HC2091 Finance Report: Commonwealth Bank Financial Performance

VerifiedAdded on 2023/06/08

|26

|4009

|388

Report

AI Summary

This report provides a detailed analysis of Commonwealth Bank's financial performance between 2016 and 2017. It examines various performance ratios, including short-term solvency (current ratio and times interest earned), long-term solvency (total debt to total assets and debt-equity ratio), asset utilization (asset turnover and receivables collection period), and profitability ratios (cash return on sales, gross profit margin, net profit margin, and return on assets). The analysis indicates improvements in liquidity and asset turnover, but also highlights concerns regarding high debt levels. The report concludes with a comparison of share price movements, offering insights into the bank's overall financial health and investment potential. Desklib provides a platform for students to access similar solved assignments and past papers for academic assistance.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Business Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

BUSINESS FINANCE

Table of Contents

1. Description of the companies......................................................................................................3

Brief Description of the Company...............................................................................................3

Core Activities.............................................................................................................................3

Competitive Advantages..............................................................................................................3

Banking Industry.........................................................................................................................4

2. Calculation and analysis of performance ratios...........................................................................5

Short term solvency.....................................................................................................................5

Current Ratio...........................................................................................................................6

Times interest earned...............................................................................................................7

Long term solvency.....................................................................................................................7

Total Debt to Total Assets.......................................................................................................8

Debt Equity Ratio....................................................................................................................9

Asset utilization.........................................................................................................................10

Assets Turnover.....................................................................................................................11

Receivables Collection Period...............................................................................................12

Profitability Ratios.....................................................................................................................12

Cash return on sales...............................................................................................................13

Gross Profit Margin...............................................................................................................14

BUSINESS FINANCE

Table of Contents

1. Description of the companies......................................................................................................3

Brief Description of the Company...............................................................................................3

Core Activities.............................................................................................................................3

Competitive Advantages..............................................................................................................3

Banking Industry.........................................................................................................................4

2. Calculation and analysis of performance ratios...........................................................................5

Short term solvency.....................................................................................................................5

Current Ratio...........................................................................................................................6

Times interest earned...............................................................................................................7

Long term solvency.....................................................................................................................7

Total Debt to Total Assets.......................................................................................................8

Debt Equity Ratio....................................................................................................................9

Asset utilization.........................................................................................................................10

Assets Turnover.....................................................................................................................11

Receivables Collection Period...............................................................................................12

Profitability Ratios.....................................................................................................................12

Cash return on sales...............................................................................................................13

Gross Profit Margin...............................................................................................................14

2

BUSINESS FINANCE

Net Profit Margin...................................................................................................................15

Return on assets.....................................................................................................................16

Market Value Ratios..................................................................................................................16

Price Earnings Ratio..............................................................................................................17

Payout Ratio...........................................................................................................................18

Earning Price Per Share.........................................................................................................19

3. Graphs and comparison of share price movements...................................................................19

References......................................................................................................................................23

BUSINESS FINANCE

Net Profit Margin...................................................................................................................15

Return on assets.....................................................................................................................16

Market Value Ratios..................................................................................................................16

Price Earnings Ratio..............................................................................................................17

Payout Ratio...........................................................................................................................18

Earning Price Per Share.........................................................................................................19

3. Graphs and comparison of share price movements...................................................................19

References......................................................................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

BUSINESS FINANCE

1. Description of the companies

Brief Description of the Company

Commonwealth of Australia was established in accordance to the Commonwealth Bank

Act 1911. Commonwealth Bank is considered to be having sufficient savings pertaining to the

general business in the bank. The initiation of the bank was further depicted in terms of

receiving a federal government guarantee. The earliest and strenuous proponent is further seen to

be flamboyant among the American-Australian politician, King O'Malley (Commbank.com.au

2018).

Core Activities

The key financial activities of the bank are seen to be based on various types of the

financial services. This is seen to be included in terms of the financial services including the

retail, funds management, institutional banking and broking services. The bank is also

recognized as one of the largest listed Australian company including the several types of the

brands pertaining to Commonwealth Insurance, Bankwest, Colonial First State Investments,

ASB Bank (New Zealand) and Commonwealth Securities (CommSec) (Commbank.com.au

2018).

Competitive Advantages

The important factors associated to the competitive advantage for the company needs to

be identified with the visionary, creative and agile initiatives. The disruptors of the company are

also considered with fresh thinking and appetite for growth. The proactive and positive change

has been also seen to be major facilitator of the competitive advantage. It needs to be also seen

BUSINESS FINANCE

1. Description of the companies

Brief Description of the Company

Commonwealth of Australia was established in accordance to the Commonwealth Bank

Act 1911. Commonwealth Bank is considered to be having sufficient savings pertaining to the

general business in the bank. The initiation of the bank was further depicted in terms of

receiving a federal government guarantee. The earliest and strenuous proponent is further seen to

be flamboyant among the American-Australian politician, King O'Malley (Commbank.com.au

2018).

Core Activities

The key financial activities of the bank are seen to be based on various types of the

financial services. This is seen to be included in terms of the financial services including the

retail, funds management, institutional banking and broking services. The bank is also

recognized as one of the largest listed Australian company including the several types of the

brands pertaining to Commonwealth Insurance, Bankwest, Colonial First State Investments,

ASB Bank (New Zealand) and Commonwealth Securities (CommSec) (Commbank.com.au

2018).

Competitive Advantages

The important factors associated to the competitive advantage for the company needs to

be identified with the visionary, creative and agile initiatives. The disruptors of the company are

also considered with fresh thinking and appetite for growth. The proactive and positive change

has been also seen to be major facilitator of the competitive advantage. It needs to be also seen

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

BUSINESS FINANCE

that the harnessers are able to improve the overall business and also pus the optimization process.

The competitive advantages need to be also considered with the approach taken by the policy

adopters. These strategies are evident with a cautious focus on the innovation and the changes.

