Corporate Accounting Report: A Financial Analysis of Harvey Norman Ltd

VerifiedAdded on 2023/06/11

|13

|2704

|282

Report

AI Summary

This report provides a detailed corporate accounting analysis of Harvey Norman Limited, an ASX-listed company, based on its financial statements from the last three years. It examines the cash flow statement, income statement, comprehensive income statement, and balance sheet. The analysis includes a discussion of changes in cash flow items, the components of comprehensive income, and an evaluation of the company's tax expenses and deferred tax liabilities. The report also addresses the differences between accounting profit and taxable income, providing insights into the company's financial recording processes and compliance with accounting standards. Desklib provides a platform for students to access similar solved assignments and past papers.

HARVEY NORMAN LIMITED

Corporate Accounting

Student’s Name

[25/5/2018]

Corporate Accounting

Student’s Name

[25/5/2018]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

2

Contents

Introduction:.....................................................................................................................3

Harvey Norman limited:...................................................................................................3

Que 1:................................................................................................................................3

Que 2:................................................................................................................................5

Que 3:................................................................................................................................5

Que 4:................................................................................................................................6

Que 5:................................................................................................................................6

Que 6:................................................................................................................................7

Que 7:................................................................................................................................7

Que 8:................................................................................................................................8

Que 9:................................................................................................................................9

Que 10:..............................................................................................................................9

Que 11:............................................................................................................................10

Conclusion:.....................................................................................................................10

References:.....................................................................................................................11

2

Contents

Introduction:.....................................................................................................................3

Harvey Norman limited:...................................................................................................3

Que 1:................................................................................................................................3

Que 2:................................................................................................................................5

Que 3:................................................................................................................................5

Que 4:................................................................................................................................6

Que 5:................................................................................................................................6

Que 6:................................................................................................................................7

Que 7:................................................................................................................................7

Que 8:................................................................................................................................8

Que 9:................................................................................................................................9

Que 10:..............................................................................................................................9

Que 11:............................................................................................................................10

Conclusion:.....................................................................................................................10

References:.....................................................................................................................11

Corporate Accounting

3

Introduction:

Evaluating the income statement recording process, cash flows recording process and

taxation recording process are one of the major elements of the accounting process. It

examines the standards and the accounting process which has been used by the company to

measure the accounting figures and their recording process in the annual report. It examines

the fair accounting valuation method, disclosure policy, materiality policy, notes to accounts

and a detailed description about all the accounting figures in the annual report of the

company.

The report explains about the various financial statement of the company such income

statement, cash flow statement, comprehensive income statement and the balance sheet of the

company. It measures the different figures and the recording style of the company to identify

that whether the company has used proper rules, regulations and the policies to record the

financial and accounting figures of the company in the final financial statement of the

company.

Harvey Norman limited:

Harvey Norman limited is one of largest Australian company in the retailing and

electrical industry. Mainly, the comapny operates it business in retailing of furniture,

computers beddings, consumer electrical products and combination products. The company

operates it business through various franchise, it has been founded in 1982. Home (2018)

explains that around 2820 franchise stores are owned by the company to run the business and

manage the performance of the company. The brand names of the company are Harvey

Norman, Domayne and Joyce, Mayne etc. the company is also operating its business at

overseas. Annual report of the company briefs that the company has followed the AASB,

FASB and IFRS rules to determines and record all the accounting activities and figures in the

annual report of the company.

Que 1:

Cash flow statement is crucial statement of an organization which is prepared by the

companies to evaluate the changes in the cash in a particular period; this statement measures

3

Introduction:

Evaluating the income statement recording process, cash flows recording process and

taxation recording process are one of the major elements of the accounting process. It

examines the standards and the accounting process which has been used by the company to

measure the accounting figures and their recording process in the annual report. It examines

the fair accounting valuation method, disclosure policy, materiality policy, notes to accounts

and a detailed description about all the accounting figures in the annual report of the

company.

The report explains about the various financial statement of the company such income

statement, cash flow statement, comprehensive income statement and the balance sheet of the

company. It measures the different figures and the recording style of the company to identify

that whether the company has used proper rules, regulations and the policies to record the

financial and accounting figures of the company in the final financial statement of the

company.

Harvey Norman limited:

Harvey Norman limited is one of largest Australian company in the retailing and

electrical industry. Mainly, the comapny operates it business in retailing of furniture,

computers beddings, consumer electrical products and combination products. The company

operates it business through various franchise, it has been founded in 1982. Home (2018)

explains that around 2820 franchise stores are owned by the company to run the business and

manage the performance of the company. The brand names of the company are Harvey

Norman, Domayne and Joyce, Mayne etc. the company is also operating its business at

overseas. Annual report of the company briefs that the company has followed the AASB,

FASB and IFRS rules to determines and record all the accounting activities and figures in the

annual report of the company.

Que 1:

Cash flow statement is crucial statement of an organization which is prepared by the

companies to evaluate the changes in the cash in a particular period; this statement measures

