Comprehensive Financial Analysis and Investment Appraisal Report

VerifiedAdded on 2020/09/03

|23

|5220

|56

Report

AI Summary

This report undertakes a comprehensive financial analysis of Harvey Homes Plc, dissecting its financial statements, including the statement of profit or loss, financial position, and cash flow statement. The analysis employs ratio analysis to evaluate profitability (gross margin, net margin, ROCE), liquidity (current and quick ratios), and solvency (debt ratio). The report also delves into market segment analysis, assessing the performance of different segments of the company. Furthermore, it explores investment appraisal techniques, such as payback period, accounting rate of return (ARR), and net present value (NPV), along with the consideration of non-financial factors. The findings highlight the company's financial performance, liquidity, and areas for improvement, providing insights into financial decision-making and investment strategies. The report includes illustrations, tables, and appendices to support the analysis.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

PART 1............................................................................................................................................1

Analysing the statement of profit or loss................................................................................1

Financial position analysis.....................................................................................................5

Analysis of cash flow statement.............................................................................................9

Market Segment Analysis.....................................................................................................10

PART 2: INVESTMENT APPRAISAL........................................................................................12

Management forecast ...........................................................................................................12

Techniques of investment appraisal ....................................................................................12

Payback period ................................................................................................................12

Accounting/Average rate of return (ARR) .....................................................................13

Net present value..................................................................................................................13

Non-financial factors ...........................................................................................................14

APPENDIX....................................................................................................................................18

EXECUTIVE SUMMARY.............................................................................................................1

PART 1............................................................................................................................................1

Analysing the statement of profit or loss................................................................................1

Financial position analysis.....................................................................................................5

Analysis of cash flow statement.............................................................................................9

Market Segment Analysis.....................................................................................................10

PART 2: INVESTMENT APPRAISAL........................................................................................12

Management forecast ...........................................................................................................12

Techniques of investment appraisal ....................................................................................12

Payback period ................................................................................................................12

Accounting/Average rate of return (ARR) .....................................................................13

Net present value..................................................................................................................13

Non-financial factors ...........................................................................................................14

APPENDIX....................................................................................................................................18

Illustration Index

Illustration 1: Comparison of gross profit and net sales..................................................................2

Illustration 2: Comparison of operating profits and revenue..........................................................3

Illustration 3: Comparison of operating profits and capital employed............................................4

Illustration 4: Current ratio of Harvey Homes Plc...........................................................................6

Illustration 5: Quick ratio of Harvey Homes Plc.............................................................................7

Illustration 6: Debt ratio of the Harvey Homes Plc.........................................................................8

Illustration 7: Cash flow from operating, investing and financing activities...................................9

Illustration 8: Comparison of Cash Conversion Cycle..................................................................10

Illustration 9: Comparison of the company's different segments..................................................11

Index of Tables

Table 1: Ratio analysis for profit and loss statement.....................................................................18

Table 2: Calculation of Capital employed.....................................................................................18

Table 3: Cash flow from operating, investing and financing activities.........................................19

Table 4: Calculation of DIO, DSO and DPO.................................................................................19

Illustration 1: Comparison of gross profit and net sales..................................................................2

Illustration 2: Comparison of operating profits and revenue..........................................................3

Illustration 3: Comparison of operating profits and capital employed............................................4

Illustration 4: Current ratio of Harvey Homes Plc...........................................................................6

Illustration 5: Quick ratio of Harvey Homes Plc.............................................................................7

Illustration 6: Debt ratio of the Harvey Homes Plc.........................................................................8

Illustration 7: Cash flow from operating, investing and financing activities...................................9

Illustration 8: Comparison of Cash Conversion Cycle..................................................................10

Illustration 9: Comparison of the company's different segments..................................................11

Index of Tables

Table 1: Ratio analysis for profit and loss statement.....................................................................18

Table 2: Calculation of Capital employed.....................................................................................18

Table 3: Cash flow from operating, investing and financing activities.........................................19

Table 4: Calculation of DIO, DSO and DPO.................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

Analysing the financial statements of the entity helps in better decision making. It is

helpful in comparative analysis of sales, profits, assets etc (Allen, Larson and Sloan, 2013).

Harvey homes is a company which is involved in creating quality homes. Ratio analysis

technique have been used to analyse the financial statement of the company. Capital

budgeting technique have been used to assess that whether the project will prove to be

profitable for the company or not. The key findings suggest that current ratio of the company

is on higher side as compared to the ideal one which shows that the entity is not optimally

utilizing its resources available with it. Further, it has taken long term loan for 150 million in

order to meet its expenses as Harvey is not generating much operating cash in order to meet

out its needs. Midlands in not generating high revenues where the entity is advised to

improve its product mix and marketing strategy for better profits in near future. Moreover,

some financial and non-financial factors have been discussed which the enterprise should

consider while expanding in other country.

PART 1

Analysing the statement of profit or loss

Gross margin ratio

1

Analysing the financial statements of the entity helps in better decision making. It is

helpful in comparative analysis of sales, profits, assets etc (Allen, Larson and Sloan, 2013).

Harvey homes is a company which is involved in creating quality homes. Ratio analysis

technique have been used to analyse the financial statement of the company. Capital

budgeting technique have been used to assess that whether the project will prove to be

profitable for the company or not. The key findings suggest that current ratio of the company

is on higher side as compared to the ideal one which shows that the entity is not optimally

utilizing its resources available with it. Further, it has taken long term loan for 150 million in

order to meet its expenses as Harvey is not generating much operating cash in order to meet

out its needs. Midlands in not generating high revenues where the entity is advised to

improve its product mix and marketing strategy for better profits in near future. Moreover,

some financial and non-financial factors have been discussed which the enterprise should

consider while expanding in other country.

