Weighted Average Cost of Capital (WACC) and Financial Analysis of GSK

VerifiedAdded on 2020/03/23

|25

|5958

|46

Report

AI Summary

This report provides a comprehensive financial analysis of GlaxoSmithKline (GSK), focusing on the calculation and interpretation of its Weighted Average Cost of Capital (WACC). The analysis utilizes financial statements, including balance sheets, income statements, and cash flow statements, from 2012 to 2016 to determine the WACC using different methodologies. The report examines the impact of borrowed funds, equity funds, and dividend payments on the cost of capital, comparing results based on current year figures, five-year averages, and cash outflow data. The report also includes a financial analysis of GSK's performance, including profitability, liquidity, and solvency ratios, and discusses the implications of the findings for the company's financial health and future performance. The report highlights the importance of assumptions and their impact on the WACC calculation and concludes with a best judgment for the company's WACC based on the provided financial data.

Running Head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note

Finance

Name of the Student:

Name of the University:

Authors Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Stage 1:............................................................................................................................................2

Stage 2:............................................................................................................................................9

Stage 3:..........................................................................................................................................17

References:....................................................................................................................................22

Table of Contents

Stage 1:............................................................................................................................................2

Stage 2:............................................................................................................................................9

Stage 3:..........................................................................................................................................17

References:....................................................................................................................................22

2FINANCE

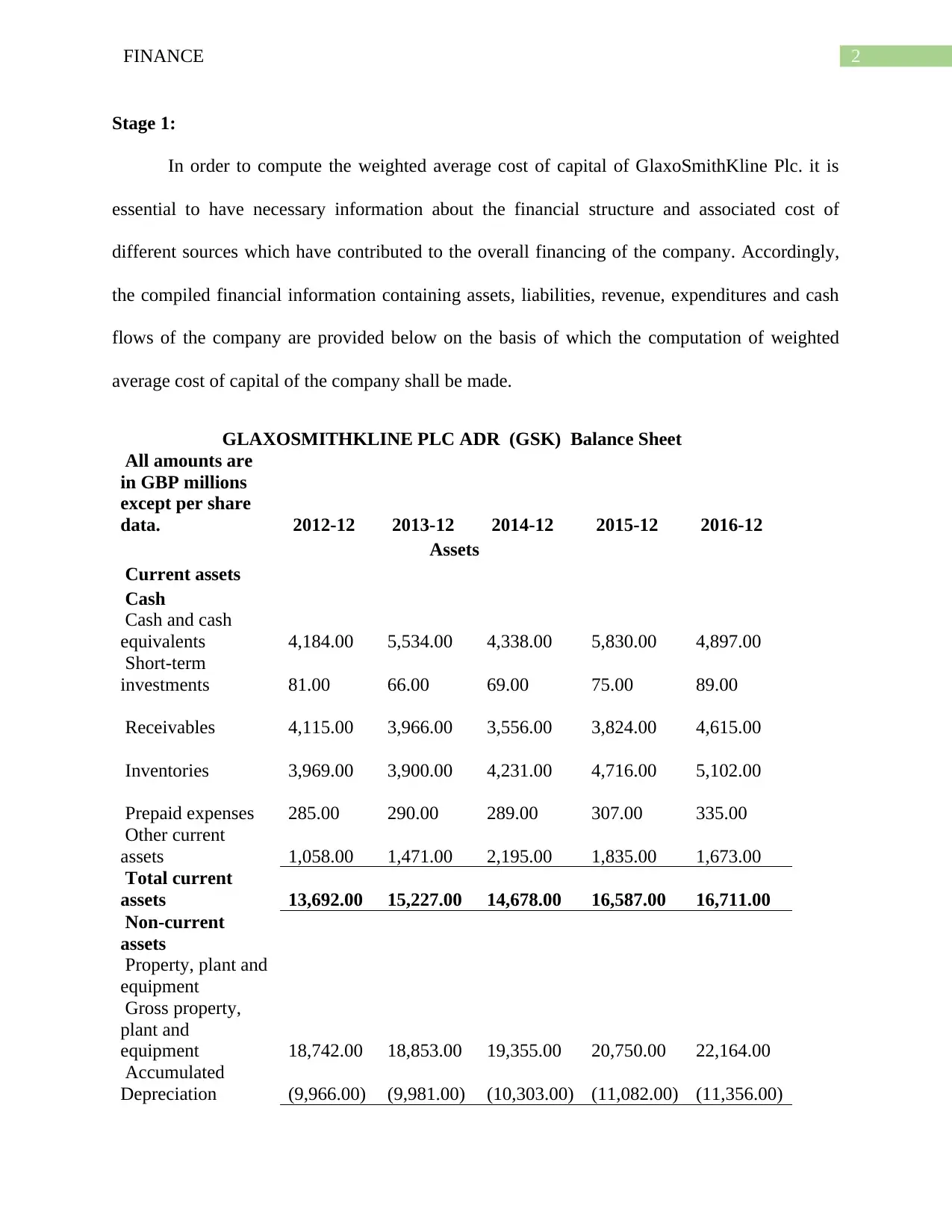

Stage 1:

In order to compute the weighted average cost of capital of GlaxoSmithKline Plc. it is

essential to have necessary information about the financial structure and associated cost of

different sources which have contributed to the overall financing of the company. Accordingly,

the compiled financial information containing assets, liabilities, revenue, expenditures and cash

flows of the company are provided below on the basis of which the computation of weighted

average cost of capital of the company shall be made.