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

4

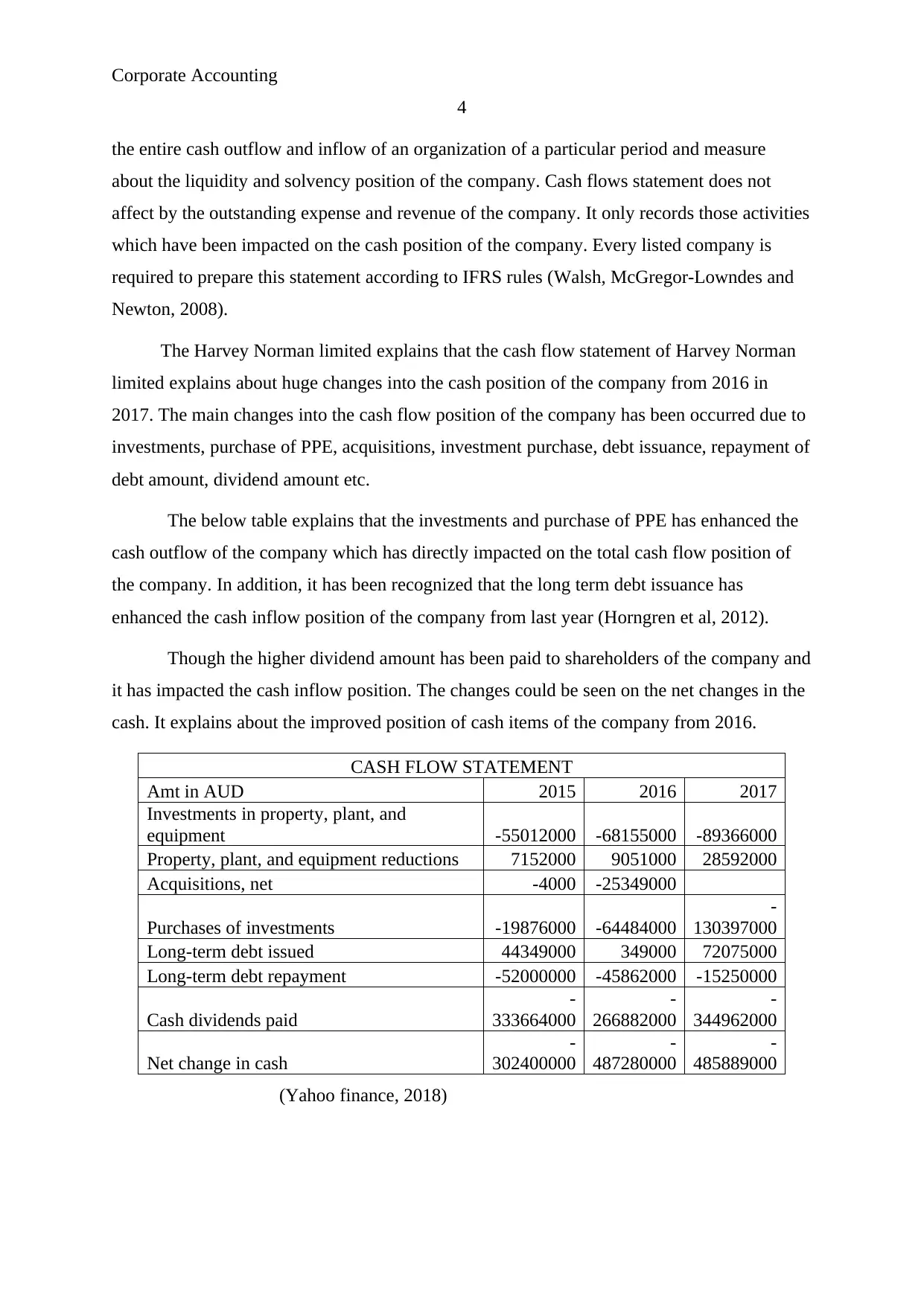

the entire cash outflow and inflow of an organization of a particular period and measure

about the liquidity and solvency position of the company. Cash flows statement does not

affect by the outstanding expense and revenue of the company. It only records those activities

which have been impacted on the cash position of the company. Every listed company is

required to prepare this statement according to IFRS rules (Walsh, McGregor‐Lowndes and

Newton, 2008).

The Harvey Norman limited explains that the cash flow statement of Harvey Norman

limited explains about huge changes into the cash position of the company from 2016 in

2017. The main changes into the cash flow position of the company has been occurred due to

investments, purchase of PPE, acquisitions, investment purchase, debt issuance, repayment of

debt amount, dividend amount etc.

The below table explains that the investments and purchase of PPE has enhanced the

cash outflow of the company which has directly impacted on the total cash flow position of

the company. In addition, it has been recognized that the long term debt issuance has

enhanced the cash inflow position of the company from last year (Horngren et al, 2012).

Though the higher dividend amount has been paid to shareholders of the company and

it has impacted the cash inflow position. The changes could be seen on the net changes in the

cash. It explains about the improved position of cash items of the company from 2016.

CASH FLOW STATEMENT

Amt in AUD 2015 2016 2017

Investments in property, plant, and

equipment -55012000 -68155000 -89366000

Property, plant, and equipment reductions 7152000 9051000 28592000

Acquisitions, net -4000 -25349000

Purchases of investments -19876000 -64484000

-

130397000

Long-term debt issued 44349000 349000 72075000

Long-term debt repayment -52000000 -45862000 -15250000

Cash dividends paid

-

333664000

-

266882000

-

344962000

Net change in cash

-

302400000

-

487280000

-

485889000

(Yahoo finance, 2018)

4

the entire cash outflow and inflow of an organization of a particular period and measure

about the liquidity and solvency position of the company. Cash flows statement does not

affect by the outstanding expense and revenue of the company. It only records those activities

which have been impacted on the cash position of the company. Every listed company is

required to prepare this statement according to IFRS rules (Walsh, McGregor‐Lowndes and

Newton, 2008).

The Harvey Norman limited explains that the cash flow statement of Harvey Norman

limited explains about huge changes into the cash position of the company from 2016 in

2017. The main changes into the cash flow position of the company has been occurred due to

investments, purchase of PPE, acquisitions, investment purchase, debt issuance, repayment of

debt amount, dividend amount etc.

The below table explains that the investments and purchase of PPE has enhanced the

cash outflow of the company which has directly impacted on the total cash flow position of

the company. In addition, it has been recognized that the long term debt issuance has

enhanced the cash inflow position of the company from last year (Horngren et al, 2012).

Though the higher dividend amount has been paid to shareholders of the company and

it has impacted the cash inflow position. The changes could be seen on the net changes in the

cash. It explains about the improved position of cash items of the company from 2016.

