HA2042 Accounting Info Systems: Adam & Co Case Study Analysis

VerifiedAdded on 2022/10/31

|11

|2806

|424

Case Study

AI Summary

This report evaluates the accounting procedures of Adam & Co., focusing on the expenditure cycle, including purchasing, cash disbursement, and payroll systems. It details the activities of purchasing and receiving clerks, along with the steps involved in each process, illustrated by flowcharts. The report identifies weaknesses in internal controls, such as the purchasing clerk's heavy workload, manual preparation of receiving reports, and manual payroll processing, highlighting the potential for human error and fraud. Risks associated with the manual accounting system, like customer loss due to lengthy processes, are also discussed. The analysis aims to inform management about system vulnerabilities and potential improvements. Desklib offers a range of solved assignments and past papers to support student learning.

Running head: ACCOUNTING INFORMATION SYSTEMS

Accounting Information Systems

Name of the Student

Name of the University

Author’s note

Accounting Information Systems

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING INFORMATION SYSTEMS

Executive Summary

The report tends to discuss on the accounting procedures of the company, Adam

and Co. These processes are considered to be a part of the expenditure cycle of the

company. The activities of the purchasing clerk of the purchase department is

elaborated in the light of the entire system. The two other processes of the company

are also explained and discussed with the help of a flowchart. These two processes

are the process of cash disbursement and the payroll process. The activities of the

clerks of these two processes are also explained. At the last section of the report, the

disadvantages of these three processes are noted down along with their probable

risks. The different weaknesses of the system are also elaborated as required.

Executive Summary

The report tends to discuss on the accounting procedures of the company, Adam

and Co. These processes are considered to be a part of the expenditure cycle of the

company. The activities of the purchasing clerk of the purchase department is

elaborated in the light of the entire system. The two other processes of the company

are also explained and discussed with the help of a flowchart. These two processes

are the process of cash disbursement and the payroll process. The activities of the

clerks of these two processes are also explained. At the last section of the report, the

disadvantages of these three processes are noted down along with their probable

risks. The different weaknesses of the system are also elaborated as required.

2ACCOUNTING INFORMATION SYSTEMS

Table of Contents

Introduction...................................................................................................................2

Discussion....................................................................................................................2

Purchase system of the company................................................................................2

Cash disbursement system of the company................................................................3

Payroll system of the company.....................................................................................3

Weakness detected in each system.............................................................................4

Risks detected in each system.....................................................................................4

Conclusion....................................................................................................................5

References...................................................................................................................6

Table of Contents

Introduction...................................................................................................................2

Discussion....................................................................................................................2

Purchase system of the company................................................................................2

Cash disbursement system of the company................................................................3

Payroll system of the company.....................................................................................3

Weakness detected in each system.............................................................................4

Risks detected in each system.....................................................................................4

Conclusion....................................................................................................................5

References...................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING INFORMATION SYSTEMS

Introduction

The primary objective of the report is to evaluate the three different kinds of

processes that are prevalent in the accounting system of the company. The

company that has been focussed for the construction of this report is Adam & Co. As

it has been seen that the company is engaged in the business of supplying important

raw materials of the different industries, the accounting procedure of the company is

studied thoroughly in details. The expenditure cycle of the company is very

prominent. The components of the expenditure cycle are the system required for

making purchases, the system for cash disbursements and lastly the system for

making the payrolls. The different weaknesses of the internal controls of the

company are pointed out in order to bring it to the notice of the management. The

different risks that are possessed in carrying out such an internal control are also

indicated and explained.

