HA3042 Taxation Law: Fringe Benefits and Capital Gains Analysis T1

VerifiedAdded on 2023/03/31

|11

|2791

|106

Homework Assignment

AI Summary

This assignment solution delves into various aspects of taxation law, focusing on fringe benefits tax (FBT) and capital gains tax (CGT). It analyzes the tax implications of providing fringe benefits, such as company cars, to employees, including calculations using both statutory formula and operating cost methods. The assignment also addresses CGT events, including the sale of property, collectables (paintings), personal assets (luxury yachts), and shares, determining whether these events result in taxable capital gains or allowable capital losses. The document is available on Desklib, a platform offering study tools and resources for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Table of Contents

Answer to Question No 1...................................................................................................2

Issues:............................................................................................................................2

Rule:...............................................................................................................................2

Application:.....................................................................................................................2

Conclusion......................................................................................................................5

Answer to Question No 2...................................................................................................5

Answer to Question No A...............................................................................................5

Answer to Question No B...............................................................................................7

Answer to Question No C..............................................................................................8

Reference List....................................................................................................................9

TAXATION LAW

Table of Contents

Answer to Question No 1...................................................................................................2

Issues:............................................................................................................................2

Rule:...............................................................................................................................2

Application:.....................................................................................................................2

Conclusion......................................................................................................................5

Answer to Question No 2...................................................................................................5

Answer to Question No A...............................................................................................5

Answer to Question No B...............................................................................................7

Answer to Question No C..............................................................................................8

Reference List....................................................................................................................9

2

TAXATION LAW

Answer to Question No 1

Issues:

The current problem that is associated to this scenario is the liability of tax of

fringe benefits that is given by the employers to their employees with respect to their

employment.

Rule:

It is seen that fringe benefit is looked upon as the payment that is provided to the

employees however, the benefit is not similar to the wages and salaries. The legislation

of Fringe Benefit Tax states that fringe benefit needs to be regarded as the benefit

provided to the employees for the relationship among the process of employment.

“Section 135 (1), FBTAA 1986”, means that the provision that is given to the employees

as they are the employees. The employers are liable to for the tax of fringe benefit of

the employer undertakes a payment to for the employees, office holders and the

company’s director and this be subject to the compulsion of withholding that is given to

the employees for the payments that are made and this issue comes under the fringe

benefit tax (Woellner et al. 2016).

The employers are required to make payments for the fringe benefits tax

irrespective of whether they are in partnership, sole trader or any kind of government

authority. This does not take into account whether the other parties or the employers

are giving any kind of fringe benefits (Bateman 2017). This tax is payable irrespective of

the fact that whether the employers is paying any kind of other tax payments especially

income tax. The employers have the power to make claims for the deduction for income

tax for the purpose of offering benefits and the fringe benefit that is paid by them.

“Section 7 (1), FBTAA 1986” cites that fringe benefit for a car takes place

employer makes use of it for the private use of the employees. The employers keep the

car for the private use of the employees for specific time period in case the car is used

for the private use of the employees for most of the time (Prince 2016). It is seen that

using the car to come to office from home is known to be the private usage of the car.

In order to calculate the value of tax for the car for the purpose of fringe benefit,

there are two alternative processes. The processes are inclusive of the method of

statutory formula and the process of operating costs (Verikios et al. 2016). It is

obligatory for a tax payer to make use of the statutory process if they are opting to use

the process of operating cost.

It is seen that the taxpayers have the authority to make use of the process of

operating cost for any car even if the process is being used for the first time. “Section 7

(8) of the FBTAA 1986” explains that for the purpose of making use of the process of

operating cost, it is essential to maintain a log book in order to maintain proper records

(Verikios, Patron and Gharibnavaz 2017).

TAXATION LAW

Answer to Question No 1

Issues:

The current problem that is associated to this scenario is the liability of tax of

fringe benefits that is given by the employers to their employees with respect to their

employment.

Rule:

It is seen that fringe benefit is looked upon as the payment that is provided to the

employees however, the benefit is not similar to the wages and salaries. The legislation

of Fringe Benefit Tax states that fringe benefit needs to be regarded as the benefit

provided to the employees for the relationship among the process of employment.

“Section 135 (1), FBTAA 1986”, means that the provision that is given to the employees

as they are the employees. The employers are liable to for the tax of fringe benefit of

the employer undertakes a payment to for the employees, office holders and the

company’s director and this be subject to the compulsion of withholding that is given to

the employees for the payments that are made and this issue comes under the fringe

benefit tax (Woellner et al. 2016).

The employers are required to make payments for the fringe benefits tax

irrespective of whether they are in partnership, sole trader or any kind of government

authority. This does not take into account whether the other parties or the employers

are giving any kind of fringe benefits (Bateman 2017). This tax is payable irrespective of

the fact that whether the employers is paying any kind of other tax payments especially

income tax. The employers have the power to make claims for the deduction for income

tax for the purpose of offering benefits and the fringe benefit that is paid by them.

