Health Insurance Analysis: Case Study for Raj and Sangeeta, Australia

VerifiedAdded on 2023/06/08

|13

|2999

|396

Case Study

AI Summary

This case study analyzes the health insurance needs of Raj and Sangeeta, an older couple in Australia. The assignment reviews their existing insurance coverage, including term life, funeral, trauma, and income protection. It recommends suitable health insurance products, focusing on hospitality or elective surgery cover and exclusive policies. The study compares health insurance providers Latrobe and BUPA, detailing their benefits, exclusions, and add-on options. It suggests Latrobe as the more suitable option for the couple, given its benefits and the couple's specific needs, including travel & accommodation and GP visits. The assignment also outlines the application process and the principle of utmost good faith in insurance, considering Raj's health condition and age. The document is a student's case study on health insurance with recommendations.

ASSIGNMENT 1 CASE

STUDY 2

STUDY 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................3

Reviewing the existing cover.......................................................................................................3

TASK 2............................................................................................................................................4

Recommendation of suitable health insurance products.............................................................4

TASK 3............................................................................................................................................5

TASK 4............................................................................................................................................8

TASK 5............................................................................................................................................9

a. Steps involved in the application process................................................................................9

TASK 6..........................................................................................................................................10

TASK 7..........................................................................................................................................10

REFERENCES..............................................................................................................................12

Books and Journals....................................................................................................................12

TASK 1............................................................................................................................................3

Reviewing the existing cover.......................................................................................................3

TASK 2............................................................................................................................................4

Recommendation of suitable health insurance products.............................................................4

TASK 3............................................................................................................................................5

TASK 4............................................................................................................................................8

TASK 5............................................................................................................................................9

a. Steps involved in the application process................................................................................9

TASK 6..........................................................................................................................................10

TASK 7..........................................................................................................................................10

REFERENCES..............................................................................................................................12

Books and Journals....................................................................................................................12

TASK 1

Reviewing the existing cover

Term life cover: The couple have taken term life cover of $300000 each which is meant for

covering the insurance coverage until the couple will reached their 80 years. This is means if any

of the couple would die then the beneficent mentioned in the policy would be going to have the

term life cover amount (Biggs, 2020). It is helpful for protecting children or other partner in the

event of the death of the person on whom the beneficent is dependent. Therefore, it would be

recommended to Raj & Sangeeta to retain their term life cover which would provide financial

support to other partner if any of them would die before arriving the age of 80 years. This

insurance cover was suggested to be retained because it has been assumed that the surviving

partner would be the only recipient of the proceedings of the insurance cover.

Funeral cover: The couple is having a funeral cover that should also be retained with

them in order to safeguard the surviving partner from spending their savings or taking on any

additional debts. This cover would be helpful in covering costs associated with the funeral

activities. At this point, the cover provides with the amount necessary for meeting the funeral

requirements and accordingly, there is no requirements for using the hard earned monies out of

savings.

Trauma cover: This cover taken by Raj & Sangeeta is reaching its maturity within a period of

one year and is meant for protecting them from any expenditure that the couple would be going

to made towards the incidence of any serious illness (Bilkey, Baynam and Molster, 2018). So, it

would be better for the couple to cancel out this cover as it has become expensive for them due

to reaching at an older age. The protection that this cover is offering could be availed through

private insurance cover as well that the couple is planning to get now.

Income protection cover: This cover is available with Raj only due to being provided by

their employer and is going to expire at the age of 65 which is about to arrive. Therefore, this

cover should be retained as it is. This is because it would be going to provide income protection

after the retirement on monthly basis to support financially.

Reviewing the existing cover

Term life cover: The couple have taken term life cover of $300000 each which is meant for

covering the insurance coverage until the couple will reached their 80 years. This is means if any

of the couple would die then the beneficent mentioned in the policy would be going to have the

term life cover amount (Biggs, 2020). It is helpful for protecting children or other partner in the

event of the death of the person on whom the beneficent is dependent. Therefore, it would be

recommended to Raj & Sangeeta to retain their term life cover which would provide financial

support to other partner if any of them would die before arriving the age of 80 years. This

insurance cover was suggested to be retained because it has been assumed that the surviving

partner would be the only recipient of the proceedings of the insurance cover.

Funeral cover: The couple is having a funeral cover that should also be retained with

them in order to safeguard the surviving partner from spending their savings or taking on any

additional debts. This cover would be helpful in covering costs associated with the funeral

activities. At this point, the cover provides with the amount necessary for meeting the funeral

requirements and accordingly, there is no requirements for using the hard earned monies out of

savings.

