Financial Statement Analysis of GTN Limited: A Comprehensive Report

VerifiedAdded on 2022/12/27

|14

|2893

|76

Report

AI Summary

This report presents a comprehensive financial analysis of GTN Limited, a major broadcast media advertising platform. It begins with an industry analysis using Porter's Five Forces to assess the competitive landscape, followed by an examination of GTN's competitive strategies, including cost leadership and differentiation. The report then delves into an accounting analysis, defining and evaluating the nature of the financial statements, including the statement of profit and loss, balance sheet, statement of changes in equity, and statement of cash flow. Performance analysis highlights key trends and areas of concern, such as the impact of discontinued operations. The report further examines the accounting strategy and evaluates the quality of the financial information, including revenue recognition and other accounting policies. Finally, it includes recasting of financial statements to provide a clearer picture of GTN Limited's financial position. The analysis concludes with a discussion of the company's overall financial performance and strategic direction.

Running head: FINANCE

Finance

Name of the Student

Name of the University

Author Note

Finance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

Table of Contents

1. Introduction.........................................................................................................................2

2. Risk and profit potential of GTN Limited..........................................................................2

2.1 Industry analysis...............................................................................................................2

2.2 Competitive strategy analysis:.........................................................................................3

3. Accounting analysis...............................................................................................................4

3.1 Nature of the financial statement.....................................................................................4

3.2 Performance Analysis......................................................................................................5

3.3 Notes for the financial statement......................................................................................5

4. Accounting Strategy and Evaluation..................................................................................6

5. Recasting financial statements:...........................................................................................8

Statement of profit and loss:......................................................................................................8

Statement of cash flow:..............................................................................................................9

Statement of financial position:.................................................................................................9

6. Conclusion:.......................................................................................................................10

7. References list...................................................................................................................11

Table of Contents

1. Introduction.........................................................................................................................2

2. Risk and profit potential of GTN Limited..........................................................................2

2.1 Industry analysis...............................................................................................................2

2.2 Competitive strategy analysis:.........................................................................................3

3. Accounting analysis...............................................................................................................4

3.1 Nature of the financial statement.....................................................................................4

3.2 Performance Analysis......................................................................................................5

3.3 Notes for the financial statement......................................................................................5

4. Accounting Strategy and Evaluation..................................................................................6

5. Recasting financial statements:...........................................................................................8

Statement of profit and loss:......................................................................................................8

Statement of cash flow:..............................................................................................................9

Statement of financial position:.................................................................................................9

6. Conclusion:.......................................................................................................................10

7. References list...................................................................................................................11

FINANCE

1. Introduction

In this report, profit and risk potential and accounting analysis of GTN Ltd has been

illustrated. The evaluation of accounting strategy and recasting financial statement is also

presented in the report. GTN Limited is one of the largest broadcast media advertising

platforms. It mainly operates in Australia, Canada and United Kingdom. It provides the

advertisers with high impact campaigns. GTN began operations in Australia in 1997

(Gtnetwork.com.au, 2019). It provides a broad reach advertising platform that enables the

advertisers to reach large audiences effectively.

2. Risk and profit potential of GTN Limited

2.1 Industry analysis

Porter’s Five Forces is a strategic management tool. In these report five competitive

forces is used to effect viability and prepare a strategy for the development of GTN Ltd.

Rivalry between the existing competitors-The market in which GTN Ltd operates is

very competitive. Though it has concentrated competition amongst the present competitors in

Media sector, it has built a suitable distinction. The process of collaborating the competitors

is suitable, as it will result in increase of market size relatively than only opposing for the

minor market. By doing these, GTN Ltd does build up a scale and can compete better.

Threats of New Entrants- The way GTN Ltd tackle the threats is by inventing new

products and services. To attract new clients and to give old client a aim to purchase GTN

Ltd products. The economies of scale should be maintained in order to reduce the fixed cost

per unit. They have to spend money on exploration and expansion in addition to build

capacities. The opportunity for new applicants is very few as GTN Ltd keeps on defining the

1. Introduction

In this report, profit and risk potential and accounting analysis of GTN Ltd has been

illustrated. The evaluation of accounting strategy and recasting financial statement is also

presented in the report. GTN Limited is one of the largest broadcast media advertising

platforms. It mainly operates in Australia, Canada and United Kingdom. It provides the

advertisers with high impact campaigns. GTN began operations in Australia in 1997

(Gtnetwork.com.au, 2019). It provides a broad reach advertising platform that enables the

advertisers to reach large audiences effectively.

