Management Accounting Techniques Used by Harrods Limited (2017)

VerifiedAdded on 2020/07/22

|19

|5107

|28

Report

AI Summary

This report provides a comprehensive analysis of the management accounting systems employed by Harrods Limited. It begins by describing various systems, including cost accounting, inventory management, price optimization, and job costing, and their importance to the company's operations. The report then delves into different management accounting reporting methods, such as budget reports, accounts receivable aging, job cost reports, and inventory manufacturing reports. A significant portion of the report is dedicated to preparing income statements using both marginal and absorption costing techniques, offering a comparative financial analysis of Harrods Limited's performance. The report also discusses the advantages and disadvantages of different budgeting tools and examines how organizations adapt management accounting techniques to overcome financial crises. The analysis includes financial statements, providing insights into the financial health and performance of the company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TASK 1............................................................................................................................................1

P1 Describing various systems of MA which are considered by Harrods Limited at the

workplace...............................................................................................................................1

TASK 2............................................................................................................................................3

P3 Preparing income statement (I/S) by taking base of two techniques of MA i.e. marginal as

well as absorption costing......................................................................................................3

Segregation between marginal and absorption costing..........................................................5

TASK 4............................................................................................................................................6

P4 Advantages and disadvantage of different budgeting tools.............................................6

. Managers may have the knowledge of other department but they don't know the strategic goals

and financial objectives of the overall organisation. ....................................................................10

P5 Comparing how organisations are adapted management accounting techniques to over

come financial crisis.............................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

TASK 1............................................................................................................................................1

P1 Describing various systems of MA which are considered by Harrods Limited at the

workplace...............................................................................................................................1

TASK 2............................................................................................................................................3

P3 Preparing income statement (I/S) by taking base of two techniques of MA i.e. marginal as

well as absorption costing......................................................................................................3

Segregation between marginal and absorption costing..........................................................5

TASK 4............................................................................................................................................6

P4 Advantages and disadvantage of different budgeting tools.............................................6

. Managers may have the knowledge of other department but they don't know the strategic goals

and financial objectives of the overall organisation. ....................................................................10

P5 Comparing how organisations are adapted management accounting techniques to over

come financial crisis.............................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

TASK 1

P1 Describing various systems of MA which are considered by Harrods Limited at the workplace

Business Report

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Systems of management accounting

Date: 6th December 2017

Introduction

A procedure through which financial plans are prepared as well as implemented and

evaluated at the workplace is referred as management accounting. It is used by only internal

stakeholders of the selected business which include managers, owners and employees. Further,

it comprises with various kinds of approaches as well as systems which are presented through

the current business report. In addition to this, essential needs of MA's systems under Harrods

Limited are described throughout the report.

Systems of MA

1

P1 Describing various systems of MA which are considered by Harrods Limited at the workplace

Business Report

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Systems of management accounting

Date: 6th December 2017

Introduction

A procedure through which financial plans are prepared as well as implemented and

evaluated at the workplace is referred as management accounting. It is used by only internal

stakeholders of the selected business which include managers, owners and employees. Further,

it comprises with various kinds of approaches as well as systems which are presented through

the current business report. In addition to this, essential needs of MA's systems under Harrods

Limited are described throughout the report.

