Holmles Institute: HA3042 Taxation Law Assignment - Semester 2, 2019

VerifiedAdded on 2022/10/15

|12

|2817

|16

Homework Assignment

AI Summary

This Taxation Law assignment presents a detailed analysis of tax implications for various scenarios. The first part examines Jasmine's tax liabilities, including capital gains tax (CGT) on the sale of her main house (pre-CGT asset), car (personal use asset), business, and furniture, as well as the sale of paintings (collectables). The assignment considers relevant sections of the ITA Act 1997, such as those concerning CGT events, personal use assets, and small business concessions. The second part focuses on capital allowances for John's manufacturing company, specifically the depreciation of a CNC machine imported from Germany. The analysis includes the calculation of the cost base, considering element 1 and element 2 costs, and determining the commencement time for depreciation purposes.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Requirement A: Sale of main house:

There is a limitation that is imposed by “sec 100.25 (1), ITA Act 1997” on the assets

where only part 3 is applicable to the assets that are purchased on or following 20 September

1985. The taxpayers must denote that taxes on capital gains is applied on the actual or the

realised gains. Besides this, the capital gains which is realised by the taxpayers are held as

statutory income in “sec 6.10” and counted into the taxpayer’s taxable earnings under “s

102.5(1), ITA Act 1997” (Burgess 2015). The capital gains which is earned by the taxpayer is

contained within computation of assessable tax liability of taxpayer while the capital loss is

only allowed for offset when a capital gain is reported by the taxpayer. Assets which is

purchased before the 20 sept 1985 is excluded for CGT purpose.

The case here is concerned with the sale of assets during the year by Jasmine. As

understood Jasmine has sold the main dwelling that she purchased for $40,000 in 1981. In the

present year the main home of Jasmine upon the sale fetched $650,000. Now it can be stated

that the house was acquired prior to 20/9/1985 (Dean 2015). As a result, the house will be

classified as the pre-CGT asset. In addition to this, the capital gains which Jasmine produced

from disposing the main home will not be exempted for being a pre-CGT asset.

Requirement B: Sale of Car

CGT events are mentioned as the different form of transactions or events which may

contribute to capital gains or loss. The “CGT event A1” under “s 104.10 ITA Act 1997”

means selling of CGT asset. This event is applied on CGT assets purchased on or succeeding

19/9/85. For the application of CGT event CGT asset needs to be sold to another entity. As

notified in “s.108.20, ITA Act 97” there are assets named personal use asset (PUA’s) which

is under the ownership of taxpayer for private satisfaction purpose (Mahar 2016). The list of

Answer to question 1:

Requirement A: Sale of main house:

There is a limitation that is imposed by “sec 100.25 (1), ITA Act 1997” on the assets

where only part 3 is applicable to the assets that are purchased on or following 20 September

1985. The taxpayers must denote that taxes on capital gains is applied on the actual or the

realised gains. Besides this, the capital gains which is realised by the taxpayers are held as

statutory income in “sec 6.10” and counted into the taxpayer’s taxable earnings under “s

102.5(1), ITA Act 1997” (Burgess 2015). The capital gains which is earned by the taxpayer is

contained within computation of assessable tax liability of taxpayer while the capital loss is

only allowed for offset when a capital gain is reported by the taxpayer. Assets which is

purchased before the 20 sept 1985 is excluded for CGT purpose.

The case here is concerned with the sale of assets during the year by Jasmine. As

understood Jasmine has sold the main dwelling that she purchased for $40,000 in 1981. In the

present year the main home of Jasmine upon the sale fetched $650,000. Now it can be stated

that the house was acquired prior to 20/9/1985 (Dean 2015). As a result, the house will be

classified as the pre-CGT asset. In addition to this, the capital gains which Jasmine produced

from disposing the main home will not be exempted for being a pre-CGT asset.

Requirement B: Sale of Car

CGT events are mentioned as the different form of transactions or events which may

contribute to capital gains or loss. The “CGT event A1” under “s 104.10 ITA Act 1997”

means selling of CGT asset. This event is applied on CGT assets purchased on or succeeding

19/9/85. For the application of CGT event CGT asset needs to be sold to another entity. As

notified in “s.108.20, ITA Act 97” there are assets named personal use asset (PUA’s) which

is under the ownership of taxpayer for private satisfaction purpose (Mahar 2016). The list of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

assets under this heads includes the boats, furniture, motor vehicle and domestic items.

Noting “sec.108.20 (1)” capital loss happening from this disposal is not accounted for tax

purpose.

