Gumboot Throwing WA Finance and Funding Report Analysis

VerifiedAdded on 2022/11/14

|20

|4950

|467

Report

AI Summary

This report provides a comprehensive financial analysis of Gumboot Throwing WA, evaluating its performance based on provided financial statements. The analysis includes an examination of revenue streams, expenses, and various financial ratios such as liquidity, debt-to-equity, and return on assets to assess the organization's financial health. The report also explores the impact of external events, specifically a reduction in grants, on the financial viability and sustainability of the organization, and suggests strategies to mitigate revenue loss. Furthermore, the report includes the development of a detailed budget for a proposed new event, with a rationale for the figures presented, aiming to improve revenue generation and manage operational expenses effectively. The conclusion offers recommendations based on the financial findings.

Running head: SPORT AND EVENTS FUNDING AND FINANCE

Sport, events funding, and finance

Name of the Student:

Name of the University:

Authors Note:

Sport, events funding, and finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SPORT, EVENTS FUNDING, AND FINANCE

1

Table of Contents

Introduction and Background:....................................................................................................2

Part A – Funding and Financial Analysis..................................................................................2

Type and nature of revenue and expenses of the organisation:.................................................2

Identifying the revenue streams:................................................................................................3

Type and nature of assets and liabilities:...................................................................................5

Liquidity ratio of the organisation:............................................................................................5

Analysing the cash reserves of the company:............................................................................6

Analysing the surplus for the financial year:.............................................................................6

Return on Assets:.......................................................................................................................7

Debt to equity ratio:...................................................................................................................7

Net Equity:.................................................................................................................................7

Identifying the potential development improvement in relevant areas:.....................................8

Part B – Financial Impact of External Event...........................................................................10

Outlining the impact of the reduction in grant on the financial viability and sustainability of

Gumboot Throwing WA:.........................................................................................................10

Explaining what needs to be done to ameliorate this loss of revenue:.....................................15

Part C – Event Budget..............................................................................................................15

Describing the event that has decided to conduct and prepare a detailed budget for the event:

..................................................................................................................................................15

Providing a rationale for the figures contained in the budget:.................................................16

Conclusion and Recommendations:.........................................................................................16

References and Bibliography:..................................................................................................17

1

Table of Contents

Introduction and Background:....................................................................................................2

Part A – Funding and Financial Analysis..................................................................................2

Type and nature of revenue and expenses of the organisation:.................................................2

Identifying the revenue streams:................................................................................................3

Type and nature of assets and liabilities:...................................................................................5

Liquidity ratio of the organisation:............................................................................................5

Analysing the cash reserves of the company:............................................................................6

Analysing the surplus for the financial year:.............................................................................6

Return on Assets:.......................................................................................................................7

Debt to equity ratio:...................................................................................................................7

Net Equity:.................................................................................................................................7

Identifying the potential development improvement in relevant areas:.....................................8

Part B – Financial Impact of External Event...........................................................................10

Outlining the impact of the reduction in grant on the financial viability and sustainability of

Gumboot Throwing WA:.........................................................................................................10

Explaining what needs to be done to ameliorate this loss of revenue:.....................................15

Part C – Event Budget..............................................................................................................15

Describing the event that has decided to conduct and prepare a detailed budget for the event:

..................................................................................................................................................15

Providing a rationale for the figures contained in the budget:.................................................16

Conclusion and Recommendations:.........................................................................................16

References and Bibliography:..................................................................................................17

SPORT, EVENTS FUNDING, AND FINANCE

2

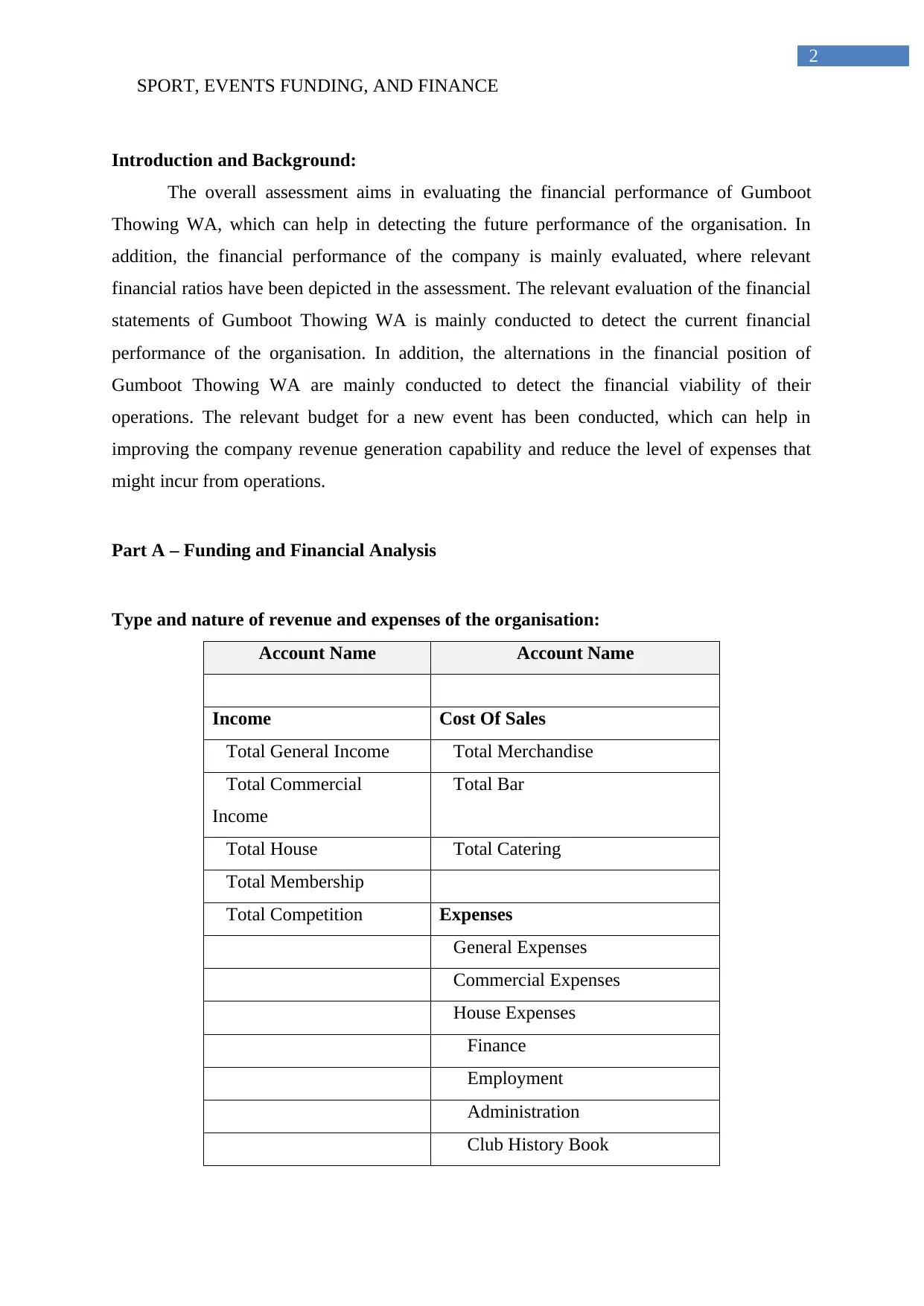

Introduction and Background:

The overall assessment aims in evaluating the financial performance of Gumboot

Thowing WA, which can help in detecting the future performance of the organisation. In

addition, the financial performance of the company is mainly evaluated, where relevant

financial ratios have been depicted in the assessment. The relevant evaluation of the financial

statements of Gumboot Thowing WA is mainly conducted to detect the current financial

performance of the organisation. In addition, the alternations in the financial position of

Gumboot Thowing WA are mainly conducted to detect the financial viability of their

operations. The relevant budget for a new event has been conducted, which can help in

improving the company revenue generation capability and reduce the level of expenses that

might incur from operations.