CASH FLOW STATEMENT

Amt in AUD 2015 2016 2017

Investments in property, plant, and

equipment -55012000 -68155000 -89366000

Property, plant, and equipment reductions 7152000 9051000 28592000

Acquisitions, net -4000 -25349000

Purchases of investments -19876000 -64484000

-

130397000

Long-term debt issued 44349000 349000 72075000

Long-term debt repayment -52000000 -45862000 -15250000

Cash dividends paid

-

333664000

-

266882000

-

344962000

Net change in cash

-

302400000

-

487280000

-

485889000

(Yahoo finance, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

5

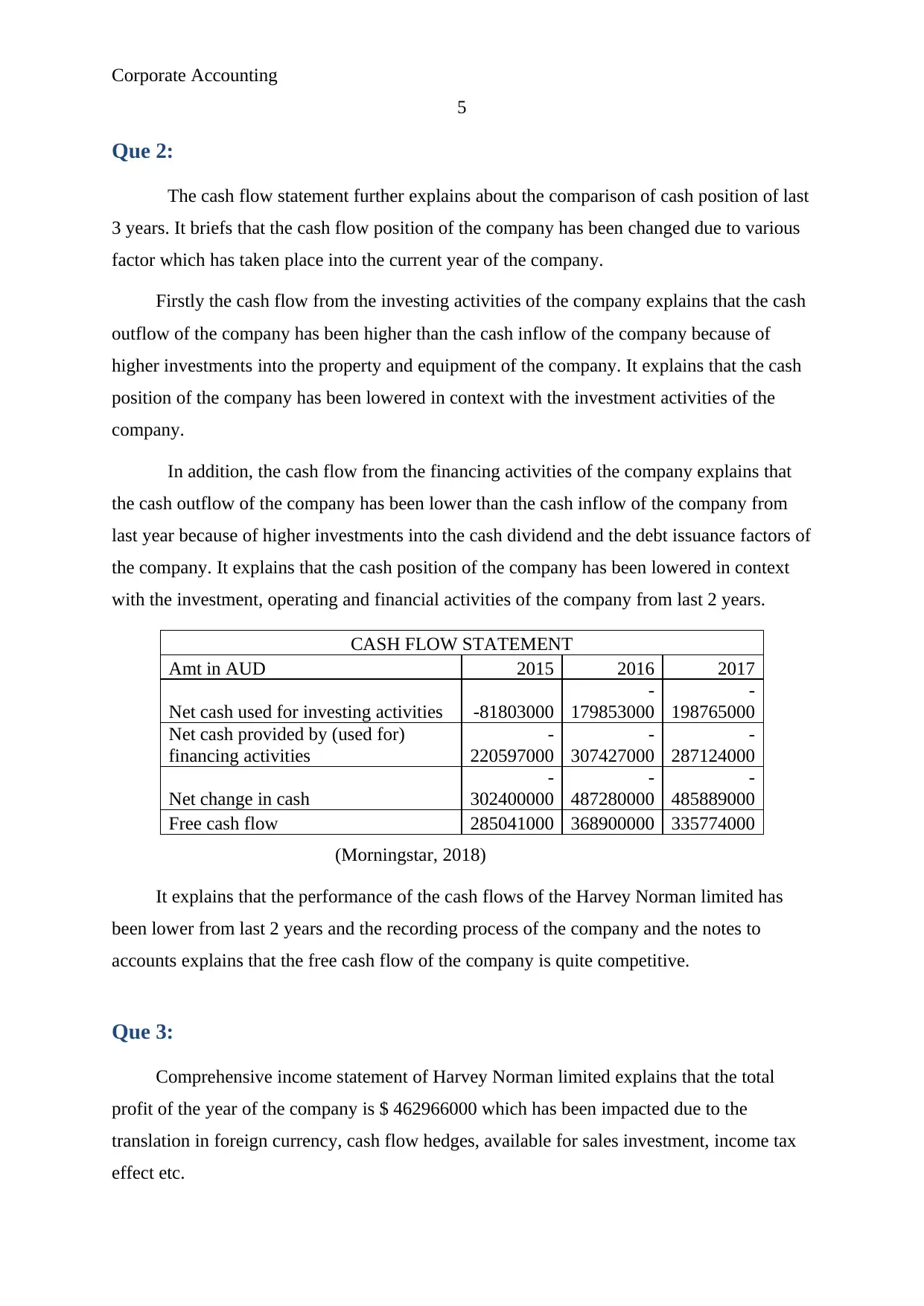

Que 2:

The cash flow statement further explains about the comparison of cash position of last

3 years. It briefs that the cash flow position of the company has been changed due to various

factor which has taken place into the current year of the company.

Firstly the cash flow from the investing activities of the company explains that the cash

outflow of the company has been higher than the cash inflow of the company because of

higher investments into the property and equipment of the company. It explains that the cash

position of the company has been lowered in context with the investment activities of the

company.

In addition, the cash flow from the financing activities of the company explains that

the cash outflow of the company has been lower than the cash inflow of the company from

last year because of higher investments into the cash dividend and the debt issuance factors of

the company. It explains that the cash position of the company has been lowered in context

with the investment, operating and financial activities of the company from last 2 years.

CASH FLOW STATEMENT

Amt in AUD 2015 2016 2017

Net cash used for investing activities -81803000

-

179853000

-

198765000

Net cash provided by (used for)

financing activities

-

220597000

-

307427000

-

287124000

Net change in cash

-

302400000

-

487280000

-

485889000

Free cash flow 285041000 368900000 335774000

(Morningstar, 2018)

It explains that the performance of the cash flows of the Harvey Norman limited has

been lower from last 2 years and the recording process of the company and the notes to

accounts explains that the free cash flow of the company is quite competitive.

Que 3:

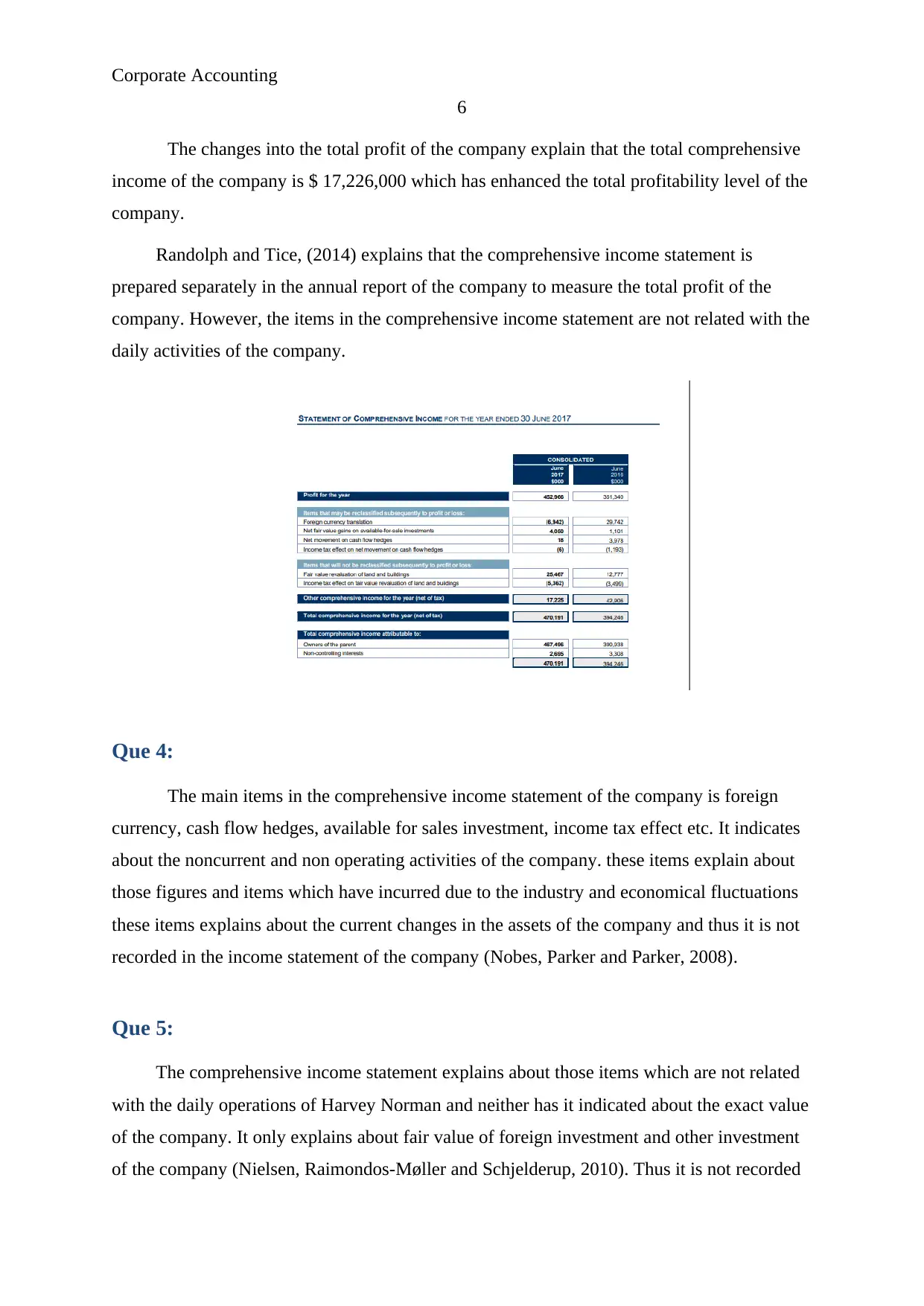

Comprehensive income statement of Harvey Norman limited explains that the total

profit of the year of the company is $ 462966000 which has been impacted due to the

translation in foreign currency, cash flow hedges, available for sales investment, income tax

effect etc.

5

Que 2:

The cash flow statement further explains about the comparison of cash position of last

3 years. It briefs that the cash flow position of the company has been changed due to various

factor which has taken place into the current year of the company.

Firstly the cash flow from the investing activities of the company explains that the cash

outflow of the company has been higher than the cash inflow of the company because of

higher investments into the property and equipment of the company. It explains that the cash

position of the company has been lowered in context with the investment activities of the

company.

In addition, the cash flow from the financing activities of the company explains that

the cash outflow of the company has been lower than the cash inflow of the company from

last year because of higher investments into the cash dividend and the debt issuance factors of

the company. It explains that the cash position of the company has been lowered in context

with the investment, operating and financial activities of the company from last 2 years.

CASH FLOW STATEMENT

Amt in AUD 2015 2016 2017

Net cash used for investing activities -81803000

-

179853000

-

198765000

Net cash provided by (used for)

financing activities

-

220597000

-

307427000

-

287124000

Net change in cash

-

302400000

-

487280000

-

485889000

Free cash flow 285041000 368900000 335774000

(Morningstar, 2018)

It explains that the performance of the cash flows of the Harvey Norman limited has

been lower from last 2 years and the recording process of the company and the notes to

accounts explains that the free cash flow of the company is quite competitive.

Que 3:

Comprehensive income statement of Harvey Norman limited explains that the total

profit of the year of the company is $ 462966000 which has been impacted due to the

translation in foreign currency, cash flow hedges, available for sales investment, income tax

effect etc.

Corporate Accounting

6

The changes into the total profit of the company explain that the total comprehensive

income of the company is $ 17,226,000 which has enhanced the total profitability level of the

company.

Randolph and Tice, (2014) explains that the comprehensive income statement is

prepared separately in the annual report of the company to measure the total profit of the

company. However, the items in the comprehensive income statement are not related with the

daily activities of the company.

Que 4:

The main items in the comprehensive income statement of the company is foreign

currency, cash flow hedges, available for sales investment, income tax effect etc. It indicates

about the noncurrent and non operating activities of the company. these items explain about

those figures and items which have incurred due to the industry and economical fluctuations

these items explains about the current changes in the assets of the company and thus it is not

recorded in the income statement of the company (Nobes, Parker and Parker, 2008).

Que 5:

The comprehensive income statement explains about those items which are not related

with the daily operations of Harvey Norman and neither has it indicated about the exact value

of the company. It only explains about fair value of foreign investment and other investment

of the company (Nielsen, Raimondos-Møller and Schjelderup, 2010). Thus it is not recorded

6

The changes into the total profit of the company explain that the total comprehensive

income of the company is $ 17,226,000 which has enhanced the total profitability level of the

company.

Randolph and Tice, (2014) explains that the comprehensive income statement is

prepared separately in the annual report of the company to measure the total profit of the

company. However, the items in the comprehensive income statement are not related with the

daily activities of the company.

