Halfords Group Plc: Financial Analysis, Investment & Acquisition

VerifiedAdded on 2023/06/13

|16

|3418

|266

Report

AI Summary

This report evaluates the financial position and performance of Halfords Group Plc, including a ratio analysis of profitability and liquidity. It assesses a potential investment project involving car part manufacturing, concluding that the project's IRR is lower than the cost of capital, making it unviable. The report further explores the possibility of acquiring ScS Group Plc, determining that the acquisition would likely be profitable based on discounted cash flow analysis and intrinsic value calculations. Ultimately, the report recommends that Halfords focus on acquisition over new project investment to enhance market share and revenue.

Running Head: Financial Analysis

1

Project Report: Financial analysis

1

Project Report: Financial analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis

2

Contents

Introduction.......................................................................................................................3

Evaluation of financial statement of Halfords..................................................................3

Invest appraisal techniques...............................................................................................5

Potential Target Company................................................................................................6

Conclusion........................................................................................................................8

References.........................................................................................................................9

Appendix.........................................................................................................................11

2

Contents

Introduction.......................................................................................................................3

Evaluation of financial statement of Halfords..................................................................3

Invest appraisal techniques...............................................................................................5

Potential Target Company................................................................................................6

Conclusion........................................................................................................................8

References.........................................................................................................................9

Appendix.........................................................................................................................11

Financial Analysis

3

Introduction:

The report has been prepared to evaluate about the Halfords limited. Being a chief

financial officer of a company, it is required to evaluate and analyze the financial position

and performance of the company. All the financial decisions of the company are required to

be done by the chief financial officer in such a way that the funds could be raised by the

company in minimum price and invested in the project from where maximum return could be

earned. In the report, financial statement of the Halfords limited has been evaluated firstly to

recognize the profitability and the short term debt obligation position of the company.

Further, the reports lead to the investment project evaluation of the company and lastly, it has

been identified that whether the company should acquire another company for the

diversification or not.

Evaluation of financial statement of Halfords:

Halfords group plc is retailing company which operates its business in UK market and

Ireland market. The company retails the car accessories, car audio, bicycles, ripspeed, tools,

child seats etc. further, various services are also provided by the company such as Bicycle

repair, Audio installation, vehicle part, fitting etc. the company has been founded in 1892 and

currently the revenue of the company is £ 1095 million (Home, 2018). The financial and non

financial position of the company is quite competitive. Being a chief financial officer of the

company, financial statement of the company has been evaluated firstly to identify that

whether the company would be able to make profit or not. The ratio analysis study of the

company is as follows:

Profitability:

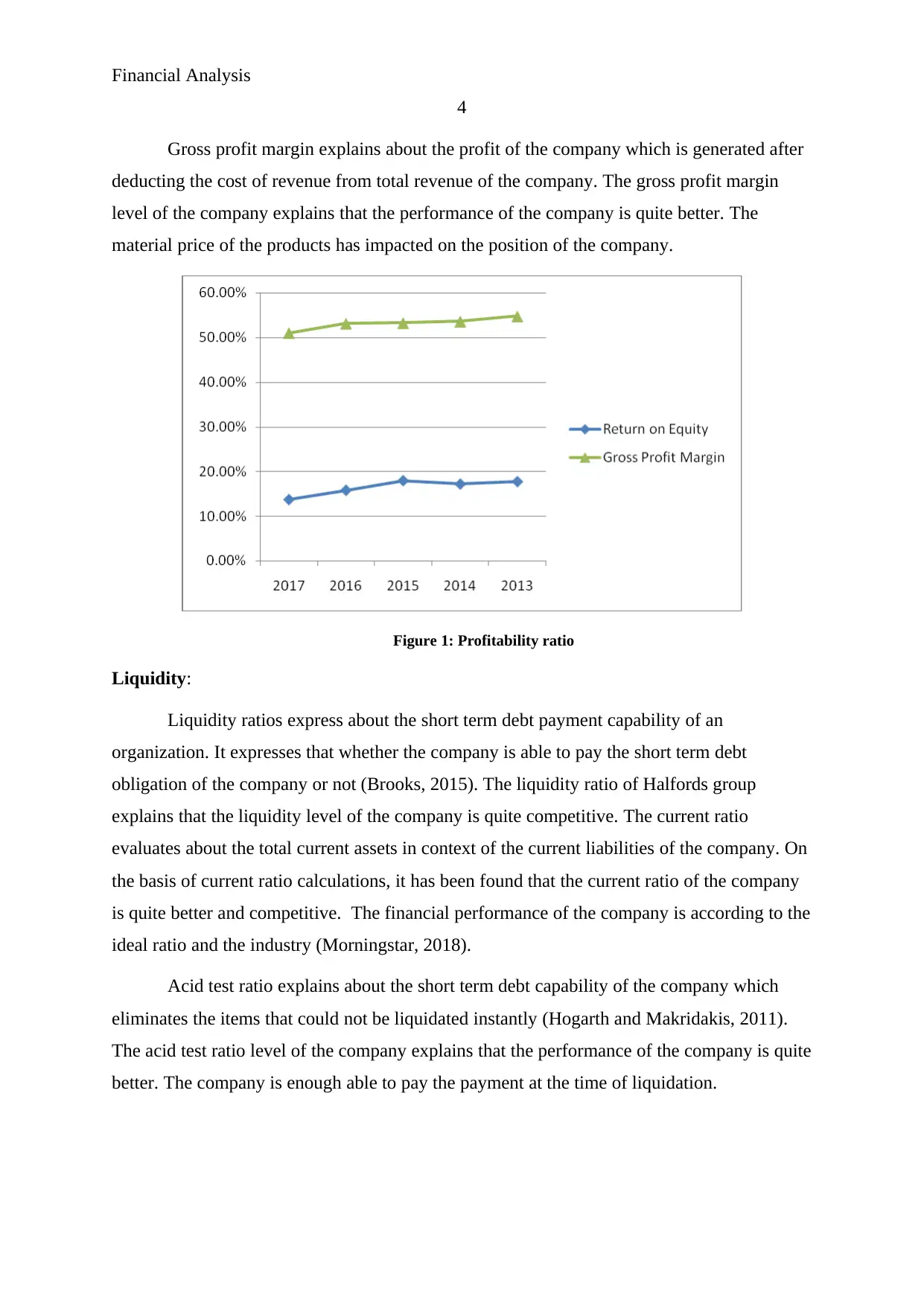

Profitability ratios express about the profit making capability of an organization. It

express that whether the company is able to make enough profits for the equity holder and

whether the resources of the company are enough (Kaplan and Atkinson, 2015). The

profitability ratio of Halfords group explains that the profitability level of the company has

been lowered in year 2017. The return on equity ratio evaluates about the total profit in

context of the total equity of the company. On the basis of Return on equity calculations, it

has been found that the return on equity in current year has been lowered due to changes in

the industry. Though, the financial performance of the company is according to the ideal ratio

(more than 15%) (Fridson and Alvarez, 2011).

3

Introduction:

The report has been prepared to evaluate about the Halfords limited. Being a chief

financial officer of a company, it is required to evaluate and analyze the financial position

and performance of the company. All the financial decisions of the company are required to

be done by the chief financial officer in such a way that the funds could be raised by the

company in minimum price and invested in the project from where maximum return could be

earned. In the report, financial statement of the Halfords limited has been evaluated firstly to

recognize the profitability and the short term debt obligation position of the company.

Further, the reports lead to the investment project evaluation of the company and lastly, it has

been identified that whether the company should acquire another company for the

diversification or not.

Evaluation of financial statement of Halfords:

Halfords group plc is retailing company which operates its business in UK market and

Ireland market. The company retails the car accessories, car audio, bicycles, ripspeed, tools,

child seats etc. further, various services are also provided by the company such as Bicycle

repair, Audio installation, vehicle part, fitting etc. the company has been founded in 1892 and

currently the revenue of the company is £ 1095 million (Home, 2018). The financial and non

financial position of the company is quite competitive. Being a chief financial officer of the

company, financial statement of the company has been evaluated firstly to identify that

whether the company would be able to make profit or not. The ratio analysis study of the

company is as follows:

Profitability:

Profitability ratios express about the profit making capability of an organization. It

express that whether the company is able to make enough profits for the equity holder and

whether the resources of the company are enough (Kaplan and Atkinson, 2015). The

profitability ratio of Halfords group explains that the profitability level of the company has

been lowered in year 2017. The return on equity ratio evaluates about the total profit in

context of the total equity of the company. On the basis of Return on equity calculations, it

has been found that the return on equity in current year has been lowered due to changes in

the industry. Though, the financial performance of the company is according to the ideal ratio

(more than 15%) (Fridson and Alvarez, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis

4

Gross profit margin explains about the profit of the company which is generated after

deducting the cost of revenue from total revenue of the company. The gross profit margin

level of the company explains that the performance of the company is quite better. The

material price of the products has impacted on the position of the company.