Discussion

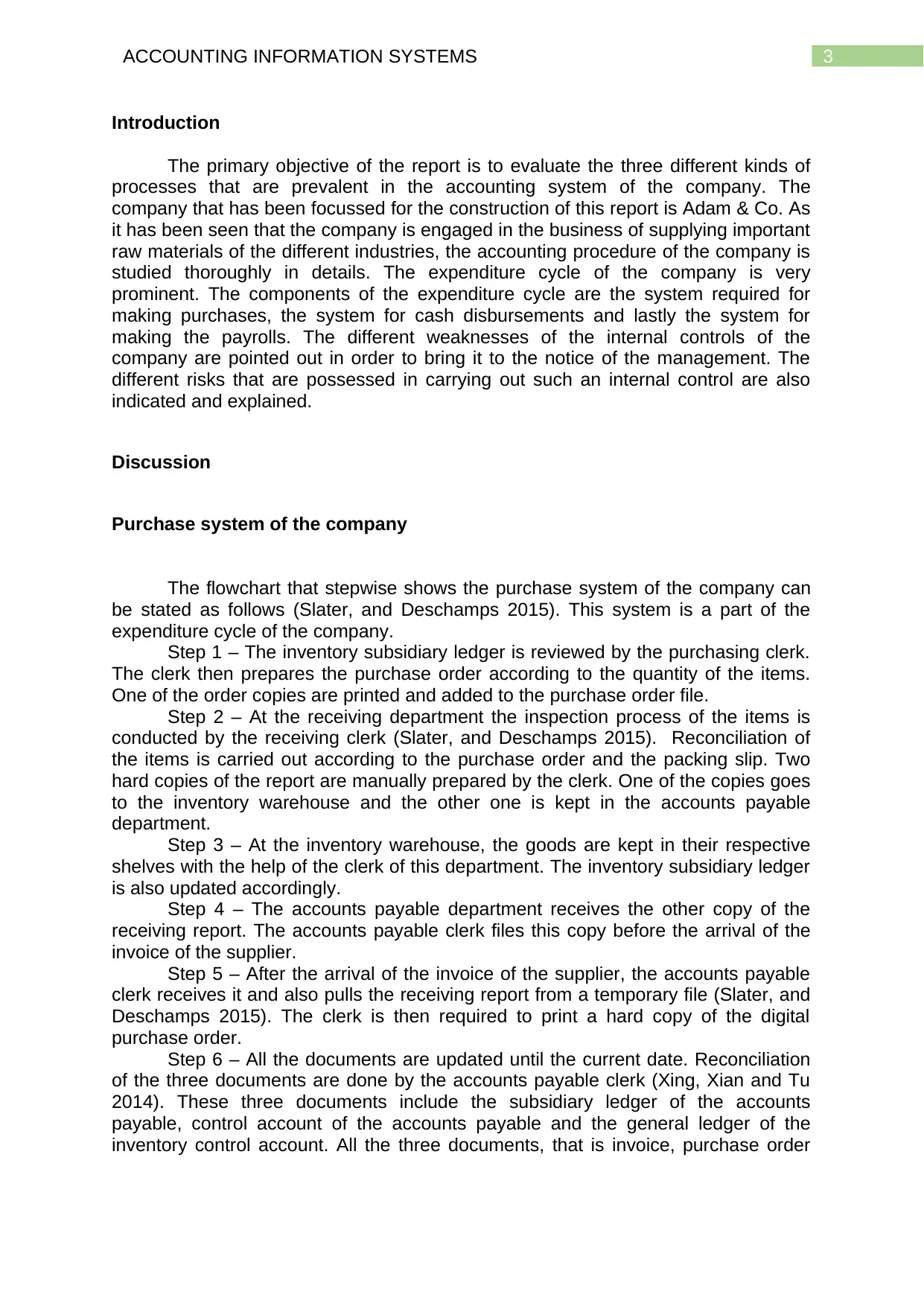

Purchase system of the company

The flowchart that stepwise shows the purchase system of the company can

be stated as follows (Slater, and Deschamps 2015). This system is a part of the

expenditure cycle of the company.

Step 1 – The inventory subsidiary ledger is reviewed by the purchasing clerk.

The clerk then prepares the purchase order according to the quantity of the items.

One of the order copies are printed and added to the purchase order file.

Step 2 – At the receiving department the inspection process of the items is

conducted by the receiving clerk (Slater, and Deschamps 2015). Reconciliation of

the items is carried out according to the purchase order and the packing slip. Two

hard copies of the report are manually prepared by the clerk. One of the copies goes

to the inventory warehouse and the other one is kept in the accounts payable

department.

Step 3 – At the inventory warehouse, the goods are kept in their respective

shelves with the help of the clerk of this department. The inventory subsidiary ledger

is also updated accordingly.

Step 4 – The accounts payable department receives the other copy of the

receiving report. The accounts payable clerk files this copy before the arrival of the

invoice of the supplier.

Step 5 – After the arrival of the invoice of the supplier, the accounts payable

clerk receives it and also pulls the receiving report from a temporary file (Slater, and

Deschamps 2015). The clerk is then required to print a hard copy of the digital

purchase order.

Step 6 – All the documents are updated until the current date. Reconciliation

of the three documents are done by the accounts payable clerk (Xing, Xian and Tu

2014). These three documents include the subsidiary ledger of the accounts

payable, control account of the accounts payable and the general ledger of the

inventory control account. All the three documents, that is invoice, purchase order

Introduction

The primary objective of the report is to evaluate the three different kinds of

processes that are prevalent in the accounting system of the company. The

company that has been focussed for the construction of this report is Adam & Co. As

it has been seen that the company is engaged in the business of supplying important

raw materials of the different industries, the accounting procedure of the company is

studied thoroughly in details. The expenditure cycle of the company is very

prominent. The components of the expenditure cycle are the system required for

making purchases, the system for cash disbursements and lastly the system for

making the payrolls. The different weaknesses of the internal controls of the

company are pointed out in order to bring it to the notice of the management. The

different risks that are possessed in carrying out such an internal control are also

indicated and explained.

Discussion

Purchase system of the company

The flowchart that stepwise shows the purchase system of the company can

be stated as follows (Slater, and Deschamps 2015). This system is a part of the

expenditure cycle of the company.

Step 1 – The inventory subsidiary ledger is reviewed by the purchasing clerk.

The clerk then prepares the purchase order according to the quantity of the items.

One of the order copies are printed and added to the purchase order file.

Step 2 – At the receiving department the inspection process of the items is

conducted by the receiving clerk (Slater, and Deschamps 2015). Reconciliation of

the items is carried out according to the purchase order and the packing slip. Two

hard copies of the report are manually prepared by the clerk. One of the copies goes

to the inventory warehouse and the other one is kept in the accounts payable

department.

Step 3 – At the inventory warehouse, the goods are kept in their respective

shelves with the help of the clerk of this department. The inventory subsidiary ledger

is also updated accordingly.

Step 4 – The accounts payable department receives the other copy of the

receiving report. The accounts payable clerk files this copy before the arrival of the

invoice of the supplier.

Step 5 – After the arrival of the invoice of the supplier, the accounts payable

clerk receives it and also pulls the receiving report from a temporary file (Slater, and

Deschamps 2015). The clerk is then required to print a hard copy of the digital

purchase order.

