HA3032 Auditing Report: Risk Assessment of Sultan Resources Limited

VerifiedAdded on 2022/11/14

|17

|4226

|405

Report

AI Summary

This report provides a comprehensive auditing analysis of Sultan Resources Limited, covering key aspects such as risk assessment, the audit risk model, and analytical procedures. It identifies various business risks, including market, credit, and liquidity risks. The report delves into the risk of material misstatement, differentiating between inherent, control, and detection risks. It employs the audit risk model to evaluate the interrelations among these risks. The analytical procedures section includes ratio analysis to assess the company's financial position. The report identifies material accounts, related assertions, and appropriate audit procedures, concluding with a sampling plan. Overall, the report offers a detailed overview of the audit process and its application to Sultan Resources Limited.

1

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The report has covered all the aspects in relation to the audit and its risk. There is the

determination of the various risks in the sultan resources limited. It has been identified that there

is a low level of risk which is involved and the analytical process is then followed. In that the

ratios have been calculated and by that the profitability and position of the business have been

evaluated. The audit risk model has been considered for the identification of the interrelations

which exists among all of the risks. The key material accounts have been identified the roper

assessment is made in relation to them. There is the identification of the assertions which are

related to them and in that the evidence and procedure which will be involved are identified. The

method of sampling which will be applicable has also be identified with the size of the sample

that will be used.

Executive summary

The report has covered all the aspects in relation to the audit and its risk. There is the

determination of the various risks in the sultan resources limited. It has been identified that there

is a low level of risk which is involved and the analytical process is then followed. In that the

ratios have been calculated and by that the profitability and position of the business have been

evaluated. The audit risk model has been considered for the identification of the interrelations

which exists among all of the risks. The key material accounts have been identified the roper

assessment is made in relation to them. There is the identification of the assertions which are

related to them and in that the evidence and procedure which will be involved are identified. The

method of sampling which will be applicable has also be identified with the size of the sample

that will be used.

3

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Overview of the company and Key business risks..........................................................................5

Risk of material misstatement.........................................................................................................5

Audit risk model..............................................................................................................................7

The analytical procedure of financial statements............................................................................8

Materiality........................................................................................................................................9

Material accounts, assertions, and audit procedures......................................................................10

Sampling plan................................................................................................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Overview of the company and Key business risks..........................................................................5

Risk of material misstatement.........................................................................................................5

Audit risk model..............................................................................................................................7

The analytical procedure of financial statements............................................................................8

Materiality........................................................................................................................................9

Material accounts, assertions, and audit procedures......................................................................10

Sampling plan................................................................................................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

In the business, there are various aspects which need to be evaluated and in that risk is the most

important. For the identification of the same there will be undertaking of the audit which will be

performed in the company in an effective manner. The report will be covering all of the aspects

in this respect with reference to the Sultan resources limited. All of the business risks which are

included will be identified and there will be proper description which will be provided. The risk

assessment will be made and in that there will be consideration which will be provided to the

inherent risk and control risk. The financial aspects of the business will also be required to be

evaluated and for that there will be undertaking of the ratio analysis. By the help of that the

profitability and financial position of the business will be analyzed. In the books there are

various material accounts and it is required that they all shall be taken into account in appropriate

manner. Ten accounts will be selected in the given case and then there will be determination of

the assertions which are related to them will be made. There will be specification of the audit

procedure which will be followed in respect of them. The sampling plane will also be provided

for them in which the manner in which samples will be selected is described.

Introduction

In the business, there are various aspects which need to be evaluated and in that risk is the most

important. For the identification of the same there will be undertaking of the audit which will be

performed in the company in an effective manner. The report will be covering all of the aspects

in this respect with reference to the Sultan resources limited. All of the business risks which are

included will be identified and there will be proper description which will be provided. The risk

assessment will be made and in that there will be consideration which will be provided to the

inherent risk and control risk. The financial aspects of the business will also be required to be

evaluated and for that there will be undertaking of the ratio analysis. By the help of that the

profitability and financial position of the business will be analyzed. In the books there are

various material accounts and it is required that they all shall be taken into account in appropriate

manner. Ten accounts will be selected in the given case and then there will be determination of

the assertions which are related to them will be made. There will be specification of the audit

procedure which will be followed in respect of them. The sampling plane will also be provided

for them in which the manner in which samples will be selected is described.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Overview of the company and Key business risks

The project is made in relation to the Sultan resources limited and this is the company which is

dealing in the mineral exploration activities. It is situated in Western Australia and covers the

projects which are related to the copper, cobalt, nickel, and gold. The listing of the company has

been made on 15 August 2018 in the Australian securities exchange (Sultan resource Limited,

2019). There are several projects which are undertaken by the company and on the license are

available and proper exploration is carried.

