Financial Analysis of GSK PLC and Zero Based Budgeting Report

VerifiedAdded on 2023/05/30

|17

|5001

|463

Report

AI Summary

This report presents a comprehensive financial analysis of GlaxoSmithKline (GSK) PLC, a leading pharmaceutical company. The first part of the report focuses on evaluating GSK's profitability performance through ratio analysis, comparing it with its competitor Pfizer Inc. Key profitability ratios, including return on capital employed, operating profit margin, and earnings per share, are calculated and analyzed for the years 2016 and 2017. The report also examines the competitive and macroeconomic influences on these ratios. The second part of the report delves into zero-based budgeting, explaining its methodology, benefits, and drawbacks, and contrasting it with incremental budgeting. The report highlights how zero-based budgeting can improve accuracy, cut costs, and enhance communication within an organization. The report utilizes data from GSK PLC's financial reports and other reliable sources to support its analysis.

1

Managing Financial Performance 7AC006

Managing Financial Performance 7AC006

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Part 1: Profitability performance of GSK PLC

GSK plc refers to GlaxoSmithKline and it ranks amongst the top companies in FT Global

500 companies. GSK is top pharmaceutical company in the world and it operates in two major

sectors: Consumer Healthcare and Pharmaceuticals. The purpose of this section of assignment is

to evaluate the financial performance of GSK Plc through use of ratio analysis. The motive is to

evaluate the profitability performance of the company through calculating some of important

profitability ratios such as return on capital employed, operating profit margin and earnings per

share. In addition to ratio analysis, various competitive and macro-economic influences on each

of profitability ratios has also been discussed in this section of the assignment. Profitability

performance of GSK plc has been compared with one of its top most competitors, Pfizer Inc.

Pfizer also rank amongst the top pharmaceutical company of the world and this company was

founded in New York, USA (GSK Plc, 2017).

Profitability analysis of GSK Plc and Pfizer for year 2016 and 2017

Profitability analysis through ratios aims to measure the management ability to earn the

profits in relation to sales revenue, equity and assets. Profitability analysis also embarks its

importance on return earned by the company on the total capital invested during the period. It is

expected from the management to make sure that there is optimum utilization of resources to

earn maximum sales revenue. Management must also make sure cost of goods sold and operating

expenses should be kept at lowest level so that company can earn maximum profits. Profitability

ratios aim to assess the ability of the company to generate profits, cash flows and earnings in

relation to some base often referred to as total capital invested, or any similar basis. It can be said

that profitability ratios is very useful to evaluate how effectively the profitability of the company

is managed. Each profitability ratio provides different category of information about the financial

health and performance of the entity. For example, operating profit margin and net profit margin

provides information on how effectively company manages its expenses whereas return on

capital employed information on how effectively company uses its capital to generate the returns.

Earnings per share tell how much profit earned by the company on each share of issued in the

market (Higgins, 2012).

Return on Capital Employed

Part 1: Profitability performance of GSK PLC

GSK plc refers to GlaxoSmithKline and it ranks amongst the top companies in FT Global

500 companies. GSK is top pharmaceutical company in the world and it operates in two major

sectors: Consumer Healthcare and Pharmaceuticals. The purpose of this section of assignment is

to evaluate the financial performance of GSK Plc through use of ratio analysis. The motive is to

evaluate the profitability performance of the company through calculating some of important

profitability ratios such as return on capital employed, operating profit margin and earnings per

share. In addition to ratio analysis, various competitive and macro-economic influences on each

of profitability ratios has also been discussed in this section of the assignment. Profitability

performance of GSK plc has been compared with one of its top most competitors, Pfizer Inc.

Pfizer also rank amongst the top pharmaceutical company of the world and this company was

founded in New York, USA (GSK Plc, 2017).

Profitability analysis of GSK Plc and Pfizer for year 2016 and 2017

Profitability analysis through ratios aims to measure the management ability to earn the

profits in relation to sales revenue, equity and assets. Profitability analysis also embarks its

importance on return earned by the company on the total capital invested during the period. It is

expected from the management to make sure that there is optimum utilization of resources to

earn maximum sales revenue. Management must also make sure cost of goods sold and operating

expenses should be kept at lowest level so that company can earn maximum profits. Profitability

ratios aim to assess the ability of the company to generate profits, cash flows and earnings in

relation to some base often referred to as total capital invested, or any similar basis. It can be said

that profitability ratios is very useful to evaluate how effectively the profitability of the company

is managed. Each profitability ratio provides different category of information about the financial

health and performance of the entity. For example, operating profit margin and net profit margin

provides information on how effectively company manages its expenses whereas return on

capital employed information on how effectively company uses its capital to generate the returns.

Earnings per share tell how much profit earned by the company on each share of issued in the

market (Higgins, 2012).

Return on Capital Employed

3

It is the most important profitability ratio that measures the profits earned by company on

percentage of capital employed. Here capital employed means total of shareholder’s fund and

non-current liabilities that is used by the company to financed the assets of the company.

