Holmes Institute: HA3032 Auditing - Risk, Materiality & Procedures

VerifiedAdded on 2023/06/04

|19

|4197

|466

Report

AI Summary

This report provides an analysis of audit risk and materiality for Resource Mining Limited, a company listed on the Australian Stock Exchange. It assesses the company's audit risk using the audit risk model, considering inherent, control, and detection risks. Analytical procedures, including liquidity, efficiency, profitability, and solvency ratios, are applied to evaluate the company's financial performance over three years. The report quantifies planning materiality based on total expenses and identifies material account balances such as cash, trade receivables, and plant and equipment. Financial reporting assertions related to these balances, including completeness, existence, and valuation, are examined, and appropriate audit procedures are suggested to address potential risks. The document concludes with a summary of the findings and recommendations. Desklib provides access to similar solved assignments for students.

HA3032 Auditing

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................3

DETAILS ABOUT THE COMPANY AND THE INDUSTRY...........................................................3

Nature of company................................................................................................................................3

AUDIT RISK MODE............................................................................................................................4

ANALYTICAL PROCEDURES...........................................................................................................5

QUANTIFYING THE PLANNING MATERIALITY..........................................................................8

MATERIAL ACCOUNT BALANCE LIST.........................................................................................9

FINANCIAL REPORTING ASSERTIONS RELATING TO ACCOUNT BALANCES THAT ARE

CONSIDERED MATERIAL..............................................................................................................10

USE OF SAMPLING TECHNIQUE...................................................................................................15

CONCLUSION...................................................................................................................................16

REFERENCES....................................................................................................................................17

2

INTRODUCTION.................................................................................................................................3

DETAILS ABOUT THE COMPANY AND THE INDUSTRY...........................................................3

Nature of company................................................................................................................................3

AUDIT RISK MODE............................................................................................................................4

ANALYTICAL PROCEDURES...........................................................................................................5

QUANTIFYING THE PLANNING MATERIALITY..........................................................................8

MATERIAL ACCOUNT BALANCE LIST.........................................................................................9

FINANCIAL REPORTING ASSERTIONS RELATING TO ACCOUNT BALANCES THAT ARE

CONSIDERED MATERIAL..............................................................................................................10

USE OF SAMPLING TECHNIQUE...................................................................................................15

CONCLUSION...................................................................................................................................16

REFERENCES....................................................................................................................................17

2

INTRODUCTION

The audit report of any organisation can be prepared by the auditor only when he is

able to gather sufficient and appropriate audit evidence. It is not possible to gather these

evidences without a proper audit planning. Proper audit plan envisages in it several kinds of

audit procedures. These range from simple trend analysis done with the help of analytical

procedures to complex financial assertion analysis that the management gives. All this

requires the auditor to define the scope of his work and get a clear understanding regarding

the operations of the entity. The report presented in the current phase deals with the same

issue of Resource Mining Limited (Byrnes, et. al 2018). A research has been made on the

company Resource Mining Corporation Limited. The basic concept relating to audit is

understood using the data and information available about the company from the annual

report published. The materiality for the audit purposes is established for the Resource

Mining Limited and the material account balances are identified. On the basis of this

identification further analysis is done for the assertions that the management has given

regarding those balances. The audit procedures required to remove any risk that lies in these

account balances are figured out with the relevant documentation purpose.

DETAILS ABOUT THE COMPANY AND THE INDUSTRY

The company Resource Mining Limited is listed on Australian Stock Exchange. The

industry in which the company is working is materials industry. The company is currently

listed with a market capitalisation of $2.96 million. It is an independently registered company

having operations related to mineral resources (Resource Mining Limited, (2017).

Nature of company

Resource Mining Limited is striving in the competition due to its innovative

marketing, technical and financial skills. The long term goal of the company lies on

construction of a strong business model lying on the development of minerals. The

sustainability of the company’ mission is in the use of the skills for creation of long lasting

wealth. Scientific innovation turns out to be the key strategy for the success of the company

(Resource Mining Limited, (2016).

3

The audit report of any organisation can be prepared by the auditor only when he is

able to gather sufficient and appropriate audit evidence. It is not possible to gather these

evidences without a proper audit planning. Proper audit plan envisages in it several kinds of

audit procedures. These range from simple trend analysis done with the help of analytical

procedures to complex financial assertion analysis that the management gives. All this

requires the auditor to define the scope of his work and get a clear understanding regarding

the operations of the entity. The report presented in the current phase deals with the same

issue of Resource Mining Limited (Byrnes, et. al 2018). A research has been made on the

company Resource Mining Corporation Limited. The basic concept relating to audit is

understood using the data and information available about the company from the annual

report published. The materiality for the audit purposes is established for the Resource

Mining Limited and the material account balances are identified. On the basis of this

identification further analysis is done for the assertions that the management has given

regarding those balances. The audit procedures required to remove any risk that lies in these

account balances are figured out with the relevant documentation purpose.

DETAILS ABOUT THE COMPANY AND THE INDUSTRY

The company Resource Mining Limited is listed on Australian Stock Exchange. The

industry in which the company is working is materials industry. The company is currently

listed with a market capitalisation of $2.96 million. It is an independently registered company

having operations related to mineral resources (Resource Mining Limited, (2017).

Nature of company

Resource Mining Limited is striving in the competition due to its innovative

marketing, technical and financial skills. The long term goal of the company lies on

construction of a strong business model lying on the development of minerals. The

sustainability of the company’ mission is in the use of the skills for creation of long lasting

wealth. Scientific innovation turns out to be the key strategy for the success of the company

(Resource Mining Limited, (2016).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT RISK MODE

This audit risk model analysis the risk associated with the particular audit activities.

