HA2032 Corporate & Financial Accounting: AASB, Regulation & Equity

VerifiedAdded on 2023/06/04

|12

|3162

|90

Report

AI Summary

This report delves into the regulation of financial accounting, examining whether mandatory regulations should persist or if voluntary disclosure by management is sufficient. It explores the contributions of the Australian Accounting Standards Board (AASB) and the rationale behind not mandating International Financial Reporting Standards (IFRS) for its members. The report provides an in-depth analysis of the equity segments of four pharmaceutical companies listed on the Australian Stock Exchange, comparing their debt and equity positions over the past four years. Key aspects covered include ordinary equity shares, preference shares, options, reserves, foreign currency translation reserves, and non-controlling interests, offering a comprehensive view of the companies' financial structures and performance.

TABLE OF CONTENTS

Executive Summary............................2

PART(i)...............................................3

PART(ii)..............................................4

PART (iii) (iv).......................................4

Executive Summary............................2

PART(i)...............................................3

PART(ii)..............................................4

PART (iii) (iv).......................................4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary

The intention behind preparation of report is to analyse whether regulation behind preparation shall be

continued or the same shall be dropped and management shall be allowed to disclose content in

annual report voluntarily. Further, the report explores the contribution made by AASB in the

implementation and setting up of AASB and the rationale for not making International Financial

Accounting Standard Compulsory for members.

In the latter half of the report a detailed analysis has been provided with regard to analysis of equity

segment of 4 listed entities in the Australian Exchange dealing in Pharmaceuticals. Further, the report

also provides an in depth analysis regarding the debt and equity position of the 4 companies by

comparing past 4 years.

Executive Summary

The intention behind preparation of report is to analyse whether regulation behind preparation shall be

continued or the same shall be dropped and management shall be allowed to disclose content in

annual report voluntarily. Further, the report explores the contribution made by AASB in the

implementation and setting up of AASB and the rationale for not making International Financial

Accounting Standard Compulsory for members.

In the latter half of the report a detailed analysis has been provided with regard to analysis of equity

segment of 4 listed entities in the Australian Exchange dealing in Pharmaceuticals. Further, the report

also provides an in depth analysis regarding the debt and equity position of the 4 companies by

comparing past 4 years.

PART(i)

Regulation of financial accounting is a very important aspect because of a variety of reasons. The

most important aspect is the use of the financial statement by the outside public and interpreting the

financials of the company in its own way, so a proper set of guidelines need to be prescribed for the

accounting to be done and a standard and method to be set so that the different users to the financial

statement interpret it accordingly and can take the future investment decision in the company .Any

hiding of material facts from the outsiders may make the financial statement fake so the financial

statement should be prepare on a going concern basis with all the material aspects and transparent

accounting, as the users to the financial statement are many which include

creditors,government,shareholders,investors,suppliers and others. The financials of the company

shows the past, present and future activities which need to be undertaken by the company which if

not properly managed and regulated can show untrue information to the outside world and can impact

many investors and users.

The second advantage and the need of controlling financial accounting is the ease of comparison of

financials of the company with the other company within same industry so that it becomes easy for the

investors to take decision to pool their surplus fund and which if not properly regulated can show a

different report for different company and the comparison will become very much difficult for the users.

The third advantage, if the financial accounting presentation and reporting is left at the end of the

management than accounting and reporting will be done in such a way that it only shows the positive

growth aspects of the company through which the small investors can be cheated and the

management of the company can follow this as a regular practice.

The other advantage is that all the company needs to appoint an auditor in order to express his

opinion whether the financial statement of the company are free from any material misstatements and

reveals a true figure .

The main aim for financial accounting regulation to ensure corporate transparency and to discipline in

maintenance in books of accounts.

Though there are various points which show the need to control the financial accounting aspects and

not to be left UN attended in the hands of top level manger.

Regulation of financial accounting is a very important aspect because of a variety of reasons. The

most important aspect is the use of the financial statement by the outside public and interpreting the

financials of the company in its own way, so a proper set of guidelines need to be prescribed for the

accounting to be done and a standard and method to be set so that the different users to the financial

statement interpret it accordingly and can take the future investment decision in the company .Any

hiding of material facts from the outsiders may make the financial statement fake so the financial

statement should be prepare on a going concern basis with all the material aspects and transparent

accounting, as the users to the financial statement are many which include

creditors,government,shareholders,investors,suppliers and others. The financials of the company

shows the past, present and future activities which need to be undertaken by the company which if

not properly managed and regulated can show untrue information to the outside world and can impact

many investors and users.

The second advantage and the need of controlling financial accounting is the ease of comparison of

financials of the company with the other company within same industry so that it becomes easy for the

investors to take decision to pool their surplus fund and which if not properly regulated can show a

different report for different company and the comparison will become very much difficult for the users.

The third advantage, if the financial accounting presentation and reporting is left at the end of the

management than accounting and reporting will be done in such a way that it only shows the positive

growth aspects of the company through which the small investors can be cheated and the

management of the company can follow this as a regular practice.

The other advantage is that all the company needs to appoint an auditor in order to express his

opinion whether the financial statement of the company are free from any material misstatements and

reveals a true figure .

The main aim for financial accounting regulation to ensure corporate transparency and to discipline in

maintenance in books of accounts.

Though there are various points which show the need to control the financial accounting aspects and

not to be left UN attended in the hands of top level manger.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART(ii)

Australia Accounting Standard Board (AASB) it is a board which sets and provides the standards

required by the public and private entity in Australia. These standards are set in such a way that it

serves as an interaction between the global business and the Australian business and contributes in

the reporting of standards which is recognised globally. The main functions of the Australian

Accounting standard Board are:

(a) to form a framework from which the standards can be evaluated.

(b) to prepare new accounting standards under the act. (Australian Government, 2018)

(c) To prepare new accounting standard which is of use to worldwide.