The reluctant nature of the adopters has been further seen with reluctant need for the reassurance

and evidence. The maintenance of the complacent resistors is also depicted with competitive

advantage (Commbank.com.au 2018).

Banking Industry

It needs to be discerned that banking in Australia mainly dominated by four major banks

includes National Australia Bank (NAB), Westpac Banking Corporation, Australia and New

Zealand Banking Group and Commonwealth Bank of Australia. In addition to this, there are very

small and medium players were associated to financial services such as providing limited

banking type services including mutual banks, unions of credit and building of society. These

types of service are often identified as deposit taking institutions. Moreover, several foreign

banks have been also depicted with presence of having retail banking experience. In general, the

banks are required to adhere to the Banking Act 1959 in order to get the license for banking.

Moreover, the foreign banks need to maintain the license through several branches in Australia

which are incorporated as foreign subsidiary banks and complying with religious charitable

development funds and several types of other requirement for license. It needs to be also

understood that Australia is comprised of a sophisticated, profitable and competitive financial

sector along with the strong regulatory system. In the last decade, Commonwealth Bank was

ranked first by Bloomberg with a total riskless adjusted ratio of 18%. Westpac bank on the other

BUSINESS FINANCE

that the harnessers are able to improve the overall business and also pus the optimization process.

The competitive advantages need to be also considered with the approach taken by the policy

adopters. These strategies are evident with a cautious focus on the innovation and the changes.

The reluctant nature of the adopters has been further seen with reluctant need for the reassurance

and evidence. The maintenance of the complacent resistors is also depicted with competitive

advantage (Commbank.com.au 2018).

Banking Industry

It needs to be discerned that banking in Australia mainly dominated by four major banks

includes National Australia Bank (NAB), Westpac Banking Corporation, Australia and New

Zealand Banking Group and Commonwealth Bank of Australia. In addition to this, there are very

small and medium players were associated to financial services such as providing limited

banking type services including mutual banks, unions of credit and building of society. These

types of service are often identified as deposit taking institutions. Moreover, several foreign

banks have been also depicted with presence of having retail banking experience. In general, the

banks are required to adhere to the Banking Act 1959 in order to get the license for banking.

Moreover, the foreign banks need to maintain the license through several branches in Australia

which are incorporated as foreign subsidiary banks and complying with religious charitable

development funds and several types of other requirement for license. It needs to be also

understood that Australia is comprised of a sophisticated, profitable and competitive financial

sector along with the strong regulatory system. In the last decade, Commonwealth Bank was

ranked first by Bloomberg with a total riskless adjusted ratio of 18%. Westpac bank on the other

5

BUSINESS FINANCE

hand is determined to be having 11% of riskless return. Similarly, Australia and New Zealand

bank is identified with 8.7% of riskless return ranking (Rebello 2016).

2. Calculation and analysis of performance ratios

Short term solvency

Liquidity ratio or short-term solvency ratio acts as a financial metrics for the ability of the

debtor to pay off the debt obligations by ensuring no withdrawal of external capital. This ratio is

able to quantify the debt obligations of the company along with its margin of safety by including

measures such as current ratio, operating cash ratio and quick ratio (Accounting Management

2015). The computation of short-term analysis for Commonwealth Bank has been considered

with identifying the current assets, liabilities, EBIT and interest expense which is conducive for

competition of current ratio and Times interest earned. The current assets of the company are

seen as cash and liquid assets which amounted to $ 45,850m in $ 2017m in 2016. The current

liabilities have included items such as payables due to other financial institutions and deferred

tax liabilities (Paramasivan and Subramaniam 2014).