PART 1

Analysing the statement of profit or loss

Gross margin ratio

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

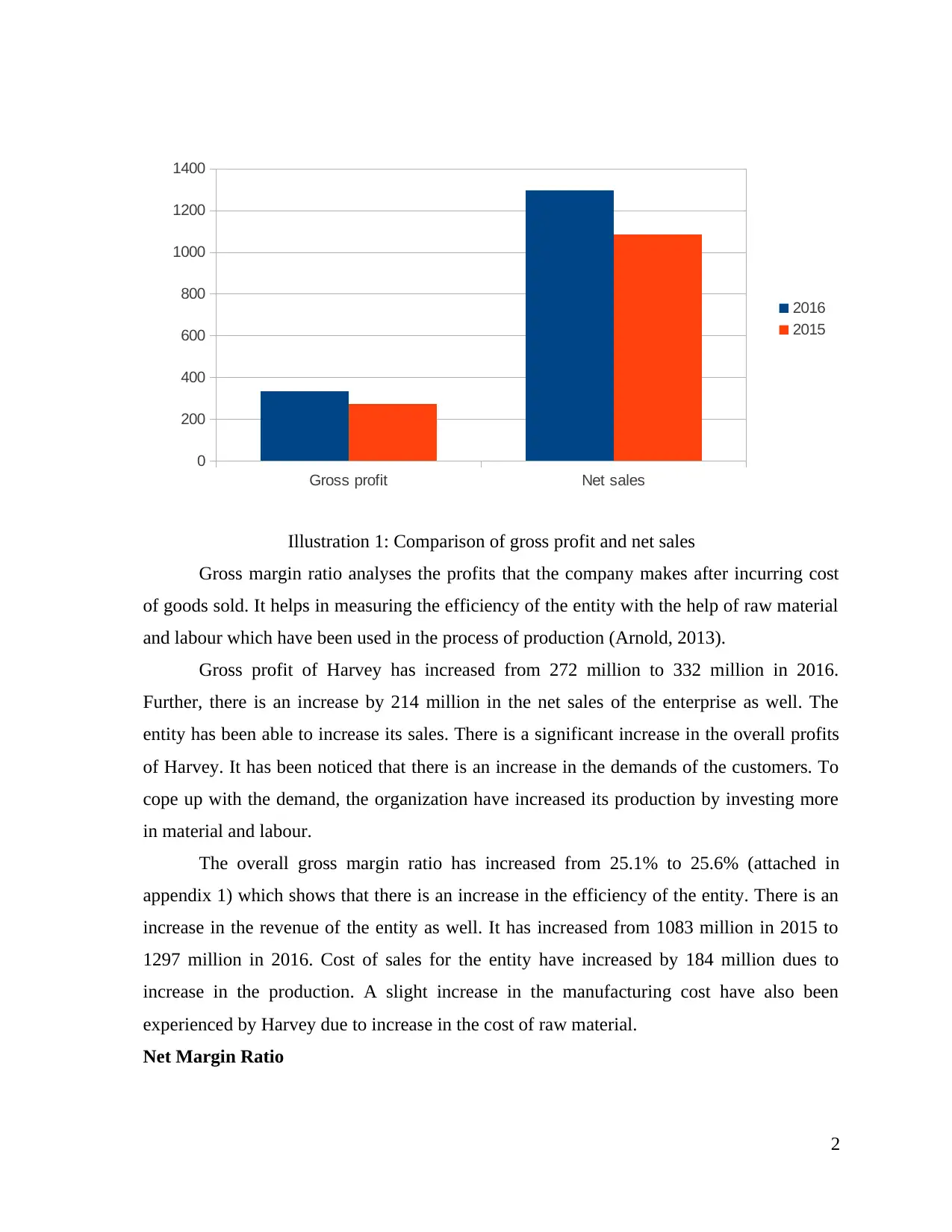

Gross margin ratio analyses the profits that the company makes after incurring cost

of goods sold. It helps in measuring the efficiency of the entity with the help of raw material

and labour which have been used in the process of production (Arnold, 2013).

Gross profit of Harvey has increased from 272 million to 332 million in 2016.

Further, there is an increase by 214 million in the net sales of the enterprise as well. The

entity has been able to increase its sales. There is a significant increase in the overall profits

of Harvey. It has been noticed that there is an increase in the demands of the customers. To

cope up with the demand, the organization have increased its production by investing more

in material and labour.

The overall gross margin ratio has increased from 25.1% to 25.6% (attached in

appendix 1) which shows that there is an increase in the efficiency of the entity. There is an

increase in the revenue of the entity as well. It has increased from 1083 million in 2015 to

1297 million in 2016. Cost of sales for the entity have increased by 184 million dues to

increase in the production. A slight increase in the manufacturing cost have also been

experienced by Harvey due to increase in the cost of raw material.

Net Margin Ratio

2

Gross profit Net sales

0

200

400

600

800

1000

1200

1400

2016

2015

Illustration 1: Comparison of gross profit and net sales

of goods sold. It helps in measuring the efficiency of the entity with the help of raw material

and labour which have been used in the process of production (Arnold, 2013).

Gross profit of Harvey has increased from 272 million to 332 million in 2016.

Further, there is an increase by 214 million in the net sales of the enterprise as well. The

entity has been able to increase its sales. There is a significant increase in the overall profits

of Harvey. It has been noticed that there is an increase in the demands of the customers. To

cope up with the demand, the organization have increased its production by investing more

in material and labour.

The overall gross margin ratio has increased from 25.1% to 25.6% (attached in

appendix 1) which shows that there is an increase in the efficiency of the entity. There is an

increase in the revenue of the entity as well. It has increased from 1083 million in 2015 to

1297 million in 2016. Cost of sales for the entity have increased by 184 million dues to

increase in the production. A slight increase in the manufacturing cost have also been

experienced by Harvey due to increase in the cost of raw material.

