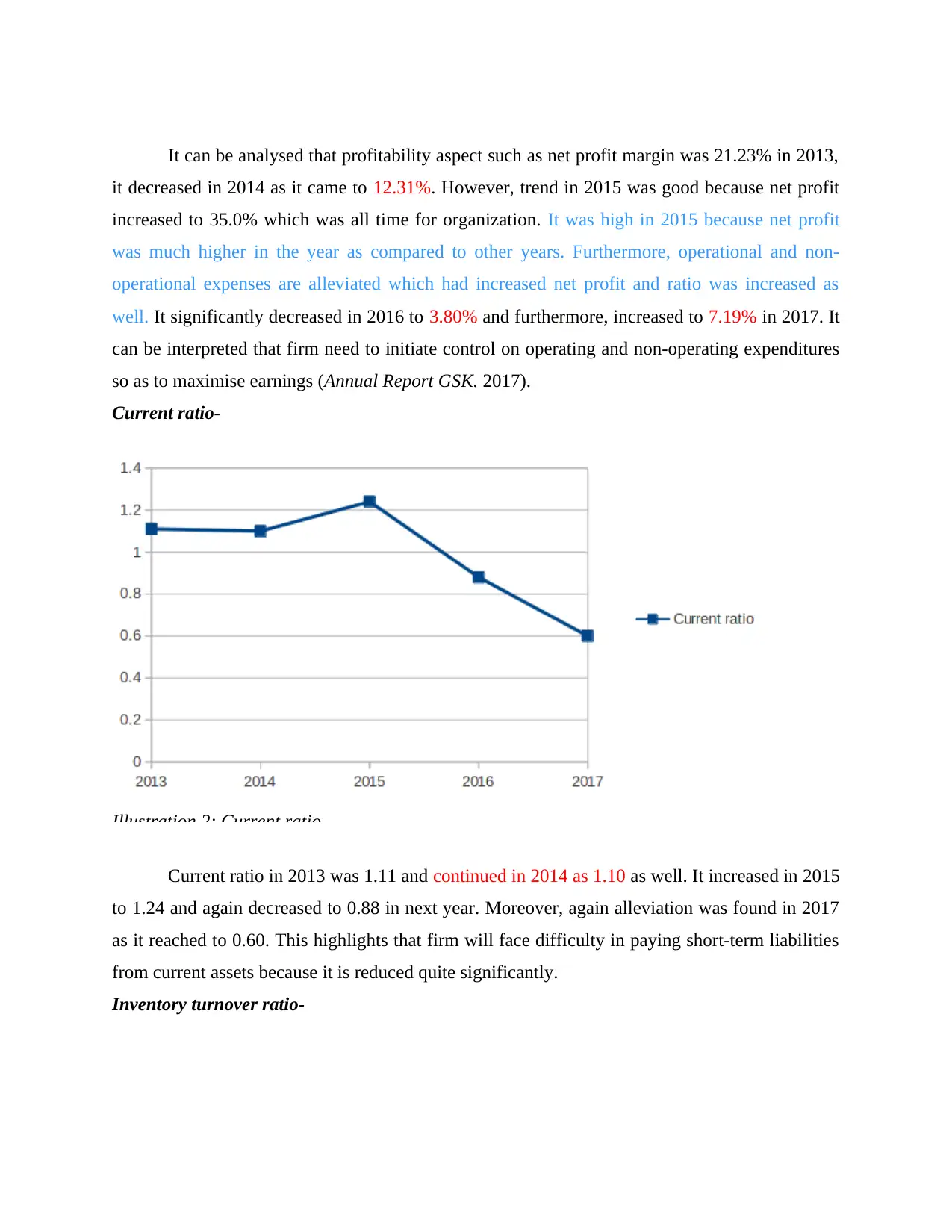

Current ratio-

Illustration 2: Current ratio

Current ratio in 2013 was 1.11 and continued in 2014 as 1.10 as well. It increased in 2015

to 1.24 and again decreased to 0.88 in next year. Moreover, again alleviation was found in 2017

as it reached to 0.60. This highlights that firm will face difficulty in paying short-term liabilities

from current assets because it is reduced quite significantly.

