Holmes Institute HA3042: Taxation Law Individual Assignment T2 2019

VerifiedAdded on 2022/11/14

|6

|2144

|55

Homework Assignment

AI Summary

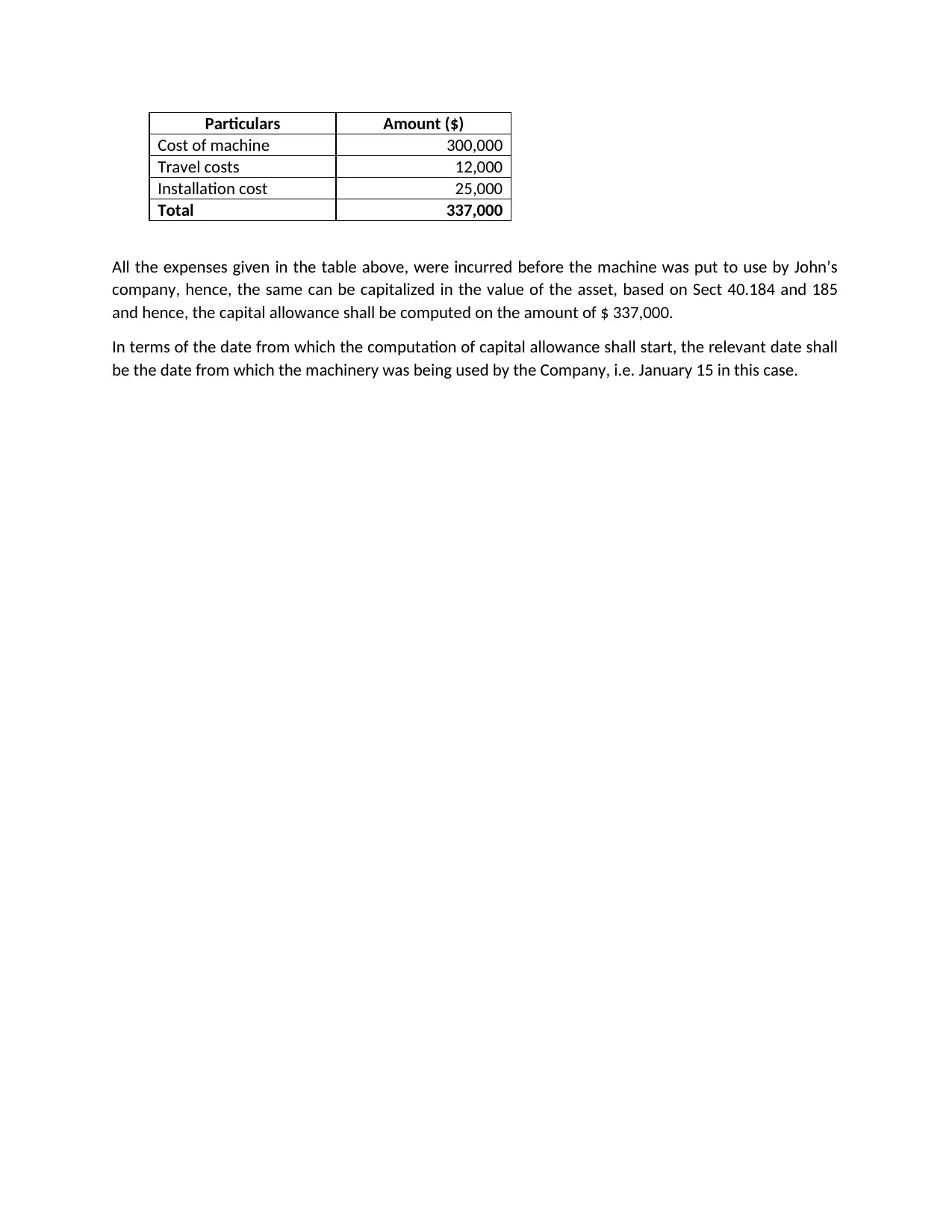

This document presents a comprehensive solution to a taxation law assignment, addressing two main questions. The first question analyzes various transactions involving capital assets, including a house, a car, a small cleaning business, furniture, and paintings, to determine the applicability of Capital Gains Tax (CGT) and relevant exemptions. The analysis considers the residency status of the individual, the nature of the assets (personal use, collectables, business), and specific provisions of the Income Tax Assessment Act 1997, such as the pre-1985 asset exemption, the small business CGT exemption, and the exclusions for personal use assets and collectables. The second question focuses on the capitalization and depreciation of an industrial CNC machine purchased by a manufacturing company, detailing the costs to be included in the asset's value and the date from which depreciation should commence. The solution references relevant sections of the Income Tax Assessment Act and provides a detailed breakdown of the costs incurred, concluding with the total cost for capitalization and the starting date for capital allowance computation. References to academic sources are included to support the analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.