Step 6 – All the documents are updated until the current date. Reconciliation

of the three documents are done by the accounts payable clerk (Xing, Xian and Tu

2014). These three documents include the subsidiary ledger of the accounts

payable, control account of the accounts payable and the general ledger of the

inventory control account. All the three documents, that is invoice, purchase order

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING INFORMATION SYSTEMS

copy and the report receipt are sent to the cash disbursement system for further

processes.

The diagrammatic representation is shown below.

Review of inventory subsidiary

ledger by purchasing clerk

Inspection and reconciliation of

items by receiving clerk

Goods are shelved in their

respective warehouses

Receipt of the receiving report by

the accounts payable department

Receipt of the invoice by the

accounts payable clerk

Documents are updated and sent

to the cash disbursement

department

copy and the report receipt are sent to the cash disbursement system for further

processes.

The diagrammatic representation is shown below.

Review of inventory subsidiary

ledger by purchasing clerk

Inspection and reconciliation of

items by receiving clerk

Goods are shelved in their

respective warehouses

Receipt of the receiving report by

the accounts payable department

Receipt of the invoice by the

accounts payable clerk

Documents are updated and sent

to the cash disbursement

department

5ACCOUNTING INFORMATION SYSTEMS

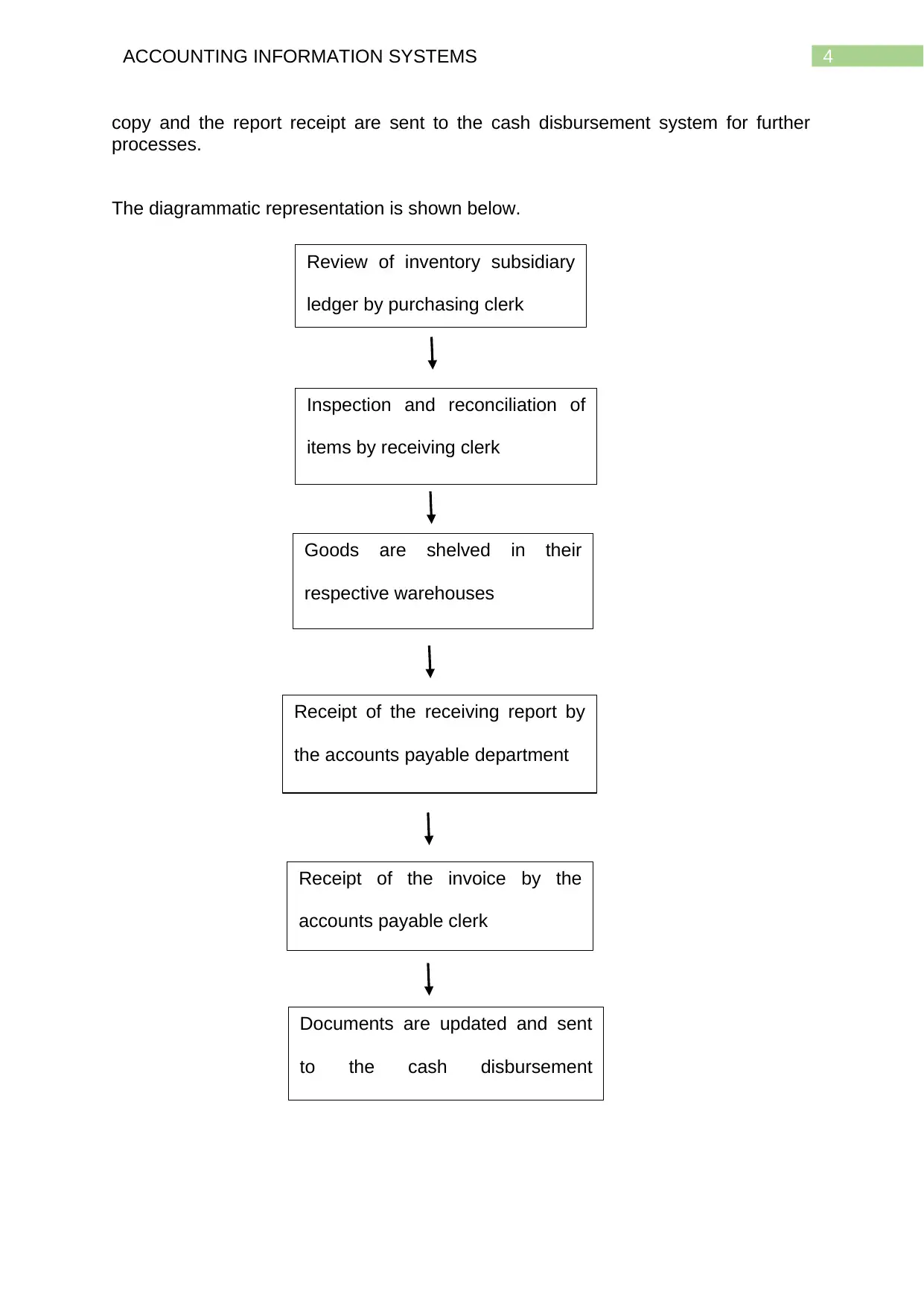

Cash disbursement system of the company

The flowchart showing the entire system of cash disbursement can be

explained in the following manner.

Step 1 – The three documents, that is, the invoice, order copy of the purchase

department, the report of receipt and the cheque copy, all are transferred from the

purchase department to the cash disbursement department (Xing, Xian and Tu

2014).

Step 2 – The cash disbursement department files all these documents and all

of them are sorted according to the due date of their payments. On the day of their

payments, a cheque of the amount in the invoice is prepared by the clerk.

