Financial Management Analysis of Harvey Norman's Performance

VerifiedAdded on 2020/06/06

|11

|2088

|117

Report

AI Summary

This report presents a comprehensive financial analysis of Harvey Norman, a prominent retail company specializing in furniture and electronics. It begins with an introduction outlining the scope, followed by an in-depth examination of debt valuation, including short-term and long-term debt, industry consistency, and the cost of debt. The analysis then transitions to share valuation, assessing the cost of equity using the CAPM model, comparing the company's performance with industry benchmarks, evaluating the PE ratio, and discussing the reasonableness of the valuation models. The report further delves into the cost of capital, calculating the weighted average cost of capital (WACC), explaining the company's tax rate, and discussing the inclusion of current liabilities. Market analysis compares the firm's performance to the industry and explores analyst perceptions. The conclusion summarizes the findings and highlights areas for improvement, such as restructuring debt and equity to mitigate business risks. The report utilizes tables, figures, and references to support its analysis, providing a detailed overview of Harvey Norman's financial position and market standing.

FINANCIAL MANAGEMENT

ANALYSIS

ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Debt valuation..................................................................................................................................1

(1)Short term and long term debt used by firms..........................................................................1

(2) Consistency of debt structure with industry...........................................................................1

(3) Impact of industry on proportion of long and short term loan of business firm....................1

(4) Harwey Norman cost of debt.................................................................................................1

Share valuation................................................................................................................................1

(1)What is your company cost of equity......................................................................................1

(2) Comparison of performance...................................................................................................2

(3) Company PE ratio evaluation................................................................................................3

(4) Reasonable values of model...................................................................................................4

(5) Additional data and information requirement for valuing company stock............................4

Cost of capital..................................................................................................................................4

(1)Calculation of weighted average cost of capital of company.................................................4

(2) Explaination of company tax rate..........................................................................................5

(3)Why is there any difference between cost of equity and debt................................................5

(4) Inclusion of current liability as cost of capital.......................................................................5

(5) WACC value and its application............................................................................................5

(6) Projects and use of WACC....................................................................................................5

(7)Defining and explaining capital structure...............................................................................6

(8)Optimal capital structure and factors that can imbalance it....................................................6

Market analysis................................................................................................................................6

(1)Comparison of firm performance to industry.........................................................................6

(2) Perception of analyst about Harvey Norman.........................................................................6

(3) Items different for company...................................................................................................6

CONCLUSION................................................................................................................................6

INTRODUCTION...........................................................................................................................1

Debt valuation..................................................................................................................................1

(1)Short term and long term debt used by firms..........................................................................1

(2) Consistency of debt structure with industry...........................................................................1

(3) Impact of industry on proportion of long and short term loan of business firm....................1

(4) Harwey Norman cost of debt.................................................................................................1

Share valuation................................................................................................................................1

(1)What is your company cost of equity......................................................................................1

(2) Comparison of performance...................................................................................................2

(3) Company PE ratio evaluation................................................................................................3

(4) Reasonable values of model...................................................................................................4

(5) Additional data and information requirement for valuing company stock............................4

Cost of capital..................................................................................................................................4

(1)Calculation of weighted average cost of capital of company.................................................4

(2) Explaination of company tax rate..........................................................................................5

(3)Why is there any difference between cost of equity and debt................................................5

(4) Inclusion of current liability as cost of capital.......................................................................5

(5) WACC value and its application............................................................................................5

(6) Projects and use of WACC....................................................................................................5

(7)Defining and explaining capital structure...............................................................................6

(8)Optimal capital structure and factors that can imbalance it....................................................6

Market analysis................................................................................................................................6

(1)Comparison of firm performance to industry.........................................................................6

(2) Perception of analyst about Harvey Norman.........................................................................6

(3) Items different for company...................................................................................................6

CONCLUSION................................................................................................................................6

Table of Index

Table 1Company PE ratio and valuation.........................................................................................3

Table 2Calculation of CAPM..........................................................................................................4

Table 3Enterprise value...................................................................................................................4

Table 4Debt and equity weight in capital structure as well as WACC...........................................4

Figure 1Sales revenue of Harwey Norman......................................................................................2