Figure 1: Profitability ratio

Liquidity:

Liquidity ratios express about the short term debt payment capability of an

organization. It expresses that whether the company is able to pay the short term debt

obligation of the company or not (Brooks, 2015). The liquidity ratio of Halfords group

explains that the liquidity level of the company is quite competitive. The current ratio

evaluates about the total current assets in context of the current liabilities of the company. On

the basis of current ratio calculations, it has been found that the current ratio of the company

is quite better and competitive. The financial performance of the company is according to the

ideal ratio and the industry (Morningstar, 2018).

Acid test ratio explains about the short term debt capability of the company which

eliminates the items that could not be liquidated instantly (Hogarth and Makridakis, 2011).

The acid test ratio level of the company explains that the performance of the company is quite

better. The company is enough able to pay the payment at the time of liquidation.

4

Gross profit margin explains about the profit of the company which is generated after

deducting the cost of revenue from total revenue of the company. The gross profit margin

level of the company explains that the performance of the company is quite better. The

material price of the products has impacted on the position of the company.

Figure 1: Profitability ratio

Liquidity:

Liquidity ratios express about the short term debt payment capability of an

organization. It expresses that whether the company is able to pay the short term debt

obligation of the company or not (Brooks, 2015). The liquidity ratio of Halfords group

explains that the liquidity level of the company is quite competitive. The current ratio

evaluates about the total current assets in context of the current liabilities of the company. On

the basis of current ratio calculations, it has been found that the current ratio of the company

is quite better and competitive. The financial performance of the company is according to the

ideal ratio and the industry (Morningstar, 2018).

Acid test ratio explains about the short term debt capability of the company which

eliminates the items that could not be liquidated instantly (Hogarth and Makridakis, 2011).

The acid test ratio level of the company explains that the performance of the company is quite

better. The company is enough able to pay the payment at the time of liquidation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis

5

Figure 2: Liquidity ratio

Invest appraisal techniques:

Investment appraisal techniques are the process to recognize the investment and

project options of an organization. It is an evaluation process which includes various tools to

identify that whether the project should be accepted by the company or not. It examines the

cash inflow and outflow of the project and on the basis of that a decision is made about the

acceptance or rejection of a project (Brown, 2015). This process is used by every

organization to make better decision about the projects and investment opportunities.

In the given case, Halfords limited is planning to invest into a new project in which

the car parts would be manufactured by the company. The investment opportunity explains

that the company would have to invest £ 3,00,00,000 in the plant and the plant would run for

10 years with no salvage value (Besley and Brigham, 2008). Further, the cash inflow of the

company has been evaluated on the basis of industry position and the production process of

the company and it has been found that the capacity of the plant would be 4,00,000 units to

5,00,000 units and the selling price of the parts would be £ 60. Thus the cash inflow of the

project would be £ 55,00,000 to £ 70,00,000.

The investment appraisal technique of the company examines the net present value

and the internal rate of return of the project further. Net present value is the process which

recognize the net cash flow of the project, if the cash flow is positive than the project should

be accepted otherwise company should reject the proposal (Titman and Martin, 2014). The

5

Figure 2: Liquidity ratio

Invest appraisal techniques:

Investment appraisal techniques are the process to recognize the investment and

project options of an organization. It is an evaluation process which includes various tools to

identify that whether the project should be accepted by the company or not. It examines the

cash inflow and outflow of the project and on the basis of that a decision is made about the

acceptance or rejection of a project (Brown, 2015). This process is used by every

organization to make better decision about the projects and investment opportunities.

In the given case, Halfords limited is planning to invest into a new project in which

the car parts would be manufactured by the company. The investment opportunity explains

that the company would have to invest £ 3,00,00,000 in the plant and the plant would run for

10 years with no salvage value (Besley and Brigham, 2008). Further, the cash inflow of the

company has been evaluated on the basis of industry position and the production process of

the company and it has been found that the capacity of the plant would be 4,00,000 units to

5,00,000 units and the selling price of the parts would be £ 60. Thus the cash inflow of the

project would be £ 55,00,000 to £ 70,00,000.

