HA2032 Corporate Accounting: Takeover Decision Making & Consolidation

VerifiedAdded on 2023/03/31

|9

|2567

|129

Report

AI Summary

This report delves into the consolidation methods employed when JKY Ltd. aims to acquire FAB Ltd., focusing on the accounting treatments required. It elucidates the equity and consolidation methods of accounting, highlighting their principles and applications. The report addresses intra-company transactions, specifically inventory purchases, and the handling of unrealized profits, emphasizing the importance of their elimination for accurate financial reporting. Furthermore, it discusses the disclosure requirements for non-controlling interests (NCI) in consolidated financial statements and the adjustments needed to ensure accurate representation, including the elimination of intercompany investments and equity portions. The report uses examples to illustrate key concepts such as unrealized profit calculation and the necessary journal entries for consolidation. Desklib provides access to this and many other solved assignments.

Running head: Corporate Accounting

Corporate Accounting

Name of the Student

Name of the University

Author Note

Corporate Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Corporate Accounting

Executive Summary

The report show about the consolidated statement and show about the JKY Ltd

which want to take over the FAB Ltd so it show the method which can adopted for

the consolidation. It even show about the intra transaction and how the unrealised

profit is to be deal with and it even show about the disclosure which is been required

in regards of the non-controlling interest.

Corporate Accounting

Executive Summary

The report show about the consolidated statement and show about the JKY Ltd

which want to take over the FAB Ltd so it show the method which can adopted for

the consolidation. It even show about the intra transaction and how the unrealised

profit is to be deal with and it even show about the disclosure which is been required

in regards of the non-controlling interest.

2

Corporate Accounting

Table of Contents

Introduction...................................................................................................................3

Part A............................................................................................................................3

Part B............................................................................................................................5

Part C............................................................................................................................6

Conclusion....................................................................................................................7

Reference.....................................................................................................................8

Corporate Accounting

Table of Contents

Introduction...................................................................................................................3

Part A............................................................................................................................3

Part B............................................................................................................................5

Part C............................................................................................................................6

Conclusion....................................................................................................................7

Reference.....................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Corporate Accounting

