Management Accounting Report: Evaluating GSQ Limited's Performance

VerifiedAdded on 2023/01/13

|14

|3010

|42

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within the context of GSQ Limited, a UK-based manufacturing company. The report begins by defining management accounting and outlining various accounting systems, including cost accounting, job-costing, price optimization, and inventory management systems, along with their advantages. It then explores different management accounting reporting methods like budget and performance reports. The core of the report delves into costing methods, specifically absorption and marginal costing, and includes detailed cost cards and profit/loss statements to illustrate their application and interpret their impact. Furthermore, the report examines the uses of different planning tools like activity-based budgeting, rolling budgets, and flexible budgets, highlighting their advantages and disadvantages. Finally, it discusses how different management accounting systems help companies address financial problems. The report serves as a valuable resource for students seeking to understand and apply management accounting concepts.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

Management accounting system and their requirement..............................................................3

Different methods of management accounting reporting............................................................4

LO2..................................................................................................................................................4

LO3..................................................................................................................................................8

Explaining uses of different planning tools that are used in management accounting................8

LO 4...............................................................................................................................................11

Comparing the different management accounting system used in order to meet the financial

problems....................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

LO 1.................................................................................................................................................3

Management accounting system and their requirement..............................................................3

Different methods of management accounting reporting............................................................4

LO2..................................................................................................................................................4

LO3..................................................................................................................................................8

Explaining uses of different planning tools that are used in management accounting................8

LO 4...............................................................................................................................................11

Comparing the different management accounting system used in order to meet the financial

problems....................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION

Management accounting is defined as analysis and evaluation of the financial information

in order to take the management decisions for the betterment of the company (Otley, 2016). The

present report is based on company GSQ limited which is a manufacturing company located in

UK. The report will discuss about different management accounting system along with their

application and advantages and disadvantages. Further the report will apply some management

accounting tools in order to calculate the cost. Next the discussion will highlight the different

planning tools which the company can use to manage the budgets. In the end some management

accounting system will be discussed and how they help company in dealing with financial

problem will be outlined.

LO 1

Management accounting system and their requirement

The management accounting system are different types of system which help the

company in order to evaluate the performance of the company with help of financial accounting.

There are many different types of accounting system which GSQ Ltd can use in order to attain

their objectives which are as follows-

Cost accounting system- This is a system which is used by GSQ Ltd in order to ascertain

the cost of producing the product or services. This is very necessary for the company to ascertain

the cost because of the fact that in this cost only the profit margin is added and then charged to

consumers. This system is applied in GSQ ltd in order to calculate the cost of per unit production

and this is done with help of different tools like lean accounting, marginal costing and many

other different types.

Job- costing system- This is a system under which cost is charged to every job separately

in order to ascertain cost of every job. The whole production includes different types of job and

every job has its own particular cost which need to be assessed separately. This costing is applied

in GSQ for estimating the individual cost of each and every job separately.

Price optimising system- This is a system which help GSQ Ltd in order to calculate the

demand for the product and services at different price levels and what will be the response of the

consumers at all these different levels of price (Maas, Schaltegger and Crutzen, 2016). This

system is applied in GSQ for estimating its profit at different types of prices in the market.

Management accounting is defined as analysis and evaluation of the financial information

in order to take the management decisions for the betterment of the company (Otley, 2016). The

present report is based on company GSQ limited which is a manufacturing company located in

UK. The report will discuss about different management accounting system along with their

application and advantages and disadvantages. Further the report will apply some management

accounting tools in order to calculate the cost. Next the discussion will highlight the different

planning tools which the company can use to manage the budgets. In the end some management

accounting system will be discussed and how they help company in dealing with financial

problem will be outlined.

LO 1

Management accounting system and their requirement

The management accounting system are different types of system which help the

company in order to evaluate the performance of the company with help of financial accounting.

There are many different types of accounting system which GSQ Ltd can use in order to attain

their objectives which are as follows-

Cost accounting system- This is a system which is used by GSQ Ltd in order to ascertain

the cost of producing the product or services. This is very necessary for the company to ascertain

the cost because of the fact that in this cost only the profit margin is added and then charged to

consumers. This system is applied in GSQ ltd in order to calculate the cost of per unit production

and this is done with help of different tools like lean accounting, marginal costing and many

other different types.

Job- costing system- This is a system under which cost is charged to every job separately

in order to ascertain cost of every job. The whole production includes different types of job and

every job has its own particular cost which need to be assessed separately. This costing is applied

in GSQ for estimating the individual cost of each and every job separately.

Price optimising system- This is a system which help GSQ Ltd in order to calculate the

demand for the product and services at different price levels and what will be the response of the

consumers at all these different levels of price (Maas, Schaltegger and Crutzen, 2016). This

system is applied in GSQ for estimating its profit at different types of prices in the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system- The inventory is the most important part in the

manufacturing company like GSQ ltd because without inventory no work can be done. Thus, it is

very necessary for GSQ ltd to manage the inventory on time and this will assist the company in

completing manufacturing process on time (Quattrone, 2016). This include application of some

software which assist the company in managing their inventory on time do that the

manufacturing process can be completed with efficiency and effectiveness and on time as well.

Advantage of management accounting system- The use of different management

accounting system is very advantageous for GSQ because of the reason that these systems help

in proper planning and organizing for the business and its development. These management

accounting systems help GSQ in improving all the business activities and this assist the business

in building coordination among all the different business areas. Hence. This result in the

development of the business as a whole and not focusing on a single issue (Dekker, 2016).

Different methods of management accounting reporting

There are a variety of different types of management accounting reporting which helps

GSQ in reporting of all the information relating to management of business activities.

Budget report- This is a report in which all the estimated income and expenses are

recorded and management try to actually incur that much only. This will assist GSQ ltd in order

to make some estimation for all the possible income and expenses and to compare it with past

records.

Performance report- This is a type of report which is prepared by GSQ in order to

evaluate the performance of each and every individual. This help company in knowing the areas

in which company need to improve and the areas which are good.

The management accounting report is integrated with organization process because this

will enhance the process within the organization (Hopper and Bui, 2016). This is because of the

reason that all these reports will help organization in deciding all the major decision for the

betterment of the company.

LO2.

