HA2032 Corporate Accounting: Financial Reporting, Regulation & Equity

VerifiedAdded on 2023/06/08

|15

|3178

|88

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, covering financial reporting regulations, the role of the Australian Accounting Standards Board (AASB) in setting global standards, and an examination of owner's equity for four companies listed on the Australian Securities Exchange (ASX): Woolworths, Wesfarmers, JB Hi-Fi, and Metcash. It discusses the importance of regulating financial reporting to ensure credible commitments, comparability, and to address information asymmetry. The report also explains the AASB's participation in the global standard-setting process and reasons why IFRS adoption isn't compulsory for IASB member countries. The analysis of owner's equity includes a review of reserves, contributed equity, and retained earnings for each of the selected companies, offering insights into their financial positions and performance.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Executive summary:

The report is divided into three sections comprising of corporate regulation, accounting standard

settings and owner’s equity. In the first section, the importance of regulation in the financial

reporting process has been addressed. The second section demonstrates critical explanation of te

standard setting process of AASB. Furthermore, last section depicts the analysis of owner’s

equity of four companies listed on Australian stock exchange. For this purpose, information have

been sourced from the published annual reports accessed from their respective websites.

Table of Contents

Executive summary:

The report is divided into three sections comprising of corporate regulation, accounting standard

settings and owner’s equity. In the first section, the importance of regulation in the financial

reporting process has been addressed. The second section demonstrates critical explanation of te

standard setting process of AASB. Furthermore, last section depicts the analysis of owner’s

equity of four companies listed on Australian stock exchange. For this purpose, information have

been sourced from the published annual reports accessed from their respective websites.

Table of Contents

2CORPORATE ACCOUNTING

Introduction:....................................................................................................................................2

Discussion:.......................................................................................................................................2

Critical discussion of regulation of financial accounting and regulation:.......................................2

Explanation of participation of Australian accounting standard board in the setting process of

global accounting standard:.............................................................................................................2

Explanation of why IFRS is not compulsory for member countries of IASB:................................2

Analysis of owner’s equity of four selected companies:.................................................................2

Conclusion:......................................................................................................................................2

References list:.................................................................................................................................3

Introduction:....................................................................................................................................2

Discussion:.......................................................................................................................................2

Critical discussion of regulation of financial accounting and regulation:.......................................2

Explanation of participation of Australian accounting standard board in the setting process of

global accounting standard:.............................................................................................................2

Explanation of why IFRS is not compulsory for member countries of IASB:................................2

Analysis of owner’s equity of four selected companies:.................................................................2

Conclusion:......................................................................................................................................2

References list:.................................................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction:

The report is prepared for evaluating the effectiveness of Internal financial reporting

standard (IFRS) and whether regulating the financial reporting is essential. In addition to this,

report also demonstrates the process of Australian accounting standard board in setting the global

accounting standard. The adoption of the international financial reporting standard has been

evaluated in terms of its mandate to the members of International Australian accounting standard

(IASB). The section of owner’s equity illustrates the analysis of the financial statements of four

public companies listed on the Australian stock exchange (ASX). Four companies that have been

selected from the list of AXS comprise of Woolworths, Wesfarmers, JB Hi-Fi and Met cash.

Discussion:

Critical discussion of regulation of financial accounting and regulation:

The need for regulation of financial accounting reporting arises because of several

reasons. Financial reporting has considerable number of users ranging from employee group,

investor group, government and public analyst adviser group to other key stakeholders. It is

essential for these users to systematically interpret and use the financial information for making

investment and financial decision. In the absence of regulation of financial report, such financial

reports would be prepared in a diversified way aligning to their requirements and therefore,

different financial reported will be interpreted by users in different way (Schührer 2018).

Consequently the financial information contained therein would be too ambiguous to understand

for users. The accounting practice differs from country to country and accounting regulation is

Introduction:

The report is prepared for evaluating the effectiveness of Internal financial reporting

standard (IFRS) and whether regulating the financial reporting is essential. In addition to this,

report also demonstrates the process of Australian accounting standard board in setting the global

accounting standard. The adoption of the international financial reporting standard has been

evaluated in terms of its mandate to the members of International Australian accounting standard

(IASB). The section of owner’s equity illustrates the analysis of the financial statements of four

public companies listed on the Australian stock exchange (ASX). Four companies that have been

selected from the list of AXS comprise of Woolworths, Wesfarmers, JB Hi-Fi and Met cash.