GLAXOSMITHKLINE PLC ADR (GSK) Balance Sheet

All amounts are

in GBP millions

except per share

data. 2012-12 2013-12 2014-12 2015-12 2016-12

Assets

Current assets

Cash

Cash and cash

equivalents 4,184.00 5,534.00 4,338.00 5,830.00 4,897.00

Short-term

investments 81.00 66.00 69.00 75.00 89.00

Receivables 4,115.00 3,966.00 3,556.00 3,824.00 4,615.00

Inventories 3,969.00 3,900.00 4,231.00 4,716.00 5,102.00

Prepaid expenses 285.00 290.00 289.00 307.00 335.00

Other current

assets 1,058.00 1,471.00 2,195.00 1,835.00 1,673.00

Total current

assets 13,692.00 15,227.00 14,678.00 16,587.00 16,711.00

Non-current

assets

Property, plant and

equipment

Gross property,

plant and

equipment 18,742.00 18,853.00 19,355.00 20,750.00 22,164.00

Accumulated

Depreciation (9,966.00) (9,981.00) (10,303.00) (11,082.00) (11,356.00)

Stage 1:

In order to compute the weighted average cost of capital of GlaxoSmithKline Plc. it is

essential to have necessary information about the financial structure and associated cost of

different sources which have contributed to the overall financing of the company. Accordingly,

the compiled financial information containing assets, liabilities, revenue, expenditures and cash

flows of the company are provided below on the basis of which the computation of weighted

average cost of capital of the company shall be made.

GLAXOSMITHKLINE PLC ADR (GSK) Balance Sheet

All amounts are

in GBP millions

except per share

data. 2012-12 2013-12 2014-12 2015-12 2016-12

Assets

Current assets

Cash

Cash and cash

equivalents 4,184.00 5,534.00 4,338.00 5,830.00 4,897.00

Short-term

investments 81.00 66.00 69.00 75.00 89.00

Receivables 4,115.00 3,966.00 3,556.00 3,824.00 4,615.00

Inventories 3,969.00 3,900.00 4,231.00 4,716.00 5,102.00

Prepaid expenses 285.00 290.00 289.00 307.00 335.00

Other current

assets 1,058.00 1,471.00 2,195.00 1,835.00 1,673.00

Total current

assets 13,692.00 15,227.00 14,678.00 16,587.00 16,711.00

Non-current

assets

Property, plant and

equipment

Gross property,

plant and

equipment 18,742.00 18,853.00 19,355.00 20,750.00 22,164.00

Accumulated

Depreciation (9,966.00) (9,981.00) (10,303.00) (11,082.00) (11,356.00)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

Net property,

plant and

equipment 8,776.00 8,872.00 9,052.00 9,668.00 10,808.00

Equity and other

investments 1,366.00 1,525.00 1,454.00 1,462.00 1,248.00

Goodwill 4,359.00 4,205.00 3,724.00 5,162.00 5,965.00

Intangible assets 10,161.00 9,283.00 8,320.00 16,672.00 18,776.00

Deferred income

taxes 2,385.00 2,084.00 2,688.00 2,905.00 4,374.00

Prepaid pension

benefit 93.00

Other long-term

assets 736.00 890.00 642.00 990.00 1,199.00

Total non-current

assets 27,783.00 26,859.00 25,973.00 36,859.00 42,370.00

Total assets 41,475.00 42,086.00 40,651.00 53,446.00 59,081.00

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 3,631.00 2,789.00 2,943.00 1,308.00 4,129.00

Accounts payable 2,666.00 2,739.00 2,790.00 3,120.00 3,596.00

Taxes payable 1,374.00 1,452.00 945.00 1,421.00 1,305.00

Accrued liabilities 4,233.00 2,797.00 4,609.00 5,206.00 6,324.00

Deferred revenues 162.00 167.00 62.00 73.00 158.00

Other current

liabilities 1,749.00 3,733.00 1,946.00 2,289.00 3,489.00

Total current

liabilities 13,815.00 13,677.00 13,295.00 13,417.00 19,001.00

Non-current

liabilities

Long-term debt 14,671.00 15,456.00 15,841.00 15,324.00 14,661.00

Deferred taxes

liabilities 1,004.00 693.00 445.00 1,522.00 1,934.00

Deferred revenues 64.00 66.00

Pensions and other

benefits 3,105.00 2,189.00 3,179.00 3,229.00 4,090.00

Net property,

plant and

equipment 8,776.00 8,872.00 9,052.00 9,668.00 10,808.00

Equity and other

investments 1,366.00 1,525.00 1,454.00 1,462.00 1,248.00

Goodwill 4,359.00 4,205.00 3,724.00 5,162.00 5,965.00

Intangible assets 10,161.00 9,283.00 8,320.00 16,672.00 18,776.00

Deferred income

taxes 2,385.00 2,084.00 2,688.00 2,905.00 4,374.00

Prepaid pension

benefit 93.00

Other long-term

assets 736.00 890.00 642.00 990.00 1,199.00

Total non-current

assets 27,783.00 26,859.00 25,973.00 36,859.00 42,370.00

Total assets 41,475.00 42,086.00 40,651.00 53,446.00 59,081.00

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 3,631.00 2,789.00 2,943.00 1,308.00 4,129.00

Accounts payable 2,666.00 2,739.00 2,790.00 3,120.00 3,596.00

Taxes payable 1,374.00 1,452.00 945.00 1,421.00 1,305.00

Accrued liabilities 4,233.00 2,797.00 4,609.00 5,206.00 6,324.00

Deferred revenues 162.00 167.00 62.00 73.00 158.00

Other current

liabilities 1,749.00 3,733.00 1,946.00 2,289.00 3,489.00

Total current

liabilities 13,815.00 13,677.00 13,295.00 13,417.00 19,001.00

Non-current

liabilities

Long-term debt 14,671.00 15,456.00 15,841.00 15,324.00 14,661.00

Deferred taxes

liabilities 1,004.00 693.00 445.00 1,522.00 1,934.00

Deferred revenues 64.00 66.00

Pensions and other

benefits 3,105.00 2,189.00 3,179.00 3,229.00 4,090.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