Step 3 – The treasurer takes the responsibility of signing the final cheque that

should be paid to the vendor and then the cheque is sent to the vendor through

treasurer (Morgan 2017).

Step 4 – After the above process is completed, the clerk of the cash

disbursement department updates all the three important documents. These

documents are the register of the payment cheque, the subsidiary ledger of the

accounts payable department and the control account of the accounts payable

department (Jing 2015). All these updates are done through the computer terminal

present at the cash disbursement department.

Step 5 – The next step is performed by the receiving clerk. The receiving clerk

files the invoice copy, the report of the receiving department, the order copy

prepared by the purchase department and the copy of the cheque. All these

functions are carried out in the cash disbursement department. This is the final step

that marks the end of the process of the cash disbursement system.

The diagrammatic representation is shown below.

A cheque of the amount in the invoice is

prepared by the clerk.

The signed cheque finally gets transferred

to the vendor through the treasurer.

Transfer of the documents from the

purchase department to the cash

disbursement department.

Cash disbursement system of the company

The flowchart showing the entire system of cash disbursement can be

explained in the following manner.

Step 1 – The three documents, that is, the invoice, order copy of the purchase

department, the report of receipt and the cheque copy, all are transferred from the

purchase department to the cash disbursement department (Xing, Xian and Tu

2014).

Step 2 – The cash disbursement department files all these documents and all

of them are sorted according to the due date of their payments. On the day of their

payments, a cheque of the amount in the invoice is prepared by the clerk.

Step 3 – The treasurer takes the responsibility of signing the final cheque that

should be paid to the vendor and then the cheque is sent to the vendor through

treasurer (Morgan 2017).

Step 4 – After the above process is completed, the clerk of the cash

disbursement department updates all the three important documents. These

documents are the register of the payment cheque, the subsidiary ledger of the

accounts payable department and the control account of the accounts payable

department (Jing 2015). All these updates are done through the computer terminal

present at the cash disbursement department.

Step 5 – The next step is performed by the receiving clerk. The receiving clerk

files the invoice copy, the report of the receiving department, the order copy

prepared by the purchase department and the copy of the cheque. All these

functions are carried out in the cash disbursement department. This is the final step

that marks the end of the process of the cash disbursement system.

The diagrammatic representation is shown below.

A cheque of the amount in the invoice is

prepared by the clerk.

The signed cheque finally gets transferred

to the vendor through the treasurer.

Transfer of the documents from the

purchase department to the cash

disbursement department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING INFORMATION SYSTEMS

