HA3032 Auditing Group Report: Angel Seafood Holdings Audit Program

VerifiedAdded on 2022/11/10

|23

|4725

|98

Report

AI Summary

This report presents a comprehensive audit analysis of Angel Seafood Holdings Pty Ltd. It begins with an introduction to the company, its operations, and its position in the oyster farming industry. The report identifies key business risks, including operational, competition, legal, environmental, and economic risks, along with financial risks such as capital investments and valuation of biological assets. An audit risk model is then developed, outlining inherent, control, and detection risks, and their impact on the overall audit risk. The report also includes analytical procedures, such as ratio analysis, to assess the company's financial performance. The selection of material account balances and financial assertions is discussed, followed by a detailed outline of audit steps and sampling techniques. The report concludes with a summary of findings and recommendations. This assignment was completed as part of the HA3032 Auditing course at Holmes Institute.

Running Head: Auditing

AUDITING – HA3032

Audit of Angel Seafood Holdings Pty Ltd

Student Name:

Student Number:

Name of the University:

Author’s Note:

AUDITING – HA3032

Audit of Angel Seafood Holdings Pty Ltd

Student Name:

Student Number:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1Auditing

Executive Summary:

For the assignment, we have been allocated the Audit process of Angel Seafood Holdings Pty

Ltd. In this assignment there shall be recognition of the industries nature that the company

belongs to. The areas related to the misstatements of material have been analyzed that can be

found in the financial statements and reports of the company.

Executive Summary:

For the assignment, we have been allocated the Audit process of Angel Seafood Holdings Pty

Ltd. In this assignment there shall be recognition of the industries nature that the company

belongs to. The areas related to the misstatements of material have been analyzed that can be

found in the financial statements and reports of the company.

2Auditing

Table of Contents

Introduction – Angel Seafood Holdings Pty Ltd.:..........................................................................................................3

Identification of Key Business Risks:.............................................................................................................................4

Audit Risk Model............................................................................................................................................................6

Analytical Procedures:....................................................................................................................................................9

Material Account Balances...........................................................................................................................................11

Selection of Top 10 Material Accounts and Financial Assertions:...............................................................................12

Audit Steps: 14

Audit Sampling 16

Conclusion 18

References 19

Table of Contents

Introduction – Angel Seafood Holdings Pty Ltd.:..........................................................................................................3

Identification of Key Business Risks:.............................................................................................................................4

Audit Risk Model............................................................................................................................................................6

Analytical Procedures:....................................................................................................................................................9

Material Account Balances...........................................................................................................................................11

Selection of Top 10 Material Accounts and Financial Assertions:...............................................................................12

Audit Steps: 14

Audit Sampling 16

Conclusion 18

References 19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3Auditing

Introduction – Angel Seafood Holdings Pty Ltd.:

Angel Seafood Holdings Pty Ltd was initially a family operated business in South Australia. Over the

years, has been developed from the oyster-growing traditional business to a pioneering and organically

certified finest Coffin Bay Oysters producer. Incorporated on September 26, 2016 as a proprietary

company, Angel Seafood turned into an unlisted company on 21 April 2017.

Angel Seafood Holdings (ASH) currently operates out of Haslam& Cowell, Coffin Bay and Smoky Bay. It

sells organic and sustainable oysters domestically as well as globally. The company possesses or leases

41.08 hectares of oyster creation licenses or leases in South Australia. (Eleftheriou,Komarev and

Klumpes 2018)

Angel Seafood is a recently listed company on the ASX. It was listed in February 2018. It runs with a

vision to become the largest oyster producer in Australia. It plans to pull off its pristine farming milieu over

time and expand seafood offerings in the market place. It is recognised by the National Association for

Sustainable Agriculture, Australia (NASAA). It is also sustainably qualifiedwith the ‘Friends of The Sea’

organisation.