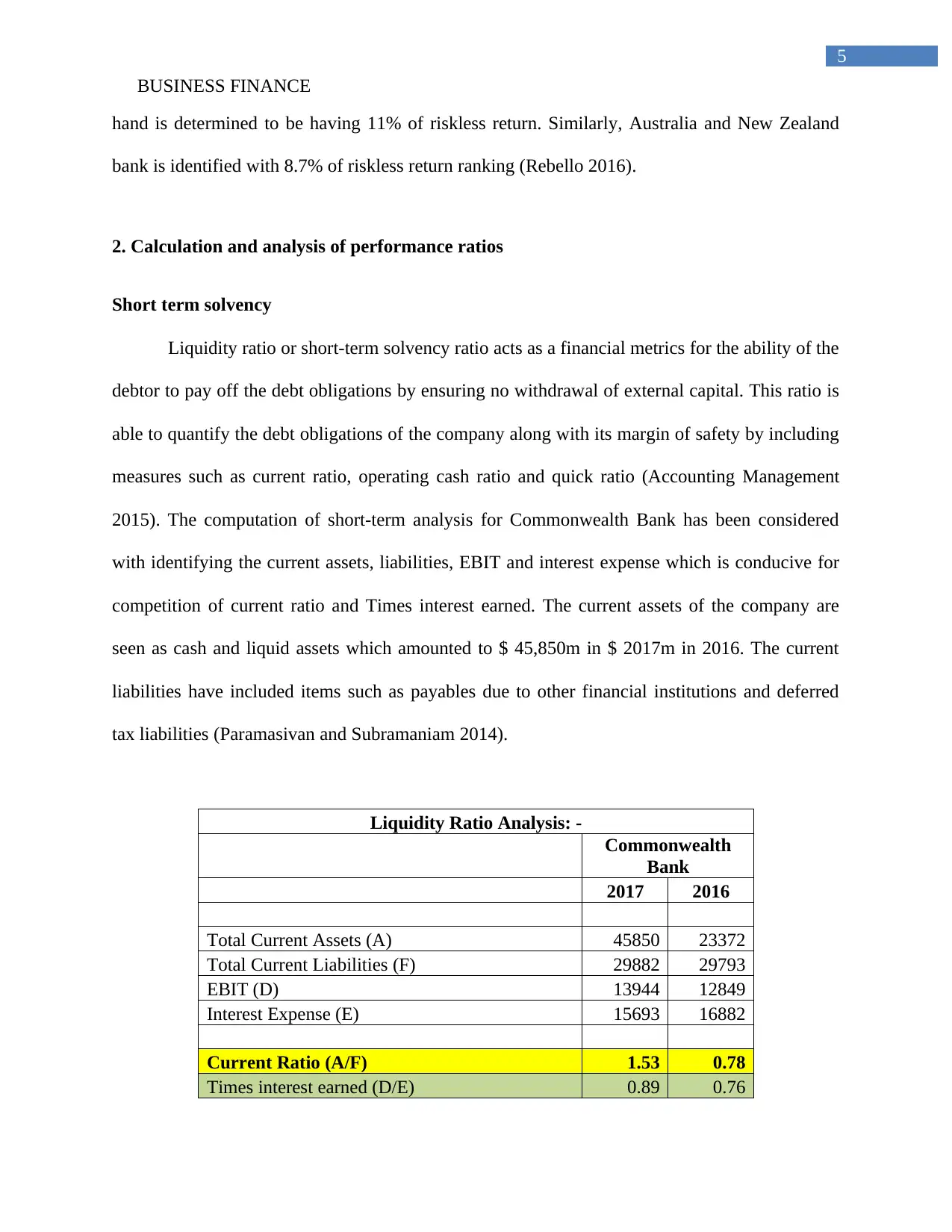

Liquidity Ratio Analysis: -

Commonwealth

Bank

2017 2016

Total Current Assets (A) 45850 23372

Total Current Liabilities (F) 29882 29793

EBIT (D) 13944 12849

Interest Expense (E) 15693 16882

Current Ratio (A/F) 1.53 0.78

Times interest earned (D/E) 0.89 0.76

BUSINESS FINANCE

hand is determined to be having 11% of riskless return. Similarly, Australia and New Zealand

bank is identified with 8.7% of riskless return ranking (Rebello 2016).

2. Calculation and analysis of performance ratios

Short term solvency

Liquidity ratio or short-term solvency ratio acts as a financial metrics for the ability of the

debtor to pay off the debt obligations by ensuring no withdrawal of external capital. This ratio is

able to quantify the debt obligations of the company along with its margin of safety by including

measures such as current ratio, operating cash ratio and quick ratio (Accounting Management

2015). The computation of short-term analysis for Commonwealth Bank has been considered

with identifying the current assets, liabilities, EBIT and interest expense which is conducive for

competition of current ratio and Times interest earned. The current assets of the company are

seen as cash and liquid assets which amounted to $ 45,850m in $ 2017m in 2016. The current

liabilities have included items such as payables due to other financial institutions and deferred

tax liabilities (Paramasivan and Subramaniam 2014).

Liquidity Ratio Analysis: -

Commonwealth

Bank

2017 2016

Total Current Assets (A) 45850 23372

Total Current Liabilities (F) 29882 29793

EBIT (D) 13944 12849

Interest Expense (E) 15693 16882

Current Ratio (A/F) 1.53 0.78

Times interest earned (D/E) 0.89 0.76

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

BUSINESS FINANCE

Table 1: Liquidity Ratio Analysis of Commonwealth Bank

(Source: Commbank.com.au. 2018)

