HA2032 Corporate & Financial Accounting Final Assessment T2 2021

VerifiedAdded on 2023/06/18

|10

|1980

|163

Homework Assignment

AI Summary

This document presents a solved final assessment for the HA2032 Corporate and Financial Accounting course. It includes detailed answers to six questions covering topics such as disclosing entities, capital reduction vs. share buybacks, acquisition journal entries, consolidated retained profits, consolidation data adjustments, and indirect ownership interests. The solutions provide calculations, journal entries, and explanations, referencing relevant academic sources. This resource is intended to aid students in understanding key concepts and improving their performance in the course. Desklib offers a wide array of study tools and resources for students.

)

HA2032

CORPORATE AND FINANCIAL ACCOUNTING

FINAL ASSESSMENT

Assessment Weight: 50 total marks

Instructions:

All questions must be answered by using the answer boxes provided in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Submission instructions are at the end of this paper.

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

HA2032 Final Assessment T2 2021

HA2032

CORPORATE AND FINANCIAL ACCOUNTING

FINAL ASSESSMENT

Assessment Weight: 50 total marks

Instructions:

All questions must be answered by using the answer boxes provided in this paper.

Completed answers must be submitted to Blackboard by the published due date

and time.

Submission instructions are at the end of this paper.

Purpose:

This assessment consists of six (6) questions and is designed to assess your level of

knowledge of the key topics covered in this unit

HA2032 Final Assessment T2 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1 (7 marks)

Explain a disclosing entity and describe the implications of being a disclosing entity?

ANSWER: ** Answer box will enlarge as you type

Disclosing entity is a medical provider except the case of individual practitioner or a group of

practitioner. Fiscal agent are also considered as the disclosing entity. The disclosing entity on the

other hand further include all the business houses as they need to disclose the financial

presentation in front of the stakeholders (Newman and et. al., 2017). There are certain

implications also attached with disclosing entity such as they need to disclose all the financial

records in front of the stakeholder group. Disclosing entity also need to ensure a yearly audit of

its records and other such documents. The financial records of the disclosing entity must be

audited with the authorised person or professional.

Question 2 (7 marks)

Compare and contrast (list the advantages or disadvantages if any) the capital reduction and a

share buyback.

ANSWER:

Advantage:

Buyback of shares creates a positive message in front of the inversions of the business regarding

the performance of venture in respective target market. This practice support the confidence

level of investor's towards the performance of venture (Hettiarachchi, Meegoda and Ryu,

2018). Surplus funds available with the company that is not being used will also get to utilise

against buying back the stocks of company. All such stockholders sold during the repurchase

program get the opportunity to generate current market price along with the premium.

Disadvantage:

HA2032 Final Assessment T2 2021

Explain a disclosing entity and describe the implications of being a disclosing entity?

ANSWER: ** Answer box will enlarge as you type

Disclosing entity is a medical provider except the case of individual practitioner or a group of

practitioner. Fiscal agent are also considered as the disclosing entity. The disclosing entity on the

other hand further include all the business houses as they need to disclose the financial

presentation in front of the stakeholders (Newman and et. al., 2017). There are certain

implications also attached with disclosing entity such as they need to disclose all the financial

records in front of the stakeholder group. Disclosing entity also need to ensure a yearly audit of

its records and other such documents. The financial records of the disclosing entity must be

audited with the authorised person or professional.

Question 2 (7 marks)

Compare and contrast (list the advantages or disadvantages if any) the capital reduction and a

share buyback.

ANSWER:

Advantage:

Buyback of shares creates a positive message in front of the inversions of the business regarding

the performance of venture in respective target market. This practice support the confidence

level of investor's towards the performance of venture (Hettiarachchi, Meegoda and Ryu,

2018). Surplus funds available with the company that is not being used will also get to utilise

against buying back the stocks of company. All such stockholders sold during the repurchase

program get the opportunity to generate current market price along with the premium.

Disadvantage:

HA2032 Final Assessment T2 2021

The cash requirements are more in case of buying back of stock as it involve opportunity cost of

capital. In most of the cases companies try to increase the stock price with the use of this

practice as this allow them selling the same stock over high price range (Shi and et.al., 2020).

The discount brokers also get an unreasonable advantage against the buying back of stock like

practice.

HA2032 Final Assessment T2 2021

capital. In most of the cases companies try to increase the stock price with the use of this

practice as this allow them selling the same stock over high price range (Shi and et.al., 2020).

The discount brokers also get an unreasonable advantage against the buying back of stock like

practice.

