HA3042 Taxation Law - Fringe Benefits and Capital Gains Analysis

VerifiedAdded on 2023/03/30

|11

|2302

|227

Case Study

AI Summary

This case study delves into Australian taxation law, specifically focusing on fringe benefits tax (FBT) and capital gains tax (CGT). The first part analyzes the consequences of fringe benefits received through operating cost and statutory cost methods, detailing calculations for car fringe benefits and determining the more beneficial method. The second part examines capital gains events related to the sale of a house, a painting, and a luxury yacht, considering CGT implications, exemptions, and cost base calculations. Each scenario applies relevant sections of the ITAA 1997 and FBTAA 1986 to determine taxable amounts and potential discounts or disregarded losses. Desklib offers a wealth of similar resources for students seeking assistance with their studies.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Taxation Law

Name of the Student

Name of the University

Authors Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer 1

In the present case study, issue is that the determination of the consequences of fringe

benefit obtained by the method of operating cost and method of statutory cost respectively.

The Fringe Benefit Tax in Australia has been dealt with in the Fringe benefits Tax

assessment Act 1986. As per s136 (1) of the said act, FBT is one of the benefits given to an

associate or an employee at a particular time, once in a year. The said phenomenon takes

place in respect of a financial year beginning with 1st of April to 31st of March of the

following year (Barkoczy 2016). FBT is one of the taxes which needs to be paid by the

employer and its gross up rate for 2018- 2019 financial year is 2.0802 and the rate is 47%.

Type 1 benefit is a benefit in which the Input Tax Credit can be claimed by an employer.

Section 7 of FBTAA throws light to Car Fringe benefits. This occurs when a car is

received by an employee from the employer for personal use.CFB can be found to be

calculated by using two different ways. Firstly, the statutory formula method defined under

the provision enumerated in Section 9(1) of FBTAA and secondly, the method of Operating

Costs enumerated under section 10(2) of FBTAA.

The statutory formula method is (0.2 * Base value of the received car * the total

number of days of year when the employee is provided the CFB / Total Taxable days of the

year)- the total payment amount of the recipient.

Under the method of operating cost; the formula is C * (100%-BP) – R,

where C denotes the cost of operation during the period of hold and it includes fuel

price, maintenance charge, registration fee and insurance payment as per s 10(3)(a). BP

denotes the percentage of business and R denotes the contribution, if any, made by the

Answer 1

In the present case study, issue is that the determination of the consequences of fringe

benefit obtained by the method of operating cost and method of statutory cost respectively.

The Fringe Benefit Tax in Australia has been dealt with in the Fringe benefits Tax

assessment Act 1986. As per s136 (1) of the said act, FBT is one of the benefits given to an

associate or an employee at a particular time, once in a year. The said phenomenon takes

place in respect of a financial year beginning with 1st of April to 31st of March of the

following year (Barkoczy 2016). FBT is one of the taxes which needs to be paid by the

employer and its gross up rate for 2018- 2019 financial year is 2.0802 and the rate is 47%.

Type 1 benefit is a benefit in which the Input Tax Credit can be claimed by an employer.

Section 7 of FBTAA throws light to Car Fringe benefits. This occurs when a car is

received by an employee from the employer for personal use.CFB can be found to be

calculated by using two different ways. Firstly, the statutory formula method defined under

the provision enumerated in Section 9(1) of FBTAA and secondly, the method of Operating

Costs enumerated under section 10(2) of FBTAA.

The statutory formula method is (0.2 * Base value of the received car * the total

number of days of year when the employee is provided the CFB / Total Taxable days of the

year)- the total payment amount of the recipient.