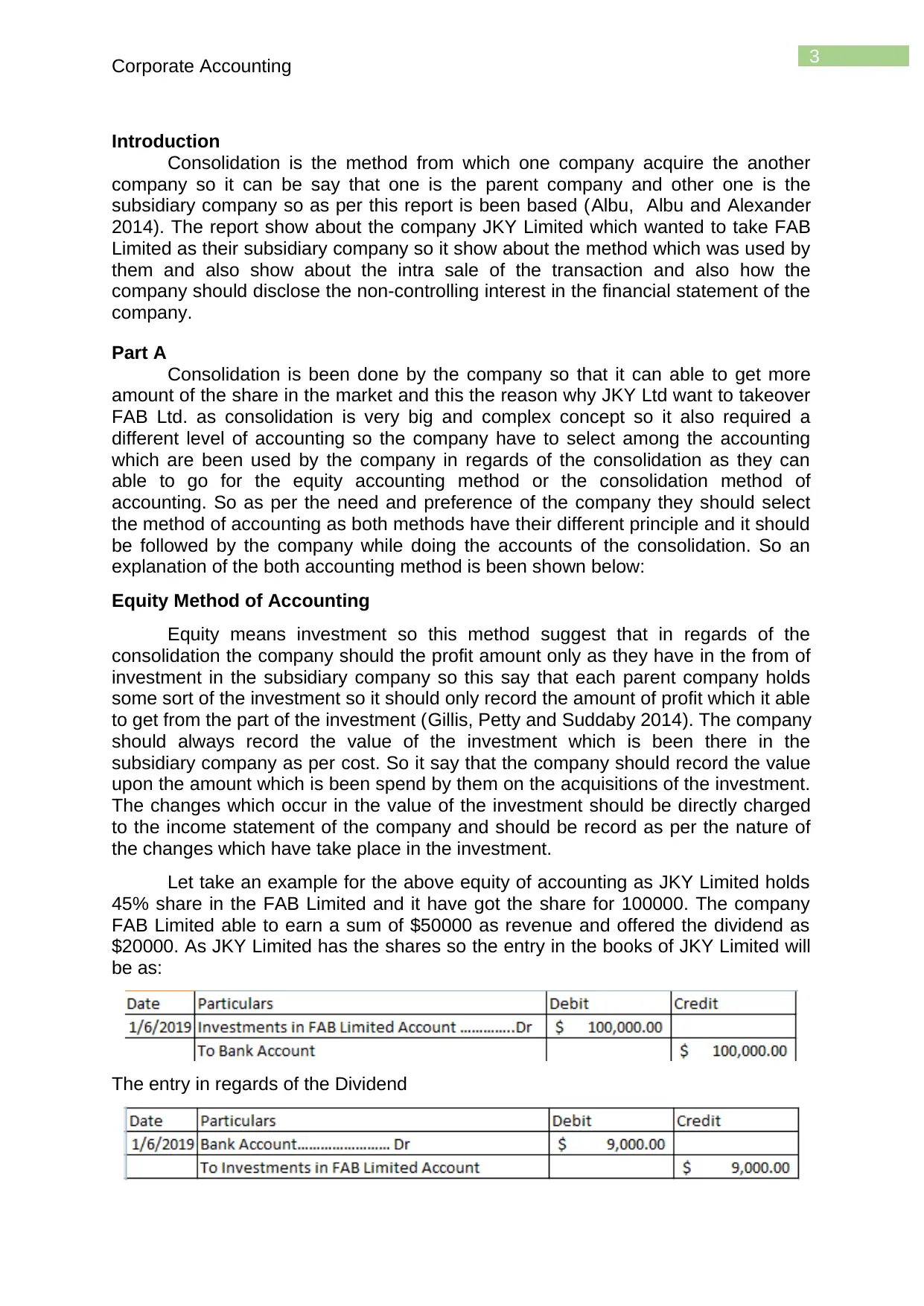

Introduction

Consolidation is the method from which one company acquire the another

company so it can be say that one is the parent company and other one is the

subsidiary company so as per this report is been based (Albu, Albu and Alexander

2014). The report show about the company JKY Limited which wanted to take FAB

Limited as their subsidiary company so it show about the method which was used by

them and also show about the intra sale of the transaction and also how the

company should disclose the non-controlling interest in the financial statement of the

company.

Part A

Consolidation is been done by the company so that it can able to get more

amount of the share in the market and this the reason why JKY Ltd want to takeover

FAB Ltd. as consolidation is very big and complex concept so it also required a

different level of accounting so the company have to select among the accounting

which are been used by the company in regards of the consolidation as they can

able to go for the equity accounting method or the consolidation method of

accounting. So as per the need and preference of the company they should select

the method of accounting as both methods have their different principle and it should

be followed by the company while doing the accounts of the consolidation. So an

explanation of the both accounting method is been shown below:

Equity Method of Accounting

Equity means investment so this method suggest that in regards of the

consolidation the company should the profit amount only as they have in the from of

investment in the subsidiary company so this say that each parent company holds

some sort of the investment so it should only record the amount of profit which it able

to get from the part of the investment (Gillis, Petty and Suddaby 2014). The company

should always record the value of the investment which is been there in the

subsidiary company as per cost. So it say that the company should record the value

upon the amount which is been spend by them on the acquisitions of the investment.

The changes which occur in the value of the investment should be directly charged

to the income statement of the company and should be record as per the nature of

the changes which have take place in the investment.

Let take an example for the above equity of accounting as JKY Limited holds

45% share in the FAB Limited and it have got the share for 100000. The company

FAB Limited able to earn a sum of $50000 as revenue and offered the dividend as

$20000. As JKY Limited has the shares so the entry in the books of JKY Limited will

be as:

The entry in regards of the Dividend

Corporate Accounting

Introduction

Consolidation is the method from which one company acquire the another

company so it can be say that one is the parent company and other one is the

subsidiary company so as per this report is been based (Albu, Albu and Alexander

2014). The report show about the company JKY Limited which wanted to take FAB

Limited as their subsidiary company so it show about the method which was used by

them and also show about the intra sale of the transaction and also how the

company should disclose the non-controlling interest in the financial statement of the

company.