HA2032 Final Assessment T2 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

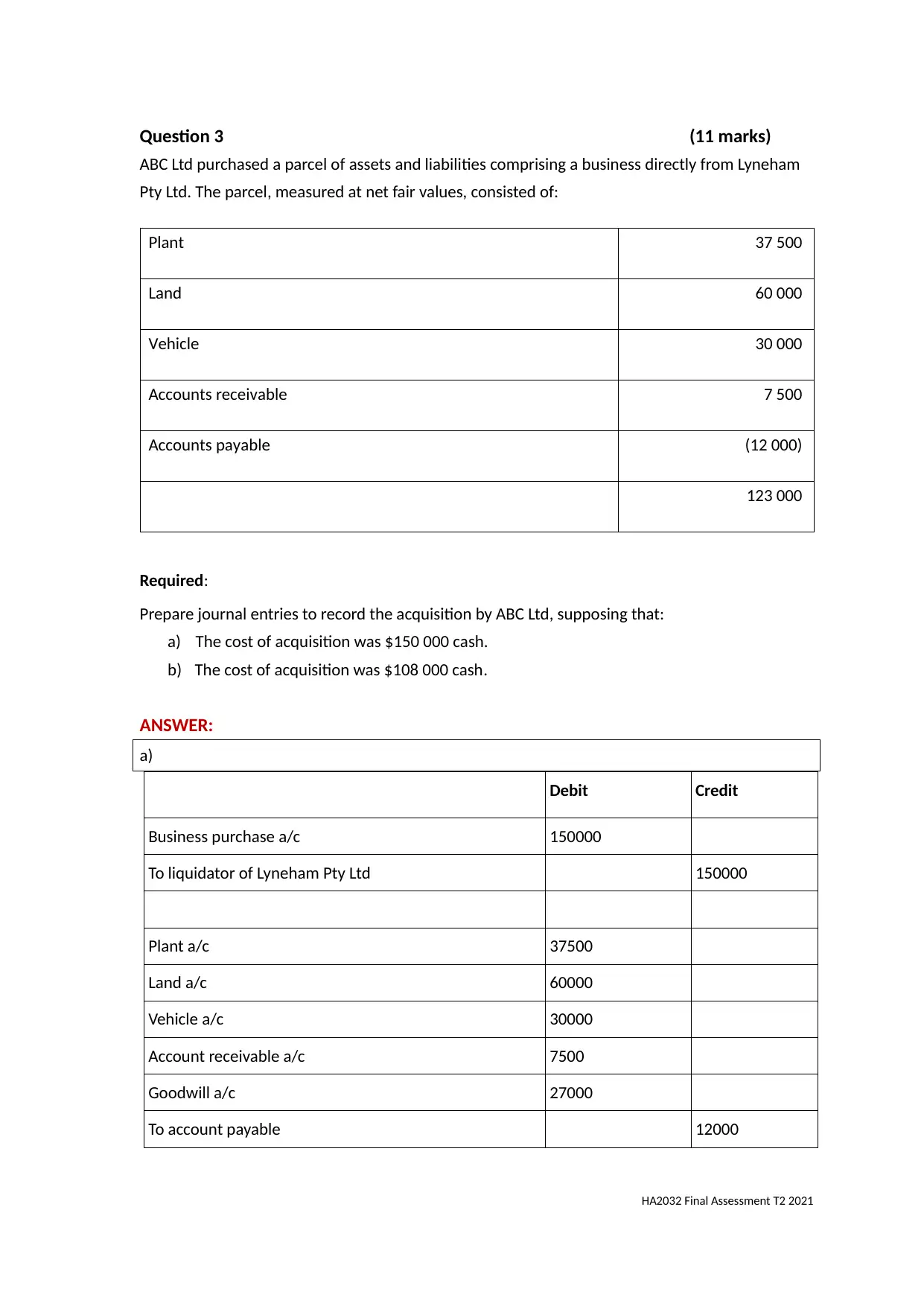

Question 3 (11 marks)

ABC Ltd purchased a parcel of assets and liabilities comprising a business directly from Lyneham

Pty Ltd. The parcel, measured at net fair values, consisted of:

Plant 37 500

Land 60 000

Vehicle 30 000

Accounts receivable 7 500

Accounts payable (12 000)

123 000

Required:

Prepare journal entries to record the acquisition by ABC Ltd, supposing that:

a) The cost of acquisition was $150 000 cash.

b) The cost of acquisition was $108 000 cash.

