HC1010 Accounting: Financial Statement Analysis and Decisions

VerifiedAdded on 2023/06/07

|13

|1932

|401

Report

AI Summary

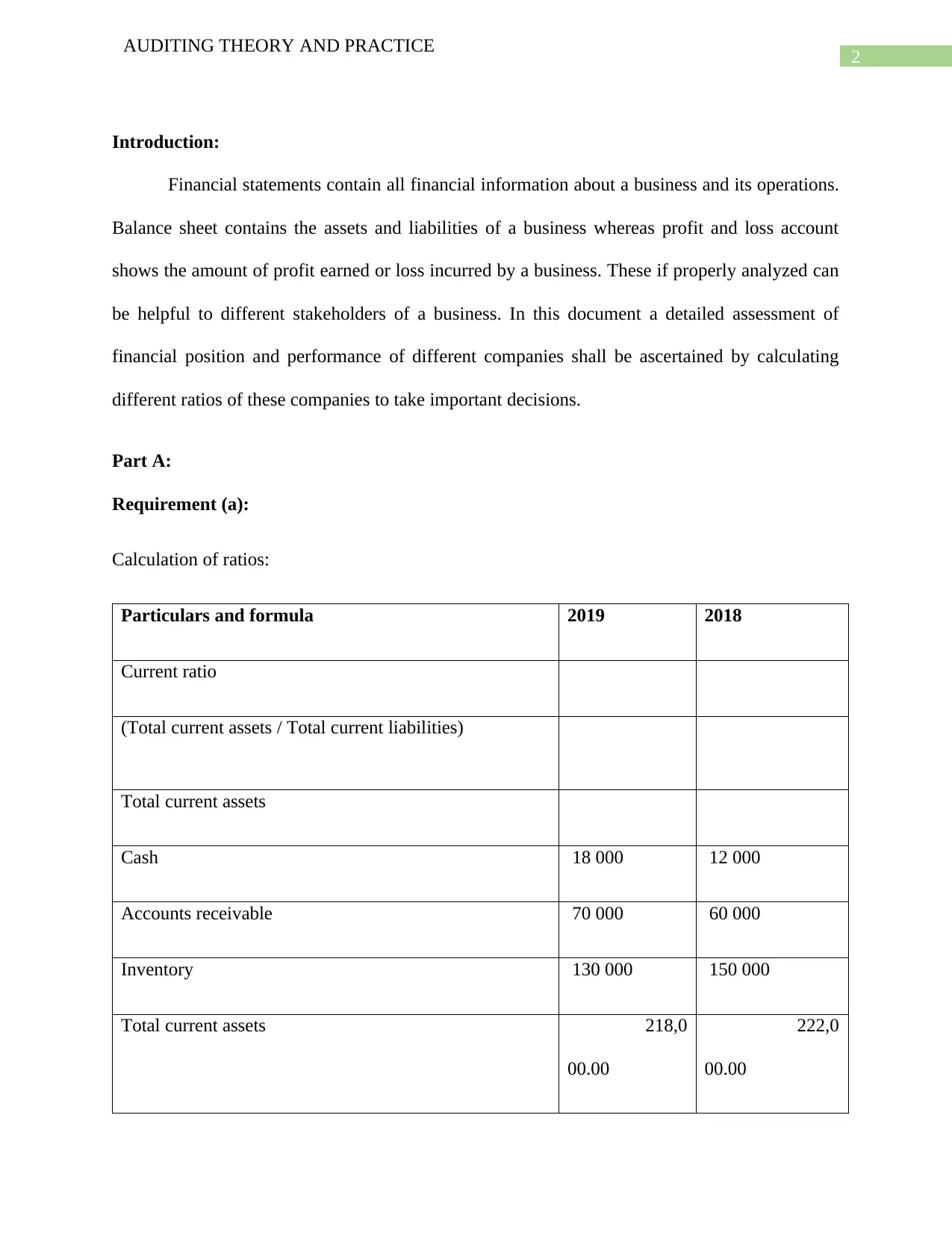

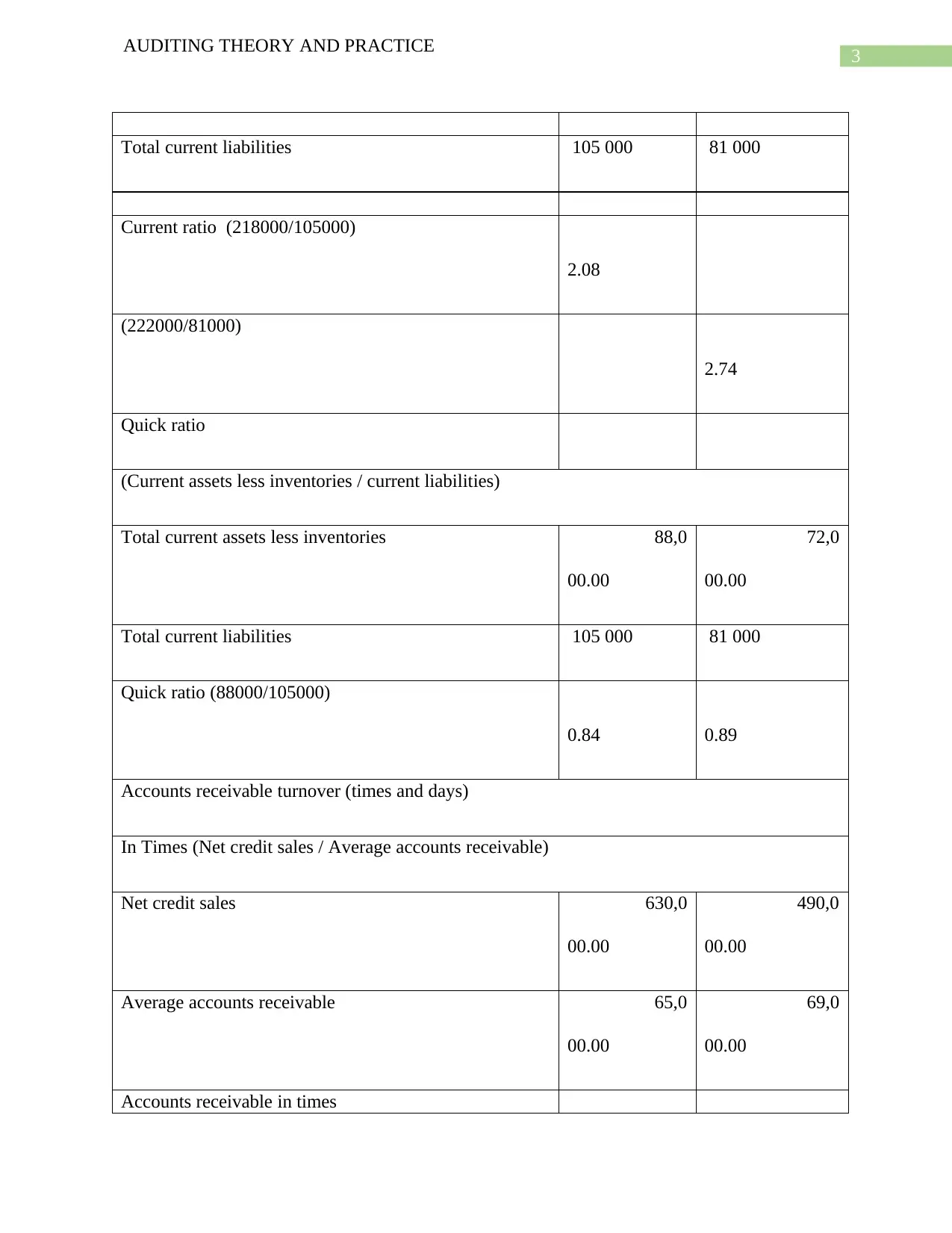

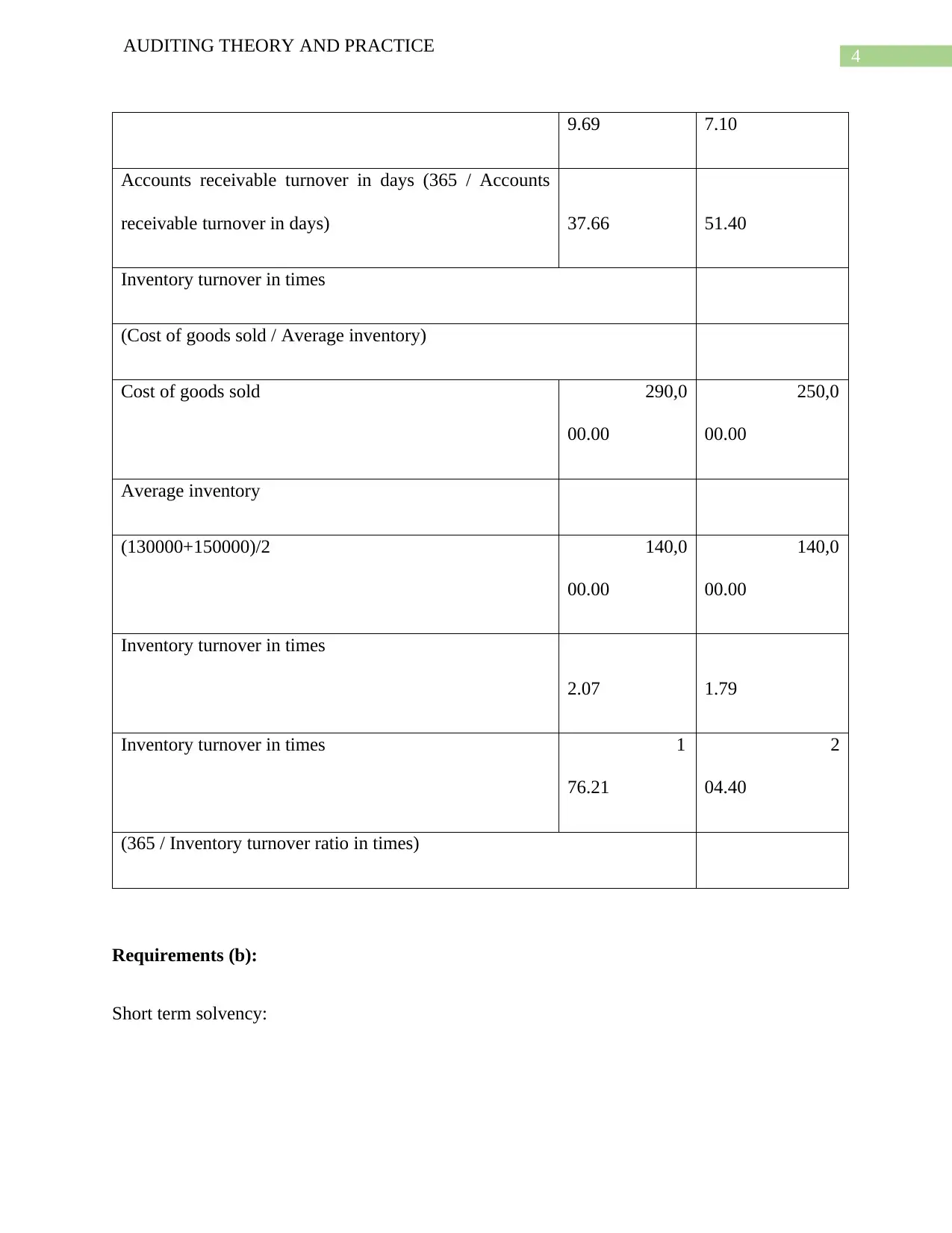

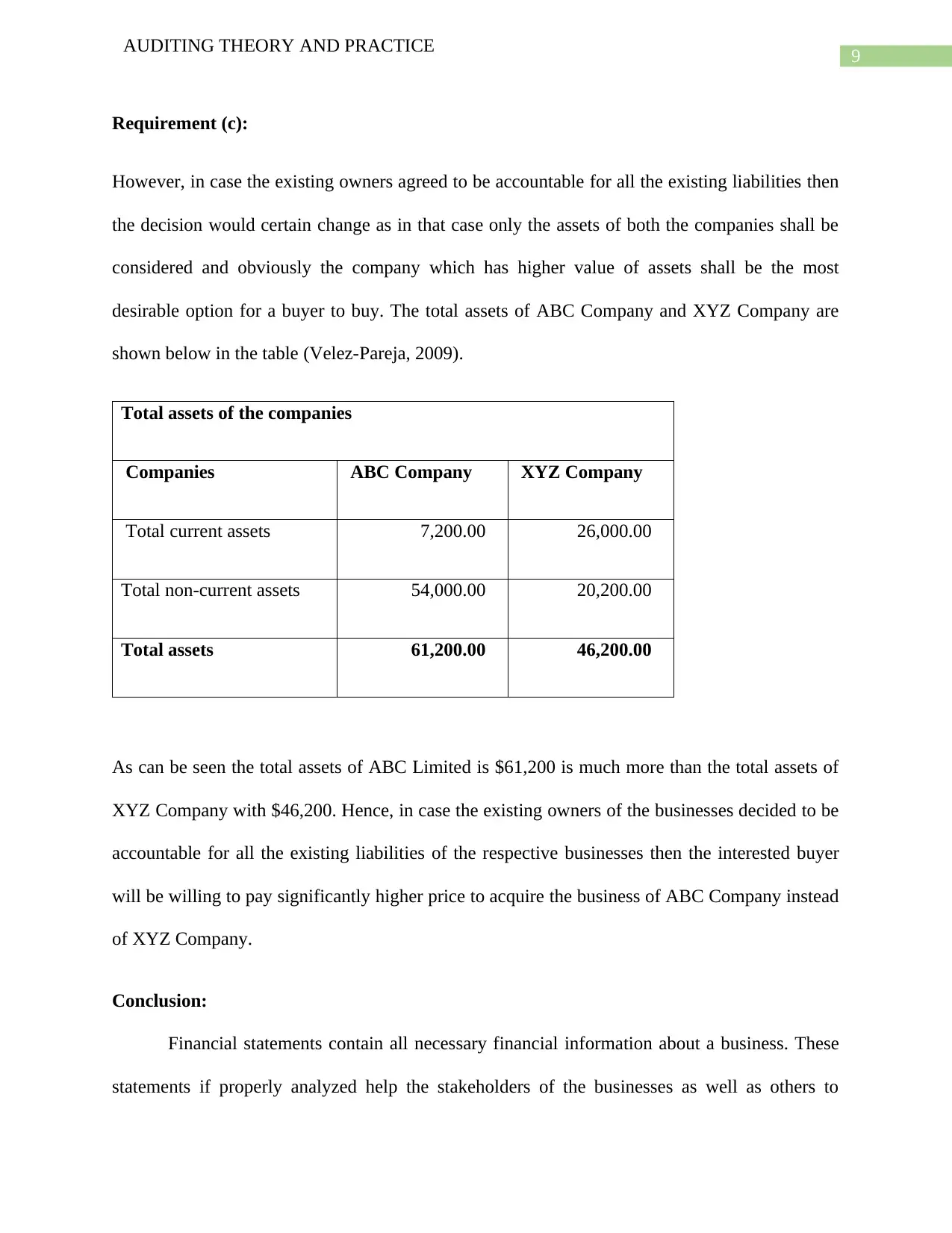

This assignment provides a comprehensive analysis of financial statements, focusing on ratio analysis and solvency assessment for Big Bang Pty Limited. It calculates key financial ratios such as current ratio, quick ratio, accounts receivable turnover, and inventory turnover to evaluate the company's short-term solvency and efficiency. The analysis reveals that while the company's short-term solvency has slightly deteriorated, its efficiency in managing accounts receivable and inventory has improved. Additionally, the assignment discusses the classification of various items as income or capital receipts and assesses loan applications based on solvency. It also evaluates the net assets of companies to determine acquisition prices, providing a detailed understanding of financial statement analysis and its applications in business decision-making. Desklib offers a platform for students to access similar solved assignments and study resources.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.