Figure 2EPS of Harwey Norman.....................................................................................................2

Figure 3Dividend chart of Harwey Norman....................................................................................3

Table 1Company PE ratio and valuation.........................................................................................3

Table 2Calculation of CAPM..........................................................................................................4

Table 3Enterprise value...................................................................................................................4

Table 4Debt and equity weight in capital structure as well as WACC...........................................4

Figure 1Sales revenue of Harwey Norman......................................................................................2

Figure 2EPS of Harwey Norman.....................................................................................................2

Figure 3Dividend chart of Harwey Norman....................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Harvey Normon is the one of famous retail company of furniture and electronic goods. In

current report capital structure of firm is analyzed and by using WACC(Weighted average cost

of capital). In middle section of report, detail analysis of company is done. At end of the report,

market analysis is done and firm image in market is measured.

Debt valuation

(1)Short term and long term debt used by firms

Short term debt used by the firm are trade and other payables and interest bearing loans

and borrowings. Whereas, in long term also interest bearing loans and borrowings are included.

It can be observed from annual report that in accounting year 2016 to 2017 trade and other

payables amount to 238628 and interest bearing loan is equal to 386651 (Harvey Normon

Holdings Limited, 2017). On other hand, in case of non current liability under interst bearing

loans and borrowing amount is 333858. Hence, both long and short term loans are used by the

firm.

(2) Consistency of debt structure with industry

Debt equity ratio of Harvey Norman is 0.11 which is much lower then industry capital

structure ratio which is 0.30. This reflects that there is not consistency of capital structure of firm

in comparison to industry. It can be said that firm is in better condition then industry and its

capital structure is balanced.

(3) Impact of industry on proportion of long and short term loan of business firm

Industry have impact on proportion of long and short term loan that is observed in the

firm’s balance sheet. Currently, in industry already there is tough competition and in order to

remain in it, it is necessary for the firm to expand its business at a rapid rate. For expansion fund

is required which is arranged by taking loan from banks. In order to meet day to day expenses

short term loan is required. Hence, it can be said that industry have impact on long and short

term loan of business firm.

1 | P a g e

Harvey Normon is the one of famous retail company of furniture and electronic goods. In

current report capital structure of firm is analyzed and by using WACC(Weighted average cost

of capital). In middle section of report, detail analysis of company is done. At end of the report,

market analysis is done and firm image in market is measured.

Debt valuation

(1)Short term and long term debt used by firms

Short term debt used by the firm are trade and other payables and interest bearing loans

and borrowings. Whereas, in long term also interest bearing loans and borrowings are included.

It can be observed from annual report that in accounting year 2016 to 2017 trade and other

payables amount to 238628 and interest bearing loan is equal to 386651 (Harvey Normon

Holdings Limited, 2017). On other hand, in case of non current liability under interst bearing

loans and borrowing amount is 333858. Hence, both long and short term loans are used by the

firm.

(2) Consistency of debt structure with industry

Debt equity ratio of Harvey Norman is 0.11 which is much lower then industry capital

structure ratio which is 0.30. This reflects that there is not consistency of capital structure of firm

in comparison to industry. It can be said that firm is in better condition then industry and its

capital structure is balanced.

(3) Impact of industry on proportion of long and short term loan of business firm

Industry have impact on proportion of long and short term loan that is observed in the

firm’s balance sheet. Currently, in industry already there is tough competition and in order to

remain in it, it is necessary for the firm to expand its business at a rapid rate. For expansion fund

is required which is arranged by taking loan from banks. In order to meet day to day expenses

short term loan is required. Hence, it can be said that industry have impact on long and short

term loan of business firm.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(4) Harwey Norman cost of debt

Cost of debt of the business firm is 20072 which is the amount of interest that is paid by

the business firm on its loan to banks. Cost of debt is usually considered as amount that is

computed by charging interest percentage of principle amount.

Share valuation

(1)What is your company cost of equity

Cost of equity is 11% as it is the rate of return that company need to give to its investors

for risk they are taking in business. Cost of equity is computed for the business firm by using

CAPM or capital asset pricing model.

