T1 2019 HA3042 Taxation Law Assignment: FBT and Capital Gains Tax

VerifiedAdded on 2023/01/12

|5

|428

|74

Homework Assignment

AI Summary

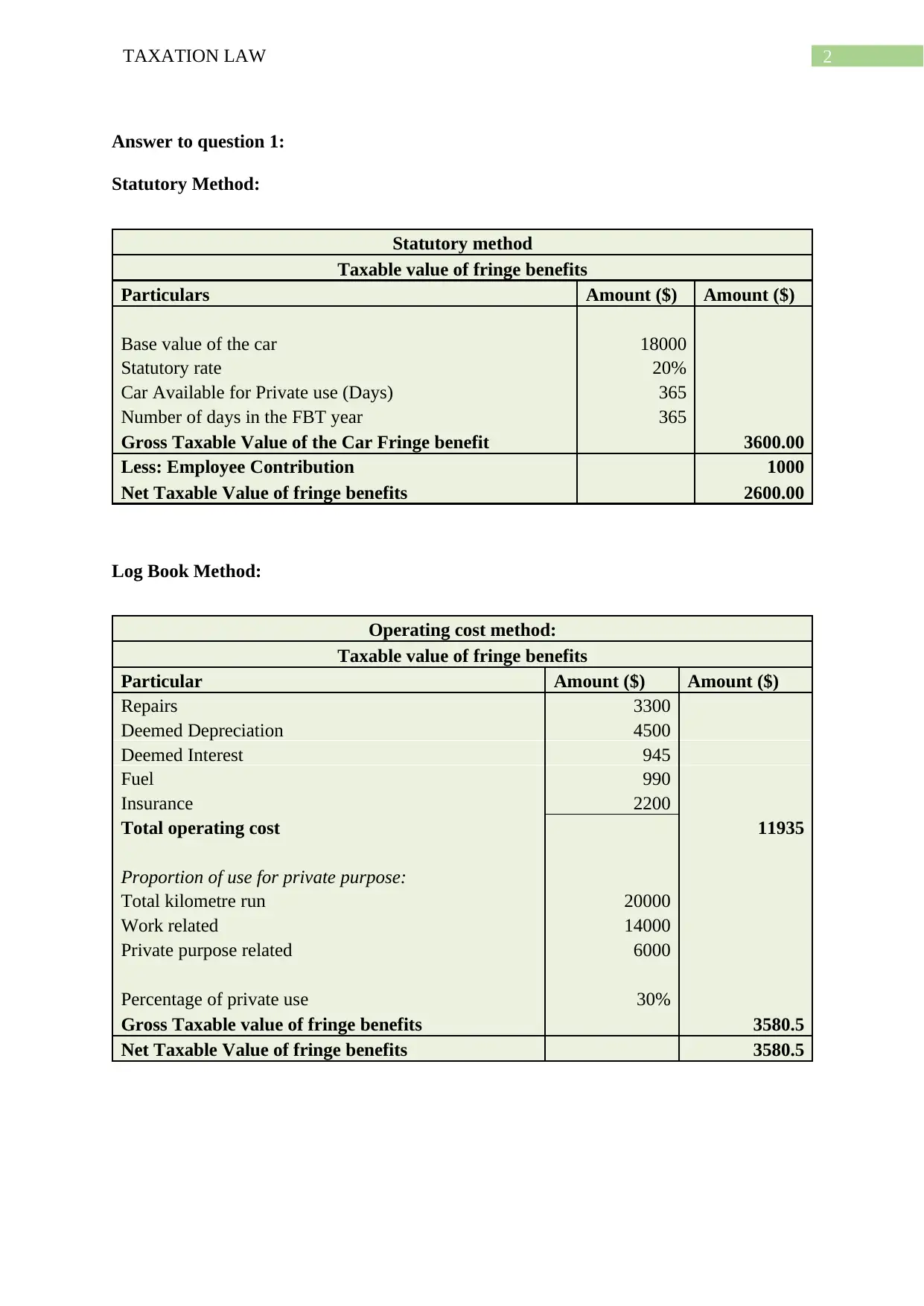

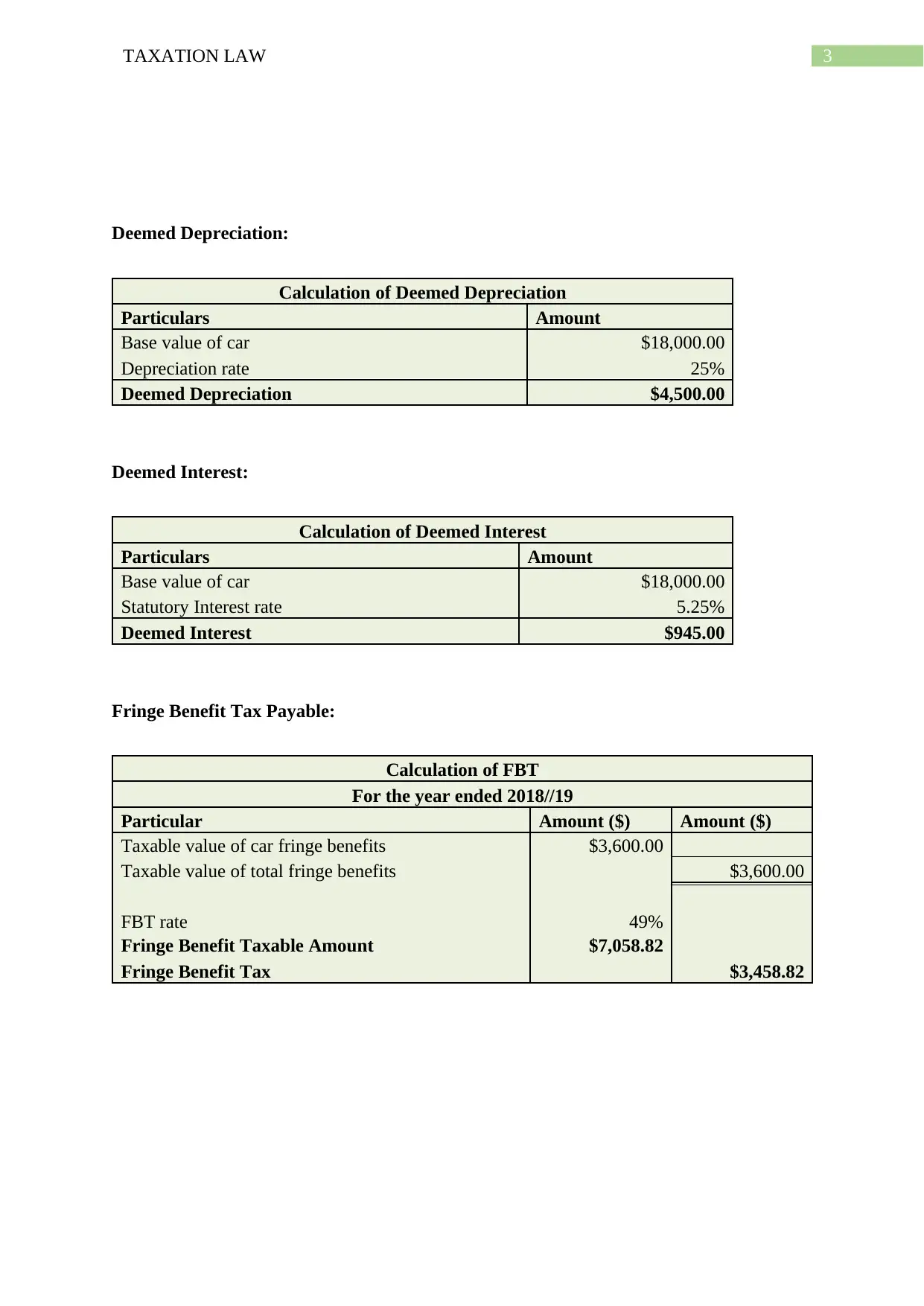

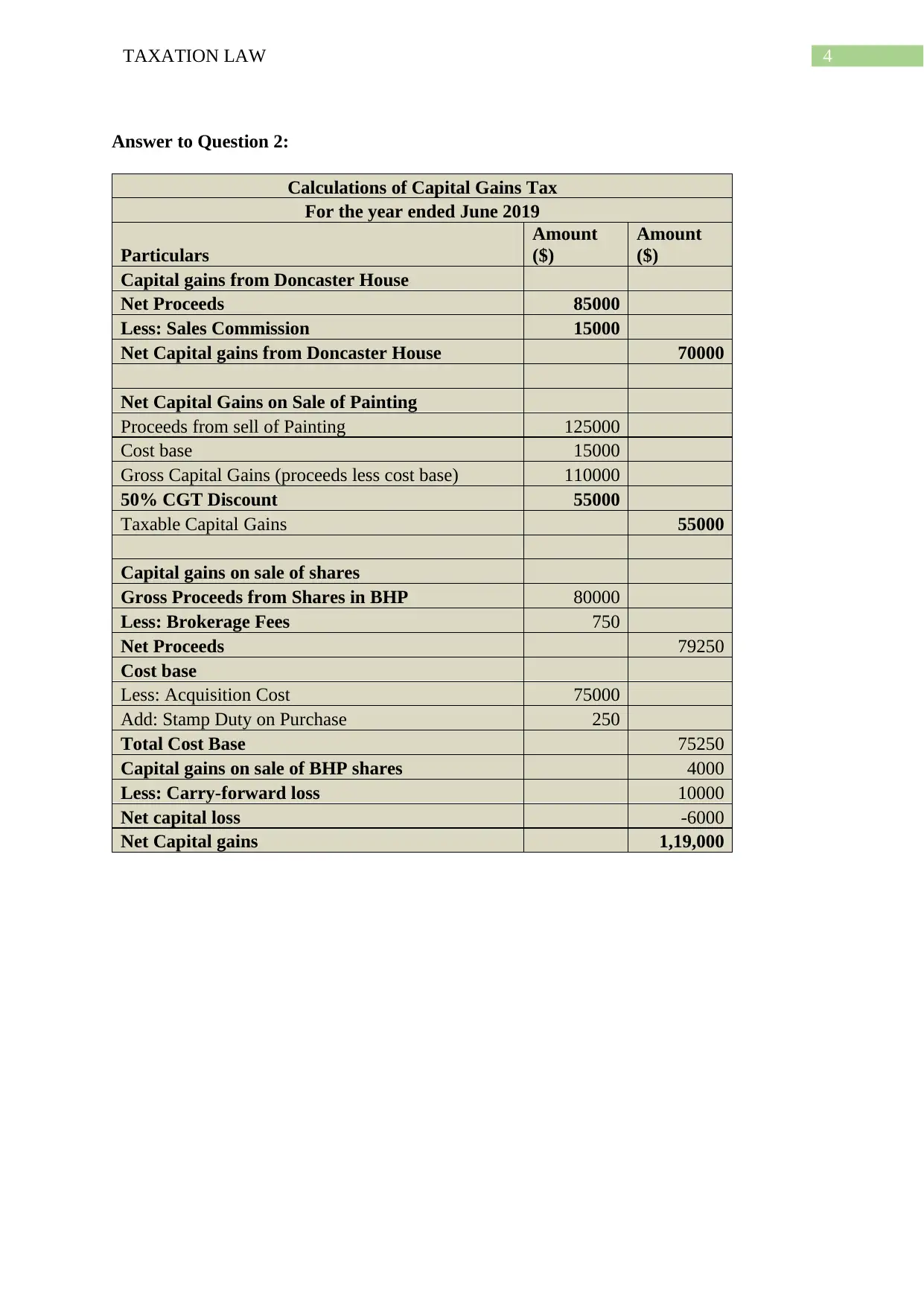

This document is a solution to a Taxation Law assignment, specifically addressing Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT) calculations. The assignment begins with an FBT calculation using both the statutory and log book methods, detailing the taxable value of fringe benefits, employee contributions, and the resulting FBT payable. The solution then proceeds to calculate Capital Gains Tax, considering the sale of a house, a painting, and shares. The calculations include net proceeds, cost bases, capital gains, and the application of a 50% CGT discount, ultimately determining the taxable capital gains and any carry-forward losses. The solution demonstrates the application of tax principles to real-world financial scenarios, providing a comprehensive overview of tax implications for various transactions.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.