“Section 7 (1), FBTAA 1986” cites that fringe benefit for a car takes place

employer makes use of it for the private use of the employees. The employers keep the

car for the private use of the employees for specific time period in case the car is used

for the private use of the employees for most of the time (Prince 2016). It is seen that

using the car to come to office from home is known to be the private usage of the car.

In order to calculate the value of tax for the car for the purpose of fringe benefit,

there are two alternative processes. The processes are inclusive of the method of

statutory formula and the process of operating costs (Verikios et al. 2016). It is

obligatory for a tax payer to make use of the statutory process if they are opting to use

the process of operating cost.

It is seen that the taxpayers have the authority to make use of the process of

operating cost for any car even if the process is being used for the first time. “Section 7

(8) of the FBTAA 1986” explains that for the purpose of making use of the process of

operating cost, it is essential to maintain a log book in order to maintain proper records

(Verikios, Patron and Gharibnavaz 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

Application:

In order to apply in accordance to the rules that have been explained earlier, it

has to be taken into account that Spiceco PTY Ltd has Lucinda the employee a car that

can be used by her for the purpose of her personal use. It is seen that Lucinda was

given the car as she is working in the company and is a part of Spiceco Pty Ltd. By

looking into “Section 135 (1), FBTAA 1986”, this provision was received by Lucinda

within the taxation year by the employer as she is working in the organization and is

employed within the company (Krever and Mellor 2016).

Spiceco Pty Ltd has provided the car to Lucinda so that she can make use of the

car even for business purpose as well for personal use with the help of which the

employee will be satisfied and better performance can be attained from the employee. It

is seen that the car has travelled a total of 20,000 km within a year and out of the total

travel, 70% of the travel was for the purpose of business and the rest of the travel was

for personal use. Hence, it can be stated the car used by Lucinda for her personal use

can be regarded to be fringe benefit as per “Section 7 (1), FBTAA 1986” (Breunig and

Carter 2018).

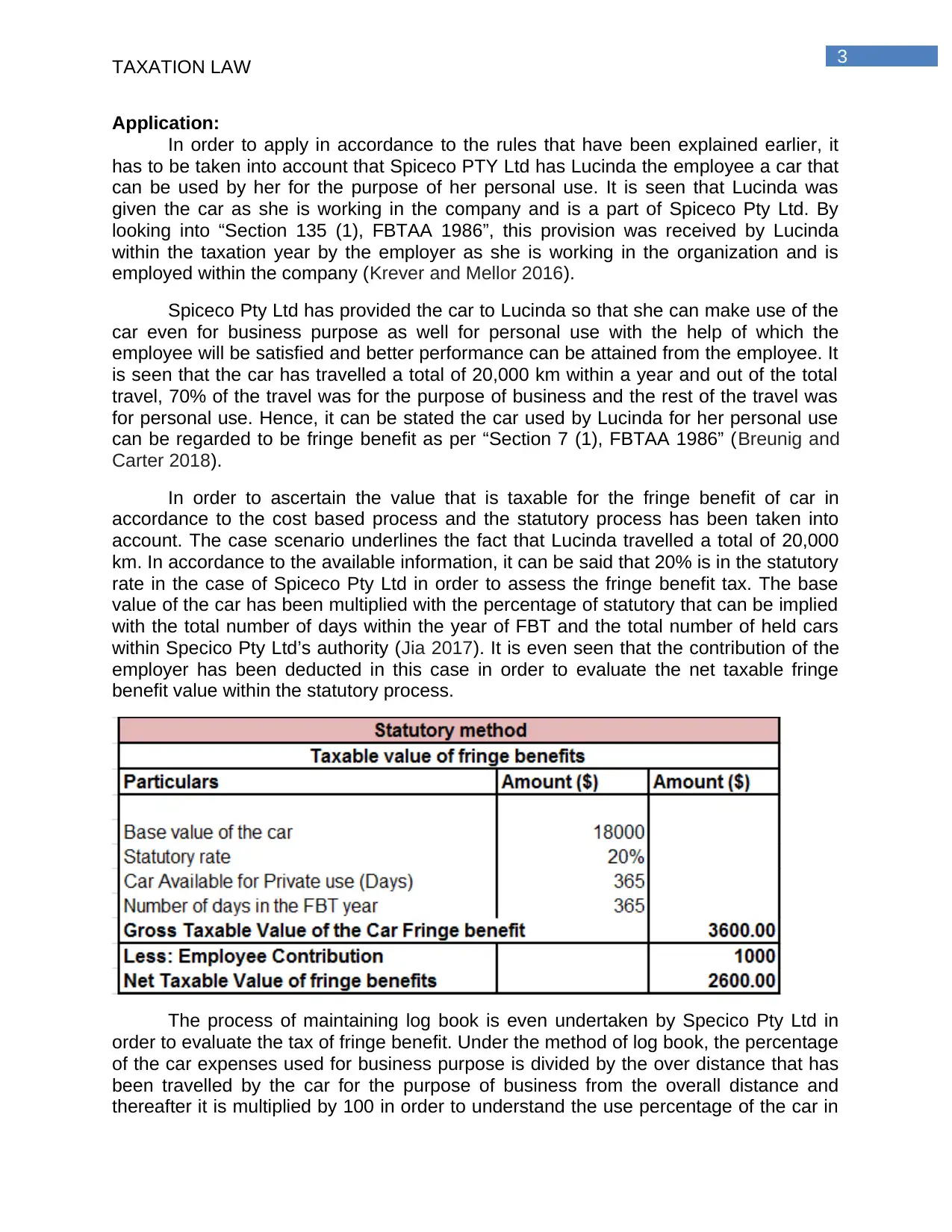

In order to ascertain the value that is taxable for the fringe benefit of car in

accordance to the cost based process and the statutory process has been taken into

