Comprehensive Financial Performance Report: Hays Plc (2017-2018)

VerifiedAdded on 2020/10/05

|13

|3215

|270

Report

AI Summary

This report presents a detailed financial analysis of Hays Plc for the years 2017 and 2018. It begins with an introduction to the company, its external auditors (Pricewaterhousecoopers LLP), and its business model, which centers on percentage fees from candidate placements. The analysis then delves into the company's financial performance, examining profitability, activity, liquidity, financial structure, and investment ratios. The report provides a comparative analysis of the financial statements, including profit and loss, balance sheet, and cash flow statements, highlighting key changes and trends. It also includes a segmental analysis of the company's operations across different geographic regions. The analysis reveals a mixed performance, with improvements in revenue, gross profit, and equity, but also declines in certain ratios such as return on capital employed. The report concludes with an assessment of Hays Plc's overall financial health and provides insights into potential areas for improvement. The report uses financial ratios such as gross profit ratio, return on capital employed, operating profit margin, asset turnover, trade receivables and payable turnover, current ratio and quick ratio to assess Hays' financial position.

CORPORATE REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1.1 Company name along with its external auditors....................................................................1

1.2 Business model......................................................................................................................1

ASSUMPTIONS..............................................................................................................................1

ANALYSIS AND INTERPRETATION ........................................................................................2

3.1 Stating overall performance...................................................................................................2

3.2 Profitability ratios..................................................................................................................4

3.3 Activity Ratio.........................................................................................................................5

3.4 Liquidity management...........................................................................................................5

3.5 Financial structure and gearing..............................................................................................6

3.6 Investment Ratios...................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

Ration Analysis............................................................................................................................9

INTRODUCTION...........................................................................................................................1

1.1 Company name along with its external auditors....................................................................1

1.2 Business model......................................................................................................................1

ASSUMPTIONS..............................................................................................................................1

ANALYSIS AND INTERPRETATION ........................................................................................2

3.1 Stating overall performance...................................................................................................2

3.2 Profitability ratios..................................................................................................................4

3.3 Activity Ratio.........................................................................................................................5

3.4 Liquidity management...........................................................................................................5

3.5 Financial structure and gearing..............................................................................................6

3.6 Investment Ratios...................................................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

Ration Analysis............................................................................................................................9

INTRODUCTION

1.1 Company name along with its external auditors

The main objective of this report is to give information about various shareholder which

might be interested to invest in Hays Plc. This report would be providing appropriate analysis of

financial statements of Hays Plc for year 2017 and 2018 which is audited by

Pricewaterhousecoopers LLP.

In the similar aspect, it would be observing percentage change from year 2017 to 2018

along with proper ratio analysis such as profitability, liquidity, solvency, investment and

efficiency. Furthermore, it would be using various financial statements for analysing its financial

performance and position of Hays Plc of these two consecutive years. Simultaneously, there will

be discussion of improvements which must be formed for enhancing other opportunities of

investment.

1.2 Business model

The revenue model is very simple in this organization as they gain percentage fee on

contingent aspect if any candidate is placed in particular role with specific client. In the similar

aspect, its delivery model is with reference to deep industry expertise among contract, permanent

and temporary recruitment markets. The most important thing is that there consultants are long

termed, trusted to both candidates and clients as well. They have equipped various technology,

data analytics and tools in this industry as there focus is on net fees instead of turnover which is

simply contributed from temp salary. Their capability for converting its net fees into operating

profit is considered as key profit metric. The highest conversion rate is at 22% in this industry.

There main belief is to have balanced exposure in their markets which is referred as key

for driving superior and resilient financial performance along with better outcome for their

clients via economic cycle. During this exposure, there recruitment market would be having deep

scale and expertise in 20 specialist areas on basis of skilled employment. Its market capitalisation

is as 2.241 Billion (Hays plc (HAS.l), 2018).

ASSUMPTIONS

In this report, it has shown % increase or decrease in specific financial variables of two

year 2017 and 2018 for articulating worse or better position of its performance. Further, the

performance would be measured through various financial ratios such as activity, profitability,

1

1.1 Company name along with its external auditors

The main objective of this report is to give information about various shareholder which

might be interested to invest in Hays Plc. This report would be providing appropriate analysis of

financial statements of Hays Plc for year 2017 and 2018 which is audited by

Pricewaterhousecoopers LLP.

In the similar aspect, it would be observing percentage change from year 2017 to 2018

along with proper ratio analysis such as profitability, liquidity, solvency, investment and

efficiency. Furthermore, it would be using various financial statements for analysing its financial

performance and position of Hays Plc of these two consecutive years. Simultaneously, there will

be discussion of improvements which must be formed for enhancing other opportunities of

investment.

1.2 Business model

The revenue model is very simple in this organization as they gain percentage fee on

contingent aspect if any candidate is placed in particular role with specific client. In the similar

aspect, its delivery model is with reference to deep industry expertise among contract, permanent

and temporary recruitment markets. The most important thing is that there consultants are long

termed, trusted to both candidates and clients as well. They have equipped various technology,

data analytics and tools in this industry as there focus is on net fees instead of turnover which is

simply contributed from temp salary. Their capability for converting its net fees into operating

profit is considered as key profit metric. The highest conversion rate is at 22% in this industry.

There main belief is to have balanced exposure in their markets which is referred as key

for driving superior and resilient financial performance along with better outcome for their

clients via economic cycle. During this exposure, there recruitment market would be having deep

scale and expertise in 20 specialist areas on basis of skilled employment. Its market capitalisation

is as 2.241 Billion (Hays plc (HAS.l), 2018).

ASSUMPTIONS

In this report, it has shown % increase or decrease in specific financial variables of two

year 2017 and 2018 for articulating worse or better position of its performance. Further, the

performance would be measured through various financial ratios such as activity, profitability,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