The flow chart has been shown here as under:

(a) Australian Accounting standard Board identifies the issues which are technical and require to

be seen

(b) The issues which have been identified is referred to IASB

(c) IASB add such issue to the agenda

(d) Further research shall be carried on the issue

(e) Shareholders shall be consulted on such issue.

(f) Accounting standards are issued

(g) Report need to be submitted for any comment from IASB

(h) Finally compliance shall be done.

The IFRS set by the International Accounting Standards Board (IASB) not compulsory for the

member countries of IASB due to following :

(a) To use and implement IFRS in Financial statement is not very easy.

(b) IFRS has got its own drawback to use.

(c) IFRS has its own set of policies and accounting procedure

PART (iii) (iv)

The companies that have been chosen by me for the purpose of analysing under Part B of the report

have an interest under basic materials and are listed on Australian Stock Exchange. The companies

that have been selected for detailed analysis has been enumerated here-in-below:-

(a) Alara Resources Limited;

(b) Alchemy Limited;

(c) Alexium International Limited;

(d) Antipa Minerals Limited.

About the Company

Australia Accounting Standard Board (AASB) it is a board which sets and provides the standards

required by the public and private entity in Australia. These standards are set in such a way that it

serves as an interaction between the global business and the Australian business and contributes in

the reporting of standards which is recognised globally. The main functions of the Australian

Accounting standard Board are:

(a) to form a framework from which the standards can be evaluated.

(b) to prepare new accounting standards under the act. (Australian Government, 2018)

(c) To prepare new accounting standard which is of use to worldwide.

The flow chart has been shown here as under:

(a) Australian Accounting standard Board identifies the issues which are technical and require to

be seen

(b) The issues which have been identified is referred to IASB

(c) IASB add such issue to the agenda

(d) Further research shall be carried on the issue

(e) Shareholders shall be consulted on such issue.

(f) Accounting standards are issued

(g) Report need to be submitted for any comment from IASB

(h) Finally compliance shall be done.

The IFRS set by the International Accounting Standards Board (IASB) not compulsory for the

member countries of IASB due to following :

(a) To use and implement IFRS in Financial statement is not very easy.

(b) IFRS has got its own drawback to use.

(c) IFRS has its own set of policies and accounting procedure

PART (iii) (iv)

The companies that have been chosen by me for the purpose of analysing under Part B of the report

have an interest under basic materials and are listed on Australian Stock Exchange. The companies

that have been selected for detailed analysis has been enumerated here-in-below:-

(a) Alara Resources Limited;

(b) Alchemy Limited;

(c) Alexium International Limited;

(d) Antipa Minerals Limited.

About the Company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alara Resources Limited is an Australian listed entity which is engaged in the exploration and

development of minerals. The company has its exploration activity in Australia, Saudi Arabia and

Oman. The resources include copper, gold etc. (Reuters.com, 2018)

For the purpose of analysing the equity portion of the balance sheet of the above four entities, the

following assumption have been undertaken: A detailed breakup of the equity of the company has

been extracted from the annual report of the company and the same has been detailed here-in–

below:

(a) Liabilities which are bearing interest have been considered as debt;

(b) Debt of non-current nature has been considered for the purpose of analysist;

(c) Analysis has been done on the basis of Consolidated Statement of Financial Position for the

past 4 years for 4 entities;

(d) Gross debt has been considered without reducing cash and cash equivalent.

(e) The Annual report has been restated under many a cases, the restated figures have been

considered.

Key terms identified

The following key terms have been identified for the purpose of analysing the equity portion of the

balance sheet of the companies:

(a) Ordinary Equity Shares: These are normal shares of the company and are issued at the time of

inception of the company as increased by additional requirement from time to time. These

shareholders are the owner of the company and have claim on the assets of the company post

disposition of all claims. The liability of such shareholders are restricted to the extent of face

value of such shares.

(b) Preference shares: These are second class of shareholders with less risk compared to equity

and a fixed rate of return. These share generally do not enjoy the benefits as enjoyed by equity

shareholders.

(c) Options: These are the rights issued to personnel of company to be exercised on vesting date

and a used for the computation of diluted Earnings per Share.

(d) Reserves: These are portion of equity which are saved by the company to meet the needs of

future expansion or any unforeseen event in the future.

(e) Foreign Currency translation Reserve: These are part of reserves of the company and are

created in terms of AASB and IFRS while consolidating the books of account of the subsidiaries

in foreign currency. The difference is passed through this reserve.

(f) Available for Sale Investment Reserve: These are created in terms of alignment with AASB

and IFRS to mark investment at fair value on reporting date.

(g) Option Reserve: These are c are created with an intention to make appropriate apportionment

to meet any liability to convert option right into equity;

(h) Cash flow hedging reserve: These reserves are created by a company to reduce the burden of

change in estimated cash flows on the financials of the company;

(i) Non-Controlling interest: These represent claim of persons who hold a minor stake in the

company and have no significant control over the functioning of the company.

development of minerals. The company has its exploration activity in Australia, Saudi Arabia and

Oman. The resources include copper, gold etc. (Reuters.com, 2018)

For the purpose of analysing the equity portion of the balance sheet of the above four entities, the

following assumption have been undertaken: A detailed breakup of the equity of the company has

been extracted from the annual report of the company and the same has been detailed here-in–

below:

(a) Liabilities which are bearing interest have been considered as debt;

(b) Debt of non-current nature has been considered for the purpose of analysist;

(c) Analysis has been done on the basis of Consolidated Statement of Financial Position for the

past 4 years for 4 entities;

(d) Gross debt has been considered without reducing cash and cash equivalent.

(e) The Annual report has been restated under many a cases, the restated figures have been

considered.

Key terms identified

The following key terms have been identified for the purpose of analysing the equity portion of the

balance sheet of the companies:

(a) Ordinary Equity Shares: These are normal shares of the company and are issued at the time of

inception of the company as increased by additional requirement from time to time. These

shareholders are the owner of the company and have claim on the assets of the company post

disposition of all claims. The liability of such shareholders are restricted to the extent of face

value of such shares.