Net Margin Ratio

2

Gross profit Net sales

0

200

400

600

800

1000

1200

1400

2016

2015

Illustration 1: Comparison of gross profit and net sales

Operating profits Revenue

0

200

400

600

800

1000

1200

1400

2016

2015

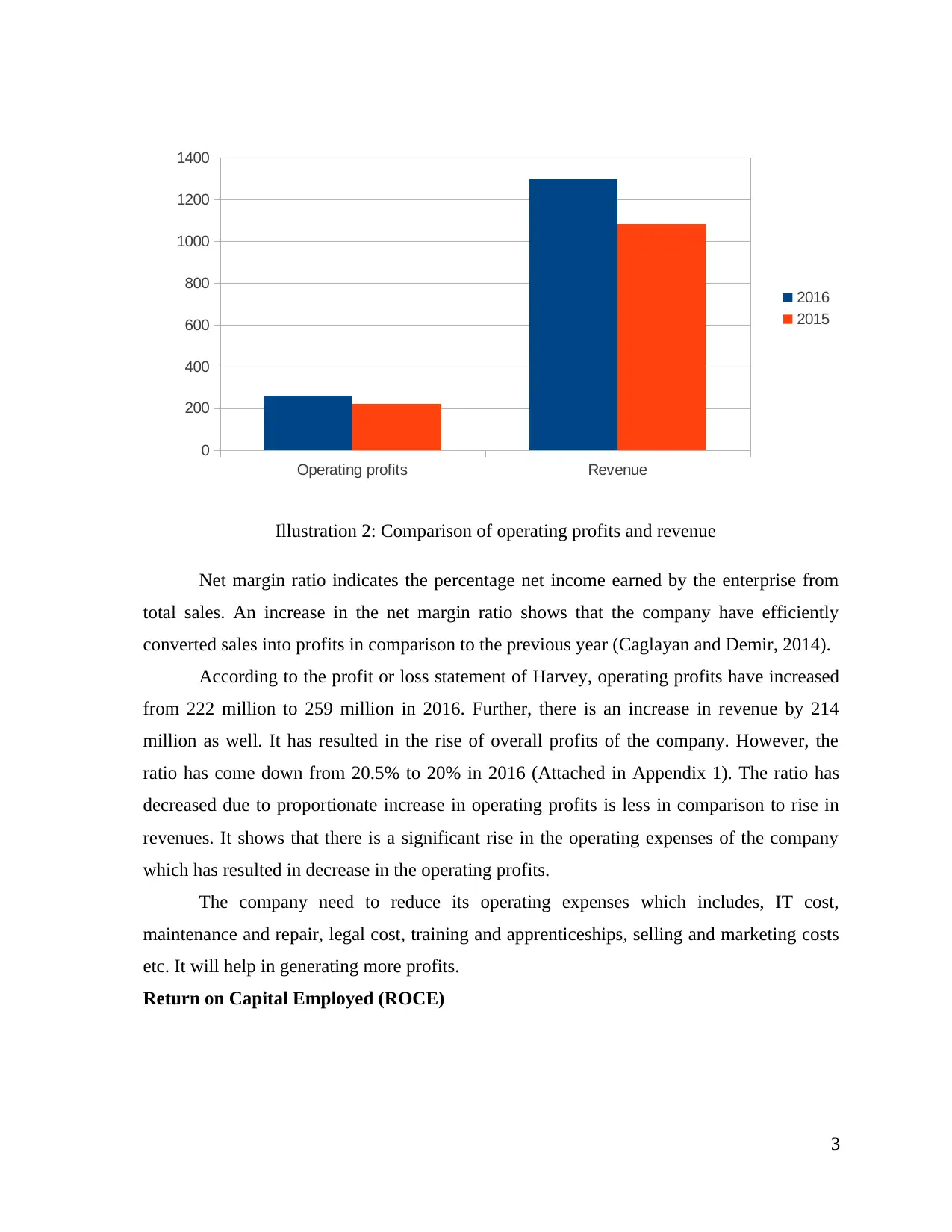

Illustration 2: Comparison of operating profits and revenue

Net margin ratio indicates the percentage net income earned by the enterprise from

total sales. An increase in the net margin ratio shows that the company have efficiently

converted sales into profits in comparison to the previous year (Caglayan and Demir, 2014).

According to the profit or loss statement of Harvey, operating profits have increased

from 222 million to 259 million in 2016. Further, there is an increase in revenue by 214

million as well. It has resulted in the rise of overall profits of the company. However, the

ratio has come down from 20.5% to 20% in 2016 (Attached in Appendix 1). The ratio has

decreased due to proportionate increase in operating profits is less in comparison to rise in

revenues. It shows that there is a significant rise in the operating expenses of the company

which has resulted in decrease in the operating profits.

The company need to reduce its operating expenses which includes, IT cost,

maintenance and repair, legal cost, training and apprenticeships, selling and marketing costs

etc. It will help in generating more profits.

Return on Capital Employed (ROCE)

3

0

200

400

600

800

1000

1200

1400

2016

2015

Illustration 2: Comparison of operating profits and revenue

Net margin ratio indicates the percentage net income earned by the enterprise from

total sales. An increase in the net margin ratio shows that the company have efficiently

converted sales into profits in comparison to the previous year (Caglayan and Demir, 2014).

According to the profit or loss statement of Harvey, operating profits have increased

from 222 million to 259 million in 2016. Further, there is an increase in revenue by 214

million as well. It has resulted in the rise of overall profits of the company. However, the

ratio has come down from 20.5% to 20% in 2016 (Attached in Appendix 1). The ratio has

decreased due to proportionate increase in operating profits is less in comparison to rise in

revenues. It shows that there is a significant rise in the operating expenses of the company

which has resulted in decrease in the operating profits.

The company need to reduce its operating expenses which includes, IT cost,

maintenance and repair, legal cost, training and apprenticeships, selling and marketing costs

etc. It will help in generating more profits.

Return on Capital Employed (ROCE)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating profits Capital employed

