University Economics Report: GST Impact on Batteries, EVs, and Petrol

VerifiedAdded on 2020/03/01

|8

|1550

|17

Report

AI Summary

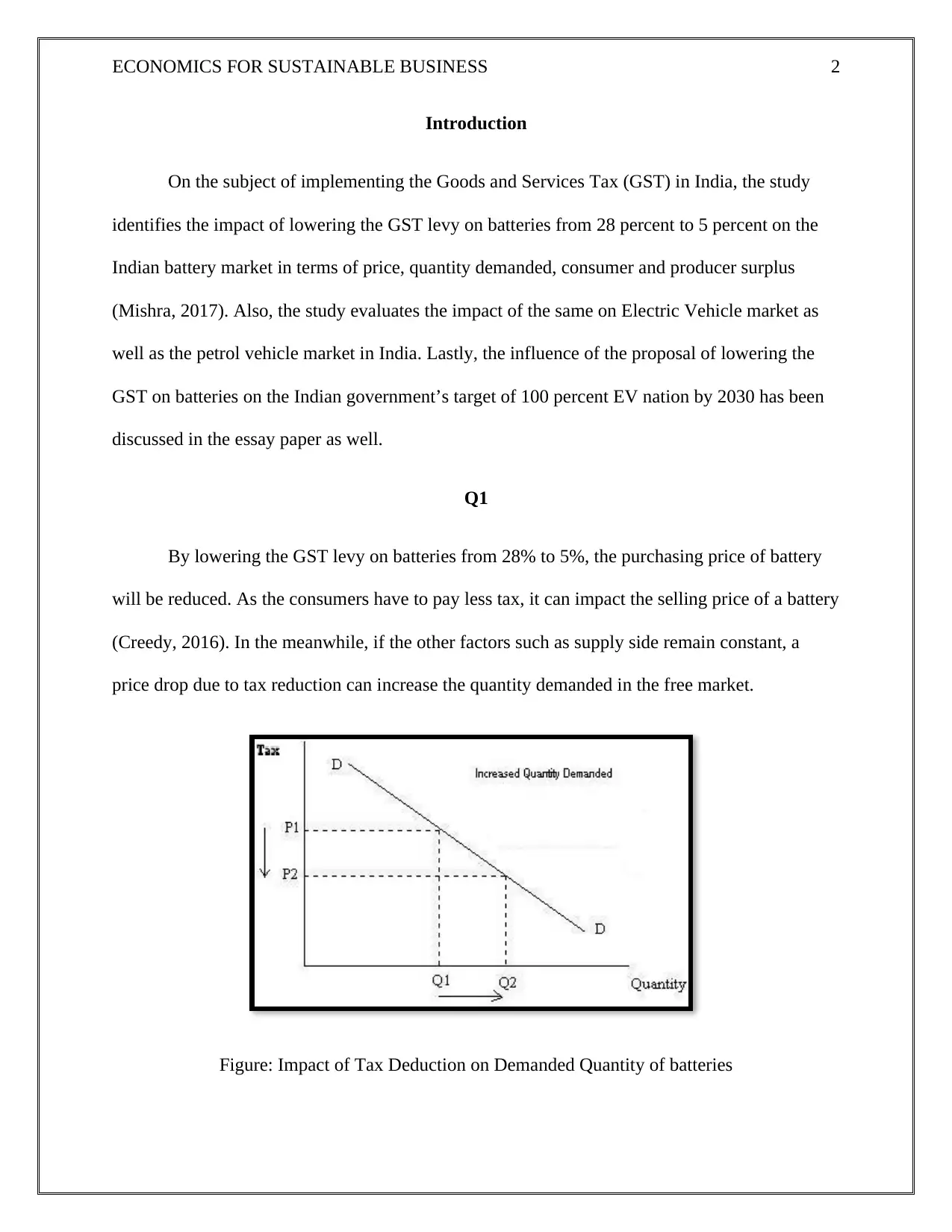

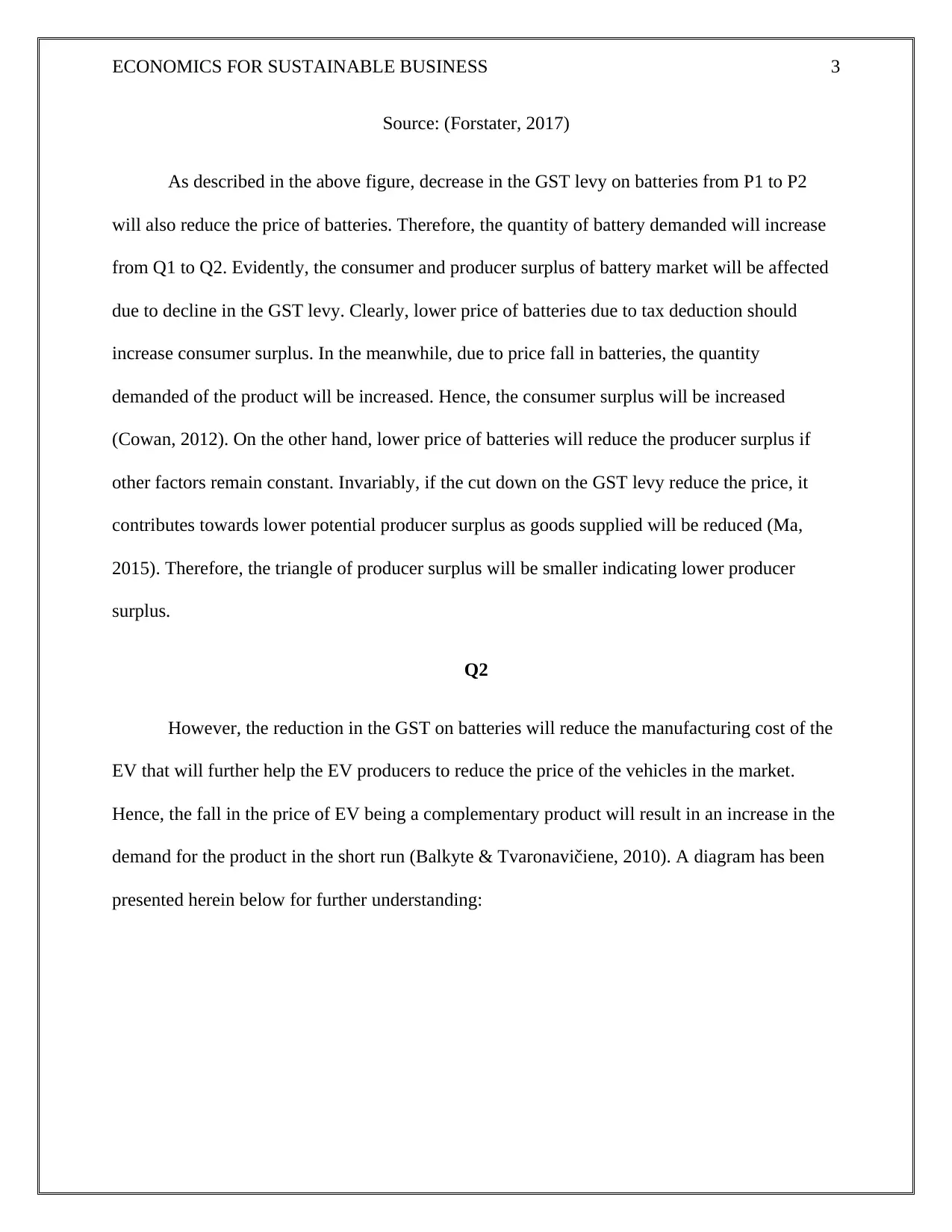

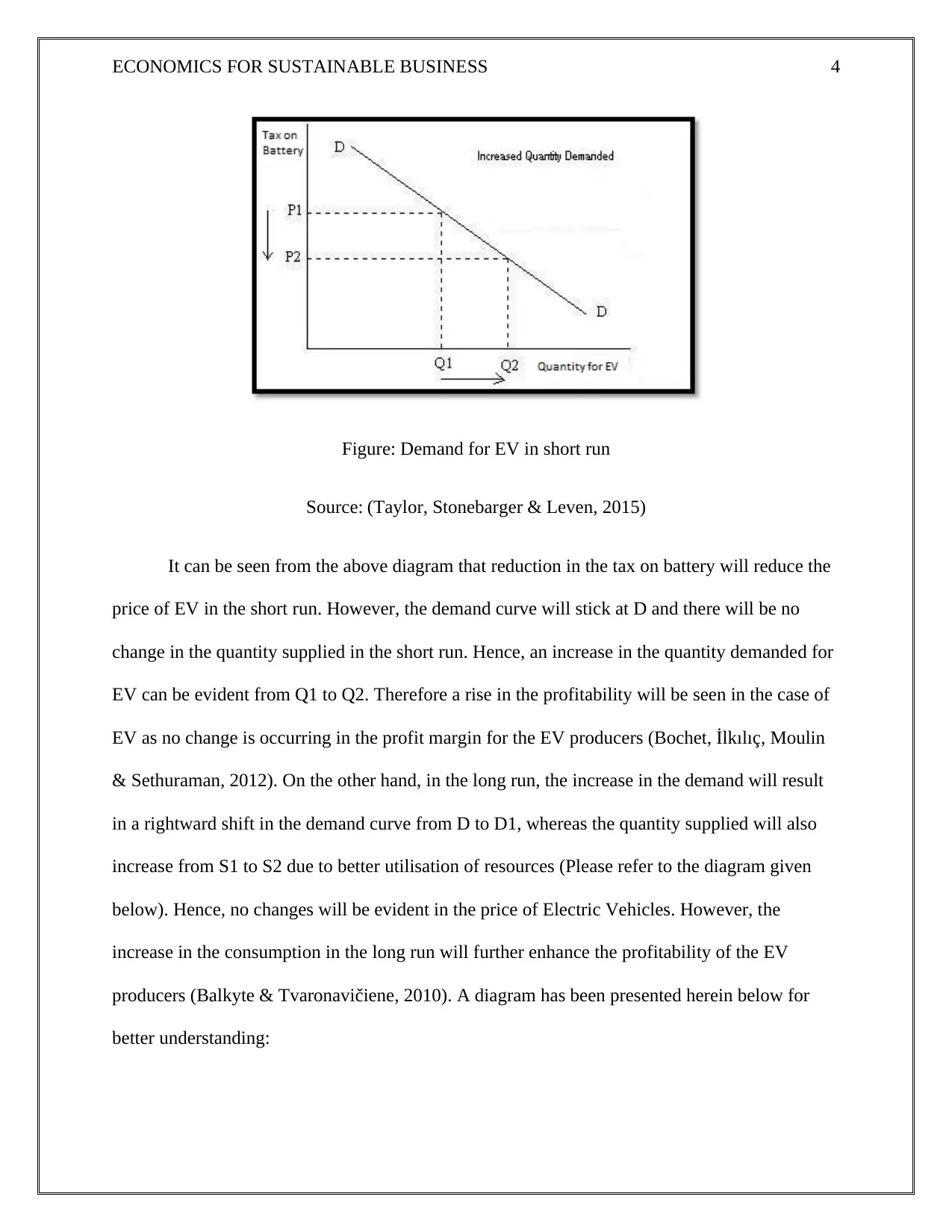