(b) Preference shares: These are second class of shareholders with less risk compared to equity

and a fixed rate of return. These share generally do not enjoy the benefits as enjoyed by equity

shareholders.

(c) Options: These are the rights issued to personnel of company to be exercised on vesting date

and a used for the computation of diluted Earnings per Share.

(d) Reserves: These are portion of equity which are saved by the company to meet the needs of

future expansion or any unforeseen event in the future.

(e) Foreign Currency translation Reserve: These are part of reserves of the company and are

created in terms of AASB and IFRS while consolidating the books of account of the subsidiaries

in foreign currency. The difference is passed through this reserve.

(f) Available for Sale Investment Reserve: These are created in terms of alignment with AASB

and IFRS to mark investment at fair value on reporting date.

(g) Option Reserve: These are c are created with an intention to make appropriate apportionment

to meet any liability to convert option right into equity;

(h) Cash flow hedging reserve: These reserves are created by a company to reduce the burden of

change in estimated cash flows on the financials of the company;

(i) Non-Controlling interest: These represent claim of persons who hold a minor stake in the

company and have no significant control over the functioning of the company.

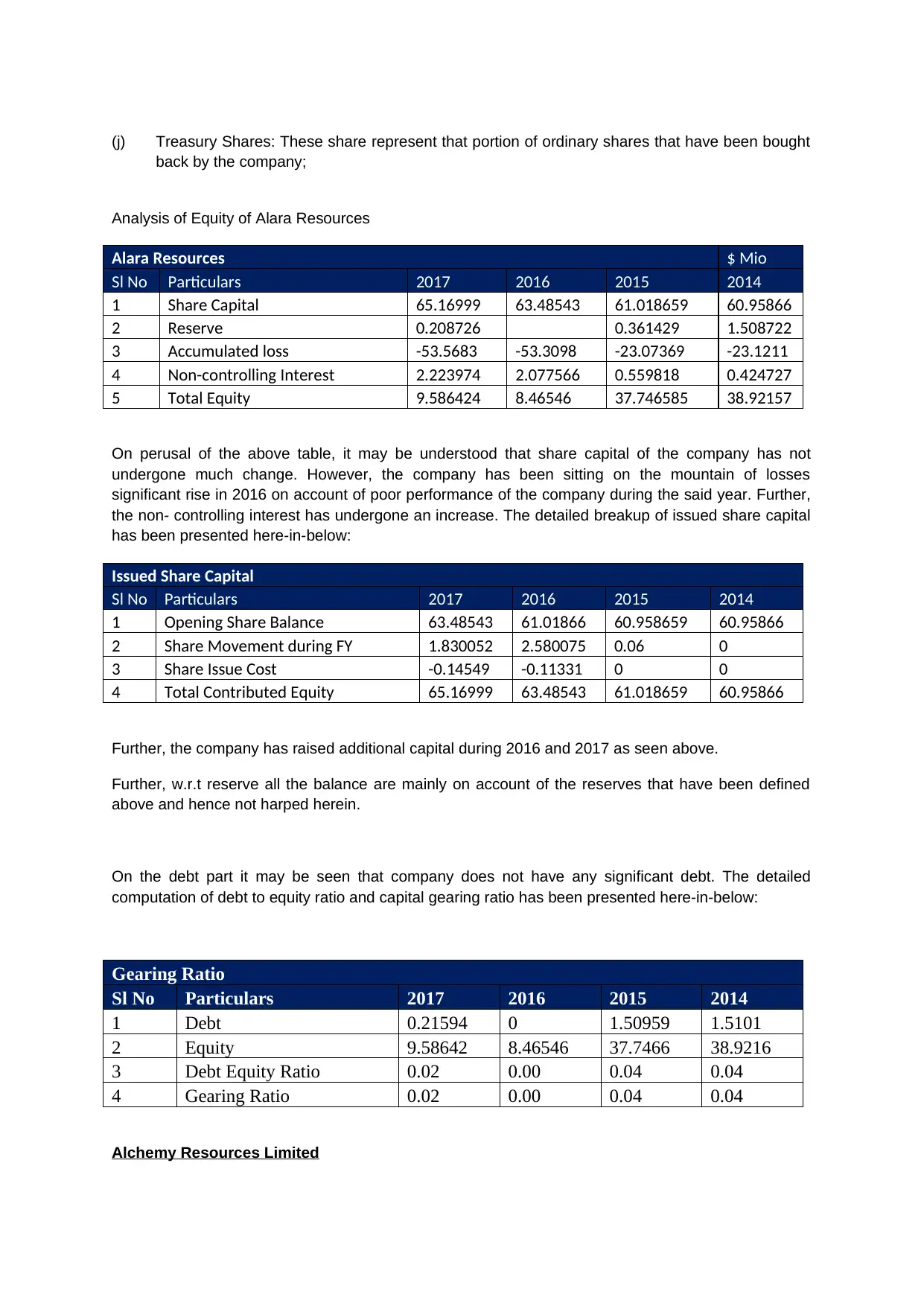

(j) Treasury Shares: These share represent that portion of ordinary shares that have been bought

back by the company;

Analysis of Equity of Alara Resources

Alara Resources $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 65.16999 63.48543 61.018659 60.95866

2 Reserve 0.208726 0.367395 0.361429 1.508722

3 Accumulated loss -53.5683 -53.3098 -23.07369 -23.1211

4 Non-controlling Interest 2.223974 2.077566 0.559818 0.424727

5 Total Equity 9.586424 8.46546 37.746585 38.92157

On perusal of the above table, it may be understood that share capital of the company has not

undergone much change. However, the company has been sitting on the mountain of losses

significant rise in 2016 on account of poor performance of the company during the said year. Further,

the non- controlling interest has undergone an increase. The detailed breakup of issued share capital

has been presented here-in-below:

Issued Share Capital

Sl No Particulars 2017 2016 2015 2014

1 Opening Share Balance 63.48543 61.01866 60.958659 60.95866

2 Share Movement during FY 1.830052 2.580075 0.06 0

3 Share Issue Cost -0.14549 -0.11331 0 0

4 Total Contributed Equity 65.16999 63.48543 61.018659 60.95866

Further, the company has raised additional capital during 2016 and 2017 as seen above.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

On the debt part it may be seen that company does not have any significant debt. The detailed

computation of debt to equity ratio and capital gearing ratio has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0.21594 0 1.50959 1.5101

2 Equity 9.58642 8.46546 37.7466 38.9216

3 Debt Equity Ratio 0.02 0.00 0.04 0.04

4 Gearing Ratio 0.02 0.00 0.04 0.04

Alchemy Resources Limited

back by the company;

Analysis of Equity of Alara Resources

Alara Resources $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Share Capital 65.16999 63.48543 61.018659 60.95866

2 Reserve 0.208726 0.367395 0.361429 1.508722

3 Accumulated loss -53.5683 -53.3098 -23.07369 -23.1211

4 Non-controlling Interest 2.223974 2.077566 0.559818 0.424727

5 Total Equity 9.586424 8.46546 37.746585 38.92157

On perusal of the above table, it may be understood that share capital of the company has not

undergone much change. However, the company has been sitting on the mountain of losses

significant rise in 2016 on account of poor performance of the company during the said year. Further,

the non- controlling interest has undergone an increase. The detailed breakup of issued share capital

has been presented here-in-below:

Issued Share Capital

Sl No Particulars 2017 2016 2015 2014

1 Opening Share Balance 63.48543 61.01866 60.958659 60.95866

2 Share Movement during FY 1.830052 2.580075 0.06 0

3 Share Issue Cost -0.14549 -0.11331 0 0

4 Total Contributed Equity 65.16999 63.48543 61.018659 60.95866

Further, the company has raised additional capital during 2016 and 2017 as seen above.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

On the debt part it may be seen that company does not have any significant debt. The detailed

computation of debt to equity ratio and capital gearing ratio has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0.21594 0 1.50959 1.5101

2 Equity 9.58642 8.46546 37.7466 38.9216

3 Debt Equity Ratio 0.02 0.00 0.04 0.04

4 Gearing Ratio 0.02 0.00 0.04 0.04

Alchemy Resources Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

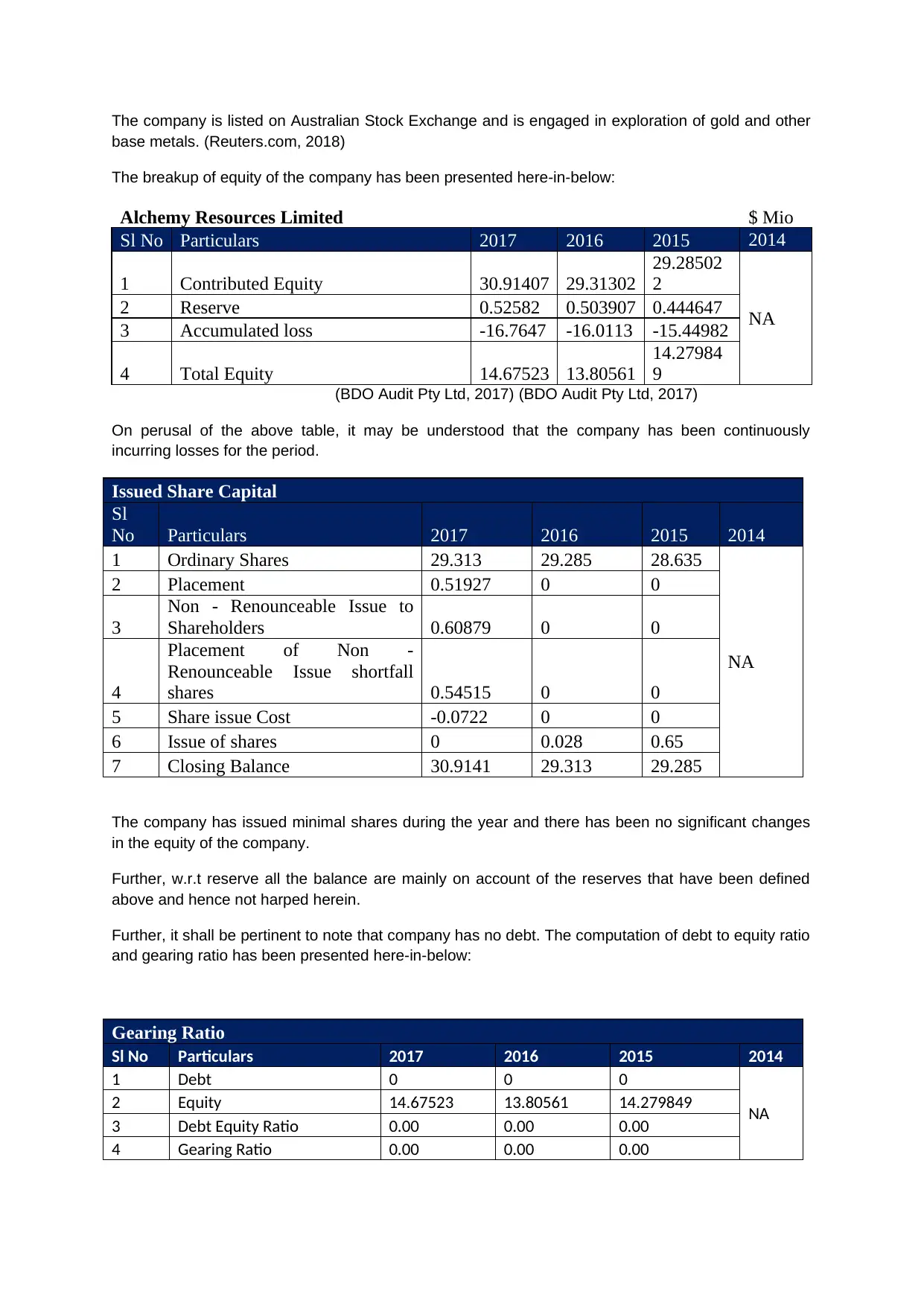

The company is listed on Australian Stock Exchange and is engaged in exploration of gold and other

base metals. (Reuters.com, 2018)