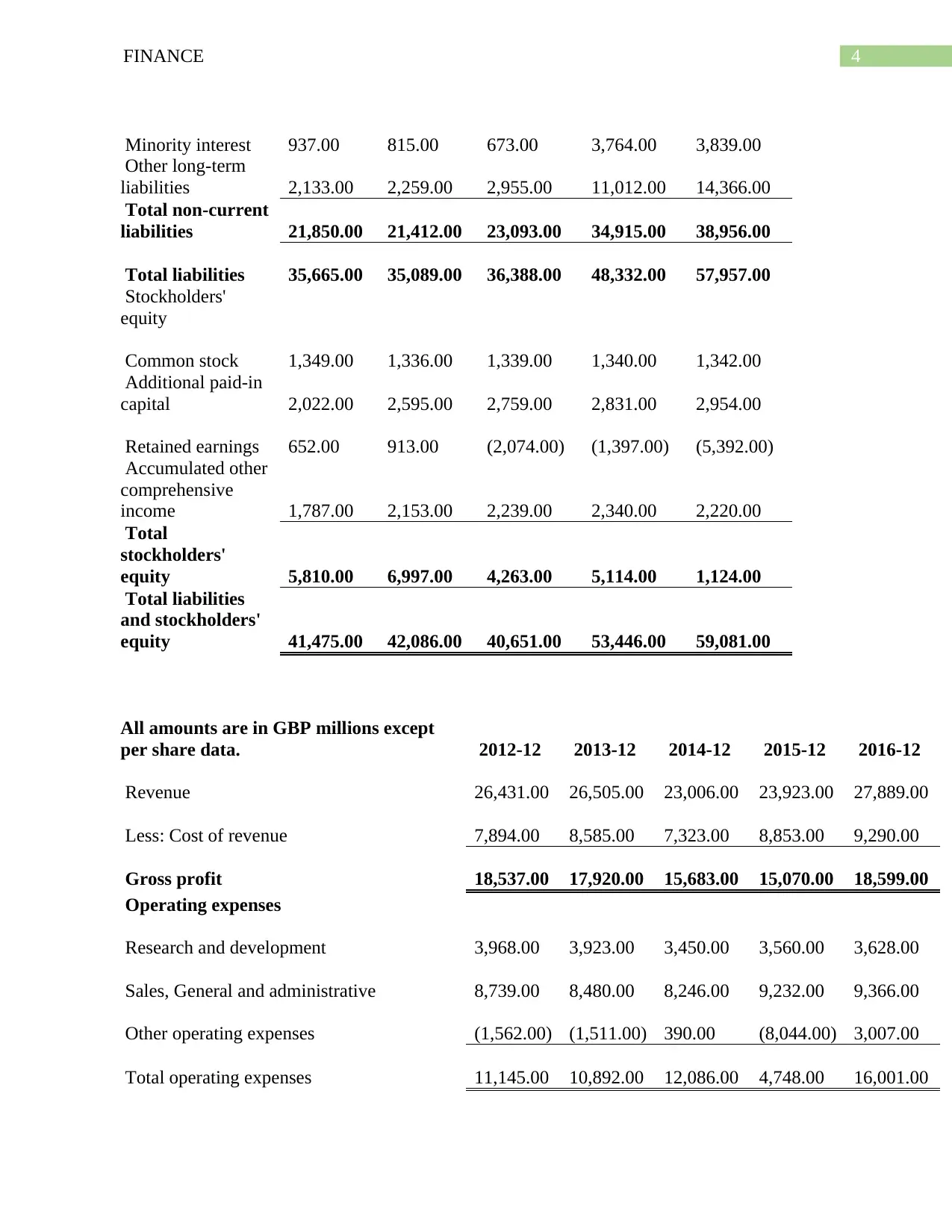

Minority interest 937.00 815.00 673.00 3,764.00 3,839.00

Other long-term

liabilities 2,133.00 2,259.00 2,955.00 11,012.00 14,366.00

Total non-current

liabilities 21,850.00 21,412.00 23,093.00 34,915.00 38,956.00

Total liabilities 35,665.00 35,089.00 36,388.00 48,332.00 57,957.00

Stockholders'

equity

Common stock 1,349.00 1,336.00 1,339.00 1,340.00 1,342.00

Additional paid-in

capital 2,022.00 2,595.00 2,759.00 2,831.00 2,954.00

Retained earnings 652.00 913.00 (2,074.00) (1,397.00) (5,392.00)

Accumulated other

comprehensive

income 1,787.00 2,153.00 2,239.00 2,340.00 2,220.00

Total

stockholders'

equity 5,810.00 6,997.00 4,263.00 5,114.00 1,124.00

Total liabilities

and stockholders'

equity 41,475.00 42,086.00 40,651.00 53,446.00 59,081.00

All amounts are in GBP millions except

per share data. 2012-12 2013-12 2014-12 2015-12 2016-12

Revenue 26,431.00 26,505.00 23,006.00 23,923.00 27,889.00

Less: Cost of revenue 7,894.00 8,585.00 7,323.00 8,853.00 9,290.00

Gross profit 18,537.00 17,920.00 15,683.00 15,070.00 18,599.00

Operating expenses

Research and development 3,968.00 3,923.00 3,450.00 3,560.00 3,628.00

Sales, General and administrative 8,739.00 8,480.00 8,246.00 9,232.00 9,366.00

Other operating expenses (1,562.00) (1,511.00) 390.00 (8,044.00) 3,007.00

Total operating expenses 11,145.00 10,892.00 12,086.00 4,748.00 16,001.00

Minority interest 937.00 815.00 673.00 3,764.00 3,839.00

Other long-term

liabilities 2,133.00 2,259.00 2,955.00 11,012.00 14,366.00

Total non-current

liabilities 21,850.00 21,412.00 23,093.00 34,915.00 38,956.00

Total liabilities 35,665.00 35,089.00 36,388.00 48,332.00 57,957.00

Stockholders'

equity

Common stock 1,349.00 1,336.00 1,339.00 1,340.00 1,342.00

Additional paid-in

capital 2,022.00 2,595.00 2,759.00 2,831.00 2,954.00

Retained earnings 652.00 913.00 (2,074.00) (1,397.00) (5,392.00)