The investment appraisal technique of the company examines the net present value

and the internal rate of return of the project further. Net present value is the process which

recognize the net cash flow of the project, if the cash flow is positive than the project should

be accepted otherwise company should reject the proposal (Titman and Martin, 2014). The

Financial Analysis

6

net present value of the project is £ 51,31,380 in case of 5,00,000 units and - £ 23,96,773. It

explains that if the capacity and the sale of the products would be 5,00,000 units than only the

project should be accepted by the company otherwise the project would lead to the company

towards loss (Higgins, 2012).

Further, internal rate of return is the total return percentage of the project where the

net present value of the project is zero (madhura, 2011). The internal rate of return of the

project is compared with the cost of capital of the company. If the cost of capital of the

company is lower than the internal rate of return, project should be accepted by the company

otherwise vice-versa.

. The internal rate of return of the project is -2.83% in case of 5,00,000 units and

3.62% in case of 4,00,000 units. It explains that in both the cases, the cost of capital of the

company (15%) would be higher than the internal rate of return of the project and thus the

proposal should not be accepted (Gibson, 2011).

The study of new project on the company explains that the net present value of the

project is better but the internal rate of return of the company is lower than the cost of capital.

So, the company should not invest into the project. Rather than investing into the new project,

company should focus on the existing project so that more revenue could be generated from

that.

Potential Target Company:

A company always looks for various ways to diversify its market so that the more

revenue could be generated by the company as well as the market share of the company could

also be enhanced. Acquisition is one of the ways through which the company could diversify

its market and meet the goals of the company. In acquisition, a company is targeted by the

potential acquirer to evaluate that the whether the company should be acquired or not. There

are various ways to evaluate that the acquisition process would be beneficial for the company

or not (Koller, Goedhart and Wessels, 2010).

In Halfords plc, if the company wants to diversify its market, than acquisition is a

good option for the company. The main target of the company should be ScS group plc. ScS

group plc has been chosen for the acquisition because of its market share and the better

financial position of the company. The company is operating in the same business and thus, it

would help the company to meet the objectives of more market share and greater revenue.

6

net present value of the project is £ 51,31,380 in case of 5,00,000 units and - £ 23,96,773. It

explains that if the capacity and the sale of the products would be 5,00,000 units than only the

project should be accepted by the company otherwise the project would lead to the company

towards loss (Higgins, 2012).

Further, internal rate of return is the total return percentage of the project where the

net present value of the project is zero (madhura, 2011). The internal rate of return of the

project is compared with the cost of capital of the company. If the cost of capital of the

company is lower than the internal rate of return, project should be accepted by the company

otherwise vice-versa.

. The internal rate of return of the project is -2.83% in case of 5,00,000 units and

3.62% in case of 4,00,000 units. It explains that in both the cases, the cost of capital of the

company (15%) would be higher than the internal rate of return of the project and thus the

proposal should not be accepted (Gibson, 2011).

The study of new project on the company explains that the net present value of the

project is better but the internal rate of return of the company is lower than the cost of capital.

So, the company should not invest into the project. Rather than investing into the new project,

company should focus on the existing project so that more revenue could be generated from

that.

Potential Target Company:

A company always looks for various ways to diversify its market so that the more

revenue could be generated by the company as well as the market share of the company could

also be enhanced. Acquisition is one of the ways through which the company could diversify

its market and meet the goals of the company. In acquisition, a company is targeted by the

potential acquirer to evaluate that the whether the company should be acquired or not. There

are various ways to evaluate that the acquisition process would be beneficial for the company

or not (Koller, Goedhart and Wessels, 2010).

In Halfords plc, if the company wants to diversify its market, than acquisition is a

good option for the company. The main target of the company should be ScS group plc. ScS

group plc has been chosen for the acquisition because of its market share and the better

financial position of the company. The company is operating in the same business and thus, it

would help the company to meet the objectives of more market share and greater revenue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis

7

The financial performance and the annual report of the company of last few year has

been analyzed to identify that whether the acquisition would be beneficial for the company or

not. The project has explained that the financial performance of the company is quite better.