ANSWER:

a)

Debit Credit

Business purchase a/c 150000

To liquidator of Lyneham Pty Ltd 150000

Plant a/c 37500

Land a/c 60000

Vehicle a/c 30000

Account receivable a/c 7500

Goodwill a/c 27000

To account payable 12000

HA2032 Final Assessment T2 2021

ABC Ltd purchased a parcel of assets and liabilities comprising a business directly from Lyneham

Pty Ltd. The parcel, measured at net fair values, consisted of:

Plant 37 500

Land 60 000

Vehicle 30 000

Accounts receivable 7 500

Accounts payable (12 000)

123 000

Required:

Prepare journal entries to record the acquisition by ABC Ltd, supposing that:

a) The cost of acquisition was $150 000 cash.

b) The cost of acquisition was $108 000 cash.

ANSWER:

a)

Debit Credit

Business purchase a/c 150000

To liquidator of Lyneham Pty Ltd 150000

Plant a/c 37500

Land a/c 60000

Vehicle a/c 30000

Account receivable a/c 7500

Goodwill a/c 27000

To account payable 12000

HA2032 Final Assessment T2 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

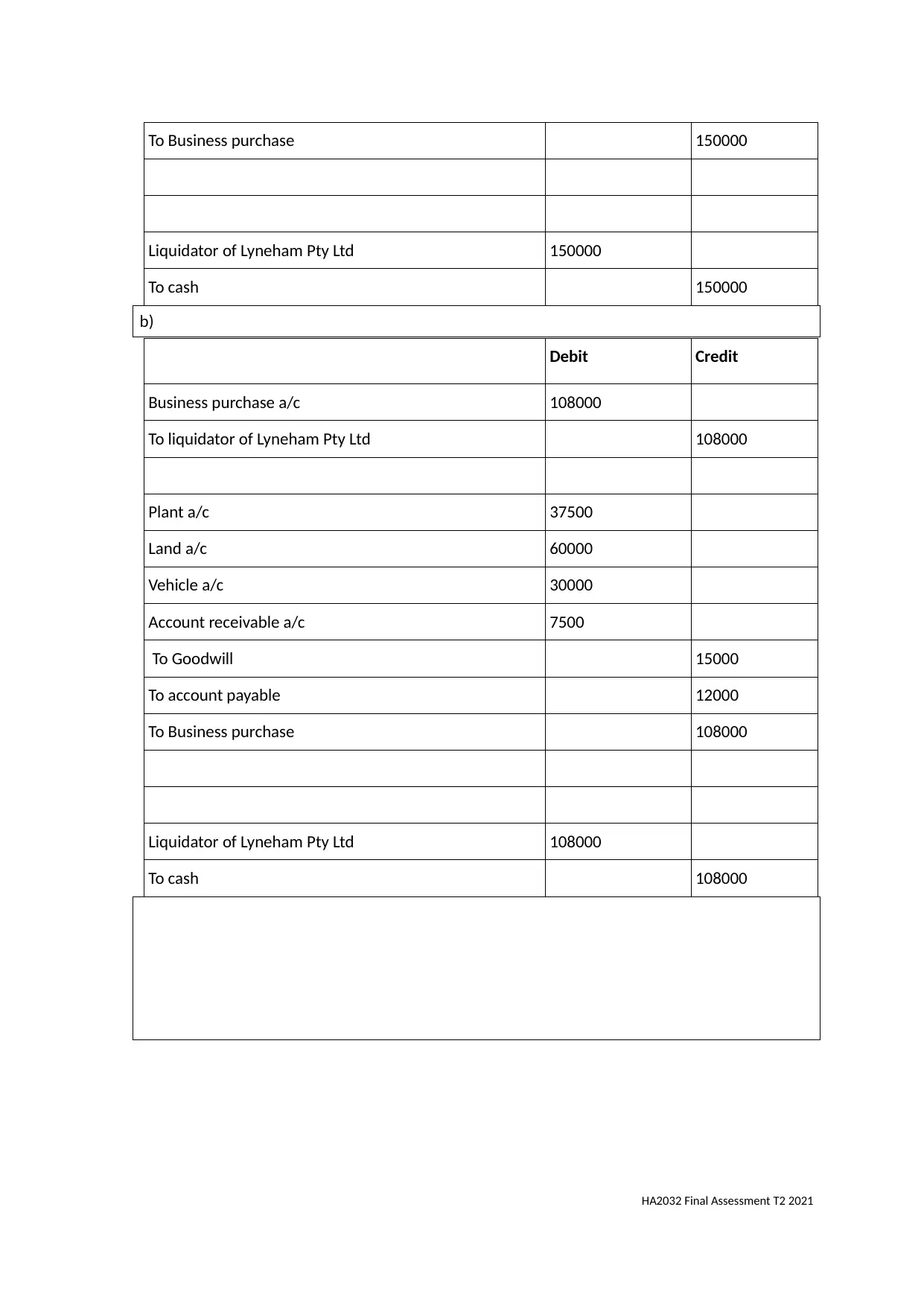

To Business purchase 150000

Liquidator of Lyneham Pty Ltd 150000

To cash 150000

b)