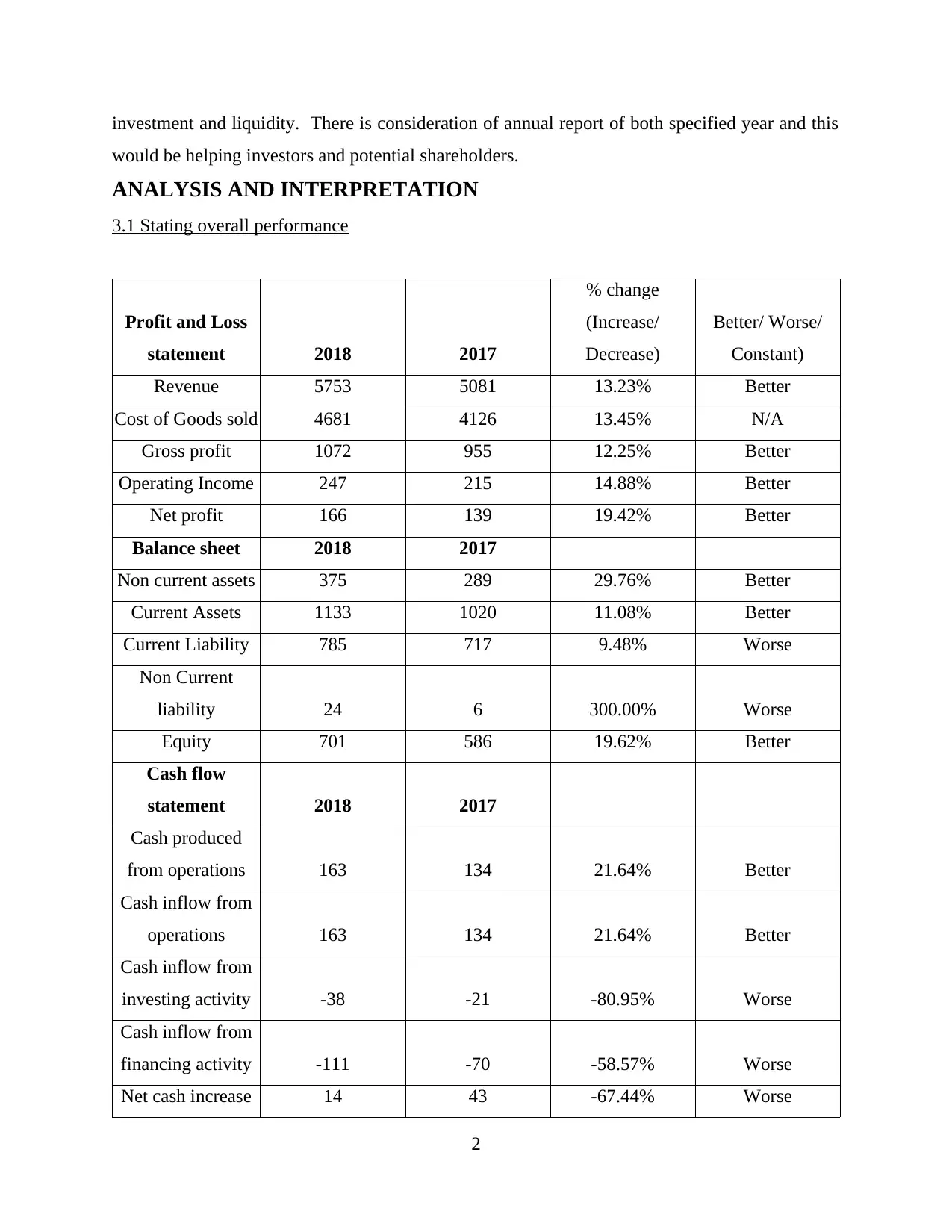

investment and liquidity. There is consideration of annual report of both specified year and this

would be helping investors and potential shareholders.

ANALYSIS AND INTERPRETATION

3.1 Stating overall performance

Profit and Loss

statement 2018 2017

% change

(Increase/

Decrease)

Better/ Worse/

Constant)

Revenue 5753 5081 13.23% Better

Cost of Goods sold 4681 4126 13.45% N/A

Gross profit 1072 955 12.25% Better

Operating Income 247 215 14.88% Better

Net profit 166 139 19.42% Better

Balance sheet 2018 2017

Non current assets 375 289 29.76% Better

Current Assets 1133 1020 11.08% Better

Current Liability 785 717 9.48% Worse

Non Current

liability 24 6 300.00% Worse

Equity 701 586 19.62% Better

Cash flow

statement 2018 2017

Cash produced

from operations 163 134 21.64% Better

Cash inflow from

operations 163 134 21.64% Better

Cash inflow from

investing activity -38 -21 -80.95% Worse

Cash inflow from

financing activity -111 -70 -58.57% Worse

Net cash increase 14 43 -67.44% Worse

2

would be helping investors and potential shareholders.

ANALYSIS AND INTERPRETATION

3.1 Stating overall performance

Profit and Loss

statement 2018 2017

% change

(Increase/

Decrease)

Better/ Worse/

Constant)