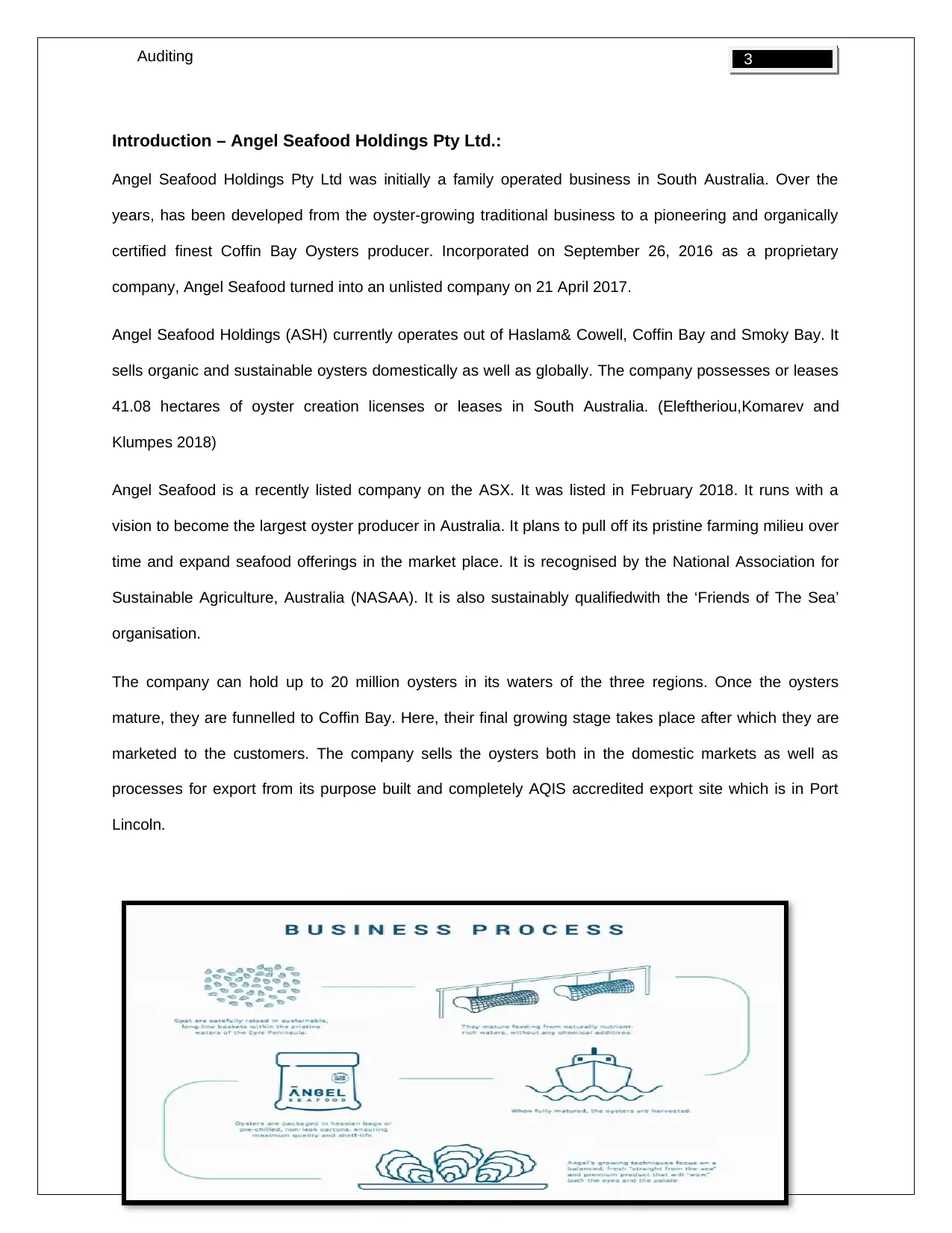

The company can hold up to 20 million oysters in its waters of the three regions. Once the oysters

mature, they are funnelled to Coffin Bay. Here, their final growing stage takes place after which they are

marketed to the customers. The company sells the oysters both in the domestic markets as well as

processes for export from its purpose built and completely AQIS accredited export site which is in Port

Lincoln.