Absorption costing- It is the method that accumulates costs attached with the process of

production and apportioning them to an individual product. It is the type of costing which is

manufacturing company like GSQ ltd because without inventory no work can be done. Thus, it is

very necessary for GSQ ltd to manage the inventory on time and this will assist the company in

completing manufacturing process on time (Quattrone, 2016). This include application of some

software which assist the company in managing their inventory on time do that the

manufacturing process can be completed with efficiency and effectiveness and on time as well.

Advantage of management accounting system- The use of different management

accounting system is very advantageous for GSQ because of the reason that these systems help

in proper planning and organizing for the business and its development. These management

accounting systems help GSQ in improving all the business activities and this assist the business

in building coordination among all the different business areas. Hence. This result in the

development of the business as a whole and not focusing on a single issue (Dekker, 2016).

Different methods of management accounting reporting

There are a variety of different types of management accounting reporting which helps

GSQ in reporting of all the information relating to management of business activities.

Budget report- This is a report in which all the estimated income and expenses are

recorded and management try to actually incur that much only. This will assist GSQ ltd in order

to make some estimation for all the possible income and expenses and to compare it with past

records.

Performance report- This is a type of report which is prepared by GSQ in order to

evaluate the performance of each and every individual. This help company in knowing the areas

in which company need to improve and the areas which are good.

The management accounting report is integrated with organization process because this

will enhance the process within the organization (Hopper and Bui, 2016). This is because of the

reason that all these reports will help organization in deciding all the major decision for the

betterment of the company.

LO2.

Absorption costing- It is the method that accumulates costs attached with the process of

production and apportioning them to an individual product. It is the type of costing which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

needed by an accounting standard for creating valuation of an inventory. A product might absorb

wide range of the variable and the fixed costs.

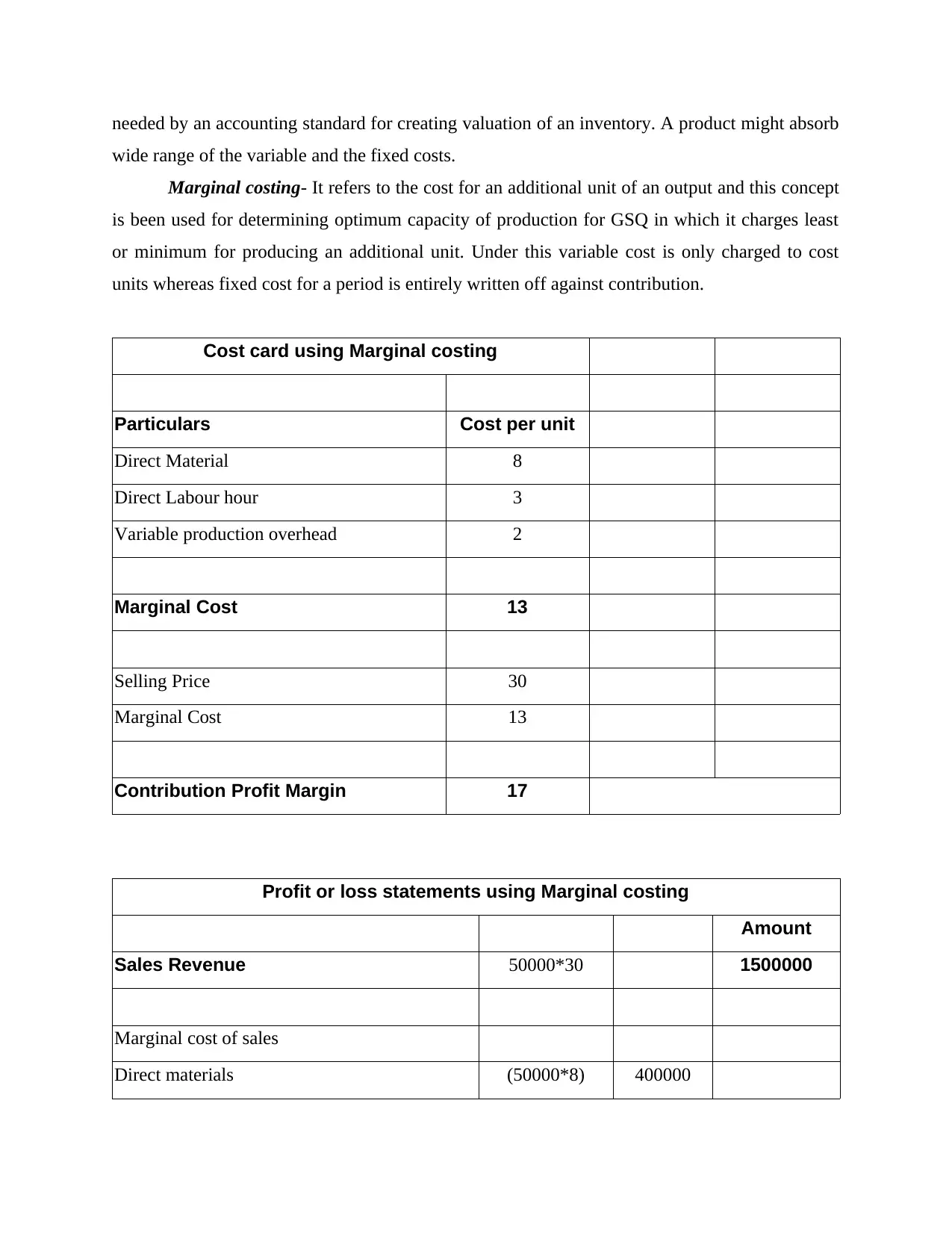

Marginal costing- It refers to the cost for an additional unit of an output and this concept

is been used for determining optimum capacity of production for GSQ in which it charges least

or minimum for producing an additional unit. Under this variable cost is only charged to cost

units whereas fixed cost for a period is entirely written off against contribution.

Cost card using Marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour hour 3

Variable production overhead 2

Marginal Cost 13

Selling Price 30

Marginal Cost 13

Contribution Profit Margin 17

Profit or loss statements using Marginal costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials (50000*8) 400000

wide range of the variable and the fixed costs.

Marginal costing- It refers to the cost for an additional unit of an output and this concept

is been used for determining optimum capacity of production for GSQ in which it charges least

or minimum for producing an additional unit. Under this variable cost is only charged to cost

units whereas fixed cost for a period is entirely written off against contribution.