Revenue 5753 5081 13.23% Better

Cost of Goods sold 4681 4126 13.45% N/A

Gross profit 1072 955 12.25% Better

Operating Income 247 215 14.88% Better

Net profit 166 139 19.42% Better

Balance sheet 2018 2017

Non current assets 375 289 29.76% Better

Current Assets 1133 1020 11.08% Better

Current Liability 785 717 9.48% Worse

Non Current

liability 24 6 300.00% Worse

Equity 701 586 19.62% Better

Cash flow

statement 2018 2017

Cash produced

from operations 163 134 21.64% Better

Cash inflow from

operations 163 134 21.64% Better

Cash inflow from

investing activity -38 -21 -80.95% Worse

Cash inflow from

financing activity -111 -70 -58.57% Worse

Net cash increase 14 43 -67.44% Worse

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

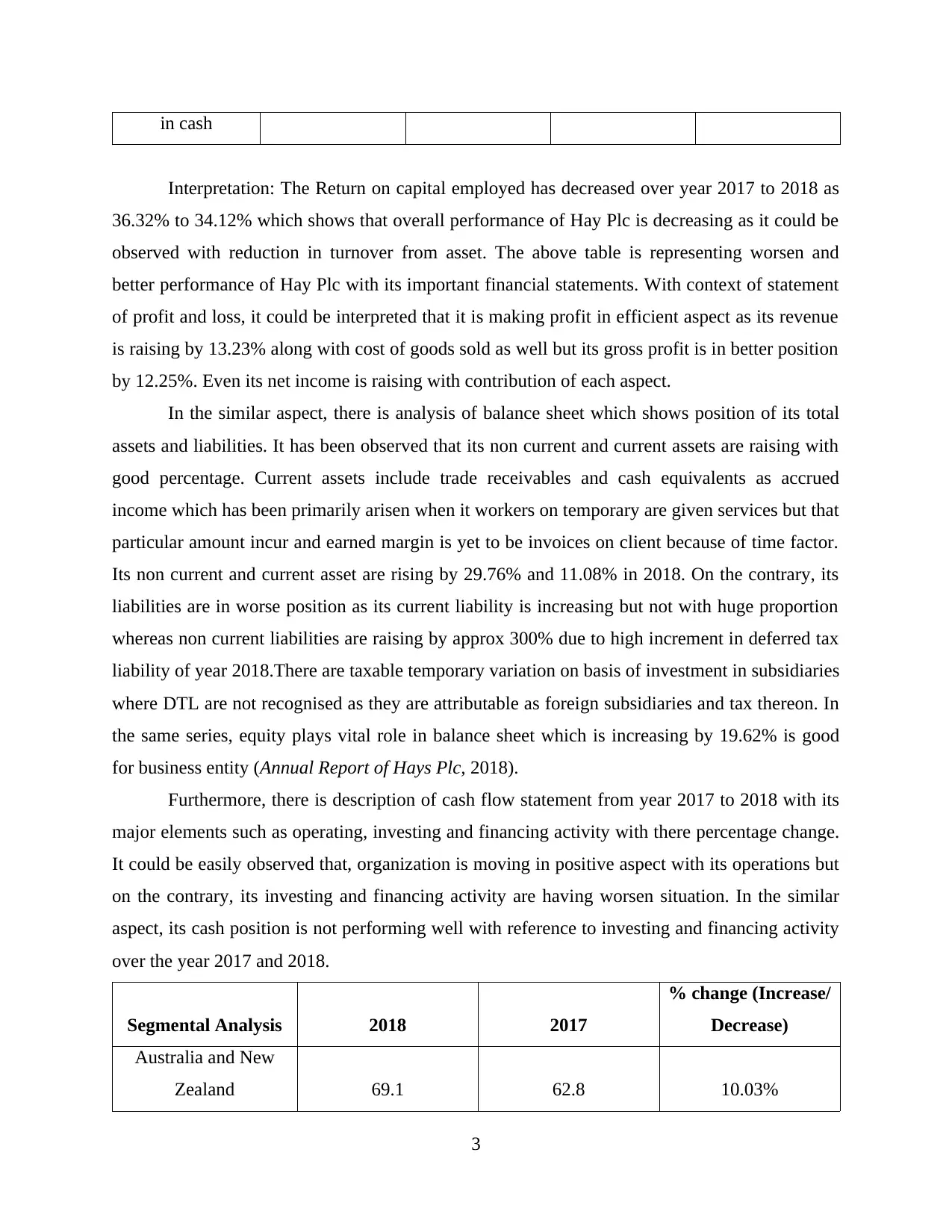

in cash

Interpretation: The Return on capital employed has decreased over year 2017 to 2018 as

36.32% to 34.12% which shows that overall performance of Hay Plc is decreasing as it could be

observed with reduction in turnover from asset. The above table is representing worsen and

better performance of Hay Plc with its important financial statements. With context of statement

of profit and loss, it could be interpreted that it is making profit in efficient aspect as its revenue

is raising by 13.23% along with cost of goods sold as well but its gross profit is in better position

by 12.25%. Even its net income is raising with contribution of each aspect.

In the similar aspect, there is analysis of balance sheet which shows position of its total

assets and liabilities. It has been observed that its non current and current assets are raising with

good percentage. Current assets include trade receivables and cash equivalents as accrued

income which has been primarily arisen when it workers on temporary are given services but that

particular amount incur and earned margin is yet to be invoices on client because of time factor.

Its non current and current asset are rising by 29.76% and 11.08% in 2018. On the contrary, its

liabilities are in worse position as its current liability is increasing but not with huge proportion

whereas non current liabilities are raising by approx 300% due to high increment in deferred tax

liability of year 2018.There are taxable temporary variation on basis of investment in subsidiaries

where DTL are not recognised as they are attributable as foreign subsidiaries and tax thereon. In

the same series, equity plays vital role in balance sheet which is increasing by 19.62% is good

for business entity (Annual Report of Hays Plc, 2018).

Furthermore, there is description of cash flow statement from year 2017 to 2018 with its

major elements such as operating, investing and financing activity with there percentage change.

It could be easily observed that, organization is moving in positive aspect with its operations but

on the contrary, its investing and financing activity are having worsen situation. In the similar

aspect, its cash position is not performing well with reference to investing and financing activity

over the year 2017 and 2018.

Segmental Analysis 2018 2017

% change (Increase/

Decrease)

Australia and New

Zealand 69.1 62.8 10.03%

3

Interpretation: The Return on capital employed has decreased over year 2017 to 2018 as

36.32% to 34.12% which shows that overall performance of Hay Plc is decreasing as it could be

observed with reduction in turnover from asset. The above table is representing worsen and

better performance of Hay Plc with its important financial statements. With context of statement

of profit and loss, it could be interpreted that it is making profit in efficient aspect as its revenue

is raising by 13.23% along with cost of goods sold as well but its gross profit is in better position

by 12.25%. Even its net income is raising with contribution of each aspect.

In the similar aspect, there is analysis of balance sheet which shows position of its total

assets and liabilities. It has been observed that its non current and current assets are raising with

good percentage. Current assets include trade receivables and cash equivalents as accrued

income which has been primarily arisen when it workers on temporary are given services but that

particular amount incur and earned margin is yet to be invoices on client because of time factor.

Its non current and current asset are rising by 29.76% and 11.08% in 2018. On the contrary, its

liabilities are in worse position as its current liability is increasing but not with huge proportion

whereas non current liabilities are raising by approx 300% due to high increment in deferred tax

liability of year 2018.There are taxable temporary variation on basis of investment in subsidiaries

where DTL are not recognised as they are attributable as foreign subsidiaries and tax thereon. In

the same series, equity plays vital role in balance sheet which is increasing by 19.62% is good

for business entity (Annual Report of Hays Plc, 2018).

Furthermore, there is description of cash flow statement from year 2017 to 2018 with its

major elements such as operating, investing and financing activity with there percentage change.

It could be easily observed that, organization is moving in positive aspect with its operations but

on the contrary, its investing and financing activity are having worsen situation. In the similar

aspect, its cash position is not performing well with reference to investing and financing activity

over the year 2017 and 2018.

Segmental Analysis 2018 2017

% change (Increase/

Decrease)

