Financial Analysis and Decision Making for Harvey Homes Plc Report

VerifiedAdded on 2019/12/28

|19

|4252

|145

Report

AI Summary

This report presents a comprehensive financial analysis of Harvey Homes Plc, a public sector firm in the real estate and construction industry. The analysis begins with an executive summary highlighting the company's good liquidity and solvency, while recommending strategic improvements in profitability. The report then delves into business performance, utilizing profitability ratios (gross profit, operating profit, and net profit), liquidity ratios (current and quick ratios), and the debt-equity ratio to assess the company's financial health. Furthermore, the report examines the cash flow statement and calculates the operating cash cycle to evaluate the efficiency of cash management. The report also explores investment appraisal methods and suitable financing sources, such as bank loans and equity financing, for potential acquisitions. The analysis reveals insights into the company's performance, identifies areas for improvement, and suggests strategies to enhance financial outcomes, making it a valuable resource for understanding the company's financial position and decision-making processes.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial decision making is the process of taking decision about project funding,

anticipation of market trend and business performance. In the recent times, for attaining success

in the competitive business environment business unit needs to make effectual use of monetary

resources. This project report is based on Harvey homes Plc which offer housing services to the

customers. It can be summarized from the report that liquidity and solvency of Harvey Homes is

good. Besides this, it can be inferred that Harvey Homes plc needs to undertake strategic move

for making improvement in the profitability position or aspect. It can be stated that by investing

money in Midland acquisition project Harvey Homes Plc can aid in profitability aspect of firm.

The current report describes those sources which supports to the Harvey Homes Plc in order to

raise fund to make acquisition in the Midlands market. Further, the suitable sources of financing

for it are such as bank loan as well as equity financing. Apart from this, non financial factors are

also explained at this case which leads to create impact on the company while expanding

business inj new market.

Financial decision making is the process of taking decision about project funding,

anticipation of market trend and business performance. In the recent times, for attaining success

in the competitive business environment business unit needs to make effectual use of monetary

resources. This project report is based on Harvey homes Plc which offer housing services to the

customers. It can be summarized from the report that liquidity and solvency of Harvey Homes is

good. Besides this, it can be inferred that Harvey Homes plc needs to undertake strategic move

for making improvement in the profitability position or aspect. It can be stated that by investing

money in Midland acquisition project Harvey Homes Plc can aid in profitability aspect of firm.

The current report describes those sources which supports to the Harvey Homes Plc in order to

raise fund to make acquisition in the Midlands market. Further, the suitable sources of financing

for it are such as bank loan as well as equity financing. Apart from this, non financial factors are

also explained at this case which leads to create impact on the company while expanding

business inj new market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is having a key and important place within the business environment of every

organisation which support it for exists in the industry. If there are financial resources are not

available in appropriate way along with the adequately then entrepreneur not able to establish a

firm in the market. The current case study is on the basis Harvey Homes plc which is a public

sector firm and operates in the industry of real estate and cpnstruction. The present report shows

and describes that the selected business entity is in which direction performing in its relevant

industry using ratios. Further, for assessing business performance there are profitability, liquidity

ratios and cash conversion cycle is to be calculated. Apart from this, it shows about the market

segment analysis of the Harvey Homes plc that which are the reasons by which one geographic

area performs well or poor. In the second part of the report there is investment appraisal methods

along with their advantages and drawbacks are described. In addition to this, here sources of

finance which are suitable for the chosen entity are shown with the help of its merits and

demerits both.

PART 1

Business Performance Analysis

For analysing performance of an organisation there are different things are to be

considered by the management among which financial is the most important. For determine

business performance of Harvey Homes plc three financial statements are interpreted using

appropriate financial ratios which are shown as below:

Interpretation of the profit and loss statement

Very key financial statement of every business entity is profit and loss account which

shows that management is up to which extent able to generate money in terms of profit. In this

statement of financials there are revenue, various types of expenditures as well as incomes are to

be recorded and calculated (Weygandt, Kimmel and Kieso, 2015). Higher the value of respective

account clearly indicate that the company is performing well among the industry. By analysing

income statement of Harvey Homes Plc it can be said that it is how much profitable within the

industry or segment of logistics. For making analysis and interpret the profit and loss account

there are various types of profitability ratios are to be calculated. Such profitability ratios are like

1

Finance is having a key and important place within the business environment of every

organisation which support it for exists in the industry. If there are financial resources are not

available in appropriate way along with the adequately then entrepreneur not able to establish a

firm in the market. The current case study is on the basis Harvey Homes plc which is a public

sector firm and operates in the industry of real estate and cpnstruction. The present report shows

and describes that the selected business entity is in which direction performing in its relevant

industry using ratios. Further, for assessing business performance there are profitability, liquidity

ratios and cash conversion cycle is to be calculated. Apart from this, it shows about the market

segment analysis of the Harvey Homes plc that which are the reasons by which one geographic

area performs well or poor. In the second part of the report there is investment appraisal methods

along with their advantages and drawbacks are described. In addition to this, here sources of

finance which are suitable for the chosen entity are shown with the help of its merits and

demerits both.