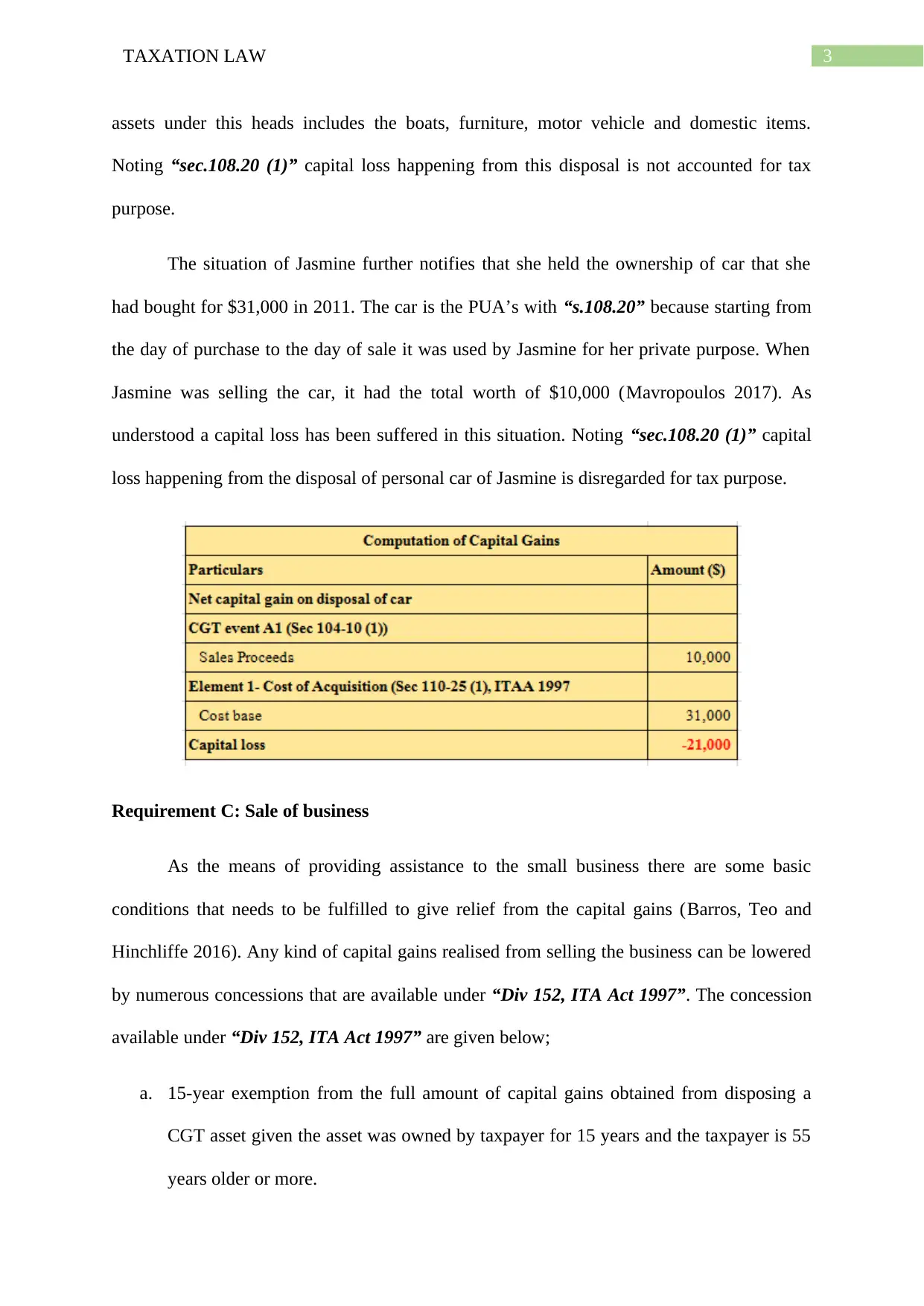

The situation of Jasmine further notifies that she held the ownership of car that she

had bought for $31,000 in 2011. The car is the PUA’s with “s.108.20” because starting from

the day of purchase to the day of sale it was used by Jasmine for her private purpose. When

Jasmine was selling the car, it had the total worth of $10,000 (Mavropoulos 2017). As

understood a capital loss has been suffered in this situation. Noting “sec.108.20 (1)” capital

loss happening from the disposal of personal car of Jasmine is disregarded for tax purpose.

Requirement C: Sale of business

As the means of providing assistance to the small business there are some basic

conditions that needs to be fulfilled to give relief from the capital gains (Barros, Teo and

Hinchliffe 2016). Any kind of capital gains realised from selling the business can be lowered

by numerous concessions that are available under “Div 152, ITA Act 1997”. The concession

available under “Div 152, ITA Act 1997” are given below;

a. 15-year exemption from the full amount of capital gains obtained from disposing a

CGT asset given the asset was owned by taxpayer for 15 years and the taxpayer is 55

years older or more.

assets under this heads includes the boats, furniture, motor vehicle and domestic items.

Noting “sec.108.20 (1)” capital loss happening from this disposal is not accounted for tax

purpose.

The situation of Jasmine further notifies that she held the ownership of car that she

had bought for $31,000 in 2011. The car is the PUA’s with “s.108.20” because starting from

the day of purchase to the day of sale it was used by Jasmine for her private purpose. When

Jasmine was selling the car, it had the total worth of $10,000 (Mavropoulos 2017). As

understood a capital loss has been suffered in this situation. Noting “sec.108.20 (1)” capital

loss happening from the disposal of personal car of Jasmine is disregarded for tax purpose.

