Management Accounting Systems Report: Decision Making at Heath Retail

VerifiedAdded on 2020/06/04

|15

|5072

|37

Report

AI Summary

This report provides a comprehensive analysis of Management Accounting (MA) systems, focusing on their application within Heath Retail. The report begins by introducing the significance of MA and its tools, emphasizing how it assists in cost control and resource optimization. It explores specific MA systems such as inventory management, price optimization, job costing, and cost accounting, detailing their advantages and disadvantages within a retail context. The report then examines managerial reporting, highlighting its role in decision-making, with examples like performance reports, costing reports, and debtor reports. Furthermore, it evaluates costing methods, comparing absorption and marginal costing, and their impact on profit margin calculations. The report offers practical insights into how these MA tools and techniques can enhance financial strategies and improve decision-making processes within Heath Retail. This document, contributed by a student, is available on Desklib, a platform for students offering AI-powered study tools and resources.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

P1 Reporting to the management team of Heath about the need of MA systems within the

firm.........................................................................................................................................1

P2 Stating how managerial reports help manager in decision making..................................3

P3 Evaluation of cost and profit margin on the basis of absorption and marginal costing

method....................................................................................................................................5

P4 Identifying planning tools associated with the field of MA.............................................8

P5 Presenting and evaluating ways of MA that assist in responding monetary problems or

issues....................................................................................................................................10

CONCLUSION........................................................................................................................11

INTRODUCTION......................................................................................................................1

P1 Reporting to the management team of Heath about the need of MA systems within the

firm.........................................................................................................................................1

P2 Stating how managerial reports help manager in decision making..................................3

P3 Evaluation of cost and profit margin on the basis of absorption and marginal costing

method....................................................................................................................................5

P4 Identifying planning tools associated with the field of MA.............................................8

P5 Presenting and evaluating ways of MA that assist in responding monetary problems or

issues....................................................................................................................................10

CONCLUSION........................................................................................................................11

INTRODUCTION

In order to carry out business operations & functions smoothly it is required for the

manager to undertake the tools and techniques of management accounting. Moreover,

techniques of MA provide highly level of assistance in exerting control on cost and hrps in

making optimum use of resources. By undertaking tactics of MA firm can evaluate the

performance of each & every department and thereby would become able to take suitable

measure for performance management as well as improvement. For the project of MA, Heath

retail store has been selected that provides customers with the grocery and other services at

suitable price level. The main motive of such retail store is to enhance customer base and

profitability aspect by exerting control on expenditure or cost. In this, present report will

provide deeper insight about the systems of MA that firm can undertake for optimum

utilization of funds. Further, it also entails the manner in managerial accounting report offers

valuable information to the management team for decision making. Along with this, it also

depicts or describe the planning tools and other techniques of MA that assist in mitigating

financial deficiencies.

P1 Reporting to the management team of Heath about the need of MA systems within the

firm

To

Management Team

HEATH

Date: 7th December 2017

Subject: Management Accounting Systems

Introduction: This report is prepared on the systems of management accounting which in turn provide

information to the management about the extent to which use of tools are essentially required.

Main body:

Meaning of Management Accounting: It is the process that helps in preparing day to day managerial

reports. Hence, MA is highly concerned with the process of collecting, analyzing and reporting

information to the management team that is associated with the internal operations.

Significance of Management Accounting:

MA provides accurate financial information to the manager and aid in decision

making aspect.

By using MA tools and techniques HEATH can develop competent plan for the

In order to carry out business operations & functions smoothly it is required for the

manager to undertake the tools and techniques of management accounting. Moreover,

techniques of MA provide highly level of assistance in exerting control on cost and hrps in

making optimum use of resources. By undertaking tactics of MA firm can evaluate the

performance of each & every department and thereby would become able to take suitable

measure for performance management as well as improvement. For the project of MA, Heath

retail store has been selected that provides customers with the grocery and other services at

suitable price level. The main motive of such retail store is to enhance customer base and

profitability aspect by exerting control on expenditure or cost. In this, present report will

provide deeper insight about the systems of MA that firm can undertake for optimum

utilization of funds. Further, it also entails the manner in managerial accounting report offers

valuable information to the management team for decision making. Along with this, it also

depicts or describe the planning tools and other techniques of MA that assist in mitigating

financial deficiencies.