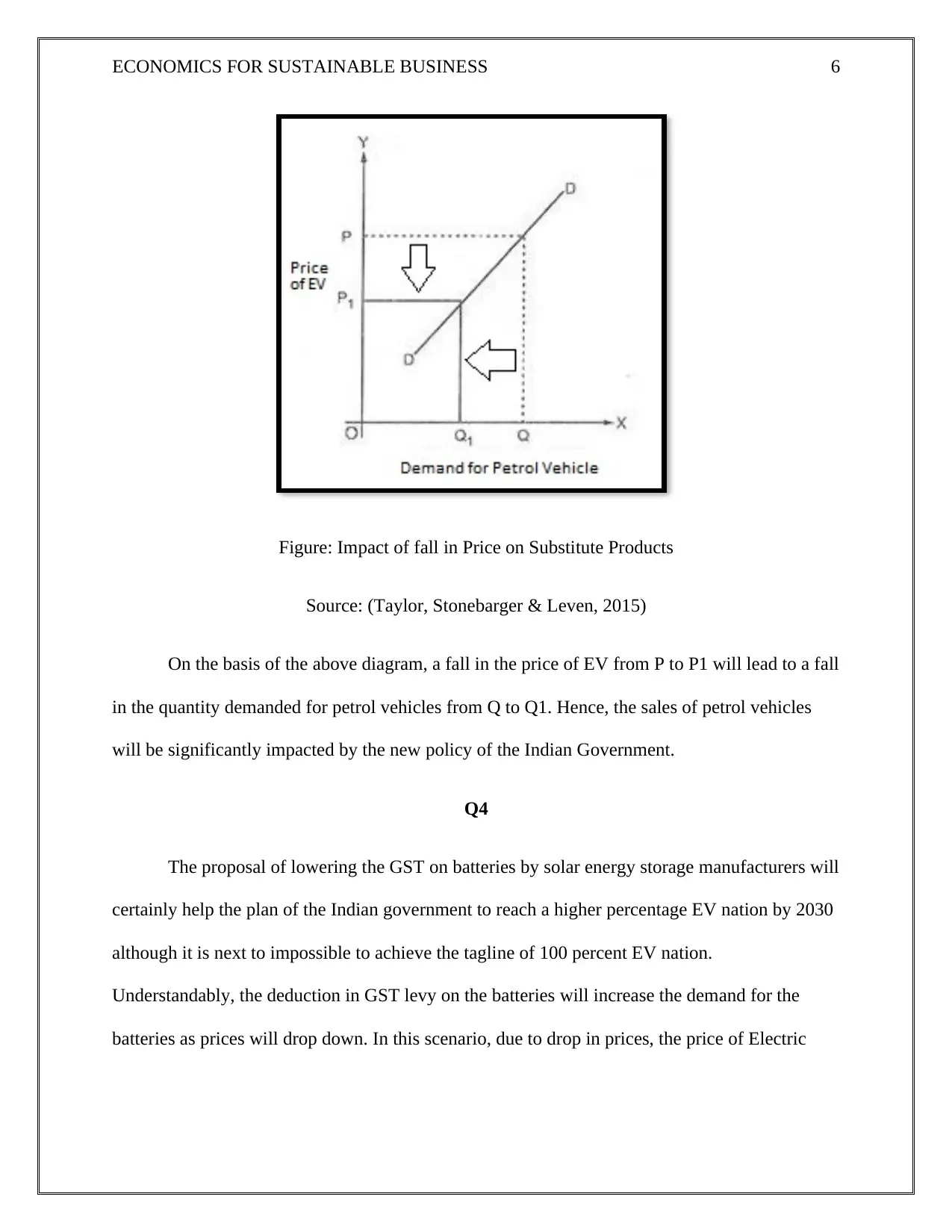

This report examines the economic implications of reducing the Goods and Services Tax (GST) on batteries in India. It analyzes the impact on battery prices, quantity demanded, consumer and producer surplus, and the electric vehicle (EV) market. The study investigates how a GST reduction from 28% to 5% affects the demand for EVs as a complementary good and petrol vehicles as substitutes. The report further assesses the long-term effects on EV profitability and the Indian government's goal of achieving 100% EV adoption by 2030, considering infrastructure limitations. The analysis uses economic principles to demonstrate how tax policies can influence market dynamics and consumer behavior within the context of sustainable business practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.