The company is performing well in terms of financial position as well as non financial

position. If the company would acquire the ScS group plc than the market share of the

company would definitely be greater.

The financial position of the company explains about the continuous growth in the

company. Future performance and position of the company has been evaluated further on the

basis of discounted cash flow technique and it has been found that the cash flow of the

company would be increased by 17.07% in next 5 years on the other hand; the inflation rate

of the company would be enhanced by 3.33% (Brigham and Ehrhardt, 2013). It explains that

the company’s growth is quite higher than the inflation rate.

The estimated cash flow of the company of next 5 years has been calculated

and it has been found that the terminal cash flow of the company after 5 years would be £

56,544.99 (Morningstar, 2018). It explains about better incremental position of the company.

Further, the present value of the terminal cash flows of the company has been evaluated and

it has been recognized that the total worth of the company is £ 5,52,897.85 which includes £

1,16,5000 worth of debt and rest amount is related to the equity of the company (Brigham

and Houston, 2012).

The calculations further explains that the total equity of ScS is £ 4,33,398 and the

number of issued share of the company is 2000 which explains that the per share value of the

company is £ 216.7. Though, the market value of the company is £ 210. It explains that the

intrinsic value of the company is higher and thus the acquisition process would help the

company to generate more profits and meet the goals and mission of the company (appendix).

The Halfords group plc would be required to pay £ 210 to each shareholder of the

company whereas the total worth of per share of the company is £ 216.7. It would lead the

company to great profits and the financial position of the project is also better which would

assist the company to meet its objectives (Vogel, 2014).

On the basis of financial performance, investment appraisal techniques and the

acquisition plan of the company, it has been found that the company should invest into the

7

The financial performance and the annual report of the company of last few year has

been analyzed to identify that whether the acquisition would be beneficial for the company or

not. The project has explained that the financial performance of the company is quite better.

The company is performing well in terms of financial position as well as non financial

position. If the company would acquire the ScS group plc than the market share of the

company would definitely be greater.

The financial position of the company explains about the continuous growth in the

company. Future performance and position of the company has been evaluated further on the

basis of discounted cash flow technique and it has been found that the cash flow of the

company would be increased by 17.07% in next 5 years on the other hand; the inflation rate

of the company would be enhanced by 3.33% (Brigham and Ehrhardt, 2013). It explains that

the company’s growth is quite higher than the inflation rate.

The estimated cash flow of the company of next 5 years has been calculated

and it has been found that the terminal cash flow of the company after 5 years would be £

56,544.99 (Morningstar, 2018). It explains about better incremental position of the company.

Further, the present value of the terminal cash flows of the company has been evaluated and

it has been recognized that the total worth of the company is £ 5,52,897.85 which includes £

1,16,5000 worth of debt and rest amount is related to the equity of the company (Brigham

and Houston, 2012).

The calculations further explains that the total equity of ScS is £ 4,33,398 and the

number of issued share of the company is 2000 which explains that the per share value of the

company is £ 216.7. Though, the market value of the company is £ 210. It explains that the

intrinsic value of the company is higher and thus the acquisition process would help the

company to generate more profits and meet the goals and mission of the company (appendix).

The Halfords group plc would be required to pay £ 210 to each shareholder of the

company whereas the total worth of per share of the company is £ 216.7. It would lead the

company to great profits and the financial position of the project is also better which would

assist the company to meet its objectives (Vogel, 2014).

On the basis of financial performance, investment appraisal techniques and the

acquisition plan of the company, it has been found that the company should invest into the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis

8

acquisition rather than investing into the new plan as it would assist the company to generate

more profits and meet the goals and mission of the company.

Conclusion:

To conclude, the financial position of the company is quite better. The

profitability ratio of the company explains about better position of the company from last 5

years. Though, the current performance of the company has been lowered due to high

material price. Further, the liquidity position of the company is quite competitive and

explains about lower risk position of the company in the industry. In addition, the study of

new project on the company explains that the net present value of the project is better but the

internal rate of return of the company is lower than the cost of capital. So, the company

should not invest into the project. Rather than investing into the new project, company should

focus on the existing project so that more revenue could be generated from that.

