Halfords Group plc: Financial Analysis, Investment, Target Company

VerifiedAdded on 2023/06/12

|11

|2474

|239

Report

AI Summary

This report presents a comprehensive financial analysis of Halfords Group plc, undertaken from a Chief Financial Officer's perspective. It begins by evaluating Halfords' financial statements to assess its performance and industry position. The report then delves into a proposed new project, a bicycle manufacturing plant, analyzing its potential profitability using investment appraisal techniques such as Net Present Value (NPV) and Internal Rate of Return (IRR). The analysis suggests that the project's IRR is lower than the company's cost of capital, advising against its acceptance. Furthermore, the report identifies and evaluates ScS Group plc as a potential acquisition target, employing discounted cash flow analysis to determine its intrinsic value. The analysis indicates that ScS Group is undervalued, making it a potentially profitable acquisition for Halfords to expand its market share. The report concludes by recommending against the bicycle manufacturing plant investment and advocating for the acquisition of ScS Group.

Running Head: Corporate Financial Analysis

1

Project Report: Corporate Financial Analysis

1

Project Report: Corporate Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Analysis

2

Contents

Introduction.......................................................................................................................3

Investment appraisal techniques.......................................................................................3

Potential Target Company................................................................................................4

Conclusion........................................................................................................................5

References.........................................................................................................................7

Appendix...........................................................................................................................8

2

Contents

Introduction.......................................................................................................................3

Investment appraisal techniques.......................................................................................3

Potential Target Company................................................................................................4

Conclusion........................................................................................................................5

References.........................................................................................................................7

Appendix...........................................................................................................................8

Corporate Financial Analysis

3

Introduction:

Financial analysis is a process which is conducted by the comapny and its

stakeholders to evaluate and identify the performance of the company. There are various

techniques of corporate finance which is used by the different stakeholders of the company.

In the given case, financial analysis study has been conducted on the business point of view.

Being a chief financial officer of a company, it becomes important for the officer to evaluate

and make decisions about all the financial transactions and activities of the company. In the

report, Halfords group plc has been taken into the concern. Being a chief financial officer of

Halfords group plc, financial statement of the company has been evaluated firstly to

recognize the performance of the company and the position of the company in the industry.

Further, the new projects of the company has been identified and it has been evaluated that

whether the company would be able to generate better inflows from the project and lastly, the

target company has been evaluated for the purpose of acquisition.

Investment appraisal techniques:

Halfords limited is a British company which operates its business in retailing the car

parts, camping, touring equipment, camping equipment and bicycle in the UK and Ireland.

The company has been founded in 1892 (Home, 2018). The company also offer various

services to its customers such as Bicycle repair and car accessories installation. The study has

been performed on the company to evaluate the performance of the company.

Investment appraisal techniques are also known as capital budgeting. The process is

done by the financial manager and officer of a company to evaluate the new projects of the

company and their returns. These techniques make it easier for the organization to make

decision about the acceptance of the project (Fridson and Alvarez, 2011).

Being the chief financial officer of the company, it becomes important to evaluate the

new project (Bicycle manufacturing plant) of the company in which company is planning to

invest £ 3,00,00,000. The life of the project would be 10 years and on the basis of the last 5

years cash flows of the company and the trend in the market, it has been found that whether

the project would offer good return to the company or not.

Firstly, the cash inflows of the company has been evaluated and it has been found that

with the help of this new project the sales units of the company would be 8,00,000 to

3

Introduction:

Financial analysis is a process which is conducted by the comapny and its

stakeholders to evaluate and identify the performance of the company. There are various

techniques of corporate finance which is used by the different stakeholders of the company.

In the given case, financial analysis study has been conducted on the business point of view.

Being a chief financial officer of a company, it becomes important for the officer to evaluate

and make decisions about all the financial transactions and activities of the company. In the

report, Halfords group plc has been taken into the concern. Being a chief financial officer of

Halfords group plc, financial statement of the company has been evaluated firstly to

recognize the performance of the company and the position of the company in the industry.

Further, the new projects of the company has been identified and it has been evaluated that

whether the company would be able to generate better inflows from the project and lastly, the

target company has been evaluated for the purpose of acquisition.

Investment appraisal techniques:

Halfords limited is a British company which operates its business in retailing the car

parts, camping, touring equipment, camping equipment and bicycle in the UK and Ireland.

The company has been founded in 1892 (Home, 2018). The company also offer various

services to its customers such as Bicycle repair and car accessories installation. The study has

been performed on the company to evaluate the performance of the company.

Investment appraisal techniques are also known as capital budgeting. The process is

done by the financial manager and officer of a company to evaluate the new projects of the

company and their returns. These techniques make it easier for the organization to make

decision about the acceptance of the project (Fridson and Alvarez, 2011).

Being the chief financial officer of the company, it becomes important to evaluate the

new project (Bicycle manufacturing plant) of the company in which company is planning to

invest £ 3,00,00,000. The life of the project would be 10 years and on the basis of the last 5

years cash flows of the company and the trend in the market, it has been found that whether

the project would offer good return to the company or not.