account. The case scenario underlines the fact that Lucinda travelled a total of 20,000

km. In accordance to the available information, it can be said that 20% is in the statutory

rate in the case of Spiceco Pty Ltd in order to assess the fringe benefit tax. The base

value of the car has been multiplied with the percentage of statutory that can be implied

with the total number of days within the year of FBT and the total number of held cars

within Specico Pty Ltd’s authority (Jia 2017). It is even seen that the contribution of the

employer has been deducted in this case in order to evaluate the net taxable fringe

benefit value within the statutory process.

The process of maintaining log book is even undertaken by Specico Pty Ltd in

order to evaluate the tax of fringe benefit. Under the method of log book, the percentage

of the car expenses used for business purpose is divided by the over distance that has

been travelled by the car for the purpose of business from the overall distance and

thereafter it is multiplied by 100 in order to understand the use percentage of the car in

TAXATION LAW

Application:

In order to apply in accordance to the rules that have been explained earlier, it

has to be taken into account that Spiceco PTY Ltd has Lucinda the employee a car that

can be used by her for the purpose of her personal use. It is seen that Lucinda was

given the car as she is working in the company and is a part of Spiceco Pty Ltd. By

looking into “Section 135 (1), FBTAA 1986”, this provision was received by Lucinda

within the taxation year by the employer as she is working in the organization and is

employed within the company (Krever and Mellor 2016).

Spiceco Pty Ltd has provided the car to Lucinda so that she can make use of the

car even for business purpose as well for personal use with the help of which the

employee will be satisfied and better performance can be attained from the employee. It

is seen that the car has travelled a total of 20,000 km within a year and out of the total

travel, 70% of the travel was for the purpose of business and the rest of the travel was

for personal use. Hence, it can be stated the car used by Lucinda for her personal use

can be regarded to be fringe benefit as per “Section 7 (1), FBTAA 1986” (Breunig and

Carter 2018).

In order to ascertain the value that is taxable for the fringe benefit of car in

accordance to the cost based process and the statutory process has been taken into

account. The case scenario underlines the fact that Lucinda travelled a total of 20,000

km. In accordance to the available information, it can be said that 20% is in the statutory

rate in the case of Spiceco Pty Ltd in order to assess the fringe benefit tax. The base

value of the car has been multiplied with the percentage of statutory that can be implied

with the total number of days within the year of FBT and the total number of held cars

within Specico Pty Ltd’s authority (Jia 2017). It is even seen that the contribution of the

employer has been deducted in this case in order to evaluate the net taxable fringe

benefit value within the statutory process.

The process of maintaining log book is even undertaken by Specico Pty Ltd in

order to evaluate the tax of fringe benefit. Under the method of log book, the percentage

of the car expenses used for business purpose is divided by the over distance that has

been travelled by the car for the purpose of business from the overall distance and

thereafter it is multiplied by 100 in order to understand the use percentage of the car in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