P1 Reporting to the management team of Heath about the need of MA systems within the

firm

To

Management Team

HEATH

Date: 7th December 2017

Subject: Management Accounting Systems

Introduction: This report is prepared on the systems of management accounting which in turn provide

information to the management about the extent to which use of tools are essentially required.

Main body:

Meaning of Management Accounting: It is the process that helps in preparing day to day managerial

reports. Hence, MA is highly concerned with the process of collecting, analyzing and reporting

information to the management team that is associated with the internal operations.

Significance of Management Accounting:

MA provides accurate financial information to the manager and aid in decision

making aspect.

By using MA tools and techniques HEATH can develop competent plan for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

upcoming time period.

MA assists in increasing efficiency of business operations as it helps in measuring

performance and gives indication for performance enhancement.

By undertaking MA tools HEATH can take suitable decision whether to produce in

house or buy outside.

Types of MA

Inventory management: This tool of MA facilitates effective supply chain management and give

indication about the limit to which inventory needs to be ordered as well as stored. There are several

techniques that can be undertaken for effective inventory management such as Just in Time (JIT),

economic order quantity (EOQ), stock requirement planning etc (Messner, 2016). It is highly required

for HEATH to maintain inventory by using management tools which in turn ensures smooth

functioning of operations.

Advantages: By using the tools of inventory management, HEATH can control cost and enhance

profit margin. In addition to this, by providing customers with product on time firm can enhance their

satisfaction to a great extent.

Disadvantages: Company faces difficulty in assessing suitable tool that needs to be considered for

managing inventory. Further, for managing record of stock firm requires highly talented personnel

which in turn also impose issue in front of firm.

Price optimization: In the dynamic business arena, firm can attain success only when it offers product

or services to the customers at competitive prices. Thus, by employing the system of price

optimization HEATH can identify how much customers want to pay for the products or services. This

system of MA helps in developing plan in against to the competitors and contributes in the success.

Advantages: It encourages HEATH to exert control on operating cost or expenses and helps in

grabbing high market share. Further, price optimization system of MA also helps company in making

planning pertaining to both price as well as profit margin.

Disadvantage: Price optimization system of MA is not suitable for all the industries because in some

sectors customers give high level of preference to the price level. On the other side, in some industries

customers compare price with the quality of product or services.

Job costing: In the field of MA, job costing method is highly effective which in turn lays focus on the

accumulation of cost pertaining to material, labour and overhead. HEATH can use this tool for

tracking the cost of individual jobs and become able to examine that it can be reduced in later jobs or

not.

Advantages: Business entity of HEATH can estimate basis for further evaluation by taking into

account job costing method. By using such technique, manager can do detailed analysis of each in the

context of material, labour and overhead expenses (Kristensen, Nielsen and Grasso, 2016). Along

with this, job costing is suitable when price of the contract is determined on the basis of cost.

MA assists in increasing efficiency of business operations as it helps in measuring

performance and gives indication for performance enhancement.

By undertaking MA tools HEATH can take suitable decision whether to produce in

house or buy outside.

Types of MA

Inventory management: This tool of MA facilitates effective supply chain management and give

indication about the limit to which inventory needs to be ordered as well as stored. There are several

techniques that can be undertaken for effective inventory management such as Just in Time (JIT),

economic order quantity (EOQ), stock requirement planning etc (Messner, 2016). It is highly required

for HEATH to maintain inventory by using management tools which in turn ensures smooth

functioning of operations.

Advantages: By using the tools of inventory management, HEATH can control cost and enhance

profit margin. In addition to this, by providing customers with product on time firm can enhance their

satisfaction to a great extent.

Disadvantages: Company faces difficulty in assessing suitable tool that needs to be considered for

managing inventory. Further, for managing record of stock firm requires highly talented personnel

which in turn also impose issue in front of firm.

Price optimization: In the dynamic business arena, firm can attain success only when it offers product

or services to the customers at competitive prices. Thus, by employing the system of price

optimization HEATH can identify how much customers want to pay for the products or services. This

system of MA helps in developing plan in against to the competitors and contributes in the success.

Advantages: It encourages HEATH to exert control on operating cost or expenses and helps in

grabbing high market share. Further, price optimization system of MA also helps company in making

planning pertaining to both price as well as profit margin.