Firstly, the cash inflows of the company has been evaluated and it has been found that

with the help of this new project the sales units of the company would be 8,00,000 to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Financial Analysis

4

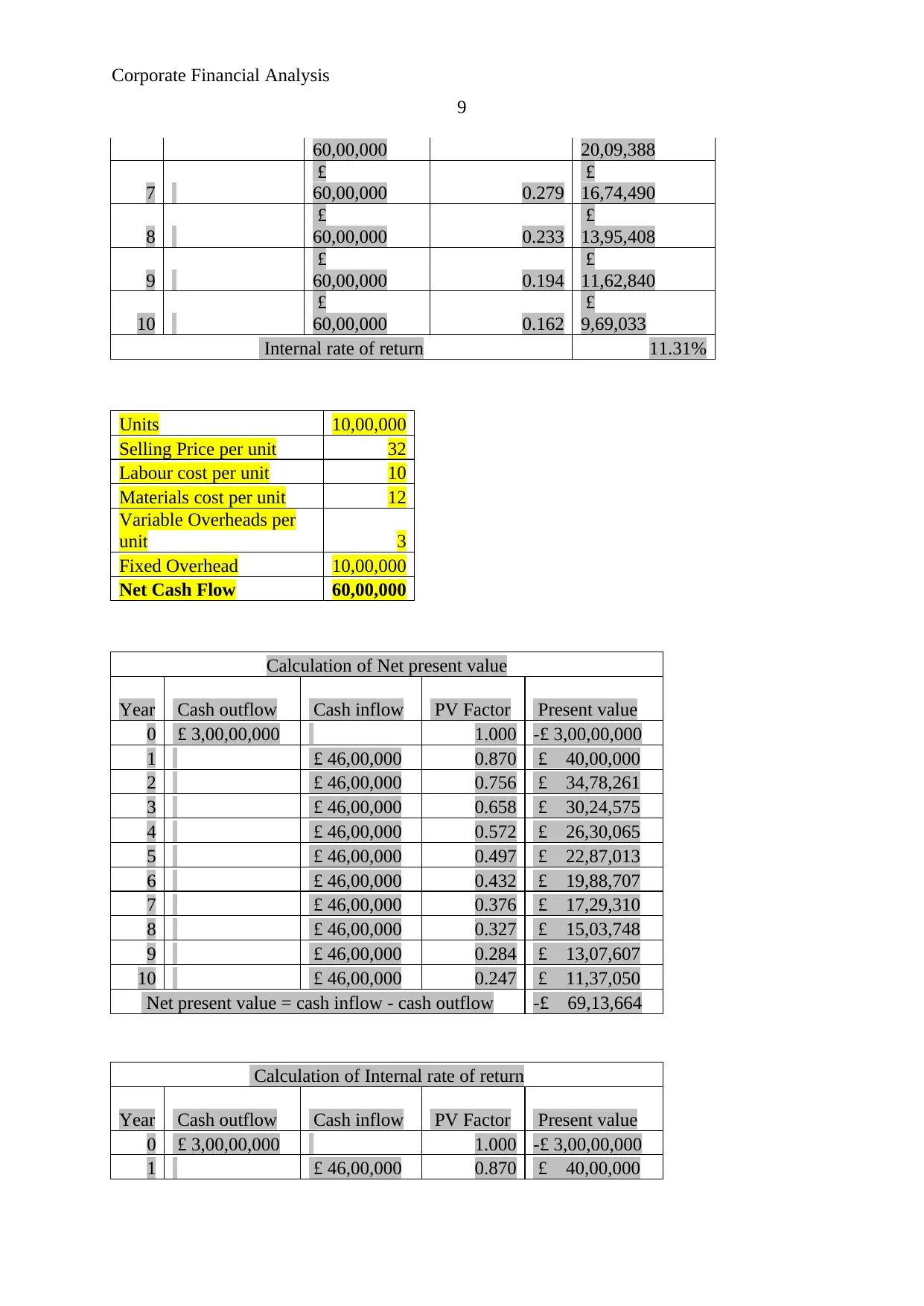

10,00,000 units. In that case, the cash inflows of the company would vary from - £ 60,00,000

to £ 46,00,000 (Ahrendsen and Katchova, 2012). It explains that if the company invest into

the new project that the cash flows of the company than the total cash inflow could vary

according to the sales units of the project.