Part A

Consolidation is been done by the company so that it can able to get more

amount of the share in the market and this the reason why JKY Ltd want to takeover

FAB Ltd. as consolidation is very big and complex concept so it also required a

different level of accounting so the company have to select among the accounting

which are been used by the company in regards of the consolidation as they can

able to go for the equity accounting method or the consolidation method of

accounting. So as per the need and preference of the company they should select

the method of accounting as both methods have their different principle and it should

be followed by the company while doing the accounts of the consolidation. So an

explanation of the both accounting method is been shown below:

Equity Method of Accounting

Equity means investment so this method suggest that in regards of the

consolidation the company should the profit amount only as they have in the from of

investment in the subsidiary company so this say that each parent company holds

some sort of the investment so it should only record the amount of profit which it able

to get from the part of the investment (Gillis, Petty and Suddaby 2014). The company

should always record the value of the investment which is been there in the

subsidiary company as per cost. So it say that the company should record the value

upon the amount which is been spend by them on the acquisitions of the investment.

The changes which occur in the value of the investment should be directly charged

to the income statement of the company and should be record as per the nature of

the changes which have take place in the investment.

Let take an example for the above equity of accounting as JKY Limited holds

45% share in the FAB Limited and it have got the share for 100000. The company

FAB Limited able to earn a sum of $50000 as revenue and offered the dividend as

$20000. As JKY Limited has the shares so the entry in the books of JKY Limited will

be as:

The entry in regards of the Dividend

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Corporate Accounting

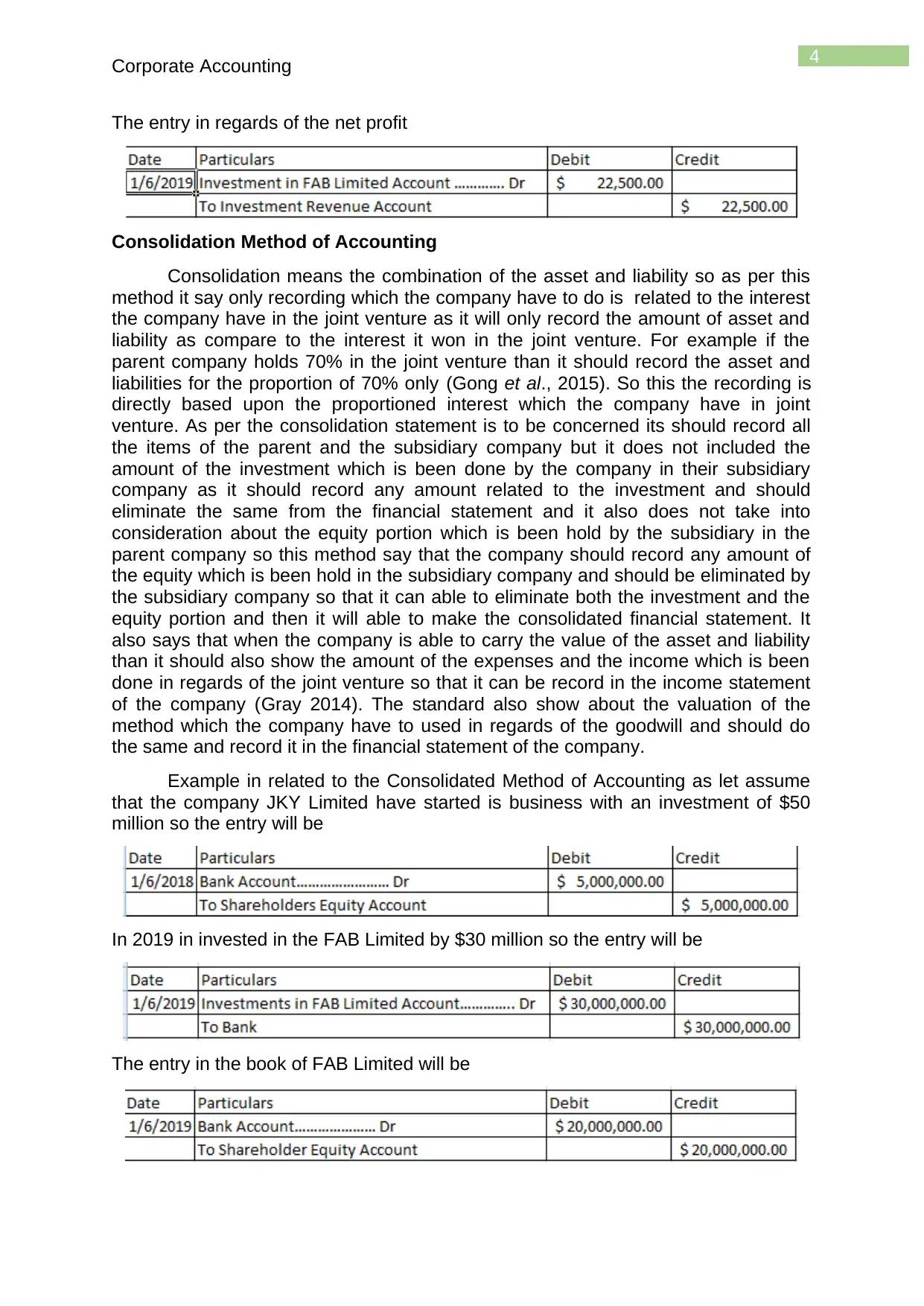

The entry in regards of the net profit

Consolidation Method of Accounting

Consolidation means the combination of the asset and liability so as per this

method it say only recording which the company have to do is related to the interest

the company have in the joint venture as it will only record the amount of asset and

liability as compare to the interest it won in the joint venture. For example if the

parent company holds 70% in the joint venture than it should record the asset and

liabilities for the proportion of 70% only (Gong et al., 2015). So this the recording is

directly based upon the proportioned interest which the company have in joint

venture. As per the consolidation statement is to be concerned its should record all

the items of the parent and the subsidiary company but it does not included the

amount of the investment which is been done by the company in their subsidiary

company as it should record any amount related to the investment and should

eliminate the same from the financial statement and it also does not take into

consideration about the equity portion which is been hold by the subsidiary in the

parent company so this method say that the company should record any amount of

the equity which is been hold in the subsidiary company and should be eliminated by

the subsidiary company so that it can able to eliminate both the investment and the

equity portion and then it will able to make the consolidated financial statement. It

also says that when the company is able to carry the value of the asset and liability

than it should also show the amount of the expenses and the income which is been

done in regards of the joint venture so that it can be record in the income statement

of the company (Gray 2014). The standard also show about the valuation of the

method which the company have to used in regards of the goodwill and should do

the same and record it in the financial statement of the company.

Example in related to the Consolidated Method of Accounting as let assume

that the company JKY Limited have started is business with an investment of $50

million so the entry will be

In 2019 in invested in the FAB Limited by $30 million so the entry will be

The entry in the book of FAB Limited will be

Corporate Accounting

The entry in regards of the net profit

Consolidation Method of Accounting

Consolidation means the combination of the asset and liability so as per this

method it say only recording which the company have to do is related to the interest

the company have in the joint venture as it will only record the amount of asset and

liability as compare to the interest it won in the joint venture. For example if the

parent company holds 70% in the joint venture than it should record the asset and

liabilities for the proportion of 70% only (Gong et al., 2015). So this the recording is

directly based upon the proportioned interest which the company have in joint

venture. As per the consolidation statement is to be concerned its should record all

the items of the parent and the subsidiary company but it does not included the

amount of the investment which is been done by the company in their subsidiary

company as it should record any amount related to the investment and should

eliminate the same from the financial statement and it also does not take into

consideration about the equity portion which is been hold by the subsidiary in the

parent company so this method say that the company should record any amount of

the equity which is been hold in the subsidiary company and should be eliminated by

the subsidiary company so that it can able to eliminate both the investment and the

equity portion and then it will able to make the consolidated financial statement. It

also says that when the company is able to carry the value of the asset and liability

than it should also show the amount of the expenses and the income which is been

done in regards of the joint venture so that it can be record in the income statement

of the company (Gray 2014). The standard also show about the valuation of the

method which the company have to used in regards of the goodwill and should do

the same and record it in the financial statement of the company.

Example in related to the Consolidated Method of Accounting as let assume

that the company JKY Limited have started is business with an investment of $50

million so the entry will be

In 2019 in invested in the FAB Limited by $30 million so the entry will be

The entry in the book of FAB Limited will be

5

Corporate Accounting

Part B

Company can only be able to make a proper consolidation statement only

when it able to remove all the details of the transaction from the company as there

should be no entry in the account related to the parent company and the subsidiary

company as there is some entry it will directly affect the same and company will not

able to make the consolidation statement (Hoyle, Schaefer and Doupnik 2015). So it

is the primary duty of the organization to remove all the transaction as is should not

show any portion of the equity which is been hold by the company in their subsidiary

company. There can be some sort if intra transaction so it should also be removed

by the company as the intra transaction are the type of the transaction which happen

between the two company so the company should remove all these type of

transaction and also should not take part of any transaction in future with the

subsidiary company. So to remove all the transaction company have to reverse the

entry which it have passed in regards of the same so that it will able to make all the

entry reversed and there will be no amount of the intra transactions in the company

balance sheet.