Under the method of operating cost; the formula is C * (100%-BP) – R,

where C denotes the cost of operation during the period of hold and it includes fuel

price, maintenance charge, registration fee and insurance payment as per s 10(3)(a). BP

denotes the percentage of business and R denotes the contribution, if any, made by the

2TAXATION LAW

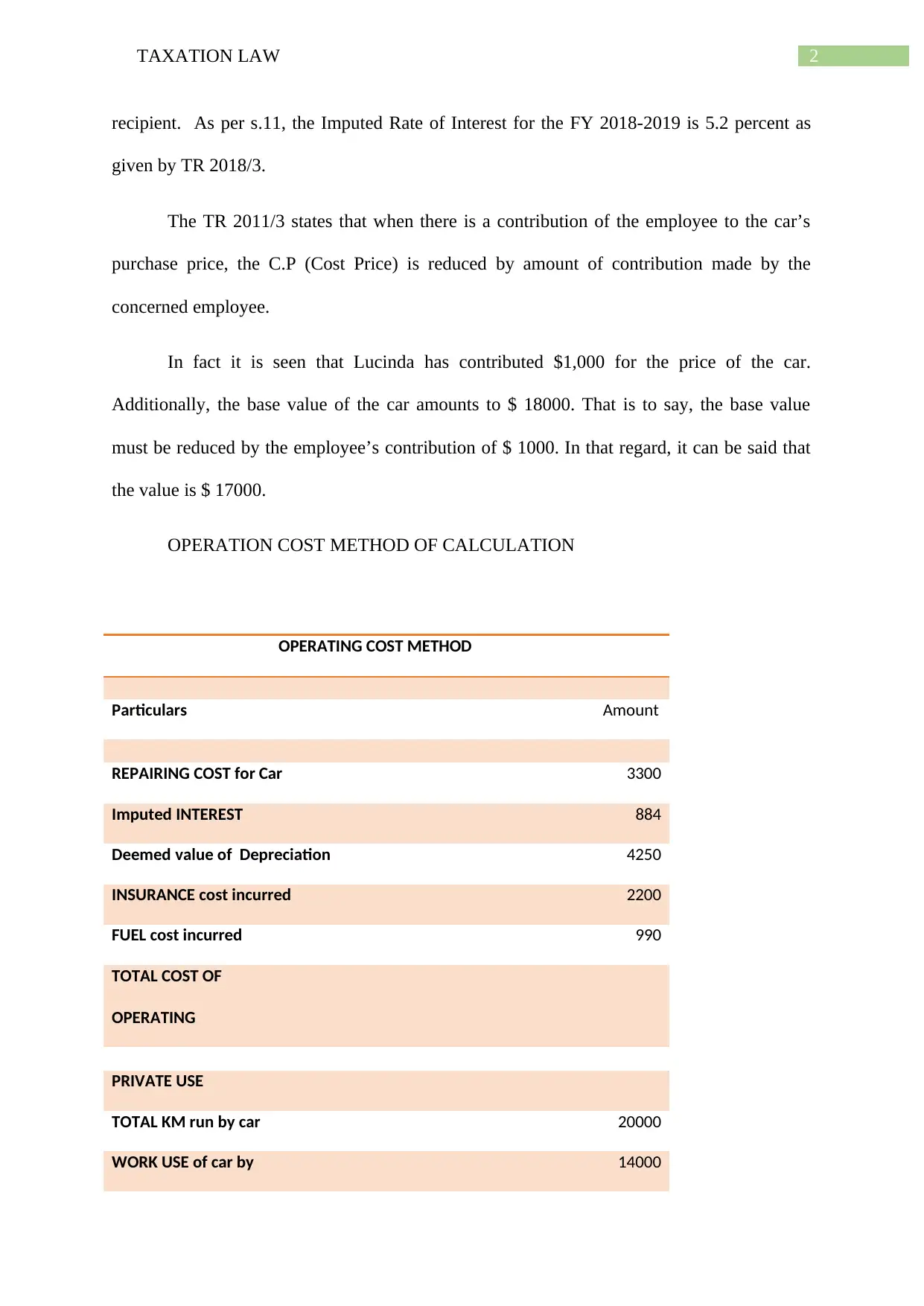

recipient. As per s.11, the Imputed Rate of Interest for the FY 2018-2019 is 5.2 percent as

given by TR 2018/3.