Trauma cover: This cover taken by Raj & Sangeeta is reaching its maturity within a period of

one year and is meant for protecting them from any expenditure that the couple would be going

to made towards the incidence of any serious illness (Bilkey, Baynam and Molster, 2018). So, it

would be better for the couple to cancel out this cover as it has become expensive for them due

to reaching at an older age. The protection that this cover is offering could be availed through

private insurance cover as well that the couple is planning to get now.

Income protection cover: This cover is available with Raj only due to being provided by

their employer and is going to expire at the age of 65 which is about to arrive. Therefore, this

cover should be retained as it is. This is because it would be going to provide income protection

after the retirement on monthly basis to support financially.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Recommendation of suitable health insurance products

Type of cover recommended: For Raj & Sangeeta, the type of cover that would be recommended

involves the hospitality only or elective surgery cover because it is useful in covering the costs

associated with major medical expenses along with being considered cheaper than

comprehensive health insurance cover (Callander, Fox and Lindsay, 2019). This is policy

provides cover for surgical costs, various tests along with several add on benefits that are

available free of costs and making this type of cover equally advantageous as comprehensive

cover.

Inclusive / exclusive: The Policy that the couple would take is exclusive in order to cover the all

the conditions except those conditions that are specifically excluded from being covered. This

would be helpful for the client (Raj & Sangeeta) in reducing the risk of any condition that could

be covered through exclusive policies over inclusive policies. However, such policies are

comparatively cheaper than that of the inclusive policies because of the unlimited liability of

insurer.

Covering the cost of treatment: With regards to the covering of cost of treatment, there are

several ways in which the costs are covered by health insurance plans. The option of getting

payment as a percentage of treatment cost, or it is limited per treatment is considered to less

attractive against the option of getting maximum amount per policy per annum. Therefore, the

couple should opt for that health insurance cover providing maximum amount per annum under

the policy because the future costs of treatment are not easily predictable, so it better and even a

profitable option for the insured person.

Excess options: Such options are available with health insurance products facilitating insured to

claim for the treatment costs after their claimable amount gets exhausted or used up. Here the

insurer after charging a set excess undertakes to make full payment towards the treatment cost of

insured by keeping their coverage within the maximum limits of the policy (Erlangga and et.al.,

2019). In case of Raj & Sangeeta, this facility would help them in getting the entire amount of

the claim within their policy’s maximum limits after using up the maximum amount of the policy

per annum. For this, Raj & Sangeeta would require to pay for the excess charge on selecting the

“excess option” and in turn, the insurer reduced the amount that is required to be paid towards

Recommendation of suitable health insurance products

Type of cover recommended: For Raj & Sangeeta, the type of cover that would be recommended

involves the hospitality only or elective surgery cover because it is useful in covering the costs

associated with major medical expenses along with being considered cheaper than

comprehensive health insurance cover (Callander, Fox and Lindsay, 2019). This is policy

provides cover for surgical costs, various tests along with several add on benefits that are

available free of costs and making this type of cover equally advantageous as comprehensive

cover.

Inclusive / exclusive: The Policy that the couple would take is exclusive in order to cover the all

the conditions except those conditions that are specifically excluded from being covered. This

would be helpful for the client (Raj & Sangeeta) in reducing the risk of any condition that could

be covered through exclusive policies over inclusive policies. However, such policies are

comparatively cheaper than that of the inclusive policies because of the unlimited liability of

insurer.

Covering the cost of treatment: With regards to the covering of cost of treatment, there are

several ways in which the costs are covered by health insurance plans. The option of getting

payment as a percentage of treatment cost, or it is limited per treatment is considered to less

attractive against the option of getting maximum amount per policy per annum. Therefore, the

couple should opt for that health insurance cover providing maximum amount per annum under

the policy because the future costs of treatment are not easily predictable, so it better and even a

profitable option for the insured person.