Systems of MA

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

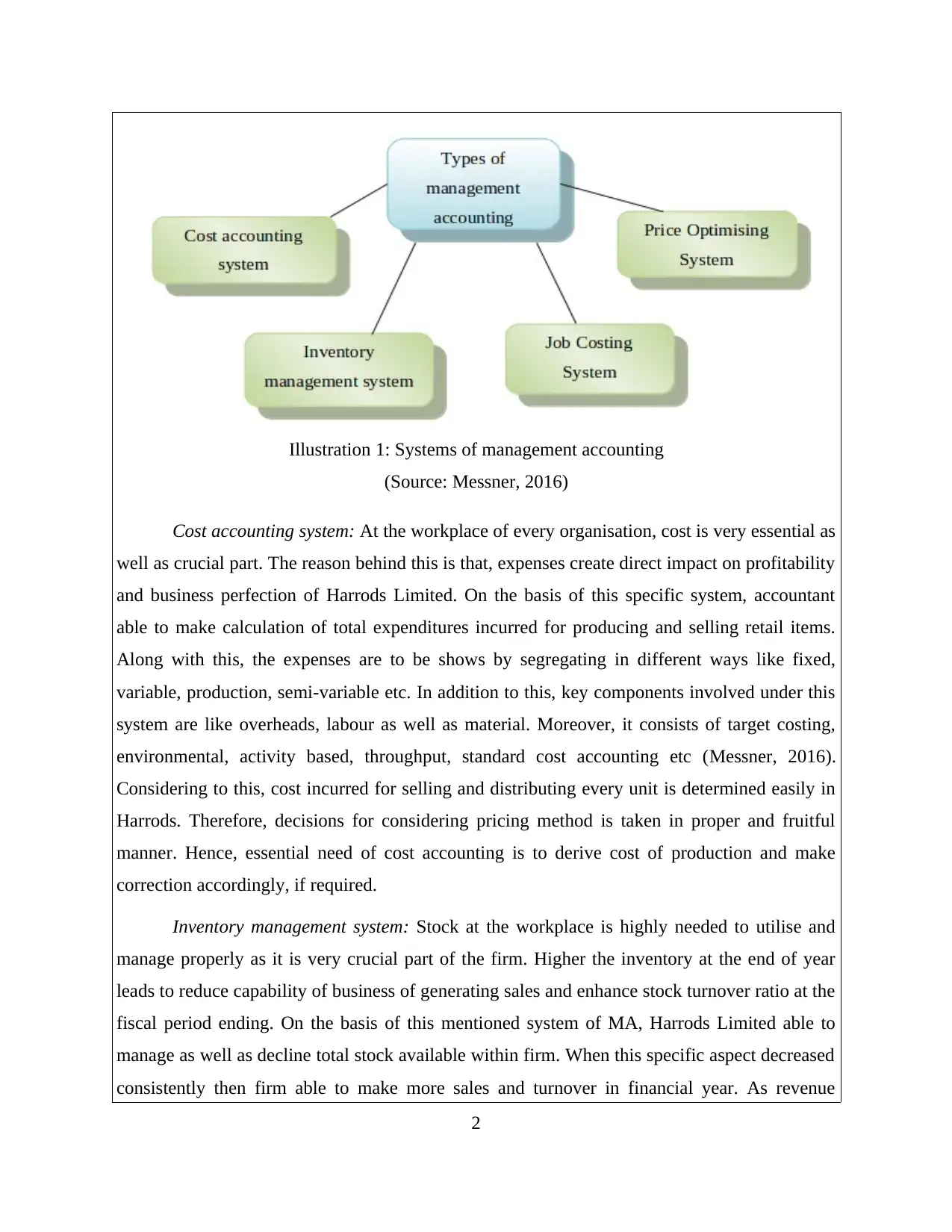

Illustration 1: Systems of management accounting

(Source: Messner, 2016)

Cost accounting system: At the workplace of every organisation, cost is very essential as

well as crucial part. The reason behind this is that, expenses create direct impact on profitability

and business perfection of Harrods Limited. On the basis of this specific system, accountant

able to make calculation of total expenditures incurred for producing and selling retail items.

Along with this, the expenses are to be shows by segregating in different ways like fixed,

variable, production, semi-variable etc. In addition to this, key components involved under this

system are like overheads, labour as well as material. Moreover, it consists of target costing,

environmental, activity based, throughput, standard cost accounting etc (Messner, 2016).

Considering to this, cost incurred for selling and distributing every unit is determined easily in

Harrods. Therefore, decisions for considering pricing method is taken in proper and fruitful

manner. Hence, essential need of cost accounting is to derive cost of production and make

correction accordingly, if required.

Inventory management system: Stock at the workplace is highly needed to utilise and

manage properly as it is very crucial part of the firm. Higher the inventory at the end of year

leads to reduce capability of business of generating sales and enhance stock turnover ratio at the

fiscal period ending. On the basis of this mentioned system of MA, Harrods Limited able to

manage as well as decline total stock available within firm. When this specific aspect decreased

consistently then firm able to make more sales and turnover in financial year. As revenue

2

(Source: Messner, 2016)

Cost accounting system: At the workplace of every organisation, cost is very essential as

well as crucial part. The reason behind this is that, expenses create direct impact on profitability

and business perfection of Harrods Limited. On the basis of this specific system, accountant

able to make calculation of total expenditures incurred for producing and selling retail items.

Along with this, the expenses are to be shows by segregating in different ways like fixed,

variable, production, semi-variable etc. In addition to this, key components involved under this

system are like overheads, labour as well as material. Moreover, it consists of target costing,

environmental, activity based, throughput, standard cost accounting etc (Messner, 2016).

Considering to this, cost incurred for selling and distributing every unit is determined easily in

Harrods. Therefore, decisions for considering pricing method is taken in proper and fruitful

manner. Hence, essential need of cost accounting is to derive cost of production and make

correction accordingly, if required.

Inventory management system: Stock at the workplace is highly needed to utilise and

manage properly as it is very crucial part of the firm. Higher the inventory at the end of year

leads to reduce capability of business of generating sales and enhance stock turnover ratio at the

fiscal period ending. On the basis of this mentioned system of MA, Harrods Limited able to

manage as well as decline total stock available within firm. When this specific aspect decreased

consistently then firm able to make more sales and turnover in financial year. As revenue

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

generated in more proportion, then the retailer easily able to boost up its turnover ratio

(Inventory Management, 2013). Therefore, profit generation capacity of the firm will be

improved up to a greater extent in the retail segment of UK. Apart from this, for managing

stock it is essential to analyse its total value. Further, there are three methods considered for

inventory valuation i.e. weighted average, LIFO as well as the FIFO.