The company performs various tasks and in that, they are exposed to the risk which includes the

following:

Market risk: This is the risk which is to be borne by the company due to various market

circumstances. There are several changes which take place in the market such as the foreign

exchange risk which is due to the fluctuations in the market that are taking place in the exchange

rate. In addition to them, there is the interest rate risk which is involved. The value of the

financial instruments fluctuates with the change in the interest rate and it acts as the risk for the

business.

Credit risk: There are several financial assets in the company and the credit risk is involved in

relation to them. In the assets, there is the inclusion of the trade receivables, cash balance, and

many other assets. If there is any default which is made by the counterparty then the risk arises in

the company (Born and Pfeifer, 2014). The maximum amount of the risk involved in this will be

up to the carrying amount of the asset.

Liquidity risk: There are several liabilities which are required to be met by the company and in

case they are failed to be repaid then that will be considered as the risk of the company. Due to

this, it is required that the liquidity shall be maintained in the company by which it will be

possible to meet all the obligations on time. Cash reserves are maintained by the company and by

that it is able to avoid the liquidity risk which is involved.

Risk of material misstatement

A misstatement is an issue which is faced by the companies and in that there is the wrong entry

Overview of the company and Key business risks

The project is made in relation to the Sultan resources limited and this is the company which is

dealing in the mineral exploration activities. It is situated in Western Australia and covers the

projects which are related to the copper, cobalt, nickel, and gold. The listing of the company has

been made on 15 August 2018 in the Australian securities exchange (Sultan resource Limited,

2019). There are several projects which are undertaken by the company and on the license are

available and proper exploration is carried.

The company performs various tasks and in that, they are exposed to the risk which includes the

following:

Market risk: This is the risk which is to be borne by the company due to various market

circumstances. There are several changes which take place in the market such as the foreign

exchange risk which is due to the fluctuations in the market that are taking place in the exchange

rate. In addition to them, there is the interest rate risk which is involved. The value of the

financial instruments fluctuates with the change in the interest rate and it acts as the risk for the

business.

Credit risk: There are several financial assets in the company and the credit risk is involved in

relation to them. In the assets, there is the inclusion of the trade receivables, cash balance, and

many other assets. If there is any default which is made by the counterparty then the risk arises in

the company (Born and Pfeifer, 2014). The maximum amount of the risk involved in this will be

up to the carrying amount of the asset.

Liquidity risk: There are several liabilities which are required to be met by the company and in

case they are failed to be repaid then that will be considered as the risk of the company. Due to

this, it is required that the liquidity shall be maintained in the company by which it will be

possible to meet all the obligations on time. Cash reserves are maintained by the company and by

that it is able to avoid the liquidity risk which is involved.

Risk of material misstatement

A misstatement is an issue which is faced by the companies and in that there is the wrong entry

6

which is made in relation to the several account balances. This is the key risk and it is required

that they shall be identified and then the appropriate actions will be taken for the elimination of

them. It will be required to be ensured that the financial statements present the true picture of the

company. In this there are two categories which are involved and they are the inherent risk and

control risk.

Internal control is established in the company and in that there are various practices which are

followed. In some of the cases, it is weak and is not able to identify the mistakes which are made

in the reporting (Acharya and Naqvi, 2012). This is considered as the control risk and shall be

controlled. This is affected by the size of the transaction and also the internal conditions of the

business.

In the process of the reporting, there are several errors which are inherent and are not able to be

identified. They are due to the nature of the transaction and will be identified to be the inherent

risk. This will be existing in the business as it is inbuilt in the processes which are undertaken.

With reference to the above-identified two risks, there is another risk which is involved and that

is the detection risk. It is also the part of the audit risk which covered the chances that the other

risks will not be detected in the company. This will be changing with the change in the control

risk and so both are affected.

The business covers various such factors which affect the risk in the business and it is required

that proper consideration shall be paid to them. The inherent risk is inbuilt in the company and

that will be affected by the transactions which are taken and the liquidity which is involved in the

company. There are certain complex activities and processes which are performed and the

business will be affected by them and they will be increasing the risk which is involved (Chugh,

2016). They are required to be controlled as with them the business is affected in an adverse

manner. There is the chance of the increase in the errors which will be made and to avoid them

the risk will have to be controlled. In a similar manner, the control risk is also affected by various

aspects such as the environment in which the operations are carried by the business. The

monitoring process of the company shall be strong by which all of the errors which arise in the

business can be identified in effective manner. To control the risk all of the systems are to be

updated and by that the reporting will be made in the best manner and there will be reflection of

which is made in relation to the several account balances. This is the key risk and it is required

that they shall be identified and then the appropriate actions will be taken for the elimination of

them. It will be required to be ensured that the financial statements present the true picture of the

company. In this there are two categories which are involved and they are the inherent risk and

control risk.