Lastly, in case of acquisition, the acquisition of ScS group plc would lead the

company to great profits and the financial position of the project is also better which would

assist the company to meet its objectives. On the basis of financial performance, investment

appraisal techniques and the acquisition plan of the company, it has been found that the

company should invest into the acquisition rather than investing into the new plan as it would

assist the company to generate more profits and meet the goals and mission of the company.

8

acquisition rather than investing into the new plan as it would assist the company to generate

more profits and meet the goals and mission of the company.

Conclusion:

To conclude, the financial position of the company is quite better. The

profitability ratio of the company explains about better position of the company from last 5

years. Though, the current performance of the company has been lowered due to high

material price. Further, the liquidity position of the company is quite competitive and

explains about lower risk position of the company in the industry. In addition, the study of

new project on the company explains that the net present value of the project is better but the

internal rate of return of the company is lower than the cost of capital. So, the company

should not invest into the project. Rather than investing into the new project, company should

focus on the existing project so that more revenue could be generated from that.

Lastly, in case of acquisition, the acquisition of ScS group plc would lead the

company to great profits and the financial position of the project is also better which would

assist the company to meet its objectives. On the basis of financial performance, investment

appraisal techniques and the acquisition plan of the company, it has been found that the

company should invest into the acquisition rather than investing into the new plan as it would

assist the company to generate more profits and meet the goals and mission of the company.

Financial Analysis

9

References:

Besley, S. and Brigham, E.F., 2008. Essentials of managerial finance. Thomson South-

Western.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Brown, R., 2012. Analysis of investments & management of portfolios. Pearson Higher Ed.

Fridson, M.S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's

guide (Vol. 597). John Wiley & Sons.

Gibson, C.H., 2011. Financial reporting and analysis. South-Western Cengage Learning.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hogarth, R.M. and Makridakis, S., 2011. Forecasting and planning: An

evaluation. Management science, 27(2), pp.115-138.

Home. 2018. Halfords group plc. [Online]. Available at: http://www.halfordscompany.com/

[Accessed as on 25th April 2018].

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Koller, T., Goedhart, M. and Wessels, D., 2010. Valuation: measuring and managing the

value of companies (Vol. 499). john Wiley and sons.

Madura, J., 2011. International financial management. Cengage Learning.

Morningstar. 2018. Halfords group plc. [Online]. Available at:

http://financials.morningstar.com/cash-flow/cf.html?

t=XFRA:HDK®ion=deu&culture=en-US [Accessed as on 25th April 2018].

Morningstar. 2018. ScS group plc. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?t=SCS®ion=gbr [Accessed as

on 25th April 2018].

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

9

References:

Besley, S. and Brigham, E.F., 2008. Essentials of managerial finance. Thomson South-

Western.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Brown, R., 2012. Analysis of investments & management of portfolios. Pearson Higher Ed.

Fridson, M.S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's

guide (Vol. 597). John Wiley & Sons.

Gibson, C.H., 2011. Financial reporting and analysis. South-Western Cengage Learning.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hogarth, R.M. and Makridakis, S., 2011. Forecasting and planning: An

evaluation. Management science, 27(2), pp.115-138.

Home. 2018. Halfords group plc. [Online]. Available at: http://www.halfordscompany.com/

[Accessed as on 25th April 2018].

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Koller, T., Goedhart, M. and Wessels, D., 2010. Valuation: measuring and managing the

value of companies (Vol. 499). john Wiley and sons.

Madura, J., 2011. International financial management. Cengage Learning.

Morningstar. 2018. Halfords group plc. [Online]. Available at:

http://financials.morningstar.com/cash-flow/cf.html?

t=XFRA:HDK®ion=deu&culture=en-US [Accessed as on 25th April 2018].

Morningstar. 2018. ScS group plc. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?t=SCS®ion=gbr [Accessed as

on 25th April 2018].