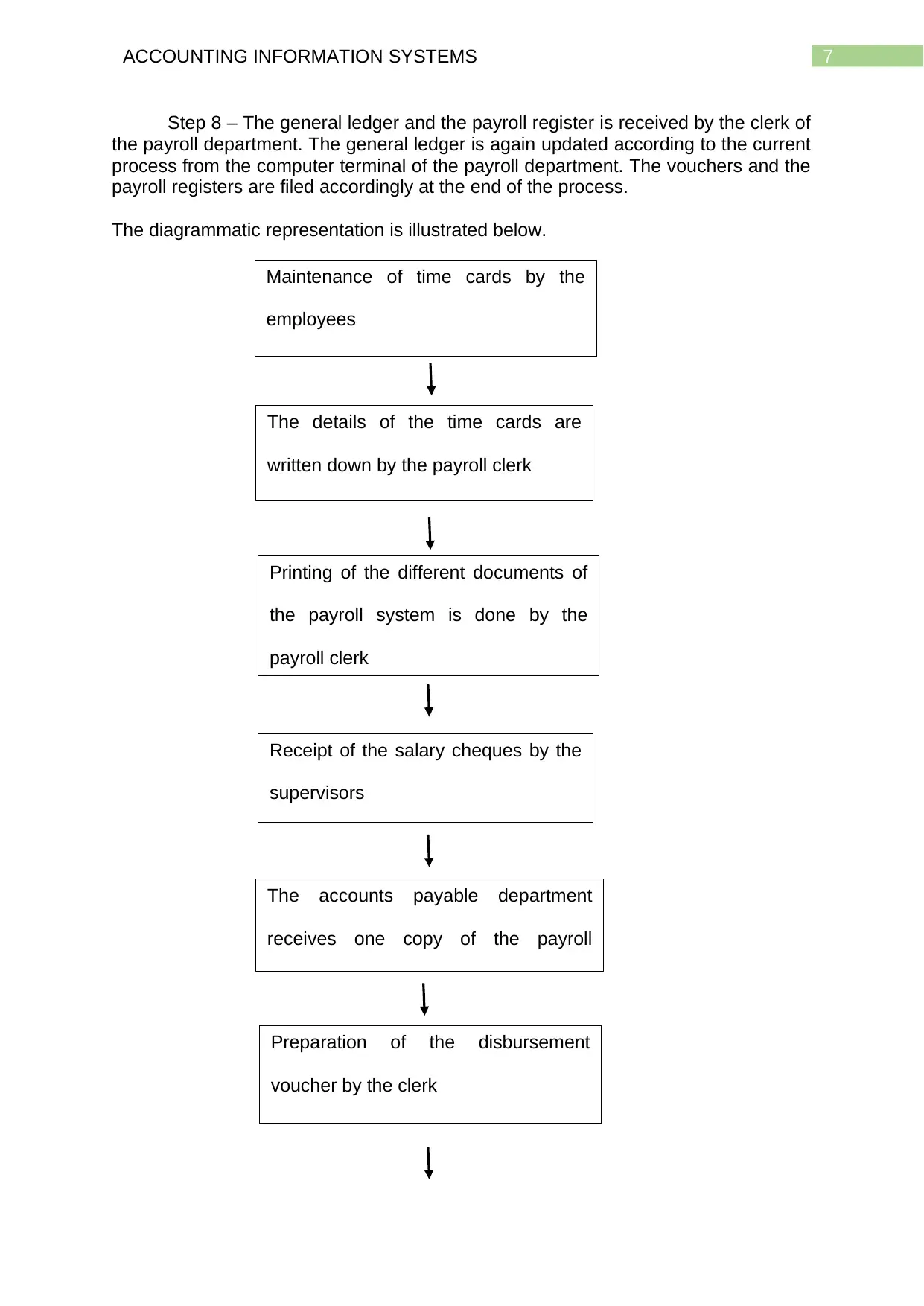

Payroll system of the company

The flowchart showing all the functions and duties of the payroll system can

be illustrated below.

Step 1 – Time cards are maintained by all the employees of the company

which are reviewed at the end of the week by the supervisors.

Step 2 – The payroll clerk inputs the details mentioned in the time card into

the system. This system is regarded as the central payroll system that is connected

to a computer terminal.

Step 3 – The payroll clerk prints the hard copies of the different documents

related to the payroll system (Thite and Sandhu 2014). These documents include

pay cheques and two copies of the payroll register. The clerk then updates the digital

records of the employees through the incorporation of the new data.

Step 4 – The payroll clerk files all the time cards of the respective employees

and finally sends all the salary cheques to the respective supervisors (Thite and

Sandhu 2014). The supervisors review and evaluated these salary cheques for

accuracy and finally distributes them among the departmental employees.

Step 5 – One copy of the payroll register is sent to the accounts payable

department and another one is filed along with the time cards (Ireland 2015). The

second process takes place in the payroll department.

Step 6 – The payroll register is reviewed again by the clerk of the accounts

payable department. The clerk then prepares a disbursement voucher.

Step 7 – The reviewed payroll register along with the disbursement voucher is

received in the general ledger department (Ireland 2015). A common cheque is

written for the entire payroll and gets deposited at the imprest account of the bank.

One copy of this cheque is again filed in the accounts payable department.

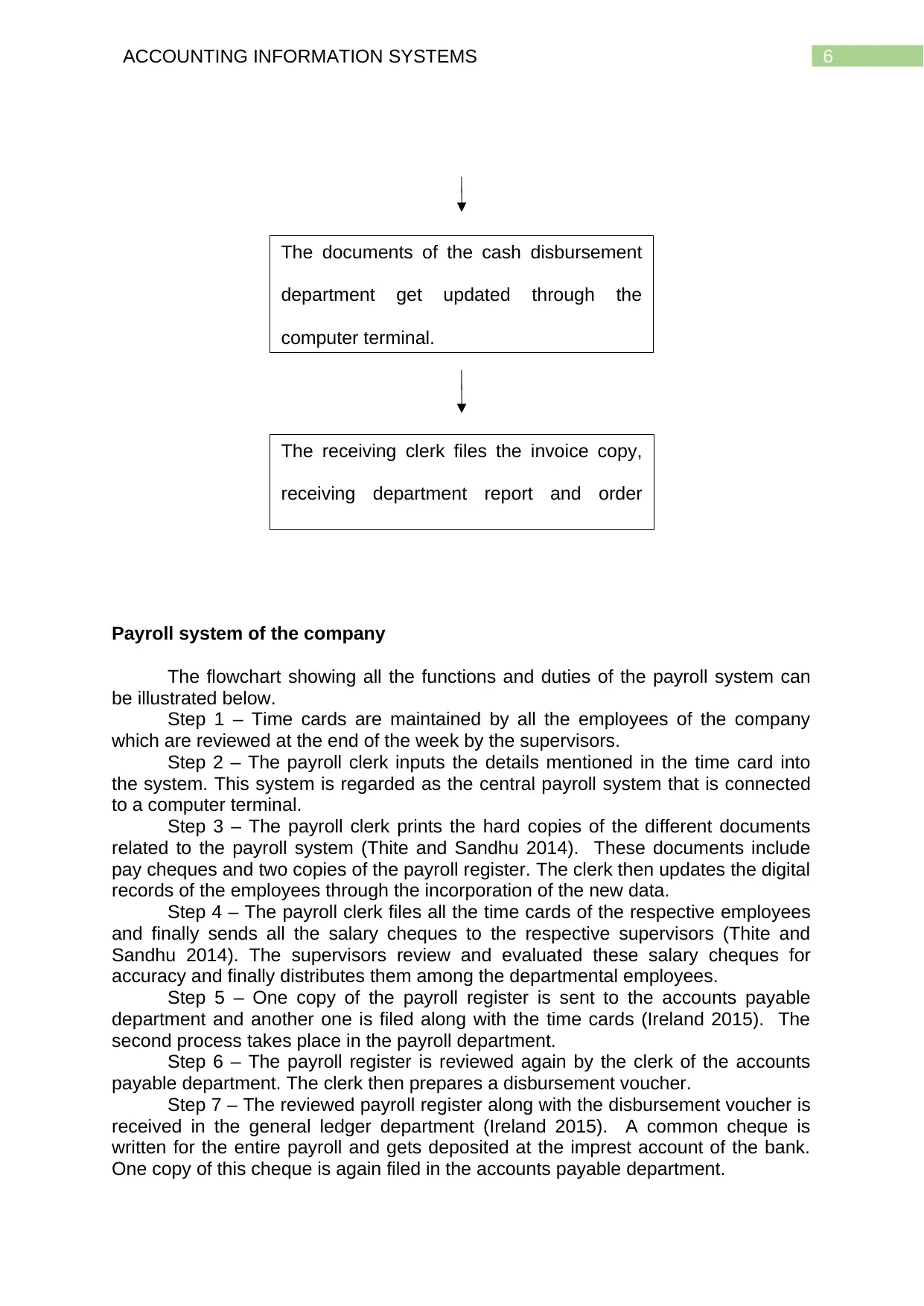

The documents of the cash disbursement

department get updated through the

computer terminal.