The TR 2011/3 states that when there is a contribution of the employee to the car’s

purchase price, the C.P (Cost Price) is reduced by amount of contribution made by the

concerned employee.

In fact it is seen that Lucinda has contributed $1,000 for the price of the car.

Additionally, the base value of the car amounts to $ 18000. That is to say, the base value

must be reduced by the employee’s contribution of $ 1000. In that regard, it can be said that

the value is $ 17000.

OPERATION COST METHOD OF CALCULATION

OPERATING COST METHOD

Particulars Amount

REPAIRING COST for Car 3300

Imputed INTEREST 884

Deemed value of Depreciation 4250

INSURANCE cost incurred 2200

FUEL cost incurred 990

TOTAL COST OF

OPERATING

PRIVATE USE

TOTAL KM run by car 20000

WORK USE of car by 14000

recipient. As per s.11, the Imputed Rate of Interest for the FY 2018-2019 is 5.2 percent as

given by TR 2018/3.

The TR 2011/3 states that when there is a contribution of the employee to the car’s

purchase price, the C.P (Cost Price) is reduced by amount of contribution made by the

concerned employee.

In fact it is seen that Lucinda has contributed $1,000 for the price of the car.

Additionally, the base value of the car amounts to $ 18000. That is to say, the base value

must be reduced by the employee’s contribution of $ 1000. In that regard, it can be said that

the value is $ 17000.