Cost card using Marginal costing

Particulars Cost per unit

Direct Material 8

Direct Labour hour 3

Variable production overhead 2

Marginal Cost 13

Selling Price 30

Marginal Cost 13

Contribution Profit Margin 17

Profit or loss statements using Marginal costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials (50000*8) 400000

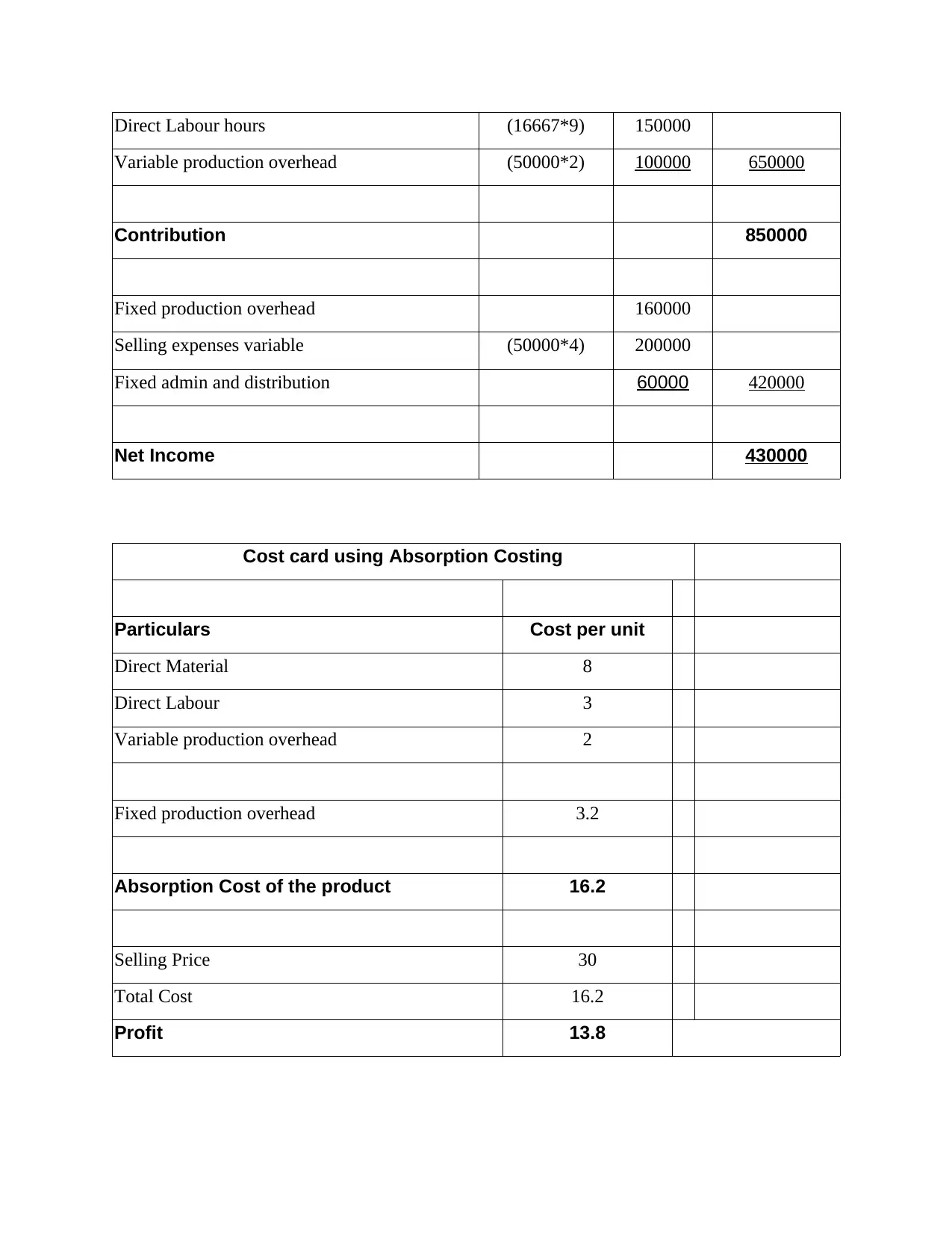

Direct Labour hours (16667*9) 150000

Variable production overhead (50000*2) 100000 650000

Contribution 850000

Fixed production overhead 160000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 420000