The receiving clerk files the invoice copy,

receiving department report and order

copy.

Payroll system of the company

The flowchart showing all the functions and duties of the payroll system can

be illustrated below.

Step 1 – Time cards are maintained by all the employees of the company

which are reviewed at the end of the week by the supervisors.

Step 2 – The payroll clerk inputs the details mentioned in the time card into

the system. This system is regarded as the central payroll system that is connected

to a computer terminal.

Step 3 – The payroll clerk prints the hard copies of the different documents

related to the payroll system (Thite and Sandhu 2014). These documents include

pay cheques and two copies of the payroll register. The clerk then updates the digital

records of the employees through the incorporation of the new data.

Step 4 – The payroll clerk files all the time cards of the respective employees

and finally sends all the salary cheques to the respective supervisors (Thite and

Sandhu 2014). The supervisors review and evaluated these salary cheques for

accuracy and finally distributes them among the departmental employees.

Step 5 – One copy of the payroll register is sent to the accounts payable

department and another one is filed along with the time cards (Ireland 2015). The

second process takes place in the payroll department.

Step 6 – The payroll register is reviewed again by the clerk of the accounts

payable department. The clerk then prepares a disbursement voucher.

Step 7 – The reviewed payroll register along with the disbursement voucher is

received in the general ledger department (Ireland 2015). A common cheque is

written for the entire payroll and gets deposited at the imprest account of the bank.

One copy of this cheque is again filed in the accounts payable department.

The documents of the cash disbursement

department get updated through the

computer terminal.

The receiving clerk files the invoice copy,

receiving department report and order

copy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING INFORMATION SYSTEMS

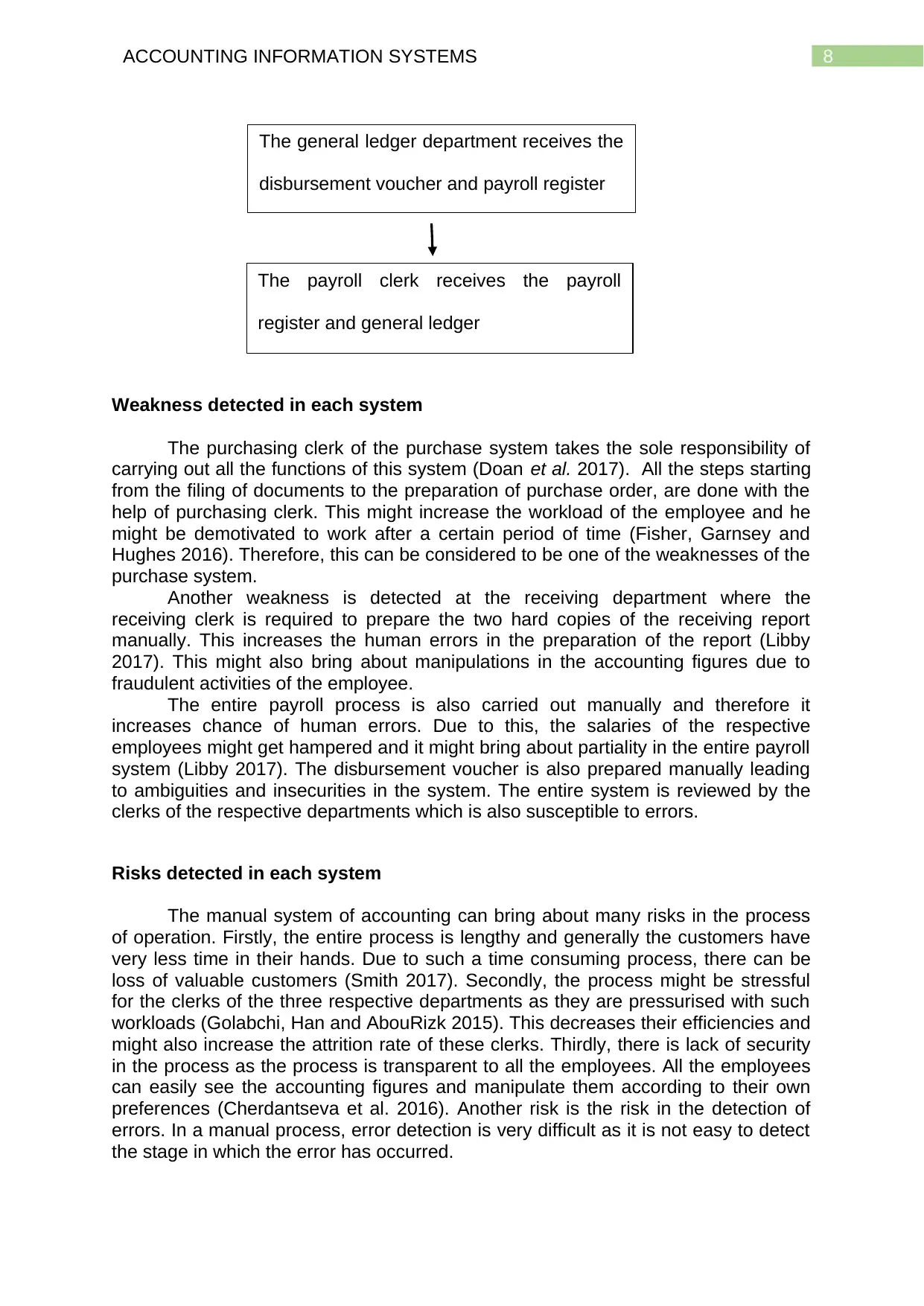

Step 8 – The general ledger and the payroll register is received by the clerk of

the payroll department. The general ledger is again updated according to the current