Price optimisation system: Along with the stock and cost, price is another key factor of

the company which must be determined in an appropriate manner. A monetary factor at which

retail products and services are to be sold among customers is termed as price. It is not

necessary that accountant of Harrods Limited charge one particular price of products up to long

term. This aspect differ within sometimes which leads to derive purchasing and consumption

level of consumers. At different level of Central Systemcharges, number of customers also

differ by which sales and profit of the retailer vary. Furthermore, basic need of price

optimisation is to select one particular price at which more numbers of customers purchased

retail items (Cadez and Guilding, 2012). On the basis of this method, Harrods Limited able to

determine that which price will be supportive for it to generate more profit and boost up

financial performance in retail sector of UK.

Job costing system: The selected company selling different range of products which are

like cloths, food items, apparels etc. On the basis of this system of MA, Harrods Limited able to

determine that cost of sales is up to which level incurred under products of each job. Once

expenses came into consideration for selling every product of job then company can derive

pricing level in an appropriate direction (Joshi and Li, 2016). Henceforth, essential need of job

costing is to assess cost of goods and services of each job occurred at the workplace of Harrods

Limited and on the basis of this make pricing decisions.

Conclusion

It can be summarised from the present analysis that, basically four types of systems are

considered by Harrods Limited which are part of MA. Cost accounting and job costing

approaches are supportive in terms of determining total cost of production and expenses

incurred to produce products under each job. Apart from this, stock management and price

optimisation is helpful to Harrods for reducing inventory level and derive one profitable price of

3

(Inventory Management, 2013). Therefore, profit generation capacity of the firm will be

improved up to a greater extent in the retail segment of UK. Apart from this, for managing

stock it is essential to analyse its total value. Further, there are three methods considered for

inventory valuation i.e. weighted average, LIFO as well as the FIFO.

Price optimisation system: Along with the stock and cost, price is another key factor of

the company which must be determined in an appropriate manner. A monetary factor at which

retail products and services are to be sold among customers is termed as price. It is not

necessary that accountant of Harrods Limited charge one particular price of products up to long

term. This aspect differ within sometimes which leads to derive purchasing and consumption

level of consumers. At different level of Central Systemcharges, number of customers also

differ by which sales and profit of the retailer vary. Furthermore, basic need of price

optimisation is to select one particular price at which more numbers of customers purchased

retail items (Cadez and Guilding, 2012). On the basis of this method, Harrods Limited able to

determine that which price will be supportive for it to generate more profit and boost up

financial performance in retail sector of UK.

Job costing system: The selected company selling different range of products which are

like cloths, food items, apparels etc. On the basis of this system of MA, Harrods Limited able to

determine that cost of sales is up to which level incurred under products of each job. Once

expenses came into consideration for selling every product of job then company can derive

pricing level in an appropriate direction (Joshi and Li, 2016). Henceforth, essential need of job

costing is to assess cost of goods and services of each job occurred at the workplace of Harrods

Limited and on the basis of this make pricing decisions.

Conclusion

It can be summarised from the present analysis that, basically four types of systems are

considered by Harrods Limited which are part of MA. Cost accounting and job costing

approaches are supportive in terms of determining total cost of production and expenses

incurred to produce products under each job. Apart from this, stock management and price

optimisation is helpful to Harrods for reducing inventory level and derive one profitable price of

3

retail goods and services respectively.

TASK 2

P2 Explaining the different methods used for management accounting reporting.

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Systems of management accounting

Date: 6th December 2017

Introduction:

Sir,

In according to the management accounting report of Harrods limited it can be said that it

include the decision making, devising planning and performance management system of the

enterprise. This depend on the report which is to be given by the financial manger to assist the

management in the formulation of the plan (Pemsel and Wiewiora, 2013). The management

accounting is important in Harrods as this help the company to:

Analysis the cost of all the products and services offered by the firm.

Allocation of the resources according to the activity cost techniques.

This will also help Harrods in forecasting the future and then to plan accordingly.

The different types of Management accounting reports are as follows:

4

TASK 2

P2 Explaining the different methods used for management accounting reporting.

From: Management accounting Officer

To: General Manager

Harrods Limited

Subject: Systems of management accounting

Date: 6th December 2017

Introduction:

Sir,

In according to the management accounting report of Harrods limited it can be said that it

include the decision making, devising planning and performance management system of the

enterprise. This depend on the report which is to be given by the financial manger to assist the

management in the formulation of the plan (Pemsel and Wiewiora, 2013). The management

accounting is important in Harrods as this help the company to:

Analysis the cost of all the products and services offered by the firm.

Allocation of the resources according to the activity cost techniques.

This will also help Harrods in forecasting the future and then to plan accordingly.

The different types of Management accounting reports are as follows:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 2: Types of management accounting reports

[Source: Collier, 2015]

Budget report: in this type of report the overall budget of the company is decided and then

allocated by the management of Harrods. This also involve using the last year's budget in

preparation of current year budget by also keeping the inflation and cost of product in mind.