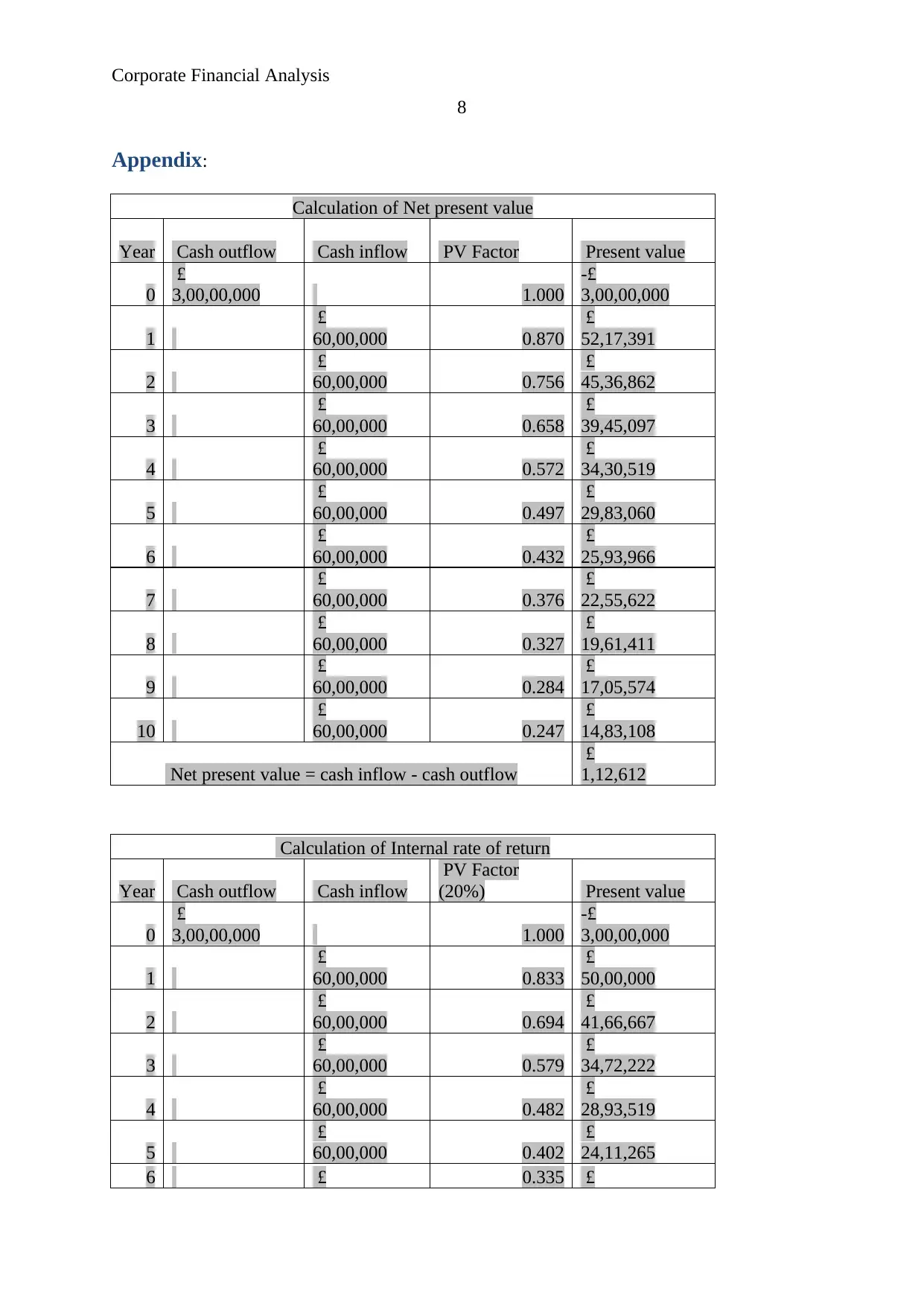

Further, the net present value technique of capital budgeting, which is evaluated to

identify that whether the cash flows of the project would be positive or negative, has been

discussed firstly and it has been found that the net cash flows of the company would be

positive. In this case, the cash inflows of the company would vary from - £ 69,13,664 to £

1,12,612 (Appendix). It explains that if the company invest into the new project that the cash

flows of the company either would be negative or very lower (Brown, 2012).

It explains that the investment into the project could be profitable for the company.

Further, the internal rate of return, which is evaluate to identify the total return percentage

where the NPV of the company would be 0, has been evaluated and it has been recognized

that the internal ret of return of the project is 1.41% to 11.31% (Appendix). In case of

8,00,000 units, the internal rate of return of the company would be 1.41% and in case of

10,00,000 units, the internal rate of return of the company would be 11.31% (Morningstar,

2018). In both the cases it has been found that the internal rate of return of the company is

lesser than the cost of capital of the company (Brooks, 2015).

On the other hand, the cost of capital of the new project of the company would be

15% which is quite higher than the internal rate of return of the company. Thus, it is

suggested to the company to not to accept the proposal (Gertler and Kiyotaki, 2010).

The investment appraisal techniques study on new project of the company explains

that the project should not be accepted by the company as it would not allow the comapny to

generate more profit as well as the performance of the company would also be worst. In

addition, the cost of the project would also be higher than the return % of the project.

Potential Target Company:

A target company is an organization which has been opted for the merger if

acquisition purpose by a potential acquirer. Takeover of an organization should be done by

the potential acquirer after evaluating and analyzing all the related aspect of the company.

The financial and non financial performance of the company is also required to be analyzed

(Brown, 2012).

4

10,00,000 units. In that case, the cash inflows of the company would vary from - £ 60,00,000

to £ 46,00,000 (Ahrendsen and Katchova, 2012). It explains that if the company invest into

the new project that the cash flows of the company than the total cash inflow could vary

according to the sales units of the project.

Further, the net present value technique of capital budgeting, which is evaluated to

identify that whether the cash flows of the project would be positive or negative, has been

discussed firstly and it has been found that the net cash flows of the company would be

positive. In this case, the cash inflows of the company would vary from - £ 69,13,664 to £

1,12,612 (Appendix). It explains that if the company invest into the new project that the cash

flows of the company either would be negative or very lower (Brown, 2012).