Accumulated other

comprehensive

income 1,787.00 2,153.00 2,239.00 2,340.00 2,220.00

Total

stockholders'

equity 5,810.00 6,997.00 4,263.00 5,114.00 1,124.00

Total liabilities

and stockholders'

equity 41,475.00 42,086.00 40,651.00 53,446.00 59,081.00

All amounts are in GBP millions except

per share data. 2012-12 2013-12 2014-12 2015-12 2016-12

Revenue 26,431.00 26,505.00 23,006.00 23,923.00 27,889.00

Less: Cost of revenue 7,894.00 8,585.00 7,323.00 8,853.00 9,290.00

Gross profit 18,537.00 17,920.00 15,683.00 15,070.00 18,599.00

Operating expenses

Research and development 3,968.00 3,923.00 3,450.00 3,560.00 3,628.00

Sales, General and administrative 8,739.00 8,480.00 8,246.00 9,232.00 9,366.00

Other operating expenses (1,562.00) (1,511.00) 390.00 (8,044.00) 3,007.00

Total operating expenses 11,145.00 10,892.00 12,086.00 4,748.00 16,001.00

5FINANCE

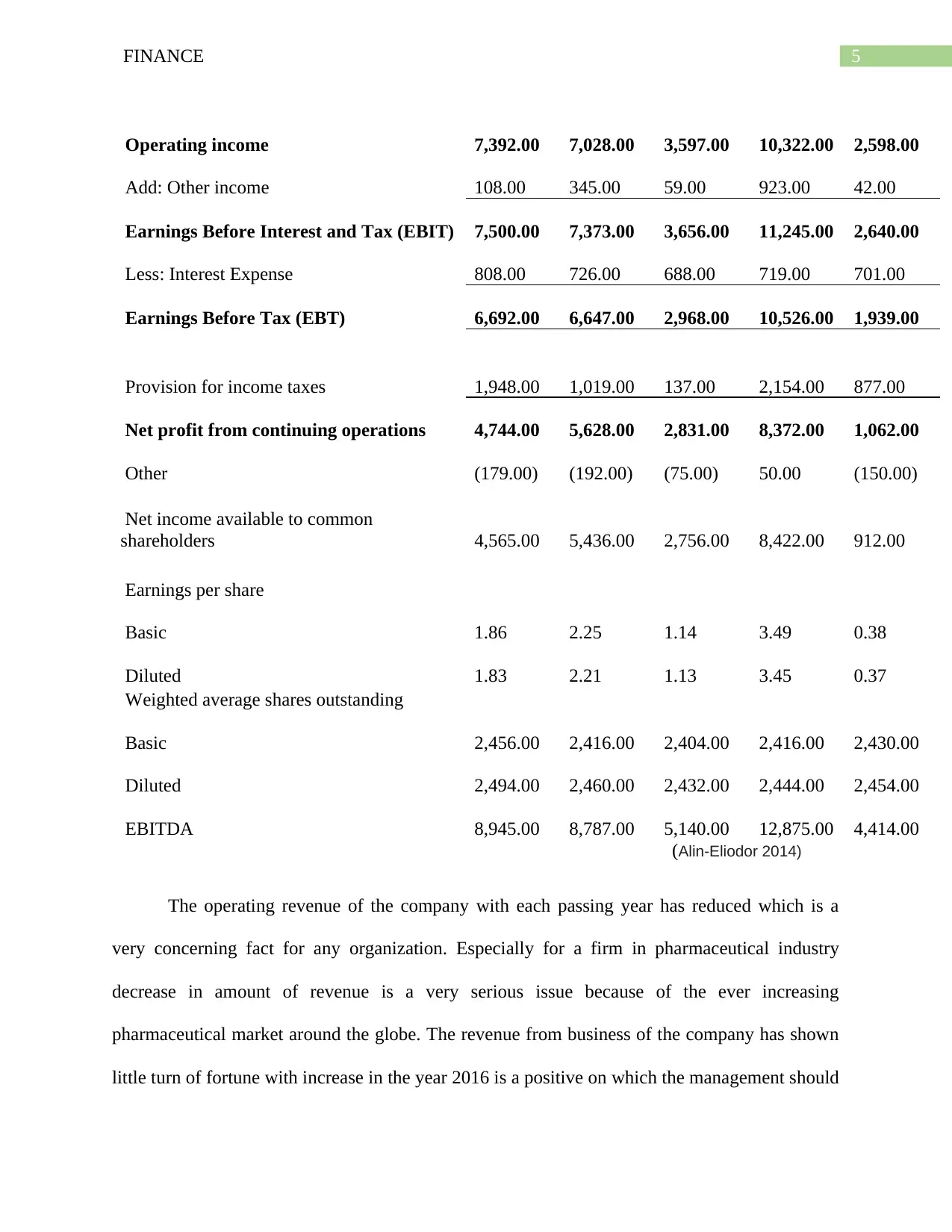

Operating income 7,392.00 7,028.00 3,597.00 10,322.00 2,598.00

Add: Other income 108.00 345.00 59.00 923.00 42.00

Earnings Before Interest and Tax (EBIT) 7,500.00 7,373.00 3,656.00 11,245.00 2,640.00