Discussion:

Critical discussion of regulation of financial accounting and regulation:

The need for regulation of financial accounting reporting arises because of several

reasons. Financial reporting has considerable number of users ranging from employee group,

investor group, government and public analyst adviser group to other key stakeholders. It is

essential for these users to systematically interpret and use the financial information for making

investment and financial decision. In the absence of regulation of financial report, such financial

reports would be prepared in a diversified way aligning to their requirements and therefore,

different financial reported will be interpreted by users in different way (Schührer 2018).

Consequently the financial information contained therein would be too ambiguous to understand

for users. The accounting practice differs from country to country and accounting regulation is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

required to eliminate the differences between the accounting practices and creating standard

practice (Schaltegger et al. 2017). Fowling mentioned points provides argument in favor of

regulation of financial disclosures and they are as follows:

Lack of credible commitment- The advantage of regulation the financial and accounting

reporting comes from the fact that they generate reliable information and many of which results

from credible commitment. There would be more effective enforcement imposed by regulatory

regimes as compared to voluntary regimes that helps in producing more credible commitments

and reliable disclosures (Morris 2017).

Lack of comparability- Regulation of financial report provides the benefit of

standardization of information that can be achieved in an effective and cheap way when such

reporting is prepared on mandatory basis (Stadler and Nobes 2018).

Asymmetry of information- It is argued that capital market participants are able to take

the advantage of people who have les information in the absence of regulation of financial

reporting. Such advantages can be taken in the form of buying share at fewer prices that they

actually worth, selling at price that it actually worth and committing outright fraud. Had the

financial reporting been regulated, such market participants would not be able to take the undue

market advantage (McConville and Cordery 2018).

Voluntary disclosure and mandated financial reporting are the two channels that is used

by managers to communicate the private information which is considered relevant as evident by

changes in liquidity and stock price. Furthermore, voluntary disclosure is used by mangers to

communicate superior knowledge of the performance of firms to investors and supplement the

mandatory reporting. Discretion of managers is often required in event of difficulty in

required to eliminate the differences between the accounting practices and creating standard

practice (Schaltegger et al. 2017). Fowling mentioned points provides argument in favor of

regulation of financial disclosures and they are as follows:

Lack of credible commitment- The advantage of regulation the financial and accounting

reporting comes from the fact that they generate reliable information and many of which results

from credible commitment. There would be more effective enforcement imposed by regulatory

regimes as compared to voluntary regimes that helps in producing more credible commitments

and reliable disclosures (Morris 2017).

Lack of comparability- Regulation of financial report provides the benefit of

standardization of information that can be achieved in an effective and cheap way when such

reporting is prepared on mandatory basis (Stadler and Nobes 2018).

Asymmetry of information- It is argued that capital market participants are able to take

the advantage of people who have les information in the absence of regulation of financial

reporting. Such advantages can be taken in the form of buying share at fewer prices that they

actually worth, selling at price that it actually worth and committing outright fraud. Had the

financial reporting been regulated, such market participants would not be able to take the undue

market advantage (McConville and Cordery 2018).

Voluntary disclosure and mandated financial reporting are the two channels that is used

by managers to communicate the private information which is considered relevant as evident by

changes in liquidity and stock price. Furthermore, voluntary disclosure is used by mangers to

communicate superior knowledge of the performance of firms to investors and supplement the

mandatory reporting. Discretion of managers is often required in event of difficulty in

5CORPORATE ACCOUNTING

implementation of fair value accounting. Since the private information of managers forms the

basis of voluntary disclosures, they tend to be more informative about the true earnings. It has

been found that there would be more informative disclosure by managers if there is increased

mandatory reporting (Domino et al. 2015).