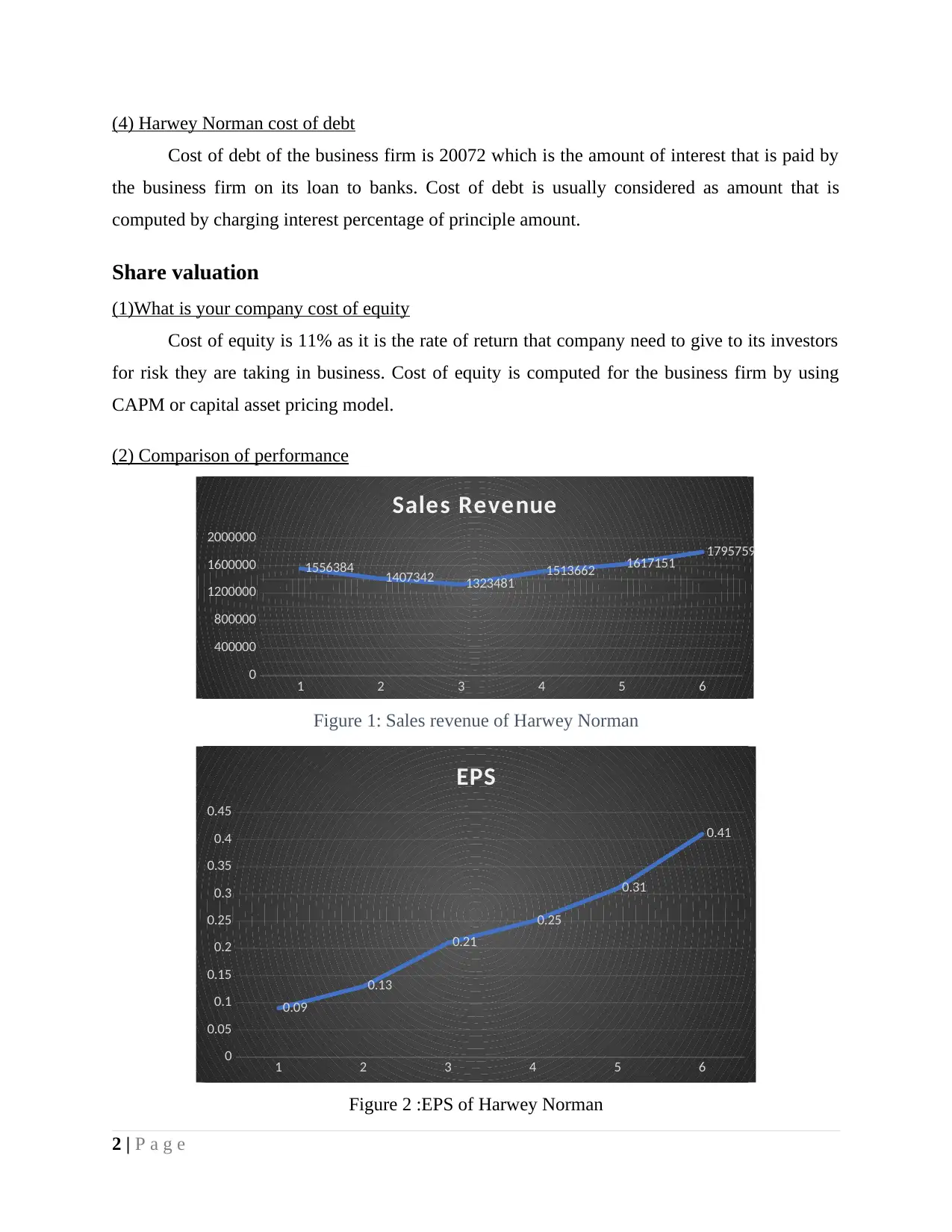

(2) Comparison of performance

1 2 3 4 5 6

0

400000

800000

1200000

1600000

2000000

1556384 1407342 1323481 1513662 1617151 1795759

Sales Revenue

Figure 1: Sales revenue of Harwey Norman

1 2 3 4 5 6

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.09

0.13

0.21

0.25

0.31

0.41

EPS

Figure 2 :EPS of Harwey Norman

2 | P a g e

Cost of debt of the business firm is 20072 which is the amount of interest that is paid by

the business firm on its loan to banks. Cost of debt is usually considered as amount that is

computed by charging interest percentage of principle amount.