PART 1

Business Performance Analysis

For analysing performance of an organisation there are different things are to be

considered by the management among which financial is the most important. For determine

business performance of Harvey Homes plc three financial statements are interpreted using

appropriate financial ratios which are shown as below:

Interpretation of the profit and loss statement

Very key financial statement of every business entity is profit and loss account which

shows that management is up to which extent able to generate money in terms of profit. In this

statement of financials there are revenue, various types of expenditures as well as incomes are to

be recorded and calculated (Weygandt, Kimmel and Kieso, 2015). Higher the value of respective

account clearly indicate that the company is performing well among the industry. By analysing

income statement of Harvey Homes Plc it can be said that it is how much profitable within the

industry or segment of logistics. For making analysis and interpret the profit and loss account

there are various types of profitability ratios are to be calculated. Such profitability ratios are like

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

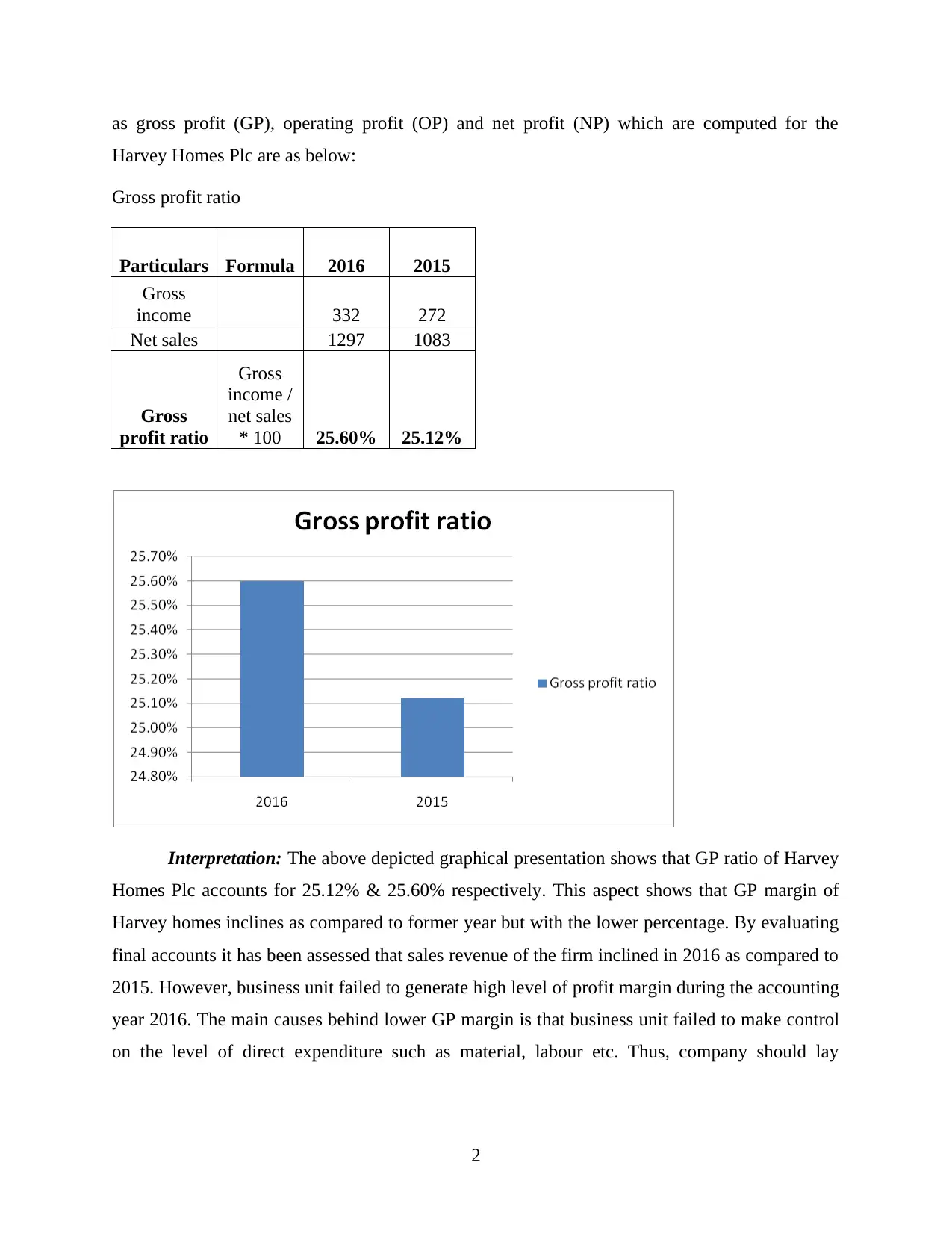

as gross profit (GP), operating profit (OP) and net profit (NP) which are computed for the

Harvey Homes Plc are as below:

Gross profit ratio

Particulars Formula 2016 2015

Gross

income 332 272

Net sales 1297 1083

Gross

profit ratio

Gross

income /

net sales

* 100 25.60% 25.12%

Interpretation: The above depicted graphical presentation shows that GP ratio of Harvey

Homes Plc accounts for 25.12% & 25.60% respectively. This aspect shows that GP margin of

Harvey homes inclines as compared to former year but with the lower percentage. By evaluating

final accounts it has been assessed that sales revenue of the firm inclined in 2016 as compared to

2015. However, business unit failed to generate high level of profit margin during the accounting

year 2016. The main causes behind lower GP margin is that business unit failed to make control

on the level of direct expenditure such as material, labour etc. Thus, company should lay

2

Harvey Homes Plc are as below:

Gross profit ratio

Particulars Formula 2016 2015

Gross

income 332 272

Net sales 1297 1083

Gross

profit ratio

Gross

income /

net sales

* 100 25.60% 25.12%

Interpretation: The above depicted graphical presentation shows that GP ratio of Harvey

Homes Plc accounts for 25.12% & 25.60% respectively. This aspect shows that GP margin of

Harvey homes inclines as compared to former year but with the lower percentage. By evaluating

final accounts it has been assessed that sales revenue of the firm inclined in 2016 as compared to

2015. However, business unit failed to generate high level of profit margin during the accounting

year 2016. The main causes behind lower GP margin is that business unit failed to make control

on the level of direct expenditure such as material, labour etc. Thus, company should lay

2

emphasis on adopting high technology which in turn may result into decline in wastage and

enhancement in operational efficiency.