Part A – Funding and Financial Analysis

Type and nature of revenue and expenses of the organisation:

Account Name Account Name

Income Cost Of Sales

Total General Income Total Merchandise

Total Commercial

Income

Total Bar

Total House Total Catering

Total Membership

Total Competition Expenses

General Expenses

Commercial Expenses

House Expenses

Finance

Employment

Administration

Club History Book

2

Introduction and Background:

The overall assessment aims in evaluating the financial performance of Gumboot

Thowing WA, which can help in detecting the future performance of the organisation. In

addition, the financial performance of the company is mainly evaluated, where relevant

financial ratios have been depicted in the assessment. The relevant evaluation of the financial

statements of Gumboot Thowing WA is mainly conducted to detect the current financial

performance of the organisation. In addition, the alternations in the financial position of

Gumboot Thowing WA are mainly conducted to detect the financial viability of their

operations. The relevant budget for a new event has been conducted, which can help in

improving the company revenue generation capability and reduce the level of expenses that

might incur from operations.

Part A – Funding and Financial Analysis

Type and nature of revenue and expenses of the organisation:

Account Name Account Name

Income Cost Of Sales

Total General Income Total Merchandise

Total Commercial

Income

Total Bar

Total House Total Catering

Total Membership

Total Competition Expenses

General Expenses

Commercial Expenses

House Expenses

Finance

Employment

Administration

Club History Book

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SPORT, EVENTS FUNDING, AND FINANCE

3

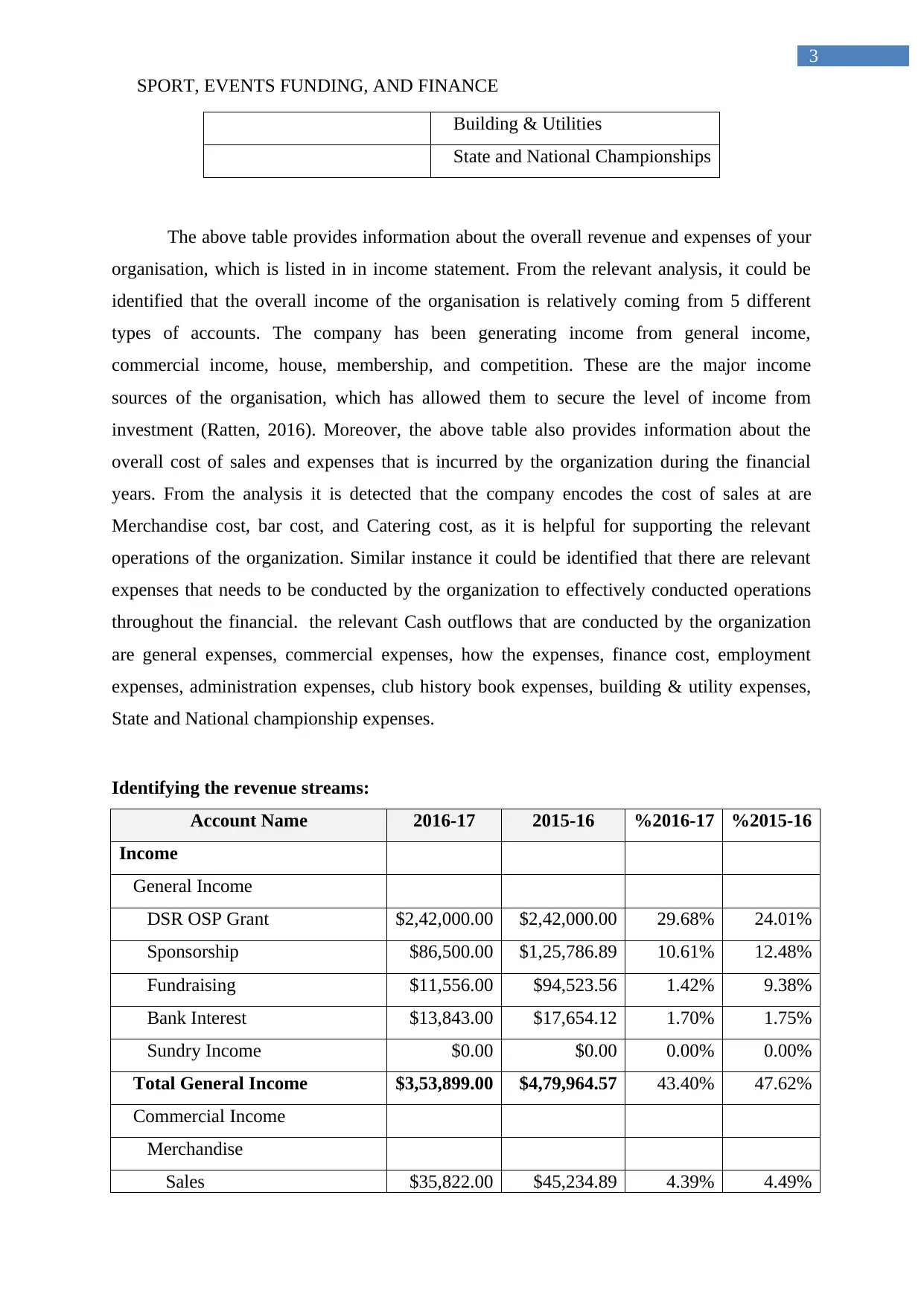

Building & Utilities

State and National Championships

The above table provides information about the overall revenue and expenses of your

organisation, which is listed in in income statement. From the relevant analysis, it could be

identified that the overall income of the organisation is relatively coming from 5 different

types of accounts. The company has been generating income from general income,

commercial income, house, membership, and competition. These are the major income

sources of the organisation, which has allowed them to secure the level of income from

investment (Ratten, 2016). Moreover, the above table also provides information about the

overall cost of sales and expenses that is incurred by the organization during the financial

years. From the analysis it is detected that the company encodes the cost of sales at are

Merchandise cost, bar cost, and Catering cost, as it is helpful for supporting the relevant

operations of the organization. Similar instance it could be identified that there are relevant

expenses that needs to be conducted by the organization to effectively conducted operations

throughout the financial. the relevant Cash outflows that are conducted by the organization

are general expenses, commercial expenses, how the expenses, finance cost, employment

expenses, administration expenses, club history book expenses, building & utility expenses,

State and National championship expenses.

Identifying the revenue streams:

Account Name 2016-17 2015-16 %2016-17 %2015-16

Income

General Income

DSR OSP Grant $2,42,000.00 $2,42,000.00 29.68% 24.01%

Sponsorship $86,500.00 $1,25,786.89 10.61% 12.48%

Fundraising $11,556.00 $94,523.56 1.42% 9.38%

Bank Interest $13,843.00 $17,654.12 1.70% 1.75%

Sundry Income $0.00 $0.00 0.00% 0.00%

Total General Income $3,53,899.00 $4,79,964.57 43.40% 47.62%

Commercial Income

Merchandise

Sales $35,822.00 $45,234.89 4.39% 4.49%

3

Building & Utilities

State and National Championships

The above table provides information about the overall revenue and expenses of your

organisation, which is listed in in income statement. From the relevant analysis, it could be

identified that the overall income of the organisation is relatively coming from 5 different

types of accounts. The company has been generating income from general income,

commercial income, house, membership, and competition. These are the major income

sources of the organisation, which has allowed them to secure the level of income from

investment (Ratten, 2016). Moreover, the above table also provides information about the

overall cost of sales and expenses that is incurred by the organization during the financial

years. From the analysis it is detected that the company encodes the cost of sales at are

Merchandise cost, bar cost, and Catering cost, as it is helpful for supporting the relevant

operations of the organization. Similar instance it could be identified that there are relevant

expenses that needs to be conducted by the organization to effectively conducted operations

throughout the financial. the relevant Cash outflows that are conducted by the organization

are general expenses, commercial expenses, how the expenses, finance cost, employment

expenses, administration expenses, club history book expenses, building & utility expenses,

State and National championship expenses.