Net Income 430000

Cost card using Absorption Costing

Particulars Cost per unit

Direct Material 8

Direct Labour 3

Variable production overhead 2

Fixed production overhead 3.2

Absorption Cost of the product 16.2

Selling Price 30

Total Cost 16.2

Profit 13.8

Variable production overhead (50000*2) 100000 650000

Contribution 850000

Fixed production overhead 160000

Selling expenses variable (50000*4) 200000

Fixed admin and distribution 60000 420000

Net Income 430000

Cost card using Absorption Costing

Particulars Cost per unit

Direct Material 8

Direct Labour 3

Variable production overhead 2

Fixed production overhead 3.2

Absorption Cost of the product 16.2

Selling Price 30

Total Cost 16.2

Profit 13.8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

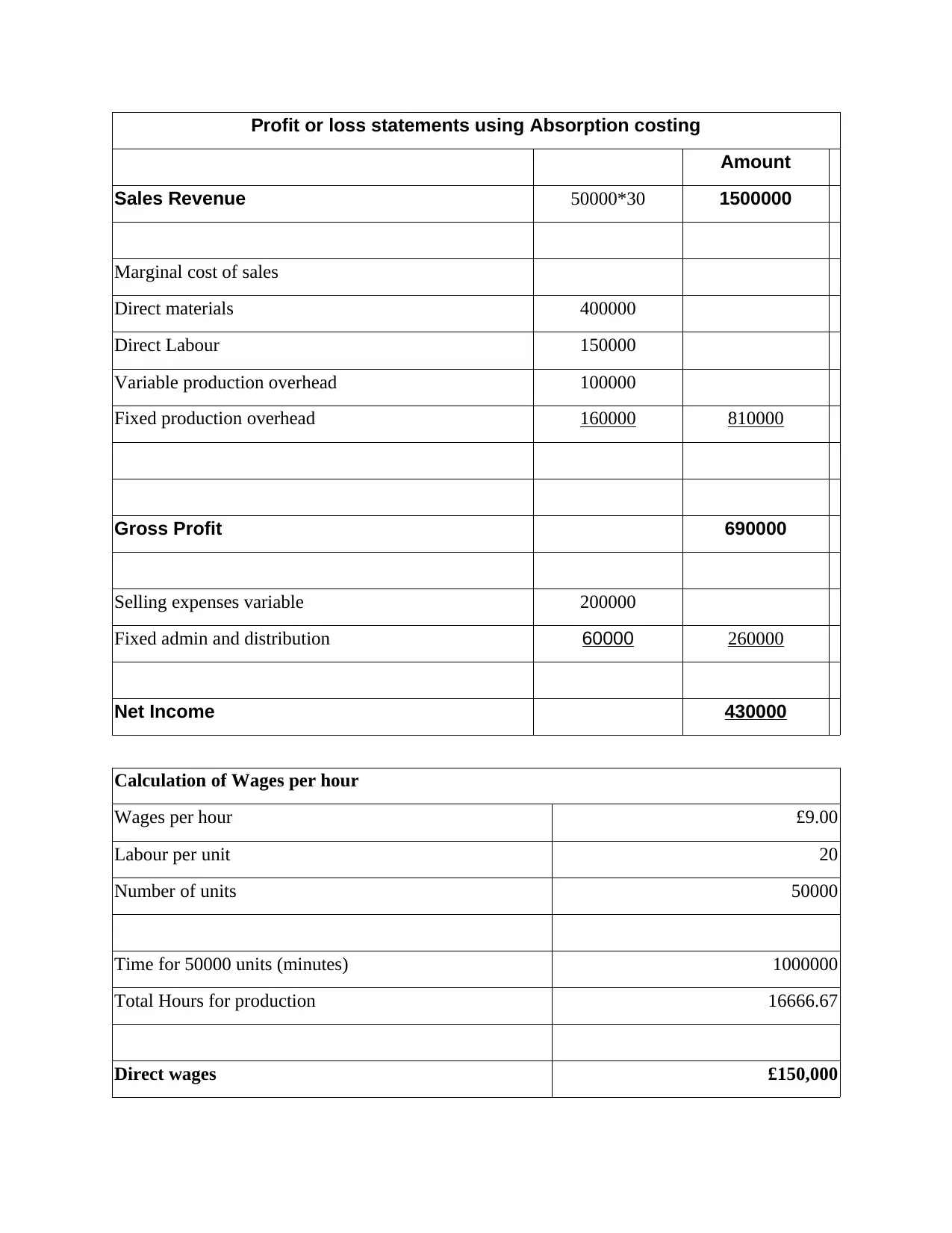

Profit or loss statements using Absorption costing

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials 400000

Direct Labour 150000

Variable production overhead 100000

Fixed production overhead 160000 810000

Gross Profit 690000

Selling expenses variable 200000

Fixed admin and distribution 60000 260000

Net Income 430000

Calculation of Wages per hour

Wages per hour £9.00

Labour per unit 20

Number of units 50000

Time for 50000 units (minutes) 1000000

Total Hours for production 16666.67

Direct wages £150,000

Amount

Sales Revenue 50000*30 1500000

Marginal cost of sales

Direct materials 400000

Direct Labour 150000

Variable production overhead 100000

Fixed production overhead 160000 810000

Gross Profit 690000

Selling expenses variable 200000

Fixed admin and distribution 60000 260000

Net Income 430000

Calculation of Wages per hour

Wages per hour £9.00

Labour per unit 20

Number of units 50000

Time for 50000 units (minutes) 1000000

Total Hours for production 16666.67

Direct wages £150,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- From the above results it has been stated that net profits resulted by

employing marginal and absorption is same that is £ 430000 because opening and closing stock

are not stated. Moreover, Absorption costing is seen as better technique than marginal costing

because it gives a true picture of profitability as it includes both fixed and marginal cost as part

of its production.

LO3.

Explaining uses of different planning tools that are used in management accounting

