Health and Aged Care Funding Models and Financial Analysis Report

VerifiedAdded on 2023/01/19

|8

|1476

|45

Report

AI Summary

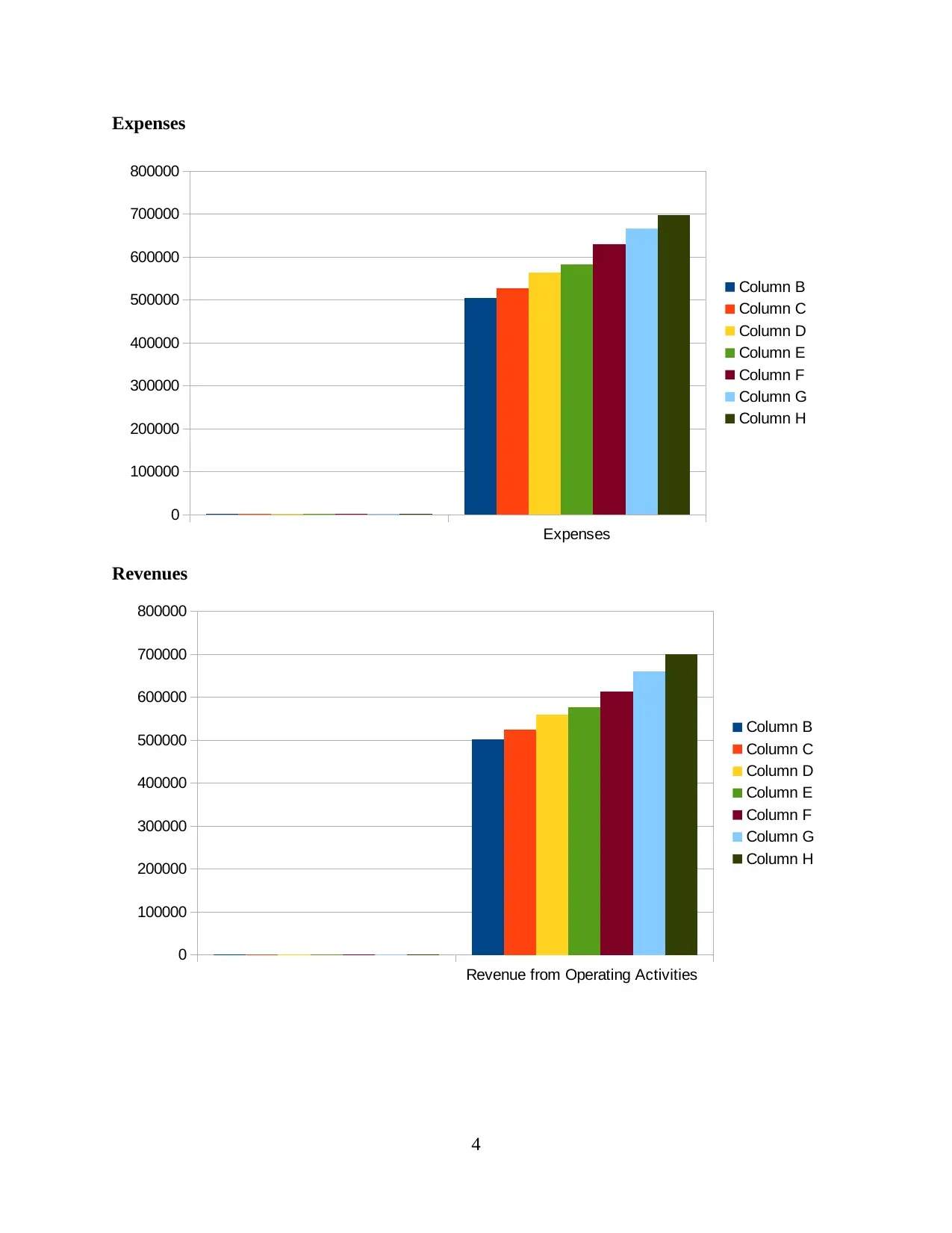

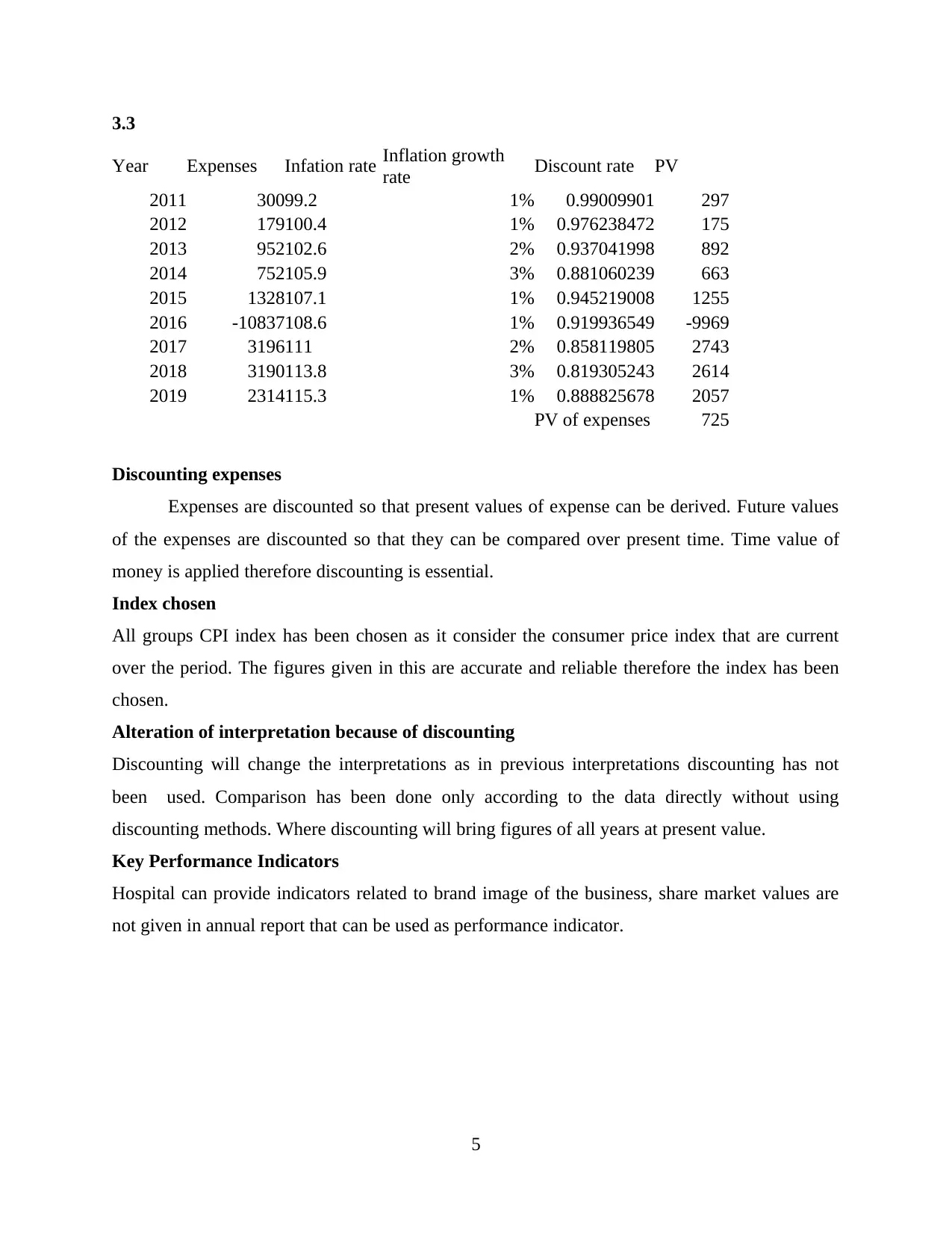

This report provides a comprehensive analysis of health care funding models, focusing on the Activity Based Funding (ABF) model within the Australian health sector. It examines the role of the Independent Hospital Pricing Authority (IHPA) in ABF, national efficiency pricing, and the challenges associated with using average length of stay for funding purposes. The report compares ABF with population-based funding models and identifies financial management issues related to consumer-directed care. Additionally, it delves into the financial statements of the Barwon Health Group, comparing financial summaries to the annual report for 2017-18 and analyzing comprehensive results for 2017 and 2018 using horizontal and vertical analysis, along with graphical representations of trends and discounted expenses. Key Performance Indicators are also discussed, offering a complete financial overview of the healthcare sector.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.