Explanation of participation of Australian accounting standard board in the setting process

of global accounting standard:

The Australian accounting standard board (AASB) outlines the functions and power

about it working and contribution to the global standard setting process. The international

financial reporting has been adopted by Australia that aligns with the financial reporting council

strategic direction. Therefore, the work program of AASB incorporates IFRIC work program

and IASB work program. However, there is variation in degree of involvement which may be

non substantive or substantive. The work program of International public sector accounting

standard board is closely monitored by AASB (Maas et al. 2016).

implementation of fair value accounting. Since the private information of managers forms the

basis of voluntary disclosures, they tend to be more informative about the true earnings. It has

been found that there would be more informative disclosure by managers if there is increased

mandatory reporting (Domino et al. 2015).

Explanation of participation of Australian accounting standard board in the setting process

of global accounting standard:

The Australian accounting standard board (AASB) outlines the functions and power

about it working and contribution to the global standard setting process. The international

financial reporting has been adopted by Australia that aligns with the financial reporting council

strategic direction. Therefore, the work program of AASB incorporates IFRIC work program

and IASB work program. However, there is variation in degree of involvement which may be

non substantive or substantive. The work program of International public sector accounting

standard board is closely monitored by AASB (Maas et al. 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

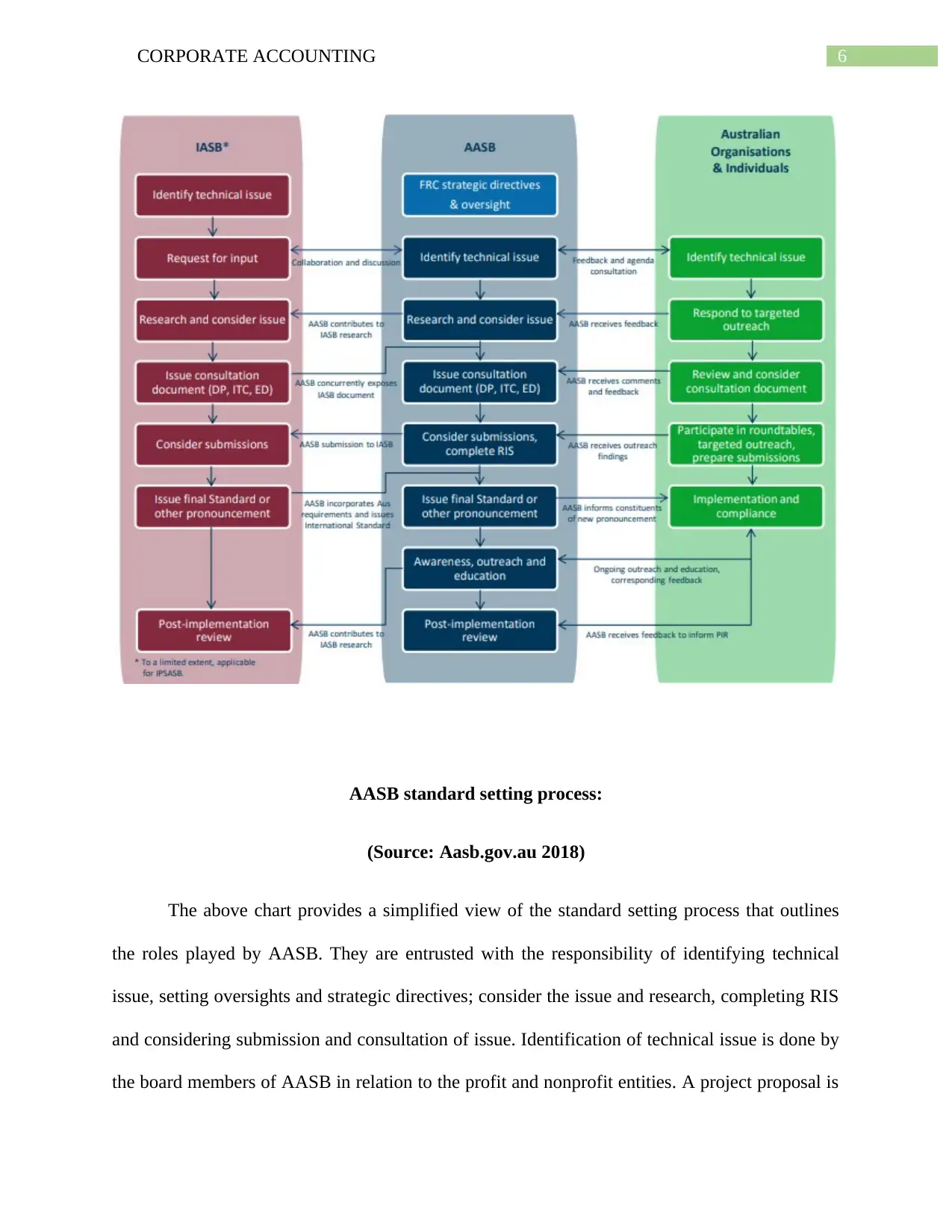

AASB standard setting process:

(Source: Aasb.gov.au 2018)

The above chart provides a simplified view of the standard setting process that outlines

the roles played by AASB. They are entrusted with the responsibility of identifying technical

issue, setting oversights and strategic directives; consider the issue and research, completing RIS

and considering submission and consultation of issue. Identification of technical issue is done by

the board members of AASB in relation to the profit and nonprofit entities. A project proposal is

AASB standard setting process:

(Source: Aasb.gov.au 2018)

The above chart provides a simplified view of the standard setting process that outlines

the roles played by AASB. They are entrusted with the responsibility of identifying technical

issue, setting oversights and strategic directives; consider the issue and research, completing RIS

and considering submission and consultation of issue. Identification of technical issue is done by

the board members of AASB in relation to the profit and nonprofit entities. A project proposal is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

developed by AASB after the identification of technical issue has been done. Furthermore, an

assessment of potential benefits of the project is done and decision about the worthiness of

project is undertaken. After adding issue to the agenda, the agenda papers are presented a

discussed with staff which addresses the alternative approaches, scope of issue and outcome