Disadvantage: Price optimization system of MA is not suitable for all the industries because in some

sectors customers give high level of preference to the price level. On the other side, in some industries

customers compare price with the quality of product or services.

Job costing: In the field of MA, job costing method is highly effective which in turn lays focus on the

accumulation of cost pertaining to material, labour and overhead. HEATH can use this tool for

tracking the cost of individual jobs and become able to examine that it can be reduced in later jobs or

not.

Advantages: Business entity of HEATH can estimate basis for further evaluation by taking into

account job costing method. By using such technique, manager can do detailed analysis of each in the

context of material, labour and overhead expenses (Kristensen, Nielsen and Grasso, 2016). Along

with this, job costing is suitable when price of the contract is determined on the basis of cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages: In this, detailed clerical work or analysis is required to create framework for decision

making. Due to the more clerical work high level of probability exists in relation to error.

Cost accounting: It may be served as a process that is undertaken by the business unit with the motive

to collect information about the cost incurred in relation to performing activities. Requirement of

using cost accounting system in the context of concerned retail unit is highly significant. By using

such system manager can collect information about cost incurred and would become able to take

decision about pricing and profitability aspect (Weetman, 2016). Cost accounting system enables firm

to assess the areas where business unit is earning or losing money.

Advantages: Cost accounting system of MA helps in identifying unprofitable activities and enables

management to take strict measure for the elimination of wastage. In addition to this, cost accounting

system also helps in disclosing both profitable and non-profitable activities. Hence, by doing

assessment of the cost, management can assess unprofitable activities and explore operations in the

profitable area.

Disadvantages: Lack of uniformity in the process is recognized as one of the main weaknesses of cost

accounting. Along with this, principles and conversions of cost accounting are not highly developed

which in turn places direct on outcome assessed for the purpose of decision making (Otley, 2016).

Conclusion: For getting success in the competitive business environment HEATH is required to

consider the tools of MA for evaluating performance. By undertaking, cost accounting, inventory

management and price optimization system HEATH can develop effective future plans.

Sincerely

Management Accountant

P2 Stating how managerial reports help manager in decision making

To

Management Team

HEATH

Date: 7th December 2017

Subject: Managerial Reporting Systems

Introduction: The present report will depict the significance of managerial reporting and its

contribution in the decision making. It also entails different reports that can be prepared by HEATH

for measuring and examining the performance of department in a prominent way.

Main Body

Managerial reports contain information about the performance of each department and helps in taking

effective decisions. It is the process that focuses on summarizing information pertaining to financial

aspects.

Need and significance of managerial reports

making. Due to the more clerical work high level of probability exists in relation to error.

Cost accounting: It may be served as a process that is undertaken by the business unit with the motive

to collect information about the cost incurred in relation to performing activities. Requirement of

using cost accounting system in the context of concerned retail unit is highly significant. By using

such system manager can collect information about cost incurred and would become able to take

decision about pricing and profitability aspect (Weetman, 2016). Cost accounting system enables firm

to assess the areas where business unit is earning or losing money.

Advantages: Cost accounting system of MA helps in identifying unprofitable activities and enables

management to take strict measure for the elimination of wastage. In addition to this, cost accounting

system also helps in disclosing both profitable and non-profitable activities. Hence, by doing

assessment of the cost, management can assess unprofitable activities and explore operations in the

profitable area.

Disadvantages: Lack of uniformity in the process is recognized as one of the main weaknesses of cost

accounting. Along with this, principles and conversions of cost accounting are not highly developed

which in turn places direct on outcome assessed for the purpose of decision making (Otley, 2016).

Conclusion: For getting success in the competitive business environment HEATH is required to

consider the tools of MA for evaluating performance. By undertaking, cost accounting, inventory

management and price optimization system HEATH can develop effective future plans.

Sincerely

Management Accountant

P2 Stating how managerial reports help manager in decision making

To

Management Team

HEATH

Date: 7th December 2017

Subject: Managerial Reporting Systems

Introduction: The present report will depict the significance of managerial reporting and its

contribution in the decision making. It also entails different reports that can be prepared by HEATH

for measuring and examining the performance of department in a prominent way.

Main Body

Managerial reports contain information about the performance of each department and helps in taking

effective decisions. It is the process that focuses on summarizing information pertaining to financial

aspects.