Debit Credit

Business purchase a/c 108000

To liquidator of Lyneham Pty Ltd 108000

Plant a/c 37500

Land a/c 60000

Vehicle a/c 30000

Account receivable a/c 7500

To Goodwill 15000

To account payable 12000

To Business purchase 108000

Liquidator of Lyneham Pty Ltd 108000

To cash 108000

HA2032 Final Assessment T2 2021

Liquidator of Lyneham Pty Ltd 150000

To cash 150000

b)

Debit Credit

Business purchase a/c 108000

To liquidator of Lyneham Pty Ltd 108000

Plant a/c 37500

Land a/c 60000

Vehicle a/c 30000

Account receivable a/c 7500

To Goodwill 15000

To account payable 12000

To Business purchase 108000

Liquidator of Lyneham Pty Ltd 108000

To cash 108000

HA2032 Final Assessment T2 2021

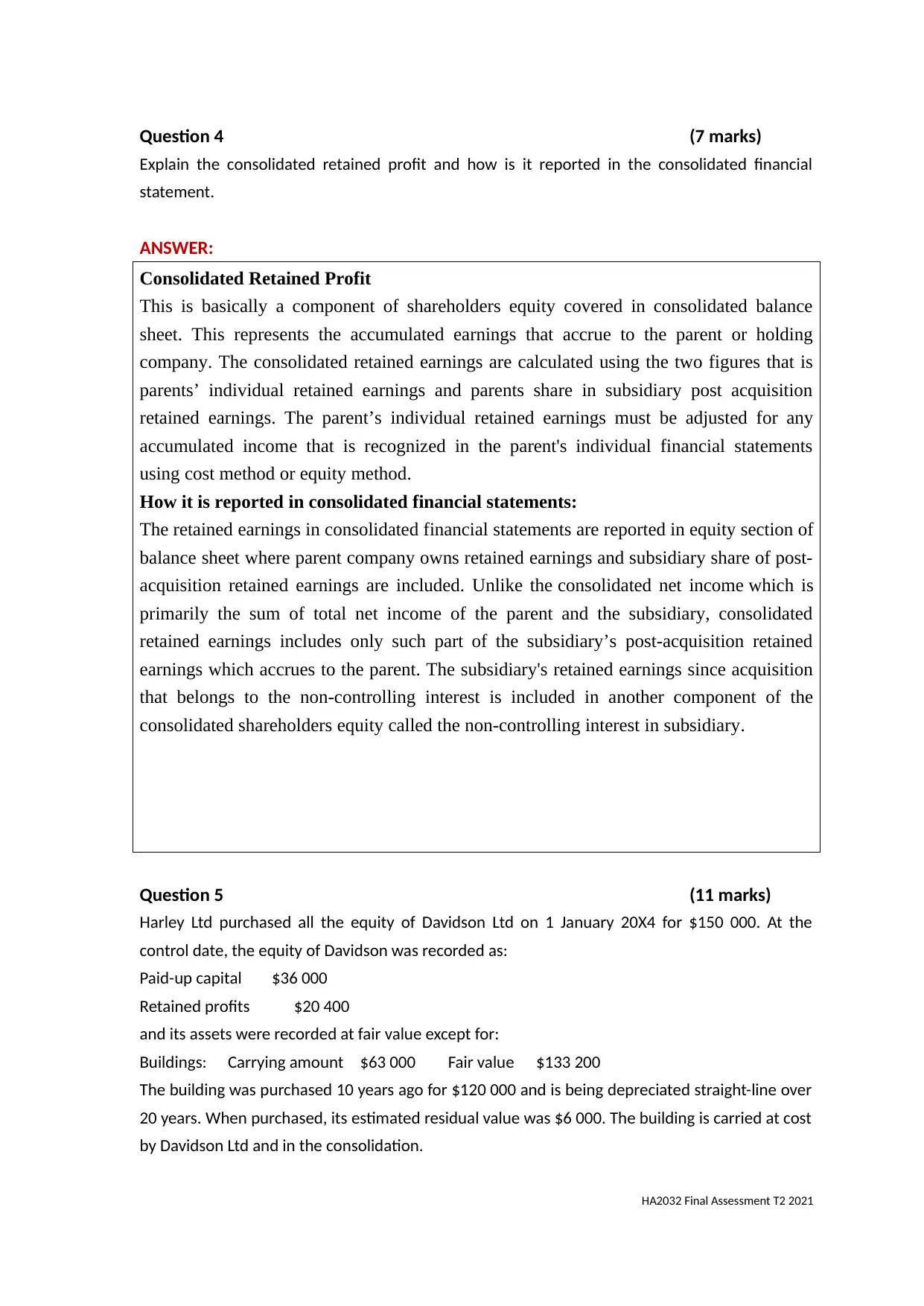

Question 4 (7 marks)

Explain the consolidated retained profit and how is it reported in the consolidated financial

statement.

ANSWER:

Consolidated Retained Profit

This is basically a component of shareholders equity covered in consolidated balance

sheet. This represents the accumulated earnings that accrue to the parent or holding

company. The consolidated retained earnings are calculated using the two figures that is

parents’ individual retained earnings and parents share in subsidiary post acquisition

retained earnings. The parent’s individual retained earnings must be adjusted for any

accumulated income that is recognized in the parent's individual financial statements

using cost method or equity method.

How it is reported in consolidated financial statements:

The retained earnings in consolidated financial statements are reported in equity section of

balance sheet where parent company owns retained earnings and subsidiary share of post-

acquisition retained earnings are included. Unlike the consolidated net income which is

primarily the sum of total net income of the parent and the subsidiary, consolidated

retained earnings includes only such part of the subsidiary’s post-acquisition retained

earnings which accrues to the parent. The subsidiary's retained earnings since acquisition

that belongs to the non-controlling interest is included in another component of the

consolidated shareholders equity called the non-controlling interest in subsidiary.

Question 5 (11 marks)

Harley Ltd purchased all the equity of Davidson Ltd on 1 January 20X4 for $150 000. At the

control date, the equity of Davidson was recorded as:

Paid-up capital $36 000

Retained profits $20 400

and its assets were recorded at fair value except for:

Buildings: Carrying amount $63 000 Fair value $133 200

The building was purchased 10 years ago for $120 000 and is being depreciated straight-line over