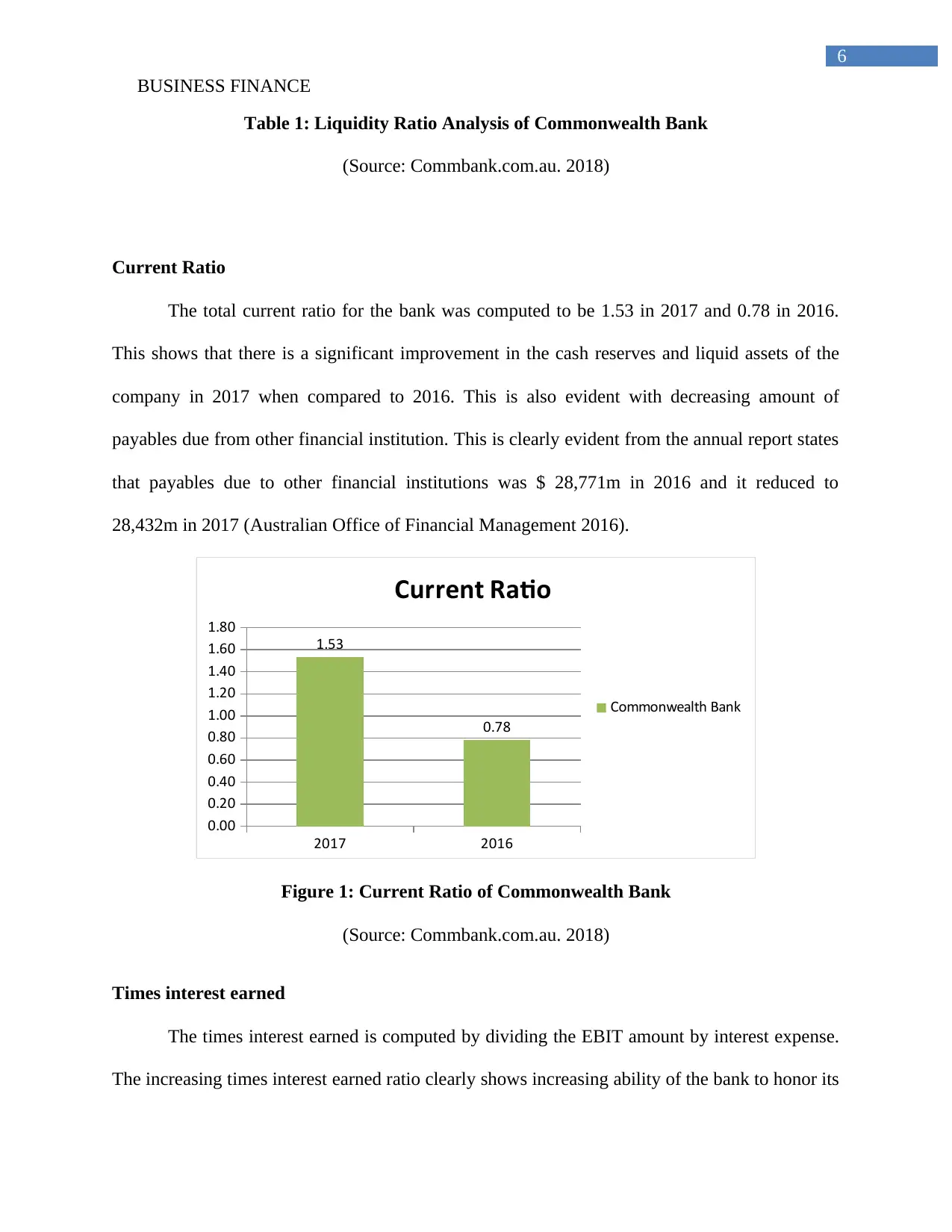

Current Ratio

The total current ratio for the bank was computed to be 1.53 in 2017 and 0.78 in 2016.

This shows that there is a significant improvement in the cash reserves and liquid assets of the

company in 2017 when compared to 2016. This is also evident with decreasing amount of

payables due from other financial institution. This is clearly evident from the annual report states

that payables due to other financial institutions was $ 28,771m in 2016 and it reduced to

28,432m in 2017 (Australian Office of Financial Management 2016).

2017 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.53

0.78

Current Ratio

Commonwealth Bank

Figure 1: Current Ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

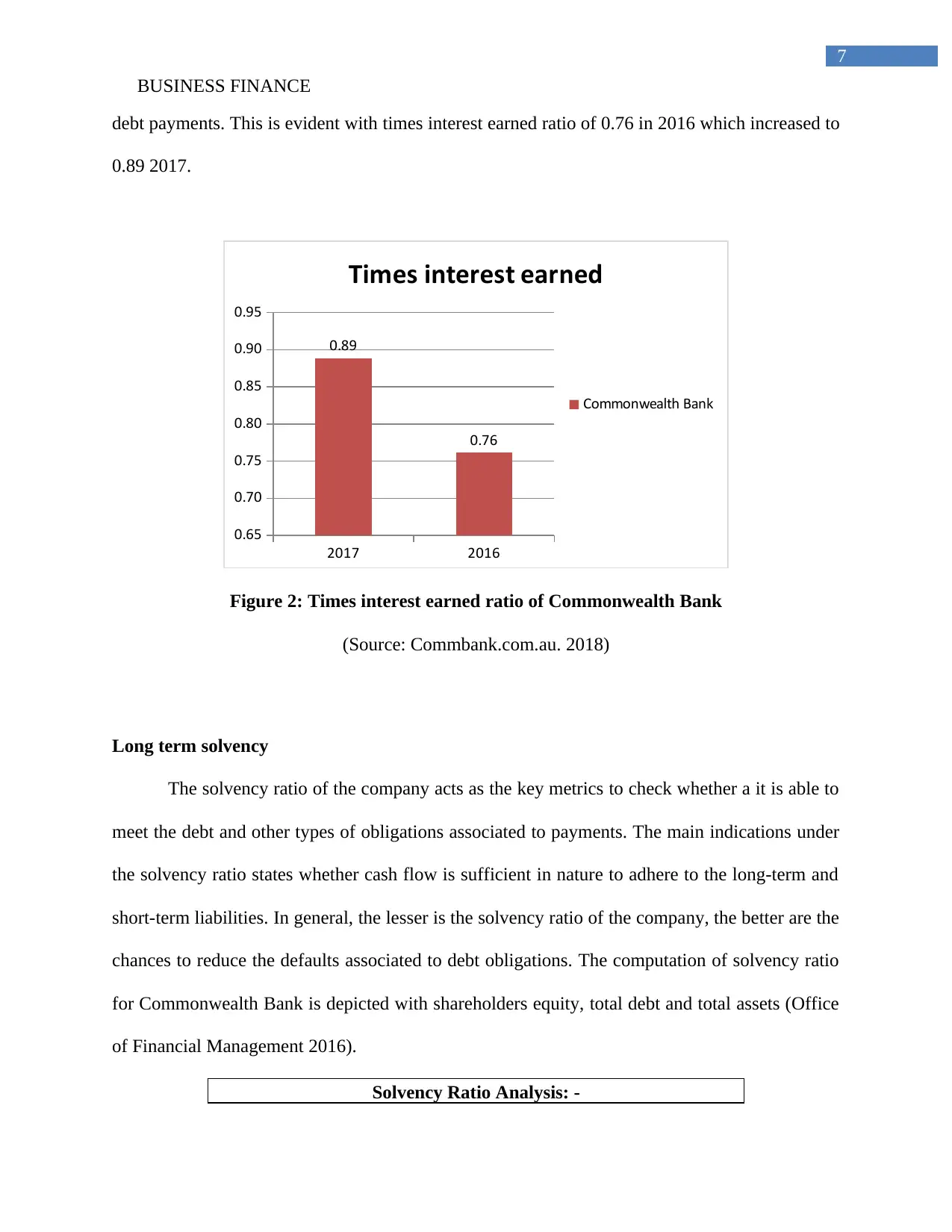

Times interest earned

The times interest earned is computed by dividing the EBIT amount by interest expense.

The increasing times interest earned ratio clearly shows increasing ability of the bank to honor its

BUSINESS FINANCE

Table 1: Liquidity Ratio Analysis of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Current Ratio

The total current ratio for the bank was computed to be 1.53 in 2017 and 0.78 in 2016.

This shows that there is a significant improvement in the cash reserves and liquid assets of the

company in 2017 when compared to 2016. This is also evident with decreasing amount of

payables due from other financial institution. This is clearly evident from the annual report states

that payables due to other financial institutions was $ 28,771m in 2016 and it reduced to

28,432m in 2017 (Australian Office of Financial Management 2016).