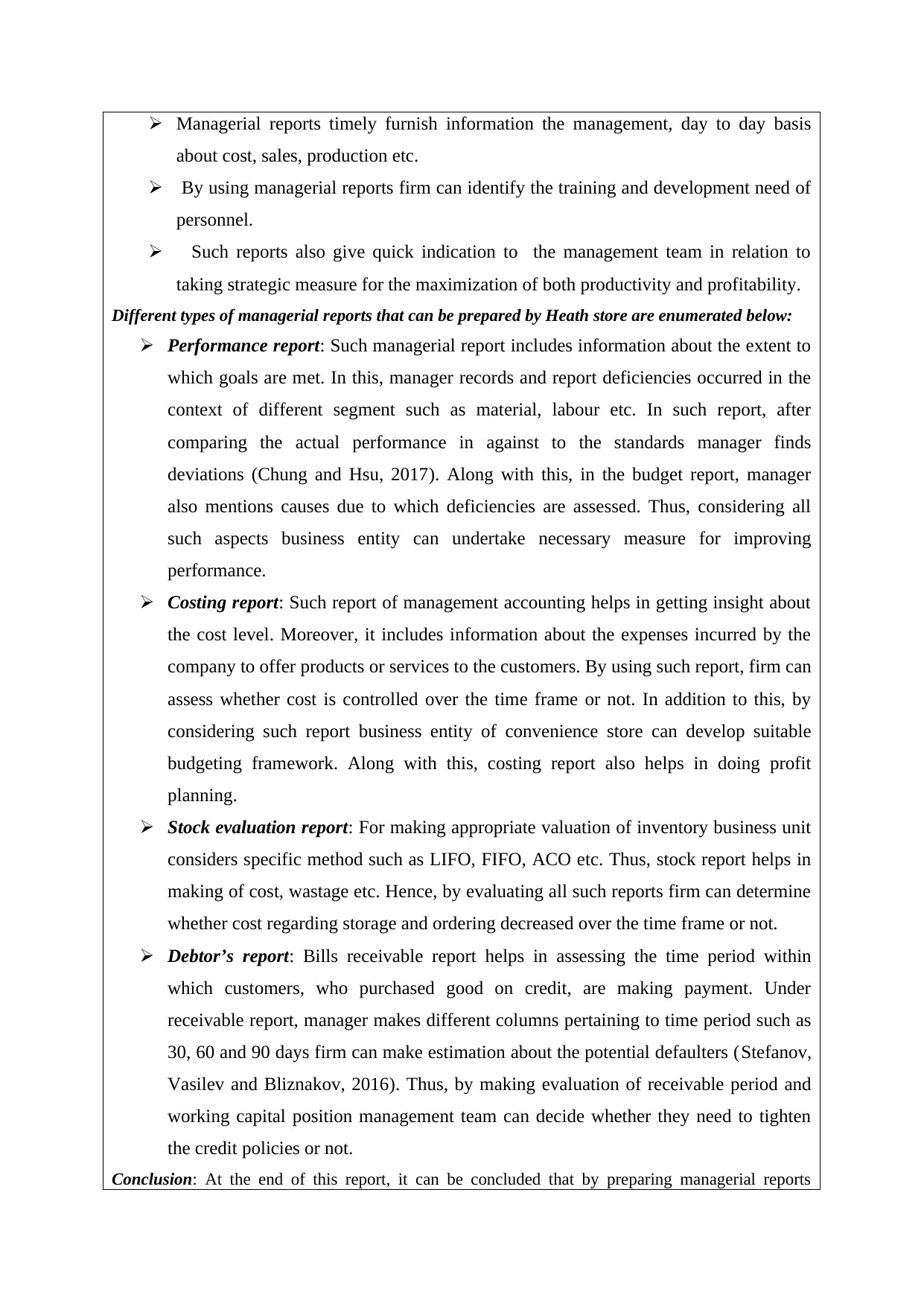

Need and significance of managerial reports

Managerial reports timely furnish information the management, day to day basis

about cost, sales, production etc.

By using managerial reports firm can identify the training and development need of

personnel.

Such reports also give quick indication to the management team in relation to

taking strategic measure for the maximization of both productivity and profitability.