Share valuation

(1)What is your company cost of equity

Cost of equity is 11% as it is the rate of return that company need to give to its investors

for risk they are taking in business. Cost of equity is computed for the business firm by using

CAPM or capital asset pricing model.

(2) Comparison of performance

1 2 3 4 5 6

0

400000

800000

1200000

1600000

2000000

1556384 1407342 1323481 1513662 1617151 1795759

Sales Revenue

Figure 1: Sales revenue of Harwey Norman

1 2 3 4 5 6

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.09

0.13

0.21

0.25

0.31

0.41

EPS

Figure 2 :EPS of Harwey Norman

2 | P a g e

1 2 3 4 5 6

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

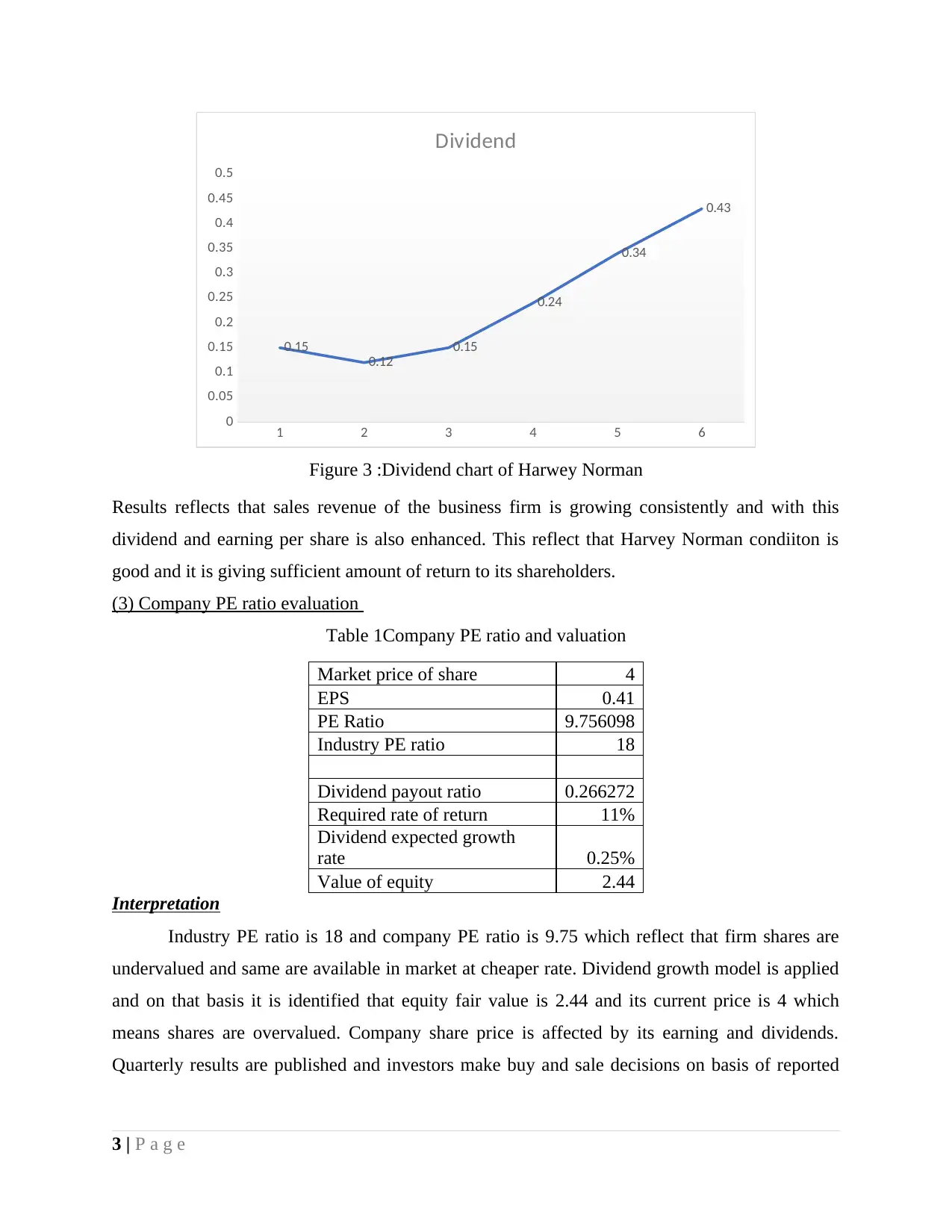

0.15

0.12

0.15

0.24

0.34

0.43

Dividend

Figure 3 :Dividend chart of Harwey Norman

Results reflects that sales revenue of the business firm is growing consistently and with this