Introduction – Angel Seafood Holdings Pty Ltd.:

Angel Seafood Holdings Pty Ltd was initially a family operated business in South Australia. Over the

years, has been developed from the oyster-growing traditional business to a pioneering and organically

certified finest Coffin Bay Oysters producer. Incorporated on September 26, 2016 as a proprietary

company, Angel Seafood turned into an unlisted company on 21 April 2017.

Angel Seafood Holdings (ASH) currently operates out of Haslam& Cowell, Coffin Bay and Smoky Bay. It

sells organic and sustainable oysters domestically as well as globally. The company possesses or leases

41.08 hectares of oyster creation licenses or leases in South Australia. (Eleftheriou,Komarev and

Klumpes 2018)

Angel Seafood is a recently listed company on the ASX. It was listed in February 2018. It runs with a

vision to become the largest oyster producer in Australia. It plans to pull off its pristine farming milieu over

time and expand seafood offerings in the market place. It is recognised by the National Association for

Sustainable Agriculture, Australia (NASAA). It is also sustainably qualifiedwith the ‘Friends of The Sea’

organisation.

The company can hold up to 20 million oysters in its waters of the three regions. Once the oysters

mature, they are funnelled to Coffin Bay. Here, their final growing stage takes place after which they are

marketed to the customers. The company sells the oysters both in the domestic markets as well as

processes for export from its purpose built and completely AQIS accredited export site which is in Port

Lincoln.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4Auditing

Identification of Key Business Risks:

On studying the Annual Reports of the company, Angel Seafood Holding Pty Ltd., we came across the

following risks highlighted by the auditors and management.

Operational Risk: The Company has a great deal of operational risks. The cultivation of oysters

could be challenging in the long run considering the enormous extractions.(Yoon,Hoogduin and

Zhang 2015) Moreover, there are other operational challenges like threat of changes in

Government policies, environmental hazards etc. which at the end affect the operations. (Nigrini

2017)

Competition Risk: The industry is pertinent in competitions across both the domestic and global

markets. Despite taking due diligence in all its corporate decisions and the operations, the

company does not have any control over the actionsof its competitors. The actions of competitors

may impact Angel Seafood’s business positively or negatively. The impact could be on the

financial or operational performance of the company.Any increase in supplies from competitors or

any new alternative seafood production could hamper the company’s business and its operations.

Moreover, there is a high degree of risk in the access to spat on which the company relies heavily

to replenish its stocks. (Mohan 2018)

Legal Risk: All the licenses required and owned by the company are issued through the PIRSA

(Primary Industries and Regions South Australia) managed by the South Australian state

government. There are a lot of regulations which the company needs to abide by failing which

there could be legal repercussions during renewals. (Mališ and Novak 2016)

Environmental Risks: There are high chances of the company’s operations being affected by

environmental challenges or incidents. Any new environmental regulation would add to the costs

of the company wherein the company would have to comply with the respective law. Besides,

risks of climate change and global warming are amongst the uncontrollable environmental risks.

(Askary, Arnaout and Abughazaleh 2018)

Identification of Key Business Risks:

On studying the Annual Reports of the company, Angel Seafood Holding Pty Ltd., we came across the

following risks highlighted by the auditors and management.

Operational Risk: The Company has a great deal of operational risks. The cultivation of oysters

could be challenging in the long run considering the enormous extractions.(Yoon,Hoogduin and

Zhang 2015) Moreover, there are other operational challenges like threat of changes in

Government policies, environmental hazards etc. which at the end affect the operations. (Nigrini

2017)

Competition Risk: The industry is pertinent in competitions across both the domestic and global

markets. Despite taking due diligence in all its corporate decisions and the operations, the

company does not have any control over the actionsof its competitors. The actions of competitors

may impact Angel Seafood’s business positively or negatively. The impact could be on the

financial or operational performance of the company.Any increase in supplies from competitors or

any new alternative seafood production could hamper the company’s business and its operations.

Moreover, there is a high degree of risk in the access to spat on which the company relies heavily

to replenish its stocks. (Mohan 2018)

Legal Risk: All the licenses required and owned by the company are issued through the PIRSA

(Primary Industries and Regions South Australia) managed by the South Australian state

government. There are a lot of regulations which the company needs to abide by failing which

there could be legal repercussions during renewals. (Mališ and Novak 2016)

Environmental Risks: There are high chances of the company’s operations being affected by

environmental challenges or incidents. Any new environmental regulation would add to the costs

of the company wherein the company would have to comply with the respective law. Besides,

risks of climate change and global warming are amongst the uncontrollable environmental risks.