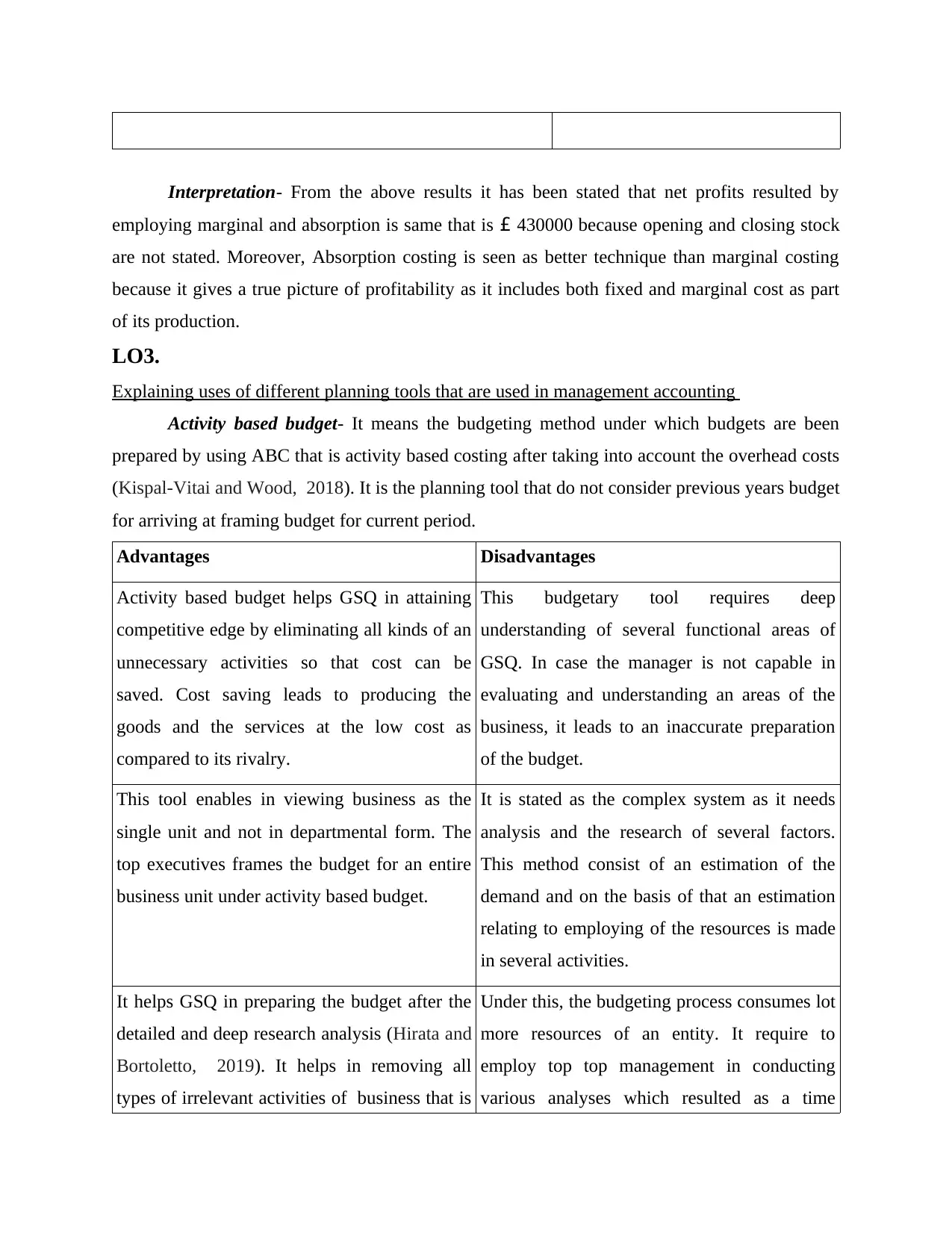

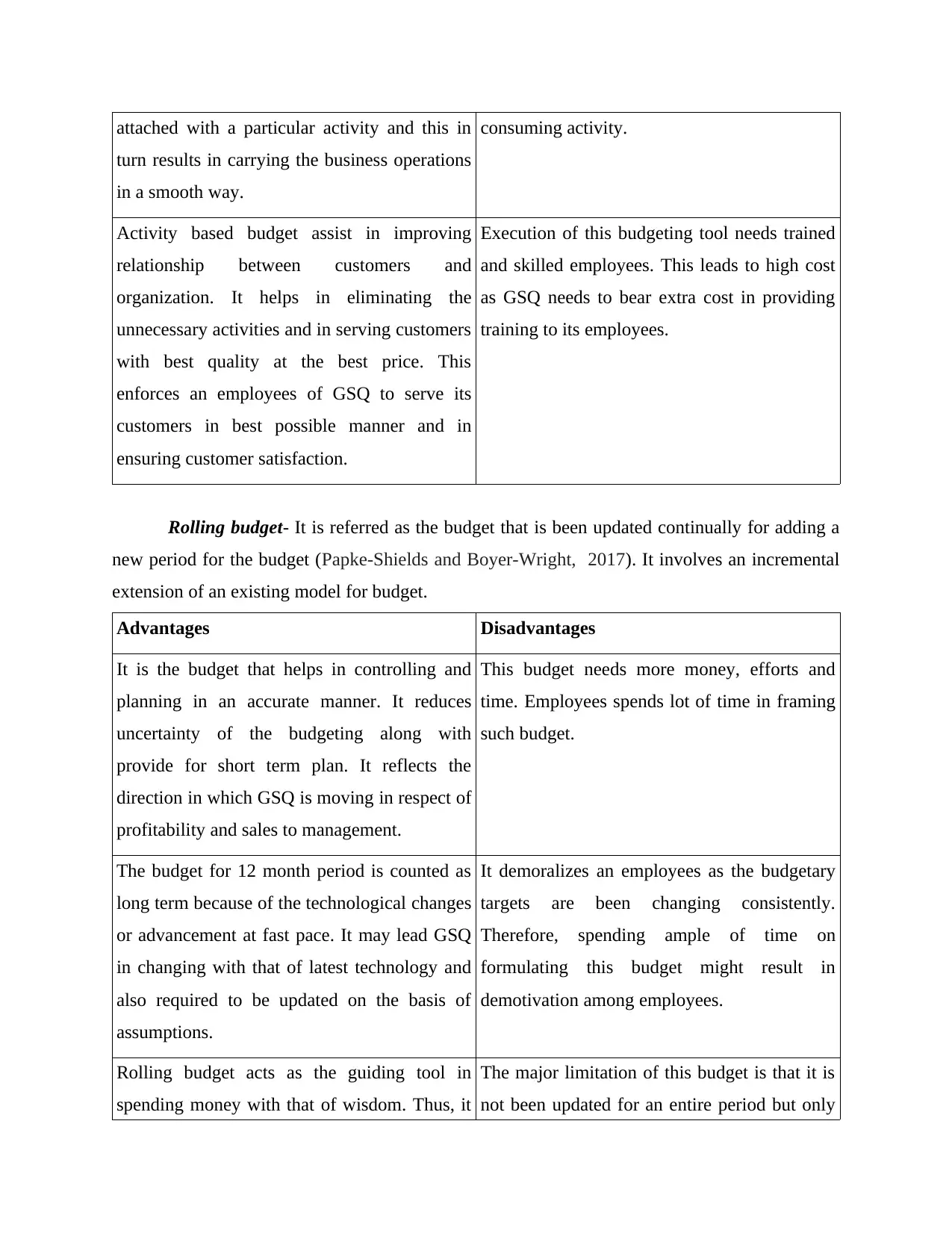

Activity based budget- It means the budgeting method under which budgets are been

prepared by using ABC that is activity based costing after taking into account the overhead costs

(Kispal-Vitai and Wood, 2018). It is the planning tool that do not consider previous years budget

for arriving at framing budget for current period.

Advantages Disadvantages

Activity based budget helps GSQ in attaining

competitive edge by eliminating all kinds of an

unnecessary activities so that cost can be

saved. Cost saving leads to producing the

goods and the services at the low cost as

compared to its rivalry.

This budgetary tool requires deep

understanding of several functional areas of

GSQ. In case the manager is not capable in

evaluating and understanding an areas of the

business, it leads to an inaccurate preparation

of the budget.

This tool enables in viewing business as the

single unit and not in departmental form. The

top executives frames the budget for an entire

business unit under activity based budget.

It is stated as the complex system as it needs

analysis and the research of several factors.

This method consist of an estimation of the

demand and on the basis of that an estimation

relating to employing of the resources is made

in several activities.