0

200

400

600

800

1000

1200

1400

1600

2016

2015

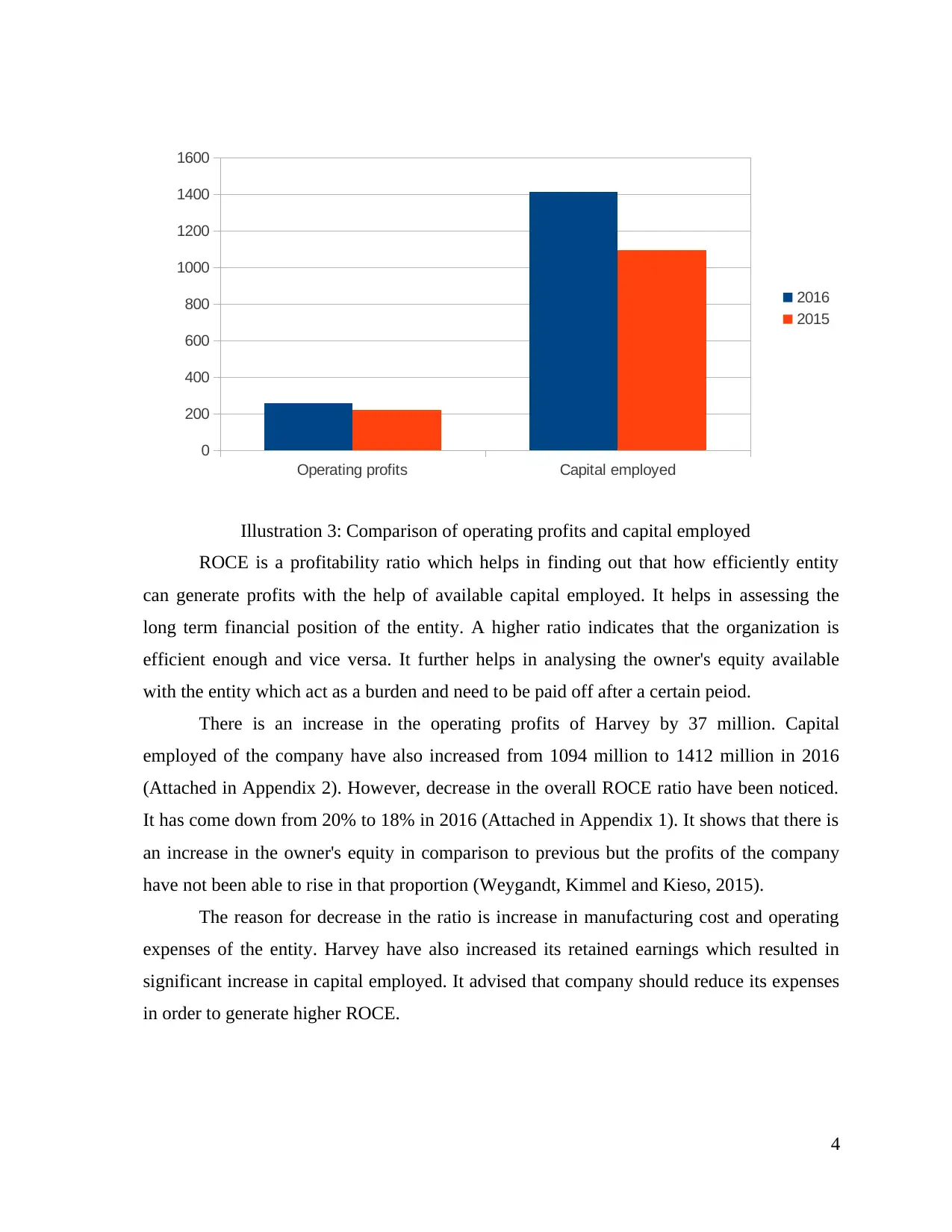

Illustration 3: Comparison of operating profits and capital employed

ROCE is a profitability ratio which helps in finding out that how efficiently entity

can generate profits with the help of available capital employed. It helps in assessing the

long term financial position of the entity. A higher ratio indicates that the organization is

efficient enough and vice versa. It further helps in analysing the owner's equity available

with the entity which act as a burden and need to be paid off after a certain peiod.

There is an increase in the operating profits of Harvey by 37 million. Capital

employed of the company have also increased from 1094 million to 1412 million in 2016

(Attached in Appendix 2). However, decrease in the overall ROCE ratio have been noticed.

It has come down from 20% to 18% in 2016 (Attached in Appendix 1). It shows that there is

an increase in the owner's equity in comparison to previous but the profits of the company

have not been able to rise in that proportion (Weygandt, Kimmel and Kieso, 2015).

The reason for decrease in the ratio is increase in manufacturing cost and operating

expenses of the entity. Harvey have also increased its retained earnings which resulted in

significant increase in capital employed. It advised that company should reduce its expenses

in order to generate higher ROCE.

4

0

200

400

600

800

1000

1200

1400

1600

2016

2015

Illustration 3: Comparison of operating profits and capital employed

ROCE is a profitability ratio which helps in finding out that how efficiently entity

can generate profits with the help of available capital employed. It helps in assessing the

long term financial position of the entity. A higher ratio indicates that the organization is

efficient enough and vice versa. It further helps in analysing the owner's equity available

with the entity which act as a burden and need to be paid off after a certain peiod.

There is an increase in the operating profits of Harvey by 37 million. Capital

employed of the company have also increased from 1094 million to 1412 million in 2016

(Attached in Appendix 2). However, decrease in the overall ROCE ratio have been noticed.

It has come down from 20% to 18% in 2016 (Attached in Appendix 1). It shows that there is

an increase in the owner's equity in comparison to previous but the profits of the company

have not been able to rise in that proportion (Weygandt, Kimmel and Kieso, 2015).

The reason for decrease in the ratio is increase in manufacturing cost and operating

expenses of the entity. Harvey have also increased its retained earnings which resulted in

significant increase in capital employed. It advised that company should reduce its expenses

in order to generate higher ROCE.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

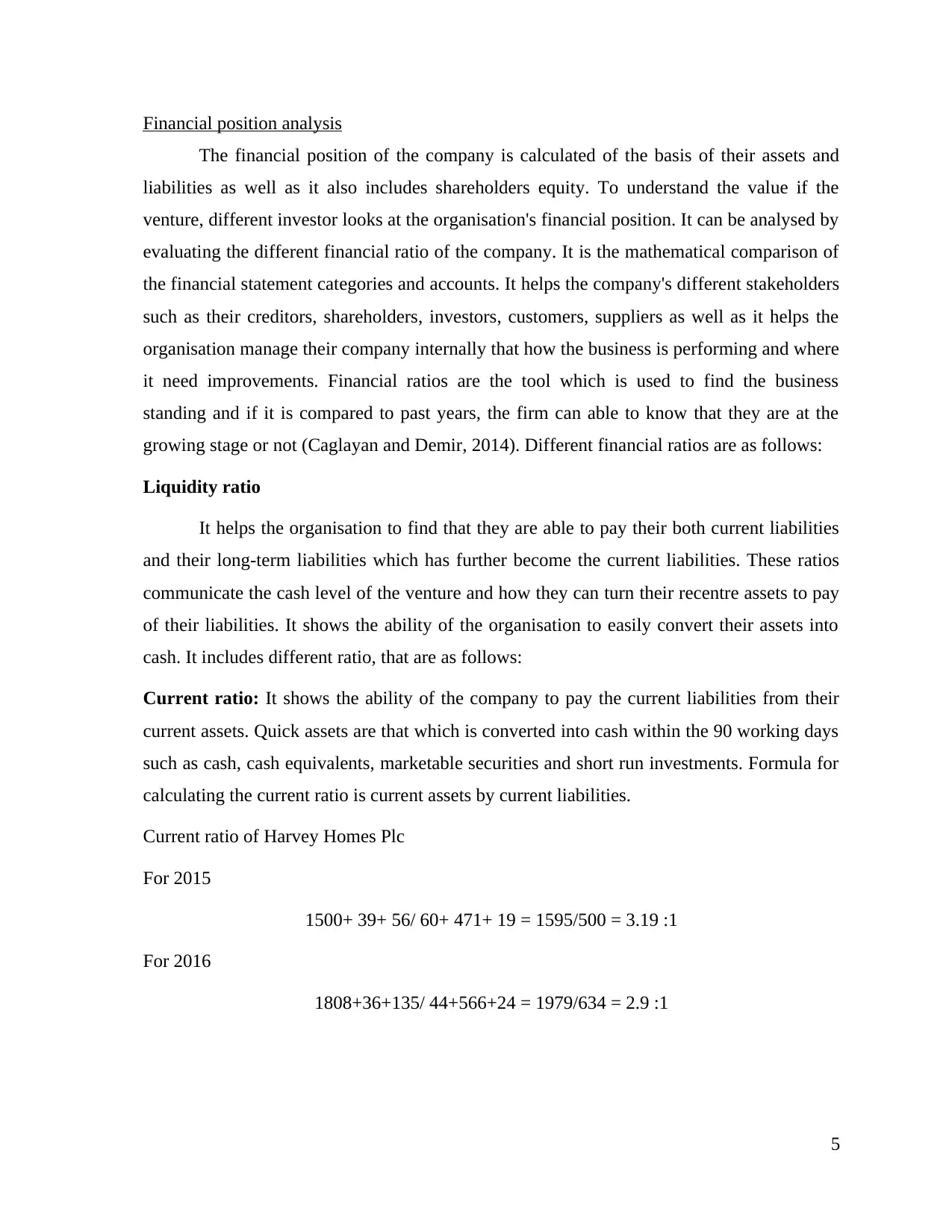

Financial position analysis

The financial position of the company is calculated of the basis of their assets and