Formula: EBIT/ (shareholder’s Funds + Non-Current Liabilities)

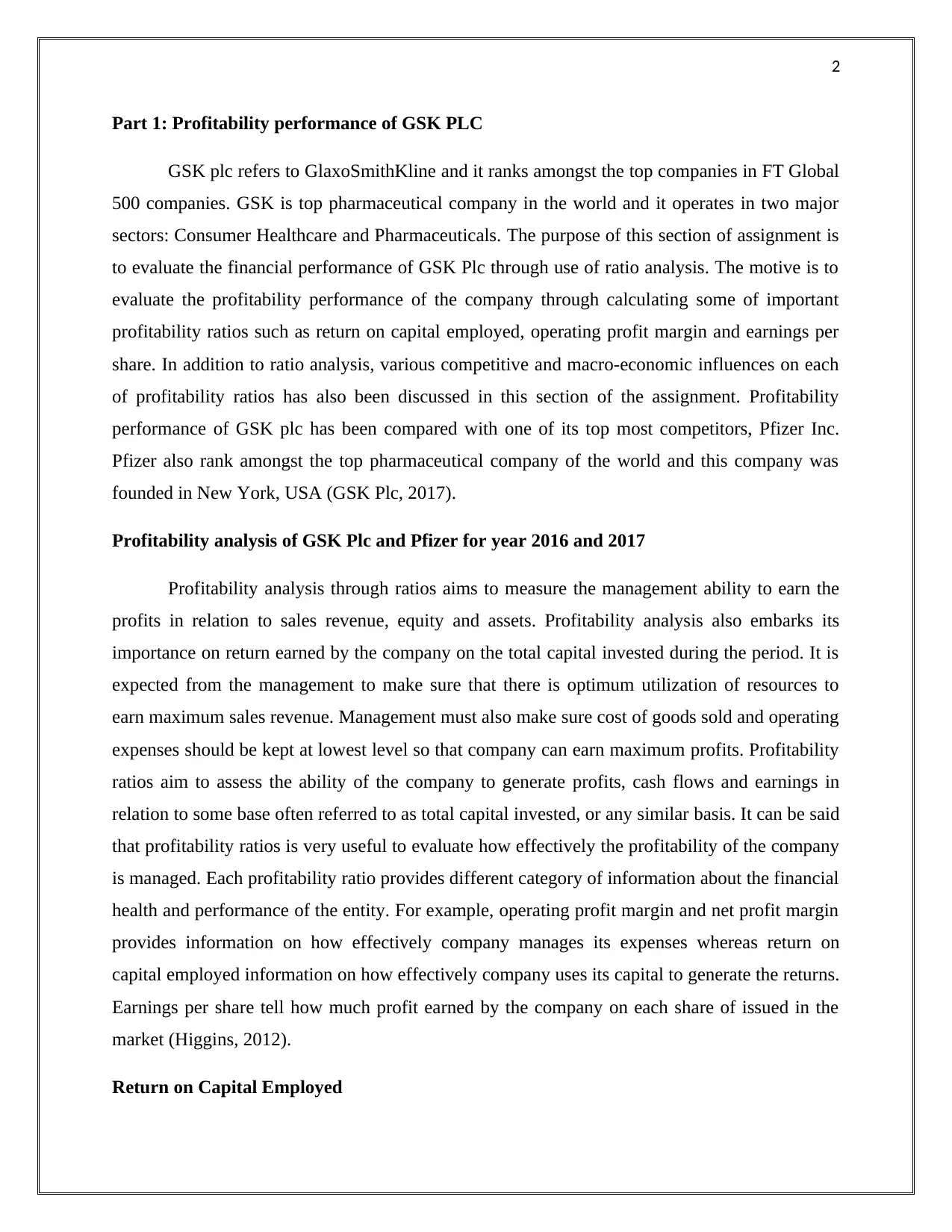

Return on capital employed for GSK

For year 2016: £ 2598 /(£ 35117+ £ 1124) = 7.17%

For year 2017: £4087 + ( £ 26323 + (-68)) = 15.57%

Return on capital employed for Pfizer

For year 2016: £ 8351 / (£ 80661 + £ 59840) = 5.94%

For year 2017: £ 12306 /( £ 69714 + £ 71656) = 8.70% (Horngren, 2009)

Return on Capital Employed

Particulars GSK Plc Pfizer

2016 2017 2016 2017

Ratio 7.17% 15.57% 5.94% 8.70%

(GSK Plc, 2017)

2016 2017

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Return on Capital Employed

Percentage

It is the most important profitability ratio that measures the profits earned by company on

percentage of capital employed. Here capital employed means total of shareholder’s fund and

non-current liabilities that is used by the company to financed the assets of the company.

Formula: EBIT/ (shareholder’s Funds + Non-Current Liabilities)

Return on capital employed for GSK

For year 2016: £ 2598 /(£ 35117+ £ 1124) = 7.17%

For year 2017: £4087 + ( £ 26323 + (-68)) = 15.57%

Return on capital employed for Pfizer

For year 2016: £ 8351 / (£ 80661 + £ 59840) = 5.94%

For year 2017: £ 12306 /( £ 69714 + £ 71656) = 8.70% (Horngren, 2009)

Return on Capital Employed

Particulars GSK Plc Pfizer

2016 2017 2016 2017

Ratio 7.17% 15.57% 5.94% 8.70%

(GSK Plc, 2017)

2016 2017

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Return on Capital Employed

Percentage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Return on capital of employed of GSK Plc was better than the Pfizer in both the years. In

year 2016, the return on capital employed was 7.17% and it was increased to 15.57% in year

2017. On the other hand, return on capital employed of Pfizer was 5.94% in year 2016 and it got

increased to 8.70%. So, it can be said that GSK plc has provided better returns on the total

capital employed by the company.