Due to the complex business nature of Resource Mining Limited, this company will have

high detention, audit and control risk in its business functioning. It is analysed that company

audit risk would be high due to the high detention and control risk. This Resource Mining

Limited has high risk due to the increased business compliance program and strict regulatory

listing requirements. The audit risk may arise due to the increased complexity of the

undertaken work. The detention risk arise due to misstatement and manipulation made by

company in its financial statement. The control risk arise due to the error and fraud made by

the accountant while managing the business process of organization (Noreen, Brewer, and

Garrison, 2014).

Practical implication of the audit risk model in Resource Mining Limited

The practical implication of the audit risk in the Resource Mining Limited could be

done by implementing the audit risk model. The increased business compliance program and

strict regulatory listing requirements has forced company to set high detention and control

risk which will also eventually result to increased audit risk in the audit assessment program.

This has shown that there would be chances that material recorded in the books of account

may be wrong and misleading (Resource Mining Limited, (2017).

This could be determined on the basis of the audit risk model undertaken in this research

The control risk is high as company does not have any internal control department

which could assess the discrepancies and issues in its audit reporting frameworks.

The control risk could be set to .20 and in order to have to 10% audit risk, company would set

its detention risk 10%. It reflects that company could only have 10% audit risk in its audit

reporting frameworks due to its high control and detention risk

Audit Risk = Inherent Risk x Control Risk x Detection Risk

10% = 20% x .5%

4

This audit risk model analysis the risk associated with the particular audit activities.

Due to the complex business nature of Resource Mining Limited, this company will have

high detention, audit and control risk in its business functioning. It is analysed that company

audit risk would be high due to the high detention and control risk. This Resource Mining

Limited has high risk due to the increased business compliance program and strict regulatory

listing requirements. The audit risk may arise due to the increased complexity of the

undertaken work. The detention risk arise due to misstatement and manipulation made by

company in its financial statement. The control risk arise due to the error and fraud made by

the accountant while managing the business process of organization (Noreen, Brewer, and

Garrison, 2014).

Practical implication of the audit risk model in Resource Mining Limited

The practical implication of the audit risk in the Resource Mining Limited could be

done by implementing the audit risk model. The increased business compliance program and

strict regulatory listing requirements has forced company to set high detention and control

risk which will also eventually result to increased audit risk in the audit assessment program.

This has shown that there would be chances that material recorded in the books of account

may be wrong and misleading (Resource Mining Limited, (2017).

This could be determined on the basis of the audit risk model undertaken in this research

The control risk is high as company does not have any internal control department

which could assess the discrepancies and issues in its audit reporting frameworks.

The control risk could be set to .20 and in order to have to 10% audit risk, company would set

its detention risk 10%. It reflects that company could only have 10% audit risk in its audit

reporting frameworks due to its high control and detention risk

Audit Risk = Inherent Risk x Control Risk x Detection Risk

10% = 20% x .5%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20% = Detection Risk = .5%

.05%

The crux is that company could have 10% audit risk which company would have in audit risk

model (Srivenkataramana, 2018).