Que 4:

The main items in the comprehensive income statement of the company is foreign

currency, cash flow hedges, available for sales investment, income tax effect etc. It indicates

about the noncurrent and non operating activities of the company. these items explain about

those figures and items which have incurred due to the industry and economical fluctuations

these items explains about the current changes in the assets of the company and thus it is not

recorded in the income statement of the company (Nobes, Parker and Parker, 2008).

Que 5:

The comprehensive income statement explains about those items which are not related

with the daily operations of Harvey Norman and neither has it indicated about the exact value

of the company. It only explains about fair value of foreign investment and other investment

of the company (Nielsen, Raimondos-Møller and Schjelderup, 2010). Thus it is not recorded

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

7

in the income statement of the company. As the income statement prepares on the basis of the

daily activities of the company and the comprehensive income statement of Harvey Norman

limited explains about the fair value of the assets and the liabilities of the company.

Que 6:

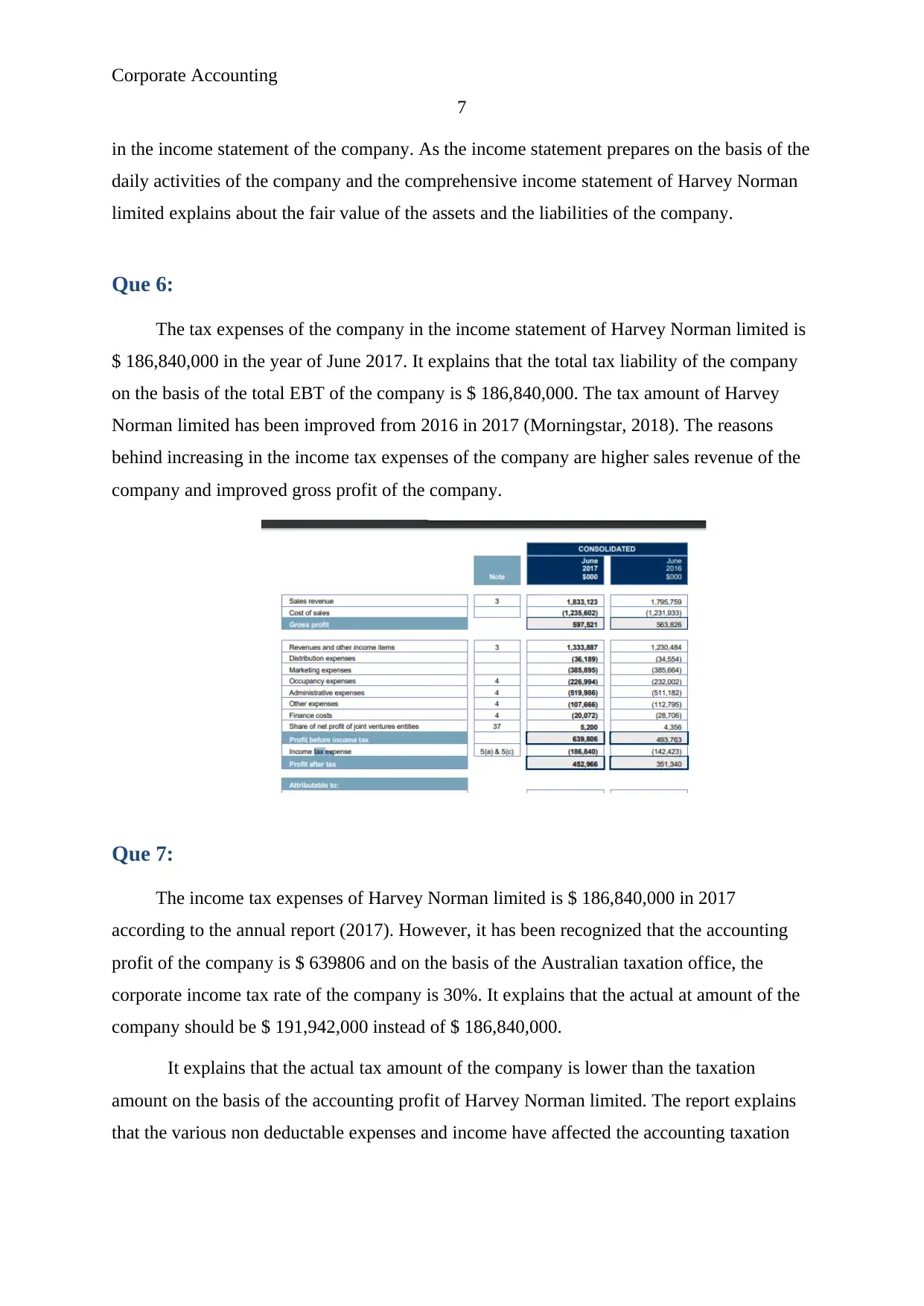

The tax expenses of the company in the income statement of Harvey Norman limited is

$ 186,840,000 in the year of June 2017. It explains that the total tax liability of the company

on the basis of the total EBT of the company is $ 186,840,000. The tax amount of Harvey

Norman limited has been improved from 2016 in 2017 (Morningstar, 2018). The reasons

behind increasing in the income tax expenses of the company are higher sales revenue of the

company and improved gross profit of the company.

Que 7:

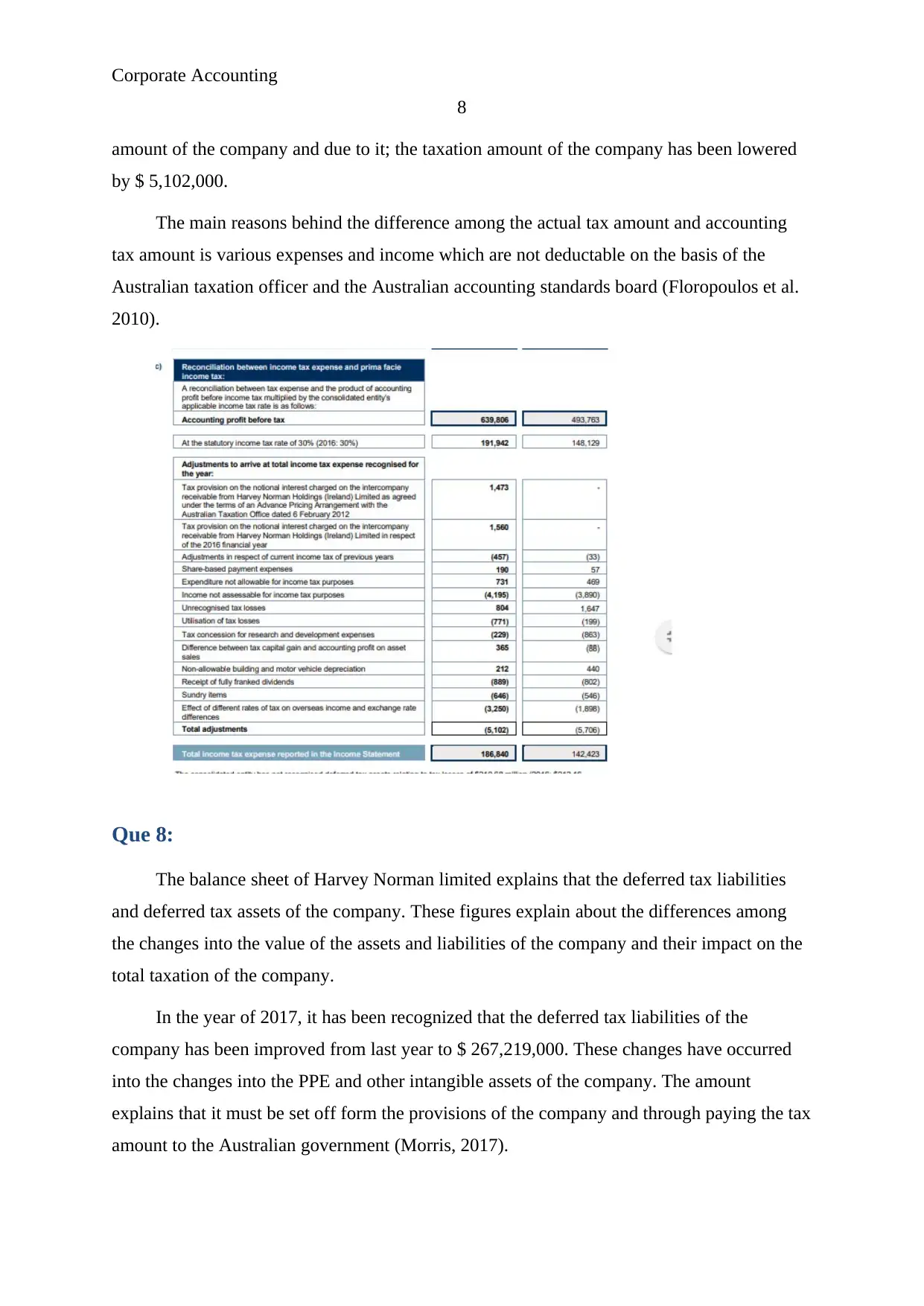

The income tax expenses of Harvey Norman limited is $ 186,840,000 in 2017

according to the annual report (2017). However, it has been recognized that the accounting

profit of the company is $ 639806 and on the basis of the Australian taxation office, the

corporate income tax rate of the company is 30%. It explains that the actual at amount of the

company should be $ 191,942,000 instead of $ 186,840,000.

It explains that the actual tax amount of the company is lower than the taxation

amount on the basis of the accounting profit of Harvey Norman limited. The report explains

that the various non deductable expenses and income have affected the accounting taxation

7

in the income statement of the company. As the income statement prepares on the basis of the

daily activities of the company and the comprehensive income statement of Harvey Norman

limited explains about the fair value of the assets and the liabilities of the company.

Que 6:

The tax expenses of the company in the income statement of Harvey Norman limited is

$ 186,840,000 in the year of June 2017. It explains that the total tax liability of the company

on the basis of the total EBT of the company is $ 186,840,000. The tax amount of Harvey

Norman limited has been improved from 2016 in 2017 (Morningstar, 2018). The reasons

behind increasing in the income tax expenses of the company are higher sales revenue of the

company and improved gross profit of the company.

Que 7:

The income tax expenses of Harvey Norman limited is $ 186,840,000 in 2017

according to the annual report (2017). However, it has been recognized that the accounting

profit of the company is $ 639806 and on the basis of the Australian taxation office, the

corporate income tax rate of the company is 30%. It explains that the actual at amount of the

company should be $ 191,942,000 instead of $ 186,840,000.

It explains that the actual tax amount of the company is lower than the taxation

amount on the basis of the accounting profit of Harvey Norman limited. The report explains

that the various non deductable expenses and income have affected the accounting taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

8

amount of the company and due to it; the taxation amount of the company has been lowered

by $ 5,102,000.

The main reasons behind the difference among the actual tax amount and accounting

tax amount is various expenses and income which are not deductable on the basis of the

Australian taxation officer and the Australian accounting standards board (Floropoulos et al.

2010).

Que 8:

The balance sheet of Harvey Norman limited explains that the deferred tax liabilities

and deferred tax assets of the company. These figures explain about the differences among

the changes into the value of the assets and liabilities of the company and their impact on the

total taxation of the company.

In the year of 2017, it has been recognized that the deferred tax liabilities of the

company has been improved from last year to $ 267,219,000. These changes have occurred

into the changes into the PPE and other intangible assets of the company. The amount

explains that it must be set off form the provisions of the company and through paying the tax

amount to the Australian government (Morris, 2017).

8

amount of the company and due to it; the taxation amount of the company has been lowered

by $ 5,102,000.

The main reasons behind the difference among the actual tax amount and accounting

tax amount is various expenses and income which are not deductable on the basis of the

Australian taxation officer and the Australian accounting standards board (Floropoulos et al.

2010).

Que 8:

The balance sheet of Harvey Norman limited explains that the deferred tax liabilities

and deferred tax assets of the company. These figures explain about the differences among

the changes into the value of the assets and liabilities of the company and their impact on the

total taxation of the company.