2017 2016

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

1.53

0.78

Current Ratio

Commonwealth Bank

Figure 1: Current Ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Times interest earned

The times interest earned is computed by dividing the EBIT amount by interest expense.

The increasing times interest earned ratio clearly shows increasing ability of the bank to honor its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BUSINESS FINANCE

debt payments. This is evident with times interest earned ratio of 0.76 in 2016 which increased to

0.89 2017.

2017 2016

0.65

0.70

0.75

0.80

0.85

0.90

0.95

0.89

0.76

Times interest earned

Commonwealth Bank

Figure 2: Times interest earned ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Long term solvency

The solvency ratio of the company acts as the key metrics to check whether a it is able to

meet the debt and other types of obligations associated to payments. The main indications under

the solvency ratio states whether cash flow is sufficient in nature to adhere to the long-term and

short-term liabilities. In general, the lesser is the solvency ratio of the company, the better are the

chances to reduce the defaults associated to debt obligations. The computation of solvency ratio

for Commonwealth Bank is depicted with shareholders equity, total debt and total assets (Office

of Financial Management 2016).

Solvency Ratio Analysis: -

BUSINESS FINANCE

debt payments. This is evident with times interest earned ratio of 0.76 in 2016 which increased to

0.89 2017.

2017 2016

0.65

0.70

0.75

0.80

0.85

0.90

0.95

0.89

0.76

Times interest earned

Commonwealth Bank

Figure 2: Times interest earned ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Long term solvency

The solvency ratio of the company acts as the key metrics to check whether a it is able to

meet the debt and other types of obligations associated to payments. The main indications under

the solvency ratio states whether cash flow is sufficient in nature to adhere to the long-term and

short-term liabilities. In general, the lesser is the solvency ratio of the company, the better are the

chances to reduce the defaults associated to debt obligations. The computation of solvency ratio

for Commonwealth Bank is depicted with shareholders equity, total debt and total assets (Office

of Financial Management 2016).

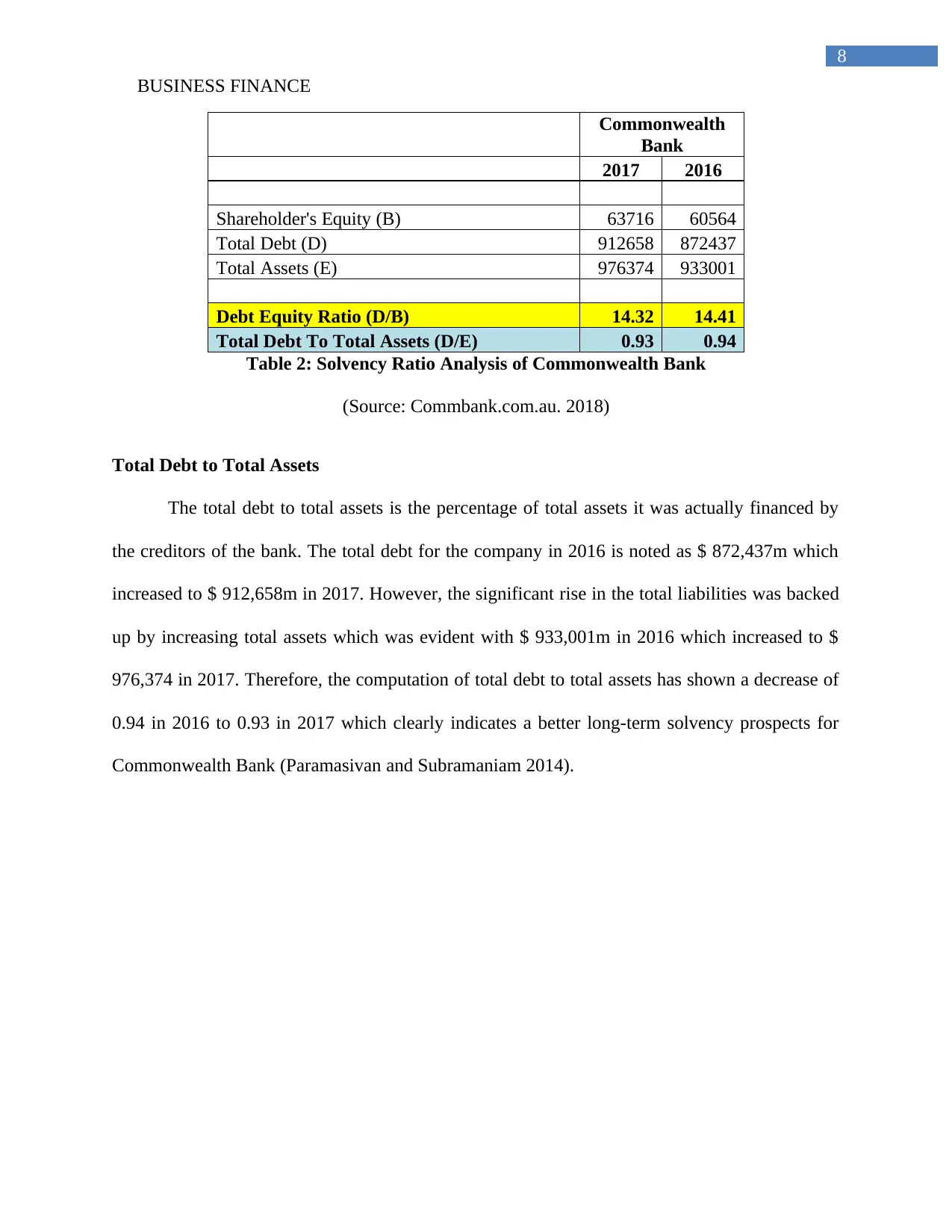

Solvency Ratio Analysis: -

8

BUSINESS FINANCE

Commonwealth

Bank

2017 2016

Shareholder's Equity (B) 63716 60564

Total Debt (D) 912658 872437

Total Assets (E) 976374 933001

Debt Equity Ratio (D/B) 14.32 14.41

Total Debt To Total Assets (D/E) 0.93 0.94

Table 2: Solvency Ratio Analysis of Commonwealth Bank

(Source: Commbank.com.au. 2018)