OPERATION COST METHOD OF CALCULATION

OPERATING COST METHOD

Particulars Amount

REPAIRING COST for Car 3300

Imputed INTEREST 884

Deemed value of Depreciation 4250

INSURANCE cost incurred 2200

FUEL cost incurred 990

TOTAL COST OF

OPERATING

PRIVATE USE

TOTAL KM run by car 20000

WORK USE of car by 14000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

employee

PRIVATE USAGE by

employee

6000

PRIVATE USE PERCENTAGE 30

Taxable FBT value

(TOC*PRIVATE USE) 3487.2

Deemeed Depreciation Amount

Cost Value of Car 18000

Employee's constibution 1000 TR

2011/3

Base Value 17000

Depreciation rate 25%

Deemed Depeciation

(BV*25%*365)/365 4250

Imputed Interest Amount

Car Base Value 18000

Less Employee contribution 1000 TR

2011/3

Base Value 17000

employee

PRIVATE USAGE by

employee

6000

PRIVATE USE PERCENTAGE 30

Taxable FBT value

(TOC*PRIVATE USE) 3487.2

Deemeed Depreciation Amount

Cost Value of Car 18000

Employee's constibution 1000 TR

2011/3

Base Value 17000

Depreciation rate 25%

Deemed Depeciation

(BV*25%*365)/365 4250

Imputed Interest Amount

Car Base Value 18000

Less Employee contribution 1000 TR

2011/3

Base Value 17000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

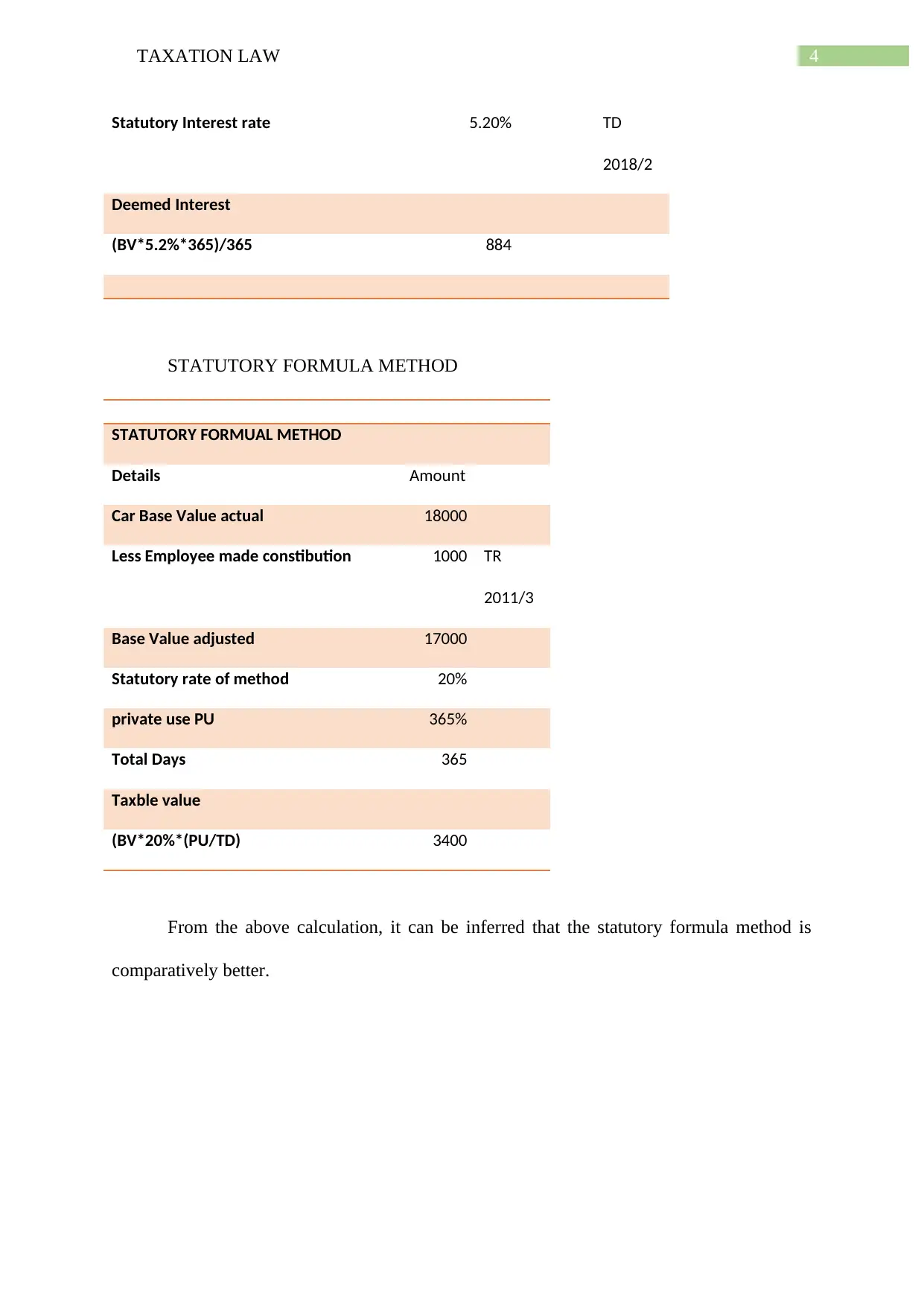

Statutory Interest rate 5.20% TD

2018/2

Deemed Interest

(BV*5.2%*365)/365 884

STATUTORY FORMULA METHOD

STATUTORY FORMUAL METHOD

Details Amount

Car Base Value actual 18000

Less Employee made constibution 1000 TR

2011/3

Base Value adjusted 17000

Statutory rate of method 20%

private use PU 365%

Total Days 365

Taxble value

(BV*20%*(PU/TD) 3400

From the above calculation, it can be inferred that the statutory formula method is

comparatively better.

Statutory Interest rate 5.20% TD

2018/2

Deemed Interest

(BV*5.2%*365)/365 884

STATUTORY FORMULA METHOD

STATUTORY FORMUAL METHOD

Details Amount

Car Base Value actual 18000

Less Employee made constibution 1000 TR

2011/3

Base Value adjusted 17000

Statutory rate of method 20%

private use PU 365%

Total Days 365

Taxble value

(BV*20%*(PU/TD) 3400

From the above calculation, it can be inferred that the statutory formula method is

comparatively better.