Internal control is established in the company and in that there are various practices which are

followed. In some of the cases, it is weak and is not able to identify the mistakes which are made

in the reporting (Acharya and Naqvi, 2012). This is considered as the control risk and shall be

controlled. This is affected by the size of the transaction and also the internal conditions of the

business.

In the process of the reporting, there are several errors which are inherent and are not able to be

identified. They are due to the nature of the transaction and will be identified to be the inherent

risk. This will be existing in the business as it is inbuilt in the processes which are undertaken.

With reference to the above-identified two risks, there is another risk which is involved and that

is the detection risk. It is also the part of the audit risk which covered the chances that the other

risks will not be detected in the company. This will be changing with the change in the control

risk and so both are affected.

The business covers various such factors which affect the risk in the business and it is required

that proper consideration shall be paid to them. The inherent risk is inbuilt in the company and

that will be affected by the transactions which are taken and the liquidity which is involved in the

company. There are certain complex activities and processes which are performed and the

business will be affected by them and they will be increasing the risk which is involved (Chugh,

2016). They are required to be controlled as with them the business is affected in an adverse

manner. There is the chance of the increase in the errors which will be made and to avoid them

the risk will have to be controlled. In a similar manner, the control risk is also affected by various

aspects such as the environment in which the operations are carried by the business. The

monitoring process of the company shall be strong by which all of the errors which arise in the

business can be identified in effective manner. To control the risk all of the systems are to be

updated and by that the reporting will be made in the best manner and there will be reflection of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

the true position of business.

Audit risk model

Audit risk is the risk which is involved in the business and the auditor will be required to provide

with the opinion by considering them in the account. The complete audit risk comprises the three

elements which include the detection risk, inherent risk, and control risk. All of them will be

covered in this process and in that there will be identification of the relation which exists among

them. There is the audit risk model which is used and it can be described as:

Audit risk model = control risk X detection risk X inherent risk

In the initial stage, there are only two types of risks which are involved and they are the control

risk and inherent risk (Petraşcu and Tieanu, 2014). The material misstatement is made and that is

responsible for the inherent risk and if the control is not made in the same then it will result in

the control risk also. For that the control system of the company will be evaluated and there will

be establishment of the strong control. The auditor is the person who will be responsible for the

risk which is identified and therefore all of them together are determined to be the audit risk. The

auditor will be required to formulate such plan by which all of them will be taken into

consideration and they will be dealt in the most appropriate manner. There are certain situations

in which the risk which is involved is at higher level. In such cases it will be the duty of the

auditor to undertake the additional measures by which the risk can be controlled and the results

of the business can be improved. The evaluation of the complete situation will be made for the

identification of the involved risk together with the reasons which are responsible for the same.

The company involves the inherent risk and that will have to be controlled. If this is not made

then the control risk will be increasing. It will be required that there shall be proper detection of

the risk which is involved. The detection will be made and if the company is unable to identify

the risk then it will give rise to the detection risk. Due to this all of them are interrelated and will

be affecting each other. If the proper identification is made then the detection risk will be low

otherwise high.

Sultan resources have recently started its operations and due to that it has been identified that

there are fewer risks which are involved and the auditor has provided the unqualified report

the true position of business.

Audit risk model

Audit risk is the risk which is involved in the business and the auditor will be required to provide

with the opinion by considering them in the account. The complete audit risk comprises the three

elements which include the detection risk, inherent risk, and control risk. All of them will be

covered in this process and in that there will be identification of the relation which exists among

them. There is the audit risk model which is used and it can be described as:

Audit risk model = control risk X detection risk X inherent risk

In the initial stage, there are only two types of risks which are involved and they are the control

risk and inherent risk (Petraşcu and Tieanu, 2014). The material misstatement is made and that is

responsible for the inherent risk and if the control is not made in the same then it will result in

the control risk also. For that the control system of the company will be evaluated and there will

be establishment of the strong control. The auditor is the person who will be responsible for the

risk which is identified and therefore all of them together are determined to be the audit risk. The

auditor will be required to formulate such plan by which all of them will be taken into

consideration and they will be dealt in the most appropriate manner. There are certain situations

in which the risk which is involved is at higher level. In such cases it will be the duty of the

auditor to undertake the additional measures by which the risk can be controlled and the results

of the business can be improved. The evaluation of the complete situation will be made for the

identification of the involved risk together with the reasons which are responsible for the same.

The company involves the inherent risk and that will have to be controlled. If this is not made

then the control risk will be increasing. It will be required that there shall be proper detection of

the risk which is involved. The detection will be made and if the company is unable to identify

the risk then it will give rise to the detection risk. Due to this all of them are interrelated and will

be affecting each other. If the proper identification is made then the detection risk will be low

otherwise high.