It helps GSQ in preparing the budget after the

detailed and deep research analysis (Hirata and

Bortoletto, 2019). It helps in removing all

types of irrelevant activities of business that is

Under this, the budgeting process consumes lot

more resources of an entity. It require to

employ top top management in conducting

various analyses which resulted as a time

employing marginal and absorption is same that is £ 430000 because opening and closing stock

are not stated. Moreover, Absorption costing is seen as better technique than marginal costing

because it gives a true picture of profitability as it includes both fixed and marginal cost as part

of its production.

LO3.

Explaining uses of different planning tools that are used in management accounting

Activity based budget- It means the budgeting method under which budgets are been

prepared by using ABC that is activity based costing after taking into account the overhead costs

(Kispal-Vitai and Wood, 2018). It is the planning tool that do not consider previous years budget

for arriving at framing budget for current period.

Advantages Disadvantages

Activity based budget helps GSQ in attaining

competitive edge by eliminating all kinds of an

unnecessary activities so that cost can be

saved. Cost saving leads to producing the

goods and the services at the low cost as

compared to its rivalry.

This budgetary tool requires deep

understanding of several functional areas of

GSQ. In case the manager is not capable in

evaluating and understanding an areas of the

business, it leads to an inaccurate preparation

of the budget.

This tool enables in viewing business as the

single unit and not in departmental form. The

top executives frames the budget for an entire

business unit under activity based budget.

It is stated as the complex system as it needs

analysis and the research of several factors.

This method consist of an estimation of the

demand and on the basis of that an estimation

relating to employing of the resources is made

in several activities.

It helps GSQ in preparing the budget after the

detailed and deep research analysis (Hirata and

Bortoletto, 2019). It helps in removing all

types of irrelevant activities of business that is

Under this, the budgeting process consumes lot

more resources of an entity. It require to

employ top top management in conducting

various analyses which resulted as a time

attached with a particular activity and this in

turn results in carrying the business operations

in a smooth way.

consuming activity.

Activity based budget assist in improving

relationship between customers and

organization. It helps in eliminating the

unnecessary activities and in serving customers

with best quality at the best price. This

enforces an employees of GSQ to serve its

customers in best possible manner and in

ensuring customer satisfaction.

Execution of this budgeting tool needs trained

and skilled employees. This leads to high cost

as GSQ needs to bear extra cost in providing

training to its employees.

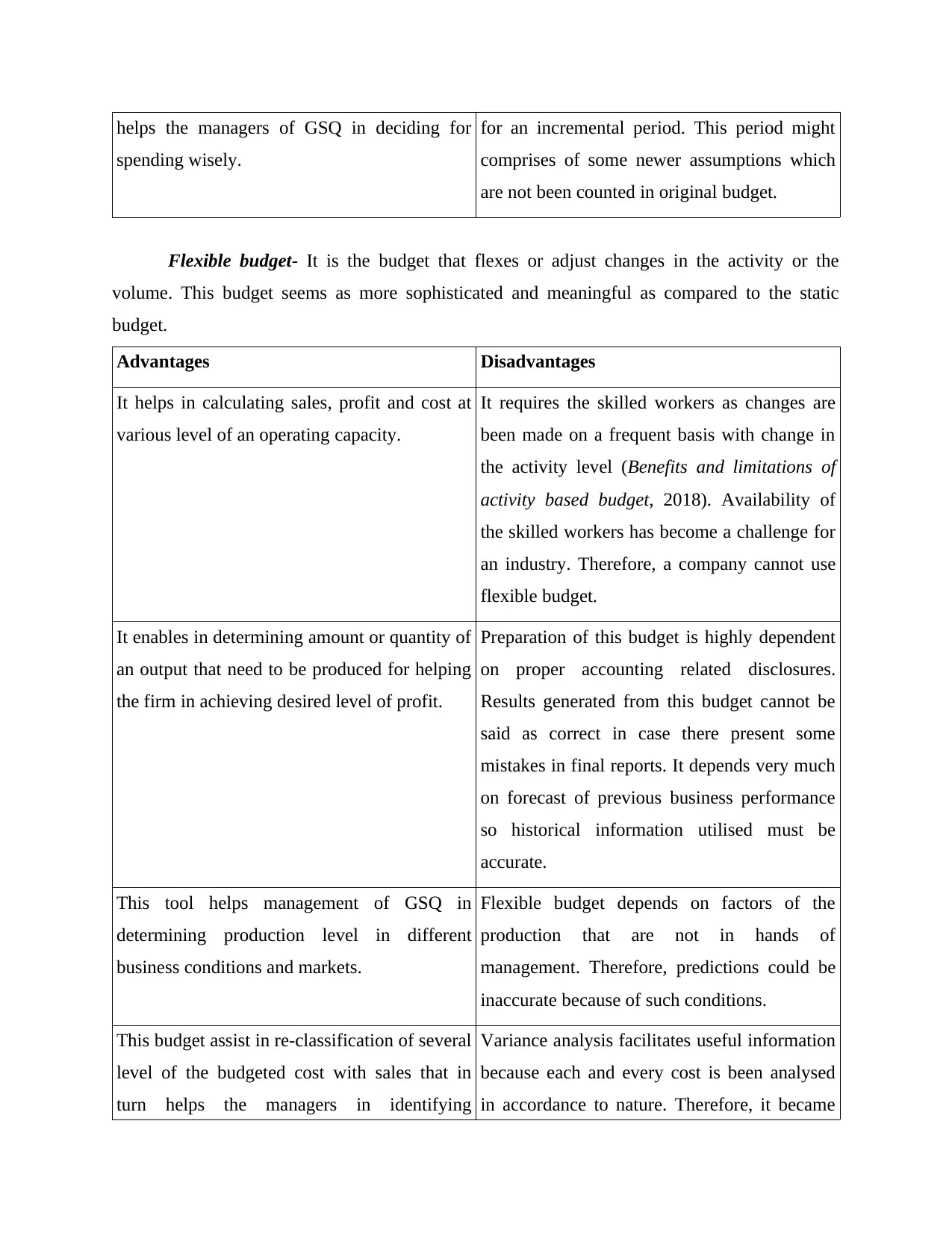

Rolling budget- It is referred as the budget that is been updated continually for adding a

new period for the budget (Papke-Shields and Boyer-Wright, 2017). It involves an incremental

extension of an existing model for budget.

Advantages Disadvantages

It is the budget that helps in controlling and

planning in an accurate manner. It reduces

uncertainty of the budgeting along with

provide for short term plan. It reflects the

direction in which GSQ is moving in respect of

profitability and sales to management.