Requirement C: Sale of business

As the means of providing assistance to the small business there are some basic

conditions that needs to be fulfilled to give relief from the capital gains (Barros, Teo and

Hinchliffe 2016). Any kind of capital gains realised from selling the business can be lowered

by numerous concessions that are available under “Div 152, ITA Act 1997”. The concession

available under “Div 152, ITA Act 1997” are given below;

a. 15-year exemption from the full amount of capital gains obtained from disposing a

CGT asset given the asset was owned by taxpayer for 15 years and the taxpayer is 55

years older or more.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

b. 50% reduction from CGT is given to small business taxpayer when they qualify for

the concession.

c. Retirement concessions is given the taxpayers that are retiring from the small business

following the disposal of the CGT asset, given that the sales proceeds derived by the

taxpayer are used for business purpose (Norbury 2016)

d. Rollover-relief is given when proceeds of capital gains are used to purchase another

asset.

Concessions that are given above can be availed to help the small business provided

that their overall assets worth is not beyond $6million and all their assets are active assets.

The case clearly explains that Jasmine is leaving Australia permanently. She carried

on a small cleaning business which she has decided to sell it. Upon selling it she procured

$125,000. The business equipment was sold by Jasmine for $65,000 and the goodwill for

$60,000. Within “Div 152, ITA Act 1997” the available four concessions are eligible for

claim because at the time of sale the business assets only worth $125.000 which is below the

$6 million limit (Burnheim and Bobbin 2017). The assets were also the active asset when the

cleaning business of Jasmine was sold. A 15-year exemption from capital gains should be

applied by Jasmine because the asset was owned by Jasmine for 15 years or more and while

selling the business assets Jasmine also ages more than 55 years. So a 15-year CGT

concession is available for Jasmine.

Requirement D: Sale of Furniture:

Personal use asset usually carries certain rules that needs to be taken into account by

taxpayers. Within the legislation of “s.118.10 (3), ITA Act 97” when a taxpayer realises any

capital gain from selling the persona use asset that has cost of less than $10,000 then such

loss is ignored. A furniture was acquired for $2,000 by Jasmine (Slegers and Marateo 2019).

b. 50% reduction from CGT is given to small business taxpayer when they qualify for

the concession.

c. Retirement concessions is given the taxpayers that are retiring from the small business

following the disposal of the CGT asset, given that the sales proceeds derived by the

taxpayer are used for business purpose (Norbury 2016)

d. Rollover-relief is given when proceeds of capital gains are used to purchase another

asset.

Concessions that are given above can be availed to help the small business provided

that their overall assets worth is not beyond $6million and all their assets are active assets.

The case clearly explains that Jasmine is leaving Australia permanently. She carried

on a small cleaning business which she has decided to sell it. Upon selling it she procured

$125,000. The business equipment was sold by Jasmine for $65,000 and the goodwill for

$60,000. Within “Div 152, ITA Act 1997” the available four concessions are eligible for

claim because at the time of sale the business assets only worth $125.000 which is below the

$6 million limit (Burnheim and Bobbin 2017). The assets were also the active asset when the

cleaning business of Jasmine was sold. A 15-year exemption from capital gains should be

applied by Jasmine because the asset was owned by Jasmine for 15 years or more and while

selling the business assets Jasmine also ages more than 55 years. So a 15-year CGT

concession is available for Jasmine.