2. Risk and profit potential of GTN Limited

2.1 Industry analysis

Porter’s Five Forces is a strategic management tool. In these report five competitive

forces is used to effect viability and prepare a strategy for the development of GTN Ltd.

Rivalry between the existing competitors-The market in which GTN Ltd operates is

very competitive. Though it has concentrated competition amongst the present competitors in

Media sector, it has built a suitable distinction. The process of collaborating the competitors

is suitable, as it will result in increase of market size relatively than only opposing for the

minor market. By doing these, GTN Ltd does build up a scale and can compete better.

Threats of New Entrants- The way GTN Ltd tackle the threats is by inventing new

products and services. To attract new clients and to give old client a aim to purchase GTN

Ltd products. The economies of scale should be maintained in order to reduce the fixed cost

per unit. They have to spend money on exploration and expansion in addition to build

capacities. The opportunity for new applicants is very few as GTN Ltd keeps on defining the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

standards regularly and it has a huge market presence. Thus, it reduces the opportunity for the

new firms to earn extraordinary profits in the industry.

Bargaining Power of Buyers- GTN Ltd has a big network of clients. This can prove

a chance for the organization to simplify its revenue and production method and decrease the

negotiating power of consumers. It often gives reductions and contributions on the

recognized products to seek customers; and by inventing new products. If there is new

products in market than the negotiating power of the consumers becomes less (Campbell et

al., 2018). Therefore, the customers use to get attracted to new product launches and there is

less diversification of existing customers.

Bargaining Power of Suppliers- GTN Ltd has an efficient supply chain with

multiple suppliers. The company use to experiment with the new product designs and with

new diverse materials, so that if one of the raw materials values increases up it will shift to

another (Roslender and Nielsen, 2018). There are many suppliers whose firm is dependent

upon the firm; it is beneficial for the GTN Ltd as they has a less bargaining power compared

to other manufacturers.

Threats of Substitute Products or Services-The risk of substitute product is more as

a new products or services meet a comparable client required in numerous ways. The way

GTN Ltd tackles the threats is by rendering service and not only delivering products. By

realizing the basic needs of the consumers, it can develop an idea what the customer wants. If

the switching cost of the products is increased, then it will be easy for the company to control

the threat (Kihn & Ihantola, 2015).

2.2 Competitive strategy analysis:

i) Cost Leadership - The main generic strategy is to keep the position as market

leader used by GTN limited is cost leadership. It can be done through an efficient

standards regularly and it has a huge market presence. Thus, it reduces the opportunity for the

new firms to earn extraordinary profits in the industry.

Bargaining Power of Buyers- GTN Ltd has a big network of clients. This can prove

a chance for the organization to simplify its revenue and production method and decrease the

negotiating power of consumers. It often gives reductions and contributions on the

recognized products to seek customers; and by inventing new products. If there is new

products in market than the negotiating power of the consumers becomes less (Campbell et

al., 2018). Therefore, the customers use to get attracted to new product launches and there is

less diversification of existing customers.

Bargaining Power of Suppliers- GTN Ltd has an efficient supply chain with

multiple suppliers. The company use to experiment with the new product designs and with

new diverse materials, so that if one of the raw materials values increases up it will shift to

another (Roslender and Nielsen, 2018). There are many suppliers whose firm is dependent

upon the firm; it is beneficial for the GTN Ltd as they has a less bargaining power compared

to other manufacturers.

Threats of Substitute Products or Services-The risk of substitute product is more as

a new products or services meet a comparable client required in numerous ways. The way

GTN Ltd tackles the threats is by rendering service and not only delivering products. By

realizing the basic needs of the consumers, it can develop an idea what the customer wants. If

the switching cost of the products is increased, then it will be easy for the company to control

the threat (Kihn & Ihantola, 2015).