timings. Thereafter completing the research work, the related documents are made available for

discussing with stakeholders and for public comments. The issue of pronouncements might be

the outcomes of consideration of AASB. All the inputs provided by the Australian organization

are submitted to international organizations. The formal letters are requested by AASB and the

interpretation and implementation of accounting standards is monitored by the standard.

Explanation of why IFRS is not compulsory for member countries of IASB:

The international financial reporting standard (IFRS) is the accounting standards that

have been implemented and developed by International accounting standard board having fifteen

member countries including IFRS. A business is able to facilitate comparison of their financial

statements by the adoption of this particular reporting standard. In the current scenario, it is not

mandatory for the member of IASB countries to adopt the reporting standard because the full

acceptance of standard results in loosing of certain level of quality. For instance, full acceptance

of IFRS would be rejected by United States because they might not have market incentive for

preparing financial statements (Camfferman and Zeff 2018). In addition to this, it is also

believed that benefits would be outweighed by the cost associated with the adoption of IFRS.

Analysis of owner’s equity of four selected companies:

In this particular section of report, the analysis of comprehensive statement of changes in

equity of four chosen companies has been demonstrated.

developed by AASB after the identification of technical issue has been done. Furthermore, an

assessment of potential benefits of the project is done and decision about the worthiness of

project is undertaken. After adding issue to the agenda, the agenda papers are presented a

discussed with staff which addresses the alternative approaches, scope of issue and outcome

timings. Thereafter completing the research work, the related documents are made available for

discussing with stakeholders and for public comments. The issue of pronouncements might be

the outcomes of consideration of AASB. All the inputs provided by the Australian organization

are submitted to international organizations. The formal letters are requested by AASB and the

interpretation and implementation of accounting standards is monitored by the standard.

Explanation of why IFRS is not compulsory for member countries of IASB:

The international financial reporting standard (IFRS) is the accounting standards that

have been implemented and developed by International accounting standard board having fifteen

member countries including IFRS. A business is able to facilitate comparison of their financial

statements by the adoption of this particular reporting standard. In the current scenario, it is not

mandatory for the member of IASB countries to adopt the reporting standard because the full

acceptance of standard results in loosing of certain level of quality. For instance, full acceptance

of IFRS would be rejected by United States because they might not have market incentive for

preparing financial statements (Camfferman and Zeff 2018). In addition to this, it is also

believed that benefits would be outweighed by the cost associated with the adoption of IFRS.