Australia and New

Zealand 69.1 62.8 10.03%

3

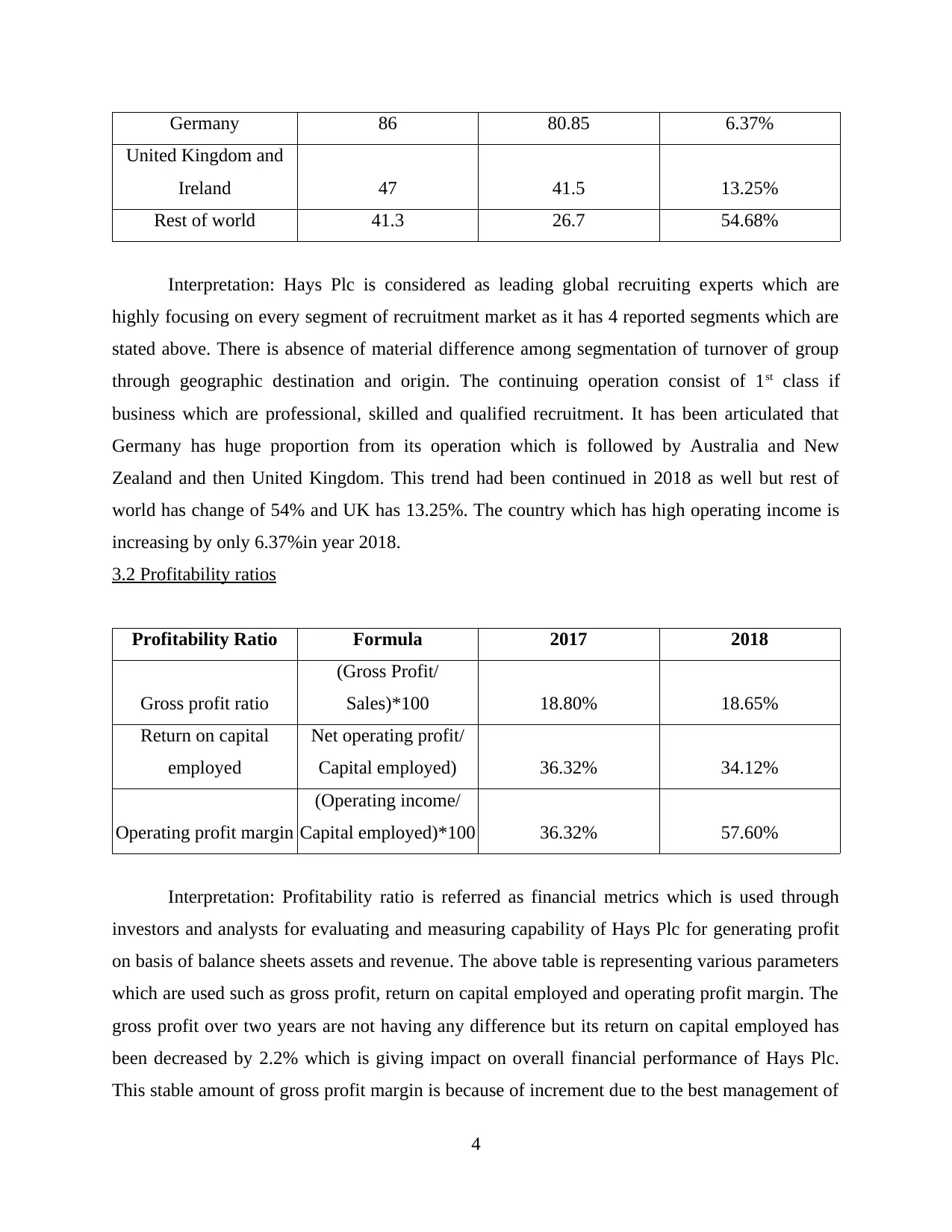

Germany 86 80.85 6.37%

United Kingdom and

Ireland 47 41.5 13.25%

Rest of world 41.3 26.7 54.68%

Interpretation: Hays Plc is considered as leading global recruiting experts which are

highly focusing on every segment of recruitment market as it has 4 reported segments which are

stated above. There is absence of material difference among segmentation of turnover of group

through geographic destination and origin. The continuing operation consist of 1st class if

business which are professional, skilled and qualified recruitment. It has been articulated that

Germany has huge proportion from its operation which is followed by Australia and New

Zealand and then United Kingdom. This trend had been continued in 2018 as well but rest of

world has change of 54% and UK has 13.25%. The country which has high operating income is

increasing by only 6.37%in year 2018.

3.2 Profitability ratios

Profitability Ratio Formula 2017 2018

Gross profit ratio

(Gross Profit/

Sales)*100 18.80% 18.65%

Return on capital

employed

Net operating profit/

Capital employed) 36.32% 34.12%

Operating profit margin

(Operating income/

Capital employed)*100 36.32% 57.60%

Interpretation: Profitability ratio is referred as financial metrics which is used through

investors and analysts for evaluating and measuring capability of Hays Plc for generating profit

on basis of balance sheets assets and revenue. The above table is representing various parameters

which are used such as gross profit, return on capital employed and operating profit margin. The

gross profit over two years are not having any difference but its return on capital employed has

been decreased by 2.2% which is giving impact on overall financial performance of Hays Plc.

This stable amount of gross profit margin is because of increment due to the best management of

4

United Kingdom and

Ireland 47 41.5 13.25%

Rest of world 41.3 26.7 54.68%

Interpretation: Hays Plc is considered as leading global recruiting experts which are

highly focusing on every segment of recruitment market as it has 4 reported segments which are

stated above. There is absence of material difference among segmentation of turnover of group

through geographic destination and origin. The continuing operation consist of 1st class if

business which are professional, skilled and qualified recruitment. It has been articulated that

Germany has huge proportion from its operation which is followed by Australia and New

Zealand and then United Kingdom. This trend had been continued in 2018 as well but rest of

world has change of 54% and UK has 13.25%. The country which has high operating income is

increasing by only 6.37%in year 2018.

3.2 Profitability ratios

Profitability Ratio Formula 2017 2018

Gross profit ratio

(Gross Profit/

Sales)*100 18.80% 18.65%

Return on capital

employed

Net operating profit/

Capital employed) 36.32% 34.12%

Operating profit margin

(Operating income/

Capital employed)*100 36.32% 57.60%

Interpretation: Profitability ratio is referred as financial metrics which is used through

investors and analysts for evaluating and measuring capability of Hays Plc for generating profit

on basis of balance sheets assets and revenue. The above table is representing various parameters

which are used such as gross profit, return on capital employed and operating profit margin. The

gross profit over two years are not having any difference but its return on capital employed has

been decreased by 2.2% which is giving impact on overall financial performance of Hays Plc.

This stable amount of gross profit margin is because of increment due to the best management of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

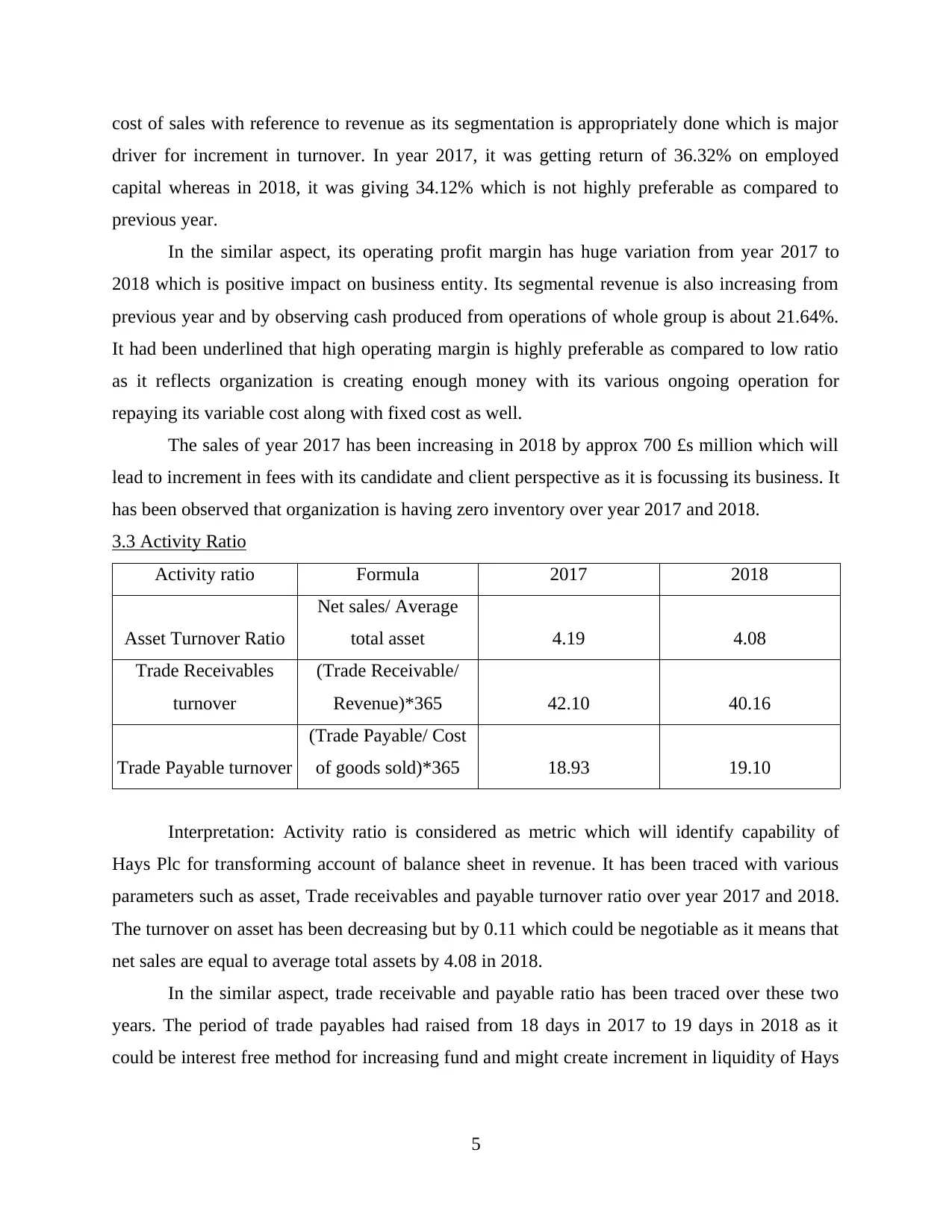

cost of sales with reference to revenue as its segmentation is appropriately done which is major