It explains that the investment into the project could be profitable for the company.

Further, the internal rate of return, which is evaluate to identify the total return percentage

where the NPV of the company would be 0, has been evaluated and it has been recognized

that the internal ret of return of the project is 1.41% to 11.31% (Appendix). In case of

8,00,000 units, the internal rate of return of the company would be 1.41% and in case of

10,00,000 units, the internal rate of return of the company would be 11.31% (Morningstar,

2018). In both the cases it has been found that the internal rate of return of the company is

lesser than the cost of capital of the company (Brooks, 2015).

On the other hand, the cost of capital of the new project of the company would be

15% which is quite higher than the internal rate of return of the company. Thus, it is

suggested to the company to not to accept the proposal (Gertler and Kiyotaki, 2010).

The investment appraisal techniques study on new project of the company explains

that the project should not be accepted by the company as it would not allow the comapny to

generate more profit as well as the performance of the company would also be worst. In

addition, the cost of the project would also be higher than the return % of the project.

Potential Target Company:

A target company is an organization which has been opted for the merger if

acquisition purpose by a potential acquirer. Takeover of an organization should be done by

the potential acquirer after evaluating and analyzing all the related aspect of the company.

The financial and non financial performance of the company is also required to be analyzed

(Brown, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Analysis

5

In the case of Halfords group plc, it has been found that the ScS group plc should be

acquired by the company. This company is operating its business in the same industry. So, it

would help the company to achieve the mission of the company to grab more market. Further,

the study of the financial performance of ScS has been evaluated to identify the performance

of the company and the profitability level of the company (Gopalan, Song and Yerramilli,

2014).

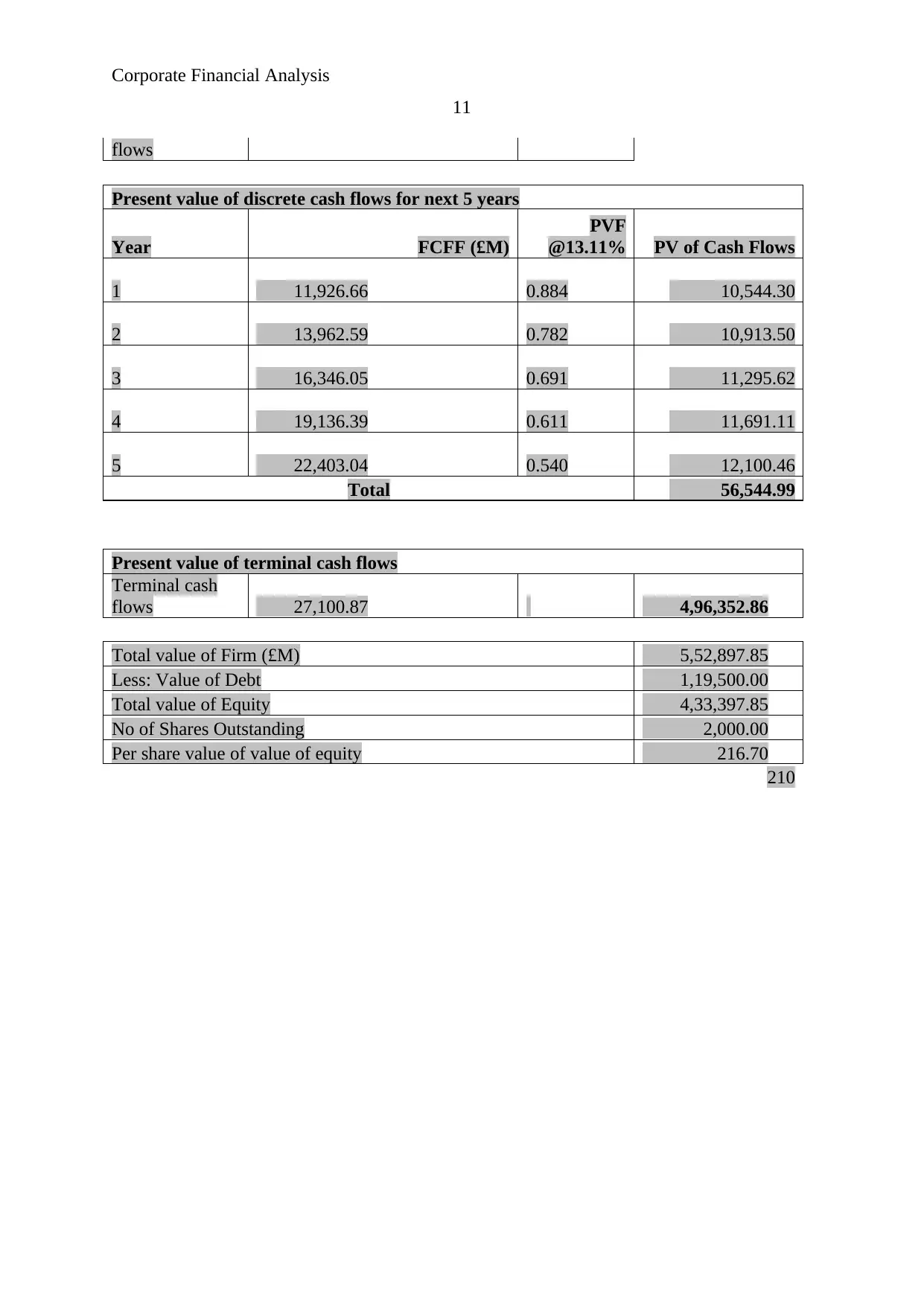

Discounted cash flow of the company has been evaluated to recognize the

performance of ScS and it has been found that the cash flow of the company is increasing by

170.17% from last 5 years. On the other hand, the performance growth rate of cash flow of

the company is 3.03%. On the basis of these figures, it has been found that the terminal cash

flows of the company are £ 27,100.87 (Appendix).