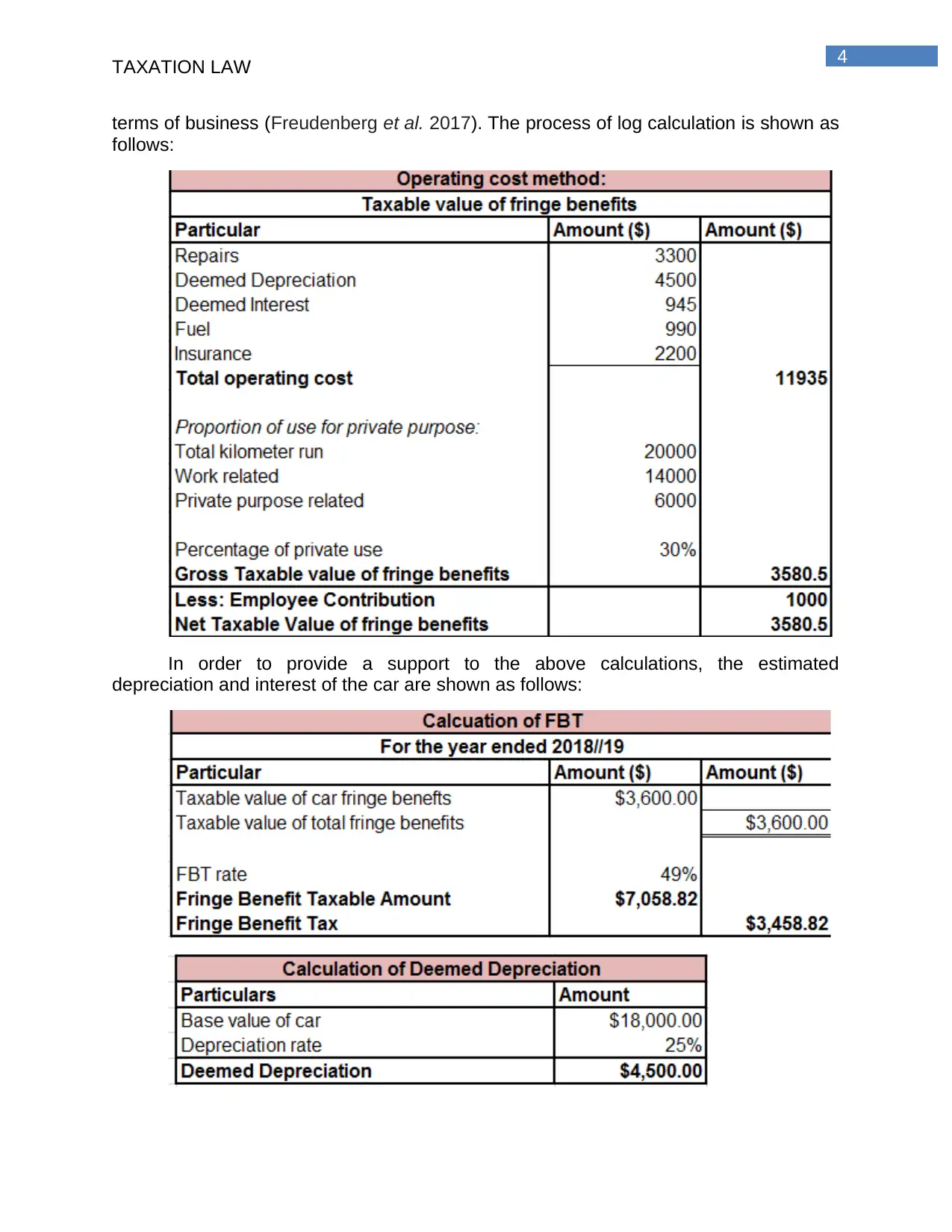

terms of business (Freudenberg et al. 2017). The process of log calculation is shown as

follows:

In order to provide a support to the above calculations, the estimated

depreciation and interest of the car are shown as follows:

TAXATION LAW

terms of business (Freudenberg et al. 2017). The process of log calculation is shown as

follows:

In order to provide a support to the above calculations, the estimated

depreciation and interest of the car are shown as follows:

5

TAXATION LAW

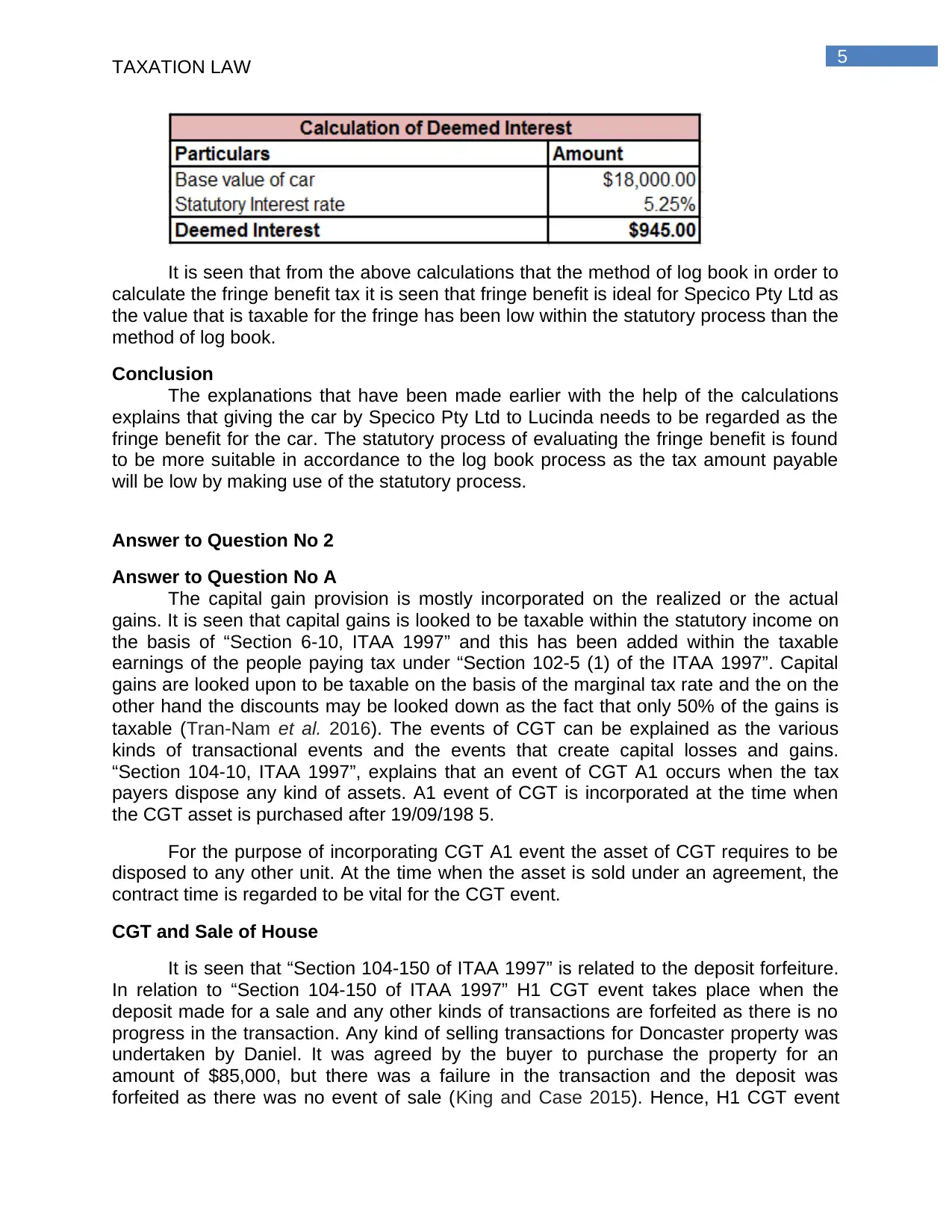

It is seen that from the above calculations that the method of log book in order to

calculate the fringe benefit tax it is seen that fringe benefit is ideal for Specico Pty Ltd as

the value that is taxable for the fringe has been low within the statutory process than the

method of log book.

Conclusion

The explanations that have been made earlier with the help of the calculations

explains that giving the car by Specico Pty Ltd to Lucinda needs to be regarded as the

fringe benefit for the car. The statutory process of evaluating the fringe benefit is found

to be more suitable in accordance to the log book process as the tax amount payable

will be low by making use of the statutory process.

Answer to Question No 2

Answer to Question No A

The capital gain provision is mostly incorporated on the realized or the actual

gains. It is seen that capital gains is looked to be taxable within the statutory income on

the basis of “Section 6-10, ITAA 1997” and this has been added within the taxable

earnings of the people paying tax under “Section 102-5 (1) of the ITAA 1997”. Capital

gains are looked upon to be taxable on the basis of the marginal tax rate and the on the

other hand the discounts may be looked down as the fact that only 50% of the gains is

taxable (Tran‐Nam et al. 2016). The events of CGT can be explained as the various

kinds of transactional events and the events that create capital losses and gains.

“Section 104-10, ITAA 1997”, explains that an event of CGT A1 occurs when the tax

payers dispose any kind of assets. A1 event of CGT is incorporated at the time when

the CGT asset is purchased after 19/09/198 5.

For the purpose of incorporating CGT A1 event the asset of CGT requires to be

disposed to any other unit. At the time when the asset is sold under an agreement, the

contract time is regarded to be vital for the CGT event.

CGT and Sale of House

It is seen that “Section 104-150 of ITAA 1997” is related to the deposit forfeiture.

In relation to “Section 104-150 of ITAA 1997” H1 CGT event takes place when the

deposit made for a sale and any other kinds of transactions are forfeited as there is no

progress in the transaction. Any kind of selling transactions for Doncaster property was

undertaken by Daniel. It was agreed by the buyer to purchase the property for an

amount of $85,000, but there was a failure in the transaction and the deposit was

forfeited as there was no event of sale (King and Case 2015). Hence, H1 CGT event

TAXATION LAW

It is seen that from the above calculations that the method of log book in order to

calculate the fringe benefit tax it is seen that fringe benefit is ideal for Specico Pty Ltd as

the value that is taxable for the fringe has been low within the statutory process than the

method of log book.

Conclusion

The explanations that have been made earlier with the help of the calculations

explains that giving the car by Specico Pty Ltd to Lucinda needs to be regarded as the

fringe benefit for the car. The statutory process of evaluating the fringe benefit is found

to be more suitable in accordance to the log book process as the tax amount payable

will be low by making use of the statutory process.

Answer to Question No 2

Answer to Question No A

The capital gain provision is mostly incorporated on the realized or the actual

gains. It is seen that capital gains is looked to be taxable within the statutory income on

the basis of “Section 6-10, ITAA 1997” and this has been added within the taxable

earnings of the people paying tax under “Section 102-5 (1) of the ITAA 1997”. Capital

gains are looked upon to be taxable on the basis of the marginal tax rate and the on the

other hand the discounts may be looked down as the fact that only 50% of the gains is

taxable (Tran‐Nam et al. 2016). The events of CGT can be explained as the various

kinds of transactional events and the events that create capital losses and gains.

“Section 104-10, ITAA 1997”, explains that an event of CGT A1 occurs when the tax

payers dispose any kind of assets. A1 event of CGT is incorporated at the time when

the CGT asset is purchased after 19/09/198 5.

For the purpose of incorporating CGT A1 event the asset of CGT requires to be

disposed to any other unit. At the time when the asset is sold under an agreement, the

contract time is regarded to be vital for the CGT event.