Sultan resources have recently started its operations and due to that it has been identified that

there are fewer risks which are involved and the auditor has provided the unqualified report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

stating that there is the fair and true position which has been reflected (Huang et al., 2017). There

is a low level of the inherent risk which is involved and this shows that company has proper

control system which reduces the control risk as the internal control of the company is strong.

The detection risk will also be low as all of the risk will be identified by the internal control and

that will lower the risk of detection.

The analytical procedure of financial statements

Financial statement involves the financial information and it is required that the same shall be

presented in the appropriate manner. There is the need to carry the analysis of the information by

which the position of the business will be evaluated. There is the consideration of various aspects

in the same by which the performance and position will be measured. This can be done with the

help of the available techniques which there in this respect and one of them is ratio analysis

(Jans, Alles, and Vasarhelyi, 2014). This is the tool in which all of the information will be

considered and then the two aspects will be compared to ascertain the relation that exists among

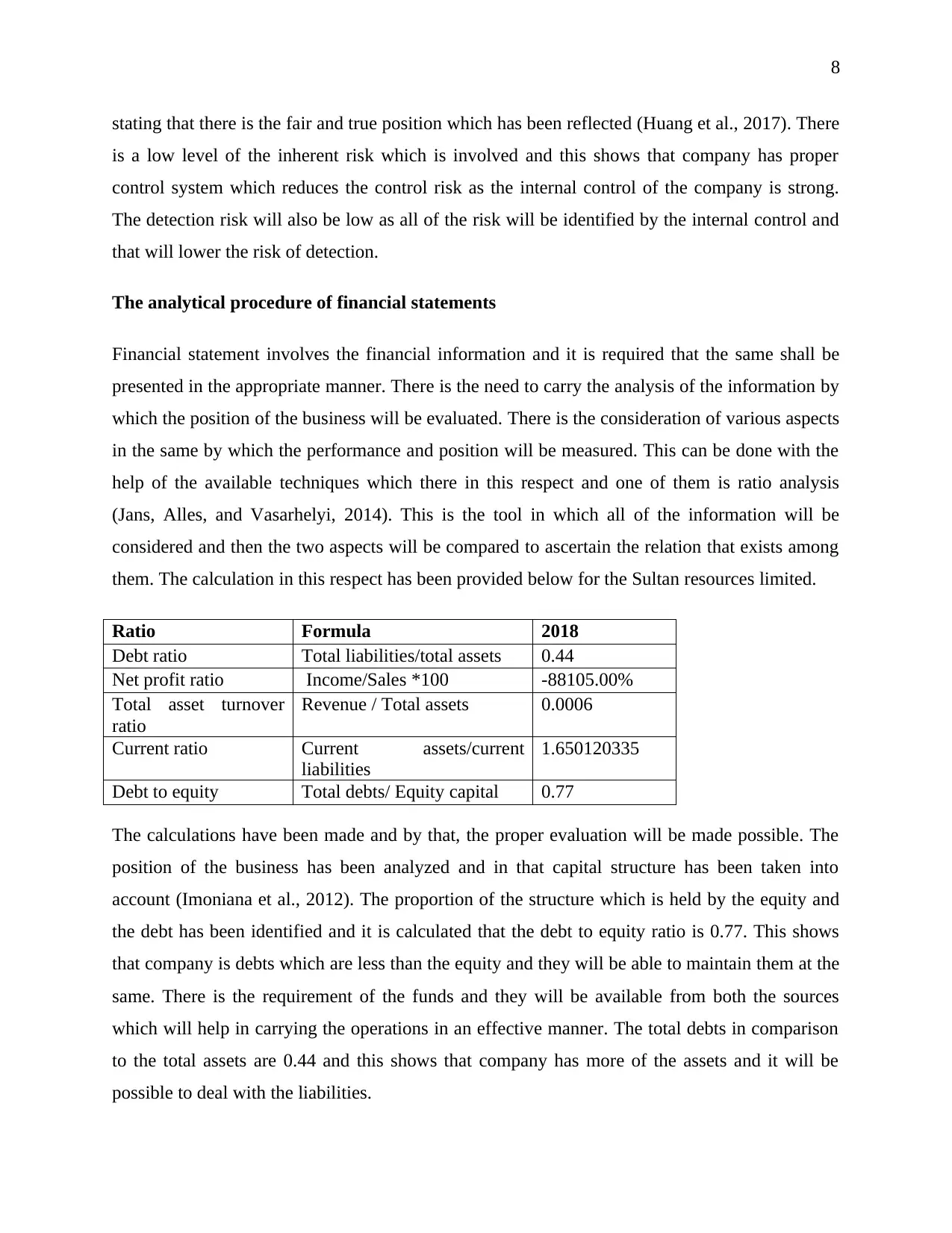

them. The calculation in this respect has been provided below for the Sultan resources limited.