This budget needs more money, efforts and

time. Employees spends lot of time in framing

such budget.

The budget for 12 month period is counted as

long term because of the technological changes

or advancement at fast pace. It may lead GSQ

in changing with that of latest technology and

also required to be updated on the basis of

assumptions.

It demoralizes an employees as the budgetary

targets are been changing consistently.

Therefore, spending ample of time on

formulating this budget might result in

demotivation among employees.

Rolling budget acts as the guiding tool in

spending money with that of wisdom. Thus, it

The major limitation of this budget is that it is

not been updated for an entire period but only

turn results in carrying the business operations

in a smooth way.

consuming activity.

Activity based budget assist in improving

relationship between customers and

organization. It helps in eliminating the

unnecessary activities and in serving customers

with best quality at the best price. This

enforces an employees of GSQ to serve its

customers in best possible manner and in

ensuring customer satisfaction.

Execution of this budgeting tool needs trained

and skilled employees. This leads to high cost

as GSQ needs to bear extra cost in providing

training to its employees.

Rolling budget- It is referred as the budget that is been updated continually for adding a

new period for the budget (Papke-Shields and Boyer-Wright, 2017). It involves an incremental

extension of an existing model for budget.

Advantages Disadvantages

It is the budget that helps in controlling and

planning in an accurate manner. It reduces

uncertainty of the budgeting along with

provide for short term plan. It reflects the

direction in which GSQ is moving in respect of

profitability and sales to management.

This budget needs more money, efforts and

time. Employees spends lot of time in framing

such budget.

The budget for 12 month period is counted as

long term because of the technological changes

or advancement at fast pace. It may lead GSQ

in changing with that of latest technology and

also required to be updated on the basis of

assumptions.

It demoralizes an employees as the budgetary

targets are been changing consistently.

Therefore, spending ample of time on

formulating this budget might result in

demotivation among employees.

Rolling budget acts as the guiding tool in

spending money with that of wisdom. Thus, it

The major limitation of this budget is that it is

not been updated for an entire period but only

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps the managers of GSQ in deciding for

spending wisely.

for an incremental period. This period might

comprises of some newer assumptions which

are not been counted in original budget.

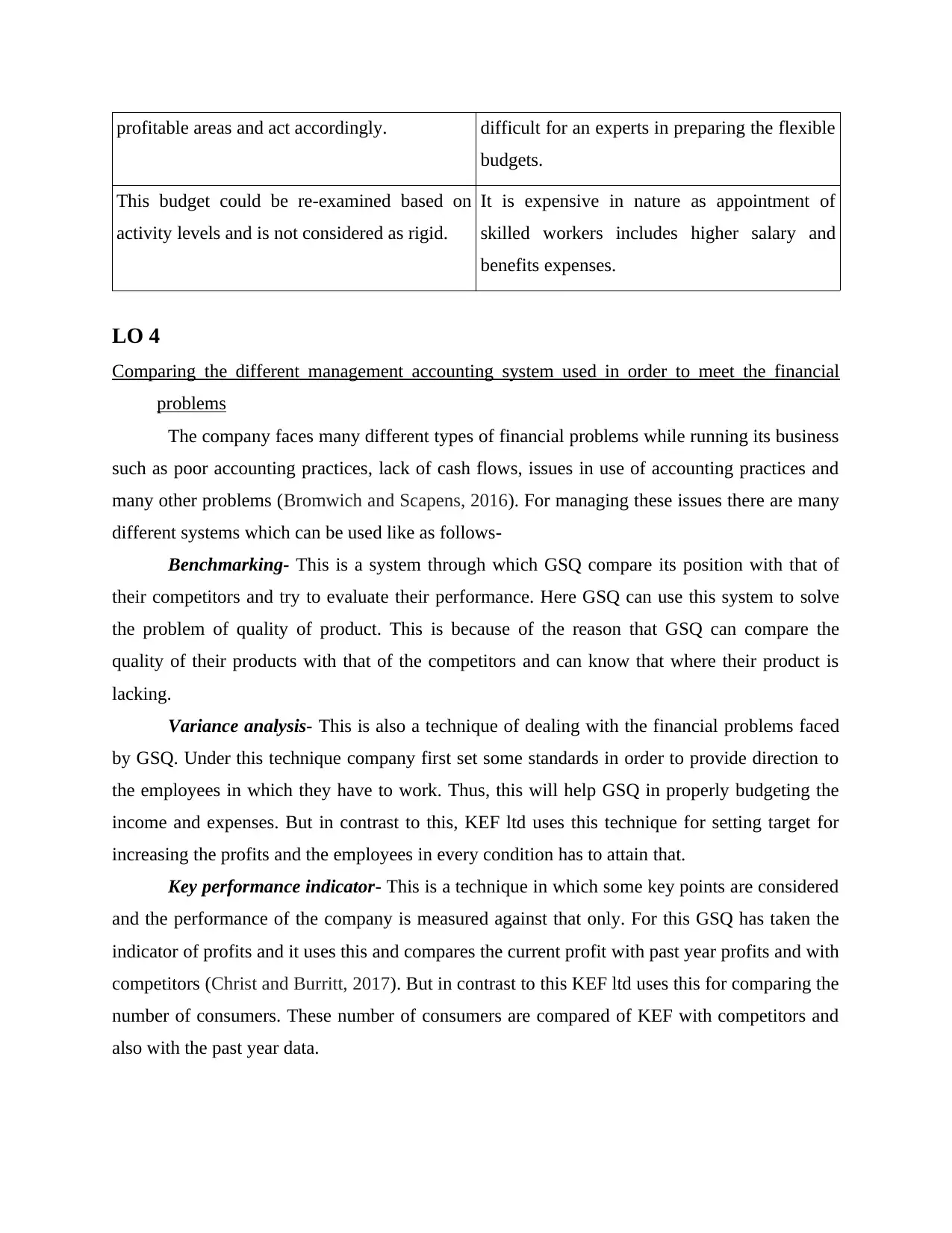

Flexible budget- It is the budget that flexes or adjust changes in the activity or the

volume. This budget seems as more sophisticated and meaningful as compared to the static

budget.

Advantages Disadvantages

It helps in calculating sales, profit and cost at

various level of an operating capacity.