liabilities as well as it also includes shareholders equity. To understand the value if the

venture, different investor looks at the organisation's financial position. It can be analysed by

evaluating the different financial ratio of the company. It is the mathematical comparison of

the financial statement categories and accounts. It helps the company's different stakeholders

such as their creditors, shareholders, investors, customers, suppliers as well as it helps the

organisation manage their company internally that how the business is performing and where

it need improvements. Financial ratios are the tool which is used to find the business

standing and if it is compared to past years, the firm can able to know that they are at the

growing stage or not (Caglayan and Demir, 2014). Different financial ratios are as follows:

Liquidity ratio

It helps the organisation to find that they are able to pay their both current liabilities

and their long-term liabilities which has further become the current liabilities. These ratios

communicate the cash level of the venture and how they can turn their recentre assets to pay

of their liabilities. It shows the ability of the organisation to easily convert their assets into

cash. It includes different ratio, that are as follows:

Current ratio: It shows the ability of the company to pay the current liabilities from their

current assets. Quick assets are that which is converted into cash within the 90 working days

such as cash, cash equivalents, marketable securities and short run investments. Formula for

calculating the current ratio is current assets by current liabilities.

Current ratio of Harvey Homes Plc

For 2015

1500+ 39+ 56/ 60+ 471+ 19 = 1595/500 = 3.19 :1

For 2016

1808+36+135/ 44+566+24 = 1979/634 = 2.9 :1

5

The financial position of the company is calculated of the basis of their assets and

liabilities as well as it also includes shareholders equity. To understand the value if the

venture, different investor looks at the organisation's financial position. It can be analysed by

evaluating the different financial ratio of the company. It is the mathematical comparison of

the financial statement categories and accounts. It helps the company's different stakeholders

such as their creditors, shareholders, investors, customers, suppliers as well as it helps the

organisation manage their company internally that how the business is performing and where

it need improvements. Financial ratios are the tool which is used to find the business

standing and if it is compared to past years, the firm can able to know that they are at the

growing stage or not (Caglayan and Demir, 2014). Different financial ratios are as follows:

Liquidity ratio

It helps the organisation to find that they are able to pay their both current liabilities

and their long-term liabilities which has further become the current liabilities. These ratios

communicate the cash level of the venture and how they can turn their recentre assets to pay

of their liabilities. It shows the ability of the organisation to easily convert their assets into

cash. It includes different ratio, that are as follows:

Current ratio: It shows the ability of the company to pay the current liabilities from their

current assets. Quick assets are that which is converted into cash within the 90 working days

such as cash, cash equivalents, marketable securities and short run investments. Formula for

calculating the current ratio is current assets by current liabilities.

Current ratio of Harvey Homes Plc

For 2015

1500+ 39+ 56/ 60+ 471+ 19 = 1595/500 = 3.19 :1

For 2016

1808+36+135/ 44+566+24 = 1979/634 = 2.9 :1

5

1 2

2.75

2.8

2.85

2.9

2.95

3

3.05

3.1

3.15

Current ratio

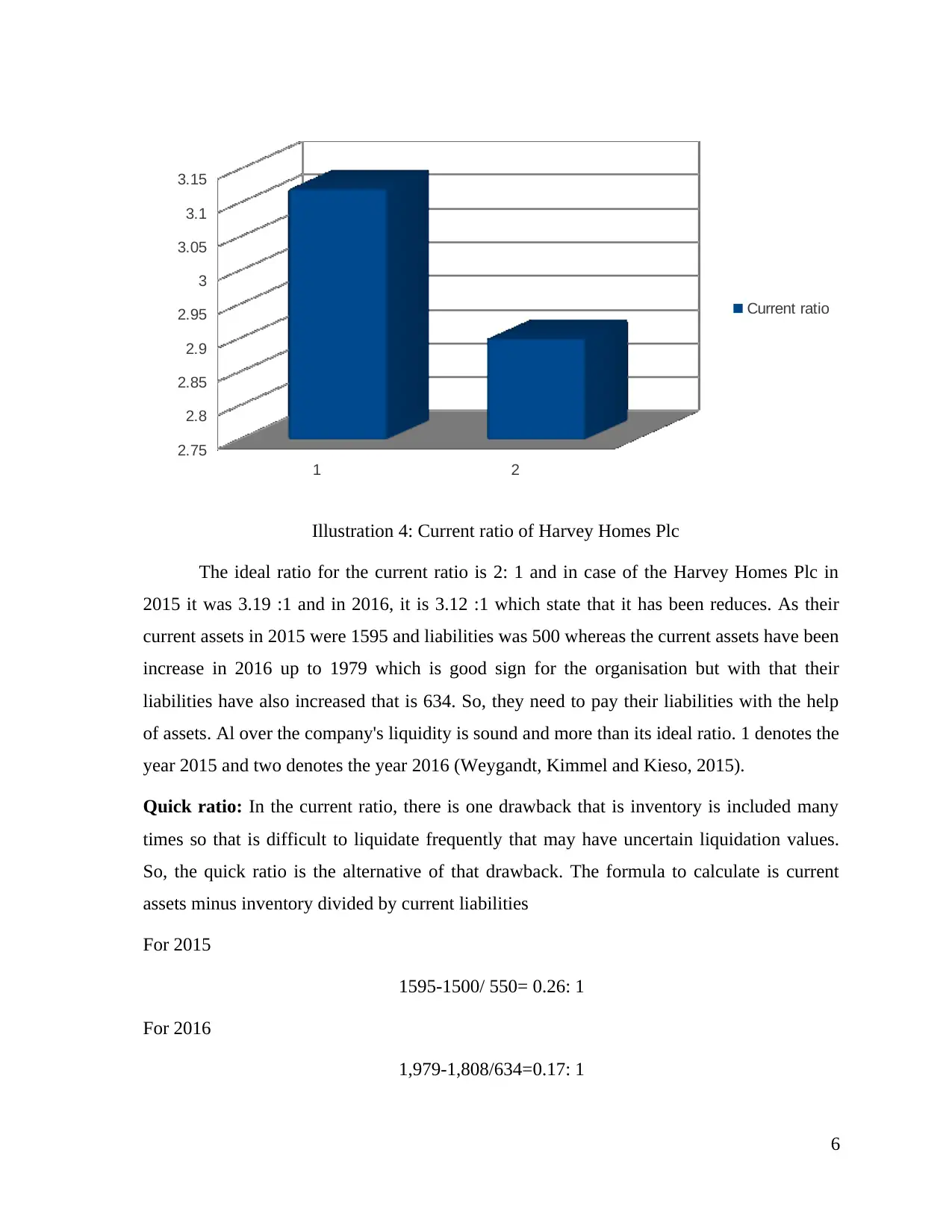

Illustration 4: Current ratio of Harvey Homes Plc

The ideal ratio for the current ratio is 2: 1 and in case of the Harvey Homes Plc in