Analysis of owner’s equity of four selected companies:

In this particular section of report, the analysis of comprehensive statement of changes in

equity of four chosen companies has been demonstrated.

8CORPORATE ACCOUNTING

Reserves- Reserves are those portions of profitability of business that helps in

strengthening the financial position of organization. The funds that forms the part of reserves are

often used by organization to repay debts, purchase fixed assets, dividend repayment and

bonuses (Tan et al. 2016).

Contributed equity- Contributed capital is one of the components of equity that are also

known as the issued capital which are contributed by the shareholders of company for buying the

stocks. They represent the contribution of owner into the business (Dagwell et al. 2015).

Retained earnings- Retained earnings are the profits that have been reinvested into the

business and they represent the net earnings after making the payment of dividends (Uyar 2016).

Analysis of each items of equity of Woolworths:

The items of equity comprised of reserves, contributed equity and retained earnings. The

amount of contributed equity stood at $ (million) 6055 in year 2018 compared to $ 5615, $ 5252

and 5064.9 in year 2017, 2016 and 2015 respectively. From the figures, it can be inferred that the

value contributed equity has increased since year 2015. Value of reserves is recorded at $ 353, $

357 in year 2018 and 2017 compared to $ 93.9 and 95.1 in year 2016 and 2015 respectively. It is

suggested by the figure that reserves value has increased in recent years. Furthermore, retained

earnings are recorded at $ 4073, $ 3554, $ 3124.5 and $ 5831.0 in year 2018, 2017, 2016 and

2015 respectively (Woolworthsgroup.com.au 2018). It can be seen that retained earning value

decreased initially and increased subsequently.

Analysis of each items of equity of Wesfarmers:

Reserves- Reserves are those portions of profitability of business that helps in

strengthening the financial position of organization. The funds that forms the part of reserves are

often used by organization to repay debts, purchase fixed assets, dividend repayment and

bonuses (Tan et al. 2016).

Contributed equity- Contributed capital is one of the components of equity that are also

known as the issued capital which are contributed by the shareholders of company for buying the

stocks. They represent the contribution of owner into the business (Dagwell et al. 2015).

Retained earnings- Retained earnings are the profits that have been reinvested into the

business and they represent the net earnings after making the payment of dividends (Uyar 2016).

Analysis of each items of equity of Woolworths:

The items of equity comprised of reserves, contributed equity and retained earnings. The

amount of contributed equity stood at $ (million) 6055 in year 2018 compared to $ 5615, $ 5252

and 5064.9 in year 2017, 2016 and 2015 respectively. From the figures, it can be inferred that the

value contributed equity has increased since year 2015. Value of reserves is recorded at $ 353, $

357 in year 2018 and 2017 compared to $ 93.9 and 95.1 in year 2016 and 2015 respectively. It is

suggested by the figure that reserves value has increased in recent years. Furthermore, retained

earnings are recorded at $ 4073, $ 3554, $ 3124.5 and $ 5831.0 in year 2018, 2017, 2016 and

2015 respectively (Woolworthsgroup.com.au 2018). It can be seen that retained earning value

decreased initially and increased subsequently.

Analysis of each items of equity of Wesfarmers:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

The items of equity comprised of equity capital, reserves, retained earnings and reserved

shares. For year ending 2018 and 2017, issued capital is reported at $ 22277 million and $ 22268

million compared to $ 21937 and $ 21844 in year 2016 and 2015 respectively. There has been

consistent increase in value of issued capital. Value of retained earnings is recorded at $ 176 for

year 2018 compared to $ 1509, $ 874 and $ 2742 for year 2017, 2016 and 2015 respectively.

Value of retained earning has declined significantly initially and increased and decline further in

the current year. Reserves other hand stood at 344, 190, 166 and 226 for year 2018, 2017, 2016

and 2015 respectively. Value of reserves declined initially and then increased thereafter

indicating that the reserves account has enhanced due to increased profits.