The breakup of equity of the company has been presented here-in-below:

Alchemy Resources Limited $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Contributed Equity 30.91407 29.31302

29.28502

2

NA

2 Reserve 0.52582 0.503907 0.444647

3 Accumulated loss -16.7647 -16.0113 -15.44982

4 Total Equity 14.67523 13.80561

14.27984

9

(BDO Audit Pty Ltd, 2017) (BDO Audit Pty Ltd, 2017)

On perusal of the above table, it may be understood that the company has been continuously

incurring losses for the period.

Issued Share Capital

Sl

No Particulars 2017 2016 2015 2014

1 Ordinary Shares 29.313 29.285 28.635

NA

2 Placement 0.51927 0 0

3

Non - Renounceable Issue to

Shareholders 0.60879 0 0

4

Placement of Non -

Renounceable Issue shortfall

shares 0.54515 0 0

5 Share issue Cost -0.0722 0 0

6 Issue of shares 0 0.028 0.65

7 Closing Balance 30.9141 29.313 29.285

The company has issued minimal shares during the year and there has been no significant changes

in the equity of the company.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

Further, it shall be pertinent to note that company has no debt. The computation of debt to equity ratio

and gearing ratio has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0

NA

2 Equity 14.67523 13.80561 14.279849

3 Debt Equity Ratio 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00

base metals. (Reuters.com, 2018)

The breakup of equity of the company has been presented here-in-below:

Alchemy Resources Limited $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Contributed Equity 30.91407 29.31302

29.28502

2

NA

2 Reserve 0.52582 0.503907 0.444647

3 Accumulated loss -16.7647 -16.0113 -15.44982

4 Total Equity 14.67523 13.80561

14.27984

9

(BDO Audit Pty Ltd, 2017) (BDO Audit Pty Ltd, 2017)

On perusal of the above table, it may be understood that the company has been continuously

incurring losses for the period.

Issued Share Capital

Sl

No Particulars 2017 2016 2015 2014

1 Ordinary Shares 29.313 29.285 28.635

NA

2 Placement 0.51927 0 0

3

Non - Renounceable Issue to

Shareholders 0.60879 0 0

4

Placement of Non -

Renounceable Issue shortfall

shares 0.54515 0 0

5 Share issue Cost -0.0722 0 0

6 Issue of shares 0 0.028 0.65

7 Closing Balance 30.9141 29.313 29.285

The company has issued minimal shares during the year and there has been no significant changes

in the equity of the company.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

Further, it shall be pertinent to note that company has no debt. The computation of debt to equity ratio

and gearing ratio has been presented here-in-below:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0

NA

2 Equity 14.67523 13.80561 14.279849

3 Debt Equity Ratio 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alexium International Limited

The company is listed on Australian Stock Exchange and is engaged in conducting research and

development of technology, licensing etc. The company also sells its specialised chemistry to

customers. ( THE FINANCIAL TIMES LTD, 2018)

The detailed breakup of the equity of the company has been presented here-in-below:

ALEXIUM INTERNATIONAL GROUP LIMITED $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Contributed Equity 52.82004 51.63448 41.363396

24.8053

4

2 Reserve 8.973213 9.051563 4.417082

0.44948

2

3 Accumulated loss -61.5738 -49.4185 -33.97364 -22.2101

4 Total Equity 0.219474 11.26753 11.806837

3.04474

6

(GRANT THORNTON AUDIT PTY LTD, 2017)(GRANT THORNTON AUDIT PTY LTD, 2017)

On perusal of the above table, it may understood that losses of the company have been increasing

continuously which is in alignment with above 2 companies reported. Further, the total equity of

company has fallen drastically on account of losses.

The company has issued additional shares during the year. The detailed breakup of the same has

been provided here-in-below:

Issued Share Capital

Sl

No Particulars 2017 2016 2015 2014

1 Balance at the beginning of the year

51.634

5

41.363

4

24.805

3

18.092

8

2 Options converted to shares

0.6630

3

3.9061

1 1.7595

0.1266

7

3 Capital Raising 6

10.162

5 5.22

4 Cost of Capital raising -0.369 -2.4496 -0.4038

5 Shares issued in lieu of salary & Sales

0.3197

5

0.2792

8

0.3457

5

0.1284

1

6 Shares issued in lieu of services

0.2027

8

0.4546

9

7 Share Purchase Plan 0 0 0

1.4999

8

8 Unmarketable Parcel Buyback 0 0 0 -0.0124

9 Derivative 0 0

5.0182

1

0.0032

9

10 Series A & B convertible Note 0 0 1.6475 0.15

11 Transfer of Conversion note 0 0 0.0742

12 Total 52.82 51.634 41.363 24.804

The company is listed on Australian Stock Exchange and is engaged in conducting research and

development of technology, licensing etc. The company also sells its specialised chemistry to

customers. ( THE FINANCIAL TIMES LTD, 2018)

The detailed breakup of the equity of the company has been presented here-in-below:

ALEXIUM INTERNATIONAL GROUP LIMITED $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Contributed Equity 52.82004 51.63448 41.363396

24.8053

4

2 Reserve 8.973213 9.051563 4.417082

0.44948

2

3 Accumulated loss -61.5738 -49.4185 -33.97364 -22.2101

4 Total Equity 0.219474 11.26753 11.806837

3.04474

6

(GRANT THORNTON AUDIT PTY LTD, 2017)(GRANT THORNTON AUDIT PTY LTD, 2017)

On perusal of the above table, it may understood that losses of the company have been increasing

continuously which is in alignment with above 2 companies reported. Further, the total equity of

company has fallen drastically on account of losses.