Harrods will list out all the possible sources of the fund and also seeing the expenditure and

revenue of the firm then to set the budget. This also help the management of the company to

analyse the performance in the market, departmental performance and also to control the cost of

the firm.

Accounts receivable ageing: this is used to assess the long and short term debts of the firms.

Who all are the debtors of firm, how much debt they all own and what among them are the

doubtful debts. The accounts receivable will analyse the amount of debts which are increasing

for the firm and will, find the effective solution helping them to gain the payments again. This

will be useful for Harrods to identify the relevant source of debt and making the report of it.

Job cost report: this report will be showing the expenditure made by a specified project of the

firm. Then after they analyse the expenditure made by all different type of project is causing to

the firm then they will allocate the budget according to the costing. This is very helpful in

identification of higher earning and lower earning areas of the firm and then controlling the cost

of them accordingly. This is used to analyse the expenses made by the project which is in

progress are the present time and them correcting the area of wastage as soon as possible.

Inventory manufacturing report: raw materials are the main source of production of the firm

5

[Source: Collier, 2015]

Budget report: in this type of report the overall budget of the company is decided and then

allocated by the management of Harrods. This also involve using the last year's budget in

preparation of current year budget by also keeping the inflation and cost of product in mind.

Harrods will list out all the possible sources of the fund and also seeing the expenditure and

revenue of the firm then to set the budget. This also help the management of the company to

analyse the performance in the market, departmental performance and also to control the cost of

the firm.

Accounts receivable ageing: this is used to assess the long and short term debts of the firms.

Who all are the debtors of firm, how much debt they all own and what among them are the

doubtful debts. The accounts receivable will analyse the amount of debts which are increasing

for the firm and will, find the effective solution helping them to gain the payments again. This

will be useful for Harrods to identify the relevant source of debt and making the report of it.

Job cost report: this report will be showing the expenditure made by a specified project of the

firm. Then after they analyse the expenditure made by all different type of project is causing to

the firm then they will allocate the budget according to the costing. This is very helpful in

identification of higher earning and lower earning areas of the firm and then controlling the cost

of them accordingly. This is used to analyse the expenses made by the project which is in

progress are the present time and them correcting the area of wastage as soon as possible.

Inventory manufacturing report: raw materials are the main source of production of the firm

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and to control them is also very important. The inventory of the firm are used by the

management to make their manufacturing process more and more efficient. The inventory

manufacturing report will be covering certain area of production like that of inventory waste,

hourly labour cost or per unit head cost of the firm while producing any product.

Conclusion: it can be summarised that management accounting there are many types of report

which need to be generated. They all are having their own importance in the firm and help in

decision making and cost allocation of the products of the firm which are been manufactured.

Management accounting is having its own importance in the firm and its decision making

process as this help the firm in reducing the cost and expense incurred by the task or job of the

firm.

TASK 2

P3 Preparing income statement (I/S) by taking base of two techniques of MA i.e. marginal as

well as absorption costing

Preparation of financial statements is very essential part of every organisation because it

supports to assess financial performance of the firm within industry. On the basis of performance

pertained effective business decisions like investing, financing, expenses making, dividend etc.

are taken into account. In the present part of the project, income statements are formulated which

show profitability position of the company. To prepare profit and loss accounts different methods

are available at there. Herein, marginal and absorption these two costing techniques are

considered by Harrods Limited for preparing such accounts. Further, statements and analysis is

presented below:

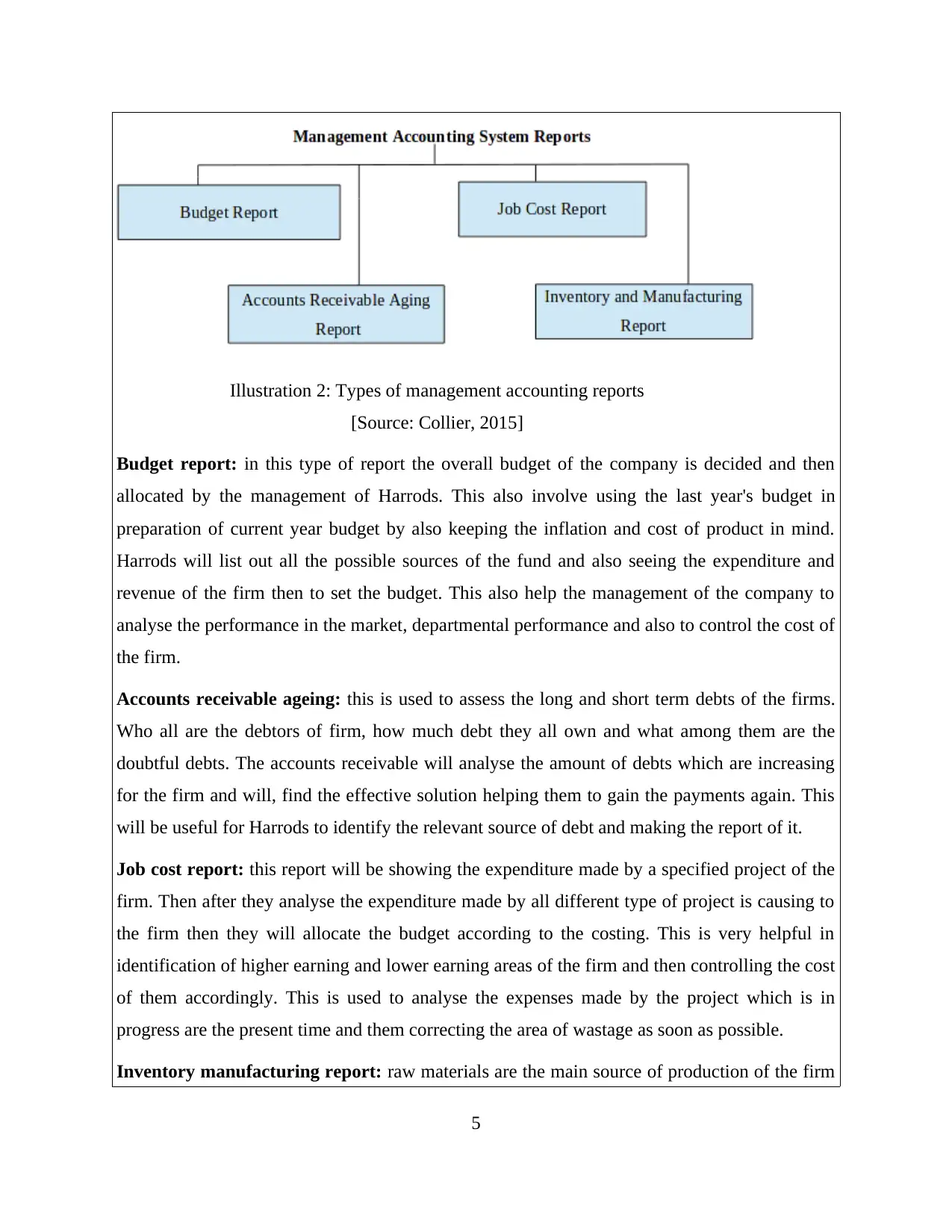

Income statement based on marginal costing

6

management to make their manufacturing process more and more efficient. The inventory

manufacturing report will be covering certain area of production like that of inventory waste,

hourly labour cost or per unit head cost of the firm while producing any product.

Conclusion: it can be summarised that management accounting there are many types of report

which need to be generated. They all are having their own importance in the firm and help in

decision making and cost allocation of the products of the firm which are been manufactured.

Management accounting is having its own importance in the firm and its decision making

process as this help the firm in reducing the cost and expense incurred by the task or job of the

firm.

TASK 2

P3 Preparing income statement (I/S) by taking base of two techniques of MA i.e. marginal as

well as absorption costing

Preparation of financial statements is very essential part of every organisation because it

supports to assess financial performance of the firm within industry. On the basis of performance

pertained effective business decisions like investing, financing, expenses making, dividend etc.

are taken into account. In the present part of the project, income statements are formulated which

show profitability position of the company. To prepare profit and loss accounts different methods

are available at there. Herein, marginal and absorption these two costing techniques are

considered by Harrods Limited for preparing such accounts. Further, statements and analysis is

presented below:

Income statement based on marginal costing

6

Considering to the above statement of income it can be said that, at the end of fiscal year

the retailer generates revenue worth of 17500 GBP by selling 500 units. On this particular sales

amount Harrods Limited is capable for earning 4300 GBP net income which is not higher and

lower. On the basis of this, it can be assessed that management of cited firm is capable for

managing total costs incurred within firm. Being a retailer any kind of manufacturing costs are

not has to bear to it. Therefore, expenses for packaging and selling several retail items are

properly managed by it. Due to this specific reason, it becomes able to generate this profit

amount at the end of accounting period. Moreover, it should apply those strategies which support

to manage and control over the unproductive costs. The reason is that, these will help to improve

net profit and boost up financial performance in the retail sector of UK.

Income statement based on absorption costing

7

the retailer generates revenue worth of 17500 GBP by selling 500 units. On this particular sales

amount Harrods Limited is capable for earning 4300 GBP net income which is not higher and

lower. On the basis of this, it can be assessed that management of cited firm is capable for

managing total costs incurred within firm. Being a retailer any kind of manufacturing costs are

not has to bear to it. Therefore, expenses for packaging and selling several retail items are

properly managed by it. Due to this specific reason, it becomes able to generate this profit

amount at the end of accounting period. Moreover, it should apply those strategies which support

to manage and control over the unproductive costs. The reason is that, these will help to improve

net profit and boost up financial performance in the retail sector of UK.