CGT and Sale of House

It is seen that “Section 104-150 of ITAA 1997” is related to the deposit forfeiture.

In relation to “Section 104-150 of ITAA 1997” H1 CGT event takes place when the

deposit made for a sale and any other kinds of transactions are forfeited as there is no

progress in the transaction. Any kind of selling transactions for Doncaster property was

undertaken by Daniel. It was agreed by the buyer to purchase the property for an

amount of $85,000, but there was a failure in the transaction and the deposit was

forfeited as there was no event of sale (King and Case 2015). Hence, H1 CGT event

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

was undertaken as the deposit made on the prospective sale was forfeited by Daniel

because of the non-completion of the transaction. The value of $85,000 therefore needs

to be regarded as capital gains for Daniel deducting the fees for the agent that has been

paid with the transaction that has failed.

Painting Sale

It has been cited in “Section 108-10 to Section 108-17” that any collectables is

regarded as one of the entities that are under “Section 108-10 (2)” and are mainly

utilized or maintained for personal usage of the people paying their taxes. The definition

that has been provided earlier regarding the collectables are inclusive various antiques

that includes books, paintings, manuscripts and jewelry that are rare. It needs to be

taken into consideration that capital losses attained from the collectables has to be

separated and the capital losses can be allowed for offsetting from the gains of capital

that are attained from any other collectables (Bond and Wright 2018).

It is even seen in the current scenario that a rare painting was bought on 20 th

September 1985 for $15,000. This painting will be regarded as an asset of post-CGT as

it was bought after the incorporation of the regime of GCT. On 31st May 2019, the

painting was disposed and the value of sales was $125,000. The painting that was sold

created capital gains. The capital gains that are created from the painting needs to be

looked upon as income that is statutory and therefore will be added in Daniel’s net

income of the taxable earnings.

Luxury Yacht Sale:

Any kinds of asset that are used personally have been addressed in “Section

108-20 to 108-20, ITAA 1997”. The section addresses the assets that are used for

private enjoyment and pleasure by the taxpayers. The assets are inclusive of furniture,

racing horses etc. It can be cited that the capital gains attained from the personal asst

sale can be ignored if the cost of asset acquisition is not more than $10,000 (Raftery

2019). “Section 108-20 (1), ITAA 1997”, even explains that when there is a loss of

capital generated from the personal asset sale then it can be ignored completely.

As per the case study, it is seen that Daniel acquired a luxury yacht in the year

2004 for a value of $110,000. The yacht that has been sold has led to loss of capital. By

looking into “Sectiion 108-20 (1), ITAA 1997” it can be stated that the capital loss that

has taken place from the sale of the yacht can be ignored from the asset that is

personally used (Jones 2018).

Share Sales

By looking into “Section 108-5, ITAA 1997”, the shares of the listed organizations

are even considered as CGT asset. ATO addresses the fact that the shares of the

organization or the entities within unit trusts are taken to be taxable like the other assets

for the tax purpose of capital gains (Samarkovski et al. 2017).

It is seen that for the investors, CGT is implied on the capital that is made from

the shares when the event of CGT takes place. It is seen that capital loss from the

TAXATION LAW

was undertaken as the deposit made on the prospective sale was forfeited by Daniel

because of the non-completion of the transaction. The value of $85,000 therefore needs

to be regarded as capital gains for Daniel deducting the fees for the agent that has been

paid with the transaction that has failed.

Painting Sale

It has been cited in “Section 108-10 to Section 108-17” that any collectables is

regarded as one of the entities that are under “Section 108-10 (2)” and are mainly

utilized or maintained for personal usage of the people paying their taxes. The definition

that has been provided earlier regarding the collectables are inclusive various antiques

that includes books, paintings, manuscripts and jewelry that are rare. It needs to be

taken into consideration that capital losses attained from the collectables has to be

separated and the capital losses can be allowed for offsetting from the gains of capital

that are attained from any other collectables (Bond and Wright 2018).

It is even seen in the current scenario that a rare painting was bought on 20 th

September 1985 for $15,000. This painting will be regarded as an asset of post-CGT as

it was bought after the incorporation of the regime of GCT. On 31st May 2019, the

painting was disposed and the value of sales was $125,000. The painting that was sold

created capital gains. The capital gains that are created from the painting needs to be

looked upon as income that is statutory and therefore will be added in Daniel’s net

income of the taxable earnings.

Luxury Yacht Sale:

Any kinds of asset that are used personally have been addressed in “Section

108-20 to 108-20, ITAA 1997”. The section addresses the assets that are used for

private enjoyment and pleasure by the taxpayers. The assets are inclusive of furniture,

racing horses etc. It can be cited that the capital gains attained from the personal asst

sale can be ignored if the cost of asset acquisition is not more than $10,000 (Raftery

2019). “Section 108-20 (1), ITAA 1997”, even explains that when there is a loss of

capital generated from the personal asset sale then it can be ignored completely.