Excess options: Such options are available with health insurance products facilitating insured to

claim for the treatment costs after their claimable amount gets exhausted or used up. Here the

insurer after charging a set excess undertakes to make full payment towards the treatment cost of

insured by keeping their coverage within the maximum limits of the policy (Erlangga and et.al.,

2019). In case of Raj & Sangeeta, this facility would help them in getting the entire amount of

the claim within their policy’s maximum limits after using up the maximum amount of the policy

per annum. For this, Raj & Sangeeta would require to pay for the excess charge on selecting the

“excess option” and in turn, the insurer reduced the amount that is required to be paid towards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the policy’s premium. There are two types of excess option available to Raj & Sangeeta that is,

fixed % per claim and fixed maximum excess per annum. It would be better for Raj & Sangeeta

to opt for fixed maximum excess per annum. Suppose, if the trauma surgery of Raj would cost

them $50000 and the fixed maximum excess per annum is $2000 per annum. In this case, the

policy would cover the amount of $48000 and the client (Raj & Sangeeta) would be having

limited liability of just $2000.

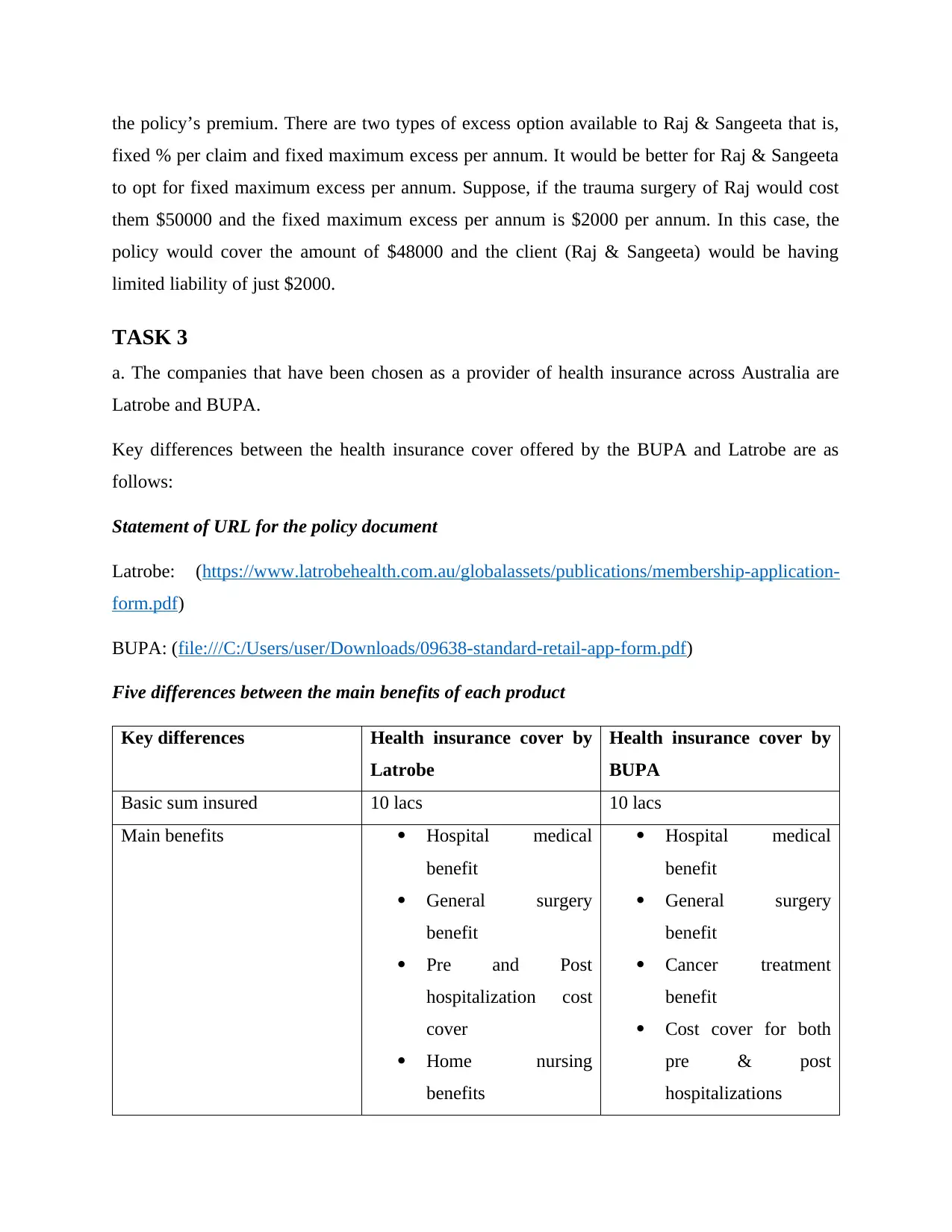

TASK 3

a. The companies that have been chosen as a provider of health insurance across Australia are

Latrobe and BUPA.