Inventory turnover ratio-

it decreased in 2014 as it came to 12.31%. However, trend in 2015 was good because net profit

increased to 35.0% which was all time for organization. It was high in 2015 because net profit

was much higher in the year as compared to other years. Furthermore, operational and non-

operational expenses are alleviated which had increased net profit and ratio was increased as

well. It significantly decreased in 2016 to 3.80% and furthermore, increased to 7.19% in 2017. It

can be interpreted that firm need to initiate control on operating and non-operating expenditures

so as to maximise earnings (Annual Report GSK. 2017).

Current ratio-

Illustration 2: Current ratio

Current ratio in 2013 was 1.11 and continued in 2014 as 1.10 as well. It increased in 2015

to 1.24 and again decreased to 0.88 in next year. Moreover, again alleviation was found in 2017

as it reached to 0.60. This highlights that firm will face difficulty in paying short-term liabilities

from current assets because it is reduced quite significantly.

Inventory turnover ratio-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

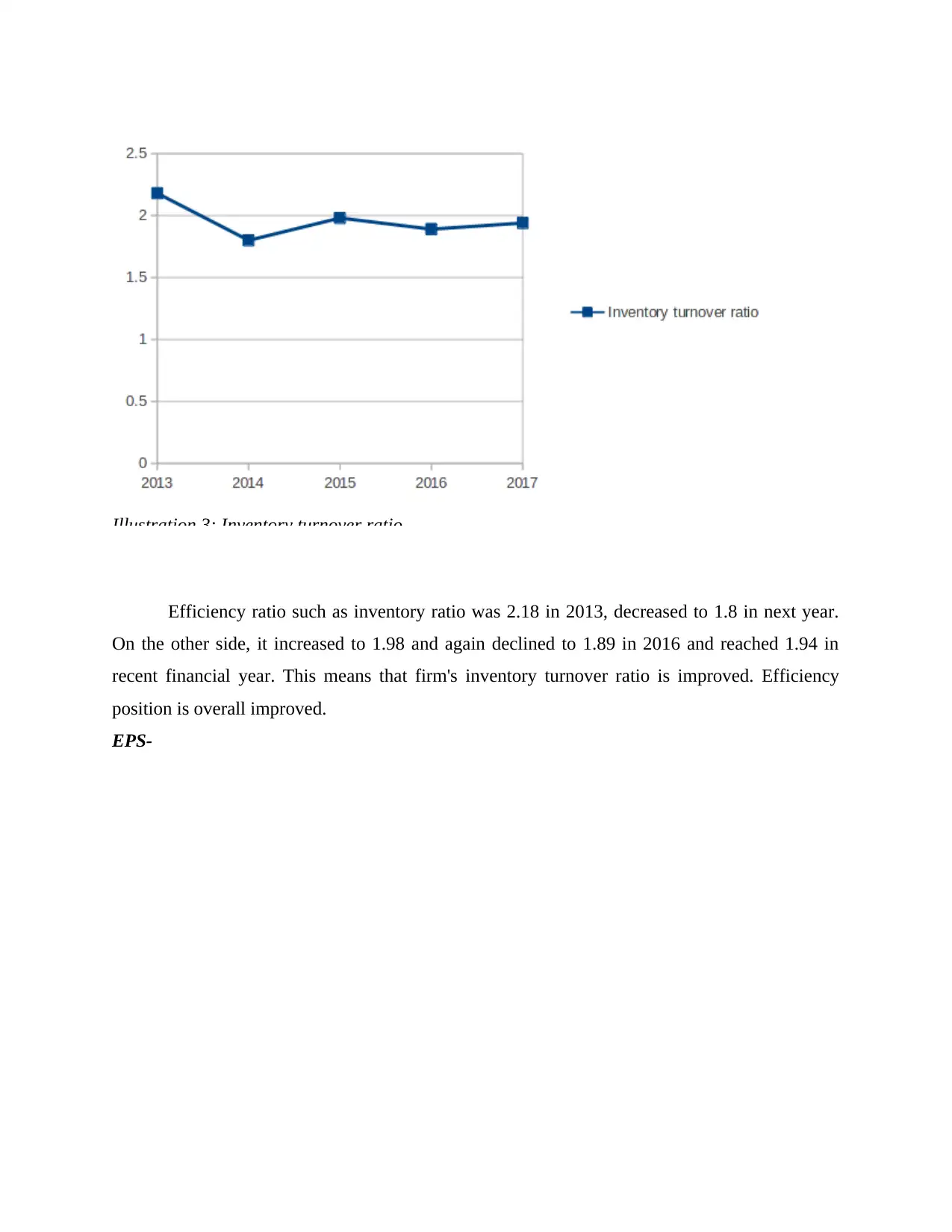

Illustration 3: Inventory turnover ratio

Efficiency ratio such as inventory ratio was 2.18 in 2013, decreased to 1.8 in next year.

On the other side, it increased to 1.98 and again declined to 1.89 in 2016 and reached 1.94 in

recent financial year. This means that firm's inventory turnover ratio is improved. Efficiency

position is overall improved.

EPS-

Efficiency ratio such as inventory ratio was 2.18 in 2013, decreased to 1.8 in next year.

On the other side, it increased to 1.98 and again declined to 1.89 in 2016 and reached 1.94 in

recent financial year. This means that firm's inventory turnover ratio is improved. Efficiency

position is overall improved.