(Askary, Arnaout and Abughazaleh 2018)

5Auditing

Disease Risk: There are risks of diseases outbreaks impacting the health of oyster stocks. One

such disease is the Pacific Oyster Mortality Syndrome (POMS) affecting infantile Pacific Oysters.

Although POMS has not befallen in the regions where Angel Seafood Holdings operate, there is

no certainty of it not affecting the coffin bay oysters. Although these have been controlled by way

of various measures, these along with other diseases may affect the health and welfare of the

oysters. (Huang, Lin, et al. 2017)

Economic Risks:Economic Risks are general risks including inflation, currency fluctuations,

industrial disputations, interest rates and growth rate. These may impact the future earnings of

the company disturbing its ability to meet forecasts. (Vovchenko, Holina, et al. 2017)

These are the general risks the company may face as a whole. Besides these, there are various financial

risks which needs to be considered.

The financial risks include:

Huge Capital Investments: The Company is a new company which have raised funds from

issue of shares. For the year ending 2017, the share proceeds were $ 5.8 million and for the year

ending 2018, the proceeds were $ 8 million. Although considering the fact that the company is a

new one, it has not been able to convert is operations into profit making yet. (Mock, Srivastava

and Wright 2017)

Risk of losses: With the kind of volatile industry, the risk of loss making is very high. Moreover,

the costs in legal agreements further add to the outflows. Although the losses have reduced from

2017 to 2018, it does not end the risk of losses. (Childress, Hagi and Turnham2018)

Negative operational and investing cash flows: The Company has been incurring losses since

its inception. The cash flows from operations and investments are all negative. To combat this the

company has issued further shares in the form of new share capital. (Comunale, Barragato and

Buhrau 2019)

Risk of valuation of biological assets: The valuation of oysters is another challenge the

company may face. The valuation is further used to determine various ratios and analyse growth

Disease Risk: There are risks of diseases outbreaks impacting the health of oyster stocks. One

such disease is the Pacific Oyster Mortality Syndrome (POMS) affecting infantile Pacific Oysters.

Although POMS has not befallen in the regions where Angel Seafood Holdings operate, there is

no certainty of it not affecting the coffin bay oysters. Although these have been controlled by way

of various measures, these along with other diseases may affect the health and welfare of the

oysters. (Huang, Lin, et al. 2017)

Economic Risks:Economic Risks are general risks including inflation, currency fluctuations,

industrial disputations, interest rates and growth rate. These may impact the future earnings of

the company disturbing its ability to meet forecasts. (Vovchenko, Holina, et al. 2017)

These are the general risks the company may face as a whole. Besides these, there are various financial

risks which needs to be considered.

The financial risks include:

Huge Capital Investments: The Company is a new company which have raised funds from

issue of shares. For the year ending 2017, the share proceeds were $ 5.8 million and for the year

ending 2018, the proceeds were $ 8 million. Although considering the fact that the company is a

new one, it has not been able to convert is operations into profit making yet. (Mock, Srivastava

and Wright 2017)

Risk of losses: With the kind of volatile industry, the risk of loss making is very high. Moreover,

the costs in legal agreements further add to the outflows. Although the losses have reduced from

2017 to 2018, it does not end the risk of losses. (Childress, Hagi and Turnham2018)

Negative operational and investing cash flows: The Company has been incurring losses since

its inception. The cash flows from operations and investments are all negative. To combat this the

company has issued further shares in the form of new share capital. (Comunale, Barragato and

Buhrau 2019)

Risk of valuation of biological assets: The valuation of oysters is another challenge the

company may face. The valuation is further used to determine various ratios and analyse growth

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6Auditing

and other prospects. Any error in valuation may lead to risk of proper analysis. (Knechel and

Salterio 2016)

and other prospects. Any error in valuation may lead to risk of proper analysis. (Knechel and

Salterio 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7Auditing

Audit Risk Model

It is an instrument used by Auditors to arrive at the affiliation among varieties of risk in an Audit

engagement. The model states that the overall risk is the product of the major components of risk that are

three in number. These components are Inherent Risk, Control Risk and Detection Risk. (Han, Rezaee, et

al. 2015)

It is embodied in equation form as:

Audit Risk = (Inherent Risk) * (Control Risk) * (Detection Risk)

Now, Inherent Risk * Control Risk = Risk of material misstatement.