Titman, S. and Martin, J.D., 2014. Valuation. Pearson Higher Ed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Analysis

10

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

10

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Analysis

11

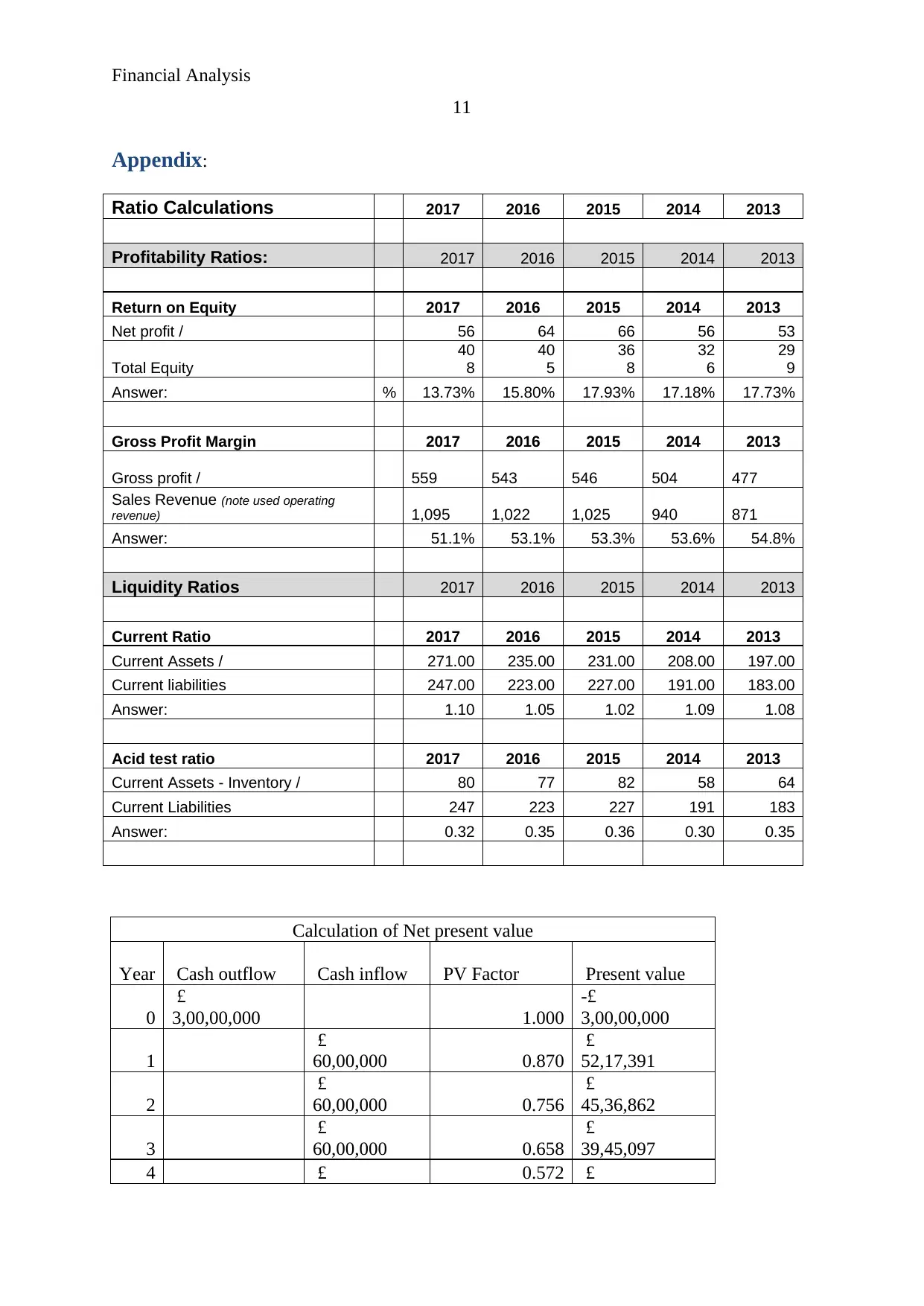

Appendix:

Ratio Calculations 2017 2016 2015 2014 2013

Profitability Ratios: 2017 2016 2015 2014 2013

Return on Equity 2017 2016 2015 2014 2013

Net profit / 56 64 66 56 53

Total Equity

40

8

40

5

36

8

32

6

29

9

Answer: % 13.73% 15.80% 17.93% 17.18% 17.73%

Gross Profit Margin 2017 2016 2015 2014 2013

Gross profit / 559 543 546 504 477

Sales Revenue (note used operating

revenue) 1,095 1,022 1,025 940 871

Answer: 51.1% 53.1% 53.3% 53.6% 54.8%

Liquidity Ratios 2017 2016 2015 2014 2013

Current Ratio 2017 2016 2015 2014 2013

Current Assets / 271.00 235.00 231.00 208.00 197.00

Current liabilities 247.00 223.00 227.00 191.00 183.00

Answer: 1.10 1.05 1.02 1.09 1.08

Acid test ratio 2017 2016 2015 2014 2013

Current Assets - Inventory / 80 77 82 58 64

Current Liabilities 247 223 227 191 183

Answer: 0.32 0.35 0.36 0.30 0.35

Calculation of Net present value

Year Cash outflow Cash inflow PV Factor Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.870