Ratio Formula 2018

Debt ratio Total liabilities/total assets 0.44

Net profit ratio Income/Sales *100 -88105.00%

Total asset turnover

ratio

Revenue / Total assets 0.0006

Current ratio Current assets/current

liabilities

1.650120335

Debt to equity Total debts/ Equity capital 0.77

The calculations have been made and by that, the proper evaluation will be made possible. The

position of the business has been analyzed and in that capital structure has been taken into

account (Imoniana et al., 2012). The proportion of the structure which is held by the equity and

the debt has been identified and it is calculated that the debt to equity ratio is 0.77. This shows

that company is debts which are less than the equity and they will be able to maintain them at the

same. There is the requirement of the funds and they will be available from both the sources

which will help in carrying the operations in an effective manner. The total debts in comparison

to the total assets are 0.44 and this shows that company has more of the assets and it will be

possible to deal with the liabilities.

stating that there is the fair and true position which has been reflected (Huang et al., 2017). There

is a low level of the inherent risk which is involved and this shows that company has proper

control system which reduces the control risk as the internal control of the company is strong.

The detection risk will also be low as all of the risk will be identified by the internal control and

that will lower the risk of detection.

The analytical procedure of financial statements

Financial statement involves the financial information and it is required that the same shall be

presented in the appropriate manner. There is the need to carry the analysis of the information by

which the position of the business will be evaluated. There is the consideration of various aspects

in the same by which the performance and position will be measured. This can be done with the

help of the available techniques which there in this respect and one of them is ratio analysis

(Jans, Alles, and Vasarhelyi, 2014). This is the tool in which all of the information will be

considered and then the two aspects will be compared to ascertain the relation that exists among

them. The calculation in this respect has been provided below for the Sultan resources limited.

Ratio Formula 2018

Debt ratio Total liabilities/total assets 0.44

Net profit ratio Income/Sales *100 -88105.00%

Total asset turnover

ratio

Revenue / Total assets 0.0006

Current ratio Current assets/current

liabilities

1.650120335

Debt to equity Total debts/ Equity capital 0.77

The calculations have been made and by that, the proper evaluation will be made possible. The

position of the business has been analyzed and in that capital structure has been taken into

account (Imoniana et al., 2012). The proportion of the structure which is held by the equity and

the debt has been identified and it is calculated that the debt to equity ratio is 0.77. This shows

that company is debts which are less than the equity and they will be able to maintain them at the

same. There is the requirement of the funds and they will be available from both the sources

which will help in carrying the operations in an effective manner. The total debts in comparison

to the total assets are 0.44 and this shows that company has more of the assets and it will be

possible to deal with the liabilities.

9

The profitability of the company is required to be analyzed and for that various available

profitability ratios are calculated. In this, the ratio of the profits earned is calculated with respect

to the sales which are made in the company. In the current year company has made losses and

they are at high rate. The ratio is for -88105% which is a heavy loss that company will be

required to recover. The main reason for the loss is fewer amounts of the incomes which are

made by the company. Due to the fewer revenues and high costs, the loss has been incurred.

In the business, there are various obligations which are required to be met as and when they

arise. They are the ones which will be arising in the coming year and company will have to pay

them. For this the liquidity of the company will be analyzed in which the assets which are

maintained by the company will be evaluated. It will be identified that whether the company is

maintaining the required amount of the assets which are required to cover the liabilities. In this

there is the consideration of the current assets and current liabilities. For this purpose there is the

calculation of the current ratio and the same in the given case is derived to be 1.65 (Sultan

resource Limited, 2018). This is good and it shows that company has the required current assets

and will not be facing the issue in the making of the payment of the current liabilities. There will

be no overdue expenses which will be remaining in the company and it can be said that company

enjoys a strong liquidity position. The turnover ratio has been calculated in relation to the total

assets and it has been calculated to be 0.0006 which shows that there is not the proper turnover

which has been derived by the company. There is very less amount of the turnover which has

been earned with the help of the available assets. It can be seen that there is the amount which

has been invested by the company in the total assets but the company has made the proper

utilization of the same. If that would have been used then the revenues of the company would

have been high. Due to this it can be said that company is required to make the improvements in

the same.

Materiality

In the business, there are various accounts which are involved and out of them some are material

which will be affecting the decision making. They will be the ones in which error and

misstatement will be made and the position of the company will be affected. By the help of them

all of the information which is entered incorrectly will be taken into account so that the

The profitability of the company is required to be analyzed and for that various available

profitability ratios are calculated. In this, the ratio of the profits earned is calculated with respect

to the sales which are made in the company. In the current year company has made losses and

they are at high rate. The ratio is for -88105% which is a heavy loss that company will be

required to recover. The main reason for the loss is fewer amounts of the incomes which are

made by the company. Due to the fewer revenues and high costs, the loss has been incurred.