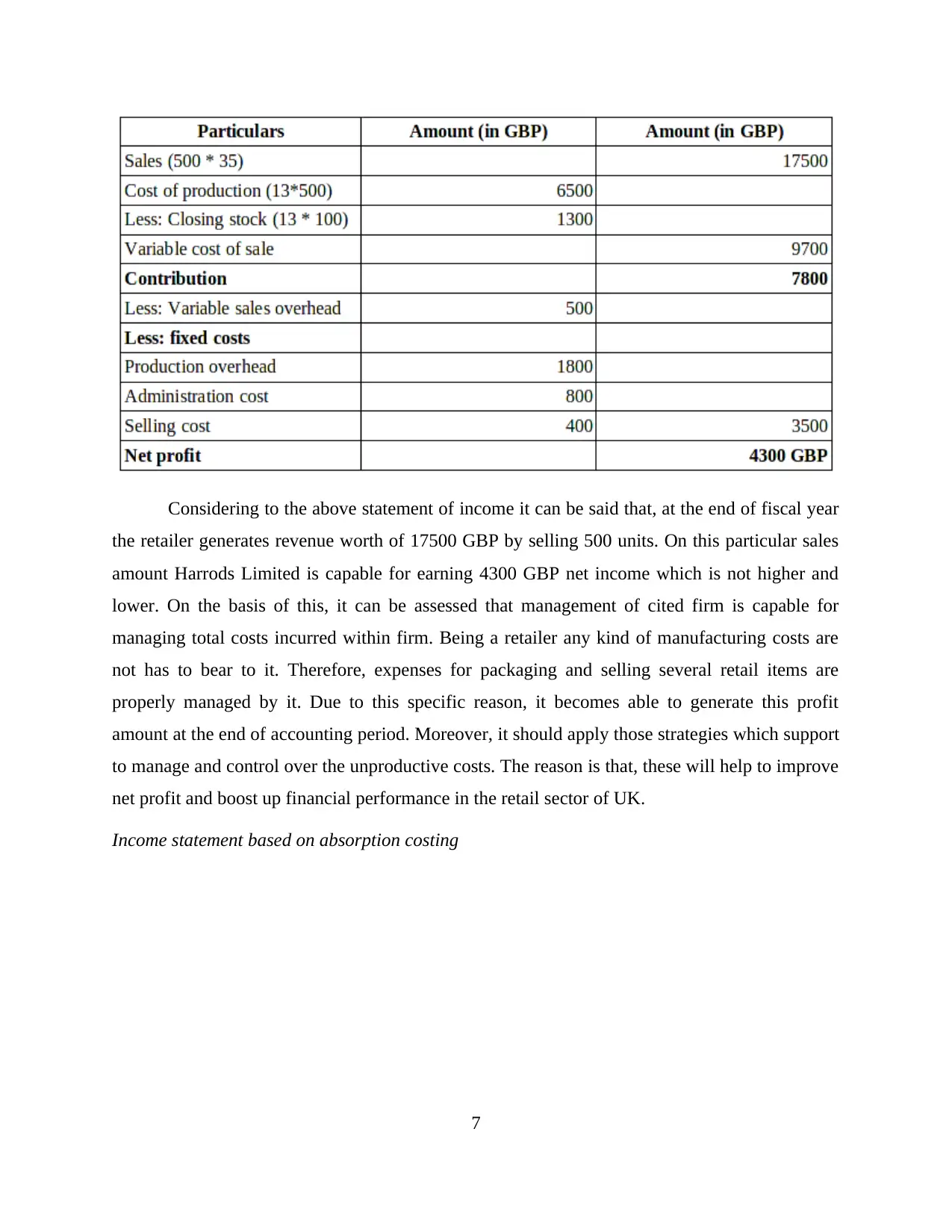

Income statement based on absorption costing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Looking at the above formulated P&L on the basis of absorption method it can be seen

that, Harrods Limited earning same amount of revenue as earned under marginal i.e. worth of

17500 GBP. However, net profit generated by it in this case is worth of 6600 GBP which is

higher as compared to the above mentioned I/S. On the basis of this, financial performance of the

retailer in industry is higher than the marginal costing. Key reason for occurring such difference

is that, both the costing methods are relied upon different nature of costs which are like fixed and

variable. Calculation under the marginal method considers only variable expenses associated

with firm while another uses every kind of costs (Grabner and Moers, 2013). Due to which

amount of total cost and profit both differs up to a greater extent at the end of financial year.

Marginal and absorption both are supportive for preparing financial statement which is

I/S. However, these have some differences which are reflected below:

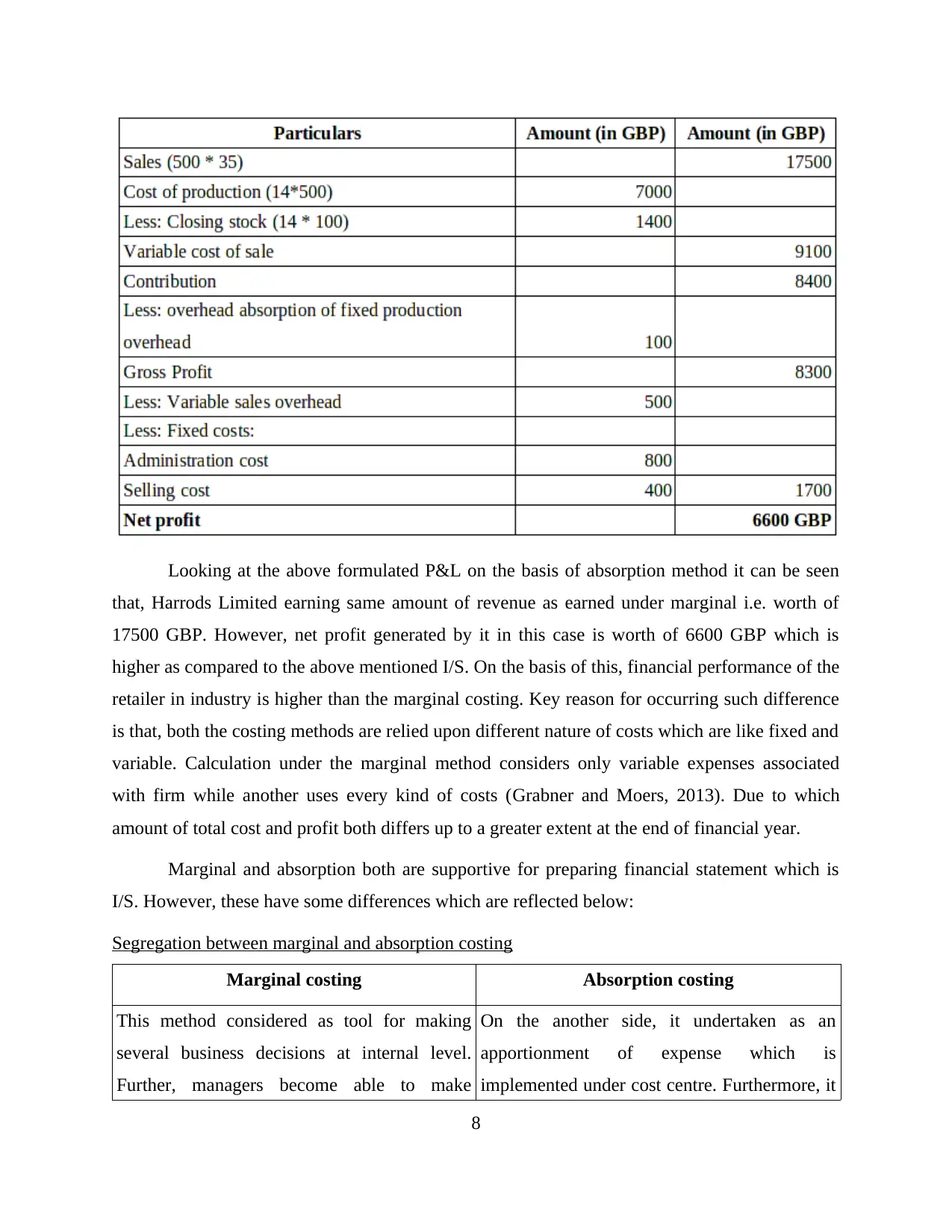

Segregation between marginal and absorption costing

Marginal costing Absorption costing

This method considered as tool for making

several business decisions at internal level.

Further, managers become able to make

On the another side, it undertaken as an

apportionment of expense which is

implemented under cost centre. Furthermore, it

8

that, Harrods Limited earning same amount of revenue as earned under marginal i.e. worth of

17500 GBP. However, net profit generated by it in this case is worth of 6600 GBP which is

higher as compared to the above mentioned I/S. On the basis of this, financial performance of the

retailer in industry is higher than the marginal costing. Key reason for occurring such difference

is that, both the costing methods are relied upon different nature of costs which are like fixed and

variable. Calculation under the marginal method considers only variable expenses associated

with firm while another uses every kind of costs (Grabner and Moers, 2013). Due to which

amount of total cost and profit both differs up to a greater extent at the end of financial year.

Marginal and absorption both are supportive for preparing financial statement which is

I/S. However, these have some differences which are reflected below:

Segregation between marginal and absorption costing

Marginal costing Absorption costing

This method considered as tool for making

several business decisions at internal level.

Further, managers become able to make

On the another side, it undertaken as an

apportionment of expense which is

implemented under cost centre. Furthermore, it

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effective judgements which support to boost up

business performance in retail industry (Nuhu

and et.al., 2017).

is one of the significant part of responsibility

centres work in an organisation.

Outcome of I/S under this method is

considered in terms of contribution of each unit

sold by Harrods Limited in the market.

Amount determined under the P&L as per

absorption costing is referred as gross profit

earned at the end of year.

Overhead costs incurred under this method is

divided in two portions which are like fixed as

well as variable.

Herein, overhead expenses are segregated in

three parts which involve production or

manufacturing, selling & distribution as well as

administration.

Profit gained by the retailer at the end of

financial year is to be measured in terms of

P/V (profit volume) ratio.