20 years. When purchased, its estimated residual value was $6 000. The building is carried at cost

by Davidson Ltd and in the consolidation.

HA2032 Final Assessment T2 2021

Explain the consolidated retained profit and how is it reported in the consolidated financial

statement.

ANSWER:

Consolidated Retained Profit

This is basically a component of shareholders equity covered in consolidated balance

sheet. This represents the accumulated earnings that accrue to the parent or holding

company. The consolidated retained earnings are calculated using the two figures that is

parents’ individual retained earnings and parents share in subsidiary post acquisition

retained earnings. The parent’s individual retained earnings must be adjusted for any

accumulated income that is recognized in the parent's individual financial statements

using cost method or equity method.

How it is reported in consolidated financial statements:

The retained earnings in consolidated financial statements are reported in equity section of

balance sheet where parent company owns retained earnings and subsidiary share of post-

acquisition retained earnings are included. Unlike the consolidated net income which is

primarily the sum of total net income of the parent and the subsidiary, consolidated

retained earnings includes only such part of the subsidiary’s post-acquisition retained

earnings which accrues to the parent. The subsidiary's retained earnings since acquisition

that belongs to the non-controlling interest is included in another component of the

consolidated shareholders equity called the non-controlling interest in subsidiary.

Question 5 (11 marks)

Harley Ltd purchased all the equity of Davidson Ltd on 1 January 20X4 for $150 000. At the

control date, the equity of Davidson was recorded as:

Paid-up capital $36 000

Retained profits $20 400

and its assets were recorded at fair value except for:

Buildings: Carrying amount $63 000 Fair value $133 200

The building was purchased 10 years ago for $120 000 and is being depreciated straight-line over

20 years. When purchased, its estimated residual value was $6 000. The building is carried at cost

by Davidson Ltd and in the consolidation.

HA2032 Final Assessment T2 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Goodwill impairment recognised was $7 000 in 20X4 and $10 500 in 20X5.

Required:

Prepare journal entries for consolidation data adjustments and/or eliminations:

a) at the control date;

b) one year after control date on 31 December 20X4; and

c) two years after control date on 31 December 20X5

ANSWER:

On the basis of above question, the total identifiable net assets are = 56400 i.e., Paid up

capital + Retained Profit = 36000 + 20400.