Less: Interest Expense 808.00 726.00 688.00 719.00 701.00

Earnings Before Tax (EBT) 6,692.00 6,647.00 2,968.00 10,526.00 1,939.00

Provision for income taxes 1,948.00 1,019.00 137.00 2,154.00 877.00

Net profit from continuing operations 4,744.00 5,628.00 2,831.00 8,372.00 1,062.00

Other (179.00) (192.00) (75.00) 50.00 (150.00)

Net income available to common

shareholders 4,565.00 5,436.00 2,756.00 8,422.00 912.00

Earnings per share

Basic 1.86 2.25 1.14 3.49 0.38

Diluted 1.83 2.21 1.13 3.45 0.37

Weighted average shares outstanding

Basic 2,456.00 2,416.00 2,404.00 2,416.00 2,430.00

Diluted 2,494.00 2,460.00 2,432.00 2,444.00 2,454.00

EBITDA 8,945.00 8,787.00 5,140.00 12,875.00 4,414.00

(Alin-Eliodor 2014)

The operating revenue of the company with each passing year has reduced which is a

very concerning fact for any organization. Especially for a firm in pharmaceutical industry

decrease in amount of revenue is a very serious issue because of the ever increasing

pharmaceutical market around the globe. The revenue from business of the company has shown

little turn of fortune with increase in the year 2016 is a positive on which the management should

Operating income 7,392.00 7,028.00 3,597.00 10,322.00 2,598.00

Add: Other income 108.00 345.00 59.00 923.00 42.00

Earnings Before Interest and Tax (EBIT) 7,500.00 7,373.00 3,656.00 11,245.00 2,640.00

Less: Interest Expense 808.00 726.00 688.00 719.00 701.00

Earnings Before Tax (EBT) 6,692.00 6,647.00 2,968.00 10,526.00 1,939.00

Provision for income taxes 1,948.00 1,019.00 137.00 2,154.00 877.00

Net profit from continuing operations 4,744.00 5,628.00 2,831.00 8,372.00 1,062.00

Other (179.00) (192.00) (75.00) 50.00 (150.00)

Net income available to common

shareholders 4,565.00 5,436.00 2,756.00 8,422.00 912.00

Earnings per share

Basic 1.86 2.25 1.14 3.49 0.38

Diluted 1.83 2.21 1.13 3.45 0.37

Weighted average shares outstanding

Basic 2,456.00 2,416.00 2,404.00 2,416.00 2,430.00

Diluted 2,494.00 2,460.00 2,432.00 2,444.00 2,454.00

EBITDA 8,945.00 8,787.00 5,140.00 12,875.00 4,414.00

(Alin-Eliodor 2014)

The operating revenue of the company with each passing year has reduced which is a

very concerning fact for any organization. Especially for a firm in pharmaceutical industry

decrease in amount of revenue is a very serious issue because of the ever increasing

pharmaceutical market around the globe. The revenue from business of the company has shown

little turn of fortune with increase in the year 2016 is a positive on which the management should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

build its momentum to improve the operating performance in the future. The operating income is

a directly measuring factor that is used to determine the operating efficiency of an organization.

The fact that Earnings before Interests and Taxes (EBIT) as well as Earnings before Taxes (EBT)

both have reduced substantially over the last five year including 2016 is an alarming sign for the

company. A clear indication that the company has been unable to perform in the last few years

the way it did in the past (Bonaimé et al. 2014)).

Weighted Average Cost of Capital:

On the basis current

year figures

Associated

costs Funds

Proportion of

funds

% of

cost

Weighted

cost

Borrowed funds 701.00

14,661.0

0 92.88 4.78 4.44

Equity funds 912.00 1,124.00 7.12 81.14 5.78

1,613.00

15,785.0

0 100.00 10.22

On the basis of last five

year's average

Associated

costs Funds

Proportion of

funds

% of

cost

Weighted

cost

Borrowed funds 728.40

15,190.6

0 76.52 4.80 3.67

Equity funds 4,418.20 4,661.60 23.48 94.78 22.26

19,852.2

0 25.92

On the basis of the

interest and dividend

paid in the current year

Cash flow Funds

Proportion of

funds

% of

cost

Weighted

cost

Borrowed funds 919.00

14,661.0

74.14

6.27

4.65

build its momentum to improve the operating performance in the future. The operating income is

a directly measuring factor that is used to determine the operating efficiency of an organization.

The fact that Earnings before Interests and Taxes (EBIT) as well as Earnings before Taxes (EBT)

both have reduced substantially over the last five year including 2016 is an alarming sign for the

company. A clear indication that the company has been unable to perform in the last few years

the way it did in the past (Bonaimé et al. 2014)).

Weighted Average Cost of Capital:

On the basis current

year figures

Associated

costs Funds

Proportion of

funds

% of

cost

Weighted

cost

Borrowed funds 701.00

14,661.0

0 92.88 4.78 4.44

Equity funds 912.00 1,124.00 7.12 81.14 5.78

1,613.00

15,785.0

0 100.00 10.22

On the basis of last five

year's average

Associated

costs Funds

Proportion of

funds

% of

cost

Weighted

cost

Borrowed funds 728.40

15,190.6

0 76.52 4.80 3.67

Equity funds 4,418.20 4,661.60 23.48 94.78 22.26

19,852.2

0 25.92

On the basis of the

interest and dividend

paid in the current year

Cash flow Funds

Proportion of

funds

% of

cost

Weighted

cost

Borrowed funds 919.00

14,661.0

74.14

6.27

4.65

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

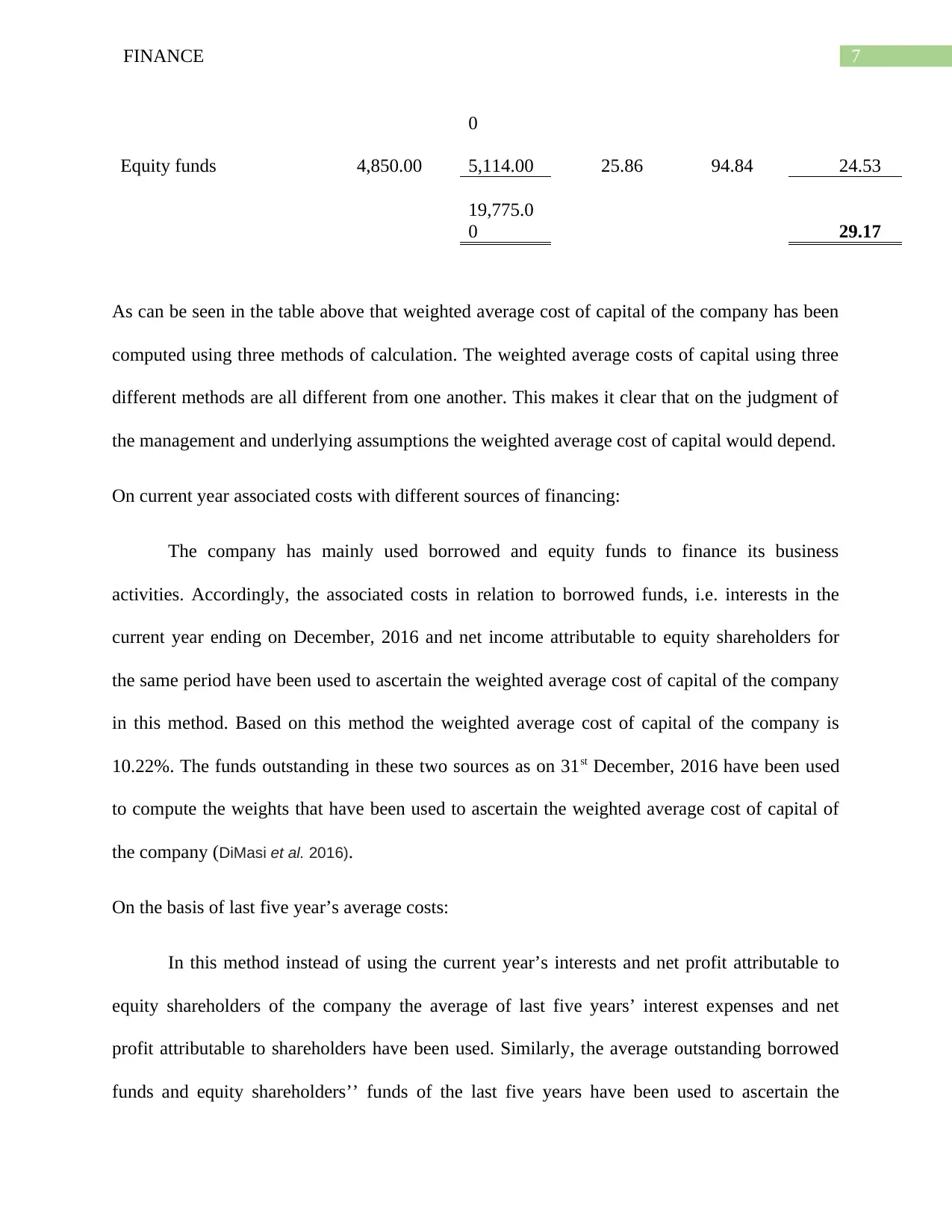

0

Equity funds 4,850.00 5,114.00 25.86 94.84 24.53

19,775.0

0 29.17

As can be seen in the table above that weighted average cost of capital of the company has been

computed using three methods of calculation. The weighted average costs of capital using three

different methods are all different from one another. This makes it clear that on the judgment of

the management and underlying assumptions the weighted average cost of capital would depend.

On current year associated costs with different sources of financing:

The company has mainly used borrowed and equity funds to finance its business

activities. Accordingly, the associated costs in relation to borrowed funds, i.e. interests in the

current year ending on December, 2016 and net income attributable to equity shareholders for

the same period have been used to ascertain the weighted average cost of capital of the company

in this method. Based on this method the weighted average cost of capital of the company is

10.22%. The funds outstanding in these two sources as on 31st December, 2016 have been used

to compute the weights that have been used to ascertain the weighted average cost of capital of

the company (DiMasi et al. 2016).

On the basis of last five year’s average costs:

In this method instead of using the current year’s interests and net profit attributable to

equity shareholders of the company the average of last five years’ interest expenses and net

profit attributable to shareholders have been used. Similarly, the average outstanding borrowed

funds and equity shareholders’’ funds of the last five years have been used to ascertain the

0

Equity funds 4,850.00 5,114.00 25.86 94.84 24.53

19,775.0

0 29.17

As can be seen in the table above that weighted average cost of capital of the company has been

computed using three methods of calculation. The weighted average costs of capital using three

different methods are all different from one another. This makes it clear that on the judgment of

the management and underlying assumptions the weighted average cost of capital would depend.

On current year associated costs with different sources of financing:

The company has mainly used borrowed and equity funds to finance its business

activities. Accordingly, the associated costs in relation to borrowed funds, i.e. interests in the

current year ending on December, 2016 and net income attributable to equity shareholders for

the same period have been used to ascertain the weighted average cost of capital of the company

in this method. Based on this method the weighted average cost of capital of the company is

10.22%. The funds outstanding in these two sources as on 31st December, 2016 have been used

to compute the weights that have been used to ascertain the weighted average cost of capital of

the company (DiMasi et al. 2016).