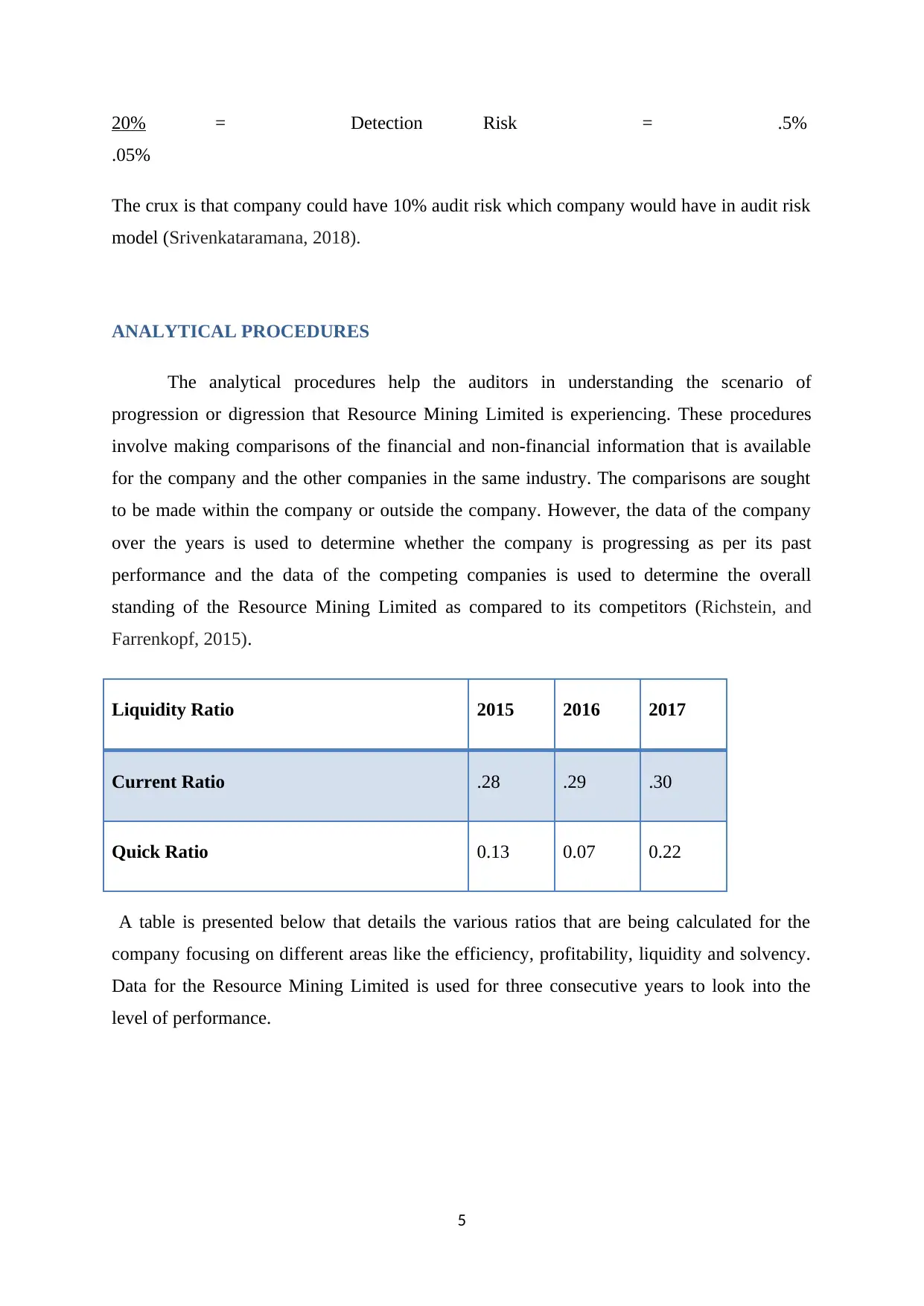

ANALYTICAL PROCEDURES

The analytical procedures help the auditors in understanding the scenario of

progression or digression that Resource Mining Limited is experiencing. These procedures

involve making comparisons of the financial and non-financial information that is available

for the company and the other companies in the same industry. The comparisons are sought

to be made within the company or outside the company. However, the data of the company

over the years is used to determine whether the company is progressing as per its past

performance and the data of the competing companies is used to determine the overall

standing of the Resource Mining Limited as compared to its competitors (Richstein, and

Farrenkopf, 2015).

Liquidity Ratio 2015 2016 2017

Current Ratio .28 .29 .30

Quick Ratio 0.13 0.07 0.22

A table is presented below that details the various ratios that are being calculated for the

company focusing on different areas like the efficiency, profitability, liquidity and solvency.

Data for the Resource Mining Limited is used for three consecutive years to look into the

level of performance.

5

.05%

The crux is that company could have 10% audit risk which company would have in audit risk

model (Srivenkataramana, 2018).

ANALYTICAL PROCEDURES

The analytical procedures help the auditors in understanding the scenario of

progression or digression that Resource Mining Limited is experiencing. These procedures

involve making comparisons of the financial and non-financial information that is available

for the company and the other companies in the same industry. The comparisons are sought

to be made within the company or outside the company. However, the data of the company

over the years is used to determine whether the company is progressing as per its past

performance and the data of the competing companies is used to determine the overall

standing of the Resource Mining Limited as compared to its competitors (Richstein, and

Farrenkopf, 2015).

Liquidity Ratio 2015 2016 2017

Current Ratio .28 .29 .30

Quick Ratio 0.13 0.07 0.22

A table is presented below that details the various ratios that are being calculated for the

company focusing on different areas like the efficiency, profitability, liquidity and solvency.

Data for the Resource Mining Limited is used for three consecutive years to look into the

level of performance.