Operating Profit Margin

This ratio is used to evaluate the operating performance of the entity and it indicates the

percentage of sales earned by the company after paying cost of goods sold charges and operating

expenses. It is generally expressed as the percentage of sales. This ratio is the best tool to

evaluate the performance of one company with the performance of other company (Kaplan and

Atkinson, 2015).

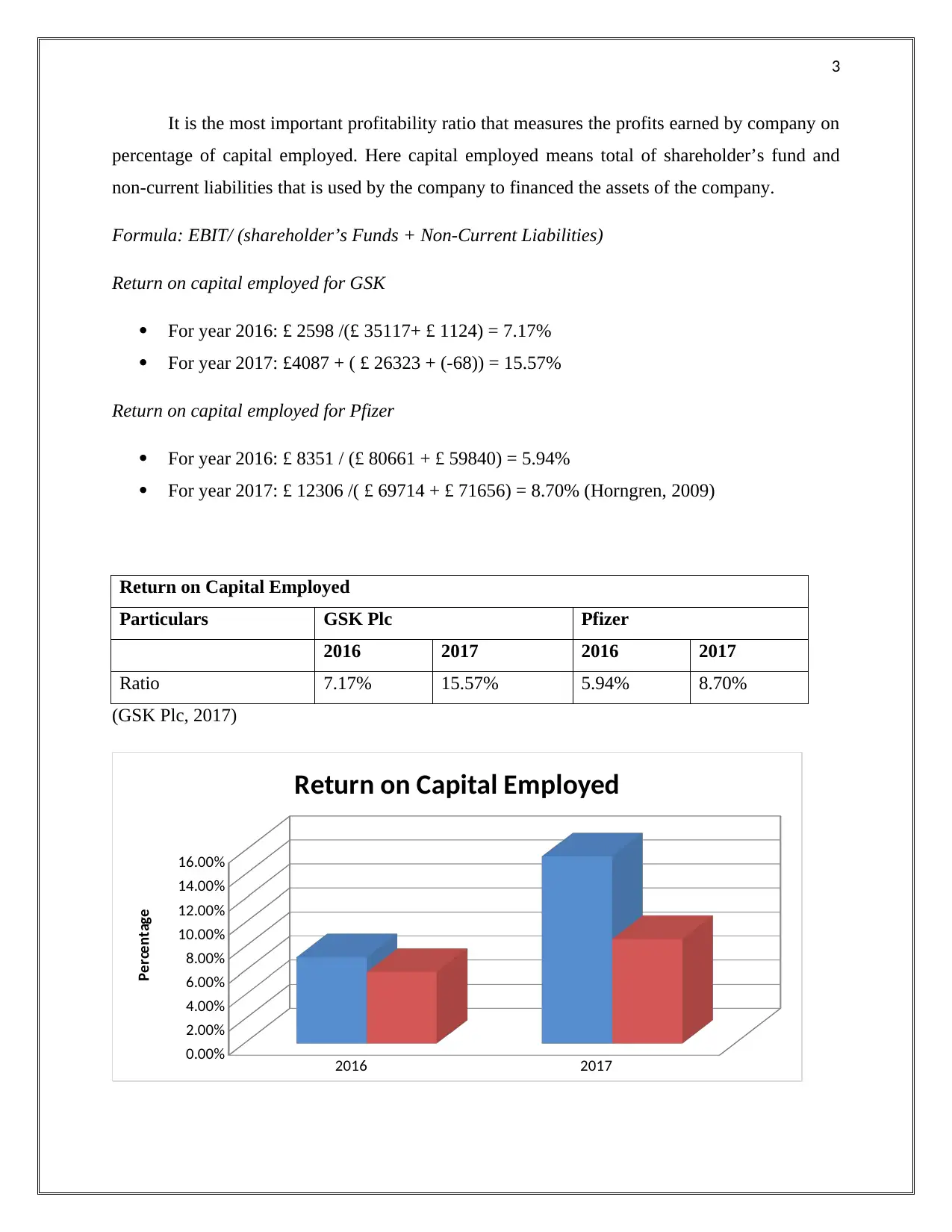

Formula: Operating profit margin / Sales Revenue * 100

Operating profit margin for GSK

For year 2016: £ 2598/£27889 = 9.32%

For year 2017: £4087/£ 30186 = 13.54%

Operating profit margin for Pfizer

For year 2016: £ 8351 / £ 52824 = 15.81%

For year 2017: £ 12306 / 52546 = 23.42%

Operating Profit Margin

Particulars GSK Plc Pfizer

2016 2017 2016 2017

Ratio 9.32% 13.54% 15.81% 23.42%

(GSK Plc, 2017)

Return on capital of employed of GSK Plc was better than the Pfizer in both the years. In

year 2016, the return on capital employed was 7.17% and it was increased to 15.57% in year

2017. On the other hand, return on capital employed of Pfizer was 5.94% in year 2016 and it got

increased to 8.70%. So, it can be said that GSK plc has provided better returns on the total

capital employed by the company.

Operating Profit Margin

This ratio is used to evaluate the operating performance of the entity and it indicates the

percentage of sales earned by the company after paying cost of goods sold charges and operating

expenses. It is generally expressed as the percentage of sales. This ratio is the best tool to

evaluate the performance of one company with the performance of other company (Kaplan and

Atkinson, 2015).