2.2 Competitive strategy analysis:

i) Cost Leadership - The main generic strategy is to keep the position as market

leader used by GTN limited is cost leadership. It can be done through an efficient

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

value chain management. This strategy allows the company to expand market

share, which makes an overall consumer market mix and it is done by targeting

middle class. Most of the consumers have a place high relevance to the pricing

factor. This strategy is the best strategy according to the customer segment. It

often give proposals of concessions and vouchers to attain higher turnover goals.

These strategies help in brand popularity (Liu & Wen, 2017).

ii) Differentiation – The adoption of this strategy allows GTN Ltd to expand the

customer base. It is used to differentiate the products by innovating and

addressing the customers demand. Through this process the product offerings is

used in way to stand out and be unique from the available alternatives. A unique

brand logo is used to establish a strong brand image in consumers mind.

Innovation is one of the important tool, which is used to differentiate from many

other brands (Williams & Dobelman, 2017). Through these, the customers

increase their preference of GTN Ltd over other brands.

3. Accounting analysis

3.1 Nature of the financial statement

i) Statement of profit & loss and other inclusive income for the time: This statement

displays the company’s incomes and costs for June 2018. The profit before income

tax was $34,204,000. As per the report, the loss for the year is $15,101,000. There

was a loss because of a loss from discontinued operation (Gtnetwork.com.au, 2019).

ii) Balance Sheet: The total asset was valued at $355,365,000 and a total liability was

valued at $106,667,000. Therefore, the net assets are $248,698,000. The total equity for the

report is $248, 698,000.

value chain management. This strategy allows the company to expand market

share, which makes an overall consumer market mix and it is done by targeting

middle class. Most of the consumers have a place high relevance to the pricing

factor. This strategy is the best strategy according to the customer segment. It

often give proposals of concessions and vouchers to attain higher turnover goals.

These strategies help in brand popularity (Liu & Wen, 2017).

ii) Differentiation – The adoption of this strategy allows GTN Ltd to expand the

customer base. It is used to differentiate the products by innovating and

addressing the customers demand. Through this process the product offerings is

used in way to stand out and be unique from the available alternatives. A unique

brand logo is used to establish a strong brand image in consumers mind.

Innovation is one of the important tool, which is used to differentiate from many

other brands (Williams & Dobelman, 2017). Through these, the customers

increase their preference of GTN Ltd over other brands.

3. Accounting analysis

3.1 Nature of the financial statement

i) Statement of profit & loss and other inclusive income for the time: This statement

displays the company’s incomes and costs for June 2018. The profit before income

tax was $34,204,000. As per the report, the loss for the year is $15,101,000. There

was a loss because of a loss from discontinued operation (Gtnetwork.com.au, 2019).

ii) Balance Sheet: The total asset was valued at $355,365,000 and a total liability was

valued at $106,667,000. Therefore, the net assets are $248,698,000. The total equity for the

report is $248, 698,000.

FINANCE

iii) Statement of changes in equity: The issues capital was $444,981,000 and the

accumulated loss was $202,823.000. Therefore, the total equity as per the report is

$248,698,000.

iv) Statement of Cash Flow: The net cash from operational activities is $9987, 000,

net cash used in financing activities is $9200, 000 and from financing activities is

50,787,000. So, the cash and cash equivalent for the conclusion of the year is

$52,232,000.

3.2 Performance Analysis

From the profit and loss statement, it can be seen that in 2017 there was a profit of

$6205,000 but in 2018 there is a loss of $15,101,000. Therefore, it directs that the

company did not be able to control their expenses properly. It does not mean a poor

presentation because there was a loss from discontinued operation.

From the balance sheet, the net asset has been decreased from $272,341,000 in 2017

to $248,698,000 in 2018. The main reason of this situation happened because of a

decrease of the total assets. Because of this, there is also a decrease of total equity from

$272,341,000 to $242,698,000 (Gtnetwork.com.au, 2019).

From the cash flow statement, the cash flow from operating activities also decreased.

For the year 2017, it was $24,486,000. It mainly happened because of the discontinued

operation. The net cash from financing activities also decreased because of payment of

dividends and the repayment of borrowings (Gtnetwork.com.au, 2019).