2015 it was 3.19 :1 and in 2016, it is 3.12 :1 which state that it has been reduces. As their

current assets in 2015 were 1595 and liabilities was 500 whereas the current assets have been

increase in 2016 up to 1979 which is good sign for the organisation but with that their

liabilities have also increased that is 634. So, they need to pay their liabilities with the help

of assets. Al over the company's liquidity is sound and more than its ideal ratio. 1 denotes the

year 2015 and two denotes the year 2016 (Weygandt, Kimmel and Kieso, 2015).

Quick ratio: In the current ratio, there is one drawback that is inventory is included many

times so that is difficult to liquidate frequently that may have uncertain liquidation values.

So, the quick ratio is the alternative of that drawback. The formula to calculate is current

assets minus inventory divided by current liabilities

For 2015

1595-1500/ 550= 0.26: 1

For 2016

1,979-1,808/634=0.17: 1

6

2.75

2.8

2.85

2.9

2.95

3

3.05

3.1

3.15

Current ratio

Illustration 4: Current ratio of Harvey Homes Plc

The ideal ratio for the current ratio is 2: 1 and in case of the Harvey Homes Plc in

2015 it was 3.19 :1 and in 2016, it is 3.12 :1 which state that it has been reduces. As their

current assets in 2015 were 1595 and liabilities was 500 whereas the current assets have been

increase in 2016 up to 1979 which is good sign for the organisation but with that their

liabilities have also increased that is 634. So, they need to pay their liabilities with the help

of assets. Al over the company's liquidity is sound and more than its ideal ratio. 1 denotes the

year 2015 and two denotes the year 2016 (Weygandt, Kimmel and Kieso, 2015).

Quick ratio: In the current ratio, there is one drawback that is inventory is included many

times so that is difficult to liquidate frequently that may have uncertain liquidation values.

So, the quick ratio is the alternative of that drawback. The formula to calculate is current

assets minus inventory divided by current liabilities

For 2015

1595-1500/ 550= 0.26: 1

For 2016

1,979-1,808/634=0.17: 1

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 2

0

0.05

0.1

0.15

0.2

0.25

0.3

Quick ratio

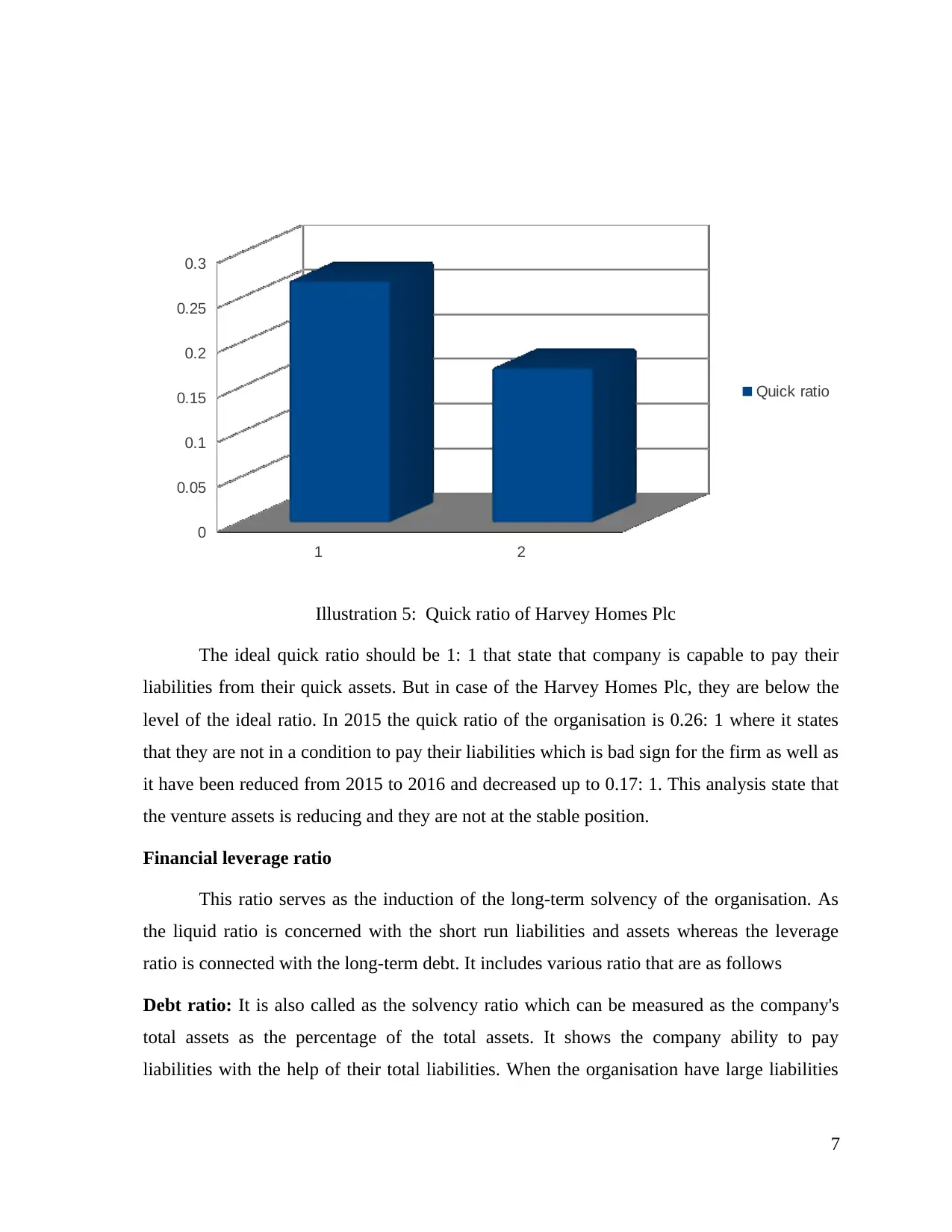

Illustration 5: Quick ratio of Harvey Homes Plc

The ideal quick ratio should be 1: 1 that state that company is capable to pay their

liabilities from their quick assets. But in case of the Harvey Homes Plc, they are below the

level of the ideal ratio. In 2015 the quick ratio of the organisation is 0.26: 1 where it states

that they are not in a condition to pay their liabilities which is bad sign for the firm as well as

it have been reduced from 2015 to 2016 and decreased up to 0.17: 1. This analysis state that

the venture assets is reducing and they are not at the stable position.