The company has issued additional shares during the year. The detailed breakup of the same has

been provided here-in-below:

Issued Share Capital

Sl

No Particulars 2017 2016 2015 2014

1 Balance at the beginning of the year

51.634

5

41.363

4

24.805

3

18.092

8

2 Options converted to shares

0.6630

3

3.9061

1 1.7595

0.1266

7

3 Capital Raising 6

10.162

5 5.22

4 Cost of Capital raising -0.369 -2.4496 -0.4038

5 Shares issued in lieu of salary & Sales

0.3197

5

0.2792

8

0.3457

5

0.1284

1

6 Shares issued in lieu of services

0.2027

8

0.4546

9

7 Share Purchase Plan 0 0 0

1.4999

8

8 Unmarketable Parcel Buyback 0 0 0 -0.0124

9 Derivative 0 0

5.0182

1

0.0032

9

10 Series A & B convertible Note 0 0 1.6475 0.15

11 Transfer of Conversion note 0 0 0.0742

12 Total 52.82 51.634 41.363 24.804

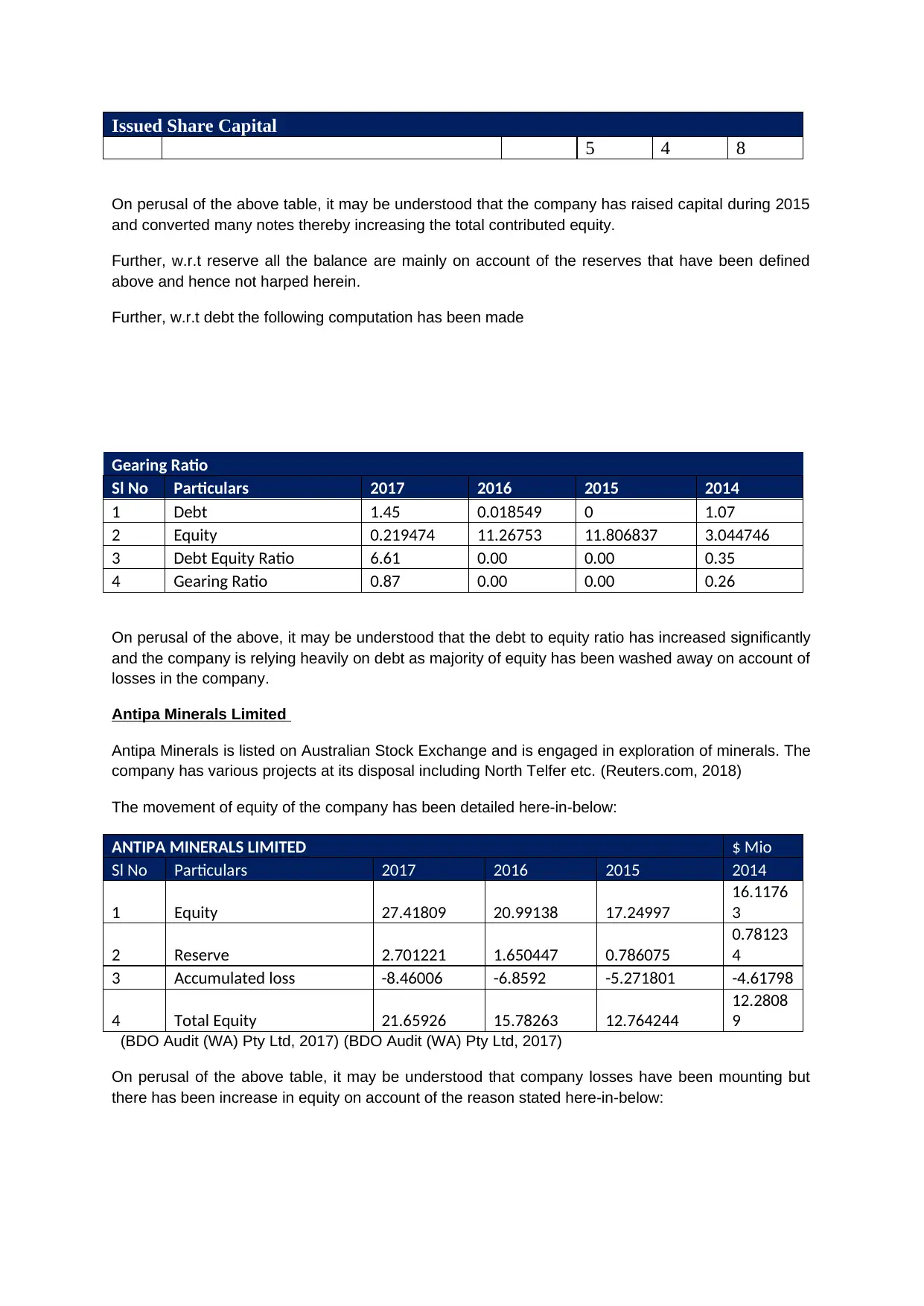

Issued Share Capital

5 4 8

On perusal of the above table, it may be understood that the company has raised capital during 2015

and converted many notes thereby increasing the total contributed equity.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

Further, w.r.t debt the following computation has been made

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 1.45 0.018549 0 1.07

2 Equity 0.219474 11.26753 11.806837 3.044746

3 Debt Equity Ratio 6.61 0.00 0.00 0.35

4 Gearing Ratio 0.87 0.00 0.00 0.26

On perusal of the above, it may be understood that the debt to equity ratio has increased significantly

and the company is relying heavily on debt as majority of equity has been washed away on account of

losses in the company.