5TAXATION LAW

Answer 2:

Section (a)

PART 1

Here in the instant situation the issue is to analyze the consequences of the capital

gain for the sale of assets.

Capital gain can be said to be one of the statutory incomes; requires capital gain’s

assets presence and an event of capital gain. One of the most capital gain events is CGE A1

which occurs when the tax payer dispose the capital gain asset. it is entrenched under s.

104.10(1) of ITAA 1997. The event’s timing is also very significant for the ascertainment

whether the said event has taken place in which Financial Year in this regard and whether the

asset is prior or post to the CGT. It is pertinent to note that a post CGT asset is allowed to be

denoted with the status of a CGT asset. It includes the assets acquired after 20th September of

the year 1985. As stated under the provisions/rules of s 108.5, a house is also included in a

CGT asset. Therefore, it is apparent from the said context that the selling of the house will

definitely and positively trigger a CGT event. As per the decision made in the case of

McDonalds v FCT (1998), an A1 CGT Event is considered to have occurred when the said

asset is sold or disposed. The Capital Gain or Loss is calculated in the formula which is CG

or CL= CP – CB. CP represents the Capital proceeds which is the price that is gained during

the sale of the asset and it also includes a house as per the provisions sated under the

provisions of s116.20 and it is also significant to note that it also includes the amount that

accrued to be received.

In addition to this, the CB consists of 5 elements which indicate that the cost to be

incurred by the TP in respect of the asset is elaborated under s. 110.25(1). The Element 1 of

CB is the Cost Price. Hence, for house, E1 is 70000dollars as entrenched in s110.25(2). E2 of

CB as entrenched in s110.25(3) is the 15000dollars paid to real estate agent. The time of

Answer 2:

Section (a)

PART 1

Here in the instant situation the issue is to analyze the consequences of the capital

gain for the sale of assets.

Capital gain can be said to be one of the statutory incomes; requires capital gain’s

assets presence and an event of capital gain. One of the most capital gain events is CGE A1

which occurs when the tax payer dispose the capital gain asset. it is entrenched under s.

104.10(1) of ITAA 1997. The event’s timing is also very significant for the ascertainment

whether the said event has taken place in which Financial Year in this regard and whether the

asset is prior or post to the CGT. It is pertinent to note that a post CGT asset is allowed to be

denoted with the status of a CGT asset. It includes the assets acquired after 20th September of

the year 1985. As stated under the provisions/rules of s 108.5, a house is also included in a

CGT asset. Therefore, it is apparent from the said context that the selling of the house will

definitely and positively trigger a CGT event. As per the decision made in the case of

McDonalds v FCT (1998), an A1 CGT Event is considered to have occurred when the said

asset is sold or disposed. The Capital Gain or Loss is calculated in the formula which is CG

or CL= CP – CB. CP represents the Capital proceeds which is the price that is gained during

the sale of the asset and it also includes a house as per the provisions sated under the

provisions of s116.20 and it is also significant to note that it also includes the amount that

accrued to be received.

In addition to this, the CB consists of 5 elements which indicate that the cost to be

incurred by the TP in respect of the asset is elaborated under s. 110.25(1). The Element 1 of

CB is the Cost Price. Hence, for house, E1 is 70000dollars as entrenched in s110.25(2). E2 of

CB as entrenched in s110.25(3) is the 15000dollars paid to real estate agent. The time of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

formation of contract is 29.06.2019. The CP will amount to $ 865000. And the Net capital

gain for Mr. Daniel is 780000. Thus he can claim a 50 percent discount under division 115.