Formula: Operating profit margin / Sales Revenue * 100

Operating profit margin for GSK

For year 2016: £ 2598/£27889 = 9.32%

For year 2017: £4087/£ 30186 = 13.54%

Operating profit margin for Pfizer

For year 2016: £ 8351 / £ 52824 = 15.81%

For year 2017: £ 12306 / 52546 = 23.42%

Operating Profit Margin

Particulars GSK Plc Pfizer

2016 2017 2016 2017

Ratio 9.32% 13.54% 15.81% 23.42%

(GSK Plc, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Operating Profit Margin

Percentage

On the basis of above graph it can be said that operating profit margin of GSK Plc was

lower than the Pfizer. It can be said that Pfizer has lower rate of operating expenses as compared

to GSK plc that helps them to maintain higher rate of operating profit margin. So it can be said

that GSK plc has poor profitability due to lower operating profit margin.

Earnings per share: Earnings per share refer to that part of profits that is meant for distribution

to the shareholders on each outstanding share. Earnings per share is very important form the

investors point of view as it is very good indicator of profitability. It is the reason why this ratio

is widely used to assess the profitability of companies (Firer, 2012).

Formula: (Net Profit after Taxes) / Number of Equity Shares

Earnings per share

Particulars GSK Plc Pfizer

2016 2017 2016 2017

Ratio £ 0.19 £ 0.31 £ 1.19 £ 3.58

(GSK Plc, 2017)

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Operating Profit Margin

Percentage

On the basis of above graph it can be said that operating profit margin of GSK Plc was

lower than the Pfizer. It can be said that Pfizer has lower rate of operating expenses as compared

to GSK plc that helps them to maintain higher rate of operating profit margin. So it can be said

that GSK plc has poor profitability due to lower operating profit margin.

Earnings per share: Earnings per share refer to that part of profits that is meant for distribution

to the shareholders on each outstanding share. Earnings per share is very important form the

investors point of view as it is very good indicator of profitability. It is the reason why this ratio

is widely used to assess the profitability of companies (Firer, 2012).

Formula: (Net Profit after Taxes) / Number of Equity Shares

Earnings per share

Particulars GSK Plc Pfizer

2016 2017 2016 2017

Ratio £ 0.19 £ 0.31 £ 1.19 £ 3.58

(GSK Plc, 2017)