It explains that the discrete cash flow of the company would be £ 56,545. It leads to

the total terminal cash flows of the company is £ 4,96,352.86. On the basis of those

calculations, it has been found that the total value of firm would be £ 5,52,897.85, Out of

which £ 1,19,500 is the total debt of the company and thus the equity value of the company is

£ 4,33,397.85. It explains that the current worth of the company is £ 4,33,397.85 (Gibson,

2011). If Halfords group plc wants to acquire the company, than the total investment of the

company would be £ 4,33,397.85. ScS group has issued 2000 shares in the market. The

market value of the company’s share is £ 216.7. On the other hand, the intrinsic value of the

company is £ 216.70 (Appendix).

It explains that the company has been undervalued and thus if the Halfords limited

would acquire the company right now, than the company just have to pay £ 210 to each

shareholder of the ScS group company whereas the total worth of each shares of the comapny

is £ 216.7 (Morningstar, 2018). It would lead to the company to huge profit and thus, it has

been found that the company should acquire the ScS group to achieve the mission of the

company to grab more market (Higgins, 2012).

Thus, it is recommended to the Halfords group limited to recognize the offer of

acquire the ScS group limited. It would make it easier for the company o achieve the mission

of grab more market and be the leader in the market.

Conclusion:

5

In the case of Halfords group plc, it has been found that the ScS group plc should be

acquired by the company. This company is operating its business in the same industry. So, it

would help the company to achieve the mission of the company to grab more market. Further,

the study of the financial performance of ScS has been evaluated to identify the performance

of the company and the profitability level of the company (Gopalan, Song and Yerramilli,

2014).

Discounted cash flow of the company has been evaluated to recognize the

performance of ScS and it has been found that the cash flow of the company is increasing by

170.17% from last 5 years. On the other hand, the performance growth rate of cash flow of

the company is 3.03%. On the basis of these figures, it has been found that the terminal cash

flows of the company are £ 27,100.87 (Appendix).

It explains that the discrete cash flow of the company would be £ 56,545. It leads to

the total terminal cash flows of the company is £ 4,96,352.86. On the basis of those

calculations, it has been found that the total value of firm would be £ 5,52,897.85, Out of

which £ 1,19,500 is the total debt of the company and thus the equity value of the company is

£ 4,33,397.85. It explains that the current worth of the company is £ 4,33,397.85 (Gibson,

2011). If Halfords group plc wants to acquire the company, than the total investment of the

company would be £ 4,33,397.85. ScS group has issued 2000 shares in the market. The

market value of the company’s share is £ 216.7. On the other hand, the intrinsic value of the

company is £ 216.70 (Appendix).

It explains that the company has been undervalued and thus if the Halfords limited

would acquire the company right now, than the company just have to pay £ 210 to each

shareholder of the ScS group company whereas the total worth of each shares of the comapny

is £ 216.7 (Morningstar, 2018). It would lead to the company to huge profit and thus, it has

been found that the company should acquire the ScS group to achieve the mission of the

company to grab more market (Higgins, 2012).

Thus, it is recommended to the Halfords group limited to recognize the offer of

acquire the ScS group limited. It would make it easier for the company o achieve the mission

of grab more market and be the leader in the market.

Conclusion:

Corporate Financial Analysis

6

To conclude, the investment appraisal techniques study on new project of the

company explains that the project should not be accepted by the company as it would not

allow the comapny to generate more profit as well as the performance of the company would

also be worst. In addition, the cost of the project would also be higher than the return % of

the project. In addition, the target company, ScS has been evaluated for the purpose of

acquisition and it has been found that if the company would invest into the project than the

mission of grabbing more market could be achieved.

6

To conclude, the investment appraisal techniques study on new project of the

company explains that the project should not be accepted by the company as it would not

allow the comapny to generate more profit as well as the performance of the company would

also be worst. In addition, the cost of the project would also be higher than the return % of

the project. In addition, the target company, ScS has been evaluated for the purpose of

acquisition and it has been found that if the company would invest into the project than the

mission of grabbing more market could be achieved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Financial Analysis

7

References:

Ahrendsen, B.L. and Katchova, A.L., 2012. Financial ratio analysis using ARMS

data. Agricultural Finance Review, 72(2), pp.262-272.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Brown, R., 2012. Analysis of investments & management of portfolios. Pearson Higher Ed.

Fridson, M.S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's

guide (Vol. 597). John Wiley & Sons.