Therefore, Audit Risk = Risk of material misstatement * Detection Risk

Inherent Risks arise because of proneness of an item of misstatement because of its nature. For

example, items which require estimations. (Wright 2016)

Control Risks arise due to the failure of internal control systems in preventing, detecting or correcting

misstatements. (Griffiths 2016)

Detection Risksarise when the auditor’s procedures and methods fail to detect the misstatements.

The goal of the Auditor is to reduce the overall audit risk to an acceptable level. They first assess the

levels of the various types of risks. These levels are not quantifiable and require professional judgement.

The risk value is thus assessed by descriptive means and not a mathematical formula. (Cannon and

Bedard 2016)

Risk of material misstatements which includes Inherent Risk and Control Risk are under the control of the

management of the company. The detection risk can be directly manipulated by the Auditor.

So, if in an audit scenario, the risks of material misstatements are high, the auditor must lessen the

detection risk to balance the overall audit risk at asatisfactory level. The detection risk can be influenced

by various means like changing the audit team’s composition, changing the procedures or duration of the

Audit Risk Model

It is an instrument used by Auditors to arrive at the affiliation among varieties of risk in an Audit

engagement. The model states that the overall risk is the product of the major components of risk that are

three in number. These components are Inherent Risk, Control Risk and Detection Risk. (Han, Rezaee, et

al. 2015)

It is embodied in equation form as:

Audit Risk = (Inherent Risk) * (Control Risk) * (Detection Risk)

Now, Inherent Risk * Control Risk = Risk of material misstatement.

Therefore, Audit Risk = Risk of material misstatement * Detection Risk

Inherent Risks arise because of proneness of an item of misstatement because of its nature. For

example, items which require estimations. (Wright 2016)

Control Risks arise due to the failure of internal control systems in preventing, detecting or correcting

misstatements. (Griffiths 2016)

Detection Risksarise when the auditor’s procedures and methods fail to detect the misstatements.

The goal of the Auditor is to reduce the overall audit risk to an acceptable level. They first assess the

levels of the various types of risks. These levels are not quantifiable and require professional judgement.

The risk value is thus assessed by descriptive means and not a mathematical formula. (Cannon and

Bedard 2016)

Risk of material misstatements which includes Inherent Risk and Control Risk are under the control of the

management of the company. The detection risk can be directly manipulated by the Auditor.

So, if in an audit scenario, the risks of material misstatements are high, the auditor must lessen the

detection risk to balance the overall audit risk at asatisfactory level. The detection risk can be influenced

by various means like changing the audit team’s composition, changing the procedures or duration of the

8Auditing

audit. Thus, detection risk and thereby audit risk can be reduced by employing skilled professionals in the

audit engagement team. (Boyle,DeZoort and Hermanson 2015)

In the given case of Angel Seafood Holding Pty. Ltd., the areas of risk of material misstatements include:

Existence and valuation of Biological Asset: The Company’s biological assets are the oysters

which the company measures at fair value less costs to sell. In the valuation method adopted, it is

very difficult to ascertain the fair value as it requires a lot of complex judgements and estimations

with respect to the inputs. The valuation technique adopted is such that it includes a lot of both

internal and external inputs which makes the valuation a complex method. (Rice, Roberts and

Fitzmaurice 2015)

Carrying value of intangible assets and property, plant and equipment: The Company has

Property, plant and equipment worth $ 3.4 million and intangible assets worth $ 2.7 million. If

recoverable value of these assets is to be ascertained, it would require exercising significant

judgement of factors such as the discount rate, inflation rates and future contract renewals. The

outcomes could vary drastically with different assumptions. Therefore, the audit of these assets is

a key concern. (Naidoo and Gasparatos 2018)

The above mentioned risks are those that has been highlighted by the existing auditors of Angel Seafood

Holding Pty. Ltd. There are other risks as well. The auditors need to apply professional scepticism and

due diligence in performing the audit of the company.