3.3 Notes for the financial statement

Revenue Recognition- Two of the important revenue sources, which is recognized, is

advertising and the other is interest and dividend income. Advertising revenue is earned

iii) Statement of changes in equity: The issues capital was $444,981,000 and the

accumulated loss was $202,823.000. Therefore, the total equity as per the report is

$248,698,000.

iv) Statement of Cash Flow: The net cash from operational activities is $9987, 000,

net cash used in financing activities is $9200, 000 and from financing activities is

50,787,000. So, the cash and cash equivalent for the conclusion of the year is

$52,232,000.

3.2 Performance Analysis

From the profit and loss statement, it can be seen that in 2017 there was a profit of

$6205,000 but in 2018 there is a loss of $15,101,000. Therefore, it directs that the

company did not be able to control their expenses properly. It does not mean a poor

presentation because there was a loss from discontinued operation.

From the balance sheet, the net asset has been decreased from $272,341,000 in 2017

to $248,698,000 in 2018. The main reason of this situation happened because of a

decrease of the total assets. Because of this, there is also a decrease of total equity from

$272,341,000 to $242,698,000 (Gtnetwork.com.au, 2019).

From the cash flow statement, the cash flow from operating activities also decreased.

For the year 2017, it was $24,486,000. It mainly happened because of the discontinued

operation. The net cash from financing activities also decreased because of payment of

dividends and the repayment of borrowings (Gtnetwork.com.au, 2019).

3.3 Notes for the financial statement

Revenue Recognition- Two of the important revenue sources, which is recognized, is

advertising and the other is interest and dividend income. Advertising revenue is earned

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

through commercial advertisements. Interest revenue and costs is stated on accrual basis and

from the investments in associates (Alewine et al,. 2016).

Trade receivables- Acknowledgement of debtors is done originally at fair value and

is reviewed on ongoing basis. The sum of impairment loss is recognized between the assets

carrying amount and the current value of projected cash flow. It is generally due for a

settlement period within 30 days (Klychova et al., 2015).

Goodwill- It represents the future economic benefits from a business amalgamation. It

is due for cash generating elements for the resolution of impairment annually. Some of the

groups is supervised for interior administration needs at a lower level, so that it can give a

better result in future.

Intangible assets- Initially, intangible assets are stated at cost and subsequently

carried at a cost less accumulated amortization and impairment losses. As per IAS 36, it

states that the assets will not recovered more than the recoverable amount, so that it can be

tested for impairment annually (Entwistle, 2015).

4. Accounting Strategy and Evaluation

The first question is that the company’s accounting policies compare to the norms of

the industry. The significant accounting policies that is used for the consolidated financial

statements are described below.

Basis of preparation: The Consolidated Financial statements of GTN limited is

prepared based on International Financial Reporting Standards (IFRS), which is issued by

International Accounting Standards Board (IASB). Historical Cost basis is used for the

preparation of financial statements. Financial assets and liabilities including derivative

through commercial advertisements. Interest revenue and costs is stated on accrual basis and

from the investments in associates (Alewine et al,. 2016).

Trade receivables- Acknowledgement of debtors is done originally at fair value and

is reviewed on ongoing basis. The sum of impairment loss is recognized between the assets

carrying amount and the current value of projected cash flow. It is generally due for a

settlement period within 30 days (Klychova et al., 2015).

Goodwill- It represents the future economic benefits from a business amalgamation. It

is due for cash generating elements for the resolution of impairment annually. Some of the

groups is supervised for interior administration needs at a lower level, so that it can give a

better result in future.

Intangible assets- Initially, intangible assets are stated at cost and subsequently

carried at a cost less accumulated amortization and impairment losses. As per IAS 36, it

states that the assets will not recovered more than the recoverable amount, so that it can be

tested for impairment annually (Entwistle, 2015).

4. Accounting Strategy and Evaluation

The first question is that the company’s accounting policies compare to the norms of

the industry. The significant accounting policies that is used for the consolidated financial

statements are described below.

Basis of preparation: The Consolidated Financial statements of GTN limited is

prepared based on International Financial Reporting Standards (IFRS), which is issued by

International Accounting Standards Board (IASB). Historical Cost basis is used for the

preparation of financial statements. Financial assets and liabilities including derivative

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

instruments, which is available for sale is measured at fair value. The assets, which is for sale

is measured at fair value less cost of disposal.