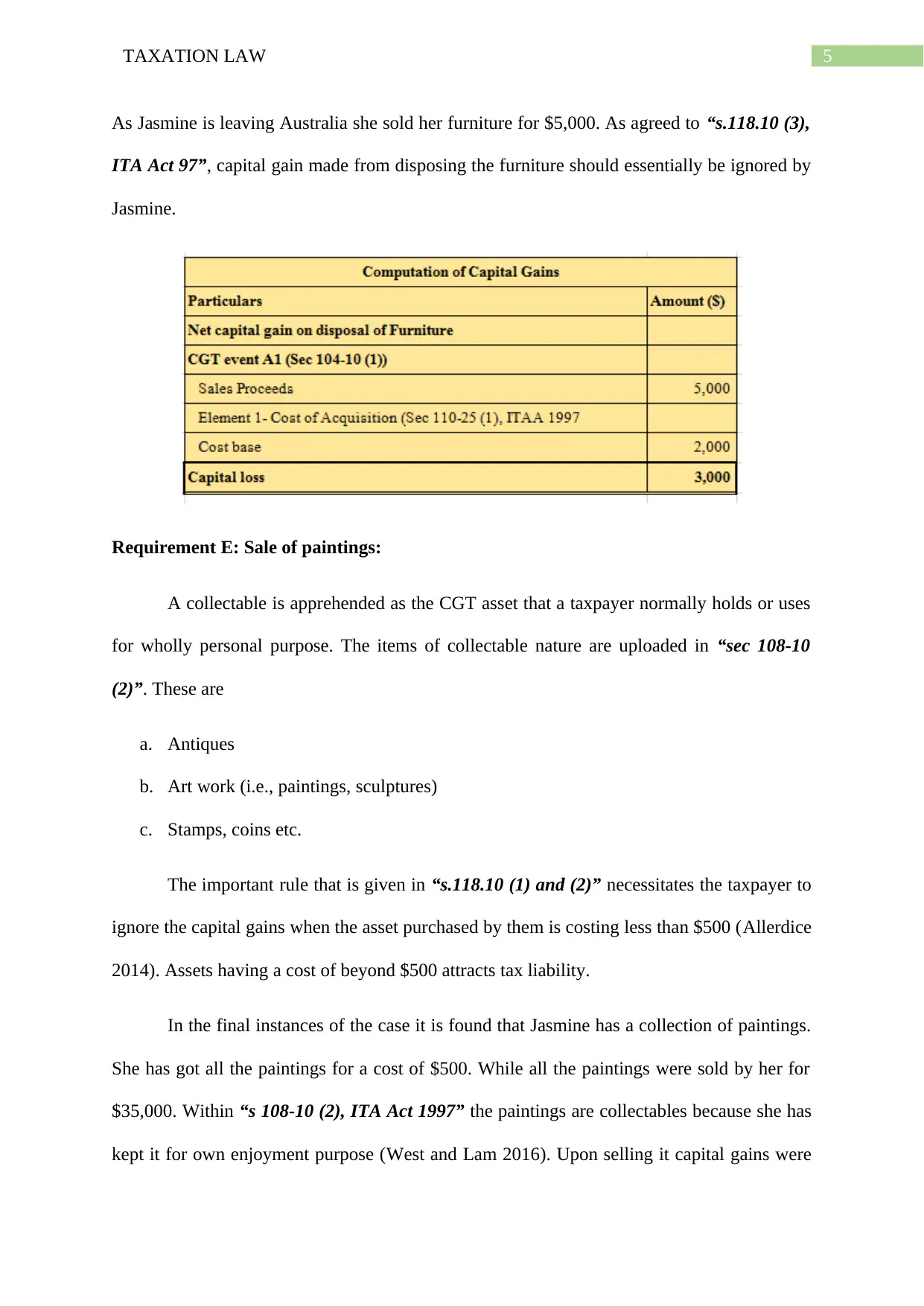

Requirement D: Sale of Furniture:

Personal use asset usually carries certain rules that needs to be taken into account by

taxpayers. Within the legislation of “s.118.10 (3), ITA Act 97” when a taxpayer realises any

capital gain from selling the persona use asset that has cost of less than $10,000 then such

loss is ignored. A furniture was acquired for $2,000 by Jasmine (Slegers and Marateo 2019).

5TAXATION LAW

As Jasmine is leaving Australia she sold her furniture for $5,000. As agreed to “s.118.10 (3),

ITA Act 97”, capital gain made from disposing the furniture should essentially be ignored by

Jasmine.

Requirement E: Sale of paintings:

A collectable is apprehended as the CGT asset that a taxpayer normally holds or uses

for wholly personal purpose. The items of collectable nature are uploaded in “sec 108-10

(2)”. These are

a. Antiques

b. Art work (i.e., paintings, sculptures)

c. Stamps, coins etc.

The important rule that is given in “s.118.10 (1) and (2)” necessitates the taxpayer to

ignore the capital gains when the asset purchased by them is costing less than $500 (Allerdice

2014). Assets having a cost of beyond $500 attracts tax liability.

In the final instances of the case it is found that Jasmine has a collection of paintings.

She has got all the paintings for a cost of $500. While all the paintings were sold by her for

$35,000. Within “s 108-10 (2), ITA Act 1997” the paintings are collectables because she has

kept it for own enjoyment purpose (West and Lam 2016). Upon selling it capital gains were

As Jasmine is leaving Australia she sold her furniture for $5,000. As agreed to “s.118.10 (3),

ITA Act 97”, capital gain made from disposing the furniture should essentially be ignored by

Jasmine.

Requirement E: Sale of paintings:

A collectable is apprehended as the CGT asset that a taxpayer normally holds or uses

for wholly personal purpose. The items of collectable nature are uploaded in “sec 108-10

(2)”. These are

a. Antiques

b. Art work (i.e., paintings, sculptures)

c. Stamps, coins etc.

The important rule that is given in “s.118.10 (1) and (2)” necessitates the taxpayer to

ignore the capital gains when the asset purchased by them is costing less than $500 (Allerdice

2014). Assets having a cost of beyond $500 attracts tax liability.

In the final instances of the case it is found that Jasmine has a collection of paintings.

She has got all the paintings for a cost of $500. While all the paintings were sold by her for

$35,000. Within “s 108-10 (2), ITA Act 1997” the paintings are collectables because she has

kept it for own enjoyment purpose (West and Lam 2016). Upon selling it capital gains were