driver for increment in turnover. In year 2017, it was getting return of 36.32% on employed

capital whereas in 2018, it was giving 34.12% which is not highly preferable as compared to

previous year.

In the similar aspect, its operating profit margin has huge variation from year 2017 to

2018 which is positive impact on business entity. Its segmental revenue is also increasing from

previous year and by observing cash produced from operations of whole group is about 21.64%.

It had been underlined that high operating margin is highly preferable as compared to low ratio

as it reflects organization is creating enough money with its various ongoing operation for

repaying its variable cost along with fixed cost as well.

The sales of year 2017 has been increasing in 2018 by approx 700 £s million which will

lead to increment in fees with its candidate and client perspective as it is focussing its business. It

has been observed that organization is having zero inventory over year 2017 and 2018.

3.3 Activity Ratio

Activity ratio Formula 2017 2018

Asset Turnover Ratio

Net sales/ Average

total asset 4.19 4.08

Trade Receivables

turnover

(Trade Receivable/

Revenue)*365 42.10 40.16

Trade Payable turnover

(Trade Payable/ Cost

of goods sold)*365 18.93 19.10

Interpretation: Activity ratio is considered as metric which will identify capability of

Hays Plc for transforming account of balance sheet in revenue. It has been traced with various

parameters such as asset, Trade receivables and payable turnover ratio over year 2017 and 2018.

The turnover on asset has been decreasing but by 0.11 which could be negotiable as it means that

net sales are equal to average total assets by 4.08 in 2018.

In the similar aspect, trade receivable and payable ratio has been traced over these two

years. The period of trade payables had raised from 18 days in 2017 to 19 days in 2018 as it

could be interest free method for increasing fund and might create increment in liquidity of Hays

5

driver for increment in turnover. In year 2017, it was getting return of 36.32% on employed

capital whereas in 2018, it was giving 34.12% which is not highly preferable as compared to

previous year.

In the similar aspect, its operating profit margin has huge variation from year 2017 to

2018 which is positive impact on business entity. Its segmental revenue is also increasing from

previous year and by observing cash produced from operations of whole group is about 21.64%.

It had been underlined that high operating margin is highly preferable as compared to low ratio

as it reflects organization is creating enough money with its various ongoing operation for

repaying its variable cost along with fixed cost as well.

The sales of year 2017 has been increasing in 2018 by approx 700 £s million which will

lead to increment in fees with its candidate and client perspective as it is focussing its business. It

has been observed that organization is having zero inventory over year 2017 and 2018.

3.3 Activity Ratio

Activity ratio Formula 2017 2018

Asset Turnover Ratio

Net sales/ Average

total asset 4.19 4.08

Trade Receivables

turnover

(Trade Receivable/

Revenue)*365 42.10 40.16

Trade Payable turnover

(Trade Payable/ Cost

of goods sold)*365 18.93 19.10

Interpretation: Activity ratio is considered as metric which will identify capability of

Hays Plc for transforming account of balance sheet in revenue. It has been traced with various

parameters such as asset, Trade receivables and payable turnover ratio over year 2017 and 2018.

The turnover on asset has been decreasing but by 0.11 which could be negotiable as it means that

net sales are equal to average total assets by 4.08 in 2018.

In the similar aspect, trade receivable and payable ratio has been traced over these two

years. The period of trade payables had raised from 18 days in 2017 to 19 days in 2018 as it

could be interest free method for increasing fund and might create increment in liquidity of Hays

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

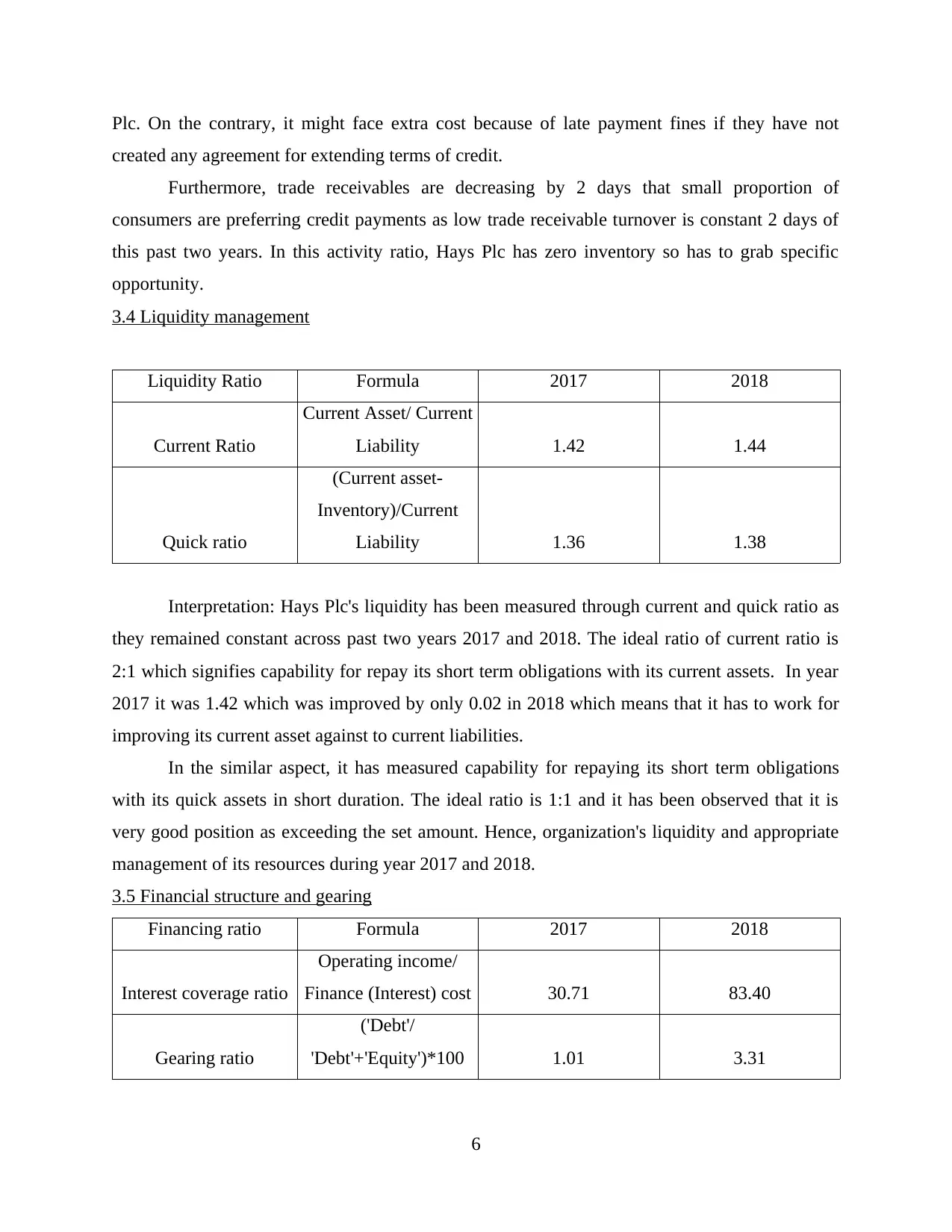

Plc. On the contrary, it might face extra cost because of late payment fines if they have not

created any agreement for extending terms of credit.