5

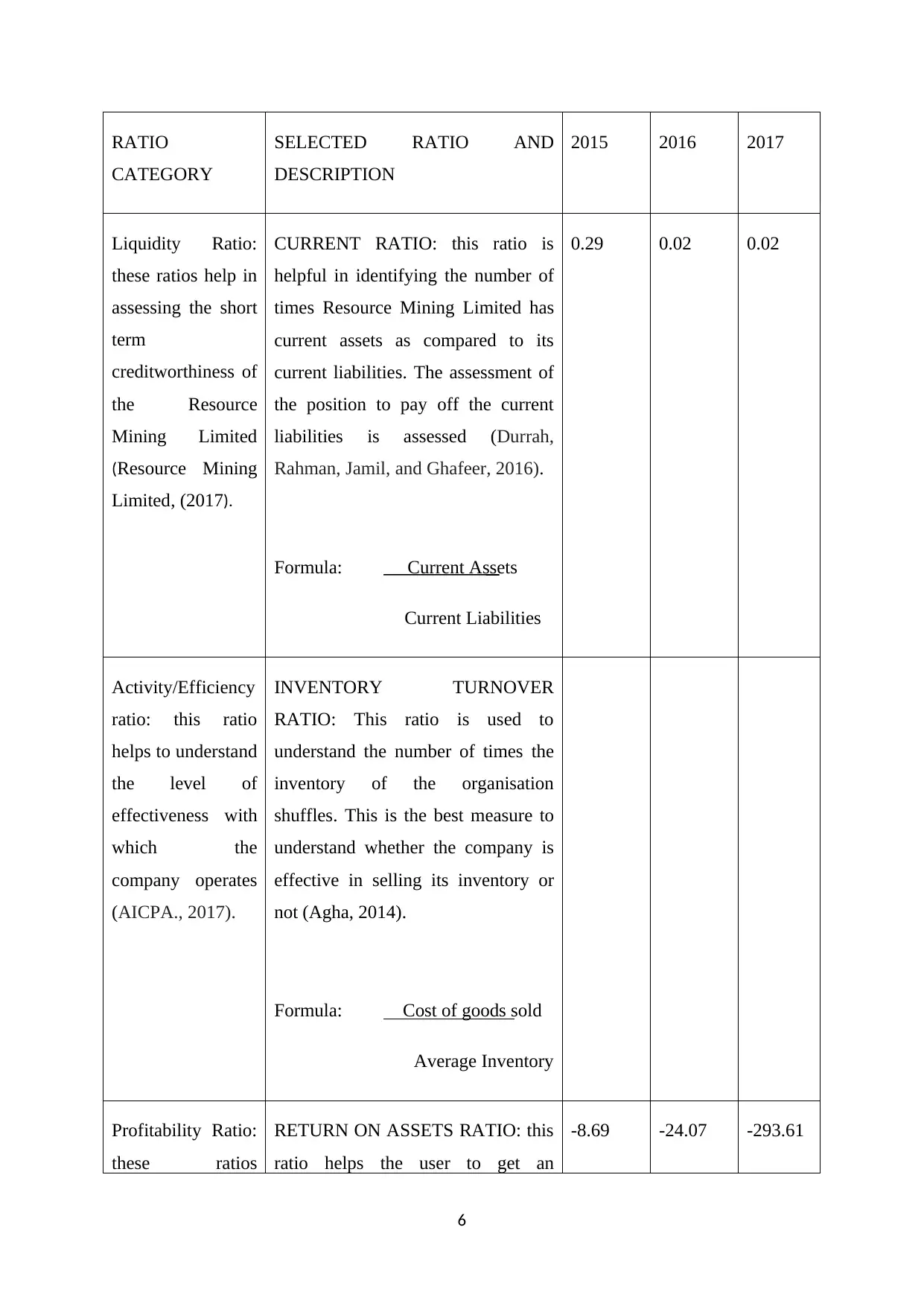

RATIO

CATEGORY

SELECTED RATIO AND

DESCRIPTION

2015 2016 2017

Liquidity Ratio:

these ratios help in

assessing the short

term

creditworthiness of

the Resource

Mining Limited

(Resource Mining

Limited, (2017).

CURRENT RATIO: this ratio is

helpful in identifying the number of

times Resource Mining Limited has

current assets as compared to its

current liabilities. The assessment of

the position to pay off the current

liabilities is assessed (Durrah,

Rahman, Jamil, and Ghafeer, 2016).

Formula: Current Assets

Current Liabilities

0.29 0.02 0.02

Activity/Efficiency

ratio: this ratio

helps to understand

the level of

effectiveness with

which the

company operates

(AICPA., 2017).

INVENTORY TURNOVER

RATIO: This ratio is used to

understand the number of times the

inventory of the organisation

shuffles. This is the best measure to

understand whether the company is

effective in selling its inventory or

not (Agha, 2014).

Formula: Cost of goods sold

Average Inventory

Profitability Ratio:

these ratios

RETURN ON ASSETS RATIO: this

ratio helps the user to get an

-8.69 -24.07 -293.61

6

CATEGORY

SELECTED RATIO AND

DESCRIPTION

2015 2016 2017

Liquidity Ratio:

these ratios help in

assessing the short

term

creditworthiness of

the Resource

Mining Limited

(Resource Mining

Limited, (2017).

CURRENT RATIO: this ratio is

helpful in identifying the number of

times Resource Mining Limited has

current assets as compared to its

current liabilities. The assessment of

the position to pay off the current

liabilities is assessed (Durrah,

Rahman, Jamil, and Ghafeer, 2016).

Formula: Current Assets

Current Liabilities

0.29 0.02 0.02

Activity/Efficiency

ratio: this ratio

helps to understand

the level of

effectiveness with

which the

company operates

(AICPA., 2017).

INVENTORY TURNOVER

RATIO: This ratio is used to

understand the number of times the

inventory of the organisation

shuffles. This is the best measure to

understand whether the company is

effective in selling its inventory or

not (Agha, 2014).

Formula: Cost of goods sold

Average Inventory

Profitability Ratio:

these ratios

RETURN ON ASSETS RATIO: this

ratio helps the user to get an

-8.69 -24.07 -293.61

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

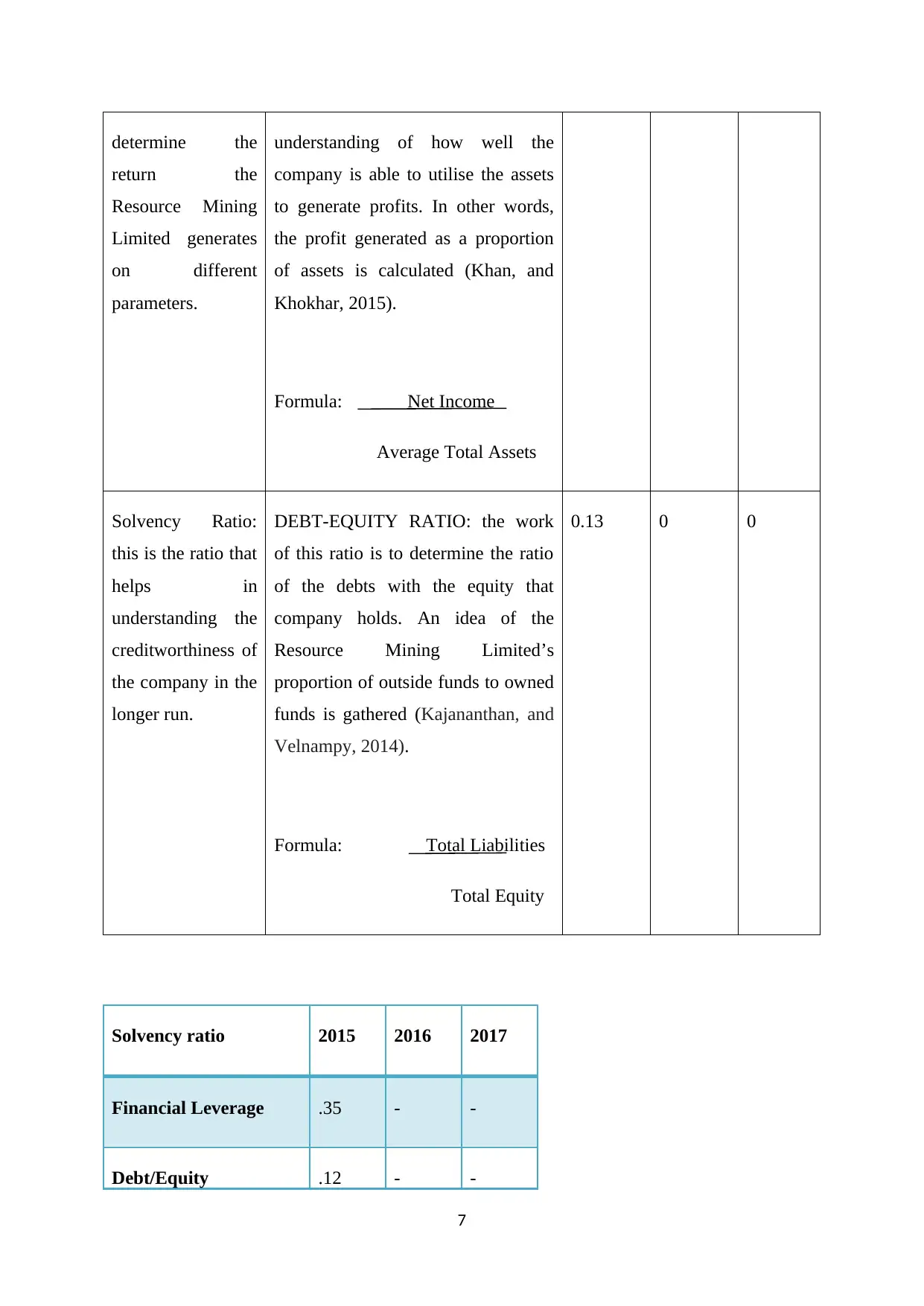

determine the

return the

Resource Mining

Limited generates

on different

parameters.

understanding of how well the

company is able to utilise the assets

to generate profits. In other words,

the profit generated as a proportion

of assets is calculated (Khan, and

Khokhar, 2015).

Formula: Net Income

Average Total Assets

Solvency Ratio:

this is the ratio that

helps in

understanding the

creditworthiness of

the company in the

longer run.

DEBT-EQUITY RATIO: the work

of this ratio is to determine the ratio

of the debts with the equity that

company holds. An idea of the

Resource Mining Limited’s

proportion of outside funds to owned

funds is gathered (Kajananthan, and

Velnampy, 2014).

Formula: Total Liabilities

Total Equity

0.13 0 0

Solvency ratio 2015 2016 2017

Financial Leverage .35 - -

Debt/Equity .12 - -

7

return the

Resource Mining

Limited generates

on different

parameters.

understanding of how well the

company is able to utilise the assets

to generate profits. In other words,

the profit generated as a proportion

of assets is calculated (Khan, and

Khokhar, 2015).

Formula: Net Income

Average Total Assets

Solvency Ratio:

this is the ratio that

helps in

understanding the

creditworthiness of

the company in the

longer run.

DEBT-EQUITY RATIO: the work

of this ratio is to determine the ratio

of the debts with the equity that

company holds. An idea of the

Resource Mining Limited’s

proportion of outside funds to owned

funds is gathered (Kajananthan, and

Velnampy, 2014).

Formula: Total Liabilities

Total Equity

0.13 0 0

Solvency ratio 2015 2016 2017

Financial Leverage .35 - -

Debt/Equity .12 - -

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above table analysis shows that the Resource Mining Limited is not working well

in any of the aspects. The profitability of the Resource Mining Limited is declining as well as

the operating effectiveness is also very low (Appelbaum, Kogan, and Vasarhelyi, (2018).

Profitability 2015 2016 2017

EPS -30.4 -39 -27

Net profit ratio -37.58 % -34.45% -31.96 %

EBIT -28 % -27% -26%

Return on assets -12% -20% -18%

Further the long term and short term creditworthiness is far from average.

QUANTIFYING THE PLANNING MATERIALITY

Any entity for which an external auditor is hired and the audit function is required to

be carried out, requires the auditor to classify the transactions. The classification becomes

must because of some inseparable limitations that the audit function carries. The time frame

given to complete an audit function is limited. Further, the company has too many

transactions going on (Resource Mining Limited, (2017). It is practically impossible for the

auditor to check all the transactions and events that are taking place in the company. At some

point certain level of segregation is required to be done. This segregation is possible only

when the auditor gets an understanding of the areas that are highly material and have the

ability to influence the decision that the users shall take (Baldauf, Steller, and Steckel, 2015).

8

in any of the aspects. The profitability of the Resource Mining Limited is declining as well as

the operating effectiveness is also very low (Appelbaum, Kogan, and Vasarhelyi, (2018).

Profitability 2015 2016 2017

EPS -30.4 -39 -27

Net profit ratio -37.58 % -34.45% -31.96 %

EBIT -28 % -27% -26%

Return on assets -12% -20% -18%

Further the long term and short term creditworthiness is far from average.