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

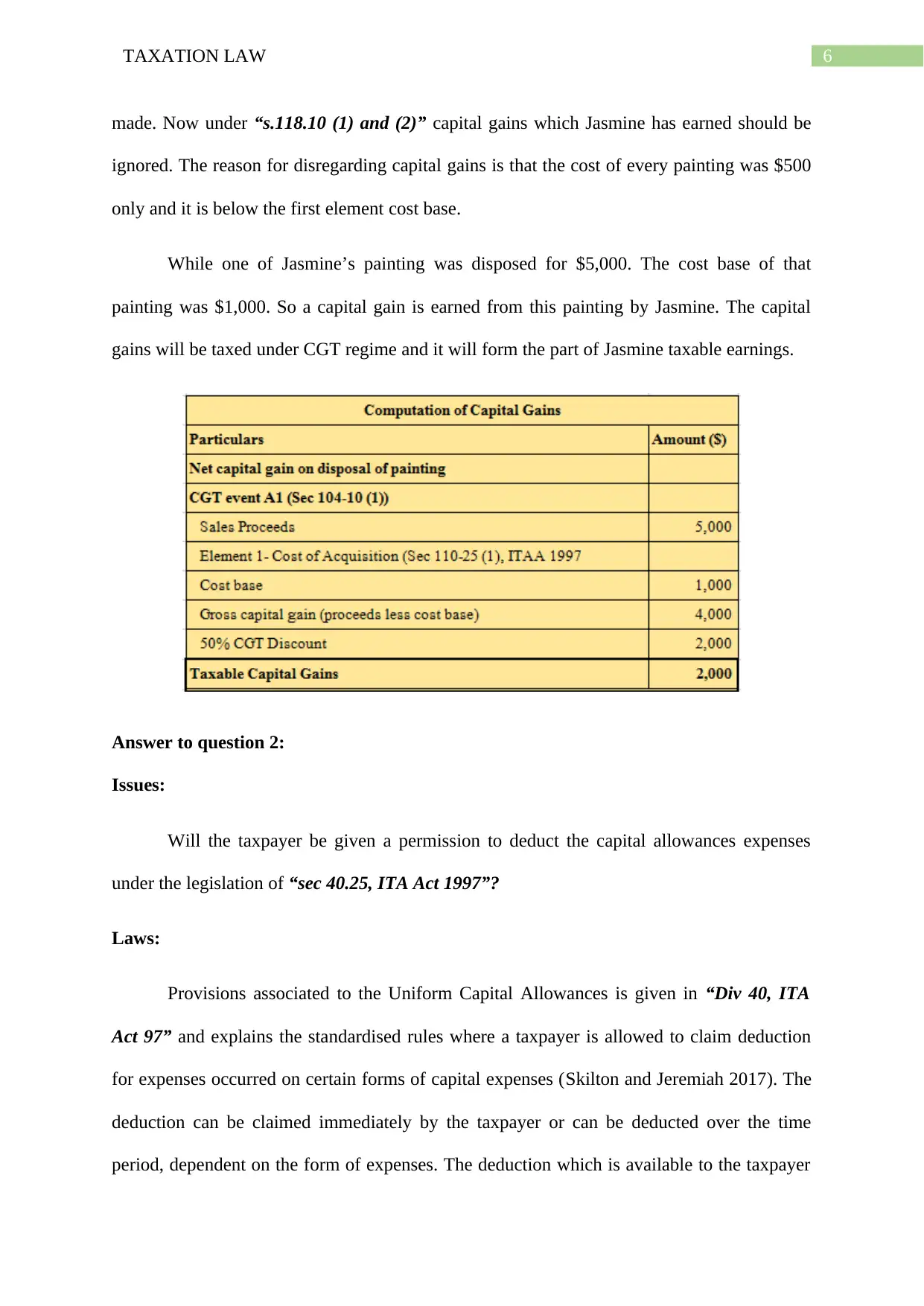

made. Now under “s.118.10 (1) and (2)” capital gains which Jasmine has earned should be

ignored. The reason for disregarding capital gains is that the cost of every painting was $500

only and it is below the first element cost base.

While one of Jasmine’s painting was disposed for $5,000. The cost base of that

painting was $1,000. So a capital gain is earned from this painting by Jasmine. The capital

gains will be taxed under CGT regime and it will form the part of Jasmine taxable earnings.

Answer to question 2:

Issues:

Will the taxpayer be given a permission to deduct the capital allowances expenses

under the legislation of “sec 40.25, ITA Act 1997”?

Laws:

Provisions associated to the Uniform Capital Allowances is given in “Div 40, ITA

Act 97” and explains the standardised rules where a taxpayer is allowed to claim deduction

for expenses occurred on certain forms of capital expenses (Skilton and Jeremiah 2017). The

deduction can be claimed immediately by the taxpayer or can be deducted over the time

period, dependent on the form of expenses. The deduction which is available to the taxpayer

made. Now under “s.118.10 (1) and (2)” capital gains which Jasmine has earned should be

ignored. The reason for disregarding capital gains is that the cost of every painting was $500

only and it is below the first element cost base.

While one of Jasmine’s painting was disposed for $5,000. The cost base of that

painting was $1,000. So a capital gain is earned from this painting by Jasmine. The capital

gains will be taxed under CGT regime and it will form the part of Jasmine taxable earnings.

Answer to question 2:

Issues:

Will the taxpayer be given a permission to deduct the capital allowances expenses

under the legislation of “sec 40.25, ITA Act 1997”?

Laws:

Provisions associated to the Uniform Capital Allowances is given in “Div 40, ITA

Act 97” and explains the standardised rules where a taxpayer is allowed to claim deduction

for expenses occurred on certain forms of capital expenses (Skilton and Jeremiah 2017). The

deduction can be claimed immediately by the taxpayer or can be deducted over the time

period, dependent on the form of expenses. The deduction which is available to the taxpayer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

is regarded as the “capital allowance” and simply substitute the rules of old depreciation. The

taxpayers are permitted to claim deduction for depreciation expenses under “s40.25 (1), ITA

Act 1997”.