Key differences between the health insurance cover offered by the BUPA and Latrobe are as

follows:

Statement of URL for the policy document

Latrobe: (https://www.latrobehealth.com.au/globalassets/publications/membership-application-

form.pdf)

BUPA: (file:///C:/Users/user/Downloads/09638-standard-retail-app-form.pdf)

Five differences between the main benefits of each product

Key differences Health insurance cover by

Latrobe

Health insurance cover by

BUPA

Basic sum insured 10 lacs 10 lacs

Main benefits Hospital medical

benefit

General surgery

benefit

Pre and Post

hospitalization cost

cover

Home nursing

benefits

Hospital medical

benefit

General surgery

benefit

Cancer treatment

benefit

Cost cover for both

pre & post

hospitalizations

fixed % per claim and fixed maximum excess per annum. It would be better for Raj & Sangeeta

to opt for fixed maximum excess per annum. Suppose, if the trauma surgery of Raj would cost

them $50000 and the fixed maximum excess per annum is $2000 per annum. In this case, the

policy would cover the amount of $48000 and the client (Raj & Sangeeta) would be having

limited liability of just $2000.

TASK 3

a. The companies that have been chosen as a provider of health insurance across Australia are

Latrobe and BUPA.

Key differences between the health insurance cover offered by the BUPA and Latrobe are as

follows:

Statement of URL for the policy document

Latrobe: (https://www.latrobehealth.com.au/globalassets/publications/membership-application-

form.pdf)

BUPA: (file:///C:/Users/user/Downloads/09638-standard-retail-app-form.pdf)