Analysis of each items of equity of JB Hi-Fi:

The amount of contributed equity stood at $ 438.7 and $ 49.3 in year 2017 and 2016

compared to $ 565.21 in year 2015. It is indicated by the figure that there has been considerable

decline in value of contributed equity. Value of reserves is recorded at $ 33.2 and $ 27.1 in year

2017 and 2016 compared to $ 17.63 in year 2015 respectively indicating a consistent increase in

value. Now, looking at the figures of retained earnings, it can be seen that the amount is recorded

at $ 381.6 and $ 328.3 in year 2017 and 2016 respectively compared to $ 269.3 in year 2015. The

figure suggests that the value of retained earnings is increasing year on year.

Analysis of each items of equity of Met cash:

For Met cash, the amount of contributed and other equity is recorded at $ 600 in year

2018 as against $ 1719.3, $ 1626, $ 2391.9 in year 2017, 2016 and 2015 respectively. It is

suggested by the figures that the value of equity decreased significantly in year 2018. Looking at

the figures of retained earnings, it indicates that value has increased to $ 780.6 in year 2018 as

The items of equity comprised of equity capital, reserves, retained earnings and reserved

shares. For year ending 2018 and 2017, issued capital is reported at $ 22277 million and $ 22268

million compared to $ 21937 and $ 21844 in year 2016 and 2015 respectively. There has been

consistent increase in value of issued capital. Value of retained earnings is recorded at $ 176 for

year 2018 compared to $ 1509, $ 874 and $ 2742 for year 2017, 2016 and 2015 respectively.

Value of retained earning has declined significantly initially and increased and decline further in

the current year. Reserves other hand stood at 344, 190, 166 and 226 for year 2018, 2017, 2016

and 2015 respectively. Value of reserves declined initially and then increased thereafter

indicating that the reserves account has enhanced due to increased profits.

Analysis of each items of equity of JB Hi-Fi:

The amount of contributed equity stood at $ 438.7 and $ 49.3 in year 2017 and 2016

compared to $ 565.21 in year 2015. It is indicated by the figure that there has been considerable

decline in value of contributed equity. Value of reserves is recorded at $ 33.2 and $ 27.1 in year

2017 and 2016 compared to $ 17.63 in year 2015 respectively indicating a consistent increase in

value. Now, looking at the figures of retained earnings, it can be seen that the amount is recorded

at $ 381.6 and $ 328.3 in year 2017 and 2016 respectively compared to $ 269.3 in year 2015. The

figure suggests that the value of retained earnings is increasing year on year.

Analysis of each items of equity of Met cash:

For Met cash, the amount of contributed and other equity is recorded at $ 600 in year

2018 as against $ 1719.3, $ 1626, $ 2391.9 in year 2017, 2016 and 2015 respectively. It is

suggested by the figures that the value of equity decreased significantly in year 2018. Looking at

the figures of retained earnings, it indicates that value has increased to $ 780.6 in year 2018 as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

against accumulated loss of $ 87.7 in year 2017, $ 184.7 and $ 765.9 in year 2017, 2016 and

2015 respectively. Amount of reserves for year 2018 stood at $ 0.7 compared to $ 3.0 in year

2017 and $ 4.1 in year 2016 and 2015 respectively (metcash.com 2018).

Comparative analysis of debt and equity position of chosen companies:

The total amount of liabilities of Woolworths limited for year ending 2018 and 2017 is

recorded at $ 12709 and $ 13167 compared to total value of equity that is recorded at $ 10849

and $ 9876. It is suggested by the figure that value of equity is less as against total amount of

debt.

For Wesfarmers limited, the total amount of liabilities is recorded at $ 14179 in year 2018

and 16174 in year 2017 respectively indicating that total amount owed by organization to other

has reduced. Looking at the figures of equity, it can be seen that equity has reduced from $

23941 in year 2017 to $ 22754 in year 2018 respectively (wesfarmers.com.au 2018).

For JB Hi-Fi, the total amount of liabilities or debt is recorded at $ 1598.9 and $ 587.6 in

year 2017 and 2016 compared to 551.5 in year 2015 respectively. It can be seen from the figures

that the total amount of liabilities has significantly increased in year 2017. Total amount of

equity on other hand stood at $ 853.5 in year 2017 compared to $ 404.7 in year 2016 and $

343.47 in year 2015 respectively (Jbhifi.com.au 2018). The figure suggests that total amount of

equity has increased considerably in year 2017.