The core provision of the “subdiv 40-B” states that;

a. Assets that are depreciable in nature has the limited actual life which is practically

estimated to fall in amount.

b. Approximately, the operational lifespan of depreciating asset represents the period

where it can be useful in generating income.

c. The depreciation of the depreciating asset is completely based on the cost and

valuable life of the asset and not its usual change in value. Under “sec 40.60 (1)”, it

commences from a start time, when the taxpayer starts to use the asset or when the

taxpayer has installed the asset as ready for usage (Bowden 2014).

d. Generally, the owner of the depreciating assets begins to hold the asset and can hence

claim the deduction for the depreciation. At times there will be situation where the

economic owner of the asset will be the different lawful owner and the economic

holder is viewed as the actual holder of asset.

Recognizing the holder of the asset may at times become difficult. As a notable fact, a

taxpayer that holds the asset is permitted for claiming deduction for depreciation on the asset.

In “sec 40-30 (1)”, a depreciating asset is denoted as those assets that has the limited

effective life and these assets are generally anticipated to fall or decline in respect to their

value over its usage time (Freundenberg and Minas 2018). The word depreciation amounts to

writing off the asset that is used by the taxpayer for generating assessable income over the

operative life span of the asset. If the asset is used by taxpayer entirely or 100% for the

is regarded as the “capital allowance” and simply substitute the rules of old depreciation. The

taxpayers are permitted to claim deduction for depreciation expenses under “s40.25 (1), ITA

Act 1997”.

The core provision of the “subdiv 40-B” states that;

a. Assets that are depreciable in nature has the limited actual life which is practically

estimated to fall in amount.

b. Approximately, the operational lifespan of depreciating asset represents the period

where it can be useful in generating income.

c. The depreciation of the depreciating asset is completely based on the cost and

valuable life of the asset and not its usual change in value. Under “sec 40.60 (1)”, it

commences from a start time, when the taxpayer starts to use the asset or when the

taxpayer has installed the asset as ready for usage (Bowden 2014).

d. Generally, the owner of the depreciating assets begins to hold the asset and can hence

claim the deduction for the depreciation. At times there will be situation where the

economic owner of the asset will be the different lawful owner and the economic

holder is viewed as the actual holder of asset.

Recognizing the holder of the asset may at times become difficult. As a notable fact, a

taxpayer that holds the asset is permitted for claiming deduction for depreciation on the asset.

In “sec 40-30 (1)”, a depreciating asset is denoted as those assets that has the limited

effective life and these assets are generally anticipated to fall or decline in respect to their

value over its usage time (Freundenberg and Minas 2018). The word depreciation amounts to

writing off the asset that is used by the taxpayer for generating assessable income over the

operative life span of the asset. If the asset is used by taxpayer entirely or 100% for the

8TAXATION LAW

purpose of generating income, then the taxpayer will be able to claim full amount of

depreciation that is related to the taxable purpose.

Depreciation is generally based assets cost. Under “subdiv 40-C” the cost base of the

asset is ascertained for depreciation purpose (Burgess 2014). Usually, an asset cost base is

divided in two elements. Namely;

I. Element 1: Under “sec 40.180” the element 1 cost base includes the following;

Price that is paid or deemed as paid including the non-cash benefits; or

Construction costs

II. Element 2: Under “sec 40.190”, the element 2 includes the following;

Any cost incurred in installation, re-erection and transportation; plus

Any kind of preliminary non-deductible repairs

Application:

The above explained laws can be applied in the case of John who is running the

manufacturing company. John is found to be the producer of motor vehicle parts and

accessories of BMW. The actual situation says that John has visited Germany and imported a

CNC machine for his manufacturing company. The machine that is imported by John satisfies

the depreciating asset meaning given in “s 40.30 (1), ITA Act 97” (Bain and Boccabella

2019). The CNC machine here is projected to fall in value on the basis of its time of usage

and it only has limited useful life.

“Sub Division 40-C” is referred to calculate the overall cost of the machine for capital

allowance purpose. To determine the Element 1 cost base of the CNC for capital allowance

purpose it is important recognize the price paid to acquire the asset. John on 1st November

paid a sum of $300,000 for the acquisition of the asset (Allerdice 2014). Therefore, under sec

purpose of generating income, then the taxpayer will be able to claim full amount of

depreciation that is related to the taxable purpose.

Depreciation is generally based assets cost. Under “subdiv 40-C” the cost base of the

asset is ascertained for depreciation purpose (Burgess 2014). Usually, an asset cost base is

divided in two elements. Namely;

I. Element 1: Under “sec 40.180” the element 1 cost base includes the following;

Price that is paid or deemed as paid including the non-cash benefits; or

Construction costs

II. Element 2: Under “sec 40.190”, the element 2 includes the following;

Any cost incurred in installation, re-erection and transportation; plus

Any kind of preliminary non-deductible repairs

Application:

The above explained laws can be applied in the case of John who is running the

manufacturing company. John is found to be the producer of motor vehicle parts and

accessories of BMW. The actual situation says that John has visited Germany and imported a

CNC machine for his manufacturing company. The machine that is imported by John satisfies

the depreciating asset meaning given in “s 40.30 (1), ITA Act 97” (Bain and Boccabella

2019). The CNC machine here is projected to fall in value on the basis of its time of usage

and it only has limited useful life.