JKY Limited have enter into the agreement of purchase of the inventory from

the subsidiary company so this show that it is an intra transaction. Subsidiary

company must have sale the inventory by adding some sort of margin to JKY Ltd

and recorded the same in their balance sheet. It can be seen that the company JKY

Limited have not able to record the inventory as their revenue as they were unable to

sale the same in the current year so it can be said that the portion of the inventory

which lies in the financial statement of JKY Limited have cost + margin so as the

company should not record the margin which can be termed as unrealized profit so it

should not be recorded by the company as it should removed the same from the

financial statement of the company (Hsu, Jung and Pourjalali 2015). As per the

standard on accounting it suggest that the company should record the same as non-

current and it should be eliminated from the inventory value so it can be said that the

company should able to remove the unrealized profit which is been there in the

inventory of the company.

Group profit of the company will also be affected as it includes all the profit

which the company earns from the subsidiary or the parent company. As the

subsidiary company have sold the goods to the parent company so the part of the

unrealized profit is still there in the profit of the subsidiary company and as the profit

is been carried forward in the group so as a result it also increase the group profit of

the company so as per the standard it should removed the part of unrealized profit

which is there in the group profit and can only be done with the help of the

adjustment entry so an example which can help to know what entry the company

have to do in regards of the removal of the unrealized profit (Aasb.gov.au 2019).

For example the company have purchased the goods for $10000 and the

subsidiary company have a margin of 10% so the amount of the unrealized profit will

be (10/110)* 10000 = 909. So the amount of unrealized profit wills $909 so it should

be removed and the entry will be

Consolidated Profit Account Dr 909

To Consolidated Inventory Account 909

So this will removed all the unrealized profit which is there in the group account and

will show a fair amount of profit which is been earned by them.

Corporate Accounting

Part B

Company can only be able to make a proper consolidation statement only

when it able to remove all the details of the transaction from the company as there

should be no entry in the account related to the parent company and the subsidiary

company as there is some entry it will directly affect the same and company will not

able to make the consolidation statement (Hoyle, Schaefer and Doupnik 2015). So it

is the primary duty of the organization to remove all the transaction as is should not

show any portion of the equity which is been hold by the company in their subsidiary

company. There can be some sort if intra transaction so it should also be removed

by the company as the intra transaction are the type of the transaction which happen

between the two company so the company should remove all these type of

transaction and also should not take part of any transaction in future with the

subsidiary company. So to remove all the transaction company have to reverse the

entry which it have passed in regards of the same so that it will able to make all the

entry reversed and there will be no amount of the intra transactions in the company

balance sheet.

JKY Limited have enter into the agreement of purchase of the inventory from

the subsidiary company so this show that it is an intra transaction. Subsidiary

company must have sale the inventory by adding some sort of margin to JKY Ltd

and recorded the same in their balance sheet. It can be seen that the company JKY

Limited have not able to record the inventory as their revenue as they were unable to

sale the same in the current year so it can be said that the portion of the inventory

which lies in the financial statement of JKY Limited have cost + margin so as the

company should not record the margin which can be termed as unrealized profit so it

should not be recorded by the company as it should removed the same from the

financial statement of the company (Hsu, Jung and Pourjalali 2015). As per the

standard on accounting it suggest that the company should record the same as non-

current and it should be eliminated from the inventory value so it can be said that the

company should able to remove the unrealized profit which is been there in the

inventory of the company.

Group profit of the company will also be affected as it includes all the profit

which the company earns from the subsidiary or the parent company. As the

subsidiary company have sold the goods to the parent company so the part of the

unrealized profit is still there in the profit of the subsidiary company and as the profit

is been carried forward in the group so as a result it also increase the group profit of

the company so as per the standard it should removed the part of unrealized profit

which is there in the group profit and can only be done with the help of the

adjustment entry so an example which can help to know what entry the company

have to do in regards of the removal of the unrealized profit (Aasb.gov.au 2019).

