Indian Taxation System: An Argumentative Essay on GST Impact

VerifiedAdded on 2023/03/30

|5

|1028

|145

Essay

AI Summary

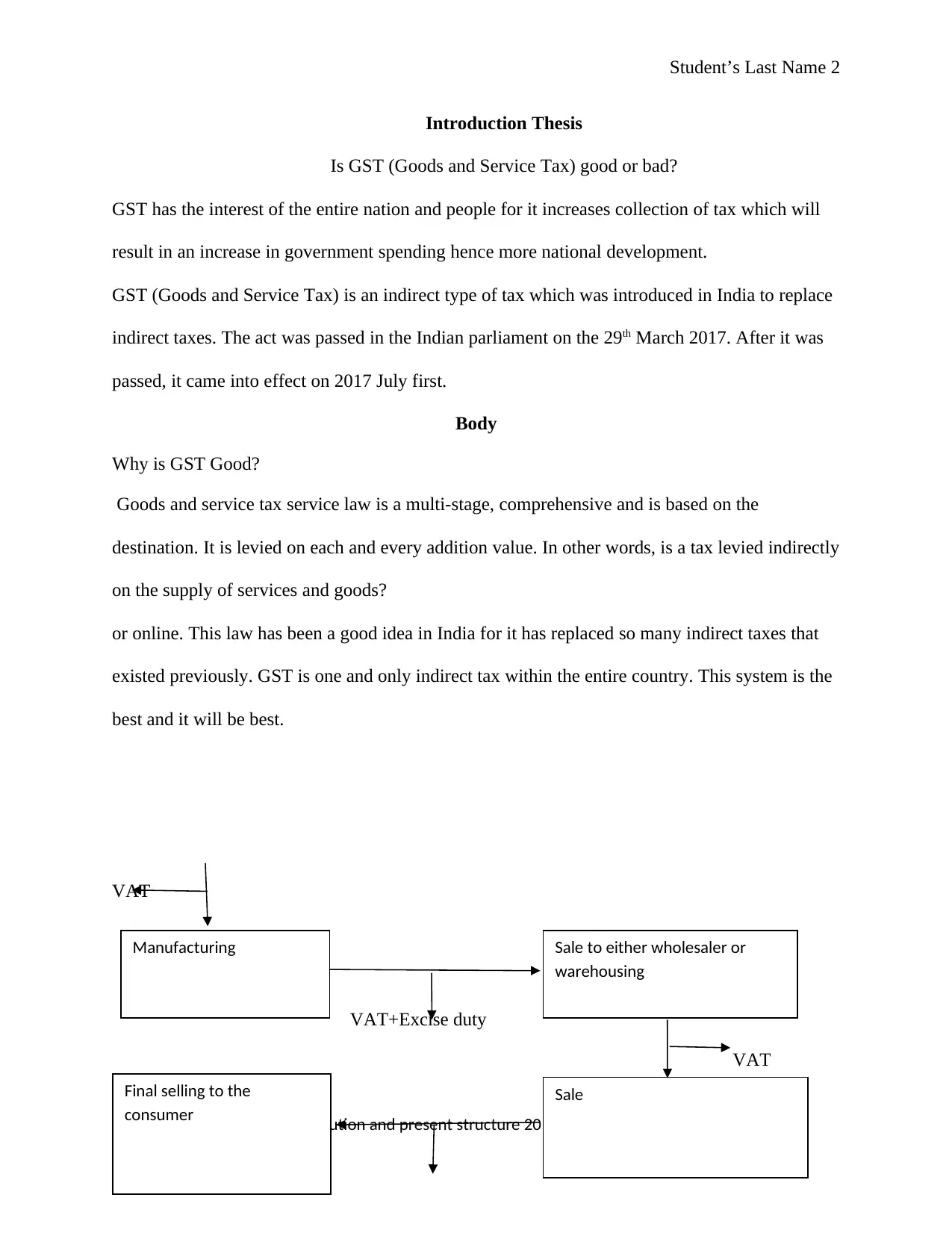

This essay provides an argumentative analysis of the Goods and Services Tax (GST) within the Indian taxation system, arguing that GST is beneficial for the nation due to increased tax collection and government spending, leading to national development. It explains GST as a multi-stage, comprehensive, and destination-based indirect tax that replaced numerous previous indirect taxes. The essay details the components of GST, including SGST, CGST, and IGST, and their application in intra-state and inter-state sales. While acknowledging concerns about the negative impact on the real estate market and increased costs in some sectors, the essay concludes that GST has simplified business operations, reduced prices, and positively impacted digitalization and macroeconomic growth, recommending its continued maintenance and improvement by the Indian government, with a focus on streamlining tax administration and stabilizing the GSTN portal. Desklib offers more solved assignments and resources for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.