EPS-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

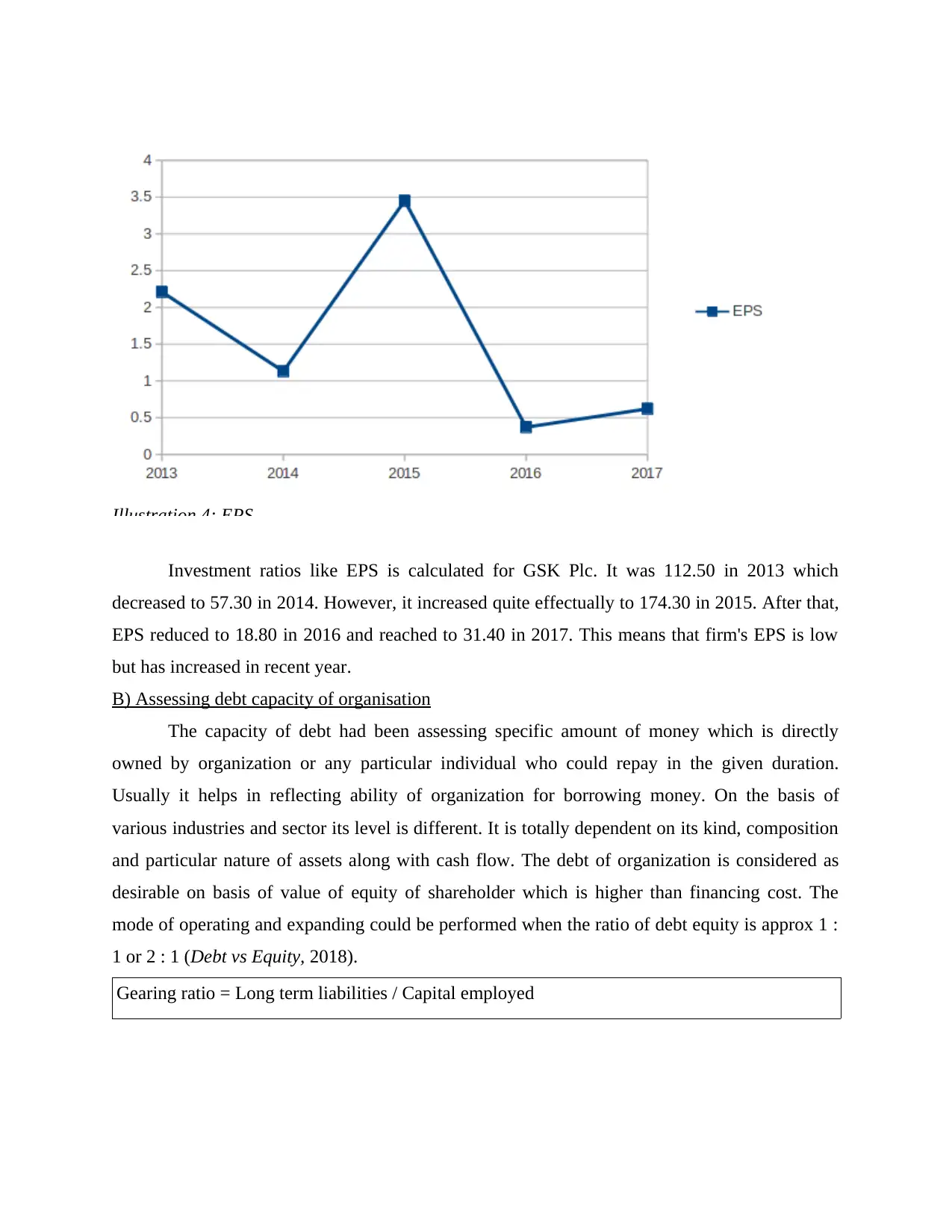

Illustration 4: EPS

Investment ratios like EPS is calculated for GSK Plc. It was 112.50 in 2013 which

decreased to 57.30 in 2014. However, it increased quite effectually to 174.30 in 2015. After that,

EPS reduced to 18.80 in 2016 and reached to 31.40 in 2017. This means that firm's EPS is low

but has increased in recent year.

B) Assessing debt capacity of organisation

The capacity of debt had been assessing specific amount of money which is directly

owned by organization or any particular individual who could repay in the given duration.

Usually it helps in reflecting ability of organization for borrowing money. On the basis of

various industries and sector its level is different. It is totally dependent on its kind, composition

and particular nature of assets along with cash flow. The debt of organization is considered as

desirable on basis of value of equity of shareholder which is higher than financing cost. The

mode of operating and expanding could be performed when the ratio of debt equity is approx 1 :

1 or 2 : 1 (Debt vs Equity, 2018).

Gearing ratio = Long term liabilities / Capital employed

Investment ratios like EPS is calculated for GSK Plc. It was 112.50 in 2013 which

decreased to 57.30 in 2014. However, it increased quite effectually to 174.30 in 2015. After that,

EPS reduced to 18.80 in 2016 and reached to 31.40 in 2017. This means that firm's EPS is low

but has increased in recent year.

B) Assessing debt capacity of organisation

The capacity of debt had been assessing specific amount of money which is directly

owned by organization or any particular individual who could repay in the given duration.

Usually it helps in reflecting ability of organization for borrowing money. On the basis of

various industries and sector its level is different. It is totally dependent on its kind, composition

and particular nature of assets along with cash flow. The debt of organization is considered as

desirable on basis of value of equity of shareholder which is higher than financing cost. The

mode of operating and expanding could be performed when the ratio of debt equity is approx 1 :

1 or 2 : 1 (Debt vs Equity, 2018).