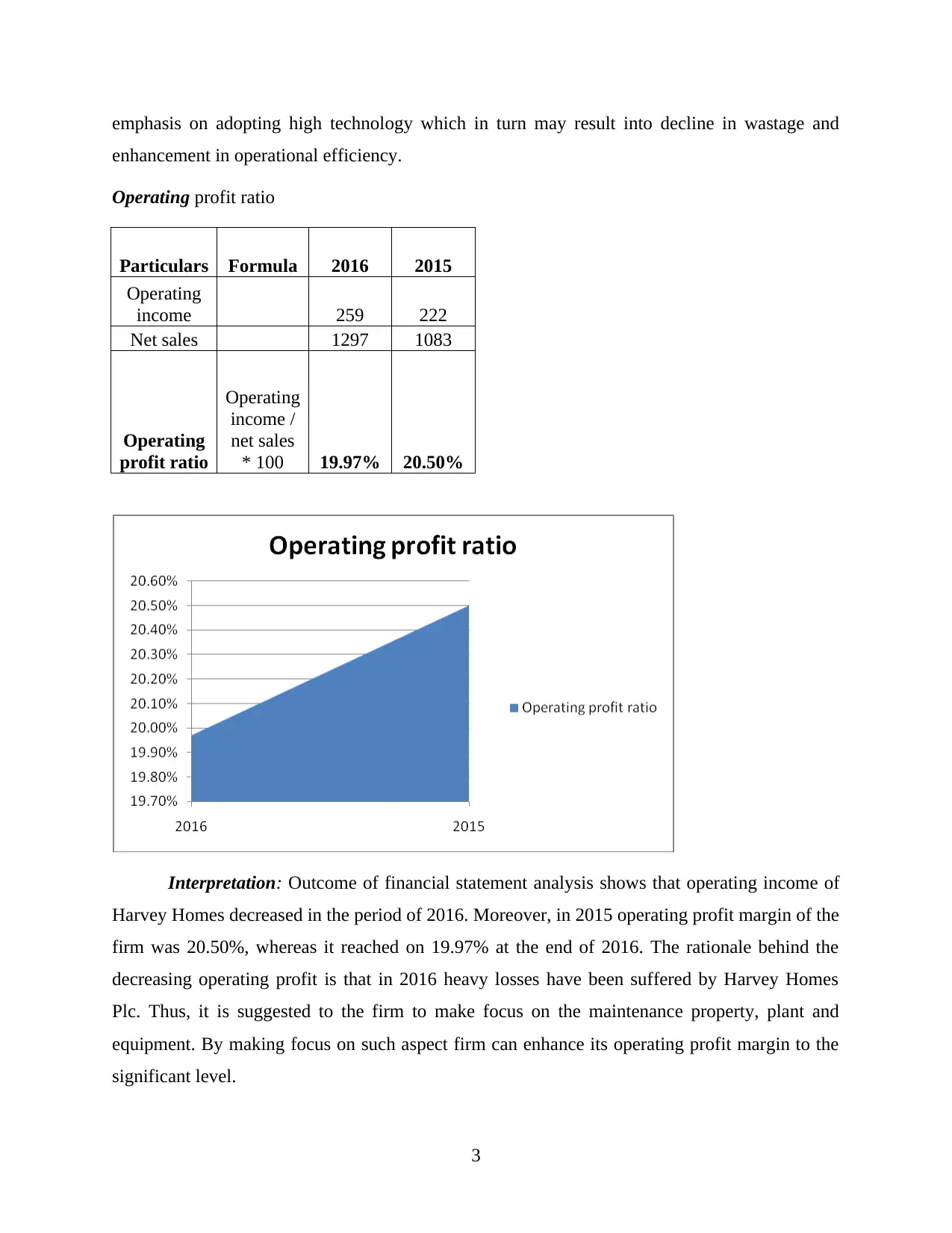

Operating profit ratio

Particulars Formula 2016 2015

Operating

income 259 222

Net sales 1297 1083

Operating

profit ratio

Operating

income /

net sales

* 100 19.97% 20.50%

Interpretation: Outcome of financial statement analysis shows that operating income of

Harvey Homes decreased in the period of 2016. Moreover, in 2015 operating profit margin of the

firm was 20.50%, whereas it reached on 19.97% at the end of 2016. The rationale behind the

decreasing operating profit is that in 2016 heavy losses have been suffered by Harvey Homes

Plc. Thus, it is suggested to the firm to make focus on the maintenance property, plant and

equipment. By making focus on such aspect firm can enhance its operating profit margin to the

significant level.

3

enhancement in operational efficiency.