It requires the skilled workers as changes are

been made on a frequent basis with change in

the activity level (Benefits and limitations of

activity based budget, 2018). Availability of

the skilled workers has become a challenge for

an industry. Therefore, a company cannot use

flexible budget.

It enables in determining amount or quantity of

an output that need to be produced for helping

the firm in achieving desired level of profit.

Preparation of this budget is highly dependent

on proper accounting related disclosures.

Results generated from this budget cannot be

said as correct in case there present some

mistakes in final reports. It depends very much

on forecast of previous business performance

so historical information utilised must be

accurate.

This tool helps management of GSQ in

determining production level in different

business conditions and markets.

Flexible budget depends on factors of the

production that are not in hands of

management. Therefore, predictions could be

inaccurate because of such conditions.

This budget assist in re-classification of several

level of the budgeted cost with sales that in

turn helps the managers in identifying

Variance analysis facilitates useful information

because each and every cost is been analysed

in accordance to nature. Therefore, it became

spending wisely.

for an incremental period. This period might

comprises of some newer assumptions which

are not been counted in original budget.

Flexible budget- It is the budget that flexes or adjust changes in the activity or the

volume. This budget seems as more sophisticated and meaningful as compared to the static

budget.

Advantages Disadvantages

It helps in calculating sales, profit and cost at

various level of an operating capacity.

It requires the skilled workers as changes are

been made on a frequent basis with change in

the activity level (Benefits and limitations of

activity based budget, 2018). Availability of

the skilled workers has become a challenge for

an industry. Therefore, a company cannot use

flexible budget.

It enables in determining amount or quantity of

an output that need to be produced for helping

the firm in achieving desired level of profit.

Preparation of this budget is highly dependent

on proper accounting related disclosures.

Results generated from this budget cannot be

said as correct in case there present some

mistakes in final reports. It depends very much

on forecast of previous business performance

so historical information utilised must be

accurate.

This tool helps management of GSQ in

determining production level in different

business conditions and markets.

Flexible budget depends on factors of the

production that are not in hands of

management. Therefore, predictions could be

inaccurate because of such conditions.

This budget assist in re-classification of several

level of the budgeted cost with sales that in

turn helps the managers in identifying

Variance analysis facilitates useful information

because each and every cost is been analysed

in accordance to nature. Therefore, it became

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitable areas and act accordingly. difficult for an experts in preparing the flexible

budgets.

This budget could be re-examined based on

activity levels and is not considered as rigid.

It is expensive in nature as appointment of

skilled workers includes higher salary and

benefits expenses.

LO 4

Comparing the different management accounting system used in order to meet the financial

problems

The company faces many different types of financial problems while running its business

such as poor accounting practices, lack of cash flows, issues in use of accounting practices and

many other problems (Bromwich and Scapens, 2016). For managing these issues there are many

different systems which can be used like as follows-

Benchmarking- This is a system through which GSQ compare its position with that of

their competitors and try to evaluate their performance. Here GSQ can use this system to solve

the problem of quality of product. This is because of the reason that GSQ can compare the

quality of their products with that of the competitors and can know that where their product is

lacking.

Variance analysis- This is also a technique of dealing with the financial problems faced

by GSQ. Under this technique company first set some standards in order to provide direction to

the employees in which they have to work. Thus, this will help GSQ in properly budgeting the

income and expenses. But in contrast to this, KEF ltd uses this technique for setting target for

increasing the profits and the employees in every condition has to attain that.

Key performance indicator- This is a technique in which some key points are considered

and the performance of the company is measured against that only. For this GSQ has taken the

indicator of profits and it uses this and compares the current profit with past year profits and with

competitors (Christ and Burritt, 2017). But in contrast to this KEF ltd uses this for comparing the

number of consumers. These number of consumers are compared of KEF with competitors and

also with the past year data.

budgets.

This budget could be re-examined based on

activity levels and is not considered as rigid.

It is expensive in nature as appointment of

skilled workers includes higher salary and

benefits expenses.

LO 4

Comparing the different management accounting system used in order to meet the financial

problems

The company faces many different types of financial problems while running its business

such as poor accounting practices, lack of cash flows, issues in use of accounting practices and

many other problems (Bromwich and Scapens, 2016). For managing these issues there are many

different systems which can be used like as follows-

Benchmarking- This is a system through which GSQ compare its position with that of

their competitors and try to evaluate their performance. Here GSQ can use this system to solve

the problem of quality of product. This is because of the reason that GSQ can compare the

quality of their products with that of the competitors and can know that where their product is

lacking.

Variance analysis- This is also a technique of dealing with the financial problems faced

by GSQ. Under this technique company first set some standards in order to provide direction to

the employees in which they have to work. Thus, this will help GSQ in properly budgeting the

income and expenses. But in contrast to this, KEF ltd uses this technique for setting target for

increasing the profits and the employees in every condition has to attain that.

Key performance indicator- This is a technique in which some key points are considered

and the performance of the company is measured against that only. For this GSQ has taken the

indicator of profits and it uses this and compares the current profit with past year profits and with

competitors (Christ and Burritt, 2017). But in contrast to this KEF ltd uses this for comparing the

number of consumers. These number of consumers are compared of KEF with competitors and

also with the past year data.

CONCLUSION

From the above it has been concluded that MA systems plays an essential role in

managing and maintaining an adequate inventory level with optimum use of resources. MA

reports helps in the preparing for the standards on the basis of which task are been performed

that in turn helps in ensuring proper controlling and gaining higher sales or revenue. Planning

tools enables the managers to focus on most crucial areas of the business and reviewing the

performance of an employees in order to eliminate variances. Further, there are different MA

systems such as benchmarking, balanced scorecard, variance analysis and key performance

indicators that helps GSQ in resolving its financial problem in an effective manner.

From the above it has been concluded that MA systems plays an essential role in

managing and maintaining an adequate inventory level with optimum use of resources. MA

reports helps in the preparing for the standards on the basis of which task are been performed

that in turn helps in ensuring proper controlling and gaining higher sales or revenue. Planning

tools enables the managers to focus on most crucial areas of the business and reviewing the

performance of an employees in order to eliminate variances. Further, there are different MA

systems such as benchmarking, balanced scorecard, variance analysis and key performance

indicators that helps GSQ in resolving its financial problem in an effective manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.