Identifying the revenue streams:

Account Name 2016-17 2015-16 %2016-17 %2015-16

Income

General Income

DSR OSP Grant $2,42,000.00 $2,42,000.00 29.68% 24.01%

Sponsorship $86,500.00 $1,25,786.89 10.61% 12.48%

Fundraising $11,556.00 $94,523.56 1.42% 9.38%

Bank Interest $13,843.00 $17,654.12 1.70% 1.75%

Sundry Income $0.00 $0.00 0.00% 0.00%

Total General Income $3,53,899.00 $4,79,964.57 43.40% 47.62%

Commercial Income

Merchandise

Sales $35,822.00 $45,234.89 4.39% 4.49%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SPORT, EVENTS FUNDING, AND FINANCE

4

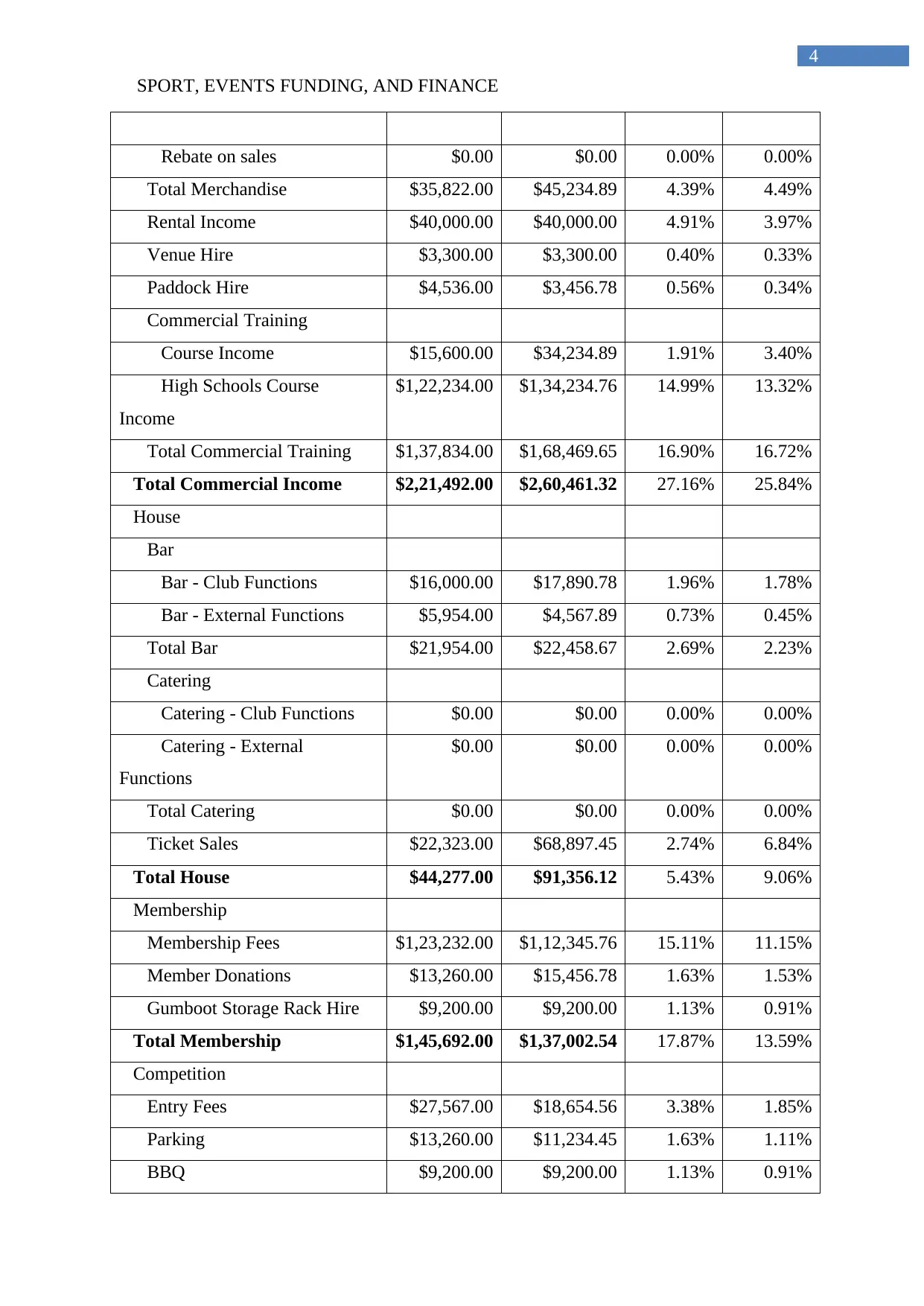

Rebate on sales $0.00 $0.00 0.00% 0.00%

Total Merchandise $35,822.00 $45,234.89 4.39% 4.49%

Rental Income $40,000.00 $40,000.00 4.91% 3.97%

Venue Hire $3,300.00 $3,300.00 0.40% 0.33%

Paddock Hire $4,536.00 $3,456.78 0.56% 0.34%

Commercial Training

Course Income $15,600.00 $34,234.89 1.91% 3.40%

High Schools Course

Income

$1,22,234.00 $1,34,234.76 14.99% 13.32%

Total Commercial Training $1,37,834.00 $1,68,469.65 16.90% 16.72%

Total Commercial Income $2,21,492.00 $2,60,461.32 27.16% 25.84%

House

Bar

Bar - Club Functions $16,000.00 $17,890.78 1.96% 1.78%

Bar - External Functions $5,954.00 $4,567.89 0.73% 0.45%

Total Bar $21,954.00 $22,458.67 2.69% 2.23%

Catering

Catering - Club Functions $0.00 $0.00 0.00% 0.00%

Catering - External

Functions

$0.00 $0.00 0.00% 0.00%

Total Catering $0.00 $0.00 0.00% 0.00%

Ticket Sales $22,323.00 $68,897.45 2.74% 6.84%

Total House $44,277.00 $91,356.12 5.43% 9.06%

Membership

Membership Fees $1,23,232.00 $1,12,345.76 15.11% 11.15%

Member Donations $13,260.00 $15,456.78 1.63% 1.53%

Gumboot Storage Rack Hire $9,200.00 $9,200.00 1.13% 0.91%

Total Membership $1,45,692.00 $1,37,002.54 17.87% 13.59%

Competition

Entry Fees $27,567.00 $18,654.56 3.38% 1.85%

Parking $13,260.00 $11,234.45 1.63% 1.11%

BBQ $9,200.00 $9,200.00 1.13% 0.91%

4

Rebate on sales $0.00 $0.00 0.00% 0.00%

Total Merchandise $35,822.00 $45,234.89 4.39% 4.49%

Rental Income $40,000.00 $40,000.00 4.91% 3.97%

Venue Hire $3,300.00 $3,300.00 0.40% 0.33%

Paddock Hire $4,536.00 $3,456.78 0.56% 0.34%

Commercial Training

Course Income $15,600.00 $34,234.89 1.91% 3.40%

High Schools Course

Income

$1,22,234.00 $1,34,234.76 14.99% 13.32%

Total Commercial Training $1,37,834.00 $1,68,469.65 16.90% 16.72%

Total Commercial Income $2,21,492.00 $2,60,461.32 27.16% 25.84%

House

Bar

Bar - Club Functions $16,000.00 $17,890.78 1.96% 1.78%

Bar - External Functions $5,954.00 $4,567.89 0.73% 0.45%

Total Bar $21,954.00 $22,458.67 2.69% 2.23%

Catering

Catering - Club Functions $0.00 $0.00 0.00% 0.00%

Catering - External

Functions

$0.00 $0.00 0.00% 0.00%

Total Catering $0.00 $0.00 0.00% 0.00%

Ticket Sales $22,323.00 $68,897.45 2.74% 6.84%

Total House $44,277.00 $91,356.12 5.43% 9.06%

Membership

Membership Fees $1,23,232.00 $1,12,345.76 15.11% 11.15%

Member Donations $13,260.00 $15,456.78 1.63% 1.53%

Gumboot Storage Rack Hire $9,200.00 $9,200.00 1.13% 0.91%

Total Membership $1,45,692.00 $1,37,002.54 17.87% 13.59%

Competition

Entry Fees $27,567.00 $18,654.56 3.38% 1.85%

Parking $13,260.00 $11,234.45 1.63% 1.11%

BBQ $9,200.00 $9,200.00 1.13% 0.91%

SPORT, EVENTS FUNDING, AND FINANCE

5

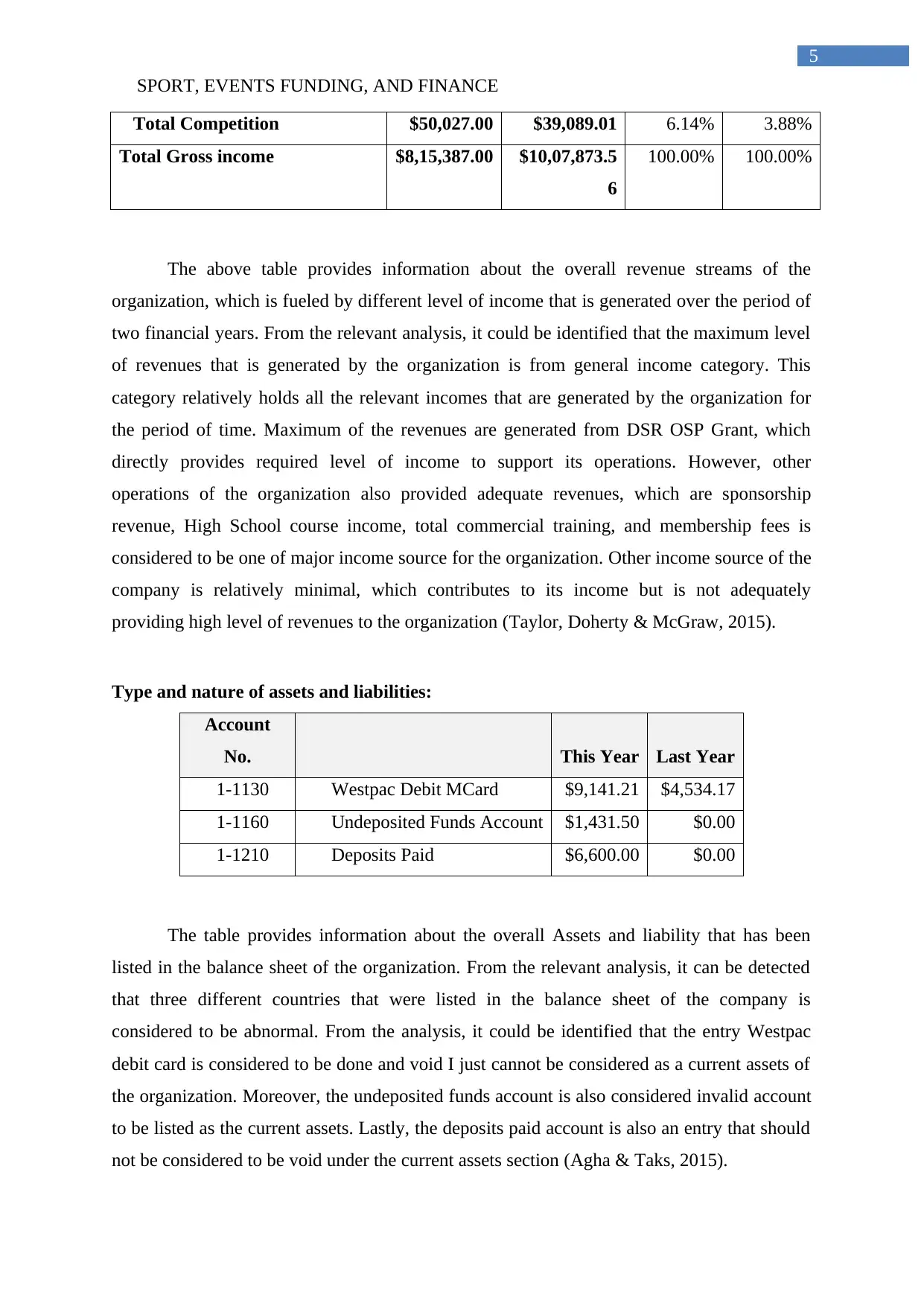

Total Competition $50,027.00 $39,089.01 6.14% 3.88%

Total Gross income $8,15,387.00 $10,07,873.5

6

100.00% 100.00%

The above table provides information about the overall revenue streams of the

organization, which is fueled by different level of income that is generated over the period of

two financial years. From the relevant analysis, it could be identified that the maximum level

of revenues that is generated by the organization is from general income category. This

category relatively holds all the relevant incomes that are generated by the organization for

the period of time. Maximum of the revenues are generated from DSR OSP Grant, which

directly provides required level of income to support its operations. However, other

operations of the organization also provided adequate revenues, which are sponsorship

revenue, High School course income, total commercial training, and membership fees is

considered to be one of major income source for the organization. Other income source of the

company is relatively minimal, which contributes to its income but is not adequately

providing high level of revenues to the organization (Taylor, Doherty & McGraw, 2015).

Type and nature of assets and liabilities:

Account

No. This Year Last Year

1-1130 Westpac Debit MCard $9,141.21 $4,534.17

1-1160 Undeposited Funds Account $1,431.50 $0.00

1-1210 Deposits Paid $6,600.00 $0.00

The table provides information about the overall Assets and liability that has been

listed in the balance sheet of the organization. From the relevant analysis, it can be detected

that three different countries that were listed in the balance sheet of the company is

considered to be abnormal. From the analysis, it could be identified that the entry Westpac