Operating profit ratio

Particulars Formula 2016 2015

Operating

income 259 222

Net sales 1297 1083

Operating

profit ratio

Operating

income /

net sales

* 100 19.97% 20.50%

Interpretation: Outcome of financial statement analysis shows that operating income of

Harvey Homes decreased in the period of 2016. Moreover, in 2015 operating profit margin of the

firm was 20.50%, whereas it reached on 19.97% at the end of 2016. The rationale behind the

decreasing operating profit is that in 2016 heavy losses have been suffered by Harvey Homes

Plc. Thus, it is suggested to the firm to make focus on the maintenance property, plant and

equipment. By making focus on such aspect firm can enhance its operating profit margin to the

significant level.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

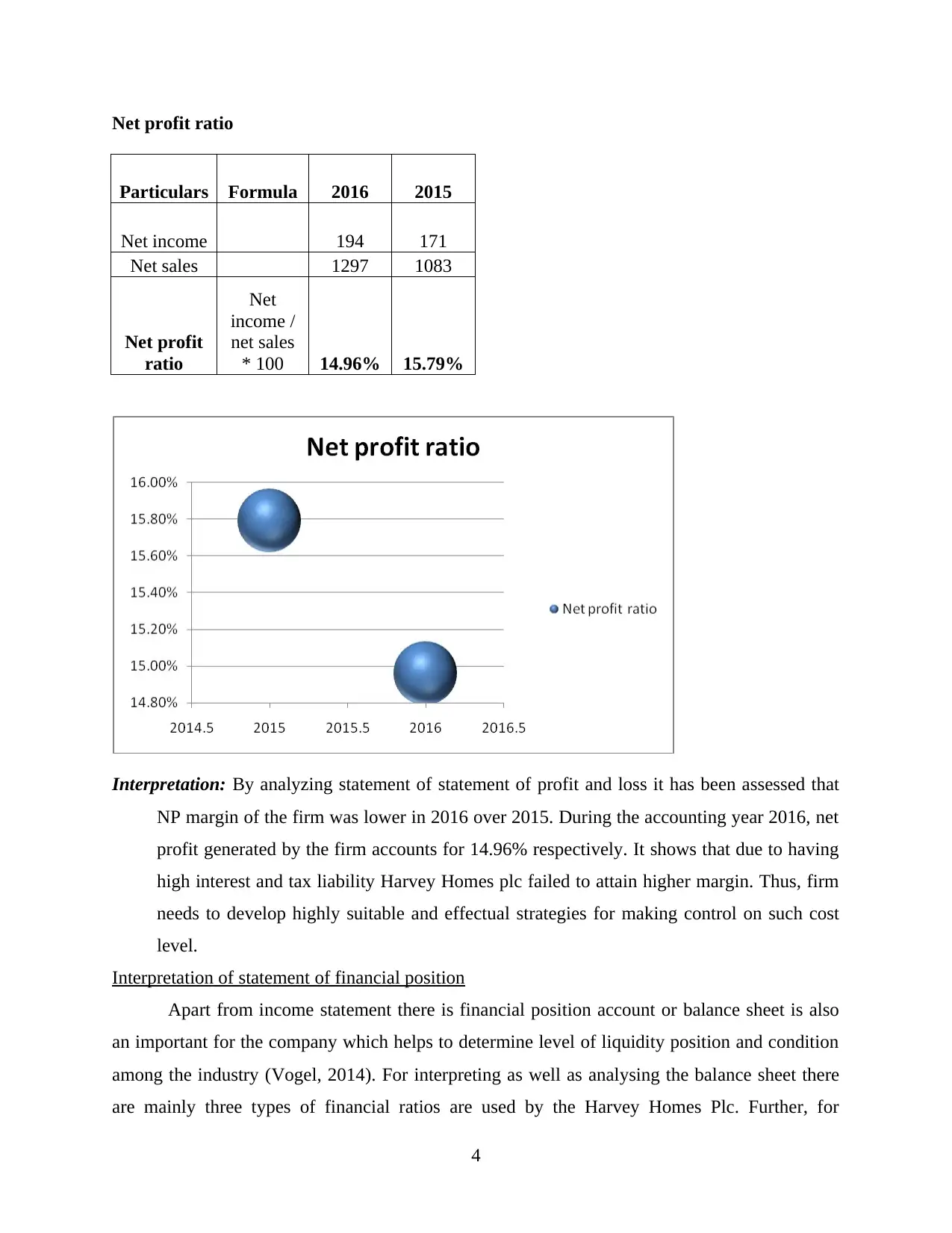

Net profit ratio

Particulars Formula 2016 2015

Net income 194 171

Net sales 1297 1083

Net profit

ratio

Net

income /

net sales

* 100 14.96% 15.79%

Interpretation: By analyzing statement of statement of profit and loss it has been assessed that

NP margin of the firm was lower in 2016 over 2015. During the accounting year 2016, net

profit generated by the firm accounts for 14.96% respectively. It shows that due to having

high interest and tax liability Harvey Homes plc failed to attain higher margin. Thus, firm

needs to develop highly suitable and effectual strategies for making control on such cost

level.