6

2016 2017

£-

£0.50

£1.00

£1.50

£2.00

£2.50

£3.00

£3.50

£4.00

EPS

Amount

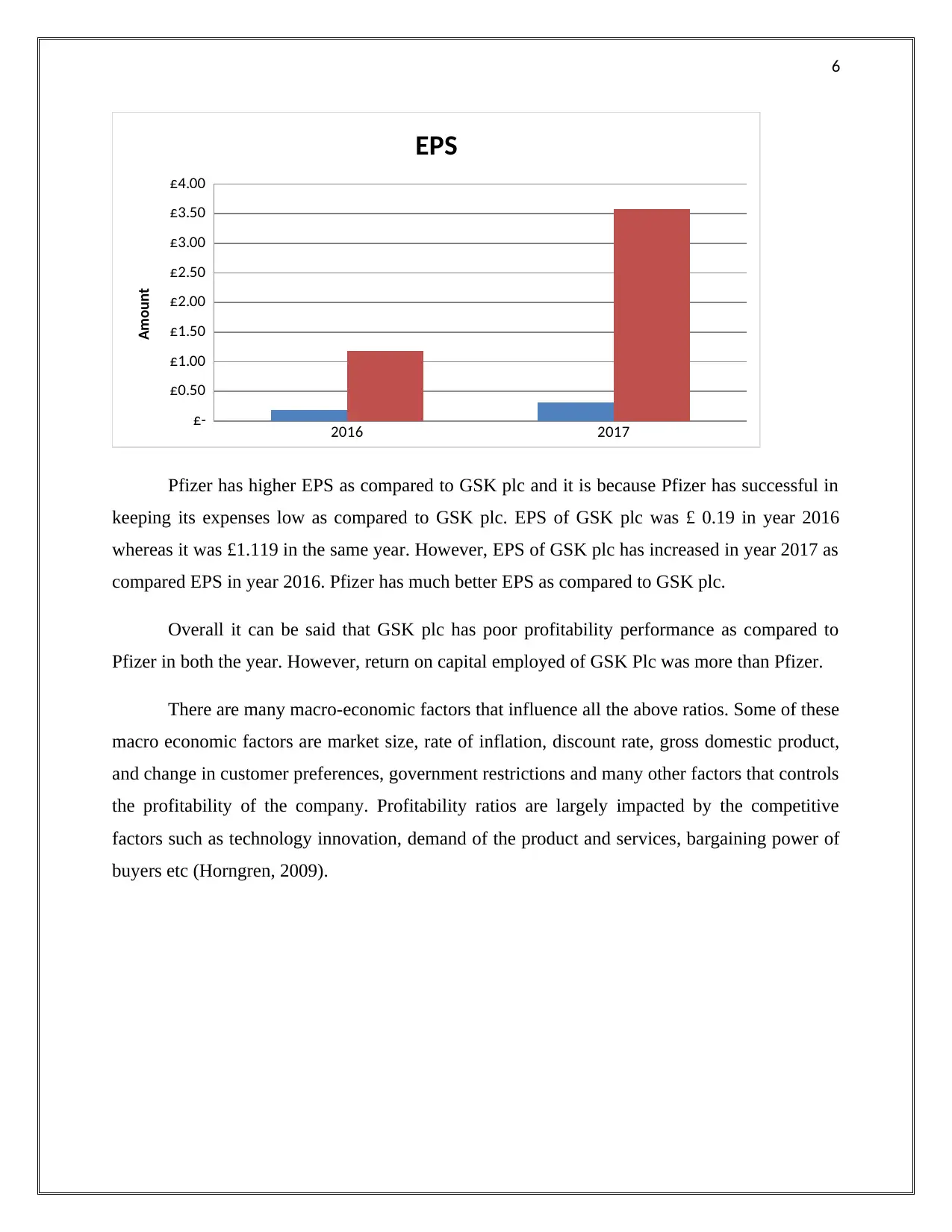

Pfizer has higher EPS as compared to GSK plc and it is because Pfizer has successful in

keeping its expenses low as compared to GSK plc. EPS of GSK plc was £ 0.19 in year 2016

whereas it was £1.119 in the same year. However, EPS of GSK plc has increased in year 2017 as

compared EPS in year 2016. Pfizer has much better EPS as compared to GSK plc.

Overall it can be said that GSK plc has poor profitability performance as compared to

Pfizer in both the year. However, return on capital employed of GSK Plc was more than Pfizer.

There are many macro-economic factors that influence all the above ratios. Some of these

macro economic factors are market size, rate of inflation, discount rate, gross domestic product,

and change in customer preferences, government restrictions and many other factors that controls

the profitability of the company. Profitability ratios are largely impacted by the competitive

factors such as technology innovation, demand of the product and services, bargaining power of

buyers etc (Horngren, 2009).

2016 2017

£-

£0.50

£1.00

£1.50

£2.00

£2.50

£3.00

£3.50

£4.00

EPS

Amount

Pfizer has higher EPS as compared to GSK plc and it is because Pfizer has successful in

keeping its expenses low as compared to GSK plc. EPS of GSK plc was £ 0.19 in year 2016

whereas it was £1.119 in the same year. However, EPS of GSK plc has increased in year 2017 as

compared EPS in year 2016. Pfizer has much better EPS as compared to GSK plc.

Overall it can be said that GSK plc has poor profitability performance as compared to

Pfizer in both the year. However, return on capital employed of GSK Plc was more than Pfizer.

There are many macro-economic factors that influence all the above ratios. Some of these

macro economic factors are market size, rate of inflation, discount rate, gross domestic product,

and change in customer preferences, government restrictions and many other factors that controls

the profitability of the company. Profitability ratios are largely impacted by the competitive

factors such as technology innovation, demand of the product and services, bargaining power of

buyers etc (Horngren, 2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Part 2: Zero Based Budgeting

Zero based budgeting is type budgeting method used under the budgeting process of the

entities. Under this process budgeting is performed from the zero base ie all the data and

information are gathered first time. In zero based budgeting process either past information is not

available or management wants from cost manager to formulate complete budgets without using

the past information. Zero based budgeting process is time consuming as it requires evaluating

every line item of the cash flow and other budgets. It requires all the cash inflows and outflows

to be justified in detail so that there will be very less variance in the budgets and actual outputs

(Wetherbe and Montanari, 1986).

Zero based budgeting is most important budgeting system that is based on current

estimates of all the activities whether old or new. It does not take into account the budget

developed for the past activities. The application of zero based budgeting takes organization very

far away from the incremental based budgeting or traditional budgeting. In incremental budget

previous year budget is taken as the starting point and any addition or modifications are carried

on previous budgets to formulate the current year budgets. Whereas in zero based budgeting cost

manager starts from zero point and takes an assumptions that previous spending patterns are no

longer used (Varlotta and Jones, 2010).

Under zero based budgeting organization are divided into lowest level possible and these

units are called as decision units. Budgeting decisions are now taken for these decisions units and

after than all the data is combined to prepare the current year budget. The procedure adopted in

zero based budgeting is complicated as compared to incremental based budgeting and it requires

more time to prepare the budgets as each cost in an activity is cross examined before preparing

the new budgets. Managers in each decision unit are required to provide detailed information

about all the activities including the spending plan required to achieve the goals of those decision

units. This end ups with minimum three decision packages of each decision units and to the

maximum it can be 10 or more. The three important decision packages that are prepared are base

package, current service package, and enhanced package. There are some difference in these

decision packages that describes difference of marginal spending and other variances (Varlotta

and Jones, 2010).

Part 2: Zero Based Budgeting

Zero based budgeting is type budgeting method used under the budgeting process of the

entities. Under this process budgeting is performed from the zero base ie all the data and

information are gathered first time. In zero based budgeting process either past information is not

available or management wants from cost manager to formulate complete budgets without using

the past information. Zero based budgeting process is time consuming as it requires evaluating

every line item of the cash flow and other budgets. It requires all the cash inflows and outflows

to be justified in detail so that there will be very less variance in the budgets and actual outputs

(Wetherbe and Montanari, 1986).

Zero based budgeting is most important budgeting system that is based on current

estimates of all the activities whether old or new. It does not take into account the budget

developed for the past activities. The application of zero based budgeting takes organization very

far away from the incremental based budgeting or traditional budgeting. In incremental budget

previous year budget is taken as the starting point and any addition or modifications are carried

on previous budgets to formulate the current year budgets. Whereas in zero based budgeting cost

manager starts from zero point and takes an assumptions that previous spending patterns are no

longer used (Varlotta and Jones, 2010).