Antipa Minerals Limited

Antipa Minerals is listed on Australian Stock Exchange and is engaged in exploration of minerals. The

company has various projects at its disposal including North Telfer etc. (Reuters.com, 2018)

The movement of equity of the company has been detailed here-in-below:

ANTIPA MINERALS LIMITED $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Equity 27.41809 20.99138 17.24997

16.1176

3

2 Reserve 2.701221 1.650447 0.786075

0.78123

4

3 Accumulated loss -8.46006 -6.8592 -5.271801 -4.61798

4 Total Equity 21.65926 15.78263 12.764244

12.2808

9

(BDO Audit (WA) Pty Ltd, 2017) (BDO Audit (WA) Pty Ltd, 2017)

On perusal of the above table, it may be understood that company losses have been mounting but

there has been increase in equity on account of the reason stated here-in-below:

5 4 8

On perusal of the above table, it may be understood that the company has raised capital during 2015

and converted many notes thereby increasing the total contributed equity.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

Further, w.r.t debt the following computation has been made

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 1.45 0.018549 0 1.07

2 Equity 0.219474 11.26753 11.806837 3.044746

3 Debt Equity Ratio 6.61 0.00 0.00 0.35

4 Gearing Ratio 0.87 0.00 0.00 0.26

On perusal of the above, it may be understood that the debt to equity ratio has increased significantly

and the company is relying heavily on debt as majority of equity has been washed away on account of

losses in the company.

Antipa Minerals Limited

Antipa Minerals is listed on Australian Stock Exchange and is engaged in exploration of minerals. The

company has various projects at its disposal including North Telfer etc. (Reuters.com, 2018)

The movement of equity of the company has been detailed here-in-below:

ANTIPA MINERALS LIMITED $ Mio

Sl No Particulars 2017 2016 2015 2014

1 Equity 27.41809 20.99138 17.24997

16.1176

3

2 Reserve 2.701221 1.650447 0.786075

0.78123

4

3 Accumulated loss -8.46006 -6.8592 -5.271801 -4.61798

4 Total Equity 21.65926 15.78263 12.764244

12.2808

9

(BDO Audit (WA) Pty Ltd, 2017) (BDO Audit (WA) Pty Ltd, 2017)

On perusal of the above table, it may be understood that company losses have been mounting but

there has been increase in equity on account of the reason stated here-in-below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