The factors that affect the Inherent risk and control risk i.e. the risk of material misstatements are:

Nature of Business: The nature of business of Angel Seafood Holding Pty Ltd. is such that it

deals in biological assets. The industry is affected by a lot of economic and environmental

factors. There could be new laws implemented from time to time or environmental concerns may

apply restrictions to the normal business operations.

Negative Reserves: The firm has been incurring losses since its inception. A negative cash flow

and reserves are matters of high concern as these affect the going concern of the entity. Losses

audit. Thus, detection risk and thereby audit risk can be reduced by employing skilled professionals in the

audit engagement team. (Boyle,DeZoort and Hermanson 2015)

In the given case of Angel Seafood Holding Pty. Ltd., the areas of risk of material misstatements include:

Existence and valuation of Biological Asset: The Company’s biological assets are the oysters

which the company measures at fair value less costs to sell. In the valuation method adopted, it is

very difficult to ascertain the fair value as it requires a lot of complex judgements and estimations

with respect to the inputs. The valuation technique adopted is such that it includes a lot of both

internal and external inputs which makes the valuation a complex method. (Rice, Roberts and

Fitzmaurice 2015)

Carrying value of intangible assets and property, plant and equipment: The Company has

Property, plant and equipment worth $ 3.4 million and intangible assets worth $ 2.7 million. If

recoverable value of these assets is to be ascertained, it would require exercising significant

judgement of factors such as the discount rate, inflation rates and future contract renewals. The

outcomes could vary drastically with different assumptions. Therefore, the audit of these assets is

a key concern. (Naidoo and Gasparatos 2018)

The above mentioned risks are those that has been highlighted by the existing auditors of Angel Seafood

Holding Pty. Ltd. There are other risks as well. The auditors need to apply professional scepticism and

due diligence in performing the audit of the company.

The factors that affect the Inherent risk and control risk i.e. the risk of material misstatements are:

Nature of Business: The nature of business of Angel Seafood Holding Pty Ltd. is such that it

deals in biological assets. The industry is affected by a lot of economic and environmental

factors. There could be new laws implemented from time to time or environmental concerns may

apply restrictions to the normal business operations.

Negative Reserves: The firm has been incurring losses since its inception. A negative cash flow

and reserves are matters of high concern as these affect the going concern of the entity. Losses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9Auditing

are highly risky as these reduce the credibility of the company because of which banks and

creditors may become less interested in investing.

On considering the above risk factors, we may assess the risk rating of Angel Seafood Holding Pty Ltd. to

be medium as the only major risk is in valuation of various assets. The negative reserves and cash flows

are a matter of time as these may improve with time. Since the business is relatively new, it needs to be

given time to expand its area of operations and earn revenues. Apart from these, there are no other major

areas of risk present in the company’s financial statements.

Since, the risk of material misstatements is medium, the detection risk should also be maintained at a

medium-low level. This shall balance the overall audit risk. The Audit engagement team appointed should

have expert professionals who can assess the fair value of the intangible and biological assets. Overall

Audit risk should be reduced as much possible.

are highly risky as these reduce the credibility of the company because of which banks and

creditors may become less interested in investing.

On considering the above risk factors, we may assess the risk rating of Angel Seafood Holding Pty Ltd. to

be medium as the only major risk is in valuation of various assets. The negative reserves and cash flows

are a matter of time as these may improve with time. Since the business is relatively new, it needs to be

given time to expand its area of operations and earn revenues. Apart from these, there are no other major

areas of risk present in the company’s financial statements.