Interpretation of statement of financial position

Apart from income statement there is financial position account or balance sheet is also

an important for the company which helps to determine level of liquidity position and condition

among the industry (Vogel, 2014). For interpreting as well as analysing the balance sheet there

are mainly three types of financial ratios are used by the Harvey Homes Plc. Further, for

4

Particulars Formula 2016 2015

Net income 194 171

Net sales 1297 1083

Net profit

ratio

Net

income /

net sales

* 100 14.96% 15.79%

Interpretation: By analyzing statement of statement of profit and loss it has been assessed that

NP margin of the firm was lower in 2016 over 2015. During the accounting year 2016, net

profit generated by the firm accounts for 14.96% respectively. It shows that due to having

high interest and tax liability Harvey Homes plc failed to attain higher margin. Thus, firm

needs to develop highly suitable and effectual strategies for making control on such cost

level.

Interpretation of statement of financial position

Apart from income statement there is financial position account or balance sheet is also

an important for the company which helps to determine level of liquidity position and condition

among the industry (Vogel, 2014). For interpreting as well as analysing the balance sheet there

are mainly three types of financial ratios are used by the Harvey Homes Plc. Further, for

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interpreting the respective account such ratios are like as current, quick and debt to equity ratio

which are computed as below:

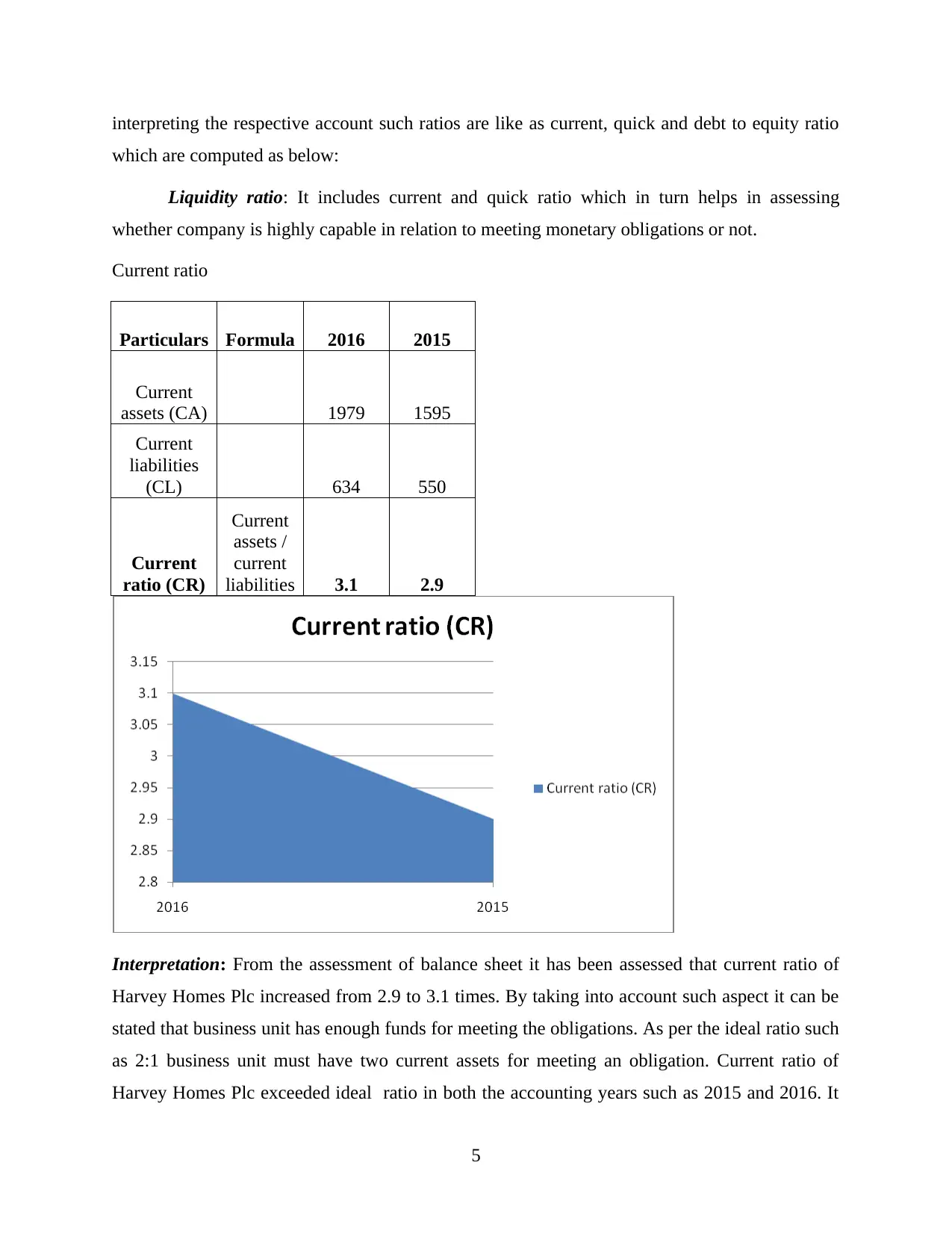

Liquidity ratio: It includes current and quick ratio which in turn helps in assessing

whether company is highly capable in relation to meeting monetary obligations or not.

Current ratio

Particulars Formula 2016 2015

Current

assets (CA) 1979 1595

Current

liabilities

(CL) 634 550

Current

ratio (CR)

Current

assets /

current

liabilities 3.1 2.9

Interpretation: From the assessment of balance sheet it has been assessed that current ratio of

Harvey Homes Plc increased from 2.9 to 3.1 times. By taking into account such aspect it can be

stated that business unit has enough funds for meeting the obligations. As per the ideal ratio such

as 2:1 business unit must have two current assets for meeting an obligation. Current ratio of

Harvey Homes Plc exceeded ideal ratio in both the accounting years such as 2015 and 2016. It

5

which are computed as below:

Liquidity ratio: It includes current and quick ratio which in turn helps in assessing

whether company is highly capable in relation to meeting monetary obligations or not.