Furthermore, trade receivables are decreasing by 2 days that small proportion of

consumers are preferring credit payments as low trade receivable turnover is constant 2 days of

this past two years. In this activity ratio, Hays Plc has zero inventory so has to grab specific

opportunity.

3.4 Liquidity management

Liquidity Ratio Formula 2017 2018

Current Ratio

Current Asset/ Current

Liability 1.42 1.44

Quick ratio

(Current asset-

Inventory)/Current

Liability 1.36 1.38

Interpretation: Hays Plc's liquidity has been measured through current and quick ratio as

they remained constant across past two years 2017 and 2018. The ideal ratio of current ratio is

2:1 which signifies capability for repay its short term obligations with its current assets. In year

2017 it was 1.42 which was improved by only 0.02 in 2018 which means that it has to work for

improving its current asset against to current liabilities.

In the similar aspect, it has measured capability for repaying its short term obligations

with its quick assets in short duration. The ideal ratio is 1:1 and it has been observed that it is

very good position as exceeding the set amount. Hence, organization's liquidity and appropriate

management of its resources during year 2017 and 2018.

3.5 Financial structure and gearing

Financing ratio Formula 2017 2018

Interest coverage ratio

Operating income/

Finance (Interest) cost 30.71 83.40

Gearing ratio

('Debt'/

'Debt'+'Equity')*100 1.01 3.31

6

created any agreement for extending terms of credit.

Furthermore, trade receivables are decreasing by 2 days that small proportion of

consumers are preferring credit payments as low trade receivable turnover is constant 2 days of

this past two years. In this activity ratio, Hays Plc has zero inventory so has to grab specific

opportunity.

3.4 Liquidity management

Liquidity Ratio Formula 2017 2018

Current Ratio

Current Asset/ Current

Liability 1.42 1.44

Quick ratio

(Current asset-

Inventory)/Current

Liability 1.36 1.38

Interpretation: Hays Plc's liquidity has been measured through current and quick ratio as

they remained constant across past two years 2017 and 2018. The ideal ratio of current ratio is

2:1 which signifies capability for repay its short term obligations with its current assets. In year

2017 it was 1.42 which was improved by only 0.02 in 2018 which means that it has to work for

improving its current asset against to current liabilities.

In the similar aspect, it has measured capability for repaying its short term obligations

with its quick assets in short duration. The ideal ratio is 1:1 and it has been observed that it is

very good position as exceeding the set amount. Hence, organization's liquidity and appropriate

management of its resources during year 2017 and 2018.

3.5 Financial structure and gearing

Financing ratio Formula 2017 2018

Interest coverage ratio

Operating income/

Finance (Interest) cost 30.71 83.40

Gearing ratio

('Debt'/

'Debt'+'Equity')*100 1.01 3.31

6

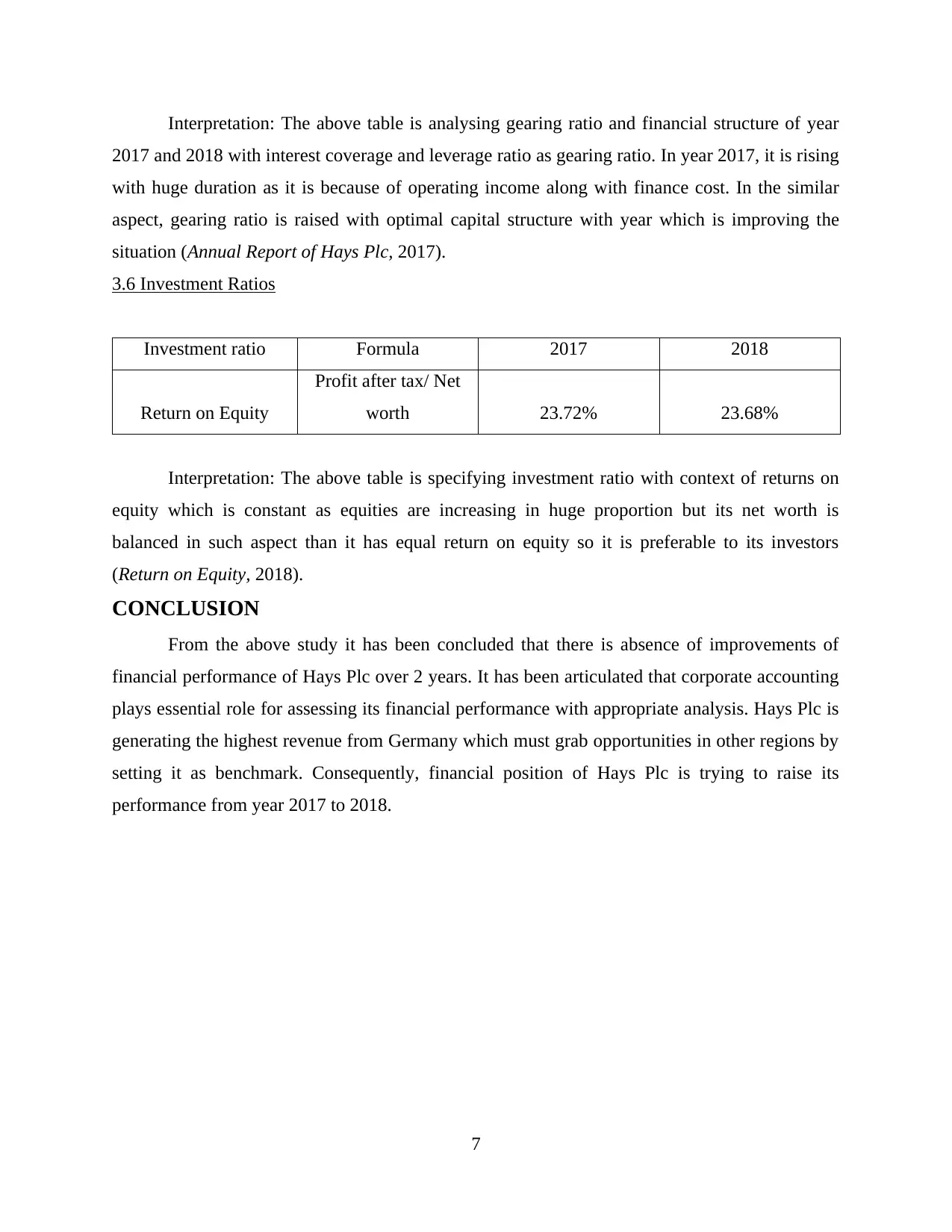

Interpretation: The above table is analysing gearing ratio and financial structure of year

2017 and 2018 with interest coverage and leverage ratio as gearing ratio. In year 2017, it is rising

with huge duration as it is because of operating income along with finance cost. In the similar

aspect, gearing ratio is raised with optimal capital structure with year which is improving the

situation (Annual Report of Hays Plc, 2017).