debit card is considered to be done and void I just cannot be considered as a current assets of

the organization. Moreover, the undeposited funds account is also considered invalid account

to be listed as the current assets. Lastly, the deposits paid account is also an entry that should

not be considered to be void under the current assets section (Agha & Taks, 2015).

5

Total Competition $50,027.00 $39,089.01 6.14% 3.88%

Total Gross income $8,15,387.00 $10,07,873.5

6

100.00% 100.00%

The above table provides information about the overall revenue streams of the

organization, which is fueled by different level of income that is generated over the period of

two financial years. From the relevant analysis, it could be identified that the maximum level

of revenues that is generated by the organization is from general income category. This

category relatively holds all the relevant incomes that are generated by the organization for

the period of time. Maximum of the revenues are generated from DSR OSP Grant, which

directly provides required level of income to support its operations. However, other

operations of the organization also provided adequate revenues, which are sponsorship

revenue, High School course income, total commercial training, and membership fees is

considered to be one of major income source for the organization. Other income source of the

company is relatively minimal, which contributes to its income but is not adequately

providing high level of revenues to the organization (Taylor, Doherty & McGraw, 2015).

Type and nature of assets and liabilities:

Account

No. This Year Last Year

1-1130 Westpac Debit MCard $9,141.21 $4,534.17

1-1160 Undeposited Funds Account $1,431.50 $0.00

1-1210 Deposits Paid $6,600.00 $0.00

The table provides information about the overall Assets and liability that has been

listed in the balance sheet of the organization. From the relevant analysis, it can be detected

that three different countries that were listed in the balance sheet of the company is

considered to be abnormal. From the analysis, it could be identified that the entry Westpac

debit card is considered to be done and void I just cannot be considered as a current assets of

the organization. Moreover, the undeposited funds account is also considered invalid account

to be listed as the current assets. Lastly, the deposits paid account is also an entry that should

not be considered to be void under the current assets section (Agha & Taks, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SPORT, EVENTS FUNDING, AND FINANCE

6

Liquidity ratio of the organisation:

Particulars This Year Last Year

Total Current Assets $7,62,913.50 $8,69,366.34

Total Current Liabilities $3,18,013.89 $96,872.06

Liquidity $4,44,899.61 $7,72,494.28

Table provides information about the current liquid ratio of the organization, which is

directed to decline during the period of 2 years. The above table also indicates that the total

current assets value of your organization declared slightly while the current liability

conditions increased exponentially. The increment in current liabilities in comparison to the

current assets directly reduced the liquidity ratio of the organization. This relatively reduces

the values of liquidity ratio from the levels of $772,494.28 in last year to $444,899.61 in this

year.

Analysing the cash reserves of the company:

Particulars This Year Last Year

Cash and cash equivalent $5,40,341.88 $5,02,268.15

Total Current Liabilities $3,18,013.89 $96,872.06

Cash reserve ratio 1.699114086 5.184860836

Table provides information about the cash reserve ratio of the company, which has

declined from sea level 5.184 in last year to the levels of 1.6991 this year. The decline is cash

reserve ratio is due to the increment, current liabilities of the organization file the cash, and

cash equivalents remained stagnant. The above table also indicated that the current cash

reserve ratio of the company is not properly and is reducing due to the high levels of current

liabilities that are accumulated by the organization to conduct its operations (Groothuis &

Rotthoff, 2016).

Analysing the surplus for the financial year:

Particulars 2016-17 2015-16

Net

Profit/(Loss)

($1,93,431.23) ($12,023.29)

6

Liquidity ratio of the organisation:

Particulars This Year Last Year

Total Current Assets $7,62,913.50 $8,69,366.34

Total Current Liabilities $3,18,013.89 $96,872.06

Liquidity $4,44,899.61 $7,72,494.28

Table provides information about the current liquid ratio of the organization, which is

directed to decline during the period of 2 years. The above table also indicates that the total

current assets value of your organization declared slightly while the current liability

conditions increased exponentially. The increment in current liabilities in comparison to the

current assets directly reduced the liquidity ratio of the organization. This relatively reduces

the values of liquidity ratio from the levels of $772,494.28 in last year to $444,899.61 in this

year.