dividend and earning per share is also enhanced. This reflect that Harvey Norman condiiton is

good and it is giving sufficient amount of return to its shareholders.

(3) Company PE ratio evaluation

Table 1Company PE ratio and valuation

Market price of share 4

EPS 0.41

PE Ratio 9.756098

Industry PE ratio 18

Dividend payout ratio 0.266272

Required rate of return 11%

Dividend expected growth

rate 0.25%

Value of equity 2.44

Interpretation

Industry PE ratio is 18 and company PE ratio is 9.75 which reflect that firm shares are

undervalued and same are available in market at cheaper rate. Dividend growth model is applied

and on that basis it is identified that equity fair value is 2.44 and its current price is 4 which

means shares are overvalued. Company share price is affected by its earning and dividends.

Quarterly results are published and investors make buy and sale decisions on basis of reported

3 | P a g e

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.15

0.12

0.15

0.24

0.34

0.43

Dividend

Figure 3 :Dividend chart of Harwey Norman

Results reflects that sales revenue of the business firm is growing consistently and with this

dividend and earning per share is also enhanced. This reflect that Harvey Norman condiiton is

good and it is giving sufficient amount of return to its shareholders.

(3) Company PE ratio evaluation

Table 1Company PE ratio and valuation

Market price of share 4

EPS 0.41

PE Ratio 9.756098

Industry PE ratio 18

Dividend payout ratio 0.266272

Required rate of return 11%

Dividend expected growth

rate 0.25%

Value of equity 2.44

Interpretation

Industry PE ratio is 18 and company PE ratio is 9.75 which reflect that firm shares are

undervalued and same are available in market at cheaper rate. Dividend growth model is applied

and on that basis it is identified that equity fair value is 2.44 and its current price is 4 which

means shares are overvalued. Company share price is affected by its earning and dividends.

Quarterly results are published and investors make buy and sale decisions on basis of reported

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

earnings not dividend. Hence, income is the factor that most affect share price and is covered by

PE ratio model.

(4) Reasonable values of model

On comparison of both model PE value seems reasonable a compared to market price of

stock as it reflect firm shares are undervalued (Bodie, 2013). Currently, firm is receving stiff

competition from its rivals and it is difficult for it maintain market share in business. From this,

point of view firm performance is below market and shares are undervalued as reflected by PE

ratio. Hence, PE ratio value seems more reasonable from this point of view in respect to market

price.

(5) Additional data and information requirement for valuing company stock

For valuation of company stock some of the information that are more required are cash

flows facts or values and cost of capital information. By using these facts stocks can be valued in

proper manner by using discounted cash flow model. Discounted cash flow model often used

along with PE ratio for valuation of company.

Cost of capital

(1)Calculation of weighted average cost of capital of company

Table 2Calculation of CAPM

CAPM Assumptions

K(e) 11.14%

RFR 5.0%

Beta 0.79

R(m) 13%

Table 3Enterprise value

Enterprise Value (EV)

Current Market Price 4

Diluted Shares 1,112

Market Capitalization 4,448

Long Term Liabilities 333,858

Less: Cash & Cash Equivalents 80,224

Enterprise Value (in lacks) 258,082

4 | P a g e

PE ratio model.

(4) Reasonable values of model

On comparison of both model PE value seems reasonable a compared to market price of

stock as it reflect firm shares are undervalued (Bodie, 2013). Currently, firm is receving stiff

competition from its rivals and it is difficult for it maintain market share in business. From this,

point of view firm performance is below market and shares are undervalued as reflected by PE

ratio. Hence, PE ratio value seems more reasonable from this point of view in respect to market

price.