“Sub Division 40-C” is referred to calculate the overall cost of the machine for capital

allowance purpose. To determine the Element 1 cost base of the CNC for capital allowance

purpose it is important recognize the price paid to acquire the asset. John on 1st November

paid a sum of $300,000 for the acquisition of the asset (Allerdice 2014). Therefore, under sec

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

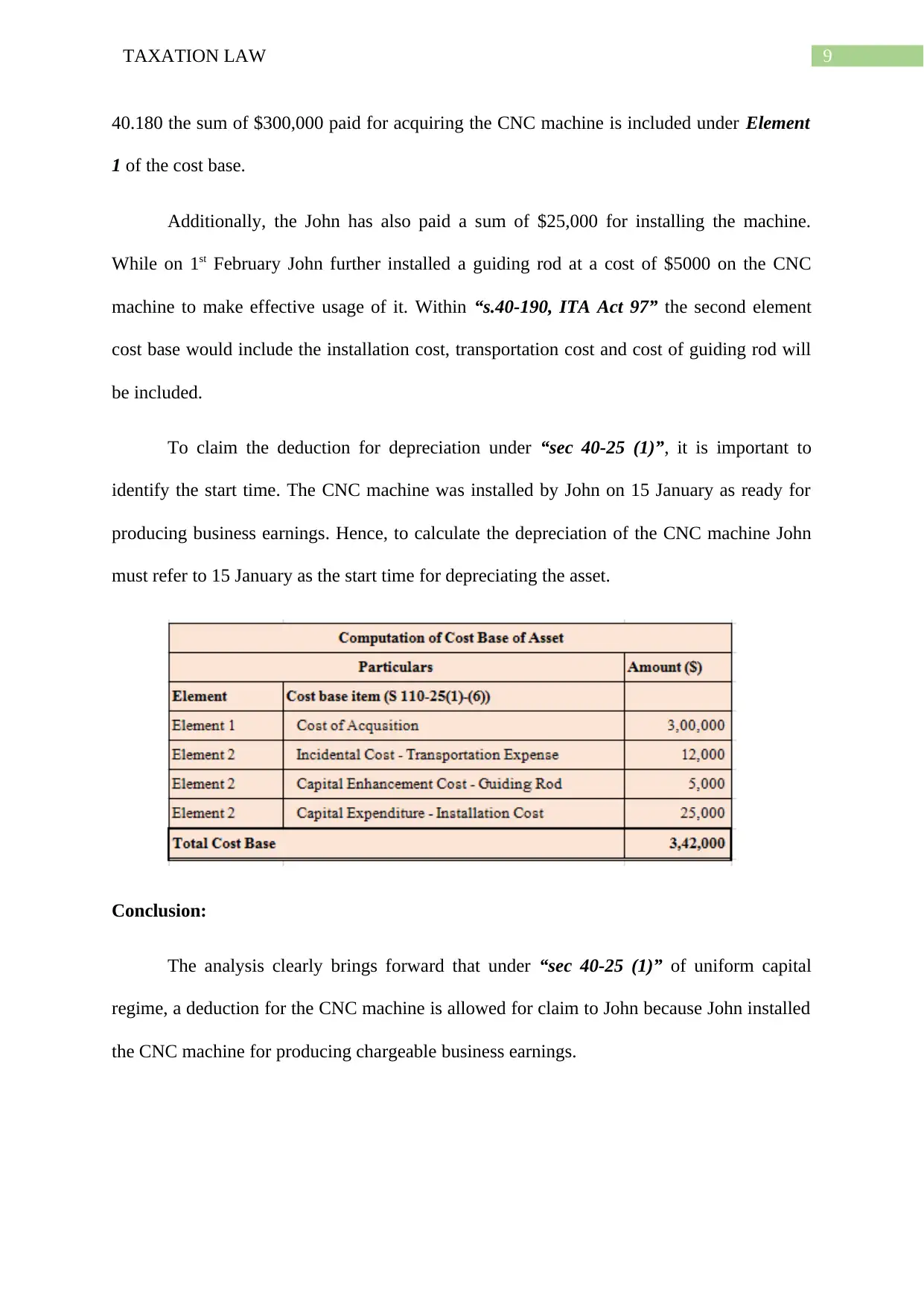

40.180 the sum of $300,000 paid for acquiring the CNC machine is included under Element

1 of the cost base.

Additionally, the John has also paid a sum of $25,000 for installing the machine.

While on 1st February John further installed a guiding rod at a cost of $5000 on the CNC

machine to make effective usage of it. Within “s.40-190, ITA Act 97” the second element

cost base would include the installation cost, transportation cost and cost of guiding rod will

be included.

To claim the deduction for depreciation under “sec 40-25 (1)”, it is important to

identify the start time. The CNC machine was installed by John on 15 January as ready for

producing business earnings. Hence, to calculate the depreciation of the CNC machine John

must refer to 15 January as the start time for depreciating the asset.

Conclusion:

The analysis clearly brings forward that under “sec 40-25 (1)” of uniform capital

regime, a deduction for the CNC machine is allowed for claim to John because John installed

the CNC machine for producing chargeable business earnings.

40.180 the sum of $300,000 paid for acquiring the CNC machine is included under Element

1 of the cost base.