In the year of 2017, it has been recognized that the deferred tax liabilities of the

company has been improved from last year to $ 267,219,000. These changes have occurred

into the changes into the PPE and other intangible assets of the company. The amount

explains that it must be set off form the provisions of the company and through paying the tax

amount to the Australian government (Morris, 2017).

Corporate Accounting

9

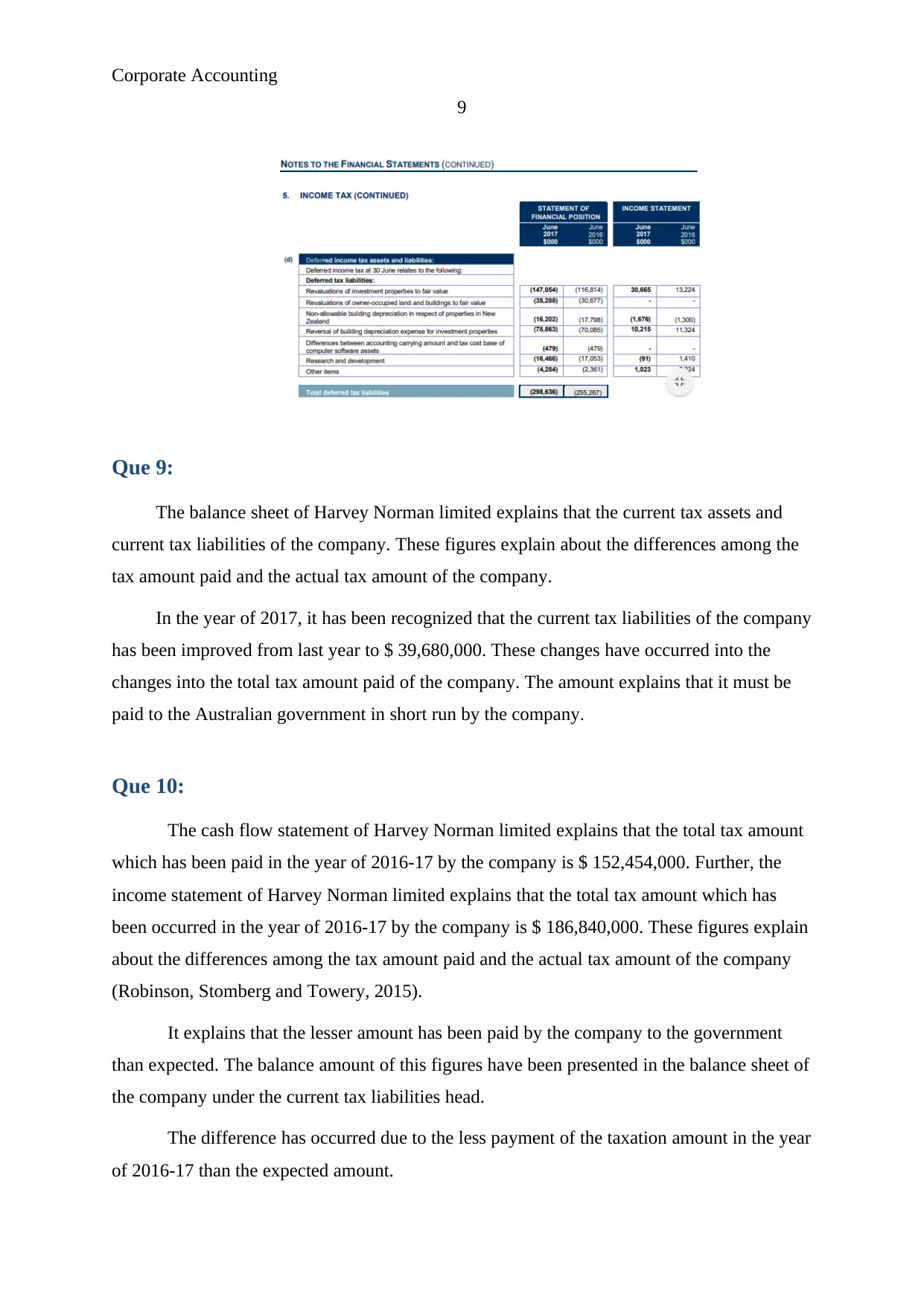

Que 9:

The balance sheet of Harvey Norman limited explains that the current tax assets and

current tax liabilities of the company. These figures explain about the differences among the

tax amount paid and the actual tax amount of the company.

In the year of 2017, it has been recognized that the current tax liabilities of the company

has been improved from last year to $ 39,680,000. These changes have occurred into the

changes into the total tax amount paid of the company. The amount explains that it must be

paid to the Australian government in short run by the company.

Que 10:

The cash flow statement of Harvey Norman limited explains that the total tax amount

which has been paid in the year of 2016-17 by the company is $ 152,454,000. Further, the

income statement of Harvey Norman limited explains that the total tax amount which has

been occurred in the year of 2016-17 by the company is $ 186,840,000. These figures explain

about the differences among the tax amount paid and the actual tax amount of the company

(Robinson, Stomberg and Towery, 2015).

It explains that the lesser amount has been paid by the company to the government

than expected. The balance amount of this figures have been presented in the balance sheet of

the company under the current tax liabilities head.

The difference has occurred due to the less payment of the taxation amount in the year

of 2016-17 than the expected amount.

9

Que 9:

The balance sheet of Harvey Norman limited explains that the current tax assets and

current tax liabilities of the company. These figures explain about the differences among the

tax amount paid and the actual tax amount of the company.

In the year of 2017, it has been recognized that the current tax liabilities of the company

has been improved from last year to $ 39,680,000. These changes have occurred into the

changes into the total tax amount paid of the company. The amount explains that it must be

paid to the Australian government in short run by the company.

Que 10:

The cash flow statement of Harvey Norman limited explains that the total tax amount

which has been paid in the year of 2016-17 by the company is $ 152,454,000. Further, the

income statement of Harvey Norman limited explains that the total tax amount which has

been occurred in the year of 2016-17 by the company is $ 186,840,000. These figures explain

about the differences among the tax amount paid and the actual tax amount of the company

(Robinson, Stomberg and Towery, 2015).