Since, the risk of material misstatements is medium, the detection risk should also be maintained at a

medium-low level. This shall balance the overall audit risk. The Audit engagement team appointed should

have expert professionals who can assess the fair value of the intangible and biological assets. Overall

Audit risk should be reduced as much possible.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10Auditing

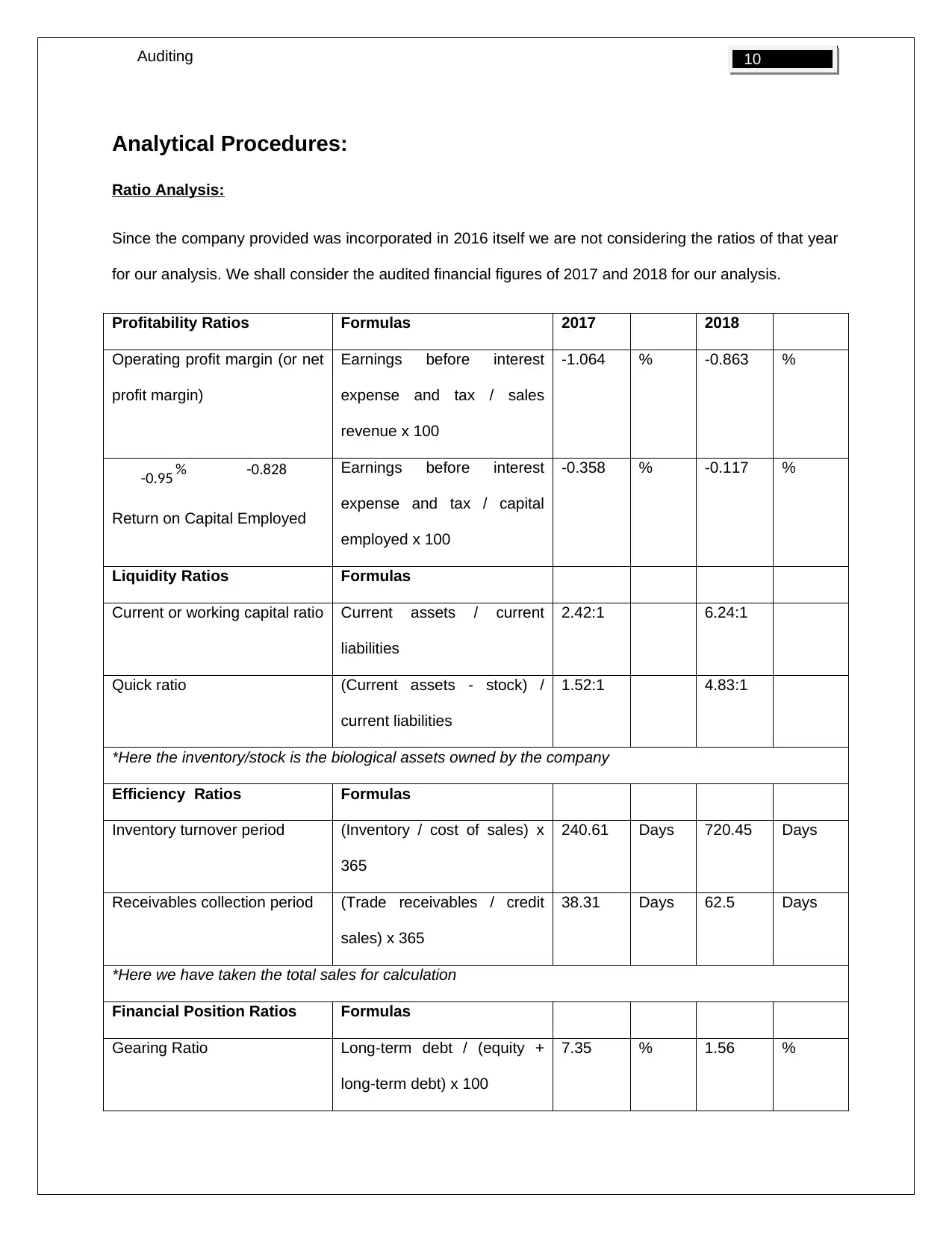

Analytical Procedures:

Ratio Analysis:

Since the company provided was incorporated in 2016 itself we are not considering the ratios of that year

for our analysis. We shall consider the audited financial figures of 2017 and 2018 for our analysis.