Calculation of monthly depreciation expenses = 120000 – 6000/ 20 = 5700

Carrying value of Building = 120000 – 5700*10 = 63000

The increase in Building value due to fair value = Fair value – Carrying value

= 133200 – 63000 = 70200.

So, the fair value of net identifiable assets will be as follows:

Total Identifiable net assets + Increase in building value due to fair value = 56400 +

70200 = 126600

Consideration paid = 150000

Calculation of Goodwill = Consideration paid – Fair Value of net identifiable assets

= 150000 – 126600 = 23400

Date Particulars Debit Credit

At control

Date

Pre-acquisition entry:

Paid up capital a/c dr.

Retained Profit a/c dr.

Building a/c dr.

Goodwill a/c dr.

Investment in Davidson Ltd. a/c

(Being journal entry for pre-acquisition is

passed)

36000

20400

70200

23400

150000

31st

December

20X4

Goodwill Impairment loss a/c dr.

To Goodwill a/c

(Being impairment loss of goodwill is

deducted from the amount of Goodwill

from acquisition.)

7000

7000

31st

December

20X4

Post- acquisition entry:

Paid up capital a/c dr.

Retained Profit a/c dr.

Building a/c dr.

36000

20400

70200

HA2032 Final Assessment T2 2021

Required:

Prepare journal entries for consolidation data adjustments and/or eliminations:

a) at the control date;

b) one year after control date on 31 December 20X4; and

c) two years after control date on 31 December 20X5

ANSWER:

On the basis of above question, the total identifiable net assets are = 56400 i.e., Paid up

capital + Retained Profit = 36000 + 20400.

Calculation of monthly depreciation expenses = 120000 – 6000/ 20 = 5700

Carrying value of Building = 120000 – 5700*10 = 63000

The increase in Building value due to fair value = Fair value – Carrying value

= 133200 – 63000 = 70200.

So, the fair value of net identifiable assets will be as follows:

Total Identifiable net assets + Increase in building value due to fair value = 56400 +

70200 = 126600

Consideration paid = 150000

Calculation of Goodwill = Consideration paid – Fair Value of net identifiable assets

= 150000 – 126600 = 23400

Date Particulars Debit Credit

At control

Date

Pre-acquisition entry:

Paid up capital a/c dr.

Retained Profit a/c dr.

Building a/c dr.

Goodwill a/c dr.

Investment in Davidson Ltd. a/c

(Being journal entry for pre-acquisition is

passed)

36000

20400

70200

23400

150000

31st

December

20X4

Goodwill Impairment loss a/c dr.

To Goodwill a/c

(Being impairment loss of goodwill is

deducted from the amount of Goodwill

from acquisition.)

7000

7000

31st

December

20X4

Post- acquisition entry:

Paid up capital a/c dr.

Retained Profit a/c dr.

Building a/c dr.