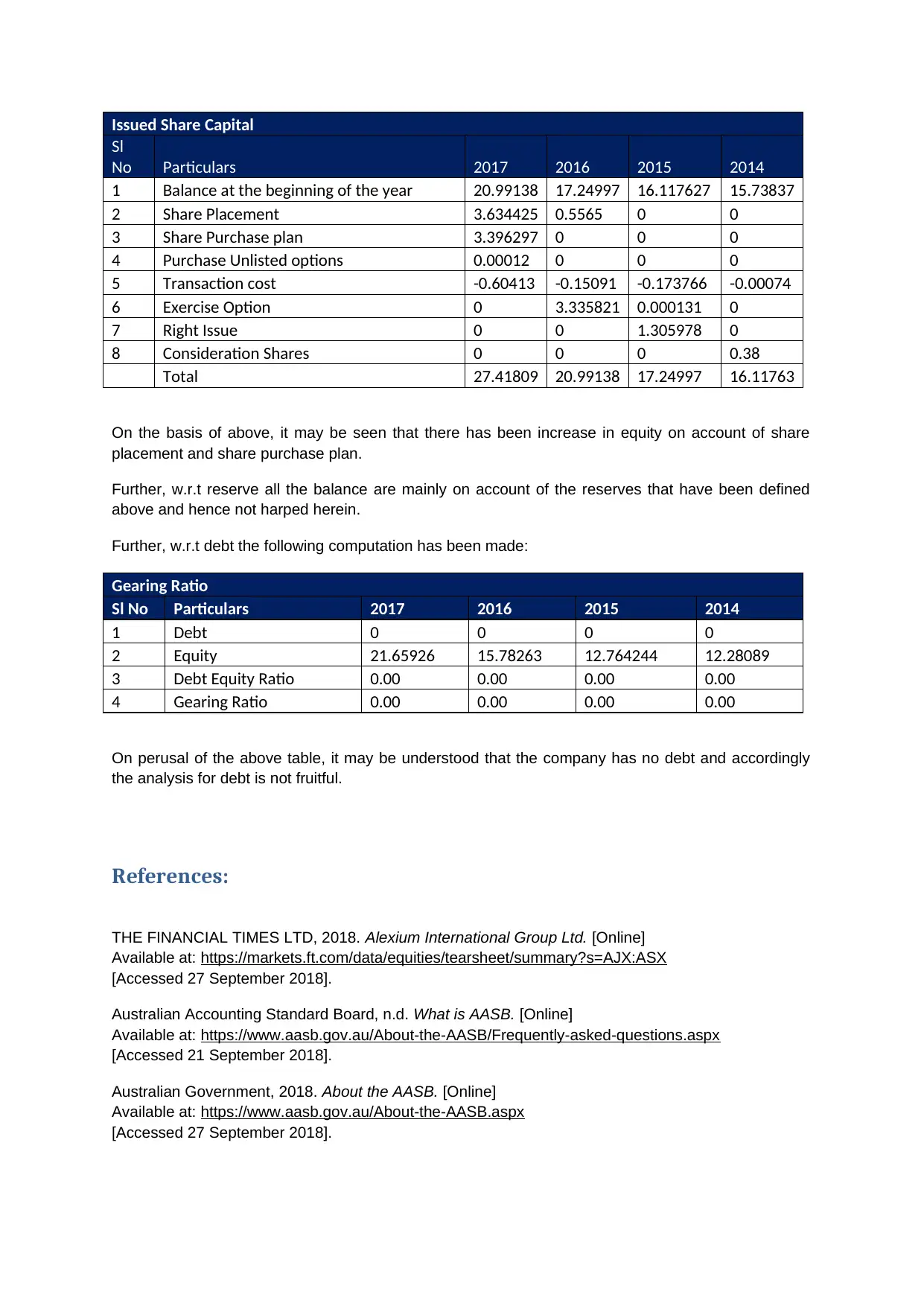

Issued Share Capital

Sl

No Particulars 2017 2016 2015 2014

1 Balance at the beginning of the year 20.99138 17.24997 16.117627 15.73837

2 Share Placement 3.634425 0.5565 0 0

3 Share Purchase plan 3.396297 0 0 0

4 Purchase Unlisted options 0.00012 0 0 0

5 Transaction cost -0.60413 -0.15091 -0.173766 -0.00074

6 Exercise Option 0 3.335821 0.000131 0

7 Right Issue 0 0 1.305978 0

8 Consideration Shares 0 0 0 0.38

Total 27.41809 20.99138 17.24997 16.11763

On the basis of above, it may be seen that there has been increase in equity on account of share

placement and share purchase plan.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

Further, w.r.t debt the following computation has been made:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 21.65926 15.78263 12.764244 12.28089

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above table, it may be understood that the company has no debt and accordingly

the analysis for debt is not fruitful.

References:

THE FINANCIAL TIMES LTD, 2018. Alexium International Group Ltd. [Online]

Available at: https://markets.ft.com/data/equities/tearsheet/summary?s=AJX:ASX

[Accessed 27 September 2018].

Australian Accounting Standard Board, n.d. What is AASB. [Online]

Available at: https://www.aasb.gov.au/About-the-AASB/Frequently-asked-questions.aspx

[Accessed 21 September 2018].

Australian Government, 2018. About the AASB. [Online]

Available at: https://www.aasb.gov.au/About-the-AASB.aspx

[Accessed 27 September 2018].

Sl

No Particulars 2017 2016 2015 2014

1 Balance at the beginning of the year 20.99138 17.24997 16.117627 15.73837

2 Share Placement 3.634425 0.5565 0 0

3 Share Purchase plan 3.396297 0 0 0

4 Purchase Unlisted options 0.00012 0 0 0

5 Transaction cost -0.60413 -0.15091 -0.173766 -0.00074

6 Exercise Option 0 3.335821 0.000131 0

7 Right Issue 0 0 1.305978 0

8 Consideration Shares 0 0 0 0.38

Total 27.41809 20.99138 17.24997 16.11763

On the basis of above, it may be seen that there has been increase in equity on account of share

placement and share purchase plan.

Further, w.r.t reserve all the balance are mainly on account of the reserves that have been defined

above and hence not harped herein.

Further, w.r.t debt the following computation has been made:

Gearing Ratio

Sl No Particulars 2017 2016 2015 2014

1 Debt 0 0 0 0

2 Equity 21.65926 15.78263 12.764244 12.28089

3 Debt Equity Ratio 0.00 0.00 0.00 0.00

4 Gearing Ratio 0.00 0.00 0.00 0.00

On perusal of the above table, it may be understood that the company has no debt and accordingly

the analysis for debt is not fruitful.

References:

THE FINANCIAL TIMES LTD, 2018. Alexium International Group Ltd. [Online]

Available at: https://markets.ft.com/data/equities/tearsheet/summary?s=AJX:ASX

[Accessed 27 September 2018].

Australian Accounting Standard Board, n.d. What is AASB. [Online]

Available at: https://www.aasb.gov.au/About-the-AASB/Frequently-asked-questions.aspx

[Accessed 21 September 2018].

Australian Government, 2018. About the AASB. [Online]

Available at: https://www.aasb.gov.au/About-the-AASB.aspx

[Accessed 27 September 2018].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BDO Audit (WA) Pty Ltd, 2017. Annual Report 2017. [Online]

Available at: http://antipaminerals.com.au/annual-report-for-the-year-ended-30-june-2017/

[Accessed 27 September 2018].

BDO Audit Pty Ltd, 2017. Annual Report 2017. [Online]

Available at: http://alchemyresources.com.au/annual-reports/2017

[Accessed 27 September 20018].

GRANT THORNTON AUDIT PTY LTD, 2017. Annual Report 2017. [Online]

Available at: alexiuminternational.com/wp-content/.../2017-Annual-Report-to-Shareholders.pd

[Accessed 27 September 2018].

Reuters.com, 2018. Alara Resources Ltd. [Online]

Available at: https://in.reuters.com/finance/stocks/overview/AUQ.AX

[Accessed 27 September 2018].

Reuters.com, 2018. Alchemy Resources Ltd (ALY.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/ALY.AX

[Accessed 27 September 2018].

Reuters.com, 2018. Antipa Minerals Ltd (AZY.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/AZY.AX

[Accessed 27 September 2018].

Available at: http://antipaminerals.com.au/annual-report-for-the-year-ended-30-june-2017/

[Accessed 27 September 2018].

BDO Audit Pty Ltd, 2017. Annual Report 2017. [Online]

Available at: http://alchemyresources.com.au/annual-reports/2017

[Accessed 27 September 20018].

GRANT THORNTON AUDIT PTY LTD, 2017. Annual Report 2017. [Online]

Available at: alexiuminternational.com/wp-content/.../2017-Annual-Report-to-Shareholders.pd

[Accessed 27 September 2018].

Reuters.com, 2018. Alara Resources Ltd. [Online]

Available at: https://in.reuters.com/finance/stocks/overview/AUQ.AX

[Accessed 27 September 2018].

Reuters.com, 2018. Alchemy Resources Ltd (ALY.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/ALY.AX

[Accessed 27 September 2018].

Reuters.com, 2018. Antipa Minerals Ltd (AZY.AX). [Online]

Available at: https://www.reuters.com/finance/stocks/overview/AZY.AX

[Accessed 27 September 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.