Gertler, M. and Kiyotaki, N., 2010. Financial intermediation and credit policy in business

cycle analysis. In Handbook of monetary economics (Vol. 3, pp. 547-599). Elsevier.

Gibson, C.H., 2011. Financial reporting and analysis. South-Western Cengage Learning.

Gopalan, R., Song, F. and Yerramilli, V., 2014. Debt maturity structure and credit

quality. Journal of Financial and Quantitative Analysis, 49(4), pp.817-842.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Home. 2018. Halfords group plc. [Online]. Available at: http://www.halfordscompany.com/

[Accessed as on 25th April 2018].

Morningstar. 2018. Halfords group plc. [Online]. Available at:

http://financials.morningstar.com/cash-flow/cf.html?

t=XFRA:HDK®ion=deu&culture=en-US [Accessed as on 25th April 2018].

Morningstar. 2018. ScS group plc. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?t=SCS®ion=gbr [Accessed as

on 25th April 2018].

7

References:

Ahrendsen, B.L. and Katchova, A.L., 2012. Financial ratio analysis using ARMS

data. Agricultural Finance Review, 72(2), pp.262-272.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Brown, R., 2012. Analysis of investments & management of portfolios. Pearson Higher Ed.

Fridson, M.S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's

guide (Vol. 597). John Wiley & Sons.

Gertler, M. and Kiyotaki, N., 2010. Financial intermediation and credit policy in business

cycle analysis. In Handbook of monetary economics (Vol. 3, pp. 547-599). Elsevier.

Gibson, C.H., 2011. Financial reporting and analysis. South-Western Cengage Learning.

Gopalan, R., Song, F. and Yerramilli, V., 2014. Debt maturity structure and credit

quality. Journal of Financial and Quantitative Analysis, 49(4), pp.817-842.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Home. 2018. Halfords group plc. [Online]. Available at: http://www.halfordscompany.com/

[Accessed as on 25th April 2018].

Morningstar. 2018. Halfords group plc. [Online]. Available at:

http://financials.morningstar.com/cash-flow/cf.html?

t=XFRA:HDK®ion=deu&culture=en-US [Accessed as on 25th April 2018].

Morningstar. 2018. ScS group plc. [Online]. Available at:

http://financials.morningstar.com/income-statement/is.html?t=SCS®ion=gbr [Accessed as

on 25th April 2018].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Analysis

8

Appendix:

Calculation of Net present value

Year Cash outflow Cash inflow PV Factor Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.870

£

52,17,391

2

£

60,00,000 0.756

£

45,36,862

3

£

60,00,000 0.658

£

39,45,097

4

£

60,00,000 0.572

£

34,30,519

5

£

60,00,000 0.497

£

29,83,060

6

£

60,00,000 0.432

£

25,93,966

7

£

60,00,000 0.376

£

22,55,622

8

£

60,00,000 0.327

£

19,61,411

9

£

60,00,000 0.284

£

17,05,574

10

£

60,00,000 0.247

£

14,83,108

Net present value = cash inflow - cash outflow

£

1,12,612

Calculation of Internal rate of return

Year Cash outflow Cash inflow

PV Factor

(20%) Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.833

£

50,00,000

2

£

60,00,000 0.694

£

41,66,667

3

£

60,00,000 0.579

£

34,72,222

4

£

60,00,000 0.482

£

28,93,519

5

£

60,00,000 0.402

£

24,11,265

6 £ 0.335 £

8

Appendix:

Calculation of Net present value

Year Cash outflow Cash inflow PV Factor Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.870