Under zero based budgeting organization are divided into lowest level possible and these

units are called as decision units. Budgeting decisions are now taken for these decisions units and

after than all the data is combined to prepare the current year budget. The procedure adopted in

zero based budgeting is complicated as compared to incremental based budgeting and it requires

more time to prepare the budgets as each cost in an activity is cross examined before preparing

the new budgets. Managers in each decision unit are required to provide detailed information

about all the activities including the spending plan required to achieve the goals of those decision

units. This end ups with minimum three decision packages of each decision units and to the

maximum it can be 10 or more. The three important decision packages that are prepared are base

package, current service package, and enhanced package. There are some difference in these

decision packages that describes difference of marginal spending and other variances (Varlotta

and Jones, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Benefits of the zero based budgeting

Zero based budgeting is quite useful to increase the accuracy within the departments as it

ensures through examination of each of the functions performed within the department.

Under this budgeting technique managers need to examine needs of resources by each

activity and also the level of efforts and different ways to complete the activities are

identified.

Zero based budgeting takes into account the opinion and concerns of mid level as well as

line managers as this budgeting technique requires detailed information for lowest level

of decision making units.

Zero based budgeting is regarded as the most important basis for cutting the cost of

budgets. Zero based budgeting offers rational and comprehensive ways to reduce the

budget expenses. Various decision packages are developed for each of decision unit

which act as the base to make use of best decision package that is suitable for the

particular activity and also provides maximum benefits as per the expenditure incurred

for that particular activity. It is possible because spending of each activity has been put

under scrutiny before any decision has been taken (Kavanagh, 2012).

Another major advantage that zero based budgeting provides is that it helps the top level

management to gain the greater insights of the workings of the lower level departments.

All the details such as activities, spending and estimates of cost and profits of each

department are documents by each line manager are forwarded to the top level manager

to include into the budgets after performing the complete evaluation.

Resources are allocated in systematic way as operations and programmes of each activity

are evaluated in detail that provides deep insight view of resources required by each

activity. So resources are allocated systematically and in required manner to fulfill the

objectives defined under each activity.

It allows cost benefit comparison of each department budgets on the basis of decision

packages developed for each activity. Unlikely in other budgeting system there is no

arbitrary allocation of resources in case of zero based budgeting (Lalli, 2011).

Activities that are redundant or unproductive can be easily identified and removed after

verification. So it can be said that zero based budgeting is very cost effective and it

Benefits of the zero based budgeting

Zero based budgeting is quite useful to increase the accuracy within the departments as it

ensures through examination of each of the functions performed within the department.

Under this budgeting technique managers need to examine needs of resources by each

activity and also the level of efforts and different ways to complete the activities are

identified.

Zero based budgeting takes into account the opinion and concerns of mid level as well as

line managers as this budgeting technique requires detailed information for lowest level

of decision making units.

Zero based budgeting is regarded as the most important basis for cutting the cost of

budgets. Zero based budgeting offers rational and comprehensive ways to reduce the

budget expenses. Various decision packages are developed for each of decision unit

which act as the base to make use of best decision package that is suitable for the

particular activity and also provides maximum benefits as per the expenditure incurred

for that particular activity. It is possible because spending of each activity has been put

under scrutiny before any decision has been taken (Kavanagh, 2012).

Another major advantage that zero based budgeting provides is that it helps the top level

management to gain the greater insights of the workings of the lower level departments.

All the details such as activities, spending and estimates of cost and profits of each

department are documents by each line manager are forwarded to the top level manager

to include into the budgets after performing the complete evaluation.

Resources are allocated in systematic way as operations and programmes of each activity

are evaluated in detail that provides deep insight view of resources required by each

activity. So resources are allocated systematically and in required manner to fulfill the

objectives defined under each activity.

It allows cost benefit comparison of each department budgets on the basis of decision

packages developed for each activity. Unlikely in other budgeting system there is no

arbitrary allocation of resources in case of zero based budgeting (Lalli, 2011).

Activities that are redundant or unproductive can be easily identified and removed after

verification. So it can be said that zero based budgeting is very cost effective and it

9

allows including all those activities that are valuable and provides some productive

results.

Zero based budgeting helps to improve the coordination and communication between the

departments. In turn it helps in increasing the efficiency of the employees as they are

involved in decision making.

Drawbacks of the zero base budgeting

Zero based budgeting is not the one day process as it involves huge time period as well as

requires investment of huge amount of money. So, zero based budgeting is very hard to

implement and requires a decision of top management before making it implement.

It is highly important to make successful implementation of ZBB but it requires full

support from the top management and it has been seen many times support from the top

management is not readily available due to many issues and communication problems.

At the time of preparing the zero based budget there is requirement of experts at every

department that can formulate the decision packages in proper manner (Ackah and

Agboyi, 2014).

Situations when zero based budgeting is most appropriate to use

There are many situations where zero based budgeting is very useful for the companies

but it is necessary to make cost benefit analysis before taking the decision to implement the

activity based budgets. When there is situation where it is not possible to implement the

incremental budgeting technique due to major modifications in the existing process and company

is ongoing with the major expansion. Although zero based is cost expensive but its advantages

proves to be beneficial in near future as it leads to major reduction in cost that is proportion to

activities that are redundant in nature (Ackah and Agboyi, 2014).

allows including all those activities that are valuable and provides some productive

results.