Analysing the cash reserves of the company:

Particulars This Year Last Year

Cash and cash equivalent $5,40,341.88 $5,02,268.15

Total Current Liabilities $3,18,013.89 $96,872.06

Cash reserve ratio 1.699114086 5.184860836

Table provides information about the cash reserve ratio of the company, which has

declined from sea level 5.184 in last year to the levels of 1.6991 this year. The decline is cash

reserve ratio is due to the increment, current liabilities of the organization file the cash, and

cash equivalents remained stagnant. The above table also indicated that the current cash

reserve ratio of the company is not properly and is reducing due to the high levels of current

liabilities that are accumulated by the organization to conduct its operations (Groothuis &

Rotthoff, 2016).

Analysing the surplus for the financial year:

Particulars 2016-17 2015-16

Net

Profit/(Loss)

($1,93,431.23) ($12,023.29)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SPORT, EVENTS FUNDING, AND FINANCE

7

The information provided in the above table directly Indicates about The losses that

has been increased by your organization during the two financial years. The decline in profit

levels has relatively indicated on negative surplus for the financial year of the organization.

The reduced profit levels of the company are directly indicating that the company generates

no surplus during financial year due to high losses incurred from operations.

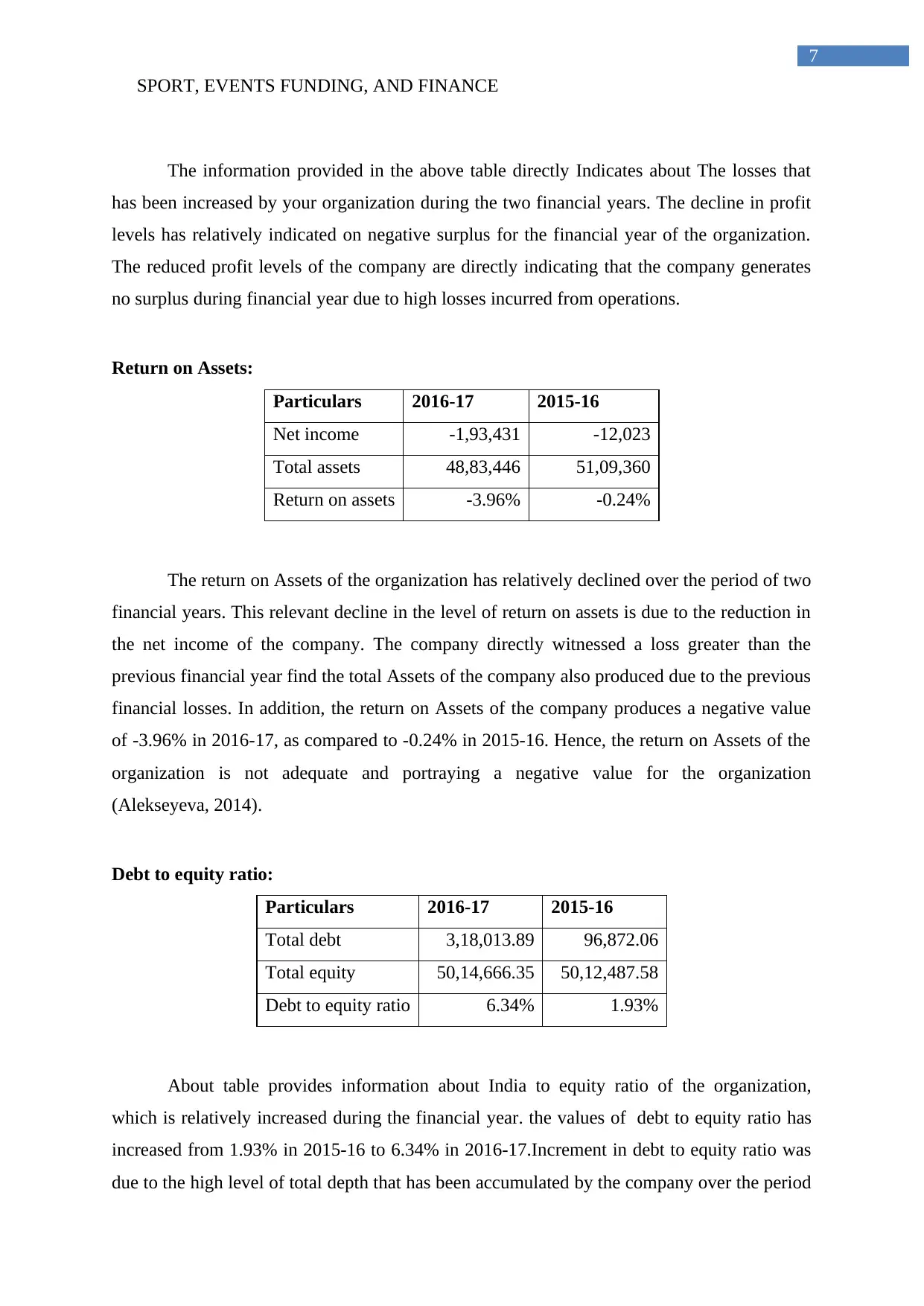

Return on Assets:

Particulars 2016-17 2015-16

Net income -1,93,431 -12,023

Total assets 48,83,446 51,09,360

Return on assets -3.96% -0.24%

The return on Assets of the organization has relatively declined over the period of two

financial years. This relevant decline in the level of return on assets is due to the reduction in

the net income of the company. The company directly witnessed a loss greater than the

previous financial year find the total Assets of the company also produced due to the previous

financial losses. In addition, the return on Assets of the company produces a negative value

of -3.96% in 2016-17, as compared to -0.24% in 2015-16. Hence, the return on Assets of the

organization is not adequate and portraying a negative value for the organization

(Alekseyeva, 2014).

Debt to equity ratio:

Particulars 2016-17 2015-16

Total debt 3,18,013.89 96,872.06

Total equity 50,14,666.35 50,12,487.58

Debt to equity ratio 6.34% 1.93%

About table provides information about India to equity ratio of the organization,

which is relatively increased during the financial year. the values of debt to equity ratio has

increased from 1.93% in 2015-16 to 6.34% in 2016-17.Increment in debt to equity ratio was

due to the high level of total depth that has been accumulated by the company over the period

7

The information provided in the above table directly Indicates about The losses that

has been increased by your organization during the two financial years. The decline in profit

levels has relatively indicated on negative surplus for the financial year of the organization.

The reduced profit levels of the company are directly indicating that the company generates

no surplus during financial year due to high losses incurred from operations.

Return on Assets:

Particulars 2016-17 2015-16

Net income -1,93,431 -12,023

Total assets 48,83,446 51,09,360

Return on assets -3.96% -0.24%

The return on Assets of the organization has relatively declined over the period of two

financial years. This relevant decline in the level of return on assets is due to the reduction in

the net income of the company. The company directly witnessed a loss greater than the

previous financial year find the total Assets of the company also produced due to the previous

financial losses. In addition, the return on Assets of the company produces a negative value

of -3.96% in 2016-17, as compared to -0.24% in 2015-16. Hence, the return on Assets of the

organization is not adequate and portraying a negative value for the organization

(Alekseyeva, 2014).

Debt to equity ratio:

Particulars 2016-17 2015-16

Total debt 3,18,013.89 96,872.06

Total equity 50,14,666.35 50,12,487.58

Debt to equity ratio 6.34% 1.93%

About table provides information about India to equity ratio of the organization,

which is relatively increased during the financial year. the values of debt to equity ratio has

increased from 1.93% in 2015-16 to 6.34% in 2016-17.Increment in debt to equity ratio was

due to the high level of total depth that has been accumulated by the company over the period

SPORT, EVENTS FUNDING, AND FINANCE

8

of two financial years. However, the changes in equity have relatively remained similar,

which can depict about the relevant stagnation in the equity capital.