Additionally, the John has also paid a sum of $25,000 for installing the machine.

While on 1st February John further installed a guiding rod at a cost of $5000 on the CNC

machine to make effective usage of it. Within “s.40-190, ITA Act 97” the second element

cost base would include the installation cost, transportation cost and cost of guiding rod will

be included.

To claim the deduction for depreciation under “sec 40-25 (1)”, it is important to

identify the start time. The CNC machine was installed by John on 15 January as ready for

producing business earnings. Hence, to calculate the depreciation of the CNC machine John

must refer to 15 January as the start time for depreciating the asset.

Conclusion:

The analysis clearly brings forward that under “sec 40-25 (1)” of uniform capital

regime, a deduction for the CNC machine is allowed for claim to John because John installed

the CNC machine for producing chargeable business earnings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Allerdice, R., 2014. Interposed companies. Marks' Trusts & Estates: Taxation and Practice,

p.940.

Allerdice, R., 2014. Taxation of other distributions and applications: Items not included in

assessable income. Marks' Trusts & Estates: Taxation and Practice, p.1345.

Bain, K. and Boccabella, D., 2019. The Age of the Home Worker–Part 2: Calculation of

Home Occupancy Expense Deductions, Deduction Apportionment and Partial Loss of CGT

Main Residence Exemption. In Australian Tax Forum (Vol. 34, No. 1).

Barros, C., Teo, E.J. and Hinchliffe, S., 2016. Clash of the deeming provisions: Pre-CGT

concessions, tax consolidation and policy in the federal court. Austl. Tax F., 31, p.509.

Bowden, R., 2014. Dealing with real property in. Taxation in Australia, 48(8), p.415.

Burgess, M., 2014. Testamentary trusts: Bespoke planning opportunities. Taxation in

Australia, 48(9), p.492.

Burgess, M., 2015. Revenue-effective corporate restructures. Taxation in Australia, 50(6),

p.323.

Burnheim, E. and Bobbin, P., 2017. Record keeping tax tips. Equity, 31(9), p.12.

Dean C, 2015. C.T.A., Tax and the sale of a pre-CGT business.

Freundenberg, B. and Minas, J., 2018. Reforming Australia's 50 per cent capital gains tax

discount incrementally. eJTR, 16, p.317.

Mahar, F., 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

p.16.

Mavropoulos, B., 2017. Tax help for Australian start-ups. Taxation in Australia, 52(6), p.319.

References:

Allerdice, R., 2014. Interposed companies. Marks' Trusts & Estates: Taxation and Practice,

p.940.

Allerdice, R., 2014. Taxation of other distributions and applications: Items not included in

assessable income. Marks' Trusts & Estates: Taxation and Practice, p.1345.

Bain, K. and Boccabella, D., 2019. The Age of the Home Worker–Part 2: Calculation of

Home Occupancy Expense Deductions, Deduction Apportionment and Partial Loss of CGT

Main Residence Exemption. In Australian Tax Forum (Vol. 34, No. 1).

Barros, C., Teo, E.J. and Hinchliffe, S., 2016. Clash of the deeming provisions: Pre-CGT

concessions, tax consolidation and policy in the federal court. Austl. Tax F., 31, p.509.

Bowden, R., 2014. Dealing with real property in. Taxation in Australia, 48(8), p.415.

Burgess, M., 2014. Testamentary trusts: Bespoke planning opportunities. Taxation in

Australia, 48(9), p.492.

Burgess, M., 2015. Revenue-effective corporate restructures. Taxation in Australia, 50(6),

p.323.

Burnheim, E. and Bobbin, P., 2017. Record keeping tax tips. Equity, 31(9), p.12.

Dean C, 2015. C.T.A., Tax and the sale of a pre-CGT business.

Freundenberg, B. and Minas, J., 2018. Reforming Australia's 50 per cent capital gains tax

discount incrementally. eJTR, 16, p.317.

Mahar, F., 2016. The distortive effects of the capital gains tax regime. Tax Specialist, 20(1),

p.16.

Mavropoulos, B., 2017. Tax help for Australian start-ups. Taxation in Australia, 52(6), p.319.

11TAXATION LAW

Norbury, M., 2016. Tax cases: Synergy in meaning?. Taxation in Australia, 50(10), p.623.

Skilton, E. and Jeremiah, R., 2017. An alternative to using estate proceeds trusts. Taxation in

Australia, 52(1), p.38.

Slegers, P. and Marateo, D., 2019. Small business restructure roll-over: Planning

issues. Taxation in Australia, 53(8), p.424.

West, M. and Lam, D., 2016. Small business restructure roll-over-Opportunities and

traps. Taxation in Australia, 50(9), p.521.

Norbury, M., 2016. Tax cases: Synergy in meaning?. Taxation in Australia, 50(10), p.623.

Skilton, E. and Jeremiah, R., 2017. An alternative to using estate proceeds trusts. Taxation in

Australia, 52(1), p.38.

Slegers, P. and Marateo, D., 2019. Small business restructure roll-over: Planning

issues. Taxation in Australia, 53(8), p.424.

West, M. and Lam, D., 2016. Small business restructure roll-over-Opportunities and

traps. Taxation in Australia, 50(9), p.521.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.