Zero based budgeting helps to improve the coordination and communication between the

departments. In turn it helps in increasing the efficiency of the employees as they are

involved in decision making.

Drawbacks of the zero base budgeting

Zero based budgeting is not the one day process as it involves huge time period as well as

requires investment of huge amount of money. So, zero based budgeting is very hard to

implement and requires a decision of top management before making it implement.

It is highly important to make successful implementation of ZBB but it requires full

support from the top management and it has been seen many times support from the top

management is not readily available due to many issues and communication problems.

At the time of preparing the zero based budget there is requirement of experts at every

department that can formulate the decision packages in proper manner (Ackah and

Agboyi, 2014).

Situations when zero based budgeting is most appropriate to use

There are many situations where zero based budgeting is very useful for the companies

but it is necessary to make cost benefit analysis before taking the decision to implement the

activity based budgets. When there is situation where it is not possible to implement the

incremental budgeting technique due to major modifications in the existing process and company

is ongoing with the major expansion. Although zero based is cost expensive but its advantages

proves to be beneficial in near future as it leads to major reduction in cost that is proportion to

activities that are redundant in nature (Ackah and Agboyi, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Part 3: Critical Evaluation of Strengths and Weaknesses of the Balance Score Card (BSC)

form of Performance Measurement

The business executives are increasingly viewing the traditional systems used for

performance measurement are largely proving to be ineffective in managing the complexity of

their business operations. This is because the traditional form of performance measurement only

assesses the business performance on the basis of financial parameters and does not take into

consideration the operational measures. As such, the need for business executives to track the

financial and operational metrics has lead to the development of balance scorecard that assesses

the performances of businesses on the basis of four set of parameters. These are financial

measures, customer satisfaction, internal processes, innovation and improvement. The financial

perspective includes the financial metrics that need to be adopted for examining the financial

performance such as return on capital and cash flow. Customer satisfaction includes measures

such as time, quality, performance, service and cost for measuring the satisfaction level of the

customers. The internal processes include measures such as cycle time, quality, employee skills

and productivity for assessing the internal performance of the businesses. The innovation and

learning perspective of the balance scorecard measures the performance of the company on the

basis of the parameters such as its ability to innovate, improve and learn in relation to the value

created for the customers. The strengths and weakness of the balance scorecard form of

performance measurement can be described as follows:

Strengths

BSC acts as a strategic management tool for businesses as it enables the managers in

developing an insight into the internal as well as external performance system. It facilitates the

business managers in transforming the strategy into tangible measures by aligning the strategy

with the overall mission and vision. The business executives with the use of BSC system can

effective coordinate a wide range of management processes such as performance appraisal,

setting of goals, allocating of resources and fostering the employee growth and development.

The project managers can integrate the use of BSC system for transforming the tasks into

tangible performance measures for successful completion of the project. It can prove to be

extremely beneficial for the project managers to continuously monitor the success of a project

and identify the gaps in the performance in advance so that they can be effectively overcome.

Part 3: Critical Evaluation of Strengths and Weaknesses of the Balance Score Card (BSC)

form of Performance Measurement

The business executives are increasingly viewing the traditional systems used for

performance measurement are largely proving to be ineffective in managing the complexity of

their business operations. This is because the traditional form of performance measurement only

assesses the business performance on the basis of financial parameters and does not take into

consideration the operational measures. As such, the need for business executives to track the

financial and operational metrics has lead to the development of balance scorecard that assesses

the performances of businesses on the basis of four set of parameters. These are financial

measures, customer satisfaction, internal processes, innovation and improvement. The financial

perspective includes the financial metrics that need to be adopted for examining the financial

performance such as return on capital and cash flow. Customer satisfaction includes measures

such as time, quality, performance, service and cost for measuring the satisfaction level of the

customers. The internal processes include measures such as cycle time, quality, employee skills

and productivity for assessing the internal performance of the businesses. The innovation and

learning perspective of the balance scorecard measures the performance of the company on the

basis of the parameters such as its ability to innovate, improve and learn in relation to the value

created for the customers. The strengths and weakness of the balance scorecard form of

performance measurement can be described as follows:

Strengths

BSC acts as a strategic management tool for businesses as it enables the managers in

developing an insight into the internal as well as external performance system. It facilitates the

business managers in transforming the strategy into tangible measures by aligning the strategy

with the overall mission and vision. The business executives with the use of BSC system can

effective coordinate a wide range of management processes such as performance appraisal,

setting of goals, allocating of resources and fostering the employee growth and development.

The project managers can integrate the use of BSC system for transforming the tasks into

tangible performance measures for successful completion of the project. It can prove to be

extremely beneficial for the project managers to continuously monitor the success of a project

and identify the gaps in the performance in advance so that they can be effectively overcome.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

This will help in maximizing the chances of project success by identifying the tasks that are

behind the schedule and taking effective measures for overcoming the performance in gaps.

Thus, it will help in enhancing the survival chances of an organization by developing a strategy

map that helps in development of a set of interrelated strategic objectives. The development of

various key performance indicators helps the businesses in gaining an overview of their overall

performance level. The balance scorecard enables the companies to report higher quality

management information and facilitates the decision-making process. The development of a well

implemented balance scorecard helps in aligning the organizational processes as per the strategic

priorities and goals.