The company’s financial statement based on consolidation that is incorporates

financial statements of GTN Limited and all its affiliates. The transaction and stabilities

among the Groups are eliminated on alliance, which comprises uncollected incomes and

losses on transaction amongst Company and Subsidiaries. In the report, financial statement of

subsidiaries is accustomed to guarantee the constancy with the accounting procedures

accepted by company (Murphy, 2016).

Business Combination: The consideration, which is transported by the organisation to

tackle the management of the subsidiary, is premeditated as the sum of procurement time fair

values of assets shifted, liabilities ascending from a reliant deliberation preparation (Dubois

& Gadde, 2018). The organization distinguish the recognizable assets and liabilities, and it is

expected in a business grouping irrespective of whether it has been formerly documented in

the acquirer’s financial statement preceding to procurement.

Foreign currency translation- Usually, the combined financial statement is

presented in Australian dollars. These declarations are done in AUD, which is the operational

currency of the largest portion of the Company’s operations. By using the exchange rates, the

foreign currency transactions are translated. In the financial statements, a functional currency

is used other than AUD to denote all assets, liabilities and dealings of units and later

translated into AUD upon consolidation (Vitasek, 2016).

Revenue Recognition- The revenue from the advertising is earned and recognized at

the times commercial advertisements are broadcast. The payments received or the amount

invoiced in advance are deferred until the amount is earned. Thus, sales tax, goods and

services tax, value added tax are collected on behalf of the government authorities not

instruments, which is available for sale is measured at fair value. The assets, which is for sale

is measured at fair value less cost of disposal.

The company’s financial statement based on consolidation that is incorporates

financial statements of GTN Limited and all its affiliates. The transaction and stabilities

among the Groups are eliminated on alliance, which comprises uncollected incomes and

losses on transaction amongst Company and Subsidiaries. In the report, financial statement of

subsidiaries is accustomed to guarantee the constancy with the accounting procedures

accepted by company (Murphy, 2016).

Business Combination: The consideration, which is transported by the organisation to

tackle the management of the subsidiary, is premeditated as the sum of procurement time fair

values of assets shifted, liabilities ascending from a reliant deliberation preparation (Dubois

& Gadde, 2018). The organization distinguish the recognizable assets and liabilities, and it is

expected in a business grouping irrespective of whether it has been formerly documented in

the acquirer’s financial statement preceding to procurement.

Foreign currency translation- Usually, the combined financial statement is

presented in Australian dollars. These declarations are done in AUD, which is the operational

currency of the largest portion of the Company’s operations. By using the exchange rates, the

foreign currency transactions are translated. In the financial statements, a functional currency

is used other than AUD to denote all assets, liabilities and dealings of units and later

translated into AUD upon consolidation (Vitasek, 2016).

Revenue Recognition- The revenue from the advertising is earned and recognized at

the times commercial advertisements are broadcast. The payments received or the amount

invoiced in advance are deferred until the amount is earned. Thus, sales tax, goods and

services tax, value added tax are collected on behalf of the government authorities not

FINANCE

included as a component of revenue. The interest revenue and costs are stated on

accumulation method by means of the operative interest method (Falkner & Hiebl, 2015).

Next query is whether administrators have inducements to control incomes with the

usage of accounting decision. The fixed remuneration of CEO was $966,809, with a

minimum 5% increase per annum thereafter. The other executive management range between

$516,600 and $623,276, with a minimum 5% increase per annum thereafter. The non-

executive directors obtain a fixed monthly fee for participating. The director’s fees are

inclusive of superannuation where applied. The base fees are $128,000 for chairperson and

for other independent and non-executive directors is $90,000. The Non-Executive director

gets the remuneration of around $6,666. For the performance, based remuneration the

executive director was awarded with 38% and the other key management people was

awarded with 39 % and 43 % (Gtnetwork.com.au, 2019).