Current ratio

Particulars Formula 2016 2015

Current

assets (CA) 1979 1595

Current

liabilities

(CL) 634 550

Current

ratio (CR)

Current

assets /

current

liabilities 3.1 2.9

Interpretation: From the assessment of balance sheet it has been assessed that current ratio of

Harvey Homes Plc increased from 2.9 to 3.1 times. By taking into account such aspect it can be

stated that business unit has enough funds for meeting the obligations. As per the ideal ratio such

as 2:1 business unit must have two current assets for meeting an obligation. Current ratio of

Harvey Homes Plc exceeded ideal ratio in both the accounting years such as 2015 and 2016. It

5

shows that company is financially more sound in relation to meeting the current obligations such

as payment to creditors, bank overdraft etc. Thus, for the enhancement of profit margin Harvey

Homes Plc should assess effectual investment opportunities. Hence, by investing money in the

profitable investment project firm would become able to get the desired level of outcome or

success.

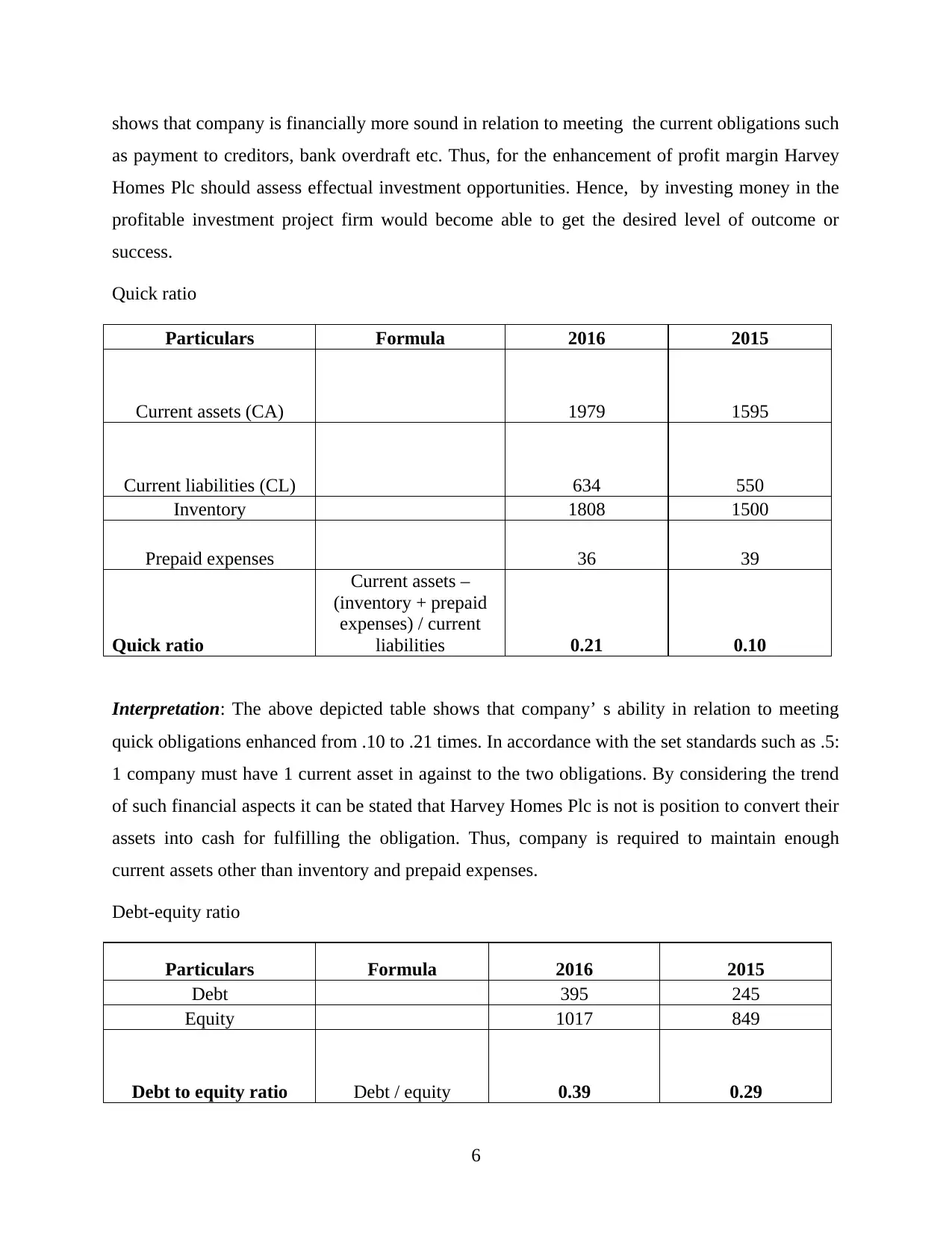

Quick ratio

Particulars Formula 2016 2015

Current assets (CA) 1979 1595

Current liabilities (CL) 634 550

Inventory 1808 1500

Prepaid expenses 36 39

Quick ratio

Current assets –

(inventory + prepaid

expenses) / current

liabilities 0.21 0.10

Interpretation: The above depicted table shows that company’ s ability in relation to meeting

quick obligations enhanced from .10 to .21 times. In accordance with the set standards such as .5:

1 company must have 1 current asset in against to the two obligations. By considering the trend

of such financial aspects it can be stated that Harvey Homes Plc is not is position to convert their

assets into cash for fulfilling the obligation. Thus, company is required to maintain enough

current assets other than inventory and prepaid expenses.