Five differences between the main benefits of each product

Key differences Health insurance cover by

Latrobe

Health insurance cover by

BUPA

Basic sum insured 10 lacs 10 lacs

Main benefits Hospital medical

benefit

General surgery

benefit

Pre and Post

hospitalization cost

cover

Home nursing

benefits

Hospital medical

benefit

General surgery

benefit

Cancer treatment

benefit

Cost cover for both

pre & post

hospitalizations

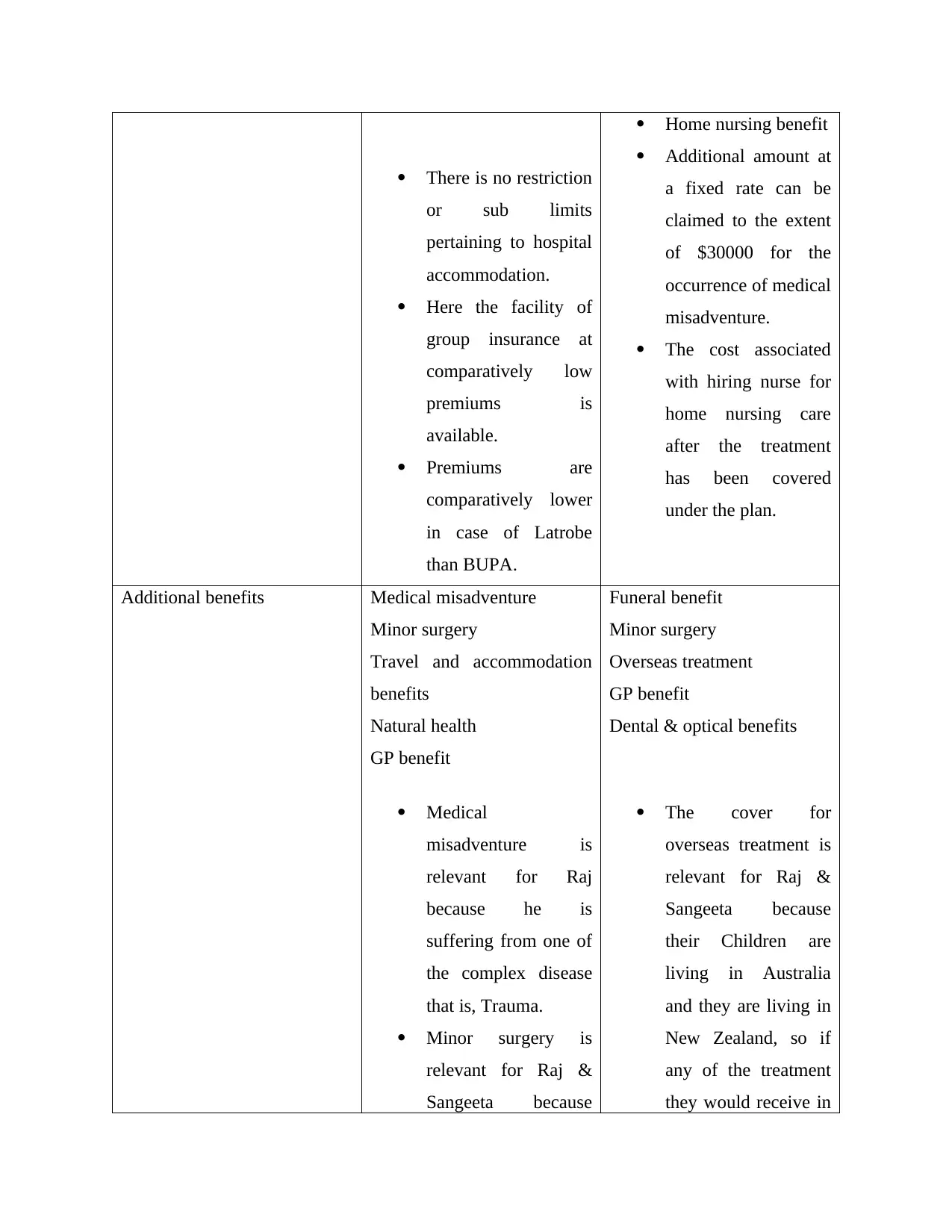

There is no restriction

or sub limits

pertaining to hospital

accommodation.

Here the facility of

group insurance at

comparatively low

premiums is

available.

Premiums are

comparatively lower

in case of Latrobe

than BUPA.

Home nursing benefit

Additional amount at

a fixed rate can be

claimed to the extent

of $30000 for the

occurrence of medical

misadventure.

The cost associated

with hiring nurse for

home nursing care

after the treatment

has been covered

under the plan.

Additional benefits Medical misadventure

Minor surgery

Travel and accommodation

benefits

Natural health

GP benefit

Medical

misadventure is

relevant for Raj

because he is

suffering from one of

the complex disease

that is, Trauma.

Minor surgery is

relevant for Raj &

Sangeeta because

Funeral benefit

Minor surgery

Overseas treatment

GP benefit

Dental & optical benefits

The cover for

overseas treatment is

relevant for Raj &

Sangeeta because

their Children are

living in Australia

and they are living in

New Zealand, so if

any of the treatment

they would receive in

or sub limits

pertaining to hospital

accommodation.

Here the facility of

group insurance at

comparatively low

premiums is

available.

Premiums are

comparatively lower

in case of Latrobe

than BUPA.

Home nursing benefit

Additional amount at

a fixed rate can be

claimed to the extent

of $30000 for the

occurrence of medical

misadventure.

The cost associated

with hiring nurse for

home nursing care

after the treatment

has been covered

under the plan.

Additional benefits Medical misadventure

Minor surgery

Travel and accommodation

benefits

Natural health

GP benefit

Medical

misadventure is

relevant for Raj

because he is

suffering from one of

the complex disease

that is, Trauma.

Minor surgery is

relevant for Raj &

Sangeeta because

Funeral benefit

Minor surgery

Overseas treatment

GP benefit

Dental & optical benefits

The cover for

overseas treatment is

relevant for Raj &

Sangeeta because

their Children are

living in Australia

and they are living in

New Zealand, so if

any of the treatment

they would receive in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they are at older age

and the frequent visit

to GP for minor

surgery or treatment

is normal.

Australia can also be

covered under the

plan.

At an older age like

the one from which

Raj & Sangeeta are

passing through, there

usually seems a

random visit for

dental & optical care.

So, the health

insurance cover

should provide for the

same.

Policy exclusions The cover does not provide

for the pre – existing disease

under the health insurance

policy.

All the treatment arising

from or related to pregnancy

are not covered under the

insurance plan offered by

Latrobe (Duckett, Cowgill

and Nemet, 2019).

The cosmetic surgery or

therapies related to it are not

covered under this private

health cover.

There is also no cover

available for pre-existing

disease and surgeries related

to cosmetics.

Health screening is also not

covered under this plan.

The assistance obtained with

regards to infertility or

reproduction is not covered

under the health insurance

product offered by BUPA.

and the frequent visit

to GP for minor

surgery or treatment

is normal.

Australia can also be

covered under the

plan.

At an older age like

the one from which

Raj & Sangeeta are

passing through, there

usually seems a

random visit for

dental & optical care.