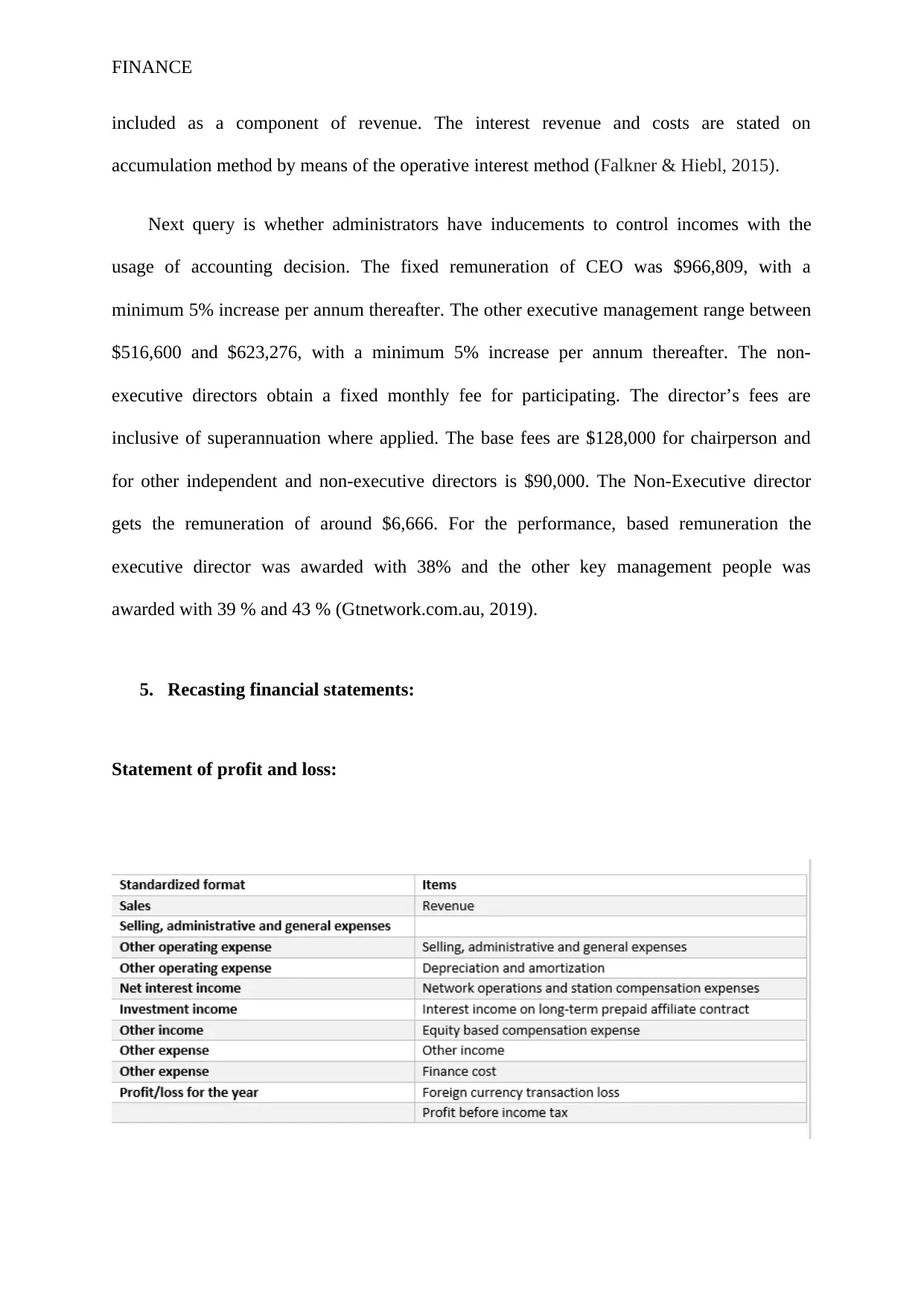

5. Recasting financial statements:

Statement of profit and loss:

included as a component of revenue. The interest revenue and costs are stated on

accumulation method by means of the operative interest method (Falkner & Hiebl, 2015).

Next query is whether administrators have inducements to control incomes with the

usage of accounting decision. The fixed remuneration of CEO was $966,809, with a

minimum 5% increase per annum thereafter. The other executive management range between

$516,600 and $623,276, with a minimum 5% increase per annum thereafter. The non-

executive directors obtain a fixed monthly fee for participating. The director’s fees are

inclusive of superannuation where applied. The base fees are $128,000 for chairperson and

for other independent and non-executive directors is $90,000. The Non-Executive director

gets the remuneration of around $6,666. For the performance, based remuneration the

executive director was awarded with 38% and the other key management people was

awarded with 39 % and 43 % (Gtnetwork.com.au, 2019).