On the basis of last five year’s average costs:

In this method instead of using the current year’s interests and net profit attributable to

equity shareholders of the company the average of last five years’ interest expenses and net

profit attributable to shareholders have been used. Similarly, the average outstanding borrowed

funds and equity shareholders’’ funds of the last five years have been used to ascertain the

8FINANCE

weightage in this case. The weighted average cost of capital using average associated costs

instead of current costs of 25.92% is a huge change from 10.22% calculated using interests and

net profit attributable to equity shareholders of the current year (Brotherson ey al. 2015).

On the basis of cash outflow in respect of dividend and interest of 2016:

The payment of dividend and debt repayment in the year 2016 have been used in this

method to compute the weighted average cost of capital of the company. The equity

shareholders’ funds as on 31st December, 2015 and outstanding amount of debt as on 31st

December, 2016 have been used to ascertain the proportion of weightage attached for

computation of cost of capital. 29.17% is the ascertained weighted average cost of capital of the

company under this method.

Neither the net profit attributable to equity shareholders of current year or average of last

five years seems correct to ascertain the cost of equity fund however, the interests in case of debt

is the only way to ascertain the cost of borrowed funds and is also correct. Thus, the better

approach it seems the use of payment of dividend to equity shareholders and interests on

borrowed funds to ascertain the appropriate weighted average cost of capital of a company. Thus,

using the dividend paid to equity shareholders and interest to lenders the weighted average cost

of capital of the company would be as following:

On the basic of dividend

and interest payment

Cash

flow Funds

Proportion of

funds % of cost

Weighted

cost

Borrowed funds 701.00 14,661.00 74.14 4.78 3.54

Equity funds 4,850.00 5,114.00 25.86 94.84 24.53

19,775.00 28.07

weightage in this case. The weighted average cost of capital using average associated costs

instead of current costs of 25.92% is a huge change from 10.22% calculated using interests and

net profit attributable to equity shareholders of the current year (Brotherson ey al. 2015).

On the basis of cash outflow in respect of dividend and interest of 2016:

The payment of dividend and debt repayment in the year 2016 have been used in this

method to compute the weighted average cost of capital of the company. The equity

shareholders’ funds as on 31st December, 2015 and outstanding amount of debt as on 31st

December, 2016 have been used to ascertain the proportion of weightage attached for

computation of cost of capital. 29.17% is the ascertained weighted average cost of capital of the

company under this method.

Neither the net profit attributable to equity shareholders of current year or average of last

five years seems correct to ascertain the cost of equity fund however, the interests in case of debt

is the only way to ascertain the cost of borrowed funds and is also correct. Thus, the better

approach it seems the use of payment of dividend to equity shareholders and interests on

borrowed funds to ascertain the appropriate weighted average cost of capital of a company. Thus,

using the dividend paid to equity shareholders and interest to lenders the weighted average cost

of capital of the company would be as following:

On the basic of dividend

and interest payment

Cash

flow Funds

Proportion of

funds % of cost

Weighted

cost

Borrowed funds 701.00 14,661.00 74.14 4.78 3.54

Equity funds 4,850.00 5,114.00 25.86 94.84 24.53

19,775.00 28.07

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

On the basis of the above it can be said that the best judgment for the weighted average cost of

capital of the company is 28.07%. It is to be membered that since the dividend paid in the year

2016 represent the dividend of 2015 hence, the equity shareholders’ funds as on 31st of

December, 2015 has been used along with the outstanding amount of debt funds as on 31st

December, 2016 to calculate the relevant weightage for ascertainment of weighted average cost

of capital of the company.

The calculation weighted average cost of capital under the three different methods are all

on the basis of certain assumptions and facts. Thus, since the future is uncertain there is always a

possibility of assumptions not materializing in real facts. In such case as the assumption changes

so will the weighted average cost of capital will change. Facts leave no room for speculation and

doubts whereas assumptions are merely estimates made by the management on the basis of their

experiences of doing business. Thus, there are certainly enough room for speculation and doubts

when certain assumptions are made. Hence, the three methods which were used to calculate the

weighted average cost of capital of the company are not completely safe and thus, there could be

substantial change in the weighted average cost of capital of the company in case the underlying

assumptions change. However, the best judgment of weighted average cost of capital of the

company of 28.07% is without any error since the associated costs as well as the attached

weights have been taken in accordance with the relevant figures provided in financial statements

of the company.

On the basis of the above it can be said that the best judgment for the weighted average cost of

capital of the company is 28.07%. It is to be membered that since the dividend paid in the year

2016 represent the dividend of 2015 hence, the equity shareholders’ funds as on 31st of

December, 2015 has been used along with the outstanding amount of debt funds as on 31st

December, 2016 to calculate the relevant weightage for ascertainment of weighted average cost

of capital of the company.

The calculation weighted average cost of capital under the three different methods are all

on the basis of certain assumptions and facts. Thus, since the future is uncertain there is always a

possibility of assumptions not materializing in real facts. In such case as the assumption changes

so will the weighted average cost of capital will change. Facts leave no room for speculation and

doubts whereas assumptions are merely estimates made by the management on the basis of their

experiences of doing business. Thus, there are certainly enough room for speculation and doubts

when certain assumptions are made. Hence, the three methods which were used to calculate the

weighted average cost of capital of the company are not completely safe and thus, there could be

substantial change in the weighted average cost of capital of the company in case the underlying

assumptions change. However, the best judgment of weighted average cost of capital of the

company of 28.07% is without any error since the associated costs as well as the attached

weights have been taken in accordance with the relevant figures provided in financial statements

of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

Stage 2:

Financial analysis of an organization involves the analysis of financial statements of the

organization. The financial position of an organization as on a particular date can be ascertained

on the basis of its assets and liabilities as on that date from the Balance sheet of the organization.