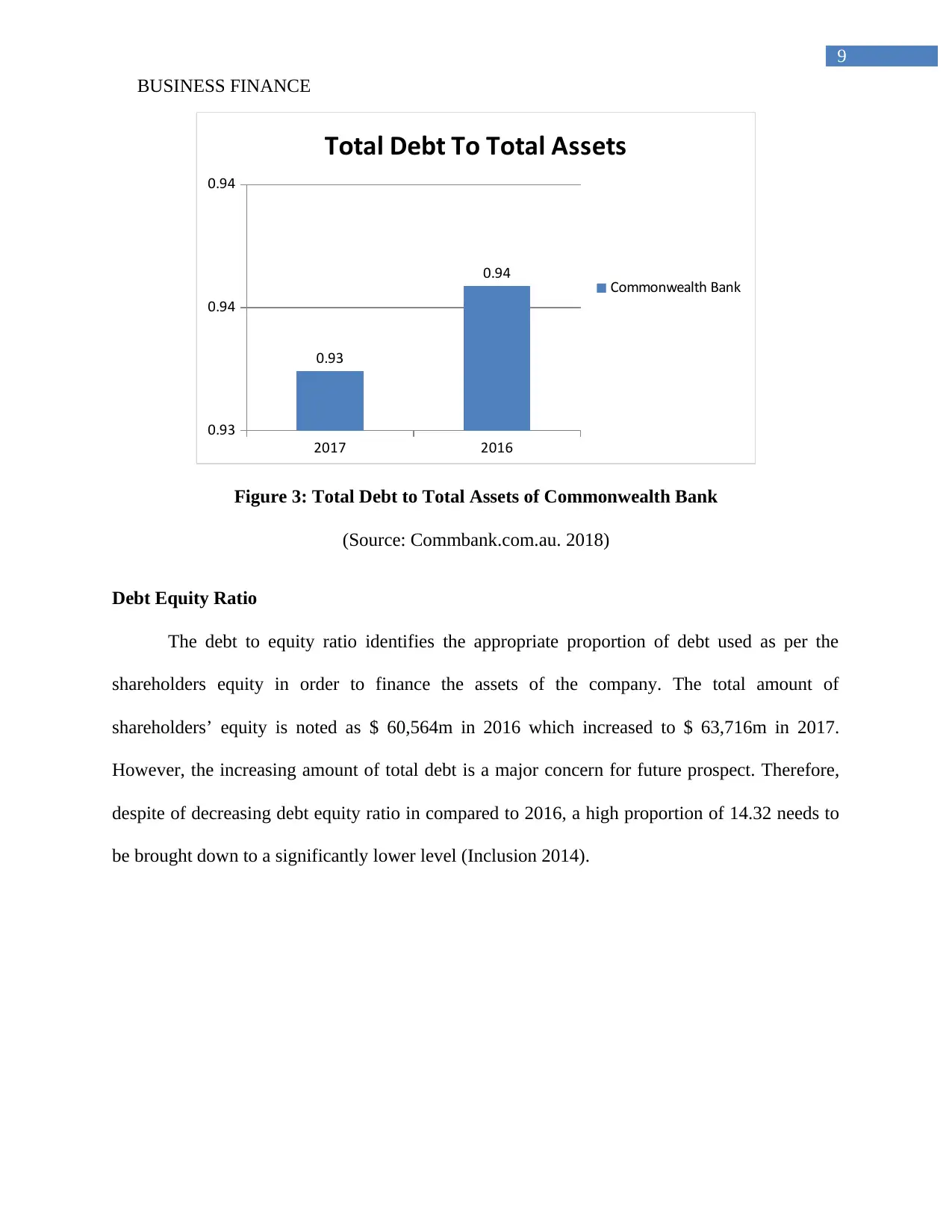

Total Debt to Total Assets

The total debt to total assets is the percentage of total assets it was actually financed by

the creditors of the bank. The total debt for the company in 2016 is noted as $ 872,437m which

increased to $ 912,658m in 2017. However, the significant rise in the total liabilities was backed

up by increasing total assets which was evident with $ 933,001m in 2016 which increased to $

976,374 in 2017. Therefore, the computation of total debt to total assets has shown a decrease of

0.94 in 2016 to 0.93 in 2017 which clearly indicates a better long-term solvency prospects for

Commonwealth Bank (Paramasivan and Subramaniam 2014).

BUSINESS FINANCE

Commonwealth

Bank

2017 2016

Shareholder's Equity (B) 63716 60564

Total Debt (D) 912658 872437

Total Assets (E) 976374 933001

Debt Equity Ratio (D/B) 14.32 14.41

Total Debt To Total Assets (D/E) 0.93 0.94

Table 2: Solvency Ratio Analysis of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Total Debt to Total Assets

The total debt to total assets is the percentage of total assets it was actually financed by

the creditors of the bank. The total debt for the company in 2016 is noted as $ 872,437m which

increased to $ 912,658m in 2017. However, the significant rise in the total liabilities was backed

up by increasing total assets which was evident with $ 933,001m in 2016 which increased to $

976,374 in 2017. Therefore, the computation of total debt to total assets has shown a decrease of

0.94 in 2016 to 0.93 in 2017 which clearly indicates a better long-term solvency prospects for

Commonwealth Bank (Paramasivan and Subramaniam 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

BUSINESS FINANCE

2017 2016

0.93

0.94

0.94

0.93

0.94

Total Debt To Total Assets

Commonwealth Bank

Figure 3: Total Debt to Total Assets of Commonwealth Bank

(Source: Commbank.com.au. 2018)