£

52,17,391

2

£

60,00,000 0.756

£

45,36,862

3

£

60,00,000 0.658

£

39,45,097

4

£

60,00,000 0.572

£

34,30,519

5

£

60,00,000 0.497

£

29,83,060

6

£

60,00,000 0.432

£

25,93,966

7

£

60,00,000 0.376

£

22,55,622

8

£

60,00,000 0.327

£

19,61,411

9

£

60,00,000 0.284

£

17,05,574

10

£

60,00,000 0.247

£

14,83,108

Net present value = cash inflow - cash outflow

£

1,12,612

Calculation of Internal rate of return

Year Cash outflow Cash inflow

PV Factor

(20%) Present value

0

£

3,00,00,000 1.000

-£

3,00,00,000

1

£

60,00,000 0.833

£

50,00,000

2

£

60,00,000 0.694

£

41,66,667

3

£

60,00,000 0.579

£

34,72,222

4

£

60,00,000 0.482

£

28,93,519

5

£

60,00,000 0.402

£

24,11,265

6 £ 0.335 £

Corporate Financial Analysis

9

60,00,000 20,09,388

7

£

60,00,000 0.279

£

16,74,490

8

£

60,00,000 0.233

£

13,95,408

9

£

60,00,000 0.194

£

11,62,840

10

£

60,00,000 0.162

£

9,69,033

Internal rate of return 11.31%

Units 10,00,000

Selling Price per unit 32

Labour cost per unit 10

Materials cost per unit 12

Variable Overheads per

unit 3

Fixed Overhead 10,00,000

Net Cash Flow 60,00,000

Calculation of Net present value

Year Cash outflow Cash inflow PV Factor Present value

0 £ 3,00,00,000 1.000 -£ 3,00,00,000

1 £ 46,00,000 0.870 £ 40,00,000

2 £ 46,00,000 0.756 £ 34,78,261

3 £ 46,00,000 0.658 £ 30,24,575

4 £ 46,00,000 0.572 £ 26,30,065

5 £ 46,00,000 0.497 £ 22,87,013

6 £ 46,00,000 0.432 £ 19,88,707

7 £ 46,00,000 0.376 £ 17,29,310

8 £ 46,00,000 0.327 £ 15,03,748

9 £ 46,00,000 0.284 £ 13,07,607

10 £ 46,00,000 0.247 £ 11,37,050

Net present value = cash inflow - cash outflow -£ 69,13,664

Calculation of Internal rate of return

Year Cash outflow Cash inflow PV Factor Present value

0 £ 3,00,00,000 1.000 -£ 3,00,00,000

1 £ 46,00,000 0.870 £ 40,00,000

9

60,00,000 20,09,388

7

£

60,00,000 0.279

£

16,74,490

8

£

60,00,000 0.233

£

13,95,408

9

£

60,00,000 0.194

£

11,62,840

10

£

60,00,000 0.162

£

9,69,033

Internal rate of return 11.31%

Units 10,00,000

Selling Price per unit 32

Labour cost per unit 10

Materials cost per unit 12

Variable Overheads per

unit 3

Fixed Overhead 10,00,000

Net Cash Flow 60,00,000

Calculation of Net present value

Year Cash outflow Cash inflow PV Factor Present value

0 £ 3,00,00,000 1.000 -£ 3,00,00,000

1 £ 46,00,000 0.870 £ 40,00,000

2 £ 46,00,000 0.756 £ 34,78,261

3 £ 46,00,000 0.658 £ 30,24,575

4 £ 46,00,000 0.572 £ 26,30,065

5 £ 46,00,000 0.497 £ 22,87,013

6 £ 46,00,000 0.432 £ 19,88,707

7 £ 46,00,000 0.376 £ 17,29,310

8 £ 46,00,000 0.327 £ 15,03,748

9 £ 46,00,000 0.284 £ 13,07,607

10 £ 46,00,000 0.247 £ 11,37,050

Net present value = cash inflow - cash outflow -£ 69,13,664

Calculation of Internal rate of return

Year Cash outflow Cash inflow PV Factor Present value

0 £ 3,00,00,000 1.000 -£ 3,00,00,000

1 £ 46,00,000 0.870 £ 40,00,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Financial Analysis