The operating result of the organization will be assessed from the income statement of the

organization which is an integral part of the financial statements of an organization. Apart from

that financial statements include the cash flow statement which will help us to assess the

liquidity position of the organization and its ability of generate cash flow from operating,

investing and financial activities. In the case GSK, firstly; the complete set of financial

statements will have to be presented along with ratio analysis, profitability ration, liquidity ratios

and solvency ratios of the company to analyze the company’s financial position and operating

results.

The financial statements of the company, income statements, balance sheet, have already

been provided at the beginning to ascertain the weighted average cost of capital of the company.

Let us now have the cash flow statement and ratio analysis of the company to conduct an in-

depth analysis of the financial position of the company.

GLAXOSMITHKLINE PLC ADR (GSK) Cash Flow Statement

All amounts are in GBP

millions except per share

data. 2012-12 2013-12 2014-12 2015-12 2016-12

Cash Flows From

Operating Activities

Net income 4,744.00 5,628.00 2,831.00 8,372.00 1,062.00

Depreciation &

amortization 1,445.00 1,414.00 1,484.00 1,630.00 1,774.00

Stage 2:

Financial analysis of an organization involves the analysis of financial statements of the

organization. The financial position of an organization as on a particular date can be ascertained

on the basis of its assets and liabilities as on that date from the Balance sheet of the organization.

The operating result of the organization will be assessed from the income statement of the

organization which is an integral part of the financial statements of an organization. Apart from

that financial statements include the cash flow statement which will help us to assess the

liquidity position of the organization and its ability of generate cash flow from operating,

investing and financial activities. In the case GSK, firstly; the complete set of financial

statements will have to be presented along with ratio analysis, profitability ration, liquidity ratios

and solvency ratios of the company to analyze the company’s financial position and operating

results.

The financial statements of the company, income statements, balance sheet, have already

been provided at the beginning to ascertain the weighted average cost of capital of the company.

Let us now have the cash flow statement and ratio analysis of the company to conduct an in-

depth analysis of the financial position of the company.

GLAXOSMITHKLINE PLC ADR (GSK) Cash Flow Statement

All amounts are in GBP

millions except per share

data. 2012-12 2013-12 2014-12 2015-12 2016-12

Cash Flows From

Operating Activities

Net income 4,744.00 5,628.00 2,831.00 8,372.00 1,062.00

Depreciation &

amortization 1,445.00 1,414.00 1,484.00 1,630.00 1,774.00

11FINANCE

Investment/asset

impairment charges 654.00 928.00 205.00 822.00 226.00

Investments losses (gains) (16.00) (318.00) (149.00)

(1,185.00

) (254.00)

Deferred income taxes

(1,673.00

) 877.00

Stock based compensation 220.00 319.00 332.00 368.00 319.00

Accounts receivable 183.00 16.00 347.00 98.00 (188.00)

Inventory 37.00 (95.00) (529.00) (111.00) 70.00

Accounts payable 177.00 125.00 91.00 40.00 96.00

Other working capital

(2,826.00

) 10.00 752.00 1,648.00 3,672.00

Other non-cash items 1,430.00 (805.00) (188.00)

(9,113.00

)

(1,157.00

)

Net cash from operating

activities 4,375.00 7,222.00 5,176.00 2,569.00 6,497.00

Cash Flows From

Investing Activities

Investments in property,

plant, and equipment

(1,051.00

)

(1,188.00

)

(1,188.00

)

(1,380.00

)

(1,543.00

)

Property, plant, and

equipment reductions 68.00 46.00 39.00 72.00 98.00

Acquisitions, net

(2,235.00

) 1,604.00 121.00 6,705.00 89.00

Purchases of investments (328.00) (141.00) (92.00) (98.00) (107.00)

Sales/Maturities of

investments 28.00 503.00 207.00 921.00 683.00

Purchases of intangibles (469.00) (513.00) (563.00) (521.00) (809.00)

Sales of intangibles 1,056.00 136.00 330.00 236.00 283.00

Other investing activities 300.00 77.00 68.00 102.00 37.00

Investment/asset

impairment charges 654.00 928.00 205.00 822.00 226.00

Investments losses (gains) (16.00) (318.00) (149.00)

(1,185.00

) (254.00)

Deferred income taxes

(1,673.00

) 877.00

Stock based compensation 220.00 319.00 332.00 368.00 319.00

Accounts receivable 183.00 16.00 347.00 98.00 (188.00)

Inventory 37.00 (95.00) (529.00) (111.00) 70.00

Accounts payable 177.00 125.00 91.00 40.00 96.00

Other working capital

(2,826.00

) 10.00 752.00 1,648.00 3,672.00

Other non-cash items 1,430.00 (805.00) (188.00)

(9,113.00

)

(1,157.00

)

Net cash from operating

activities 4,375.00 7,222.00 5,176.00 2,569.00 6,497.00

Cash Flows From

Investing Activities

Investments in property,

plant, and equipment

(1,051.00

)

(1,188.00

)

(1,188.00

)

(1,380.00

)

(1,543.00

)

Property, plant, and

equipment reductions 68.00 46.00 39.00 72.00 98.00

Acquisitions, net

(2,235.00

) 1,604.00 121.00 6,705.00 89.00

Purchases of investments (328.00) (141.00) (92.00) (98.00) (107.00)

Sales/Maturities of

investments 28.00 503.00 207.00 921.00 683.00

Purchases of intangibles (469.00) (513.00) (563.00) (521.00) (809.00)

Sales of intangibles 1,056.00 136.00 330.00 236.00 283.00

Other investing activities 300.00 77.00 68.00 102.00 37.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.