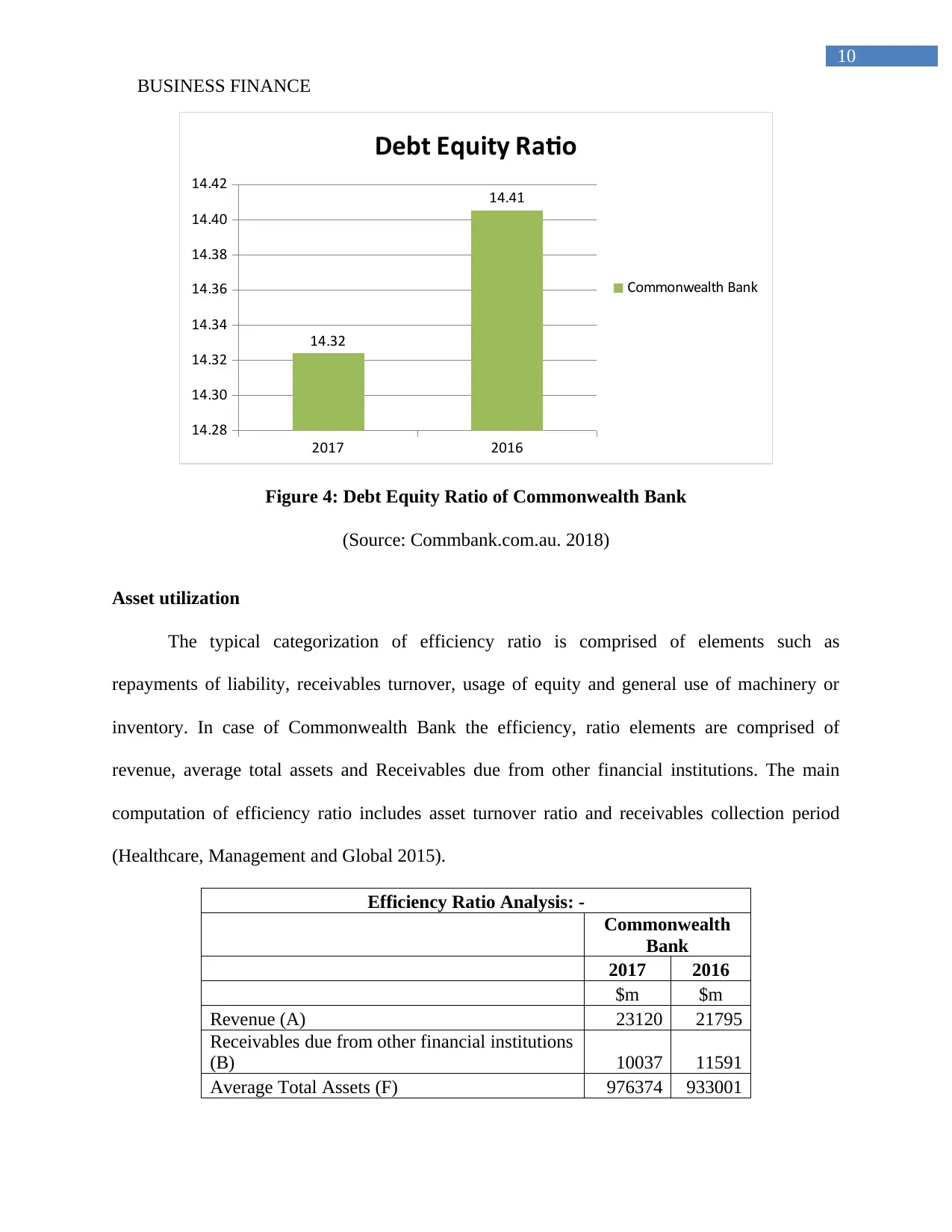

Debt Equity Ratio

The debt to equity ratio identifies the appropriate proportion of debt used as per the

shareholders equity in order to finance the assets of the company. The total amount of

shareholders’ equity is noted as $ 60,564m in 2016 which increased to $ 63,716m in 2017.

However, the increasing amount of total debt is a major concern for future prospect. Therefore,

despite of decreasing debt equity ratio in compared to 2016, a high proportion of 14.32 needs to

be brought down to a significantly lower level (Inclusion 2014).

BUSINESS FINANCE

2017 2016

0.93

0.94

0.94

0.93

0.94

Total Debt To Total Assets

Commonwealth Bank

Figure 3: Total Debt to Total Assets of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Debt Equity Ratio

The debt to equity ratio identifies the appropriate proportion of debt used as per the

shareholders equity in order to finance the assets of the company. The total amount of

shareholders’ equity is noted as $ 60,564m in 2016 which increased to $ 63,716m in 2017.

However, the increasing amount of total debt is a major concern for future prospect. Therefore,

despite of decreasing debt equity ratio in compared to 2016, a high proportion of 14.32 needs to

be brought down to a significantly lower level (Inclusion 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BUSINESS FINANCE

2017 2016

14.28

14.30

14.32

14.34

14.36

14.38

14.40

14.42

14.32

14.41

Debt Equity Ratio

Commonwealth Bank

Figure 4: Debt Equity Ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Asset utilization

The typical categorization of efficiency ratio is comprised of elements such as

repayments of liability, receivables turnover, usage of equity and general use of machinery or

inventory. In case of Commonwealth Bank the efficiency, ratio elements are comprised of

revenue, average total assets and Receivables due from other financial institutions. The main

computation of efficiency ratio includes asset turnover ratio and receivables collection period

(Healthcare, Management and Global 2015).

Efficiency Ratio Analysis: -

Commonwealth

Bank

2017 2016

$m $m

Revenue (A) 23120 21795

Receivables due from other financial institutions

(B) 10037 11591

Average Total Assets (F) 976374 933001

BUSINESS FINANCE

2017 2016

14.28

14.30

14.32

14.34

14.36

14.38

14.40

14.42

14.32

14.41

Debt Equity Ratio

Commonwealth Bank

Figure 4: Debt Equity Ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Asset utilization

The typical categorization of efficiency ratio is comprised of elements such as

repayments of liability, receivables turnover, usage of equity and general use of machinery or

inventory. In case of Commonwealth Bank the efficiency, ratio elements are comprised of

revenue, average total assets and Receivables due from other financial institutions. The main

computation of efficiency ratio includes asset turnover ratio and receivables collection period

(Healthcare, Management and Global 2015).