In the business, there are various obligations which are required to be met as and when they

arise. They are the ones which will be arising in the coming year and company will have to pay

them. For this the liquidity of the company will be analyzed in which the assets which are

maintained by the company will be evaluated. It will be identified that whether the company is

maintaining the required amount of the assets which are required to cover the liabilities. In this

there is the consideration of the current assets and current liabilities. For this purpose there is the

calculation of the current ratio and the same in the given case is derived to be 1.65 (Sultan

resource Limited, 2018). This is good and it shows that company has the required current assets

and will not be facing the issue in the making of the payment of the current liabilities. There will

be no overdue expenses which will be remaining in the company and it can be said that company

enjoys a strong liquidity position. The turnover ratio has been calculated in relation to the total

assets and it has been calculated to be 0.0006 which shows that there is not the proper turnover

which has been derived by the company. There is very less amount of the turnover which has

been earned with the help of the available assets. It can be seen that there is the amount which

has been invested by the company in the total assets but the company has made the proper

utilization of the same. If that would have been used then the revenues of the company would

have been high. Due to this it can be said that company is required to make the improvements in

the same.

Materiality

In the business, there are various accounts which are involved and out of them some are material

which will be affecting the decision making. They will be the ones in which error and

misstatement will be made and the position of the company will be affected. By the help of them

all of the information which is entered incorrectly will be taken into account so that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

elimination of the same is made possible. The materiality can be decided with the help of

auditing standard ASA 320 that is set in this respect and the auditor will be required to take that

into consideration (ASA 320, 2009). By the help of this material accounts will be identified and

there are certain factors which are incorporated to make the proper determination. In this process

there will be consideration of the value of the transaction which is taking place. There are certain

events in which huge amount is invested and they are identified to be the material accounts as

they will be affecting the overall position of the business. There is a change to misstate them so

that the financial position of the company can be shown as better (Han et al., 2015). The nature

in respect of the account will be taken into account and by that the materiality will be

ascertained. There will be proper process which will be used in this as it will be difficult to

identify all of the accounts which are material. After this the errors will be identified and the

corrective measures will be taken to make the corrections in them.