There are also few criteria which need to be met to avail the discount. It can be said that the

assests which are being hold for 1 year, acquired after 21.09.1999 and concerned person is

the individuals as laid down in s115.10, 115.15 and 115.25. Henceforth, total CGT appears to

be 390000. On the contrary, Daniel has been residing for 30 years in such property; that

shows it has become his main residence. So there is no reason for Daniel to pay the taxes for

capital gain since contract is retracted and Daniel retained the deposit. Therefore all events

that may take place in the next financial year (FY) have no importance.

Part 2:

Capital gain can be said to be one of the statutory incomes; requires capital gain’s assets

presence and an event of capital gain. One of the most capital gain events is CGE A1 which

occurs when the tax payer dispose the capital gain asset. it is entrenched under s. 104.10(1) of

ITAA 1997. The event’s timing is also very significant for the ascertainment whether the said

event has taken place in which Financial Year in this regard and whether the asset is prior or

post to the CGT. It is pertinent to note that a post CGT asset is allowed to be denoted with the

status of a CGT asset. It includes the assets acquired after 20th September of the year 1985.

The Capital Gain or Loss is calculated in the formula which is CP – CB. CP is the Capital

proceeds which is the price that is gained during the sale of the asset. Moreover, CB contains

5 elements (E) which indicates that the price to be paid by TP for an asset is laid down in

s110.25(1). The EI provides the cost price. It is also significant to note that it also includes

the amount that accrued to be received. There fore, the price is borne in relation to the TP of

the asset concerned. Here in this case, Margaret Preston’s painting has been acquired $15000

under section 110-25(2). The painting has been acquired in the 20th day of September 1985,

henceforth it is a CGT asset as it was not incurred prior to 23:55 hours of the 19th day of

formation of contract is 29.06.2019. The CP will amount to $ 865000. And the Net capital

gain for Mr. Daniel is 780000. Thus he can claim a 50 percent discount under division 115.

There are also few criteria which need to be met to avail the discount. It can be said that the

assests which are being hold for 1 year, acquired after 21.09.1999 and concerned person is

the individuals as laid down in s115.10, 115.15 and 115.25. Henceforth, total CGT appears to

be 390000. On the contrary, Daniel has been residing for 30 years in such property; that

shows it has become his main residence. So there is no reason for Daniel to pay the taxes for

capital gain since contract is retracted and Daniel retained the deposit. Therefore all events

that may take place in the next financial year (FY) have no importance.

Part 2:

Capital gain can be said to be one of the statutory incomes; requires capital gain’s assets

presence and an event of capital gain. One of the most capital gain events is CGE A1 which

occurs when the tax payer dispose the capital gain asset. it is entrenched under s. 104.10(1) of

ITAA 1997. The event’s timing is also very significant for the ascertainment whether the said

event has taken place in which Financial Year in this regard and whether the asset is prior or

post to the CGT. It is pertinent to note that a post CGT asset is allowed to be denoted with the

status of a CGT asset. It includes the assets acquired after 20th September of the year 1985.

The Capital Gain or Loss is calculated in the formula which is CP – CB. CP is the Capital

proceeds which is the price that is gained during the sale of the asset. Moreover, CB contains

5 elements (E) which indicates that the price to be paid by TP for an asset is laid down in

s110.25(1). The EI provides the cost price. It is also significant to note that it also includes

the amount that accrued to be received. There fore, the price is borne in relation to the TP of

the asset concerned. Here in this case, Margaret Preston’s painting has been acquired $15000

under section 110-25(2). The painting has been acquired in the 20th day of September 1985,

henceforth it is a CGT asset as it was not incurred prior to 23:55 hours of the 19th day of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

September of 1985, the CP, here is 125000 that is the price gained from the sale. And the

asset sold on Sept 21, 1999, the asset being hold for a year, the total CGT amounts to 55000,

therefore Daniel meets all the aforementioned criteria as he is an individual too. Hence all

conditions were met by Daniel.