QUANTIFYING THE PLANNING MATERIALITY

Any entity for which an external auditor is hired and the audit function is required to

be carried out, requires the auditor to classify the transactions. The classification becomes

must because of some inseparable limitations that the audit function carries. The time frame

given to complete an audit function is limited. Further, the company has too many

transactions going on (Resource Mining Limited, (2017). It is practically impossible for the

auditor to check all the transactions and events that are taking place in the company. At some

point certain level of segregation is required to be done. This segregation is possible only

when the auditor gets an understanding of the areas that are highly material and have the

ability to influence the decision that the users shall take (Baldauf, Steller, and Steckel, 2015).

8

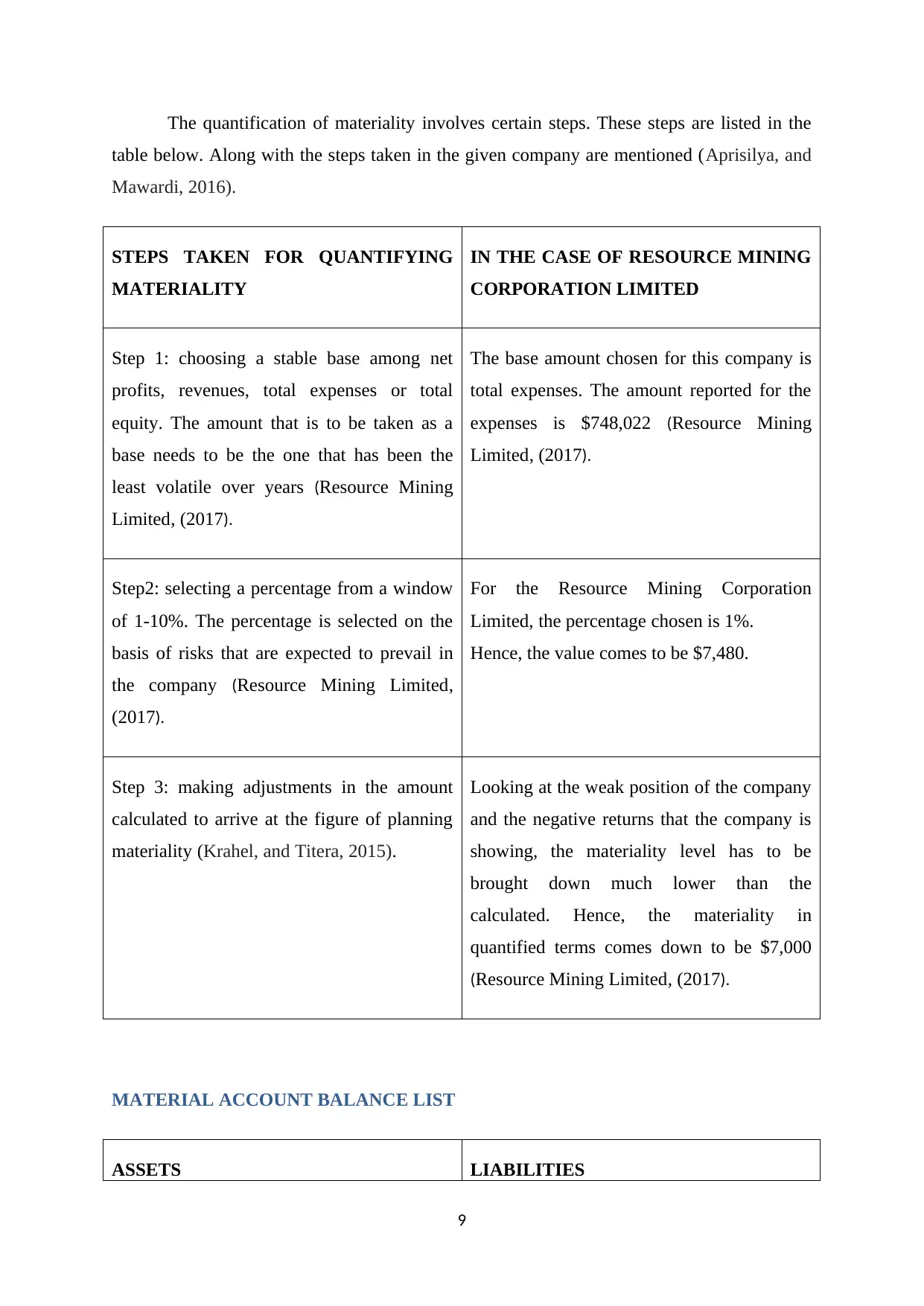

The quantification of materiality involves certain steps. These steps are listed in the

table below. Along with the steps taken in the given company are mentioned (Aprisilya, and

Mawardi, 2016).

STEPS TAKEN FOR QUANTIFYING

MATERIALITY

IN THE CASE OF RESOURCE MINING

CORPORATION LIMITED

Step 1: choosing a stable base among net

profits, revenues, total expenses or total

equity. The amount that is to be taken as a

base needs to be the one that has been the

least volatile over years (Resource Mining

Limited, (2017).

The base amount chosen for this company is

total expenses. The amount reported for the

expenses is $748,022 (Resource Mining

Limited, (2017).

Step2: selecting a percentage from a window

of 1-10%. The percentage is selected on the

basis of risks that are expected to prevail in

the company (Resource Mining Limited,

(2017).

For the Resource Mining Corporation

Limited, the percentage chosen is 1%.

Hence, the value comes to be $7,480.

Step 3: making adjustments in the amount

calculated to arrive at the figure of planning

materiality (Krahel, and Titera, 2015).