10

2 £ 46,00,000 0.756 £ 34,78,261

3 £ 46,00,000 0.658 £ 30,24,575

4 £ 46,00,000 0.572 £ 26,30,065

5 £ 46,00,000 0.497 £ 22,87,013

6 £ 46,00,000 0.432 £ 19,88,707

7 £ 46,00,000 0.376 £ 17,29,310

8 £ 46,00,000 0.327 £ 15,03,748

9 £ 46,00,000 0.284 £ 13,07,607

10 £ 46,00,000 0.247 £ 11,37,050

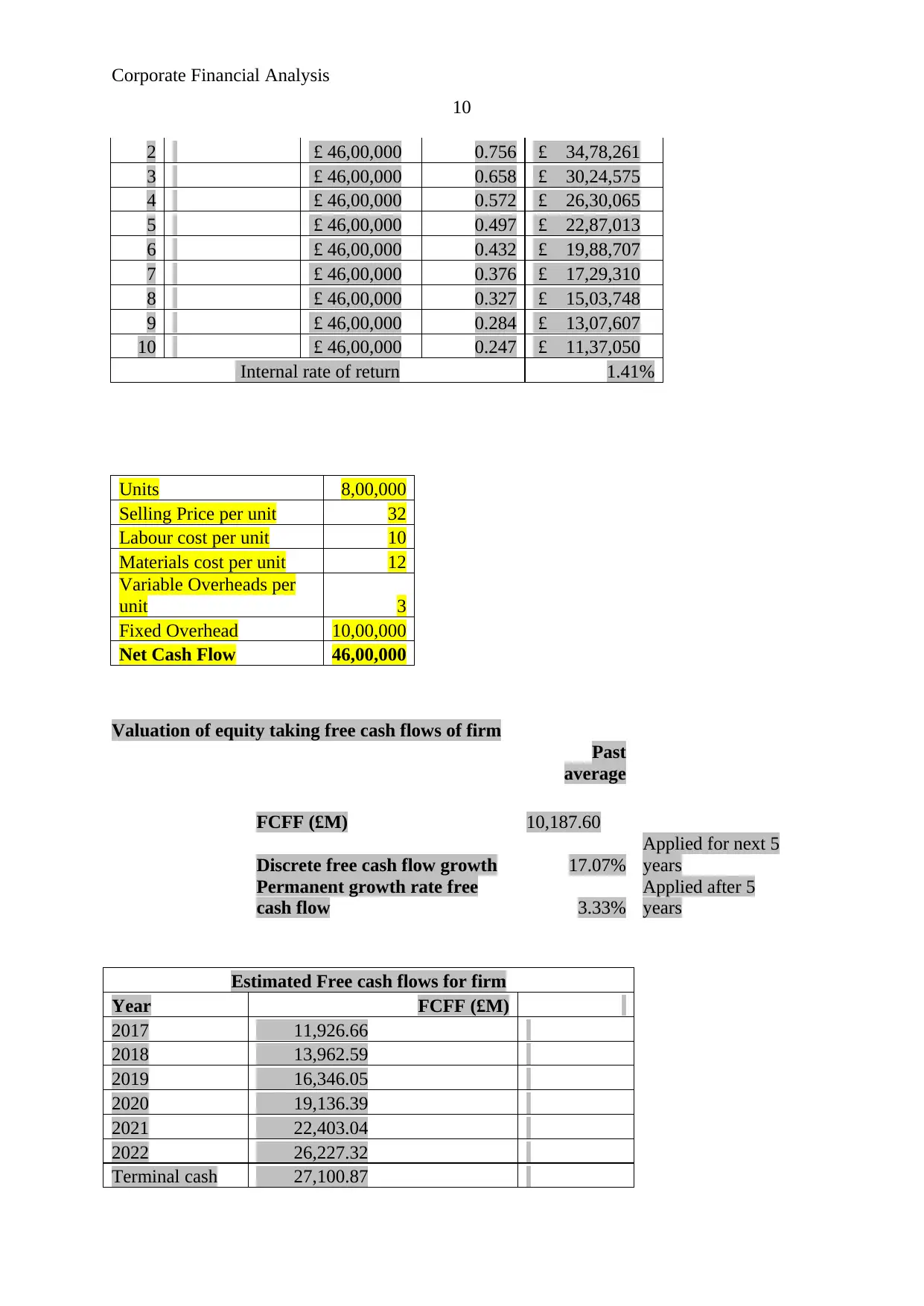

Internal rate of return 1.41%

Units 8,00,000

Selling Price per unit 32

Labour cost per unit 10

Materials cost per unit 12

Variable Overheads per

unit 3

Fixed Overhead 10,00,000

Net Cash Flow 46,00,000

Valuation of equity taking free cash flows of firm

Past

average

FCFF (£M) 10,187.60

Discrete free cash flow growth 17.07%

Applied for next 5

years

Permanent growth rate free

cash flow 3.33%

Applied after 5

years

Estimated Free cash flows for firm

Year FCFF (£M)

2017 11,926.66

2018 13,962.59

2019 16,346.05

2020 19,136.39

2021 22,403.04

2022 26,227.32

Terminal cash 27,100.87

10

2 £ 46,00,000 0.756 £ 34,78,261

3 £ 46,00,000 0.658 £ 30,24,575

4 £ 46,00,000 0.572 £ 26,30,065

5 £ 46,00,000 0.497 £ 22,87,013

6 £ 46,00,000 0.432 £ 19,88,707

7 £ 46,00,000 0.376 £ 17,29,310

8 £ 46,00,000 0.327 £ 15,03,748

9 £ 46,00,000 0.284 £ 13,07,607

10 £ 46,00,000 0.247 £ 11,37,050

Internal rate of return 1.41%

Units 8,00,000

Selling Price per unit 32

Labour cost per unit 10

Materials cost per unit 12

Variable Overheads per

unit 3

Fixed Overhead 10,00,000

Net Cash Flow 46,00,000

Valuation of equity taking free cash flows of firm

Past

average

FCFF (£M) 10,187.60

Discrete free cash flow growth 17.07%

Applied for next 5

years

Permanent growth rate free

cash flow 3.33%

Applied after 5

years

Estimated Free cash flows for firm

Year FCFF (£M)

2017 11,926.66

2018 13,962.59

2019 16,346.05

2020 19,136.39

2021 22,403.04

2022 26,227.32

Terminal cash 27,100.87

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Financial Analysis

11

flows

Present value of discrete cash flows for next 5 years

Year FCFF (£M)

PVF

@13.11% PV of Cash Flows

1 11,926.66 0.884 10,544.30

2 13,962.59 0.782 10,913.50

3 16,346.05 0.691 11,295.62

4 19,136.39 0.611 11,691.11

5 22,403.04 0.540 12,100.46

Total 56,544.99

Present value of terminal cash flows

Terminal cash

flows 27,100.87 4,96,352.86

Total value of Firm (£M) 5,52,897.85

Less: Value of Debt 1,19,500.00

Total value of Equity 4,33,397.85

No of Shares Outstanding 2,000.00

Per share value of value of equity 216.70

210

11

flows

Present value of discrete cash flows for next 5 years

Year FCFF (£M)

PVF

@13.11% PV of Cash Flows

1 11,926.66 0.884 10,544.30

2 13,962.59 0.782 10,913.50

3 16,346.05 0.691 11,295.62

4 19,136.39 0.611 11,691.11

5 22,403.04 0.540 12,100.46

Total 56,544.99

Present value of terminal cash flows

Terminal cash

flows 27,100.87 4,96,352.86

Total value of Firm (£M) 5,52,897.85

Less: Value of Debt 1,19,500.00

Total value of Equity 4,33,397.85

No of Shares Outstanding 2,000.00

Per share value of value of equity 216.70

210

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.