Financial leverage ratio

This ratio serves as the induction of the long-term solvency of the organisation. As

the liquid ratio is concerned with the short run liabilities and assets whereas the leverage

ratio is connected with the long-term debt. It includes various ratio that are as follows

Debt ratio: It is also called as the solvency ratio which can be measured as the company's

total assets as the percentage of the total assets. It shows the company ability to pay

liabilities with the help of their total liabilities. When the organisation have large liabilities

7

0

0.05

0.1

0.15

0.2

0.25

0.3

Quick ratio

Illustration 5: Quick ratio of Harvey Homes Plc

The ideal quick ratio should be 1: 1 that state that company is capable to pay their

liabilities from their quick assets. But in case of the Harvey Homes Plc, they are below the

level of the ideal ratio. In 2015 the quick ratio of the organisation is 0.26: 1 where it states

that they are not in a condition to pay their liabilities which is bad sign for the firm as well as

it have been reduced from 2015 to 2016 and decreased up to 0.17: 1. This analysis state that

the venture assets is reducing and they are not at the stable position.

Financial leverage ratio

This ratio serves as the induction of the long-term solvency of the organisation. As

the liquid ratio is concerned with the short run liabilities and assets whereas the leverage

ratio is connected with the long-term debt. It includes various ratio that are as follows

Debt ratio: It is also called as the solvency ratio which can be measured as the company's

total assets as the percentage of the total assets. It shows the company ability to pay

liabilities with the help of their total liabilities. When the organisation have large liabilities

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

over their assets that states that the company is at risk stage, it is calculated as the total debt/

total liabilities (Arnold, 2013).

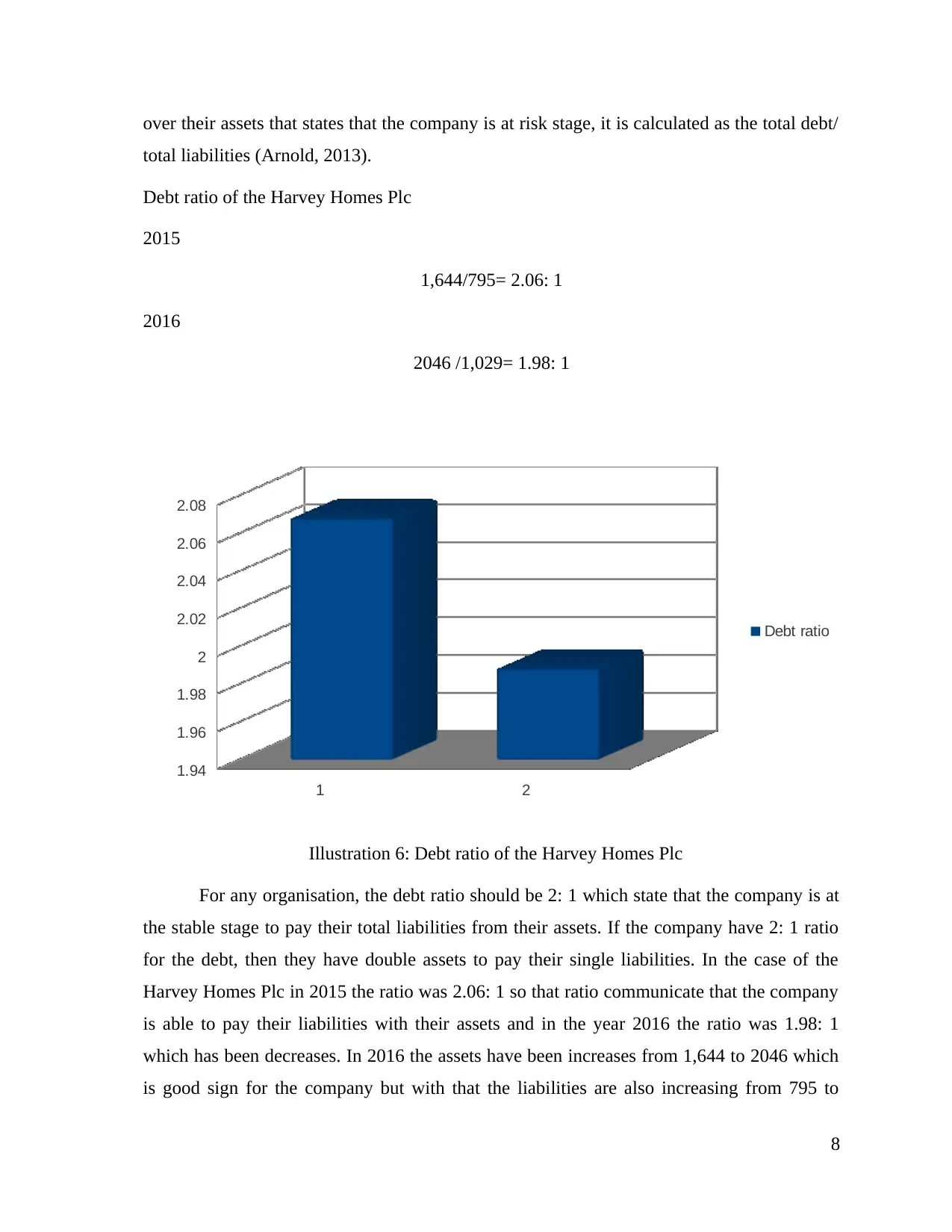

Debt ratio of the Harvey Homes Plc

2015

1,644/795= 2.06: 1

2016

2046 /1,029= 1.98: 1

1 2

1.94

1.96

1.98

2

2.02

2.04

2.06

2.08

Debt ratio

Illustration 6: Debt ratio of the Harvey Homes Plc

For any organisation, the debt ratio should be 2: 1 which state that the company is at

the stable stage to pay their total liabilities from their assets. If the company have 2: 1 ratio

for the debt, then they have double assets to pay their single liabilities. In the case of the

Harvey Homes Plc in 2015 the ratio was 2.06: 1 so that ratio communicate that the company

is able to pay their liabilities with their assets and in the year 2016 the ratio was 1.98: 1

which has been decreases. In 2016 the assets have been increases from 1,644 to 2046 which

is good sign for the company but with that the liabilities are also increasing from 795 to

8

total liabilities (Arnold, 2013).