Weaknesses

The weaknesses of the BSC can be regarded on the basis of high cost and time required

on the part of the companies to implement this management tool. The usefulness of the balance

scorecard depends on outweighing the cost and benefits that are associated with the

implementation of this scorecard. In addition to this, the employee resistance to change can also

negatively impact the successful implementation of the BSC and thus can undermine the benefits

that an organization could achieved by its adoption (Awadallah, 2015).

Extent of Adoption of BSC in global Context

Balance scorecard can be regarded as an integrated performance measurement system

that is being largely accepted by several countries. The large and complex firms are adopting the

use of balance scorecard as the increasing number of stakeholders within these firms requires the

use of comprehensive measurement systems that enables them to adopt the use of such systems

that helps in assessing both financial as well as non-financial performance. For example, Philips

Electronics has adopted the use of BSC for aligning its vision and mission with its overall

strategy. The use of BSC has proved to be largely beneficial for the company for assessing both

its qualitative and quantitative performance. It has been prove to be largely helpful for the

management of the company to measure its qualitative as well as quantitative performance and

thus facilitating the quick decision-making process (Neely, 2005).

Another example that can be cited in the context of a global corporation implemented a BSC is

Toyota Motor Corporation, recognized as most successful and renowned global automaker. The

This will help in maximizing the chances of project success by identifying the tasks that are

behind the schedule and taking effective measures for overcoming the performance in gaps.

Thus, it will help in enhancing the survival chances of an organization by developing a strategy

map that helps in development of a set of interrelated strategic objectives. The development of

various key performance indicators helps the businesses in gaining an overview of their overall

performance level. The balance scorecard enables the companies to report higher quality

management information and facilitates the decision-making process. The development of a well

implemented balance scorecard helps in aligning the organizational processes as per the strategic

priorities and goals.

Weaknesses

The weaknesses of the BSC can be regarded on the basis of high cost and time required

on the part of the companies to implement this management tool. The usefulness of the balance

scorecard depends on outweighing the cost and benefits that are associated with the

implementation of this scorecard. In addition to this, the employee resistance to change can also

negatively impact the successful implementation of the BSC and thus can undermine the benefits

that an organization could achieved by its adoption (Awadallah, 2015).

Extent of Adoption of BSC in global Context

Balance scorecard can be regarded as an integrated performance measurement system

that is being largely accepted by several countries. The large and complex firms are adopting the

use of balance scorecard as the increasing number of stakeholders within these firms requires the

use of comprehensive measurement systems that enables them to adopt the use of such systems

that helps in assessing both financial as well as non-financial performance. For example, Philips

Electronics has adopted the use of BSC for aligning its vision and mission with its overall

strategy. The use of BSC has proved to be largely beneficial for the company for assessing both

its qualitative and quantitative performance. It has been prove to be largely helpful for the

management of the company to measure its qualitative as well as quantitative performance and

thus facilitating the quick decision-making process (Neely, 2005).

Another example that can be cited in the context of a global corporation implemented a BSC is

Toyota Motor Corporation, recognized as most successful and renowned global automaker. The

12

company has developed its corporate scorecard in the year 2003 for assessing the performance of

its operational, internal business processes, financial and stakeholders. It has established its key

performance indicators in all the above mentioned business areas for continual review of

performance of overall business. The adoption of BSC concept has proved to be largely helpful

for the company to record sales and profits, improving customer loyalty and increasing employee

commitment and morale (Kaplan and Norton, 2005). Therefore, it can be stated from the above

examples that global corporations are adopting the use of BSC concept for attaining competitive

advantage by measuring of its financial and non-financial performance. The operational and

financial measures assessed by the development of BSC are aligned with the company’s

strategies for promoting its overall growth and development. It is regarded as critical for

promoting the success of companies in a highly competitive global environment (The Balanced

Scorecard, 2014).

The drawbacks that have been faced by the global corporations by the adoption of a balance

scorecard approach are its increasing complexity and consumption of large amount of resources

on the part of the company for its successful implementation. The implementation of BSC has

resulted in creating workload for some department of companies implementing it as it requires

gathering of complex data. It has also resulted in causing employee resistance and thus it has

been stated in this regard that these potential issues faced by the companies for adoption of BSC

have resulted in incurring them more costs rather than achieving benefits (Mahmoud , 2014).

company has developed its corporate scorecard in the year 2003 for assessing the performance of

its operational, internal business processes, financial and stakeholders. It has established its key

performance indicators in all the above mentioned business areas for continual review of

performance of overall business. The adoption of BSC concept has proved to be largely helpful

for the company to record sales and profits, improving customer loyalty and increasing employee

commitment and morale (Kaplan and Norton, 2005). Therefore, it can be stated from the above

examples that global corporations are adopting the use of BSC concept for attaining competitive

advantage by measuring of its financial and non-financial performance. The operational and

financial measures assessed by the development of BSC are aligned with the company’s

strategies for promoting its overall growth and development. It is regarded as critical for

promoting the success of companies in a highly competitive global environment (The Balanced

Scorecard, 2014).

The drawbacks that have been faced by the global corporations by the adoption of a balance

scorecard approach are its increasing complexity and consumption of large amount of resources

on the part of the company for its successful implementation. The implementation of BSC has

resulted in creating workload for some department of companies implementing it as it requires

gathering of complex data. It has also resulted in causing employee resistance and thus it has

been stated in this regard that these potential issues faced by the companies for adoption of BSC

have resulted in incurring them more costs rather than achieving benefits (Mahmoud , 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.