So, the health

insurance cover

should provide for the

same.

Policy exclusions The cover does not provide

for the pre – existing disease

under the health insurance

policy.

All the treatment arising

from or related to pregnancy

are not covered under the

insurance plan offered by

Latrobe (Duckett, Cowgill

and Nemet, 2019).

The cosmetic surgery or

therapies related to it are not

covered under this private

health cover.

There is also no cover

available for pre-existing

disease and surgeries related

to cosmetics.

Health screening is also not

covered under this plan.

The assistance obtained with

regards to infertility or

reproduction is not covered

under the health insurance

product offered by BUPA.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Choosing a different Add on benefit

Latrobe: Travel & accommodation benefit

BUPA: Funeral benefit

The importance of these add on benefit to Raj & Sangeeta

The travel and accommodation benefit is important to Raj & Sangeeta because if they would

receive their treatment in Australia where their children are living, then this benefit would be

helpful in covering the cost of travel to the place of treatment in other country or city (Biggs,

2020).

Also, the funeral benefit provides the surviving partner with the facility of claiming the expenses

incurred for the funeral related activities.

TASK 4

From the discussion done in Task 3, the health insurance product offered by Latrobe is suitable

for Raj & Sangeeta. This is because it is providing more number of main benefits than BUPA

along with the facility of group insurance at lower premiums (Mooney, 2020). Further, the

additional benefits include the benefits like treatment related to natural health deterioration, GP

visits, cover for travel & accommodation costs, minor surgeries as well as the medical

misadventure which is possible in case of Raj due to suffering from trauma. The travel &

accommodation is beneficial in covering the additional costs associated with taking oversees

treatment while the GP visits on a frequent basis are normal in case of older people like Raj &

Sangeeta. The exclusions associated with this product is not of greater significance because

exclusion pertaining to pre-existing disease and cosmetic surgeries are common in all plans

while the coverage for pregnancy related costs would definitely not relevant in case of older

people like Raj & Sangeeta.

TASK 5

a. Steps involved in the application process

Usually different insurers have their own specific application process, the following are the key

steps that are necessarily required to be their while applying for the insurance policy (Dineen-

Griffin, Benrimoj and Garcia-Cardenas, 2020).

Latrobe: Travel & accommodation benefit

BUPA: Funeral benefit

The importance of these add on benefit to Raj & Sangeeta

The travel and accommodation benefit is important to Raj & Sangeeta because if they would

receive their treatment in Australia where their children are living, then this benefit would be

helpful in covering the cost of travel to the place of treatment in other country or city (Biggs,

2020).

Also, the funeral benefit provides the surviving partner with the facility of claiming the expenses

incurred for the funeral related activities.

TASK 4

From the discussion done in Task 3, the health insurance product offered by Latrobe is suitable

for Raj & Sangeeta. This is because it is providing more number of main benefits than BUPA

along with the facility of group insurance at lower premiums (Mooney, 2020). Further, the

additional benefits include the benefits like treatment related to natural health deterioration, GP

visits, cover for travel & accommodation costs, minor surgeries as well as the medical

misadventure which is possible in case of Raj due to suffering from trauma. The travel &

accommodation is beneficial in covering the additional costs associated with taking oversees

treatment while the GP visits on a frequent basis are normal in case of older people like Raj &

Sangeeta. The exclusions associated with this product is not of greater significance because

exclusion pertaining to pre-existing disease and cosmetic surgeries are common in all plans

while the coverage for pregnancy related costs would definitely not relevant in case of older

people like Raj & Sangeeta.

TASK 5

a. Steps involved in the application process

Usually different insurers have their own specific application process, the following are the key

steps that are necessarily required to be their while applying for the insurance policy (Dineen-

Griffin, Benrimoj and Garcia-Cardenas, 2020).

Step 1: Completion of the application form: After deciding the type of insurance product that Raj

& Sangeeta are planning to buy, they need to complete the application form that is being

provided by the insurer.

Step 2: Underwriting: Here the assessment & appropriate verification of the applicant is done by

the insurer to determine the risk associated with their client.

Step 3: Acceptance or amended terms: Here the application made by the client for the policy gets

accepted on the determined conditions & rates and the contract of insurance comes into place.

Step 4: Policy issue: After signing & accepting the terms by the clients, the policy is being

issued.

b.