36000

20400

70200

HA2032 Final Assessment T2 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

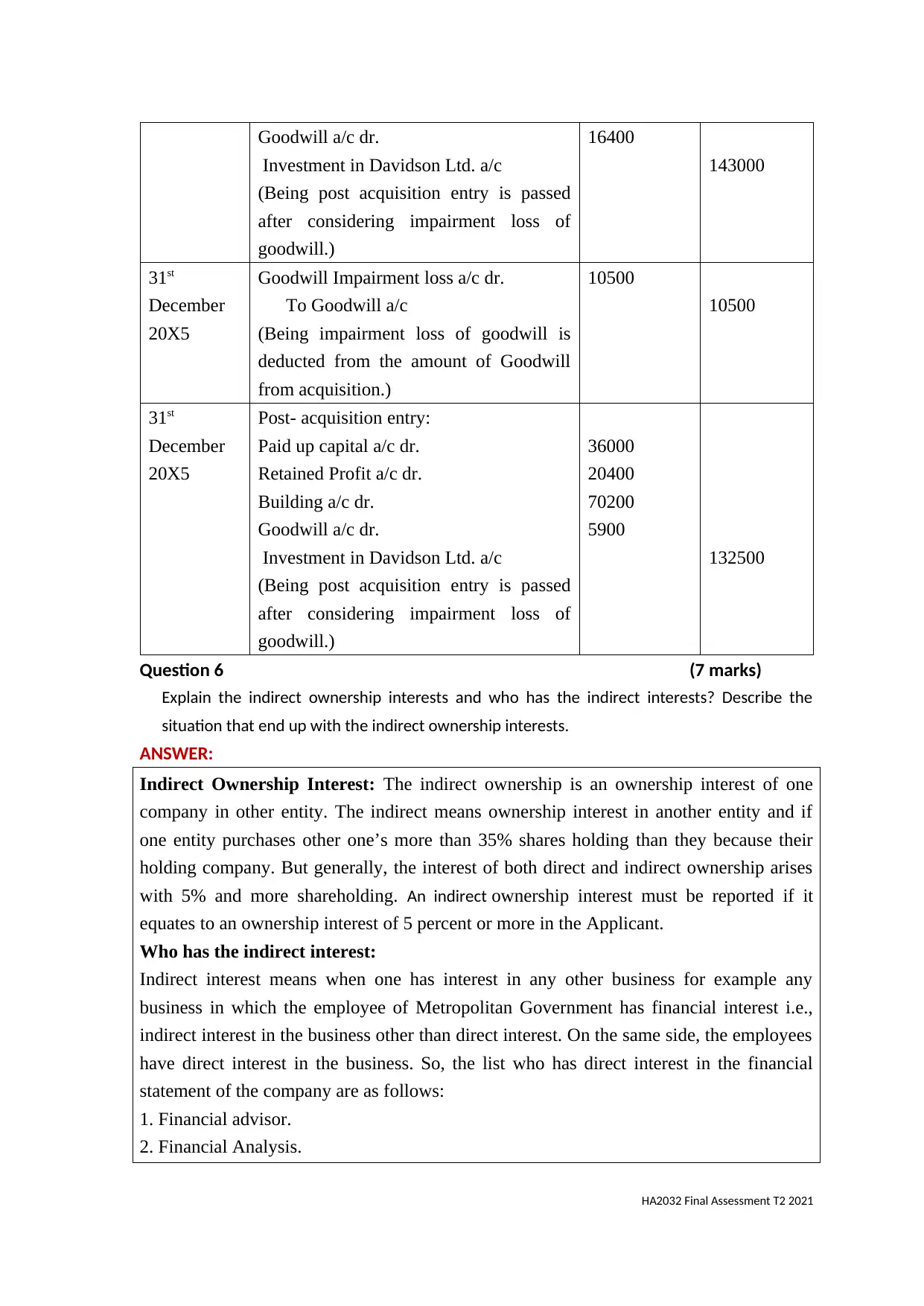

Goodwill a/c dr.

Investment in Davidson Ltd. a/c

(Being post acquisition entry is passed

after considering impairment loss of

goodwill.)

16400

143000

31st

December

20X5

Goodwill Impairment loss a/c dr.

To Goodwill a/c

(Being impairment loss of goodwill is

deducted from the amount of Goodwill

from acquisition.)

10500

10500

31st

December

20X5

Post- acquisition entry:

Paid up capital a/c dr.

Retained Profit a/c dr.

Building a/c dr.

Goodwill a/c dr.

Investment in Davidson Ltd. a/c

(Being post acquisition entry is passed

after considering impairment loss of

goodwill.)

36000

20400

70200

5900

132500

Question 6 (7 marks)

Explain the indirect ownership interests and who has the indirect interests? Describe the

situation that end up with the indirect ownership interests.

ANSWER:

Indirect Ownership Interest: The indirect ownership is an ownership interest of one

company in other entity. The indirect means ownership interest in another entity and if

one entity purchases other one’s more than 35% shares holding than they because their

holding company. But generally, the interest of both direct and indirect ownership arises

with 5% and more shareholding. An indirect ownership interest must be reported if it

equates to an ownership interest of 5 percent or more in the Applicant.

Who has the indirect interest:

Indirect interest means when one has interest in any other business for example any

business in which the employee of Metropolitan Government has financial interest i.e.,

indirect interest in the business other than direct interest. On the same side, the employees

have direct interest in the business. So, the list who has direct interest in the financial

statement of the company are as follows:

1. Financial advisor.

2. Financial Analysis.

HA2032 Final Assessment T2 2021

Investment in Davidson Ltd. a/c

(Being post acquisition entry is passed

after considering impairment loss of

goodwill.)

16400

143000

31st

December

20X5

Goodwill Impairment loss a/c dr.

To Goodwill a/c

(Being impairment loss of goodwill is

deducted from the amount of Goodwill

from acquisition.)

10500

10500

31st

December

20X5

Post- acquisition entry:

Paid up capital a/c dr.

Retained Profit a/c dr.

Building a/c dr.

Goodwill a/c dr.

Investment in Davidson Ltd. a/c

(Being post acquisition entry is passed

after considering impairment loss of

goodwill.)