As per the case study, it is seen that Daniel acquired a luxury yacht in the year

2004 for a value of $110,000. The yacht that has been sold has led to loss of capital. By

looking into “Sectiion 108-20 (1), ITAA 1997” it can be stated that the capital loss that

has taken place from the sale of the yacht can be ignored from the asset that is

personally used (Jones 2018).

Share Sales

By looking into “Section 108-5, ITAA 1997”, the shares of the listed organizations

are even considered as CGT asset. ATO addresses the fact that the shares of the

organization or the entities within unit trusts are taken to be taxable like the other assets

for the tax purpose of capital gains (Samarkovski et al. 2017).

It is seen that for the investors, CGT is implied on the capital that is made from

the shares when the event of CGT takes place. It is seen that capital loss from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

shares are permitted only for the purpose of off-setting the capital gains from the

shares. It is seen that selling the BHP shares, a capital gain was made (Tran-Nam

2016). The taxpayer even has a capital loss from AZJ shares which has been carried

ahead in the present year for the purpose of off-setting. The shares have been offset in

order to reduce the net gains of capital from the shares.

Particulars Amount ($) Amount ($)

Capital gains from Doncaster House

Net Proceeds 85000

Less: Sales Commission 15000

Net Capital gains from Doncaster House 70000

Net Capital Gains on Sale of Painting

Proceeds from sell of Painting 125000

Cost base 15000

Gross Capital Gains (proceeds less cost base) 110000

50% CGT Discount 55000

Taxable Capital Gains 55000

Capital gains on sale of shares

Gross Proceeds from Shares in BHP 80000

Less: Brokerage Fees 750

Net Proceeds 79250

Cost base

Less: Acqusition Cost 75000

Add: Stamp Duty on Purchase 250

Total Cost Base 75250

Capital gains on sale of BHP shares 4000

Less: Carryforward loss 10000

Net capital loss -6000

Net Capital gains 119,000

Calculations of Capital Gains Tax

For the year ended June 2019

Answer to Question No B

Daniel has attained capital gains by selling the painting that is antique and has

even reported some capital from the deposit that has been forfeited for the Doncaster

House. The capital gains net amount that has been attained in the year by Daniel can

be utilized for the purpose of investing in the superannuation fund (White and Townsend

2018).

TAXATION LAW

shares are permitted only for the purpose of off-setting the capital gains from the

shares. It is seen that selling the BHP shares, a capital gain was made (Tran-Nam

2016). The taxpayer even has a capital loss from AZJ shares which has been carried

ahead in the present year for the purpose of off-setting. The shares have been offset in

order to reduce the net gains of capital from the shares.

Particulars Amount ($) Amount ($)

Capital gains from Doncaster House

Net Proceeds 85000

Less: Sales Commission 15000

Net Capital gains from Doncaster House 70000

Net Capital Gains on Sale of Painting

Proceeds from sell of Painting 125000

Cost base 15000

Gross Capital Gains (proceeds less cost base) 110000

50% CGT Discount 55000

Taxable Capital Gains 55000

Capital gains on sale of shares

Gross Proceeds from Shares in BHP 80000

Less: Brokerage Fees 750

Net Proceeds 79250

Cost base

Less: Acqusition Cost 75000

Add: Stamp Duty on Purchase 250

Total Cost Base 75250

Capital gains on sale of BHP shares 4000

Less: Carryforward loss 10000

Net capital loss -6000

Net Capital gains 119,000

Calculations of Capital Gains Tax

For the year ended June 2019

Answer to Question No B

Daniel has attained capital gains by selling the painting that is antique and has

even reported some capital from the deposit that has been forfeited for the Doncaster

House. The capital gains net amount that has been attained in the year by Daniel can

be utilized for the purpose of investing in the superannuation fund (White and Townsend

2018).

8

TAXATION LAW

Answer to Question No C

It is seen that Daniel has faced a capital loss by selling the yacht and the rest of

the amount of loss from the shares of AJZ shares has been carried forward (Silver,

McGregor-Lowndes and Tarr 2016). It can therefore be recommended that the loss from

the AJZ shares can be carried forward for the coming years and the capital loss from

the personal assets can be ignored.

TAXATION LAW

Answer to Question No C

It is seen that Daniel has faced a capital loss by selling the yacht and the rest of

the amount of loss from the shares of AJZ shares has been carried forward (Silver,

McGregor-Lowndes and Tarr 2016). It can therefore be recommended that the loss from

the AJZ shares can be carried forward for the coming years and the capital loss from

the personal assets can be ignored.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

Reference List

Bateman, H., 2017. Taxing Pensions–The Australian Approach. Chapter 7 of the draft

manuscript The Taxation of Pensions, pp.118-140.

Bond, D. and Wright, A., 2018. A Snapshot of the Australian Taxpayer. Australian

Accounting Review, 28(4), pp.598-615.

Breunig, R.V. and Carter, A., 2018. Do Earned Income Tax Credits for Older Workers

Prolong Labor Market Participation and Boost Earned Income? Evidence from

Australia's Mature Age Worker Tax Offset.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of

Australian small businesses. J. Austl. Tax'n, 19, p.21.

Jia, Q., 2017. It is time to cut the corporate tax rate. Bulletin (Law Society of South

Australia), 39(10), p.36.