(5) Additional data and information requirement for valuing company stock

For valuation of company stock some of the information that are more required are cash

flows facts or values and cost of capital information. By using these facts stocks can be valued in

proper manner by using discounted cash flow model. Discounted cash flow model often used

along with PE ratio for valuation of company.

Cost of capital

(1)Calculation of weighted average cost of capital of company

Table 2Calculation of CAPM

CAPM Assumptions

K(e) 11.14%

RFR 5.0%

Beta 0.79

R(m) 13%

Table 3Enterprise value

Enterprise Value (EV)

Current Market Price 4

Diluted Shares 1,112

Market Capitalization 4,448

Long Term Liabilities 333,858

Less: Cash & Cash Equivalents 80,224

Enterprise Value (in lacks) 258,082

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 4 Debt and equity weight in capital structure as well as WACC

Debt Equity

Weightage

E/(D+E) @

Enterprise Value 1.31%

D/(D+E) @

Enterprise Value 98.69%

Interest Rate

(%) 1%

Tax Rate (@) 30%

WACC Calculation

WACC

1%

(2) Explaination of company tax rate

Company’s tax rate is 30% and it is for long time. In 2016 government of Australia

proposed change in corporate tax rate to 25% from 30%. These amendements are on bill and will

be passed in senate as it is beneficial for firms.

(3)Why is there any difference between cost of equity and debt

There is significant difference between cost of equity and debt because usually rate of

interest is charged at less rate then dividend rate. Due to this reason cost of equity and debt can

never be same (Cumming and Walz, 2010). Proportion of debt and equity are also different in the

capital structure and due to this reason also cost of debt and equity can never remain same.

(4) Inclusion of current liability as cost of capital

Current liability must be included in cost of capital because it is also sort of liability and

many times big amount of current liability gets accumulated in business. Ignorance of current

liability specially when it is big in number can not help finance manager in computing accurate

amount cost of capital in business. Thus, advantage of inclusion of current liability in calculation

is that it give true and fair picture of overall cost of capital in business. Disadvantage is that if it

will be included even small amount of current liability is in business cost of capital will be

inflated.

5 | P a g e

Debt Equity

Weightage

E/(D+E) @

Enterprise Value 1.31%

D/(D+E) @

Enterprise Value 98.69%

Interest Rate

(%) 1%

Tax Rate (@) 30%

WACC Calculation

WACC

1%

(2) Explaination of company tax rate

Company’s tax rate is 30% and it is for long time. In 2016 government of Australia

proposed change in corporate tax rate to 25% from 30%. These amendements are on bill and will

be passed in senate as it is beneficial for firms.

(3)Why is there any difference between cost of equity and debt

There is significant difference between cost of equity and debt because usually rate of

interest is charged at less rate then dividend rate. Due to this reason cost of equity and debt can

never be same (Cumming and Walz, 2010). Proportion of debt and equity are also different in the

capital structure and due to this reason also cost of debt and equity can never remain same.

(4) Inclusion of current liability as cost of capital

Current liability must be included in cost of capital because it is also sort of liability and

many times big amount of current liability gets accumulated in business. Ignorance of current

liability specially when it is big in number can not help finance manager in computing accurate

amount cost of capital in business. Thus, advantage of inclusion of current liability in calculation

is that it give true and fair picture of overall cost of capital in business. Disadvantage is that if it

will be included even small amount of current liability is in business cost of capital will be

inflated.

5 | P a g e

(5) WACC value and its application

Results are reflecting that weighted average cost of capital is 1% which is very low for

the firm. It can also be seen that there is relatively very low proportion of debt in the firm capital

structure. It is used by investment banks for equity valuation.

(6) Projects and use of WACC

Currently firm is working on Westgate project as it has stores in Westgate are where

construction of residential properties is carried out. Millenia store is another project on which

firm is working. WACC is used to compute overall cost of capital and to discount cash flows of

these projects.

(7)Defining and explaining capital structure

Capital structure refers to mix of debt and equity in the capital structure. Company’s

capital structure is not consistent to industry and it is also not balanced as debt equity ratio is

0.11.