3.6 Investment Ratios

Investment ratio Formula 2017 2018

Return on Equity

Profit after tax/ Net

worth 23.72% 23.68%

Interpretation: The above table is specifying investment ratio with context of returns on

equity which is constant as equities are increasing in huge proportion but its net worth is

balanced in such aspect than it has equal return on equity so it is preferable to its investors

(Return on Equity, 2018).

CONCLUSION

From the above study it has been concluded that there is absence of improvements of

financial performance of Hays Plc over 2 years. It has been articulated that corporate accounting

plays essential role for assessing its financial performance with appropriate analysis. Hays Plc is

generating the highest revenue from Germany which must grab opportunities in other regions by

setting it as benchmark. Consequently, financial position of Hays Plc is trying to raise its

performance from year 2017 to 2018.

7

2017 and 2018 with interest coverage and leverage ratio as gearing ratio. In year 2017, it is rising

with huge duration as it is because of operating income along with finance cost. In the similar

aspect, gearing ratio is raised with optimal capital structure with year which is improving the

situation (Annual Report of Hays Plc, 2017).

3.6 Investment Ratios

Investment ratio Formula 2017 2018

Return on Equity

Profit after tax/ Net

worth 23.72% 23.68%

Interpretation: The above table is specifying investment ratio with context of returns on

equity which is constant as equities are increasing in huge proportion but its net worth is

balanced in such aspect than it has equal return on equity so it is preferable to its investors

(Return on Equity, 2018).

CONCLUSION

From the above study it has been concluded that there is absence of improvements of

financial performance of Hays Plc over 2 years. It has been articulated that corporate accounting

plays essential role for assessing its financial performance with appropriate analysis. Hays Plc is

generating the highest revenue from Germany which must grab opportunities in other regions by

setting it as benchmark. Consequently, financial position of Hays Plc is trying to raise its

performance from year 2017 to 2018.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

ONLINE

Annual Report of Hays Plc. 2017. [Online]. Available through

<https://www.haysplc.com/investors/annual-report-2017>.

Annual Report of Hays Plc. 2018. [Online]. Available through

<https://www.haysplc.com/~/media/Files/H/Hays/annual-reports/ar-2018/ar-2018.pdf>.

Hays plc (HAS.l). 2018. [Online]. Available through <https://finance.yahoo.com/quote/HAS.L/>.

Hays PLC. 2018. [Online]. Available through

<https://markets.ft.com/data/equities/tearsheet/summary?s=HAS:LSE>.

Return on Equity. 2018. [Online]. Available through

<https://www.myaccountingcourse.com/financial-ratios/return-on-equity-ratio>.

8

ONLINE

Annual Report of Hays Plc. 2017. [Online]. Available through

<https://www.haysplc.com/investors/annual-report-2017>.

Annual Report of Hays Plc. 2018. [Online]. Available through

<https://www.haysplc.com/~/media/Files/H/Hays/annual-reports/ar-2018/ar-2018.pdf>.

Hays plc (HAS.l). 2018. [Online]. Available through <https://finance.yahoo.com/quote/HAS.L/>.

Hays PLC. 2018. [Online]. Available through

<https://markets.ft.com/data/equities/tearsheet/summary?s=HAS:LSE>.

Return on Equity. 2018. [Online]. Available through

<https://www.myaccountingcourse.com/financial-ratios/return-on-equity-ratio>.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Ration Analysis