Net Equity:

Particulars 2016-17 2015-16

Total Assets 48,83,446.45 51,09,359.64

Total Liabilities

3,18,013.8

9 96,872.06

Net Equity 45,65,432.56 50,12,487.58

The net equity capital has been derived Buy directly deducting total assets with the

total liabilities of the organization. The calculation has indicated that there is a relevant

decline in the nativity conditions of the organization as the overall liabilities of the company

increases while total assets declined during the financial year (Wu, Li & Lin, 2016). The total

Assets of the company relatively reduced from the levels of 5,109,359.64 in 2015- 16 to

4,883,446.45 in 2016-17. In the similar instance, the overall total liabilities of the company

increased from 96,872.06 in 2015- 16 to 318,013.89 in 2016-17. The changes in value of

Assets and liabilities are selectively altered the overall net equity of the company was

declined from the values of 5,012,487.58 in 2015-16 to 4,565,432.56 in 2016-17.

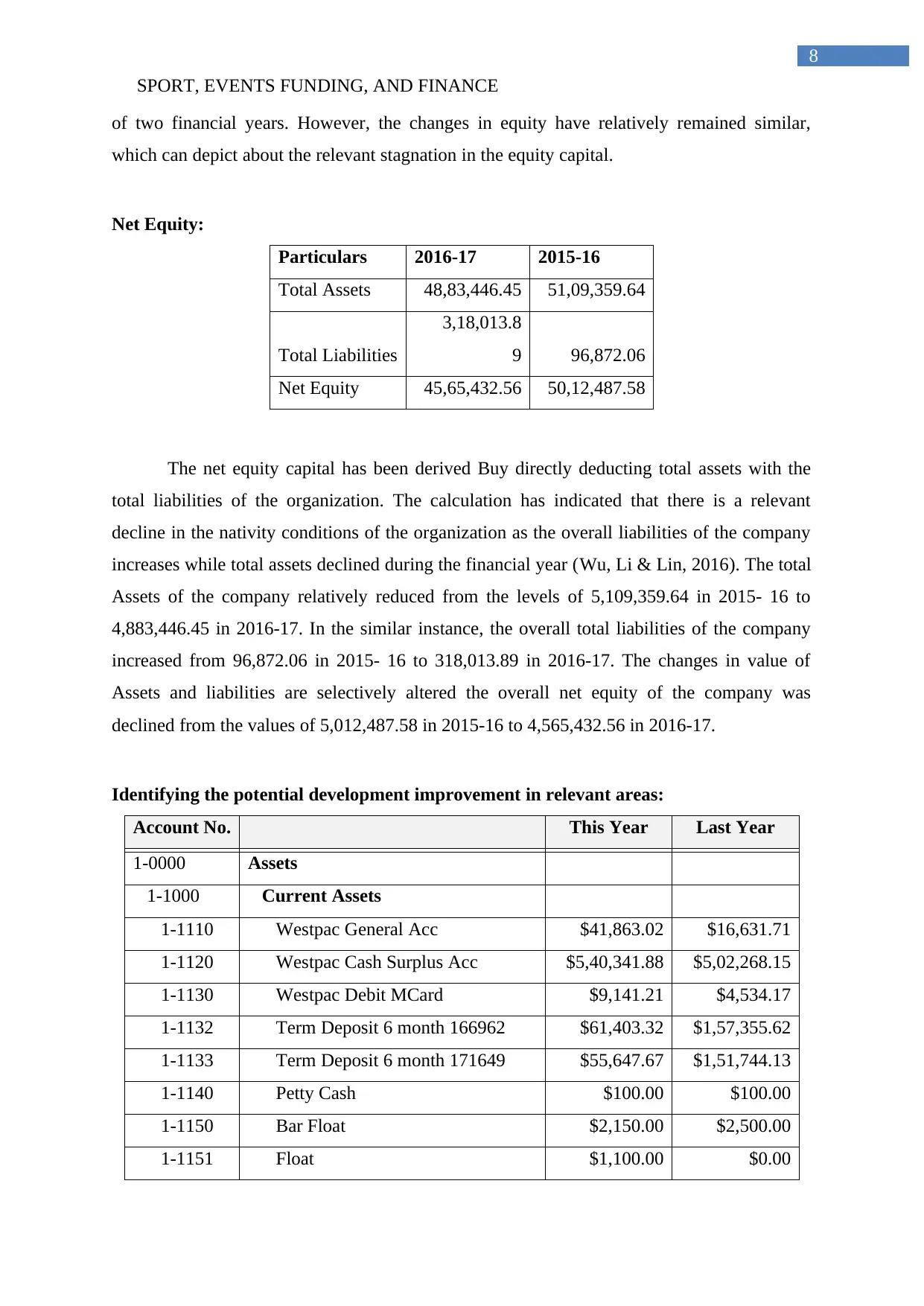

Identifying the potential development improvement in relevant areas:

Account No. This Year Last Year

1-0000 Assets

1-1000 Current Assets

1-1110 Westpac General Acc $41,863.02 $16,631.71

1-1120 Westpac Cash Surplus Acc $5,40,341.88 $5,02,268.15

1-1130 Westpac Debit MCard $9,141.21 $4,534.17

1-1132 Term Deposit 6 month 166962 $61,403.32 $1,57,355.62

1-1133 Term Deposit 6 month 171649 $55,647.67 $1,51,744.13

1-1140 Petty Cash $100.00 $100.00

1-1150 Bar Float $2,150.00 $2,500.00

1-1151 Float $1,100.00 $0.00

8

of two financial years. However, the changes in equity have relatively remained similar,

which can depict about the relevant stagnation in the equity capital.

Net Equity:

Particulars 2016-17 2015-16

Total Assets 48,83,446.45 51,09,359.64

Total Liabilities

3,18,013.8

9 96,872.06

Net Equity 45,65,432.56 50,12,487.58

The net equity capital has been derived Buy directly deducting total assets with the

total liabilities of the organization. The calculation has indicated that there is a relevant

decline in the nativity conditions of the organization as the overall liabilities of the company

increases while total assets declined during the financial year (Wu, Li & Lin, 2016). The total

Assets of the company relatively reduced from the levels of 5,109,359.64 in 2015- 16 to

4,883,446.45 in 2016-17. In the similar instance, the overall total liabilities of the company

increased from 96,872.06 in 2015- 16 to 318,013.89 in 2016-17. The changes in value of

Assets and liabilities are selectively altered the overall net equity of the company was

declined from the values of 5,012,487.58 in 2015-16 to 4,565,432.56 in 2016-17.