Part 3:

Capital gain can be said to be one of the statutory incomes; requires capital gain’s assets

presence and an event of capital gain. One of the most capital gain events is CGE A1 which

occurs when the tax payer dispose the capital gain asset. it is entrenched under s. 104.10(1) of

ITAA 1997. The event’s timing is also very significant for the ascertainment whether the said

event has taken place in which Financial Year in this regard and whether the asset is prior or

post to the CGT. It is pertinent to note that a post CGT asset is allowed to be denoted with the

status of a CGT asset. It includes the assets acquired after 20th September of the year 1985.

The Capital Gain or Loss is calculated in the formula which is CP – CB. CP is the Capital

proceeds which is the price that is gained during the sale of the asset. Moreover, CB contains

5 elements (E) which indicates that the price to be paid by TP for an asset is laid down in

s110.25(1). The EI provides the cost price. It is also significant to note that it also includes

the amount that accrued to be received. There fore, the price is borne in relation to the TP of

the asset concerned. Here in this case the 1st element is inclusive of the cost price,that is to

say the 1st element of the luxury yacht’s cost base results into $110000 under section

110.25(2). The CP is $60000 which means the CL amounts to $ 50000. However, the said

section 108.20(2) stated that CL on personal asset use is not taken into account therefore

disregarded, then this loss is also disregarded. Here the cost base is said as reduced cost base.

Part 4:

Capital gain can be said to be one of the statutory incomes; requires capital gain’s assets

presence and an event of capital gain. One of the most capital gain events is CGE A1 which

September of 1985, the CP, here is 125000 that is the price gained from the sale. And the

asset sold on Sept 21, 1999, the asset being hold for a year, the total CGT amounts to 55000,

therefore Daniel meets all the aforementioned criteria as he is an individual too. Hence all

conditions were met by Daniel.

Part 3:

Capital gain can be said to be one of the statutory incomes; requires capital gain’s assets

presence and an event of capital gain. One of the most capital gain events is CGE A1 which

occurs when the tax payer dispose the capital gain asset. it is entrenched under s. 104.10(1) of

ITAA 1997. The event’s timing is also very significant for the ascertainment whether the said

event has taken place in which Financial Year in this regard and whether the asset is prior or

post to the CGT. It is pertinent to note that a post CGT asset is allowed to be denoted with the

status of a CGT asset. It includes the assets acquired after 20th September of the year 1985.

The Capital Gain or Loss is calculated in the formula which is CP – CB. CP is the Capital

proceeds which is the price that is gained during the sale of the asset. Moreover, CB contains

5 elements (E) which indicates that the price to be paid by TP for an asset is laid down in

s110.25(1). The EI provides the cost price. It is also significant to note that it also includes

the amount that accrued to be received. There fore, the price is borne in relation to the TP of

the asset concerned. Here in this case the 1st element is inclusive of the cost price,that is to

say the 1st element of the luxury yacht’s cost base results into $110000 under section

110.25(2). The CP is $60000 which means the CL amounts to $ 50000. However, the said

section 108.20(2) stated that CL on personal asset use is not taken into account therefore

disregarded, then this loss is also disregarded. Here the cost base is said as reduced cost base.

Part 4:

Capital gain can be said to be one of the statutory incomes; requires capital gain’s assets

presence and an event of capital gain. One of the most capital gain events is CGE A1 which

8TAXATION LAW

occurs when the tax payer dispose the capital gain asset. it is entrenched under s. 104.10(1) of

ITAA 1997. The event’s timing is also very significant for the ascertainment whether the said

event has taken place in which Financial Year in this regard and whether the asset is prior or

post to the CGT. It is pertinent to note that a post CGT asset is allowed to be denoted with the

status of a CGT asset. It includes the assets acquired after 20th September of the year 1985.