(8)Optimal capital structure and factors that can imbalance it

Optimal capital structure is one where at appropriate debt and equity mix cost of capital

is minimum. Change in economic condition of nation can imbalance it.

Market analysis

(1)Comparison of firm performance to industry

In comparison to industry firm is giving similar performance as competition increased in

industry. Hence, firm need to develop unique business strategy in order to solve problem.

(2) Perception of analyst about Harvey Norman

Analysts have perception that firm can give tough competition to Amazon in comparison

to other retailers as its sales is increasing consistently in the business. There are number of strong

points of the business firm and due to these reasons there is positive perception among analysts

about firm (Harvey Normon sales surge, 2017). I am fully agreed with comment because sales of

Harvey increased by 6% which is good and if this performance remain consistent it can give

tough competiton to rivals.

(3) Items different for company

6 | P a g e

Results are reflecting that weighted average cost of capital is 1% which is very low for

the firm. It can also be seen that there is relatively very low proportion of debt in the firm capital

structure. It is used by investment banks for equity valuation.

(6) Projects and use of WACC

Currently firm is working on Westgate project as it has stores in Westgate are where

construction of residential properties is carried out. Millenia store is another project on which

firm is working. WACC is used to compute overall cost of capital and to discount cash flows of

these projects.

(7)Defining and explaining capital structure

Capital structure refers to mix of debt and equity in the capital structure. Company’s

capital structure is not consistent to industry and it is also not balanced as debt equity ratio is

0.11.

(8)Optimal capital structure and factors that can imbalance it

Optimal capital structure is one where at appropriate debt and equity mix cost of capital

is minimum. Change in economic condition of nation can imbalance it.

Market analysis

(1)Comparison of firm performance to industry

In comparison to industry firm is giving similar performance as competition increased in

industry. Hence, firm need to develop unique business strategy in order to solve problem.

(2) Perception of analyst about Harvey Norman

Analysts have perception that firm can give tough competition to Amazon in comparison

to other retailers as its sales is increasing consistently in the business. There are number of strong

points of the business firm and due to these reasons there is positive perception among analysts

about firm (Harvey Normon sales surge, 2017). I am fully agreed with comment because sales of

Harvey increased by 6% which is good and if this performance remain consistent it can give

tough competiton to rivals.

(3) Items different for company

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Item that is different for company is its capital structure as it is totally imbalanced as debt

cover 90% of capital structure.

CONCLUSION

On the basis of above discussion it is concluded that Harvey Normon is in better

condition as its sales are increasing consistently and it is ahead of rivals. It need to restructure its

debt and equity so that risk in busines can be minimized.

7 | P a g e

cover 90% of capital structure.

CONCLUSION

On the basis of above discussion it is concluded that Harvey Normon is in better

condition as its sales are increasing consistently and it is ahead of rivals. It need to restructure its

debt and equity so that risk in busines can be minimized.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Bodie, Z., 2013. Investments. McGraw-Hill.

Cumming, D. and Walz, U., 2010. Private equity returns and disclosure around the

world. Journal of International Business Studies. 41(4). pp.727-754.

Online

Harvey Normon Holdings Limited. 2017. [Online]. Available through:<

file:///C:/Users/user/Desktop/01902066.pdf>. [Accessed on 14th Octomber 2017].

Harvey Normon sales surge. 2017. [Online]. Available through:<

http://www.theaustralian.com.au/business/companies/harvey-norman-sales-surge/news-

story/176234b0f243f7be6c9d30864b197169>. [Accessed on 14th Octomber 2017].

8 | P a g e

Books and Journals

Bodie, Z., 2013. Investments. McGraw-Hill.

Cumming, D. and Walz, U., 2010. Private equity returns and disclosure around the

world. Journal of International Business Studies. 41(4). pp.727-754.

Online

Harvey Normon Holdings Limited. 2017. [Online]. Available through:<

file:///C:/Users/user/Desktop/01902066.pdf>. [Accessed on 14th Octomber 2017].

Harvey Normon sales surge. 2017. [Online]. Available through:<

http://www.theaustralian.com.au/business/companies/harvey-norman-sales-surge/news-

story/176234b0f243f7be6c9d30864b197169>. [Accessed on 14th Octomber 2017].

8 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.