HA3011 Advanced Financial Accounting: Final Assessment T2 2021

VerifiedAdded on 2023/06/18

|10

|1863

|90

Homework Assignment

AI Summary

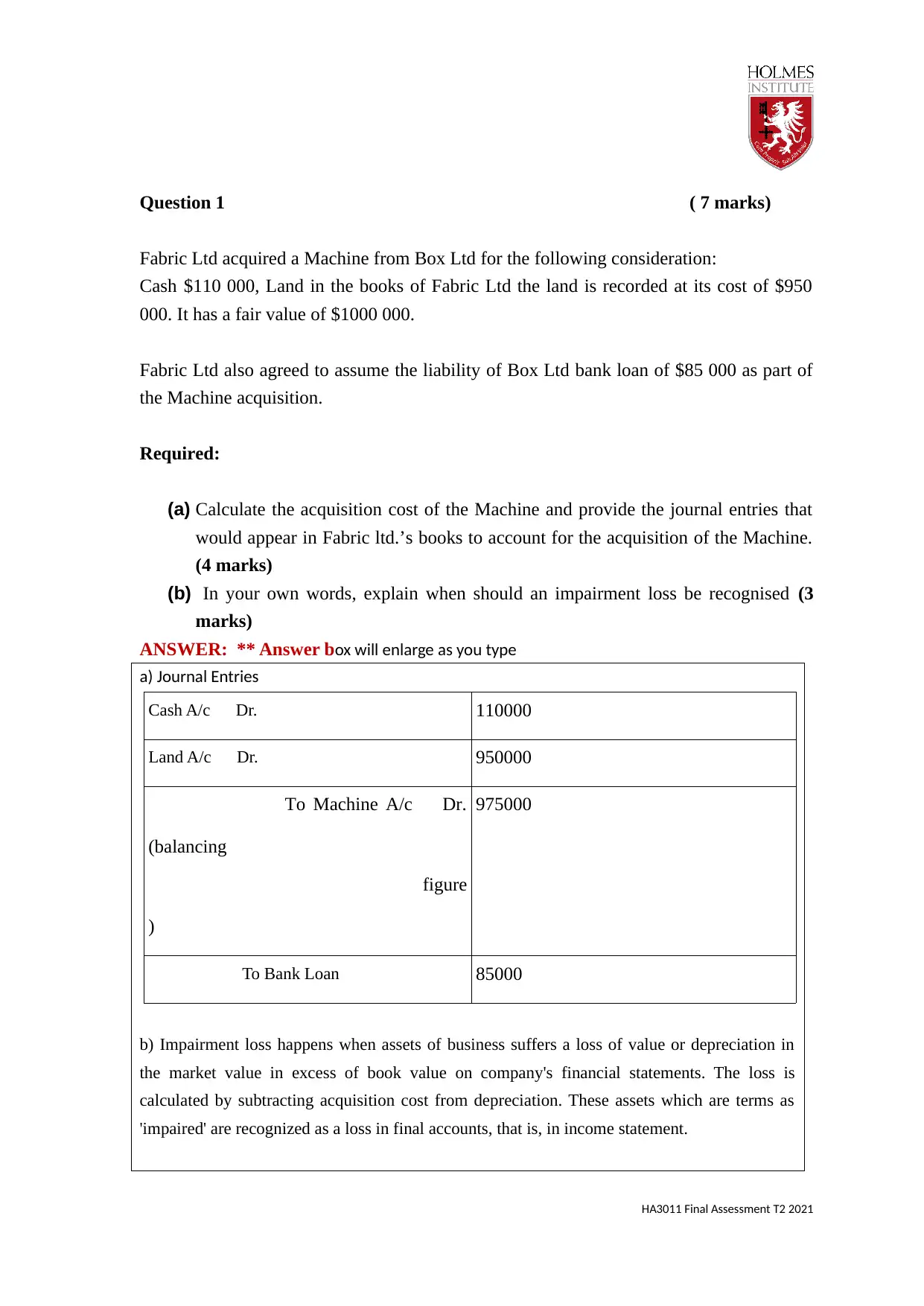