The amount of total debt for Met Cash is recorded at $ 2330.4 and $ 2294.9 in year 2018

and 2017 compared to $ 2254.2 and $ 2313.3 in year 2016 and 2015 respectively. It can be seen

from there is not much fluctuation in the value of total debt for considerable number of years. On

against accumulated loss of $ 87.7 in year 2017, $ 184.7 and $ 765.9 in year 2017, 2016 and

2015 respectively. Amount of reserves for year 2018 stood at $ 0.7 compared to $ 3.0 in year

2017 and $ 4.1 in year 2016 and 2015 respectively (metcash.com 2018).

Comparative analysis of debt and equity position of chosen companies:

The total amount of liabilities of Woolworths limited for year ending 2018 and 2017 is

recorded at $ 12709 and $ 13167 compared to total value of equity that is recorded at $ 10849

and $ 9876. It is suggested by the figure that value of equity is less as against total amount of

debt.

For Wesfarmers limited, the total amount of liabilities is recorded at $ 14179 in year 2018

and 16174 in year 2017 respectively indicating that total amount owed by organization to other

has reduced. Looking at the figures of equity, it can be seen that equity has reduced from $

23941 in year 2017 to $ 22754 in year 2018 respectively (wesfarmers.com.au 2018).

For JB Hi-Fi, the total amount of liabilities or debt is recorded at $ 1598.9 and $ 587.6 in

year 2017 and 2016 compared to 551.5 in year 2015 respectively. It can be seen from the figures

that the total amount of liabilities has significantly increased in year 2017. Total amount of

equity on other hand stood at $ 853.5 in year 2017 compared to $ 404.7 in year 2016 and $

343.47 in year 2015 respectively (Jbhifi.com.au 2018). The figure suggests that total amount of

equity has increased considerably in year 2017.

The amount of total debt for Met Cash is recorded at $ 2330.4 and $ 2294.9 in year 2018

and 2017 compared to $ 2254.2 and $ 2313.3 in year 2016 and 2015 respectively. It can be seen

from there is not much fluctuation in the value of total debt for considerable number of years. On

11CORPORATE ACCOUNTING

other hand, the value of equity is recorded at $ 1388.6 and $ 1637.4 in year 2018 and 2017

compared to $ 1538.4 and $ 1275.2 in year 2016 and 2015 respectively.

From the figures of all the four companies, it can be seen that JB Hi-Fi has lower amount

of total debt followed by Woolworths compared to Wesfarmers and Met Cash. For the figures of

equities, it can be seen that the value of equity of Wesfarmers is more than all other companies.

Conclusion:

The report has helped in addressing the importance of corporate regulation in the

financial and accounting reporting process that has outline the fact that regulations provides the

users with several benefits in terms of standardization, information reliability and symmetry and

comparability. In addition to this, conducting research on the AASB have identified that the

standard takes several steps for setting the process of global accounting standard. From the

analysis of the annual report of all the four selected companies concerning the area of entity, it

has been found that Wesfarmers has highest value of total equity compared to other companies

and the lowest value of debt represented by JB Hi-Fi indicating a better financial leverage.

other hand, the value of equity is recorded at $ 1388.6 and $ 1637.4 in year 2018 and 2017

compared to $ 1538.4 and $ 1275.2 in year 2016 and 2015 respectively.

From the figures of all the four companies, it can be seen that JB Hi-Fi has lower amount

of total debt followed by Woolworths compared to Wesfarmers and Met Cash. For the figures of

equities, it can be seen that the value of equity of Wesfarmers is more than all other companies.

Conclusion:

The report has helped in addressing the importance of corporate regulation in the

financial and accounting reporting process that has outline the fact that regulations provides the

users with several benefits in terms of standardization, information reliability and symmetry and

comparability. In addition to this, conducting research on the AASB have identified that the

standard takes several steps for setting the process of global accounting standard. From the

analysis of the annual report of all the four selected companies concerning the area of entity, it

has been found that Wesfarmers has highest value of total equity compared to other companies

and the lowest value of debt represented by JB Hi-Fi indicating a better financial leverage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.