process from the computer terminal of the payroll department. The vouchers and the

payroll registers are filed accordingly at the end of the process.

The diagrammatic representation is illustrated below.

Maintenance of time cards by the

employees

The details of the time cards are

written down by the payroll clerk

Printing of the different documents of

the payroll system is done by the

payroll clerk

Receipt of the salary cheques by the

supervisors

The accounts payable department

receives one copy of the payroll

register

Preparation of the disbursement

voucher by the clerk

Step 8 – The general ledger and the payroll register is received by the clerk of

the payroll department. The general ledger is again updated according to the current

process from the computer terminal of the payroll department. The vouchers and the

payroll registers are filed accordingly at the end of the process.

The diagrammatic representation is illustrated below.

Maintenance of time cards by the

employees

The details of the time cards are

written down by the payroll clerk

Printing of the different documents of

the payroll system is done by the

payroll clerk

Receipt of the salary cheques by the

supervisors

The accounts payable department

receives one copy of the payroll

register

Preparation of the disbursement

voucher by the clerk

8ACCOUNTING INFORMATION SYSTEMS

Weakness detected in each system

The purchasing clerk of the purchase system takes the sole responsibility of

carrying out all the functions of this system (Doan et al. 2017). All the steps starting

from the filing of documents to the preparation of purchase order, are done with the

help of purchasing clerk. This might increase the workload of the employee and he

might be demotivated to work after a certain period of time (Fisher, Garnsey and

Hughes 2016). Therefore, this can be considered to be one of the weaknesses of the

purchase system.

Another weakness is detected at the receiving department where the

receiving clerk is required to prepare the two hard copies of the receiving report

manually. This increases the human errors in the preparation of the report (Libby

2017). This might also bring about manipulations in the accounting figures due to

fraudulent activities of the employee.

The entire payroll process is also carried out manually and therefore it

increases chance of human errors. Due to this, the salaries of the respective

employees might get hampered and it might bring about partiality in the entire payroll

system (Libby 2017). The disbursement voucher is also prepared manually leading

to ambiguities and insecurities in the system. The entire system is reviewed by the

clerks of the respective departments which is also susceptible to errors.

Risks detected in each system

The manual system of accounting can bring about many risks in the process

of operation. Firstly, the entire process is lengthy and generally the customers have

very less time in their hands. Due to such a time consuming process, there can be

loss of valuable customers (Smith 2017). Secondly, the process might be stressful

for the clerks of the three respective departments as they are pressurised with such

workloads (Golabchi, Han and AbouRizk 2015). This decreases their efficiencies and

might also increase the attrition rate of these clerks. Thirdly, there is lack of security

in the process as the process is transparent to all the employees. All the employees

can easily see the accounting figures and manipulate them according to their own

preferences (Cherdantseva et al. 2016). Another risk is the risk in the detection of

errors. In a manual process, error detection is very difficult as it is not easy to detect

the stage in which the error has occurred.

The general ledger department receives the

disbursement voucher and payroll register

The payroll clerk receives the payroll

register and general ledger

Weakness detected in each system

The purchasing clerk of the purchase system takes the sole responsibility of

carrying out all the functions of this system (Doan et al. 2017). All the steps starting

from the filing of documents to the preparation of purchase order, are done with the

help of purchasing clerk. This might increase the workload of the employee and he

might be demotivated to work after a certain period of time (Fisher, Garnsey and

Hughes 2016). Therefore, this can be considered to be one of the weaknesses of the

purchase system.

Another weakness is detected at the receiving department where the

receiving clerk is required to prepare the two hard copies of the receiving report

manually. This increases the human errors in the preparation of the report (Libby

2017). This might also bring about manipulations in the accounting figures due to

fraudulent activities of the employee.

The entire payroll process is also carried out manually and therefore it

increases chance of human errors. Due to this, the salaries of the respective

employees might get hampered and it might bring about partiality in the entire payroll

system (Libby 2017). The disbursement voucher is also prepared manually leading

to ambiguities and insecurities in the system. The entire system is reviewed by the

clerks of the respective departments which is also susceptible to errors.

Risks detected in each system

The manual system of accounting can bring about many risks in the process

of operation. Firstly, the entire process is lengthy and generally the customers have

very less time in their hands. Due to such a time consuming process, there can be

loss of valuable customers (Smith 2017). Secondly, the process might be stressful

for the clerks of the three respective departments as they are pressurised with such

workloads (Golabchi, Han and AbouRizk 2015). This decreases their efficiencies and

might also increase the attrition rate of these clerks. Thirdly, there is lack of security

in the process as the process is transparent to all the employees. All the employees

can easily see the accounting figures and manipulate them according to their own

preferences (Cherdantseva et al. 2016). Another risk is the risk in the detection of

errors. In a manual process, error detection is very difficult as it is not easy to detect

the stage in which the error has occurred.