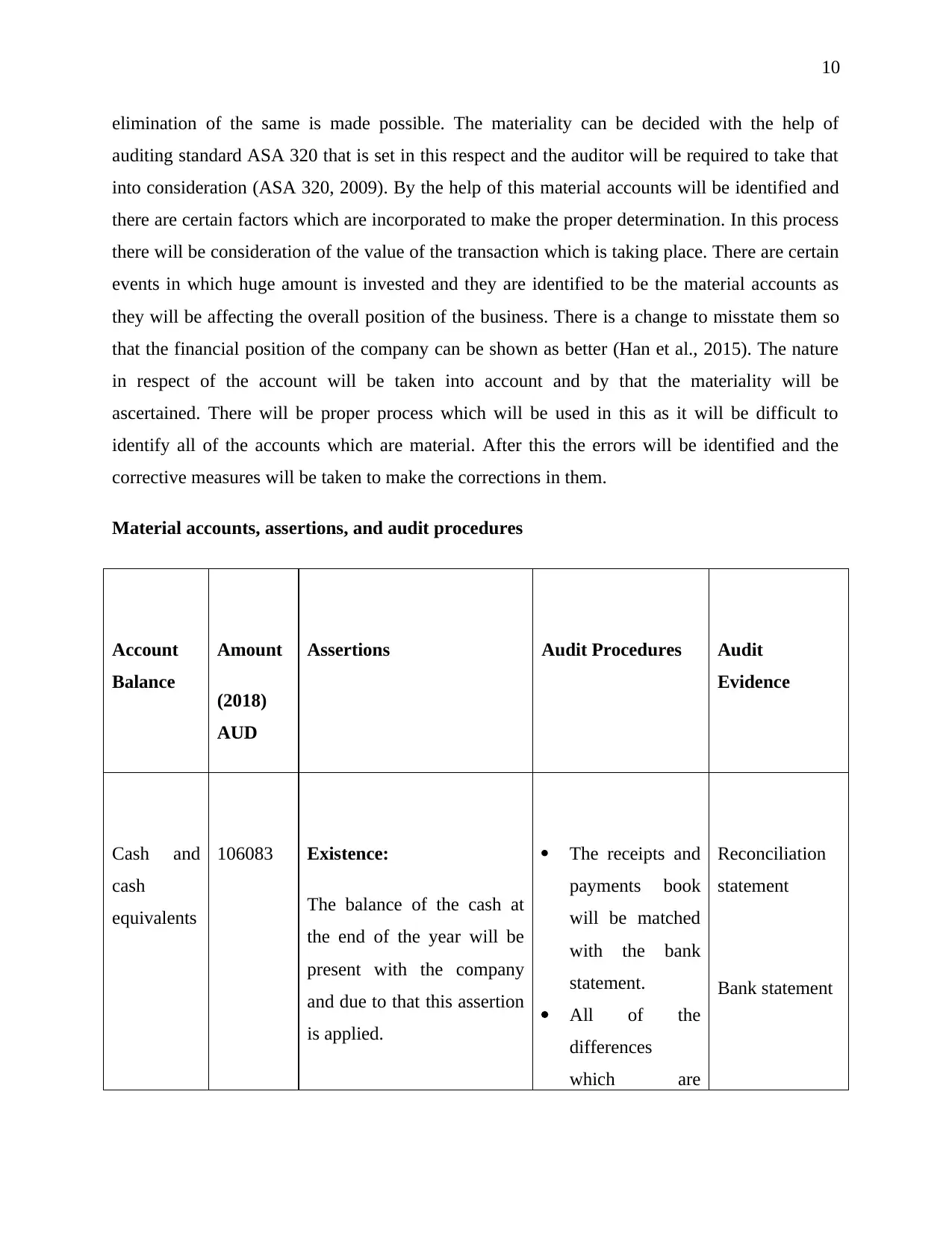

Material accounts, assertions, and audit procedures

Account

Balance

Amount

(2018)

AUD

Assertions Audit Procedures Audit

Evidence

Cash and

cash

equivalents

106083 Existence:

The balance of the cash at

the end of the year will be

present with the company

and due to that this assertion

is applied.

The receipts and

payments book

will be matched

with the bank

statement.

All of the

differences

which are

Reconciliation

statement

Bank statement

elimination of the same is made possible. The materiality can be decided with the help of

auditing standard ASA 320 that is set in this respect and the auditor will be required to take that

into consideration (ASA 320, 2009). By the help of this material accounts will be identified and

there are certain factors which are incorporated to make the proper determination. In this process

there will be consideration of the value of the transaction which is taking place. There are certain

events in which huge amount is invested and they are identified to be the material accounts as

they will be affecting the overall position of the business. There is a change to misstate them so

that the financial position of the company can be shown as better (Han et al., 2015). The nature

in respect of the account will be taken into account and by that the materiality will be

ascertained. There will be proper process which will be used in this as it will be difficult to

identify all of the accounts which are material. After this the errors will be identified and the

corrective measures will be taken to make the corrections in them.

Material accounts, assertions, and audit procedures

Account

Balance

Amount

(2018)

AUD

Assertions Audit Procedures Audit

Evidence

Cash and

cash

equivalents

106083 Existence:

The balance of the cash at

the end of the year will be

present with the company

and due to that this assertion

is applied.

The receipts and

payments book

will be matched

with the bank

statement.