Jones, D., 2018. Complexity of tax residency attracts review. Taxation in

Australia, 53(6), p.296.

King, D. and Case, C., 2015. AN INTERNATIONAL INDIVIDUAL INCOME TAX

COMPARSION: THE UNITED STATES, AUSTRALIA, AND UNITED

KINGDOM. Business Studies Journal, 7(2).

Krever, R. and Mellor, P., 2016. Australia, GAARs–A Key Element of Tax Systems in

the Post-BEPS World. GAARs–A Key Element of Tax Systems in the Post-BEPS World

(Amsterdam: IBFD, 2016), pp.45-64.

Prince, J.B., 2016. Tax for Australians for Dummies. John Wiley & Sons.

Raftery, A., 2019. 101 Ways to Save Money on Your Tax-Legally! 2019-2020. Wiley.

Samarkovski, L., Copp, R., Wiafe, O.K. and Freudenberg, B., 2017. The impact of tax

on the prospects of achieving target retirement wealth in Australian default

superannuation plans. Austl. Tax F., 32, p.225.

Silver, N., McGregor-Lowndes, M. and Tarr, J.A., 2016. Should Tax Incentives for

Charitable Giving Stop at Australia's Borders. Sydney L. Rev., 38, p.85.

Tran-Nam, B., 2016. Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-44).

Palgrave Macmillan, London.

Tran‐Nam, B., Evans, C., Krever, R. and Lignier, P., 2016. Managing tax complexity: the

state of play after Henry. Economic Papers: A journal of applied economics and

policy, 35(4), pp.347-358.

Verikios, G., Patron, J. and Gharibnavaz, R., 2017. Decomposing the Marginal Excess

Burden of Australia’s Goods and Services Tax.

TAXATION LAW

Reference List

Bateman, H., 2017. Taxing Pensions–The Australian Approach. Chapter 7 of the draft

manuscript The Taxation of Pensions, pp.118-140.

Bond, D. and Wright, A., 2018. A Snapshot of the Australian Taxpayer. Australian

Accounting Review, 28(4), pp.598-615.

Breunig, R.V. and Carter, A., 2018. Do Earned Income Tax Credits for Older Workers

Prolong Labor Market Participation and Boost Earned Income? Evidence from

Australia's Mature Age Worker Tax Offset.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of

Australian small businesses. J. Austl. Tax'n, 19, p.21.

Jia, Q., 2017. It is time to cut the corporate tax rate. Bulletin (Law Society of South

Australia), 39(10), p.36.

Jones, D., 2018. Complexity of tax residency attracts review. Taxation in

Australia, 53(6), p.296.

King, D. and Case, C., 2015. AN INTERNATIONAL INDIVIDUAL INCOME TAX

COMPARSION: THE UNITED STATES, AUSTRALIA, AND UNITED

KINGDOM. Business Studies Journal, 7(2).

Krever, R. and Mellor, P., 2016. Australia, GAARs–A Key Element of Tax Systems in

the Post-BEPS World. GAARs–A Key Element of Tax Systems in the Post-BEPS World

(Amsterdam: IBFD, 2016), pp.45-64.

Prince, J.B., 2016. Tax for Australians for Dummies. John Wiley & Sons.

Raftery, A., 2019. 101 Ways to Save Money on Your Tax-Legally! 2019-2020. Wiley.

Samarkovski, L., Copp, R., Wiafe, O.K. and Freudenberg, B., 2017. The impact of tax

on the prospects of achieving target retirement wealth in Australian default

superannuation plans. Austl. Tax F., 32, p.225.

Silver, N., McGregor-Lowndes, M. and Tarr, J.A., 2016. Should Tax Incentives for

Charitable Giving Stop at Australia's Borders. Sydney L. Rev., 38, p.85.

Tran-Nam, B., 2016. Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-44).

Palgrave Macmillan, London.

Tran‐Nam, B., Evans, C., Krever, R. and Lignier, P., 2016. Managing tax complexity: the

state of play after Henry. Economic Papers: A journal of applied economics and

policy, 35(4), pp.347-358.

Verikios, G., Patron, J. and Gharibnavaz, R., 2017. Decomposing the Marginal Excess

Burden of Australia’s Goods and Services Tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

Verikios, G., Patron, J., Gharibnavaz, R., Economics, K.P.M.G. and Winston, A., 2016,

June. Options for Reforming Australia’s Goods and Services Tax. In 19th Annual

Conference on Global Economic Analysis, Washington, DC, June (pp. 15-17).

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The

ATO's guidance. Taxation in Australia, 52(11), p.608.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law 2016. OUP Catalogue.

TAXATION LAW

Verikios, G., Patron, J., Gharibnavaz, R., Economics, K.P.M.G. and Winston, A., 2016,

June. Options for Reforming Australia’s Goods and Services Tax. In 19th Annual

Conference on Global Economic Analysis, Washington, DC, June (pp. 15-17).

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The

ATO's guidance. Taxation in Australia, 52(11), p.608.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law 2016. OUP Catalogue.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.