For example the company have purchased the goods for $10000 and the

subsidiary company have a margin of 10% so the amount of the unrealized profit will

be (10/110)* 10000 = 909. So the amount of unrealized profit wills $909 so it should

be removed and the entry will be

Consolidated Profit Account Dr 909

To Consolidated Inventory Account 909

So this will removed all the unrealized profit which is there in the group account and

will show a fair amount of profit which is been earned by them.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Corporate Accounting

Part C

Effects of NCI disclosure requirement in regards to the separate item in the

process of consolidation

To make a better presentation the company have to separately present the

non-controlling which it had in the equity of the parent company. So it should

disclose all the matter properly so that the company can able to know how to deal

with them in the financial statement. As non-controlling interest is been made so this

asset help the user to know how it is been implemented and also this standard help

to develop more easy accounting for the purpose (Aasb.gov.au 2019). The

consolidated statement is a bit different with regards of the non-controlling interest so

it should all the detail of the equity and non-controlling asset properly in the

consolidated statement. The standard help the company to do the accounting in a

more simple way so that the financial user can able to collect the information

properly and also able to analysis the same and able to take proper decision in

regards of the same.

Each parent company have some kind of holding in the financial statement of

the subsidiary company so that if the company is losing the interest upon the

business of the subsidiary so it should report it properly in the financial statement as

it is the most important p[art and each person should able to know the reason for

such happening of the event. It should also able to know the amount of non-

controlling interest which should be record by the company in the financial

statement.

Changes in order to ensure the accurate representation of the consolidated

financial statement

As per the consolidated statement is there company should record all the

adjusted amount of the asset and liabilities of both the company. It should not record

any amount which is in related to the investments which are been done by the

company in their subsidiary company and also it should not record the portion of the

equity which the company holds in the parent company (Aasb.gov.au 2019). If the

company have any kind of the loss so that should be reported and should be

recorded in the consolidation statement. The company should able to follow all the

regulation and the norms which are there in the standard related to the consolidation.

It should do proper estimation of the policy while preparing the consolidated financial

statement of the company. All the items so the both company should be there in the

consolidated statement and should also show the valuation of the goodwill.

The company can do the adjustment of the dividend in regards of the

preference share so that it can able to clear all its obligation before making the

consolidated statement.

Effects of the changes upon the disclosure in the annual report

The company should give all the necessary disclosure of the method and the

assumption which are been used by the company in regards of the consolidation of

the financial statement (Aasb.gov.au 2019). As it should record the amount of the

investment in the cost which is been done by the company in the joint venture. It

should show all the adjustment entry which they have passed to remove the intra

sale from the company transaction.

Corporate Accounting

Part C

Effects of NCI disclosure requirement in regards to the separate item in the

process of consolidation

To make a better presentation the company have to separately present the

non-controlling which it had in the equity of the parent company. So it should

disclose all the matter properly so that the company can able to know how to deal

with them in the financial statement. As non-controlling interest is been made so this

asset help the user to know how it is been implemented and also this standard help

to develop more easy accounting for the purpose (Aasb.gov.au 2019). The

consolidated statement is a bit different with regards of the non-controlling interest so

it should all the detail of the equity and non-controlling asset properly in the

consolidated statement. The standard help the company to do the accounting in a

more simple way so that the financial user can able to collect the information

properly and also able to analysis the same and able to take proper decision in

regards of the same.

Each parent company have some kind of holding in the financial statement of

the subsidiary company so that if the company is losing the interest upon the

business of the subsidiary so it should report it properly in the financial statement as

it is the most important p[art and each person should able to know the reason for

such happening of the event. It should also able to know the amount of non-

controlling interest which should be record by the company in the financial

statement.

Changes in order to ensure the accurate representation of the consolidated

financial statement

As per the consolidated statement is there company should record all the

adjusted amount of the asset and liabilities of both the company. It should not record

any amount which is in related to the investments which are been done by the

company in their subsidiary company and also it should not record the portion of the

equity which the company holds in the parent company (Aasb.gov.au 2019). If the

company have any kind of the loss so that should be reported and should be

recorded in the consolidation statement. The company should able to follow all the

regulation and the norms which are there in the standard related to the consolidation.