The principle of utmost good faith: According to this principle, it is must for both the insurer as

well as the insured to act in a transparent manner and accordingly disclose all the material facts

and essential information to each other while signing up for the health insurance policy (Bilkey,

Baynam and Molster, 2018).

The purpose of declaration & consent section at the end of the application is to confirm that the

information provided by the client is complete & true. It gives rise to the insurer’s requirement of

getting notified of the changes taking place in the health of insured from the date of application

till the commencement of the policy.

The role of the underwriter includes the assessment of risk that is being posed by the applicants.

Based on the assessment, the applicants are classified as falling in the category of standard risk

sun-standard risk and deferred (Harvey and Campbell, 2020). Accordingly, the rates for the

premiums are determined. In case of Raj & Sangeeta, the private health insurance cover would

be fall in the category of sub-standard risk as they are at older age and Raj is having the risk of

getting suffered from trauma.

Insurer’s duty of disclosure:

The insurer’s duty of disclosure is such that they need to tell client about each and every

term and conditions of their insurance policy. They should provide client with the hard and soft

copy of term and conditions (Pradana, 2021).

& Sangeeta are planning to buy, they need to complete the application form that is being

provided by the insurer.

Step 2: Underwriting: Here the assessment & appropriate verification of the applicant is done by

the insurer to determine the risk associated with their client.

Step 3: Acceptance or amended terms: Here the application made by the client for the policy gets

accepted on the determined conditions & rates and the contract of insurance comes into place.

Step 4: Policy issue: After signing & accepting the terms by the clients, the policy is being

issued.

b.

The principle of utmost good faith: According to this principle, it is must for both the insurer as

well as the insured to act in a transparent manner and accordingly disclose all the material facts

and essential information to each other while signing up for the health insurance policy (Bilkey,

Baynam and Molster, 2018).

The purpose of declaration & consent section at the end of the application is to confirm that the

information provided by the client is complete & true. It gives rise to the insurer’s requirement of

getting notified of the changes taking place in the health of insured from the date of application

till the commencement of the policy.

The role of the underwriter includes the assessment of risk that is being posed by the applicants.

Based on the assessment, the applicants are classified as falling in the category of standard risk

sun-standard risk and deferred (Harvey and Campbell, 2020). Accordingly, the rates for the

premiums are determined. In case of Raj & Sangeeta, the private health insurance cover would

be fall in the category of sub-standard risk as they are at older age and Raj is having the risk of

getting suffered from trauma.

Insurer’s duty of disclosure:

The insurer’s duty of disclosure is such that they need to tell client about each and every

term and conditions of their insurance policy. They should provide client with the hard and soft

copy of term and conditions (Pradana, 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 6

1.

After analyzing the case of Sangeeta, the best way to claim the health insurance under health

insurance policy is that Sangeeta should seek prior-approval from the health insurer. It is best for

the client who knows whether their medical issue cover under the insurance agreement terms and

condition or not. Under this way, the health insurer of Sangeeta will arrange to pay medical

provider directly which means less than any excess. But in case, if Sangeeta won’t know about

whether their medical issue covered under insurance or not than she can decide to pay the for the

treatment or can wait to know whether it have been done under the public system. Here,

Sangeeta is also required to ask for the referral to a specialist from its GP to file online form of

health insurance (Hick and Murphy, 2021). This helps the patient to claim the cost of treatment

from insurance company.

2.

The three insurer’s requirement that have to be follow by Sangeeta to settle the claim are as

follows:

A completed pre-approval claim form.

A copy of referral letter as well as the clinical notes of Sangeeta’s General Practitioner

(GP).

An estimate for cost of Sangeeta’s hip surgery.

TASK 7

1.

In the situation when the health policy of insurance was lapsed due to the non-payment of due

for more than 3 months and insured have adviser, in that case, insurance company make the

adviser aware of the non-payment and potential lapses (Unruh and et.al., 2022). The adviser

would initially try to contact insured to resolve this situation. They should also contact and hire

advocate to have the policy reinstated and the arrears paid.

2.

1.

After analyzing the case of Sangeeta, the best way to claim the health insurance under health

insurance policy is that Sangeeta should seek prior-approval from the health insurer. It is best for

the client who knows whether their medical issue cover under the insurance agreement terms and

condition or not. Under this way, the health insurer of Sangeeta will arrange to pay medical

provider directly which means less than any excess. But in case, if Sangeeta won’t know about

whether their medical issue covered under insurance or not than she can decide to pay the for the

treatment or can wait to know whether it have been done under the public system. Here,

Sangeeta is also required to ask for the referral to a specialist from its GP to file online form of

health insurance (Hick and Murphy, 2021). This helps the patient to claim the cost of treatment

from insurance company.