The general ledger department receives the

disbursement voucher and payroll register

The payroll clerk receives the payroll

register and general ledger

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING INFORMATION SYSTEMS

Conclusion

From the above report it can be concluded that there has been a convenient

and a simple system that is followed in the company, Adam & Co. The accounting

system of expenditure is segregated broadly into three departments, that is,

purchase, cash disbursement and payroll. This technique increases the accessibility

of the information to the respective authorities but at the same time decreases the

security of the system. In the paper, all the system processes are presented through

a flowchart in a stepwise manner. The weaknesses and the risks of the system are

predicted accordingly in the last section of the report.

Conclusion

From the above report it can be concluded that there has been a convenient

and a simple system that is followed in the company, Adam & Co. The accounting

system of expenditure is segregated broadly into three departments, that is,

purchase, cash disbursement and payroll. This technique increases the accessibility

of the information to the respective authorities but at the same time decreases the

security of the system. In the paper, all the system processes are presented through

a flowchart in a stepwise manner. The weaknesses and the risks of the system are

predicted accordingly in the last section of the report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING INFORMATION SYSTEMS

References

Cherdantseva, Y., Burnap, P., Blyth, A., Eden, P., Jones, K., Soulsby, H. and

Stoddart, K., 2016. A review of cyber security risk assessment methods for SCADA

systems. Computers & security, 56, pp.1-27.

Doan, D.T., Ghaffarianhoseini, A., Naismith, N., Zhang, T., Ghaffarianhoseini, A. and

Tookey, J., 2017. A critical comparison of green building rating systems. Building

and Environment, 123, pp.243-260.

Fisher, I.E., Garnsey, M.R. and Hughes, M.E., 2016. Natural language processing in

accounting, auditing and finance: A synthesis of the literature with a roadmap for

future research. Intelligent Systems in Accounting, Finance and Management, 23(3),

pp.157-214.

Golabchi, A., Han, S. and AbouRizk, S.M., 2015, September. Integration of

ergonomic analysis into simulation modeling of manual operations. In Proceedings

of the 16th ASIM Dedicated Conference on Simulation in Production and

Logistics (pp. 491-501).

Ireland, E., 2015. Annual Report & Accounts| 2012.

Jing, H., 2015. The study on the impact of data storage from accounting information

processing procedure. International Journal of Database Theory and

Application, 8(3), pp.323-332.

Libby, R., 2017. Accounting and human information processing. In The Routledge

Companion to Behavioural Accounting Research (pp. 42-54). Routledge.

Morgan, G.G., 2017. The charity treasurer's handbook. London: Directory of Social

Change.

Slater, J. and Deschamps, M., 2015. College accounting. Prentice Hall.

Smith, D.J., 2017. Reliability, maintainability and risk: practical methods for

engineers. Butterworth-Heinemann.

Thite, M. and Sandhu, K., 2014. Where is My Pay? Critical Success Factors of a

Payroll System–A System Life Cycle Approach. Australasian Journal of Information

Systems, 18(2).

Xing, W., Xian, M. and Tu, Y.Y., 2014. Research on the internal control and

reorganization of enterprise accounting process under the information environment.

In Applied Mechanics and Materials (Vol. 687, pp. 4503-4506). Trans Tech

Publications.

References

Cherdantseva, Y., Burnap, P., Blyth, A., Eden, P., Jones, K., Soulsby, H. and

Stoddart, K., 2016. A review of cyber security risk assessment methods for SCADA

systems. Computers & security, 56, pp.1-27.

Doan, D.T., Ghaffarianhoseini, A., Naismith, N., Zhang, T., Ghaffarianhoseini, A. and

Tookey, J., 2017. A critical comparison of green building rating systems. Building

and Environment, 123, pp.243-260.

Fisher, I.E., Garnsey, M.R. and Hughes, M.E., 2016. Natural language processing in

accounting, auditing and finance: A synthesis of the literature with a roadmap for

future research. Intelligent Systems in Accounting, Finance and Management, 23(3),

pp.157-214.

Golabchi, A., Han, S. and AbouRizk, S.M., 2015, September. Integration of

ergonomic analysis into simulation modeling of manual operations. In Proceedings

of the 16th ASIM Dedicated Conference on Simulation in Production and

Logistics (pp. 491-501).

Ireland, E., 2015. Annual Report & Accounts| 2012.

Jing, H., 2015. The study on the impact of data storage from accounting information

processing procedure. International Journal of Database Theory and

Application, 8(3), pp.323-332.

Libby, R., 2017. Accounting and human information processing. In The Routledge

Companion to Behavioural Accounting Research (pp. 42-54). Routledge.

Morgan, G.G., 2017. The charity treasurer's handbook. London: Directory of Social

Change.

Slater, J. and Deschamps, M., 2015. College accounting. Prentice Hall.

Smith, D.J., 2017. Reliability, maintainability and risk: practical methods for

engineers. Butterworth-Heinemann.

Thite, M. and Sandhu, K., 2014. Where is My Pay? Critical Success Factors of a

Payroll System–A System Life Cycle Approach. Australasian Journal of Information

Systems, 18(2).

Xing, W., Xian, M. and Tu, Y.Y., 2014. Research on the internal control and

reorganization of enterprise accounting process under the information environment.

In Applied Mechanics and Materials (Vol. 687, pp. 4503-4506). Trans Tech

Publications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.