In this method, changes or fluctuations in fixed

income lead to create huge impact on

profitability situations of the retailer (Hiebl,

2014).

Stock is to be measured in marginal costing in

form of non-fixed expenses of the company.

Herein, valuation of inventory is to be done on

the basis of production expenses incurred at the

end of financial period.

At the time of making calculations and P&L on

the basis of marginal costing, there is not

requirement to follow accounting principles,

standards, theories etc.

On the another side, treatment of stock is done

on the basis of International Accounting

Standard 2 (IAS 2).

TASK 4

P4 Advantages and disadvantage of different budgeting tools.

The formulation of plans in numerical terms for future period is called budgeting. Business

prepare budgets for various departments, units, divisions, etc. budgets are generally made for one

year. The comparison of budgets and actual performance of organisation will help in calculating

variances. It will also help managers to find out discrepancies and take remedial actions at

9

business performance in retail industry (Nuhu

and et.al., 2017).

is one of the significant part of responsibility

centres work in an organisation.

Outcome of I/S under this method is

considered in terms of contribution of each unit

sold by Harrods Limited in the market.

Amount determined under the P&L as per

absorption costing is referred as gross profit

earned at the end of year.

Overhead costs incurred under this method is

divided in two portions which are like fixed as

well as variable.

Herein, overhead expenses are segregated in

three parts which involve production or

manufacturing, selling & distribution as well as

administration.

Profit gained by the retailer at the end of

financial year is to be measured in terms of

P/V (profit volume) ratio.

In this method, changes or fluctuations in fixed

income lead to create huge impact on

profitability situations of the retailer (Hiebl,

2014).

Stock is to be measured in marginal costing in

form of non-fixed expenses of the company.

Herein, valuation of inventory is to be done on

the basis of production expenses incurred at the

end of financial period.

At the time of making calculations and P&L on

the basis of marginal costing, there is not

requirement to follow accounting principles,

standards, theories etc.

On the another side, treatment of stock is done

on the basis of International Accounting

Standard 2 (IAS 2).

TASK 4

P4 Advantages and disadvantage of different budgeting tools.

The formulation of plans in numerical terms for future period is called budgeting. Business

prepare budgets for various departments, units, divisions, etc. budgets are generally made for one

year. The comparison of budgets and actual performance of organisation will help in calculating

variances. It will also help managers to find out discrepancies and take remedial actions at

9

proper time. It is a continuous process which helps in planning and coordinating. It helps in

controlling as the standard cost are set in this. The main objectives of budgetary control is to

operate various departments of cost with efficiency and economically. It also helps in eliminating

waste and increase in profitability. It is a centralised control system which anticipate the capital

expenditure for future. It corrects the deviations from the established standards. It also fixes the

responsibilities of various individual in the organisation. The various essentials of budgetary

controlling are budget centres, budget committee, budget officer, budget period, budget mammal

and determination of key factor. There are different kinds of tools for preparing budgets.

Following are the various tools:

different tools of budgeting

standards: in this specific standards are set by the manager. It guides the manager to determine

the progress of report. By maintaining the specific cost and amount required for project it helps

the controlling the budget .(Hiebl,, 2014.) .

Advantages- it helps the manager to focus on other issues because the budget is specific

in terms.

It provides the benchmark for judging the performance of employees.

It helps in maintaining actual cost because the standard cost are set for each activity.

Provides integrity in business as excessive cost reasons can be found out.

It establish standards like what the cost should be, who will be responsible for them and

if actual costs are under control or not.

Disadvantage:

they are prepared on monthly basis and are released on the end of each month.

It becomes difficult for managers to take favourable decisions whether incentives are

provided to employees or not.

This budget often create variances(.Messner,., 2016.)

10

controlling as the standard cost are set in this. The main objectives of budgetary control is to

operate various departments of cost with efficiency and economically. It also helps in eliminating

waste and increase in profitability. It is a centralised control system which anticipate the capital

expenditure for future. It corrects the deviations from the established standards. It also fixes the

responsibilities of various individual in the organisation. The various essentials of budgetary

controlling are budget centres, budget committee, budget officer, budget period, budget mammal

and determination of key factor. There are different kinds of tools for preparing budgets.

Following are the various tools:

different tools of budgeting

standards: in this specific standards are set by the manager. It guides the manager to determine

the progress of report. By maintaining the specific cost and amount required for project it helps

the controlling the budget .(Hiebl,, 2014.) .

Advantages- it helps the manager to focus on other issues because the budget is specific

in terms.

It provides the benchmark for judging the performance of employees.

It helps in maintaining actual cost because the standard cost are set for each activity.

Provides integrity in business as excessive cost reasons can be found out.

It establish standards like what the cost should be, who will be responsible for them and

if actual costs are under control or not.

Disadvantage:

they are prepared on monthly basis and are released on the end of each month.

It becomes difficult for managers to take favourable decisions whether incentives are

provided to employees or not.

This budget often create variances(.Messner,., 2016.)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.