It should do proper estimation of the policy while preparing the consolidated financial

statement of the company. All the items so the both company should be there in the

consolidated statement and should also show the valuation of the goodwill.

The company can do the adjustment of the dividend in regards of the

preference share so that it can able to clear all its obligation before making the

consolidated statement.

Effects of the changes upon the disclosure in the annual report

The company should give all the necessary disclosure of the method and the

assumption which are been used by the company in regards of the consolidation of

the financial statement (Aasb.gov.au 2019). As it should record the amount of the

investment in the cost which is been done by the company in the joint venture. It

should show all the adjustment entry which they have passed to remove the intra

sale from the company transaction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Corporate Accounting

The both company should have same date of reporting the financial statement

so if the date is been different than the company should give proper explanation

about why the date are different and the reason should be clearly mention in the

financial statement of the company. It is necessary for the company to hold at least

50% upon the subsidiary company so if the company is not able to hold the

prescribed amount that it should properly disclose it in the financial statement so

that the user can able to know that it any happen the company may lose its control

over the subsidiary company. So all these matters should be properly disclosed by

the company in their notes on account.

Conclusion

On a conclusive note, the above discussion concludes as the how the consolidation

is done between the two company and what are the methods which can be used by

the company in regards of the consolidation as it show about the equity and

consolidation method of accounting. It even shows the details of the accounting in

regards of the intra sale and how the company can able to remove the unrealized

profit from the same. It even shows about the disclosure which should be made by

the company in regards of the non-controlling interest.

Corporate Accounting

The both company should have same date of reporting the financial statement

so if the date is been different than the company should give proper explanation

about why the date are different and the reason should be clearly mention in the

financial statement of the company. It is necessary for the company to hold at least

50% upon the subsidiary company so if the company is not able to hold the

prescribed amount that it should properly disclose it in the financial statement so

that the user can able to know that it any happen the company may lose its control

over the subsidiary company. So all these matters should be properly disclosed by

the company in their notes on account.

Conclusion

On a conclusive note, the above discussion concludes as the how the consolidation

is done between the two company and what are the methods which can be used by

the company in regards of the consolidation as it show about the equity and

consolidation method of accounting. It even shows the details of the accounting in

regards of the intra sale and how the company can able to remove the unrealized

profit from the same. It even shows about the disclosure which should be made by

the company in regards of the non-controlling interest.

8

Corporate Accounting

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 31

May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

31 May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 31

May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 31 May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed

31 May2019].

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards

meet the local context—Insights from an emerging economy. Critical Perspectives

on Accounting, 25(6), pp.489-510.

Gillis, P., Petty, R. and Suddaby, R., 2014. The transnational regulation of

accounting: insights, gaps and an agenda for future research. Accounting, Auditing &

Accountability Journal, 27(6), pp.894-902.

Gong, Q., Li, O.Z., Lin, Y. and Wu, L., 2015. On the benefits of audit market

consolidation: Evidence from merged audit firms. The Accounting Review, 91(2),

pp.463-488.

Gray, S.J. ed., 2014. International accounting and transnational decisions.

Butterworth-Heinemann.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Hsu, A.W.H., Jung, B. and Pourjalali, H., 2015. Does international accounting

standard no. 27 improve investment efficiency?. Journal of Accounting, Auditing &

Finance, 30(4), pp.484-508.

Corporate Accounting

Reference

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 31

May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

31 May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 31

May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 31 May2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed

31 May2019].

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards

meet the local context—Insights from an emerging economy. Critical Perspectives

on Accounting, 25(6), pp.489-510.

Gillis, P., Petty, R. and Suddaby, R., 2014. The transnational regulation of

accounting: insights, gaps and an agenda for future research. Accounting, Auditing &

Accountability Journal, 27(6), pp.894-902.

Gong, Q., Li, O.Z., Lin, Y. and Wu, L., 2015. On the benefits of audit market

consolidation: Evidence from merged audit firms. The Accounting Review, 91(2),

pp.463-488.

Gray, S.J. ed., 2014. International accounting and transnational decisions.

Butterworth-Heinemann.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Hsu, A.W.H., Jung, B. and Pourjalali, H., 2015. Does international accounting

standard no. 27 improve investment efficiency?. Journal of Accounting, Auditing &

Finance, 30(4), pp.484-508.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.