Looking at the weak position of the company

and the negative returns that the company is

showing, the materiality level has to be

brought down much lower than the

calculated. Hence, the materiality in

quantified terms comes down to be $7,000

(Resource Mining Limited, (2017).

MATERIAL ACCOUNT BALANCE LIST

ASSETS LIABILITIES

9

table below. Along with the steps taken in the given company are mentioned (Aprisilya, and

Mawardi, 2016).

STEPS TAKEN FOR QUANTIFYING

MATERIALITY

IN THE CASE OF RESOURCE MINING

CORPORATION LIMITED

Step 1: choosing a stable base among net

profits, revenues, total expenses or total

equity. The amount that is to be taken as a

base needs to be the one that has been the

least volatile over years (Resource Mining

Limited, (2017).

The base amount chosen for this company is

total expenses. The amount reported for the

expenses is $748,022 (Resource Mining

Limited, (2017).

Step2: selecting a percentage from a window

of 1-10%. The percentage is selected on the

basis of risks that are expected to prevail in

the company (Resource Mining Limited,

(2017).

For the Resource Mining Corporation

Limited, the percentage chosen is 1%.

Hence, the value comes to be $7,480.

Step 3: making adjustments in the amount

calculated to arrive at the figure of planning

materiality (Krahel, and Titera, 2015).

Looking at the weak position of the company

and the negative returns that the company is

showing, the materiality level has to be

brought down much lower than the

calculated. Hence, the materiality in

quantified terms comes down to be $7,000

(Resource Mining Limited, (2017).

MATERIAL ACCOUNT BALANCE LIST

ASSETS LIABILITIES

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

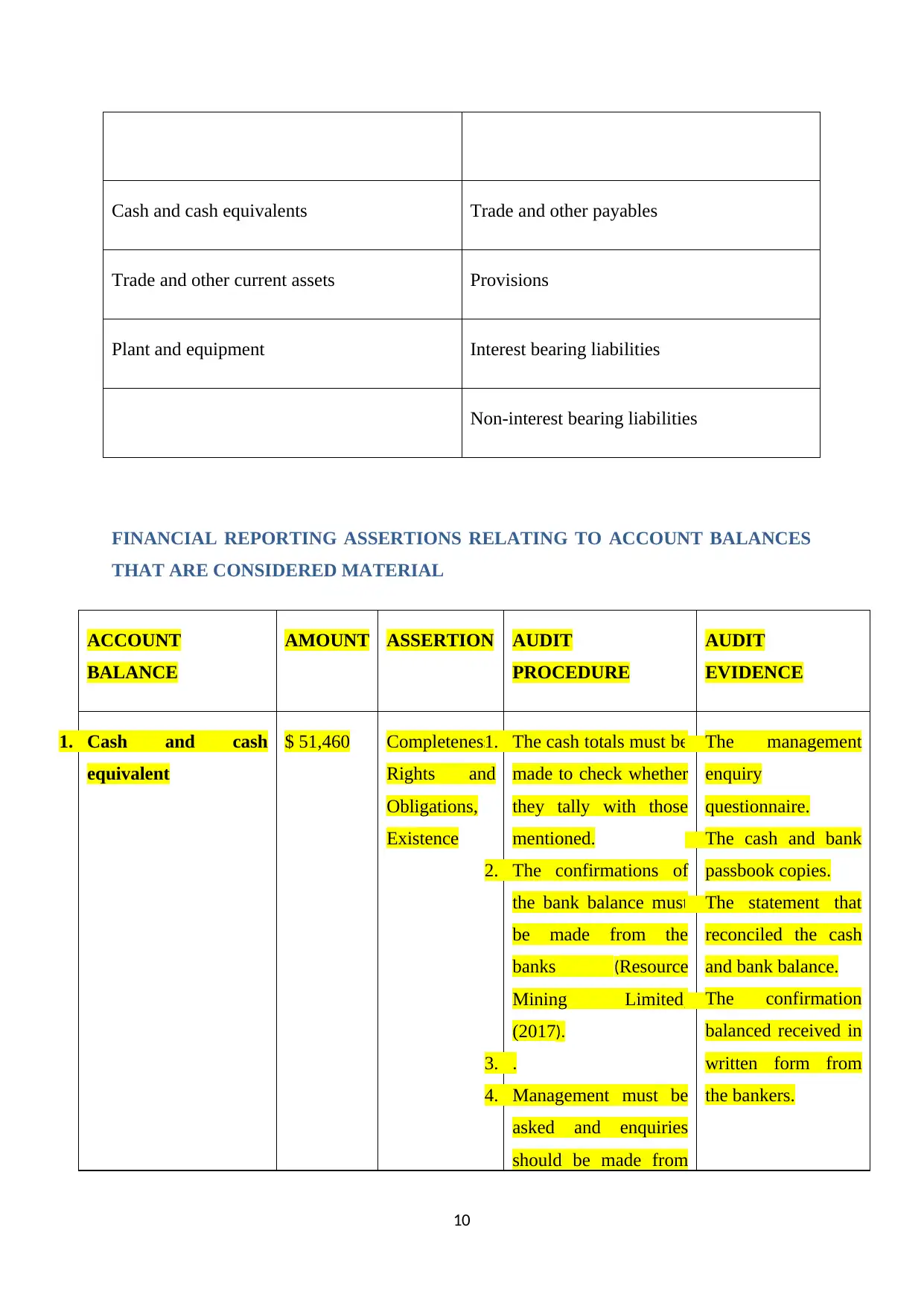

Cash and cash equivalents Trade and other payables

Trade and other current assets Provisions

Plant and equipment Interest bearing liabilities

Non-interest bearing liabilities

FINANCIAL REPORTING ASSERTIONS RELATING TO ACCOUNT BALANCES

THAT ARE CONSIDERED MATERIAL

ACCOUNT

BALANCE

AMOUNT ASSERTION AUDIT

PROCEDURE

AUDIT

EVIDENCE

1. Cash and cash

equivalent

$ 51,460 Completeness,

Rights and

Obligations,

Existence

1. The cash totals must be

made to check whether

they tally with those

mentioned.