Gearing ratio = Long term liabilities / Capital employed

2013 2014 2015 2016 2017

-250.00

-200.00

-150.00

-100.00

-50.00

0.00

50.00

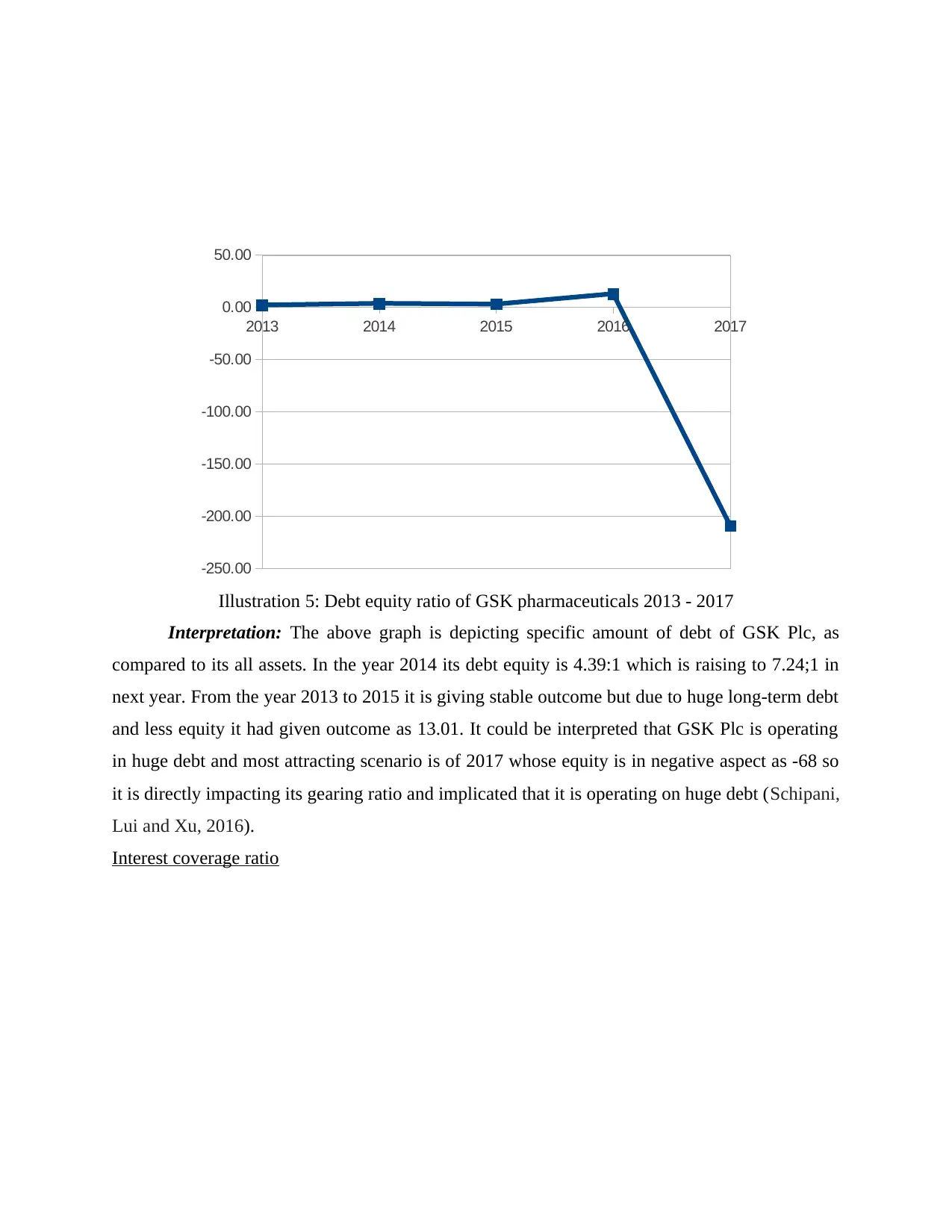

Illustration 5: Debt equity ratio of GSK pharmaceuticals 2013 - 2017

Interpretation: The above graph is depicting specific amount of debt of GSK Plc, as

compared to its all assets. In the year 2014 its debt equity is 4.39:1 which is raising to 7.24;1 in

next year. From the year 2013 to 2015 it is giving stable outcome but due to huge long-term debt

and less equity it had given outcome as 13.01. It could be interpreted that GSK Plc is operating

in huge debt and most attracting scenario is of 2017 whose equity is in negative aspect as -68 so

it is directly impacting its gearing ratio and implicated that it is operating on huge debt (Schipani,

Lui and Xu, 2016).

Interest coverage ratio

-250.00

-200.00

-150.00

-100.00

-50.00

0.00

50.00

Illustration 5: Debt equity ratio of GSK pharmaceuticals 2013 - 2017

Interpretation: The above graph is depicting specific amount of debt of GSK Plc, as

compared to its all assets. In the year 2014 its debt equity is 4.39:1 which is raising to 7.24;1 in

next year. From the year 2013 to 2015 it is giving stable outcome but due to huge long-term debt

and less equity it had given outcome as 13.01. It could be interpreted that GSK Plc is operating

in huge debt and most attracting scenario is of 2017 whose equity is in negative aspect as -68 so

it is directly impacting its gearing ratio and implicated that it is operating on huge debt (Schipani,

Lui and Xu, 2016).

Interest coverage ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.