2.

The three insurer’s requirement that have to be follow by Sangeeta to settle the claim are as

follows:

A completed pre-approval claim form.

A copy of referral letter as well as the clinical notes of Sangeeta’s General Practitioner

(GP).

An estimate for cost of Sangeeta’s hip surgery.

TASK 7

1.

In the situation when the health policy of insurance was lapsed due to the non-payment of due

for more than 3 months and insured have adviser, in that case, insurance company make the

adviser aware of the non-payment and potential lapses (Unruh and et.al., 2022). The adviser

would initially try to contact insured to resolve this situation. They should also contact and hire

advocate to have the policy reinstated and the arrears paid.

2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The risk arising from this situation is as follows:

Cancellation of policy.

The cover will not further restart until all missed payment was done by client.

Cancellation of policy.

The cover will not further restart until all missed payment was done by client.

REFERENCES

Books and Journals

Biggs, A., 2020. COVID-19 and private health insurance.

Bilkey, G. A., Baynam, G. and Molster, C., 2018. Changes to the employers' use of genetic

information and non-discrimination for health insurance in the USA: implications for

Australians. Frontiers in Public Health. 6. p.183.

Callander, E. J., Fox, H. and Lindsay, D., 2019. Out-of-pocket healthcare expenditure in

Australia: trends, inequalities and the impact on household living standards in a high-

income country with a universal health care system. Health economics review. 9(1). pp.1-

8.

Dineen-Griffin, S., Benrimoj, S. I. and Garcia-Cardenas, V., 2020. Primary health care policy

and vision for community pharmacy and pharmacists in Australia. Pharmacy Practice

(Granada). 18(2).

Duckett, S., Cowgill, M. and Nemet, K., 2019. Saving Private Health 2: Making private health

insurance viable.

Erlangga, D. and et.al., 2019. The impact of public health insurance on health care utilisation,

financial protection and health status in low-and middle-income countries: A systematic

review. PloS one. 14(8). p.e0219731.

Harvey, D. R. and Campbell, R., 2020. Private eyes…, hips, etc: Health insurance benefits

during the Covid crisis.

Hick, R. and Murphy, M. P., 2021. Common shock, different paths? Comparing social policy

responses to COVID‐19 in the UK and Ireland. Social Policy & Administration. 55(2).

pp.312-325.

Mooney, G., 2020. Economics and Australian health policy. Routledge.

Pradana, A. W., 2021. Policyholder protection for insurance companies with default claims:

comparative analysis in Indonesia and the UK. Borobudur Law Review. 3(1). pp.1-15.

Books and Journals

Biggs, A., 2020. COVID-19 and private health insurance.

Bilkey, G. A., Baynam, G. and Molster, C., 2018. Changes to the employers' use of genetic

information and non-discrimination for health insurance in the USA: implications for

Australians. Frontiers in Public Health. 6. p.183.

Callander, E. J., Fox, H. and Lindsay, D., 2019. Out-of-pocket healthcare expenditure in

Australia: trends, inequalities and the impact on household living standards in a high-

income country with a universal health care system. Health economics review. 9(1). pp.1-

8.

Dineen-Griffin, S., Benrimoj, S. I. and Garcia-Cardenas, V., 2020. Primary health care policy

and vision for community pharmacy and pharmacists in Australia. Pharmacy Practice

(Granada). 18(2).

Duckett, S., Cowgill, M. and Nemet, K., 2019. Saving Private Health 2: Making private health

insurance viable.

Erlangga, D. and et.al., 2019. The impact of public health insurance on health care utilisation,

financial protection and health status in low-and middle-income countries: A systematic

review. PloS one. 14(8). p.e0219731.

Harvey, D. R. and Campbell, R., 2020. Private eyes…, hips, etc: Health insurance benefits

during the Covid crisis.

Hick, R. and Murphy, M. P., 2021. Common shock, different paths? Comparing social policy

responses to COVID‐19 in the UK and Ireland. Social Policy & Administration. 55(2).

pp.312-325.

Mooney, G., 2020. Economics and Australian health policy. Routledge.

Pradana, A. W., 2021. Policyholder protection for insurance companies with default claims:

comparative analysis in Indonesia and the UK. Borobudur Law Review. 3(1). pp.1-15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.