£

52,17,391

2

£

60,00,000 0.756

£

45,36,862

3

£

60,00,000 0.658

£

39,45,097

4 £ 0.572 £

11

Appendix:

Ratio Calculations 2017 2016 2015 2014 2013

Profitability Ratios: 2017 2016 2015 2014 2013

Return on Equity 2017 2016 2015 2014 2013

Net profit / 56 64 66 56 53

Total Equity

40

8

40

5

36

8

32

6

29

9

Answer: % 13.73% 15.80% 17.93% 17.18% 17.73%

Gross Profit Margin 2017 2016 2015 2014 2013

Gross profit / 559 543 546 504 477

Sales Revenue (note used operating

revenue) 1,095 1,022 1,025 940 871

Answer: 51.1% 53.1% 53.3% 53.6% 54.8%

Liquidity Ratios 2017 2016 2015 2014 2013

Current Ratio 2017 2016 2015 2014 2013

Current Assets / 271.00 235.00 231.00 208.00 197.00

Current liabilities 247.00 223.00 227.00 191.00 183.00

Answer: 1.10 1.05 1.02 1.09 1.08

Acid test ratio 2017 2016 2015 2014 2013

Current Assets - Inventory / 80 77 82 58 64

Current Liabilities 247 223 227 191 183

Answer: 0.32 0.35 0.36 0.30 0.35

Calculation of Net present value

Year Cash outflow Cash inflow PV Factor Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.870

£

52,17,391

2

£

60,00,000 0.756

£

45,36,862

3

£

60,00,000 0.658

£

39,45,097

4 £ 0.572 £

Financial Analysis

12

60,00,000 34,30,519

5

£

60,00,000 0.497

£

29,83,060

6

£

60,00,000 0.432

£

25,93,966

7

£

60,00,000 0.376

£

22,55,622

8

£

60,00,000 0.327

£

19,61,411

9

£

60,00,000 0.284

£

17,05,574

10

£

60,00,000 0.247

£

14,83,108

Net present value = cash inflow - cash outflow

£

1,12,612

Calculation of Internal rate of return

Year Cash outflow Cash inflow

PV Factor

(20%) Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.833

£

50,00,000

2

£

60,00,000 0.694

£

41,66,667

3

£

60,00,000 0.579

£

34,72,222

4

£

60,00,000 0.482

£

28,93,519

5

£

60,00,000 0.402

£

24,11,265

6

£

60,00,000 0.335

£

20,09,388

7

£

60,00,000 0.279

£

16,74,490

8

£

60,00,000 0.233

£

13,95,408

9

£

60,00,000 0.194

£

11,62,840

10

£

60,00,000 0.162

£

9,69,033

Internal rate of return 11.31%

Units 10,00,000

Selling Price per unit 32

12

60,00,000 34,30,519

5

£

60,00,000 0.497

£

29,83,060

6

£

60,00,000 0.432

£

25,93,966

7

£

60,00,000 0.376

£

22,55,622

8

£

60,00,000 0.327

£

19,61,411

9

£

60,00,000 0.284

£

17,05,574

10

£

60,00,000 0.247

£

14,83,108

Net present value = cash inflow - cash outflow

£

1,12,612

Calculation of Internal rate of return

Year Cash outflow Cash inflow

PV Factor

(20%) Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.833

£

50,00,000

2

£

60,00,000 0.694

£

41,66,667

3

£

60,00,000 0.579

£

34,72,222

4

£

60,00,000 0.482

£

28,93,519

5

£

60,00,000 0.402

£

24,11,265

6

£

60,00,000 0.335

£

20,09,388

7

£

60,00,000 0.279

£

16,74,490

8

£

60,00,000 0.233

£

13,95,408

9

£

60,00,000 0.194

£

11,62,840

10

£

60,00,000 0.162

£

9,69,033

Internal rate of return 11.31%

Units 10,00,000

Selling Price per unit 32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.