Debt ratio of the Harvey Homes Plc

2015

1,644/795= 2.06: 1

2016

2046 /1,029= 1.98: 1

1 2

1.94

1.96

1.98

2

2.02

2.04

2.06

2.08

Debt ratio

Illustration 6: Debt ratio of the Harvey Homes Plc

For any organisation, the debt ratio should be 2: 1 which state that the company is at

the stable stage to pay their total liabilities from their assets. If the company have 2: 1 ratio

for the debt, then they have double assets to pay their single liabilities. In the case of the

Harvey Homes Plc in 2015 the ratio was 2.06: 1 so that ratio communicate that the company

is able to pay their liabilities with their assets and in the year 2016 the ratio was 1.98: 1

which has been decreases. In 2016 the assets have been increases from 1,644 to 2046 which

is good sign for the company but with that the liabilities are also increasing from 795 to

8

1,029. So, they need to make that organisation such sound that the can able to increase their

assets so that they can able to pay increasing liabilities.

Analysis of cash flow statement

Cash flow from operating activities

Cash flow from investing activities

Cash flow from financing activities

-50

0

50

100

150

200

Cash flows

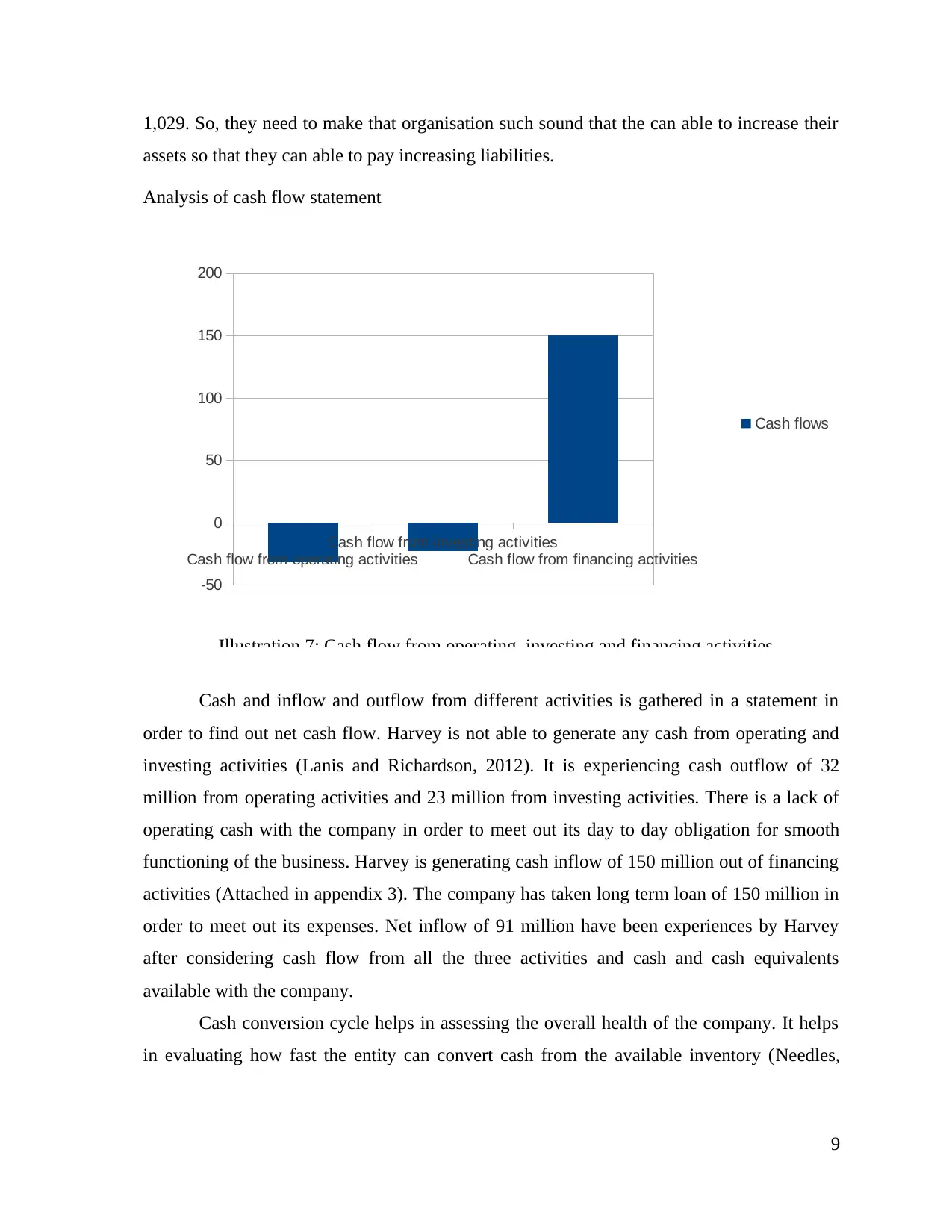

Illustration 7: Cash flow from operating, investing and financing activities

Cash and inflow and outflow from different activities is gathered in a statement in

order to find out net cash flow. Harvey is not able to generate any cash from operating and

investing activities (Lanis and Richardson, 2012). It is experiencing cash outflow of 32

million from operating activities and 23 million from investing activities. There is a lack of

operating cash with the company in order to meet out its day to day obligation for smooth

functioning of the business. Harvey is generating cash inflow of 150 million out of financing

activities (Attached in appendix 3). The company has taken long term loan of 150 million in

order to meet out its expenses. Net inflow of 91 million have been experiences by Harvey

after considering cash flow from all the three activities and cash and cash equivalents

available with the company.

Cash conversion cycle helps in assessing the overall health of the company. It helps

in evaluating how fast the entity can convert cash from the available inventory (Needles,

9

assets so that they can able to pay increasing liabilities.

Analysis of cash flow statement

Cash flow from operating activities

Cash flow from investing activities

Cash flow from financing activities

-50

0

50

100

150

200

Cash flows

Illustration 7: Cash flow from operating, investing and financing activities

Cash and inflow and outflow from different activities is gathered in a statement in

order to find out net cash flow. Harvey is not able to generate any cash from operating and

investing activities (Lanis and Richardson, 2012). It is experiencing cash outflow of 32

million from operating activities and 23 million from investing activities. There is a lack of

operating cash with the company in order to meet out its day to day obligation for smooth

functioning of the business. Harvey is generating cash inflow of 150 million out of financing

activities (Attached in appendix 3). The company has taken long term loan of 150 million in

order to meet out its expenses. Net inflow of 91 million have been experiences by Harvey

after considering cash flow from all the three activities and cash and cash equivalents

available with the company.

Cash conversion cycle helps in assessing the overall health of the company. It helps

in evaluating how fast the entity can convert cash from the available inventory (Needles,

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.