Debt-equity ratio

Particulars Formula 2016 2015

Debt 395 245

Equity 1017 849

Debt to equity ratio Debt / equity 0.39 0.29

6

as payment to creditors, bank overdraft etc. Thus, for the enhancement of profit margin Harvey

Homes Plc should assess effectual investment opportunities. Hence, by investing money in the

profitable investment project firm would become able to get the desired level of outcome or

success.

Quick ratio

Particulars Formula 2016 2015

Current assets (CA) 1979 1595

Current liabilities (CL) 634 550

Inventory 1808 1500

Prepaid expenses 36 39

Quick ratio

Current assets –

(inventory + prepaid

expenses) / current

liabilities 0.21 0.10

Interpretation: The above depicted table shows that company’ s ability in relation to meeting

quick obligations enhanced from .10 to .21 times. In accordance with the set standards such as .5:

1 company must have 1 current asset in against to the two obligations. By considering the trend

of such financial aspects it can be stated that Harvey Homes Plc is not is position to convert their

assets into cash for fulfilling the obligation. Thus, company is required to maintain enough

current assets other than inventory and prepaid expenses.

Debt-equity ratio

Particulars Formula 2016 2015

Debt 395 245

Equity 1017 849

Debt to equity ratio Debt / equity 0.39 0.29

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: Graphical presentation entails that in 2016 level of long term loan increased as

compared to 2015. For the development of optimal capital structure and maintaining the

periodical burden company is required to follow ideal ratio such as .5:1. On the basis of current

performance level it can be said that debt-equity ratio of Harvey Homes Plc is far from the ideal

one. Thus, for making balance in the financial aspects Harvey Homes Plc should issue 2 equity

shares in against to 1 debt. By doing this, firm would become able to generate high profit

through exerting control on fixed monetary burden such as interest.

Interpretation of cash flow statement

In addition to this, there are statement of cash flow is also one of the key accounts which

shows about the incomes and outcomes of the firm in for of monetary. On the basis of the current

financial statement the management of Harvey Homes Plc can highly determine that there is how

much amount remains with firm in form of cash and cash equivalents (Muscettola, 2014).

Apart from such all the activities such as operating, investing and financing for making

analysis of the statement of cash flow there is a ratio used which is such as operating cash cycle

(OCC) It shows that company takes how many days in order to generate cash receipts by using

the purchase and buy of the stock or inventory. For the Harvey Homes Plc operating cash cycle

is calculated and interpreted as below:

Operating Cash Cycle =365 / purchase * Average stock + 365 / sales revenue * average B/R

= (365 / 965) * 1654 + (365 / 1297) * 37.5

= 626 days + 10 days

= 636 days

Average stock or inventory = (1808 + 1500) / 2

= £1654

Average bills receivable = (36 + 39) / 2

= £37.5

Interpretation: By doing analysis of operating cash cycle it has been assessed that Harvey

Homes Plc will take 626 days for converting its inventory into cash. Hence, inventory turnover

of the firm is very high which in turn places direct impact on the working capital aspect or

7

compared to 2015. For the development of optimal capital structure and maintaining the

periodical burden company is required to follow ideal ratio such as .5:1. On the basis of current

performance level it can be said that debt-equity ratio of Harvey Homes Plc is far from the ideal

one. Thus, for making balance in the financial aspects Harvey Homes Plc should issue 2 equity

shares in against to 1 debt. By doing this, firm would become able to generate high profit

through exerting control on fixed monetary burden such as interest.

Interpretation of cash flow statement

In addition to this, there are statement of cash flow is also one of the key accounts which

shows about the incomes and outcomes of the firm in for of monetary. On the basis of the current

financial statement the management of Harvey Homes Plc can highly determine that there is how

much amount remains with firm in form of cash and cash equivalents (Muscettola, 2014).

Apart from such all the activities such as operating, investing and financing for making

analysis of the statement of cash flow there is a ratio used which is such as operating cash cycle

(OCC) It shows that company takes how many days in order to generate cash receipts by using

the purchase and buy of the stock or inventory. For the Harvey Homes Plc operating cash cycle

is calculated and interpreted as below:

Operating Cash Cycle =365 / purchase * Average stock + 365 / sales revenue * average B/R

= (365 / 965) * 1654 + (365 / 1297) * 37.5

= 626 days + 10 days

= 636 days

Average stock or inventory = (1808 + 1500) / 2

= £1654

Average bills receivable = (36 + 39) / 2

= £37.5

Interpretation: By doing analysis of operating cash cycle it has been assessed that Harvey

Homes Plc will take 626 days for converting its inventory into cash. Hence, inventory turnover

of the firm is very high which in turn places direct impact on the working capital aspect or

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

position of the firm. Thus, business unit should place emphasis on the employing effectual

inventory control tools and techniques. Further, by making focus on innovation and uniqueness

Harvey Homes Plc would become able to entice the decision making aspect of customers. In this

way, by selling more houses firm can convert its inventory level into cash within the appropriate

time frame. On the other side, receivable turnover ratio entails that firm has to wait for 10 days in

relation to recover amount from debtors. On an average cash conversion cycle is 636 days which

is too higher. Thus, it can be presented that Harvey Homes plc should undertake effectual

measure and modify the existing strategies for making improvement in the cash cycle.