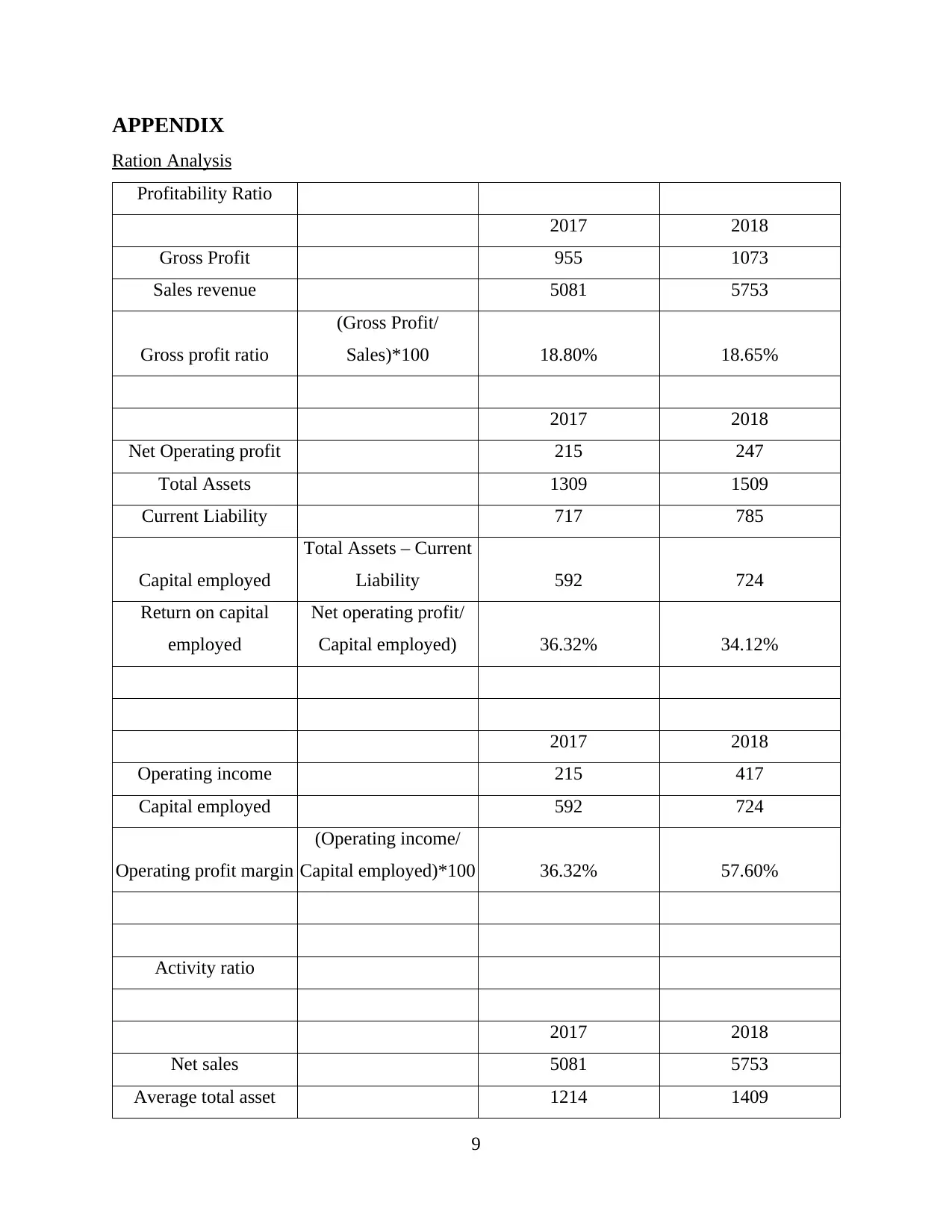

Profitability Ratio

2017 2018

Gross Profit 955 1073

Sales revenue 5081 5753

Gross profit ratio

(Gross Profit/

Sales)*100 18.80% 18.65%

2017 2018

Net Operating profit 215 247

Total Assets 1309 1509

Current Liability 717 785

Capital employed

Total Assets – Current

Liability 592 724

Return on capital

employed

Net operating profit/

Capital employed) 36.32% 34.12%

2017 2018

Operating income 215 417

Capital employed 592 724

Operating profit margin

(Operating income/

Capital employed)*100 36.32% 57.60%

Activity ratio

2017 2018

Net sales 5081 5753

Average total asset 1214 1409

9

Ration Analysis

Profitability Ratio

2017 2018

Gross Profit 955 1073

Sales revenue 5081 5753

Gross profit ratio

(Gross Profit/

Sales)*100 18.80% 18.65%

2017 2018

Net Operating profit 215 247

Total Assets 1309 1509

Current Liability 717 785

Capital employed

Total Assets – Current

Liability 592 724

Return on capital

employed

Net operating profit/

Capital employed) 36.32% 34.12%

2017 2018

Operating income 215 417

Capital employed 592 724

Operating profit margin

(Operating income/

Capital employed)*100 36.32% 57.60%

Activity ratio

2017 2018

Net sales 5081 5753

Average total asset 1214 1409

9

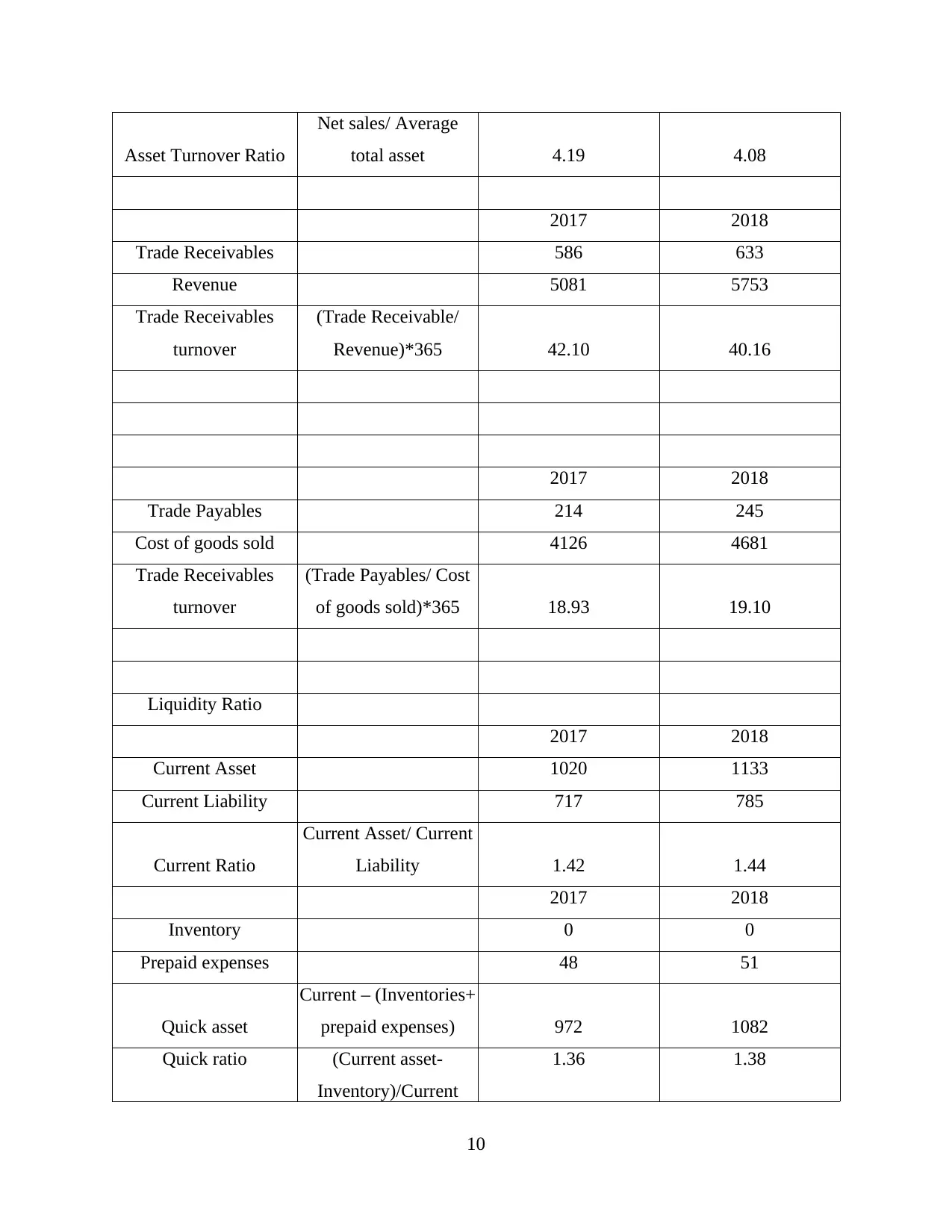

Asset Turnover Ratio

Net sales/ Average

total asset 4.19 4.08

2017 2018

Trade Receivables 586 633

Revenue 5081 5753

Trade Receivables

turnover

(Trade Receivable/

Revenue)*365 42.10 40.16

2017 2018

Trade Payables 214 245

Cost of goods sold 4126 4681

Trade Receivables

turnover

(Trade Payables/ Cost

of goods sold)*365 18.93 19.10

Liquidity Ratio

2017 2018

Current Asset 1020 1133

Current Liability 717 785

Current Ratio

Current Asset/ Current

Liability 1.42 1.44

2017 2018

Inventory 0 0

Prepaid expenses 48 51

Quick asset

Current – (Inventories+

prepaid expenses) 972 1082

Quick ratio (Current asset-

Inventory)/Current

1.36 1.38

10

Net sales/ Average

total asset 4.19 4.08

2017 2018

Trade Receivables 586 633

Revenue 5081 5753

Trade Receivables

turnover

(Trade Receivable/

Revenue)*365 42.10 40.16

2017 2018

Trade Payables 214 245

Cost of goods sold 4126 4681

Trade Receivables

turnover

(Trade Payables/ Cost

of goods sold)*365 18.93 19.10

Liquidity Ratio

2017 2018

Current Asset 1020 1133

Current Liability 717 785

Current Ratio

Current Asset/ Current

Liability 1.42 1.44

2017 2018

Inventory 0 0

Prepaid expenses 48 51

Quick asset

Current – (Inventories+

prepaid expenses) 972 1082

Quick ratio (Current asset-

Inventory)/Current

1.36 1.38

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.