Efficiency Ratio Analysis: -

Commonwealth

Bank

2017 2016

$m $m

Revenue (A) 23120 21795

Receivables due from other financial institutions

(B) 10037 11591

Average Total Assets (F) 976374 933001

11

BUSINESS FINANCE

Assets turnover (A/F) 0.024 0.023

Receivables Collection Period (365/(A/B)) 158 194

Table 3: Efficiency Ratio Analysis of Commonwealth Bank

(Source: Commbank.com.au. 2018)

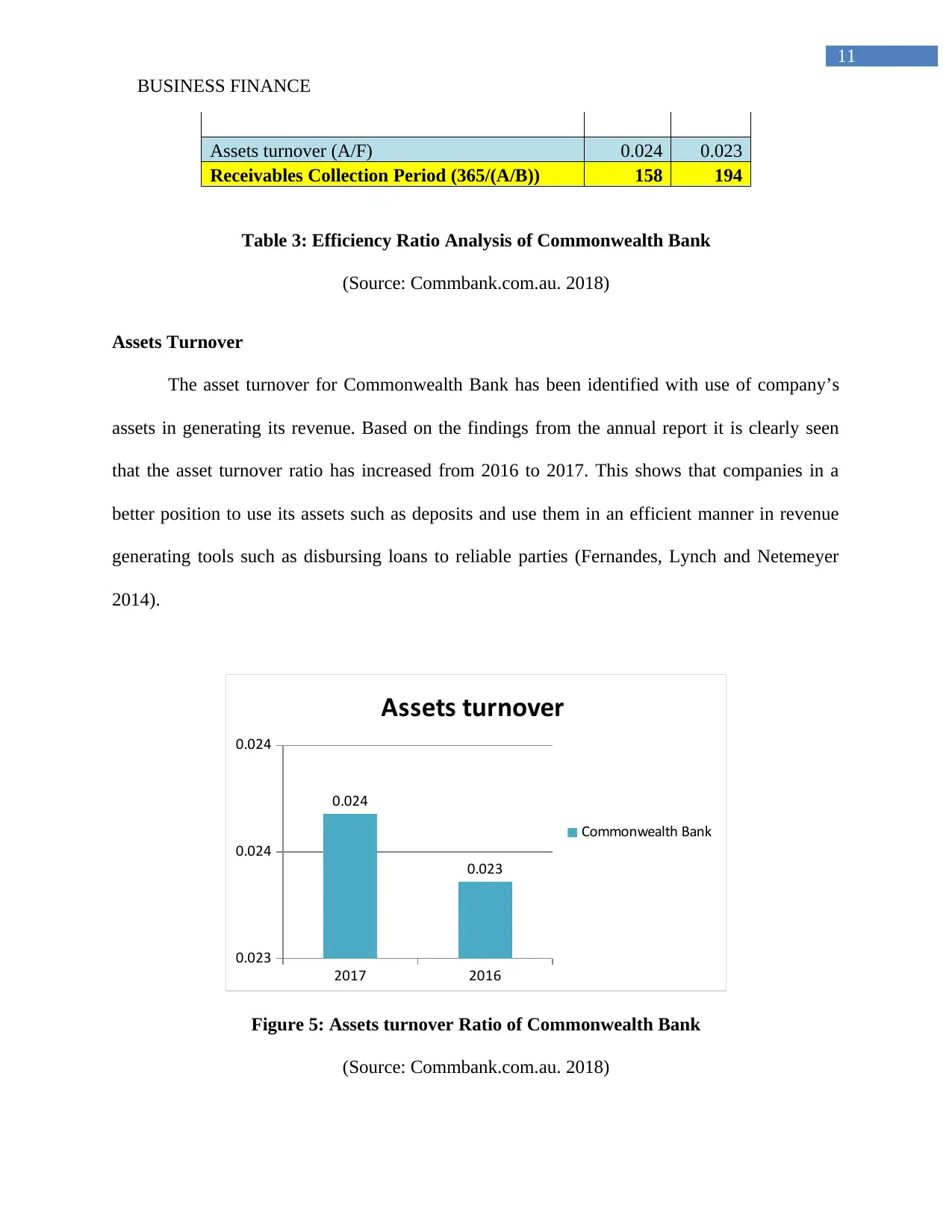

Assets Turnover

The asset turnover for Commonwealth Bank has been identified with use of company’s

assets in generating its revenue. Based on the findings from the annual report it is clearly seen

that the asset turnover ratio has increased from 2016 to 2017. This shows that companies in a

better position to use its assets such as deposits and use them in an efficient manner in revenue

generating tools such as disbursing loans to reliable parties (Fernandes, Lynch and Netemeyer

2014).

2017 2016

0.023

0.024

0.024

0.024

0.023

Assets turnover

Commonwealth Bank

Figure 5: Assets turnover Ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

BUSINESS FINANCE

Assets turnover (A/F) 0.024 0.023

Receivables Collection Period (365/(A/B)) 158 194

Table 3: Efficiency Ratio Analysis of Commonwealth Bank

(Source: Commbank.com.au. 2018)

Assets Turnover

The asset turnover for Commonwealth Bank has been identified with use of company’s

assets in generating its revenue. Based on the findings from the annual report it is clearly seen

that the asset turnover ratio has increased from 2016 to 2017. This shows that companies in a

better position to use its assets such as deposits and use them in an efficient manner in revenue

generating tools such as disbursing loans to reliable parties (Fernandes, Lynch and Netemeyer

2014).

2017 2016

0.023

0.024

0.024

0.024

0.023

Assets turnover

Commonwealth Bank

Figure 5: Assets turnover Ratio of Commonwealth Bank

(Source: Commbank.com.au. 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.