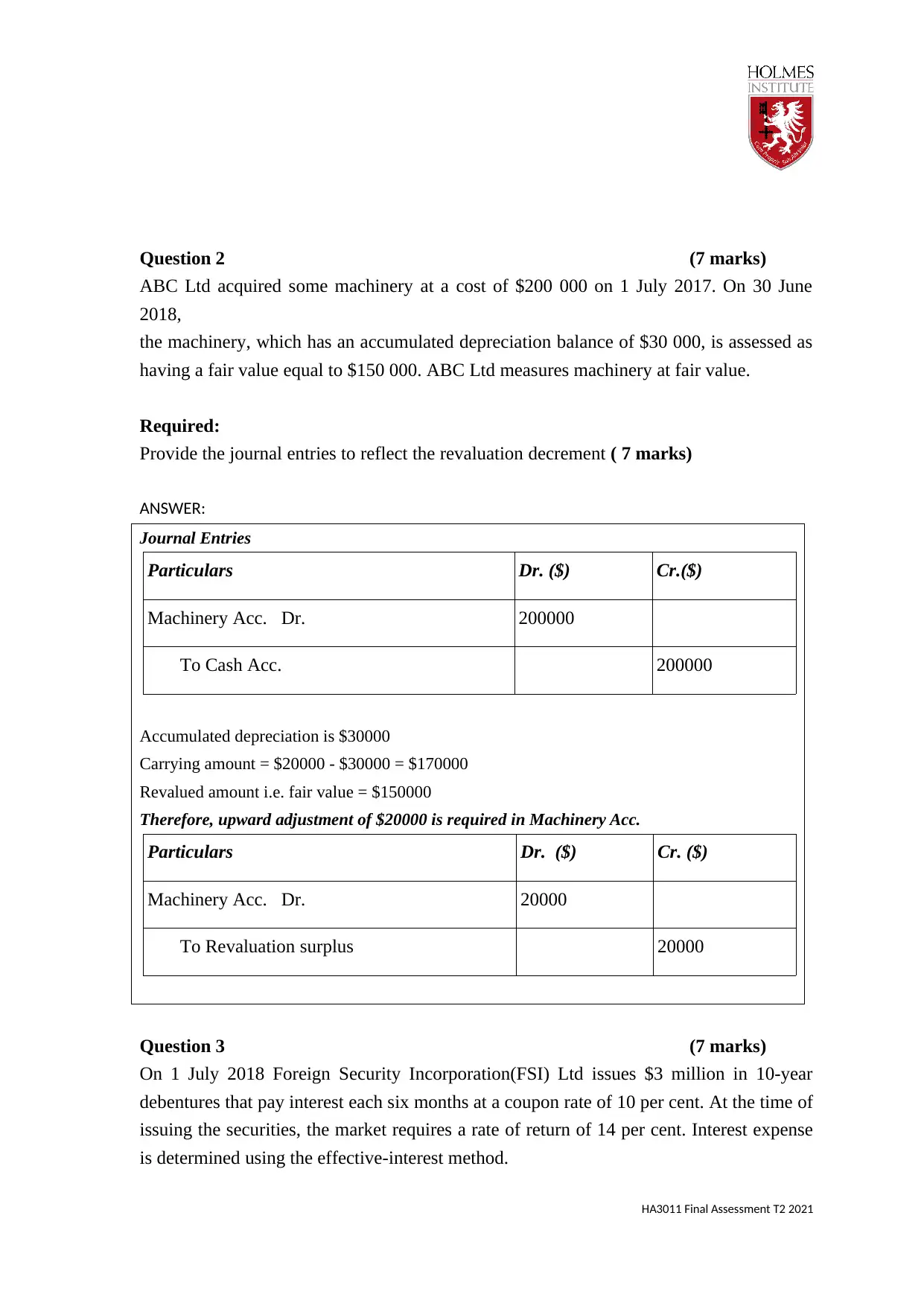

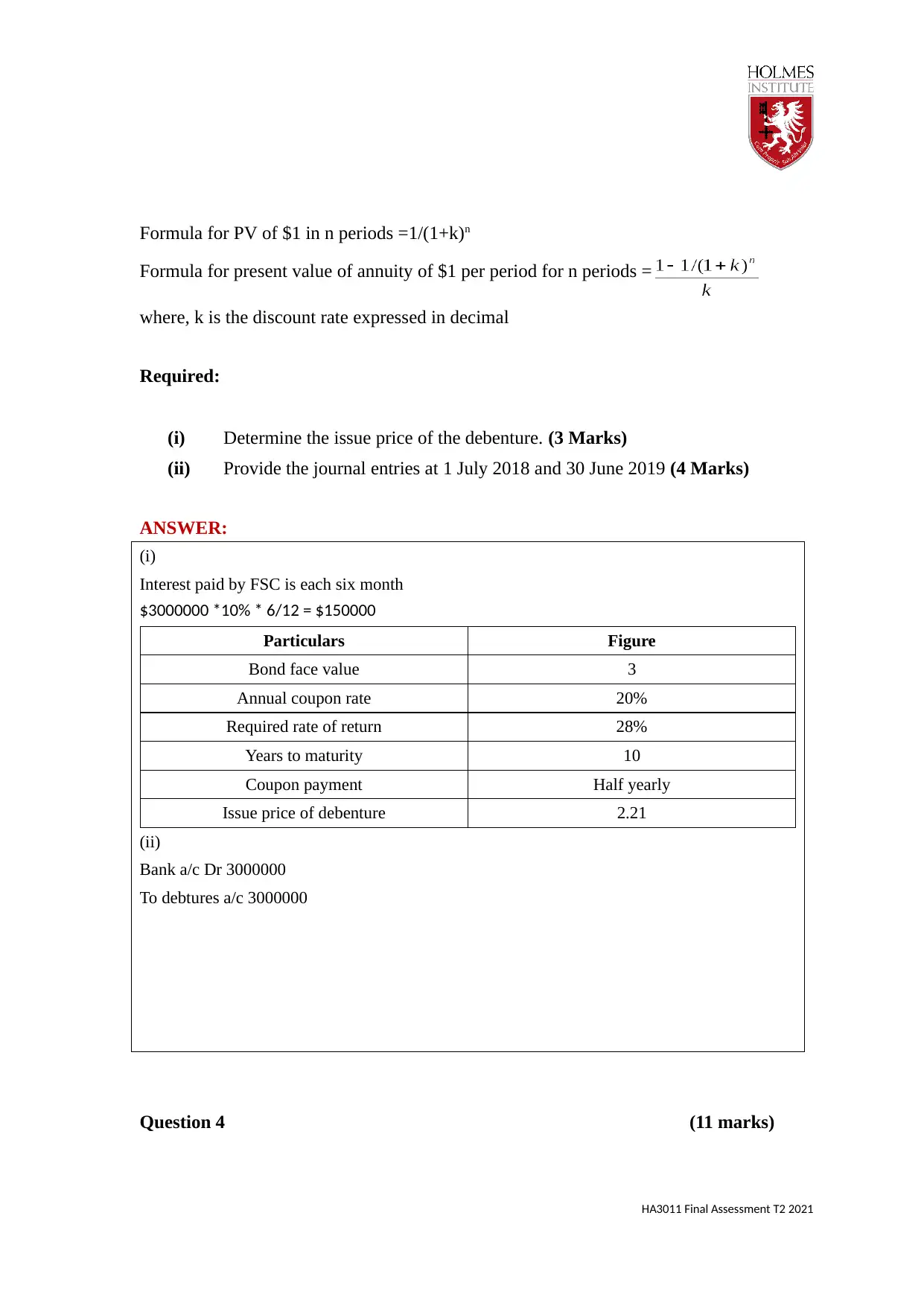

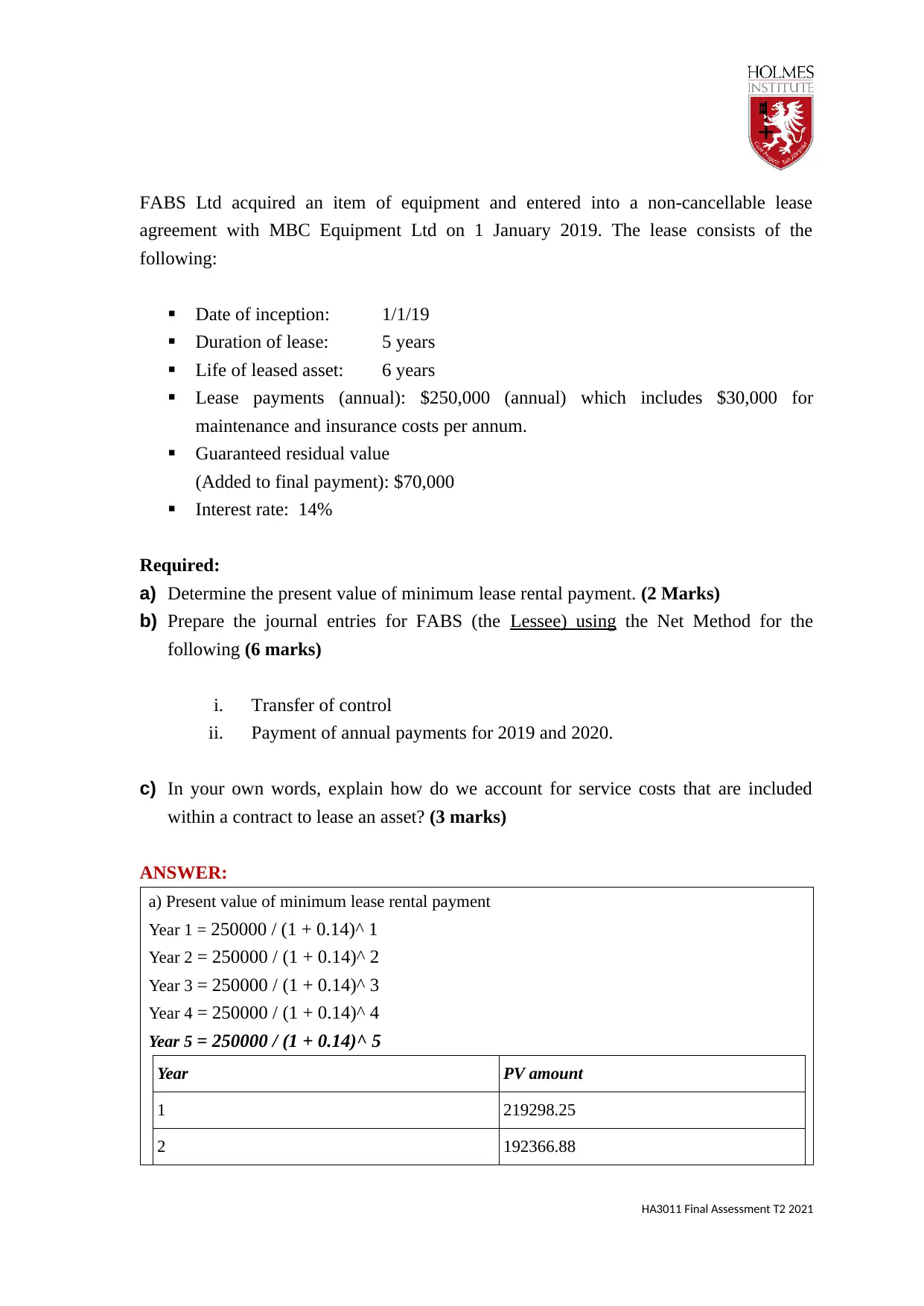

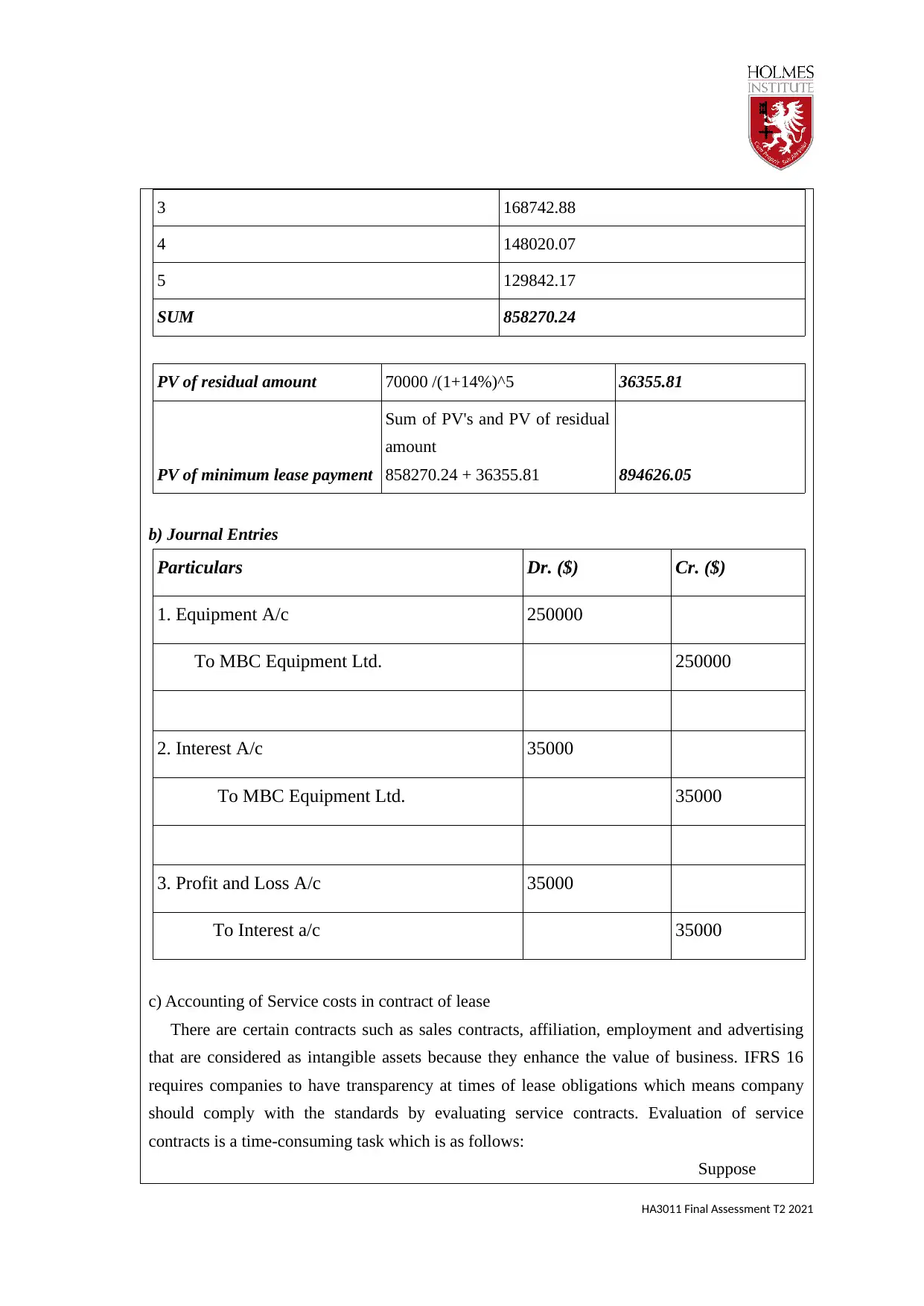