2. The confirmations of

the bank balance must

be made from the

banks (Resource

Mining Limited,

(2017).

3. .

4. Management must be

asked and enquiries

should be made from

The management

enquiry

questionnaire.

The cash and bank

passbook copies.

The statement that

reconciled the cash

and bank balance.

The confirmation

balanced received in

written form from

the bankers.

10

Trade and other current assets Provisions

Plant and equipment Interest bearing liabilities

Non-interest bearing liabilities

FINANCIAL REPORTING ASSERTIONS RELATING TO ACCOUNT BALANCES

THAT ARE CONSIDERED MATERIAL

ACCOUNT

BALANCE

AMOUNT ASSERTION AUDIT

PROCEDURE

AUDIT

EVIDENCE

1. Cash and cash

equivalent

$ 51,460 Completeness,

Rights and

Obligations,

Existence

1. The cash totals must be

made to check whether

they tally with those

mentioned.

2. The confirmations of

the bank balance must

be made from the

banks (Resource

Mining Limited,

(2017).

3. .

4. Management must be

asked and enquiries

should be made from

The management

enquiry

questionnaire.

The cash and bank

passbook copies.

The statement that

reconciled the cash

and bank balance.

The confirmation

balanced received in

written form from

the bankers.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

them regarding the

major transactions

done in cash (Resource

Mining Limited,

(2016).

Goodwill 54254 Completeness,

Rights and

Obligations,

Existence

5. A statement must be

made which tallies and

reconciles the

revaluation of the

assets

Use of impairment

test.

Rights and obligations The entity is completely authorised and able to deploy the cash and bank

balance they have for the purpose of carrying on the entity’s business.

Completeness Any amount of cash or bank balance has not been missed. All the entries

have been counted and the final balance is provided.

Existence The cash that has been reported by the Resource Mining Limited is present

with it either in physical cash form or in the form of bank balance.

2. Trade and other

current assets

$ 21,145 Completeness,

existence,

valuation

1. The component of the

trade receivables of the

entity must be

confirmed by

requesting them to

make confirmations in

written form.

2. The details of the other

current assets must be

checked to identify the

nature of the assets and

The list of all the

assets that fall in this

account balance.

The confirmations

that the receivables

have provided.

The valuation

calculations made

by the management.

11

major transactions

done in cash (Resource

Mining Limited,

(2016).

Goodwill 54254 Completeness,

Rights and

Obligations,

Existence

5. A statement must be

made which tallies and

reconciles the

revaluation of the

assets

Use of impairment

test.

Rights and obligations The entity is completely authorised and able to deploy the cash and bank

balance they have for the purpose of carrying on the entity’s business.

Completeness Any amount of cash or bank balance has not been missed. All the entries

have been counted and the final balance is provided.

Existence The cash that has been reported by the Resource Mining Limited is present

with it either in physical cash form or in the form of bank balance.

2. Trade and other

current assets

$ 21,145 Completeness,

existence,

valuation

1. The component of the

trade receivables of the

entity must be

confirmed by

requesting them to

make confirmations in

written form.

2. The details of the other

current assets must be

checked to identify the

nature of the assets and

The list of all the

assets that fall in this

account balance.

The confirmations

that the receivables

have provided.

The valuation

calculations made

by the management.

11

the amount of

transactions happened

that involved them.

3. The value that has been

provided to the assets

under this balance

should be checked.

Existence The assets that have been mentioned are existent and available at the time of

balance sheet date.

Completeness All the other current assets and the receivables that should have been entered

in this list have been entered.

Valuation The valuation done for the elements of these account balances is reliable

(Resource Mining Limited, (2017).

3. Plants $ 142,283 Completeness,

existence,

valuation

1. There must be physical

inspection of the assets

that the entity has

listed.

2. The condition in which

the assets lay in the

company must be

checked to see whether

the valuation done has

been correct or not.

3.

.the report of

valuation provided

by the valuation

expert.

The commentary on

the physical

condition of the

assets.

4. equipment $52124 Completeness,

existence,

valuation

4. Help of experts of

valuation of tangible

assets must be taken to

The asset list of the

Resource Mining

12

transactions happened

that involved them.

3. The value that has been

provided to the assets

under this balance

should be checked.

Existence The assets that have been mentioned are existent and available at the time of

balance sheet date.

Completeness All the other current assets and the receivables that should have been entered

in this list have been entered.

Valuation The valuation done for the elements of these account balances is reliable

(Resource Mining Limited, (2017).

3. Plants $ 142,283 Completeness,

existence,

valuation

1. There must be physical

inspection of the assets

that the entity has

listed.

2. The condition in which

the assets lay in the

company must be

checked to see whether

the valuation done has

been correct or not.

3.

.the report of

valuation provided

by the valuation

expert.

The commentary on

the physical

condition of the

assets.

4. equipment $52124 Completeness,

existence,

valuation

4. Help of experts of

valuation of tangible

assets must be taken to

The asset list of the

Resource Mining

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.