All of the

differences

which are

Reconciliation

statement

Bank statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

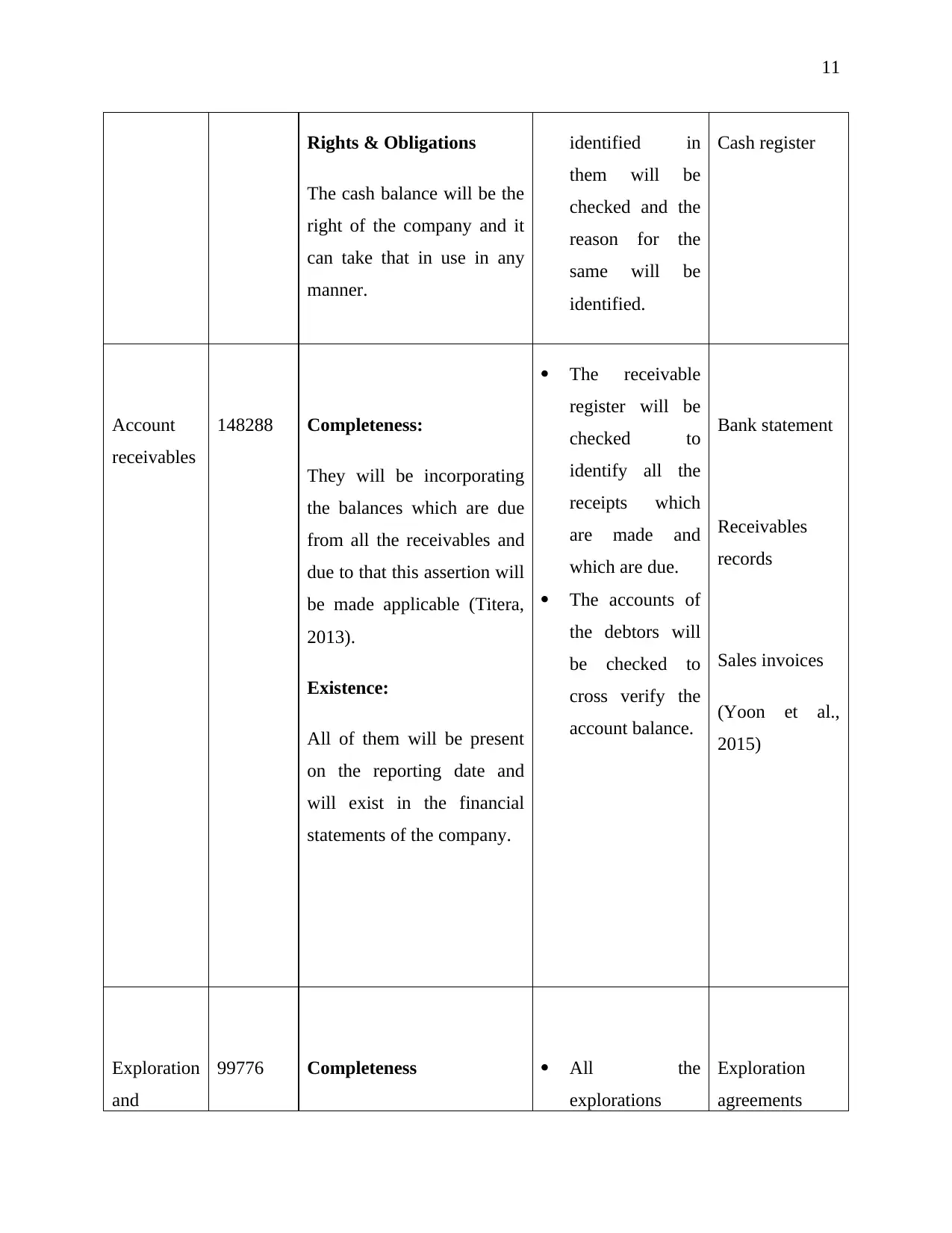

Rights & Obligations

The cash balance will be the

right of the company and it

can take that in use in any

manner.

identified in

them will be

checked and the

reason for the

same will be

identified.

Cash register

Account

receivables

148288 Completeness:

They will be incorporating

the balances which are due

from all the receivables and

due to that this assertion will

be made applicable (Titera,

2013).

Existence:

All of them will be present

on the reporting date and

will exist in the financial

statements of the company.

The receivable

register will be

checked to

identify all the

receipts which

are made and

which are due.

The accounts of

the debtors will

be checked to

cross verify the

account balance.

Bank statement

Receivables

records

Sales invoices

(Yoon et al.,

2015)

Exploration

and

99776 Completeness All the

explorations

Exploration

agreements

Rights & Obligations

The cash balance will be the

right of the company and it

can take that in use in any

manner.

identified in

them will be

checked and the

reason for the

same will be

identified.

Cash register

Account

receivables

148288 Completeness:

They will be incorporating

the balances which are due

from all the receivables and

due to that this assertion will

be made applicable (Titera,

2013).

Existence:

All of them will be present

on the reporting date and

will exist in the financial

statements of the company.

The receivable

register will be

checked to

identify all the

receipts which

are made and

which are due.

The accounts of

the debtors will

be checked to

cross verify the

account balance.

Bank statement

Receivables

records

Sales invoices

(Yoon et al.,

2015)

Exploration

and

99776 Completeness All the

explorations

Exploration

agreements

12

evaluation They are the non-current

assets which will be reported

in the financial statements.

Valuation

They will be valued as per

the specified methods and

policies.

which have been

done will be

evaluated.

The documents

which are

available will be

analyzed.

All the laws and

their

applicability will

be cross-

checked.

Payments

which are made

in this respect

Liability accounts

Trade and

other

payables

153240 Completeness:

There will be various

creditors and the balance of

all will be included

Existence:

They are the obligation of

the company which exists at

the year and end and will be

required to be borne in the

coming year.

The purchase

invoices will be

checked with the

register to ensure

correct entries

are made.

The bank

statement will be

evaluated to

identify the

payments which

have been made.

Purchase

invoices

Bank statement

creditor sheets

evaluation They are the non-current

assets which will be reported

in the financial statements.

Valuation

They will be valued as per

the specified methods and

policies.

which have been

done will be

evaluated.

The documents

which are

available will be

analyzed.

All the laws and

their

applicability will

be cross-

checked.

Payments

which are made

in this respect

Liability accounts

Trade and

other

payables

153240 Completeness:

There will be various

creditors and the balance of

all will be included

Existence:

They are the obligation of

the company which exists at

the year and end and will be

required to be borne in the

coming year.

The purchase

invoices will be

checked with the

register to ensure

correct entries

are made.

The bank

statement will be

evaluated to

identify the

payments which

have been made.

Purchase

invoices

Bank statement

creditor sheets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.