Profitability Ratios Formulas 2017 2018

Operating profit margin (or net

profit margin)

Earnings before interest

expense and tax / sales

revenue x 100

-1.064 % -0.863 %

-0.95 % -0.828

Return on Capital Employed

Earnings before interest

expense and tax / capital

employed x 100

-0.358 % -0.117 %

Liquidity Ratios Formulas

Current or working capital ratio Current assets / current

liabilities

2.42:1 6.24:1

Quick ratio (Current assets - stock) /

current liabilities

1.52:1 4.83:1

*Here the inventory/stock is the biological assets owned by the company

Efficiency Ratios Formulas

Inventory turnover period (Inventory / cost of sales) x

365

240.61 Days 720.45 Days

Receivables collection period (Trade receivables / credit

sales) x 365

38.31 Days 62.5 Days

*Here we have taken the total sales for calculation

Financial Position Ratios Formulas

Gearing Ratio Long-term debt / (equity +

long-term debt) x 100

7.35 % 1.56 %

Analytical Procedures:

Ratio Analysis:

Since the company provided was incorporated in 2016 itself we are not considering the ratios of that year

for our analysis. We shall consider the audited financial figures of 2017 and 2018 for our analysis.

Profitability Ratios Formulas 2017 2018

Operating profit margin (or net

profit margin)

Earnings before interest

expense and tax / sales

revenue x 100

-1.064 % -0.863 %

-0.95 % -0.828

Return on Capital Employed

Earnings before interest

expense and tax / capital

employed x 100

-0.358 % -0.117 %

Liquidity Ratios Formulas

Current or working capital ratio Current assets / current

liabilities

2.42:1 6.24:1

Quick ratio (Current assets - stock) /

current liabilities

1.52:1 4.83:1

*Here the inventory/stock is the biological assets owned by the company

Efficiency Ratios Formulas

Inventory turnover period (Inventory / cost of sales) x

365

240.61 Days 720.45 Days

Receivables collection period (Trade receivables / credit

sales) x 365

38.31 Days 62.5 Days

*Here we have taken the total sales for calculation

Financial Position Ratios Formulas

Gearing Ratio Long-term debt / (equity +

long-term debt) x 100

7.35 % 1.56 %

11Auditing

Analysis of 4 key ratios:

Operating Profit Margin: The operating profit margin of the company is negative because of losses.

Since the ratio has improved from 2017 to 2018, it shows that the company is taking efforts to yield higher

returns. Since, it is the beginning years of the company, this ratio needs to be analysed in depth in the

future years.

Current Ratio: The current ration of the company is very satisfactory. It meets the standard requirements

in 2017 and further improves in 2019.

Inventory turnover period: The inventory turnover days have increased to almost three times in a year.

This shows that the production is more than the sales. This is a serious cause of concern as it would lead

to stocking up of oysters in the company’s bays. Such stocking up has environmental concerns and legal

repercussions as well.

Gearing Ratio: The Gearing ratio of the company has enriched over the year. With a 7% debt in the

overall capital, the debt component has reduced drastically to 1.56%. This leads to reduction in interest

cost. A balance of debt and equity is required for every entity.

Analysis of 4 key ratios:

Operating Profit Margin: The operating profit margin of the company is negative because of losses.

Since the ratio has improved from 2017 to 2018, it shows that the company is taking efforts to yield higher

returns. Since, it is the beginning years of the company, this ratio needs to be analysed in depth in the

future years.

Current Ratio: The current ration of the company is very satisfactory. It meets the standard requirements

in 2017 and further improves in 2019.

Inventory turnover period: The inventory turnover days have increased to almost three times in a year.

This shows that the production is more than the sales. This is a serious cause of concern as it would lead

to stocking up of oysters in the company’s bays. Such stocking up has environmental concerns and legal

repercussions as well.

Gearing Ratio: The Gearing ratio of the company has enriched over the year. With a 7% debt in the

overall capital, the debt component has reduced drastically to 1.56%. This leads to reduction in interest

cost. A balance of debt and equity is required for every entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.