5. Recasting financial statements:

Statement of profit and loss:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

Statement of cash flow:

Statement of financial position:

Statement of cash flow:

Statement of financial position:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

6. Conclusion:

From the investigation of the financial performance of GTN limited in the current year, it can

be said that the company has performed poorly compared to last year. It is so because the

company incurred loss, however, total amount of comprehensive income increased

considerably. Success of the company can be attributed to the value proposition and their

ability to provide differentiated platforms assisted advertisers in reaching the audiences

effectively and frequently. Investors seeking investment in the company should hold as the

company in running in loss due to the combination of increasing expense and lower revenue.

6. Conclusion:

From the investigation of the financial performance of GTN limited in the current year, it can

be said that the company has performed poorly compared to last year. It is so because the

company incurred loss, however, total amount of comprehensive income increased

considerably. Success of the company can be attributed to the value proposition and their

ability to provide differentiated platforms assisted advertisers in reaching the audiences

effectively and frequently. Investors seeking investment in the company should hold as the

company in running in loss due to the combination of increasing expense and lower revenue.

FINANCE

7. References list

Alewine, H. C., Allport, C. D., & Shen, W. C. M. (2016). How measurement framing and

accounting information system evaluation mode influence environmental performance

judgments. International Journal of Accounting Information Systems, 23, 28-44.

Annual Report. (2019). Gtnetwork.com.au. Retrieved 1 September 2019, from

http://www.gtnetwork.com.au/FormBuilder/_Resource/_module/sGsmQsi2oE6q0dzY

NAADzA/file/reports/annual/GTN-Annual-Report-2018.pdf

Campbell, J. L., Khan, U., & Pierce, S. (2018). The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number

161. Columbia Business School Research Paper, (17-94).

Dubois, A., & Gadde, L. E. (2018). Accounting and Networking. In Accounting, Innovation

and Inter-Organisational Relationships (pp. 197-215). Routledge.

Entwistle, G. (2015). Reflections on teaching financial statement analysis. Accounting

Education, 24(6), pp.555-558.

Falkner, E. M., & Hiebl, M. R. (2015). Risk management in SMEs: a systematic review of

available evidence. The Journal of Risk Finance, 16(2), 122-144.

Kihn, L. A., & Ihantola, E. M. (2015). Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management, 12(3), 230-255.

Klychova, G., Antonova, N., Klychova, A., & Fakhretdinova, E. (2015). Development of

accounting and financial reporting for small and medium-sized businesses in

accordance with international financial reporting standards.

7. References list

Alewine, H. C., Allport, C. D., & Shen, W. C. M. (2016). How measurement framing and

accounting information system evaluation mode influence environmental performance

judgments. International Journal of Accounting Information Systems, 23, 28-44.

Annual Report. (2019). Gtnetwork.com.au. Retrieved 1 September 2019, from

http://www.gtnetwork.com.au/FormBuilder/_Resource/_module/sGsmQsi2oE6q0dzY

NAADzA/file/reports/annual/GTN-Annual-Report-2018.pdf

Campbell, J. L., Khan, U., & Pierce, S. (2018). The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number

161. Columbia Business School Research Paper, (17-94).

Dubois, A., & Gadde, L. E. (2018). Accounting and Networking. In Accounting, Innovation

and Inter-Organisational Relationships (pp. 197-215). Routledge.

Entwistle, G. (2015). Reflections on teaching financial statement analysis. Accounting

Education, 24(6), pp.555-558.

Falkner, E. M., & Hiebl, M. R. (2015). Risk management in SMEs: a systematic review of

available evidence. The Journal of Risk Finance, 16(2), 122-144.

Kihn, L. A., & Ihantola, E. M. (2015). Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management, 12(3), 230-255.

Klychova, G., Antonova, N., Klychova, A., & Fakhretdinova, E. (2015). Development of

accounting and financial reporting for small and medium-sized businesses in

accordance with international financial reporting standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.