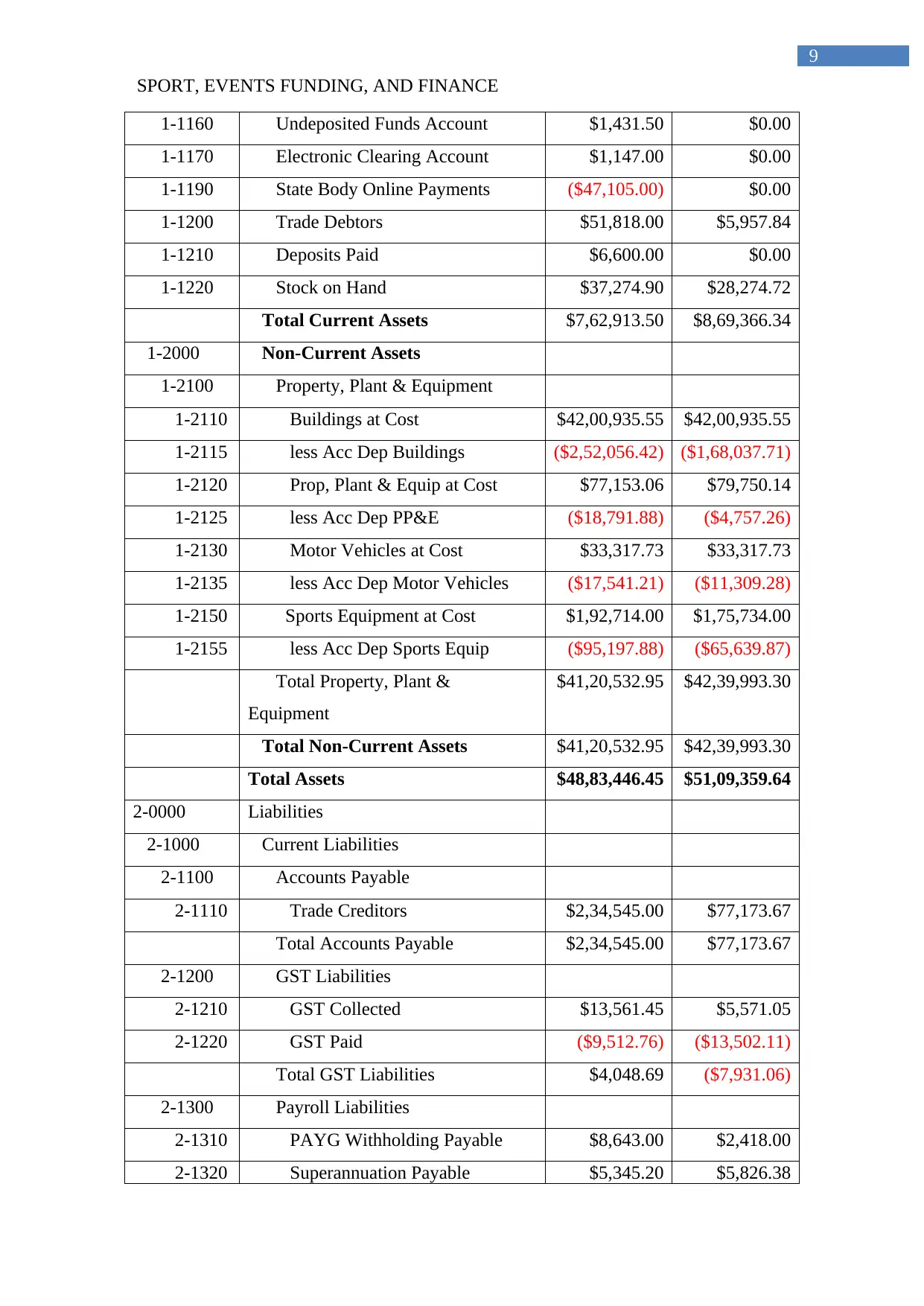

Identifying the potential development improvement in relevant areas:

Account No. This Year Last Year

1-0000 Assets

1-1000 Current Assets

1-1110 Westpac General Acc $41,863.02 $16,631.71

1-1120 Westpac Cash Surplus Acc $5,40,341.88 $5,02,268.15

1-1130 Westpac Debit MCard $9,141.21 $4,534.17

1-1132 Term Deposit 6 month 166962 $61,403.32 $1,57,355.62

1-1133 Term Deposit 6 month 171649 $55,647.67 $1,51,744.13

1-1140 Petty Cash $100.00 $100.00

1-1150 Bar Float $2,150.00 $2,500.00

1-1151 Float $1,100.00 $0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SPORT, EVENTS FUNDING, AND FINANCE

9

1-1160 Undeposited Funds Account $1,431.50 $0.00

1-1170 Electronic Clearing Account $1,147.00 $0.00

1-1190 State Body Online Payments ($47,105.00) $0.00

1-1200 Trade Debtors $51,818.00 $5,957.84

1-1210 Deposits Paid $6,600.00 $0.00

1-1220 Stock on Hand $37,274.90 $28,274.72

Total Current Assets $7,62,913.50 $8,69,366.34

1-2000 Non-Current Assets

1-2100 Property, Plant & Equipment

1-2110 Buildings at Cost $42,00,935.55 $42,00,935.55

1-2115 less Acc Dep Buildings ($2,52,056.42) ($1,68,037.71)

1-2120 Prop, Plant & Equip at Cost $77,153.06 $79,750.14

1-2125 less Acc Dep PP&E ($18,791.88) ($4,757.26)

1-2130 Motor Vehicles at Cost $33,317.73 $33,317.73

1-2135 less Acc Dep Motor Vehicles ($17,541.21) ($11,309.28)

1-2150 Sports Equipment at Cost $1,92,714.00 $1,75,734.00

1-2155 less Acc Dep Sports Equip ($95,197.88) ($65,639.87)

Total Property, Plant &

Equipment

$41,20,532.95 $42,39,993.30

Total Non-Current Assets $41,20,532.95 $42,39,993.30

Total Assets $48,83,446.45 $51,09,359.64

2-0000 Liabilities

2-1000 Current Liabilities

2-1100 Accounts Payable

2-1110 Trade Creditors $2,34,545.00 $77,173.67

Total Accounts Payable $2,34,545.00 $77,173.67

2-1200 GST Liabilities

2-1210 GST Collected $13,561.45 $5,571.05

2-1220 GST Paid ($9,512.76) ($13,502.11)

Total GST Liabilities $4,048.69 ($7,931.06)

2-1300 Payroll Liabilities

2-1310 PAYG Withholding Payable $8,643.00 $2,418.00

2-1320 Superannuation Payable $5,345.20 $5,826.38

9

1-1160 Undeposited Funds Account $1,431.50 $0.00

1-1170 Electronic Clearing Account $1,147.00 $0.00

1-1190 State Body Online Payments ($47,105.00) $0.00

1-1200 Trade Debtors $51,818.00 $5,957.84

1-1210 Deposits Paid $6,600.00 $0.00

1-1220 Stock on Hand $37,274.90 $28,274.72

Total Current Assets $7,62,913.50 $8,69,366.34

1-2000 Non-Current Assets

1-2100 Property, Plant & Equipment

1-2110 Buildings at Cost $42,00,935.55 $42,00,935.55

1-2115 less Acc Dep Buildings ($2,52,056.42) ($1,68,037.71)

1-2120 Prop, Plant & Equip at Cost $77,153.06 $79,750.14

1-2125 less Acc Dep PP&E ($18,791.88) ($4,757.26)

1-2130 Motor Vehicles at Cost $33,317.73 $33,317.73

1-2135 less Acc Dep Motor Vehicles ($17,541.21) ($11,309.28)

1-2150 Sports Equipment at Cost $1,92,714.00 $1,75,734.00

1-2155 less Acc Dep Sports Equip ($95,197.88) ($65,639.87)

Total Property, Plant &

Equipment

$41,20,532.95 $42,39,993.30

Total Non-Current Assets $41,20,532.95 $42,39,993.30

Total Assets $48,83,446.45 $51,09,359.64

2-0000 Liabilities

2-1000 Current Liabilities

2-1100 Accounts Payable

2-1110 Trade Creditors $2,34,545.00 $77,173.67

Total Accounts Payable $2,34,545.00 $77,173.67

2-1200 GST Liabilities

2-1210 GST Collected $13,561.45 $5,571.05

2-1220 GST Paid ($9,512.76) ($13,502.11)

Total GST Liabilities $4,048.69 ($7,931.06)

2-1300 Payroll Liabilities

2-1310 PAYG Withholding Payable $8,643.00 $2,418.00

2-1320 Superannuation Payable $5,345.20 $5,826.38

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SPORT, EVENTS FUNDING, AND FINANCE