36000

20400

70200

5900

132500

Question 6 (7 marks)

Explain the indirect ownership interests and who has the indirect interests? Describe the

situation that end up with the indirect ownership interests.

ANSWER:

Indirect Ownership Interest: The indirect ownership is an ownership interest of one

company in other entity. The indirect means ownership interest in another entity and if

one entity purchases other one’s more than 35% shares holding than they because their

holding company. But generally, the interest of both direct and indirect ownership arises

with 5% and more shareholding. An indirect ownership interest must be reported if it

equates to an ownership interest of 5 percent or more in the Applicant.

Who has the indirect interest:

Indirect interest means when one has interest in any other business for example any

business in which the employee of Metropolitan Government has financial interest i.e.,

indirect interest in the business other than direct interest. On the same side, the employees

have direct interest in the business. So, the list who has direct interest in the financial

statement of the company are as follows:

1. Financial advisor.

2. Financial Analysis.

HA2032 Final Assessment T2 2021

3. Stock exchanges.

4. Regulatory bodies.

The list who has direct interest are as follows:

1. Company management

2. Company staff

3. Company supplier or creditor

4. Investors or shareholders

The situation which ends up with the indirect ownership interest:

The situation which determines the indirect ownership or interest of stock in corporation,

profit in interest and beneficial interest in trust are as follows:

1. The stock holdings, profit and beneficial interest amount is more than 20% of the total

combined voting power or more than 20% of the profits or beneficial interest

Or

2. More than 35% of the total combined voting power of the company or more than 35%

of the profit or beneficial interest are owned by person described under category of

disqualified person.

END OF FINAL ASSESSMENT

Submission instructions:

Save submission with your STUDENT ID NUMBER and UNIT CODE e.g. EMV54897 HI6025

Submission must be in MICROSOFT WORD FORMAT ONLY

Upload your submission to the appropriate link on Blackboard

Only one submission is accepted. Please ensure your submission is the correct

document.

All submissions are automatically passed through SafeAssign to assess academic integrity.

REFERENCES

Books and Journal

Newman, W. and et.al., 2017. An evaluation of the effectiveness of Financial Statements

in disclosing true business performance to stakeholders in hospitality industry (A

case of Lester-Lesley Limited). Academy of Accounting and Financial Studies

Journal. 21(3). pp.1-22.

HA2032 Final Assessment T2 2021

4. Regulatory bodies.

The list who has direct interest are as follows:

1. Company management

2. Company staff

3. Company supplier or creditor

4. Investors or shareholders

The situation which ends up with the indirect ownership interest:

The situation which determines the indirect ownership or interest of stock in corporation,

profit in interest and beneficial interest in trust are as follows:

1. The stock holdings, profit and beneficial interest amount is more than 20% of the total

combined voting power or more than 20% of the profits or beneficial interest

Or

2. More than 35% of the total combined voting power of the company or more than 35%

of the profit or beneficial interest are owned by person described under category of

disqualified person.

END OF FINAL ASSESSMENT

Submission instructions:

Save submission with your STUDENT ID NUMBER and UNIT CODE e.g. EMV54897 HI6025

Submission must be in MICROSOFT WORD FORMAT ONLY

Upload your submission to the appropriate link on Blackboard

Only one submission is accepted. Please ensure your submission is the correct

document.

All submissions are automatically passed through SafeAssign to assess academic integrity.

REFERENCES

Books and Journal

Newman, W. and et.al., 2017. An evaluation of the effectiveness of Financial Statements

in disclosing true business performance to stakeholders in hospitality industry (A

case of Lester-Lesley Limited). Academy of Accounting and Financial Studies

Journal. 21(3). pp.1-22.

HA2032 Final Assessment T2 2021

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hettiarachchi, H., Meegoda, J. N. and Ryu, S., 2018. Organic waste buyback as a viable

method to enhance sustainable municipal solid waste management in developing

countries. International journal of environmental research and public

health. 15(11). p.2483.

Shi, J. and et.al., 2020. Coordinating the supply chain finance system with buyback

contract: A capital-constrained newsvendor problem. Computers & Industrial

Engineering. 146. p.106587.

HA2032 Final Assessment T2 2021

method to enhance sustainable municipal solid waste management in developing

countries. International journal of environmental research and public

health. 15(11). p.2483.

Shi, J. and et.al., 2020. Coordinating the supply chain finance system with buyback

contract: A capital-constrained newsvendor problem. Computers & Industrial

Engineering. 146. p.106587.

HA2032 Final Assessment T2 2021

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.