Market segment analysis

In the segmentation there is Harvey Homes plc firm divides into small parts on the basis

of geographical areas and on the basis of it products and services are to be provided. In the

current case, Harvey Homes plc operate in the Northern, Midlands and Southern market which

provide different value of profits in their respective workplace. It can be said from the statement

of segmental analysis that Northern market earns and generates lesser gross profit as compare to

the Midlands and Southern segment. The key and important reason behind generating lesser

gross profit is that cost of goods sold and revenue both reduces but with the lower and higher rate

respectively (Lin and et.al., 2014). Apart from this, it can be ascertained from the respective

statement that level of assets and the liabilities both are reduces in all segments but in the

Midlands segment it decreases with the higher rate. Furthermore, it can be clearly said that

Midlands segment does not have effectual strategies for enhancing attraction of the consumers.

PART 2

Investment Appraisal

The techniques which are used by the firm in order to estimate and forecast that whether

to make investment in a project will be profitable or not in the future is called as an investment

appraisal. At the time of making investment in Midlands market the Harvey Homes Plc consider

three investment appraisal methods which are such as payback period, ARR and NPV which are

evaluated below:

8

inventory control tools and techniques. Further, by making focus on innovation and uniqueness

Harvey Homes Plc would become able to entice the decision making aspect of customers. In this

way, by selling more houses firm can convert its inventory level into cash within the appropriate

time frame. On the other side, receivable turnover ratio entails that firm has to wait for 10 days in

relation to recover amount from debtors. On an average cash conversion cycle is 636 days which

is too higher. Thus, it can be presented that Harvey Homes plc should undertake effectual

measure and modify the existing strategies for making improvement in the cash cycle.

Market segment analysis

In the segmentation there is Harvey Homes plc firm divides into small parts on the basis

of geographical areas and on the basis of it products and services are to be provided. In the

current case, Harvey Homes plc operate in the Northern, Midlands and Southern market which

provide different value of profits in their respective workplace. It can be said from the statement

of segmental analysis that Northern market earns and generates lesser gross profit as compare to

the Midlands and Southern segment. The key and important reason behind generating lesser

gross profit is that cost of goods sold and revenue both reduces but with the lower and higher rate

respectively (Lin and et.al., 2014). Apart from this, it can be ascertained from the respective

statement that level of assets and the liabilities both are reduces in all segments but in the

Midlands segment it decreases with the higher rate. Furthermore, it can be clearly said that

Midlands segment does not have effectual strategies for enhancing attraction of the consumers.

PART 2

Investment Appraisal

The techniques which are used by the firm in order to estimate and forecast that whether

to make investment in a project will be profitable or not in the future is called as an investment

appraisal. At the time of making investment in Midlands market the Harvey Homes Plc consider

three investment appraisal methods which are such as payback period, ARR and NPV which are

evaluated below:

8

Payback period

Under this method Harvey Homes Plc able to determine that within how many years the

initial investment amount will be recover. The project which has lower the years of payback

period that will be consider to make investment.

Advantages:

It is very easy method as well as simple in order to calculate payback period.

It provides cleat indication about the certainty of cash flows of the project to the Harvey

Homes Plc. It helps to ranking the project that which one will give recover potential investment

amount earlier (Lima, 2014).

Drawbacks:

Payback period method not consider the time value of money which lead to reduce

effective decision for investment.

Particular year at which the initial amount is recovered and after that it not takes cash

flow of further year.

Accounting rate of return

It shows total the average return that will be provided by the initial investment at the end

of completing the project years. When there are two more simultaneous projects and one which

has higher ARR that will be undertaken by the Harvey Homes Plc.

Benefits:

To make the calculation of the average rate of return is very simple and easy and because

of this reason an employee which has basic knowledge of finance can be compute

(Cohen, Naoum and Vlismas, 2014).

It shows the clear scenario and picture of the level of profit and return of a project. Furthermore, it supports to Harvey Homes Plc in order to measure existing business

performance.

Limitations:

9

Under this method Harvey Homes Plc able to determine that within how many years the

initial investment amount will be recover. The project which has lower the years of payback

period that will be consider to make investment.

Advantages:

It is very easy method as well as simple in order to calculate payback period.

It provides cleat indication about the certainty of cash flows of the project to the Harvey

Homes Plc. It helps to ranking the project that which one will give recover potential investment

amount earlier (Lima, 2014).

Drawbacks:

Payback period method not consider the time value of money which lead to reduce

effective decision for investment.

Particular year at which the initial amount is recovered and after that it not takes cash

flow of further year.

Accounting rate of return

It shows total the average return that will be provided by the initial investment at the end

of completing the project years. When there are two more simultaneous projects and one which

has higher ARR that will be undertaken by the Harvey Homes Plc.

Benefits:

To make the calculation of the average rate of return is very simple and easy and because

of this reason an employee which has basic knowledge of finance can be compute

(Cohen, Naoum and Vlismas, 2014).

It shows the clear scenario and picture of the level of profit and return of a project. Furthermore, it supports to Harvey Homes Plc in order to measure existing business

performance.

Limitations:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.