The Capital Gain or Loss is calculated in the formula which is CP – CB. CP is the Capital

proceeds which is the price that is gained during the sale of the asset. Moreover, CB contains

5 elements (E) which indicates that the price to be paid by TP for an asset is laid down in

s110.25(1). The EI provides the cost price. It is also significant to note that it also includes

the amount that accrued to be received. There fore, the price is borne in relation to the TP of

the asset concerned. Additionally there are five elements. The Element E1 of the CB of

shares is $75000 under the provision of section 110.25(2). Daniel incurred a capital loss and

RCB is not inclusive of 3re element of Section 110-25(4) therefore the loans will not be part

of calculation in this case being an undeductible expenditure. The element E2 is inclusive of a

$250 stamp duty. The capital proceeds, as enumerated under section 116.20 which is the

selling price. CP in the instant case is $ 80000 which will be modified by the reduction of $

750 under the head of brokerage fees under the provisions of section 116.30. Here in this

situation total loss of capital is $ 4000 (75250-79250). There is a further capital loss incurred

in the previous year on the heads of shares which leads to a reduction of total CG by $ 10000.

The net CG or CL for Daniel in FY 2018-2019 is:

House – 0

Painting – 55000

Yacht – 50000 (not regarded)

Shares – 4000

occurs when the tax payer dispose the capital gain asset. it is entrenched under s. 104.10(1) of

ITAA 1997. The event’s timing is also very significant for the ascertainment whether the said

event has taken place in which Financial Year in this regard and whether the asset is prior or

post to the CGT. It is pertinent to note that a post CGT asset is allowed to be denoted with the

status of a CGT asset. It includes the assets acquired after 20th September of the year 1985.

The Capital Gain or Loss is calculated in the formula which is CP – CB. CP is the Capital

proceeds which is the price that is gained during the sale of the asset. Moreover, CB contains

5 elements (E) which indicates that the price to be paid by TP for an asset is laid down in

s110.25(1). The EI provides the cost price. It is also significant to note that it also includes

the amount that accrued to be received. There fore, the price is borne in relation to the TP of

the asset concerned. Additionally there are five elements. The Element E1 of the CB of

shares is $75000 under the provision of section 110.25(2). Daniel incurred a capital loss and

RCB is not inclusive of 3re element of Section 110-25(4) therefore the loans will not be part

of calculation in this case being an undeductible expenditure. The element E2 is inclusive of a

$250 stamp duty. The capital proceeds, as enumerated under section 116.20 which is the

selling price. CP in the instant case is $ 80000 which will be modified by the reduction of $

750 under the head of brokerage fees under the provisions of section 116.30. Here in this

situation total loss of capital is $ 4000 (75250-79250). There is a further capital loss incurred

in the previous year on the heads of shares which leads to a reduction of total CG by $ 10000.

The net CG or CL for Daniel in FY 2018-2019 is:

House – 0

Painting – 55000

Yacht – 50000 (not regarded)

Shares – 4000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Loss incurred from previous year – 10000

Total capital gain is – 49000

Section b:

Daniel is liable for payment of income tax in relation to the net capital gain of the present

financial year as it is a statutory income. The gain, then gets added in his assessable income.

Section c:

In regard to a net CL of the financial year it can be stated that Daniel has the eligibility to get

the amount in the subsequent financial year as an offset done for the pertaining shares,

provided, the collectibles is not able to be offset only in contrary to the collectibles. Loss of

Private property asset is not able to be offset against loss.

Loss incurred from previous year – 10000

Total capital gain is – 49000

Section b:

Daniel is liable for payment of income tax in relation to the net capital gain of the present

financial year as it is a statutory income. The gain, then gets added in his assessable income.

Section c:

In regard to a net CL of the financial year it can be stated that Daniel has the eligibility to get

the amount in the subsequent financial year as an offset done for the pertaining shares,

provided, the collectibles is not able to be offset only in contrary to the collectibles. Loss of

Private property asset is not able to be offset against loss.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1997 (Cth)

McDonalds v FCT (1998)

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1997 (Cth)

McDonalds v FCT (1998)

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.