It explains that the lesser amount has been paid by the company to the government

than expected. The balance amount of this figures have been presented in the balance sheet of

the company under the current tax liabilities head.

The difference has occurred due to the less payment of the taxation amount in the year

of 2016-17 than the expected amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

10

Que 11:

The study on the Harvey Norman limited, its annual report and its tax amount in the

balance sheet, income statement and the cash flow statement explains that the study was quite

interesting as it is interested to read the annual report of a real company and measure that

how the items are recorded in the annual report of the company.

Though, few minor difficulties have also been faced while evaluating the accounting

process and the recording process of Harvey Norman limited. It has been found that the tax

amounts are required to be studied in depth to understand all the factors of the company.

Conclusion:

To conclude, Harvey Norman limited has recorded the entire accounting figures on the

basis of IFRS, AASB and IASB rules. The taxation figures have been added by the company

on the basis of AASB 112 rules. The performance of the company explains about the better

performance of the company.

10

Que 11:

The study on the Harvey Norman limited, its annual report and its tax amount in the

balance sheet, income statement and the cash flow statement explains that the study was quite

interesting as it is interested to read the annual report of a real company and measure that

how the items are recorded in the annual report of the company.

Though, few minor difficulties have also been faced while evaluating the accounting

process and the recording process of Harvey Norman limited. It has been found that the tax

amounts are required to be studied in depth to understand all the factors of the company.

Conclusion:

To conclude, Harvey Norman limited has recorded the entire accounting figures on the

basis of IFRS, AASB and IASB rules. The taxation figures have been added by the company

on the basis of AASB 112 rules. The performance of the company explains about the better

performance of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

11

References:

Annual report. 2017. Harvey Norman limited. [online]. Available at:

https://static1.squarespace.com/static/54803162e4b08e1b8a472201/t/

59cded6780bd5e4dbeef7f83/1506667916831/2017-Annual-Report.pdf (accessed 24/5/18).

Floropoulos, J., Spathis, C., Halvatzis, D. and Tsipouridou, M., 2010. Measuring the success

of the Greek taxation information system. International Journal of Information

Management, 30(1), pp.47-56.

Home. 2018. Harvey Norman limited. [online]. Available at:

http://www.harveynorman.com.au/ (accessed 24/5/18).

Horngren, C., Harrison, W., Oliver, S., Best, P., Fraser, D., Tan, R. and Willett, R.,

2012. Accounting. Pearson Higher Education AU.

Morningstar. 2018. Harvey Norman limited. [online]. Available at:

http://financials.morningstar.com/cash-flow/cf.html?t=HVN®ion=aus&culture=en-US

(accessed 24/5/18).

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplication. Journal of Accounting and

Finance, 17(8), pp.198-208.

Nielsen, S.B., Raimondos-Møller, P. and Schjelderup, G., 2010. Company taxation and tax

spillovers: Separate accounting versus formula apportionment. European Economic

Review, 54(1), pp.121-132.

Nobes, C., Parker, R.B. and Parker, R.H., 2008. Comparative international accounting.

Pearson Education.

Randolph, B. and Tice, A., 2014. Suburbanizing disadvantage in Australian cities:

sociospatial change in an era of neoliberalism. Journal of urban affairs, 36(s1), pp.384-399.

Robinson, L.A., Stomberg, B. and Towery, E.M., 2015. One size does not fit all: How the

uniform rules of FIN 48 affect the relevance of income tax accounting. The Accounting

Review, 91(4), pp.1195-1217.

11

References:

Annual report. 2017. Harvey Norman limited. [online]. Available at:

https://static1.squarespace.com/static/54803162e4b08e1b8a472201/t/

59cded6780bd5e4dbeef7f83/1506667916831/2017-Annual-Report.pdf (accessed 24/5/18).

Floropoulos, J., Spathis, C., Halvatzis, D. and Tsipouridou, M., 2010. Measuring the success

of the Greek taxation information system. International Journal of Information

Management, 30(1), pp.47-56.

Home. 2018. Harvey Norman limited. [online]. Available at:

http://www.harveynorman.com.au/ (accessed 24/5/18).

Horngren, C., Harrison, W., Oliver, S., Best, P., Fraser, D., Tan, R. and Willett, R.,

2012. Accounting. Pearson Higher Education AU.

Morningstar. 2018. Harvey Norman limited. [online]. Available at:

http://financials.morningstar.com/cash-flow/cf.html?t=HVN®ion=aus&culture=en-US

(accessed 24/5/18).

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplication. Journal of Accounting and

Finance, 17(8), pp.198-208.

Nielsen, S.B., Raimondos-Møller, P. and Schjelderup, G., 2010. Company taxation and tax

spillovers: Separate accounting versus formula apportionment. European Economic

Review, 54(1), pp.121-132.

Nobes, C., Parker, R.B. and Parker, R.H., 2008. Comparative international accounting.

Pearson Education.

Randolph, B. and Tice, A., 2014. Suburbanizing disadvantage in Australian cities:

sociospatial change in an era of neoliberalism. Journal of urban affairs, 36(s1), pp.384-399.

Robinson, L.A., Stomberg, B. and Towery, E.M., 2015. One size does not fit all: How the

uniform rules of FIN 48 affect the relevance of income tax accounting. The Accounting

Review, 91(4), pp.1195-1217.

Corporate Accounting

12

Walsh, P., McGregor‐Lowndes, M. and Newton, C.J., 2008. Shared services: Lessons from

the public and private sectors for the nonprofit sector. Australian Journal of Public

Administration, 67(2), pp.200-212.

Yahoo Finance. 2018. Harvey Norman limited. [online]. Available at:

https://au.finance.yahoo.com/quote/HVN.AX/ (accessed 24/5/18).

12

Walsh, P., McGregor‐Lowndes, M. and Newton, C.J., 2008. Shared services: Lessons from

the public and private sectors for the nonprofit sector. Australian Journal of Public

Administration, 67(2), pp.200-212.

Yahoo Finance. 2018. Harvey Norman limited. [online]. Available at:

https://au.finance.yahoo.com/quote/HVN.AX/ (accessed 24/5/18).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.