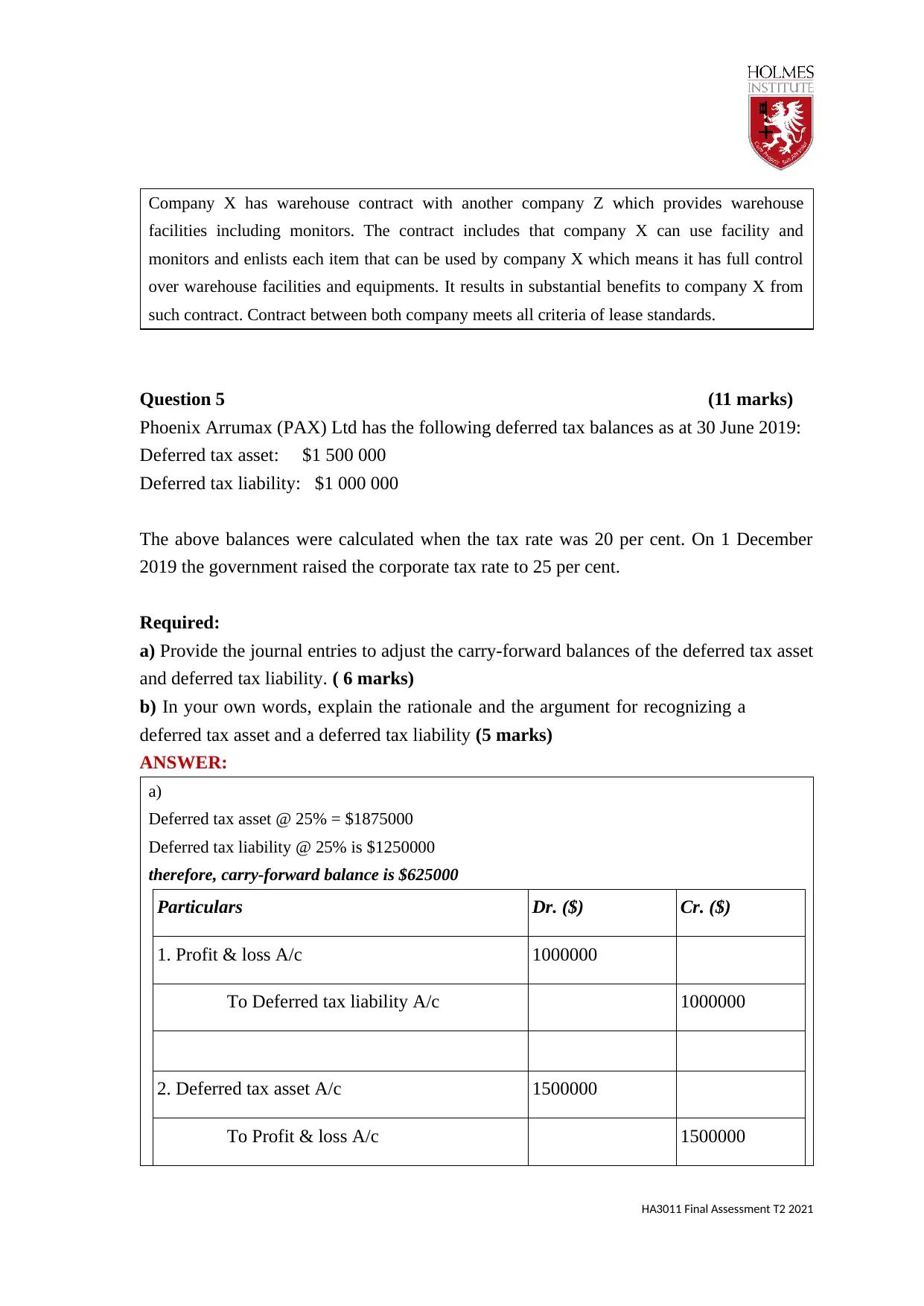

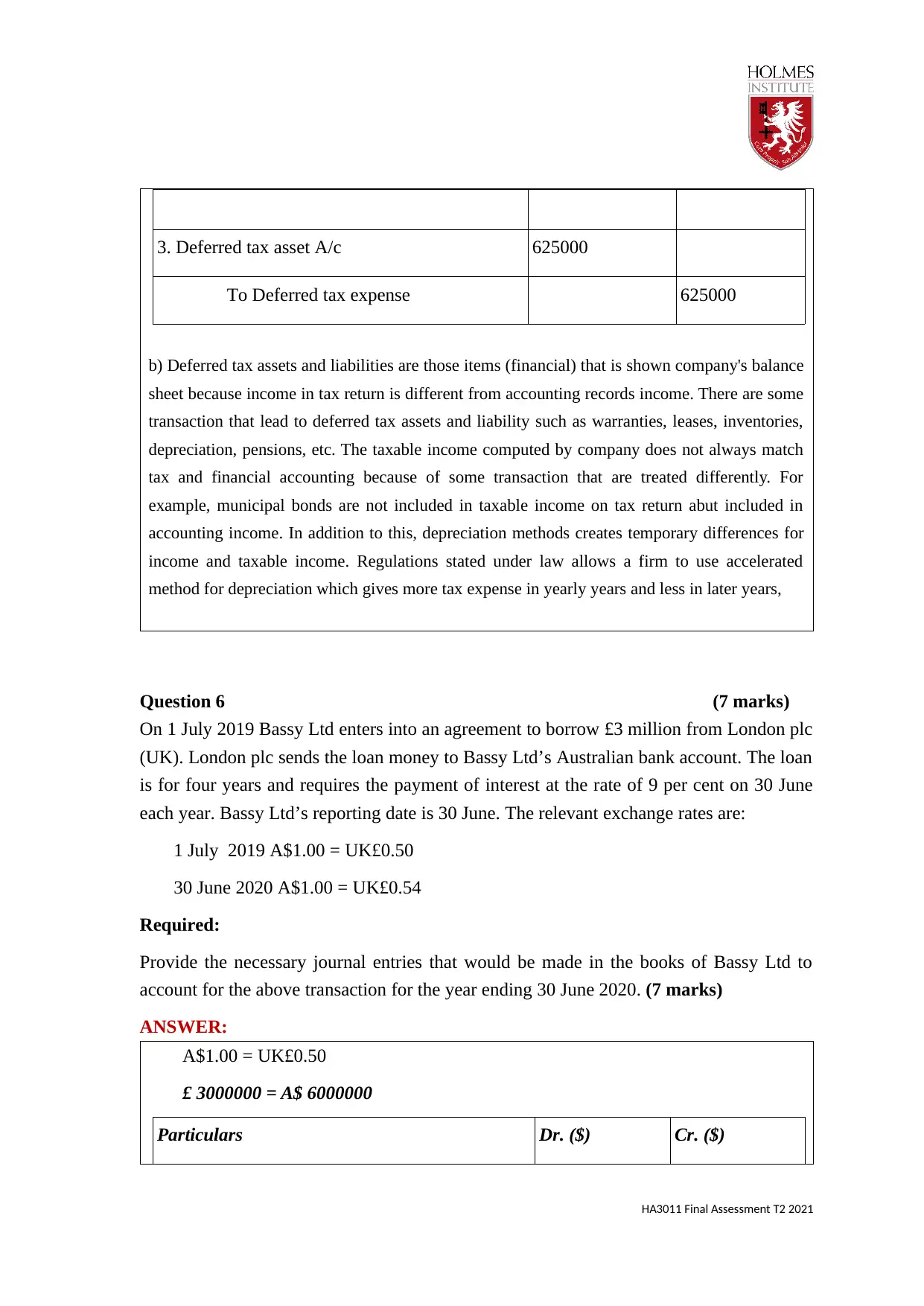

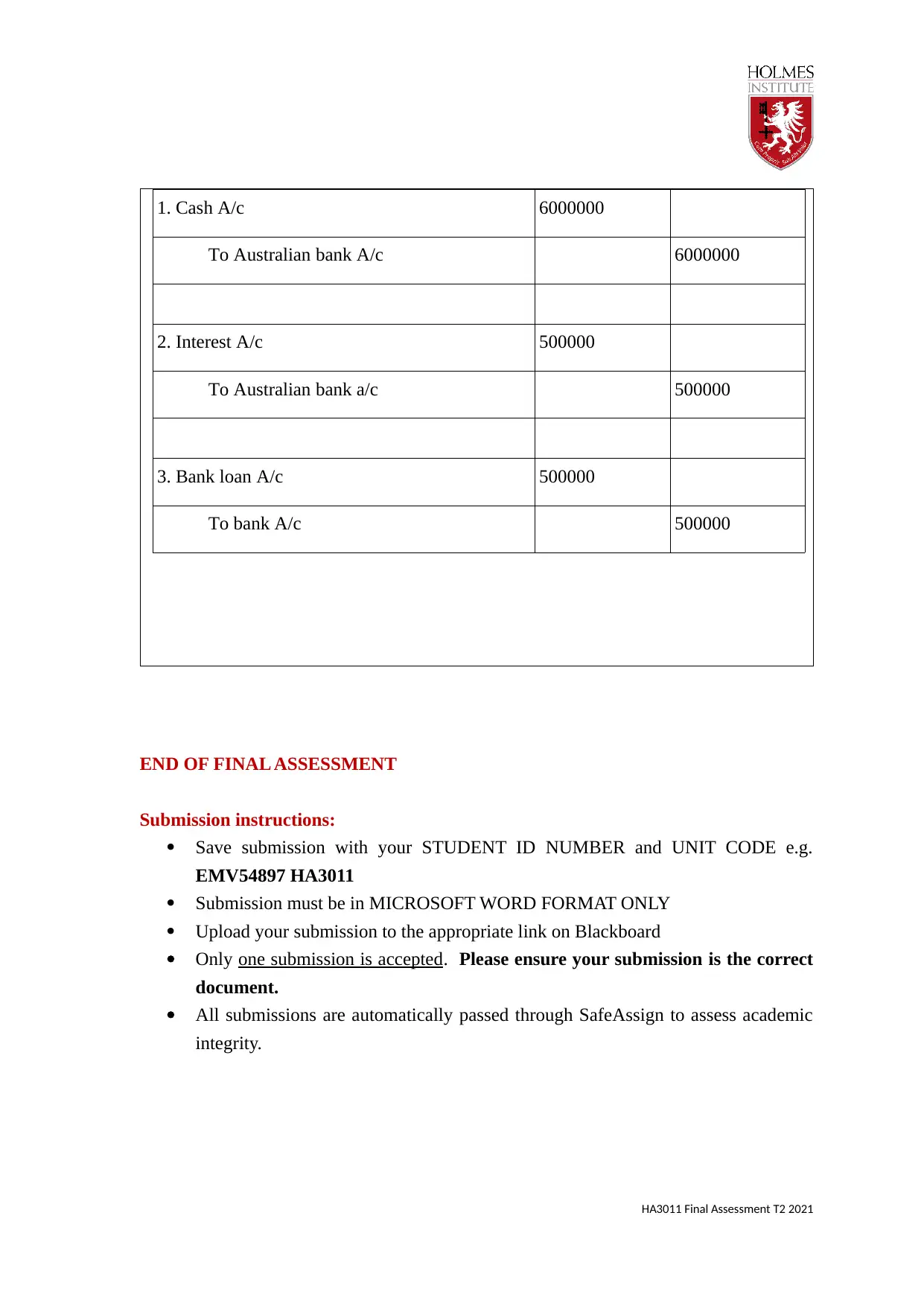

This assignment solution covers several key areas of advanced financial accounting. It includes calculating the acquisition cost of a machine and providing relevant journal entries, explaining when an impairment loss should be recognized, and providing journal entries to reflect a revaluation decrement. The solution also addresses determining the issue price of a debenture and providing journal entries, preparing journal entries for a lessee using the net method, and explaining how to account for service costs included in a lease agreement. Furthermore, it covers adjusting deferred tax asset and liability balances due to a change in the corporate tax rate, explaining the rationale for recognizing deferred tax assets and liabilities, and providing journal entries to account for a foreign loan transaction. Desklib offers a wealth of resources including past papers and solved assignments to aid students in their studies.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.