10

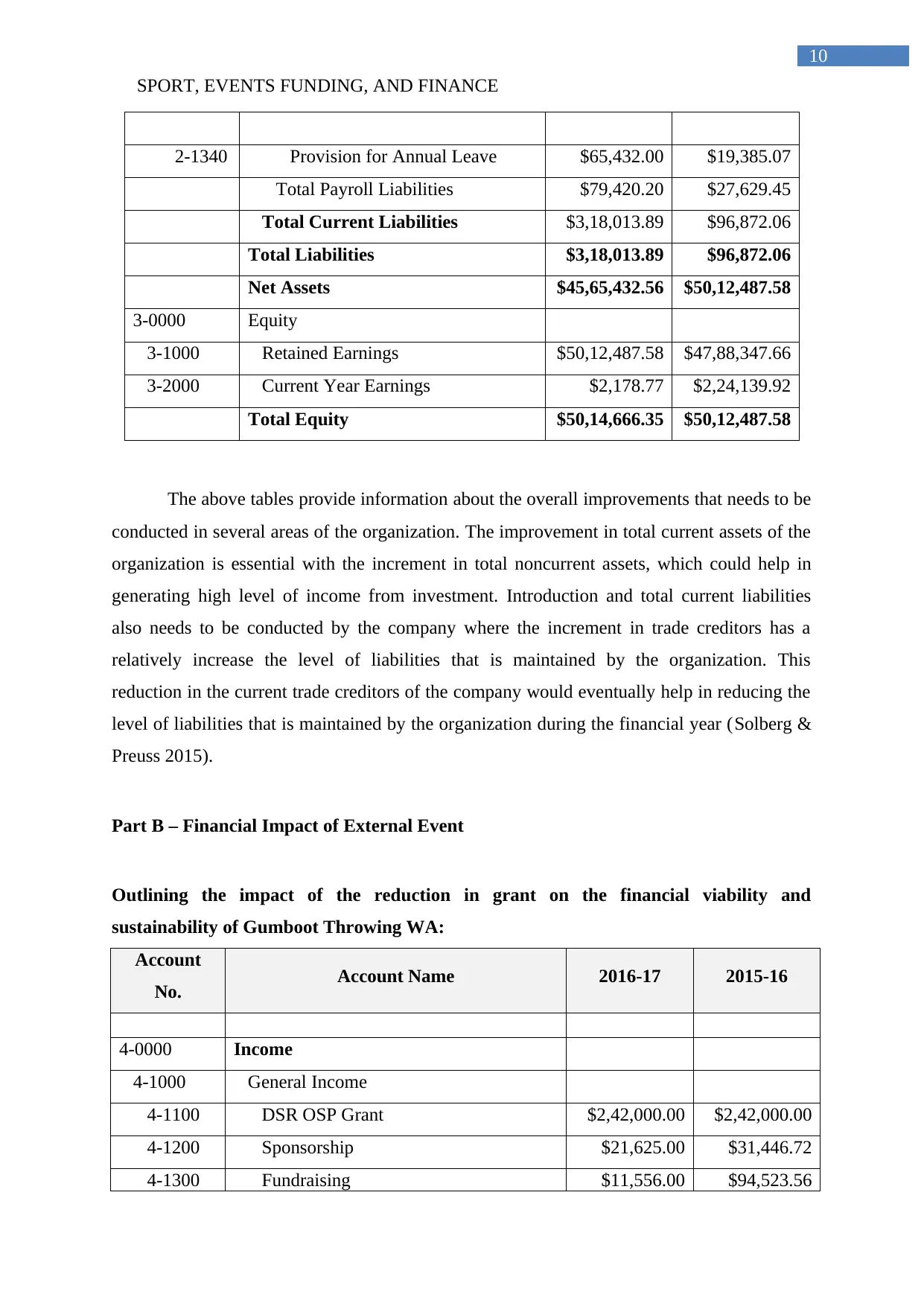

2-1340 Provision for Annual Leave $65,432.00 $19,385.07

Total Payroll Liabilities $79,420.20 $27,629.45

Total Current Liabilities $3,18,013.89 $96,872.06

Total Liabilities $3,18,013.89 $96,872.06

Net Assets $45,65,432.56 $50,12,487.58

3-0000 Equity

3-1000 Retained Earnings $50,12,487.58 $47,88,347.66

3-2000 Current Year Earnings $2,178.77 $2,24,139.92

Total Equity $50,14,666.35 $50,12,487.58

The above tables provide information about the overall improvements that needs to be

conducted in several areas of the organization. The improvement in total current assets of the

organization is essential with the increment in total noncurrent assets, which could help in

generating high level of income from investment. Introduction and total current liabilities

also needs to be conducted by the company where the increment in trade creditors has a

relatively increase the level of liabilities that is maintained by the organization. This

reduction in the current trade creditors of the company would eventually help in reducing the

level of liabilities that is maintained by the organization during the financial year (Solberg &

Preuss 2015).

Part B – Financial Impact of External Event

Outlining the impact of the reduction in grant on the financial viability and

sustainability of Gumboot Throwing WA:

Account

No. Account Name 2016-17 2015-16

4-0000 Income

4-1000 General Income

4-1100 DSR OSP Grant $2,42,000.00 $2,42,000.00

4-1200 Sponsorship $21,625.00 $31,446.72

4-1300 Fundraising $11,556.00 $94,523.56

10

2-1340 Provision for Annual Leave $65,432.00 $19,385.07

Total Payroll Liabilities $79,420.20 $27,629.45

Total Current Liabilities $3,18,013.89 $96,872.06

Total Liabilities $3,18,013.89 $96,872.06

Net Assets $45,65,432.56 $50,12,487.58

3-0000 Equity

3-1000 Retained Earnings $50,12,487.58 $47,88,347.66

3-2000 Current Year Earnings $2,178.77 $2,24,139.92

Total Equity $50,14,666.35 $50,12,487.58

The above tables provide information about the overall improvements that needs to be

conducted in several areas of the organization. The improvement in total current assets of the

organization is essential with the increment in total noncurrent assets, which could help in

generating high level of income from investment. Introduction and total current liabilities

also needs to be conducted by the company where the increment in trade creditors has a

relatively increase the level of liabilities that is maintained by the organization. This

reduction in the current trade creditors of the company would eventually help in reducing the

level of liabilities that is maintained by the organization during the financial year (Solberg &

Preuss 2015).

Part B – Financial Impact of External Event

Outlining the impact of the reduction in grant on the financial viability and

sustainability of Gumboot Throwing WA:

Account

No. Account Name 2016-17 2015-16

4-0000 Income

4-1000 General Income

4-1100 DSR OSP Grant $2,42,000.00 $2,42,000.00

4-1200 Sponsorship $21,625.00 $31,446.72

4-1300 Fundraising $11,556.00 $94,523.56

SPORT, EVENTS FUNDING, AND FINANCE

11

4-1400 Bank Interest $13,843.00 $17,654.12

4-1500 Sundry Income $0.00 $0.00

Total General Income $2,89,024.00 $3,85,624.40

4-2000 Commercial Income

4-2100 Merchandise

4-2110 Sales $35,822.00 $45,234.89

4-2130 Rebate on sales $0.00 $0.00

Total Merchandise $35,822.00 $45,234.89

4-2200 Rental Income $40,000.00 $40,000.00

4-2300 Venue Hire $3,300.00 $3,300.00

4-2400 Paddock Hire $4,536.00 $3,456.78

4-2500 Commercial Training

4-2510 Course Income $15,600.00 $34,234.89

4-2520 High Schools Course Income $1,22,234.00 $1,34,234.76

Total Commercial Training $1,37,834.00 $1,68,469.65

Total Commercial Income $2,21,492.00 $2,60,461.32

4-3000 House

4-3100 Bar

4-3110 Bar - Club Functions $16,000.00 $17,890.78

4-3120 Bar - External Functions $5,954.00 $4,567.89

Total Bar $21,954.00 $22,458.67

4-3200 Catering

4-3210 Catering - Club Functions $0.00 $0.00

4-3220 Catering - External Functions $0.00 $0.00

Total Catering $0.00 $0.00

4-3300 Ticket Sales $22,323.00 $68,897.45

Total House $44,277.00 $91,356.12

4-4000 Membership

4-4100 Membership Fees $1,23,232.00 $1,12,345.76

4-4110 Member Donations $13,260.00 $15,456.78

4-4200 Gumboot Storage Rack Hire $9,200.00 $9,200.00

11

4-1400 Bank Interest $13,843.00 $17,654.12

4-1500 Sundry Income $0.00 $0.00

Total General Income $2,89,024.00 $3,85,624.40

4-2000 Commercial Income

4-2100 Merchandise

4-2110 Sales $35,822.00 $45,234.89

4-2130 Rebate on sales $0.00 $0.00

Total Merchandise $35,822.00 $45,234.89

4-2200 Rental Income $40,000.00 $40,000.00

4-2300 Venue Hire $3,300.00 $3,300.00

4-2400 Paddock Hire $4,536.00 $3,456.78

4-2500 Commercial Training

4-2510 Course Income $15,600.00 $34,234.89

4-2520 High Schools Course Income $1,22,234.00 $1,34,234.76

Total Commercial Training $1,37,834.00 $1,68,469.65

Total Commercial Income $2,21,492.00 $2,60,461.32

4-3000 House

4-3100 Bar

4-3110 Bar - Club Functions $16,000.00 $17,890.78

4-3120 Bar - External Functions $5,954.00 $4,567.89

Total Bar $21,954.00 $22,458.67

4-3200 Catering

4-3210 Catering - Club Functions $0.00 $0.00

4-3220 Catering - External Functions $0.00 $0.00

Total Catering $0.00 $0.00

4-3300 Ticket Sales $22,323.00 $68,897.45

Total House $44,277.00 $91,356.12

4-4000 Membership

4-4100 Membership Fees $1,23,232.00 $1,12,345.76

4-4110 Member Donations $13,260.00 $15,456.78

4-4200 Gumboot Storage Rack Hire $9,200.00 $9,200.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.