Different types of managerial reports that can be prepared by Heath store are enumerated below:

Performance report: Such managerial report includes information about the extent to

which goals are met. In this, manager records and report deficiencies occurred in the

context of different segment such as material, labour etc. In such report, after

comparing the actual performance in against to the standards manager finds

deviations (Chung and Hsu, 2017). Along with this, in the budget report, manager

also mentions causes due to which deficiencies are assessed. Thus, considering all

such aspects business entity can undertake necessary measure for improving

performance.

Costing report: Such report of management accounting helps in getting insight about

the cost level. Moreover, it includes information about the expenses incurred by the

company to offer products or services to the customers. By using such report, firm can

assess whether cost is controlled over the time frame or not. In addition to this, by

considering such report business entity of convenience store can develop suitable

budgeting framework. Along with this, costing report also helps in doing profit

planning.

Stock evaluation report: For making appropriate valuation of inventory business unit

considers specific method such as LIFO, FIFO, ACO etc. Thus, stock report helps in

making of cost, wastage etc. Hence, by evaluating all such reports firm can determine

whether cost regarding storage and ordering decreased over the time frame or not.

Debtor’s report: Bills receivable report helps in assessing the time period within

which customers, who purchased good on credit, are making payment. Under

receivable report, manager makes different columns pertaining to time period such as

30, 60 and 90 days firm can make estimation about the potential defaulters (Stefanov,

Vasilev and Bliznakov, 2016). Thus, by making evaluation of receivable period and

working capital position management team can decide whether they need to tighten

the credit policies or not.

Conclusion: At the end of this report, it can be concluded that by preparing managerial reports

about cost, sales, production etc.

By using managerial reports firm can identify the training and development need of

personnel.

Such reports also give quick indication to the management team in relation to

taking strategic measure for the maximization of both productivity and profitability.

Different types of managerial reports that can be prepared by Heath store are enumerated below:

Performance report: Such managerial report includes information about the extent to

which goals are met. In this, manager records and report deficiencies occurred in the

context of different segment such as material, labour etc. In such report, after

comparing the actual performance in against to the standards manager finds

deviations (Chung and Hsu, 2017). Along with this, in the budget report, manager

also mentions causes due to which deficiencies are assessed. Thus, considering all

such aspects business entity can undertake necessary measure for improving

performance.

Costing report: Such report of management accounting helps in getting insight about

the cost level. Moreover, it includes information about the expenses incurred by the

company to offer products or services to the customers. By using such report, firm can

assess whether cost is controlled over the time frame or not. In addition to this, by

considering such report business entity of convenience store can develop suitable

budgeting framework. Along with this, costing report also helps in doing profit

planning.

Stock evaluation report: For making appropriate valuation of inventory business unit

considers specific method such as LIFO, FIFO, ACO etc. Thus, stock report helps in

making of cost, wastage etc. Hence, by evaluating all such reports firm can determine

whether cost regarding storage and ordering decreased over the time frame or not.

Debtor’s report: Bills receivable report helps in assessing the time period within

which customers, who purchased good on credit, are making payment. Under

receivable report, manager makes different columns pertaining to time period such as

30, 60 and 90 days firm can make estimation about the potential defaulters (Stefanov,

Vasilev and Bliznakov, 2016). Thus, by making evaluation of receivable period and

working capital position management team can decide whether they need to tighten

the credit policies or not.

Conclusion: At the end of this report, it can be concluded that by preparing managerial reports

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

HEATH can identify deviations within the suitable time. Along with this, through preparing and

evaluating debtors as well as inventory report firm can develop appropriate policy framework for

decision making.

Sincerely

Management Accountant

P3 Evaluation of cost and profit margin on the basis of absorption and marginal costing

method

Absorption costing: In the modern business context, now business units are making

focus on undertaking full costing method which is also known as absorption. Moreover, it

considers both fixed and variable cost while doing valuation of inventory as well as margin.

Under absorption costing method, value of inventory is higher because it valued at total

production cost. International Accounting standards 2 also exhibit that absorption costing is

the best method of inventory valuation as compared to others. Thus, by using such full

costing method manager of Heath can do valuation of stock and profit margin more

effectually. Moreover, such costing method assumes that fixed cost can be recovered by the

firm so it needs to be considered at the time stock as well as gross and net profit evaluation.

Marginal costing: This costing method helps manager in getting information about

the cost that needs to be incurred on the production of one additional unit. Hence, direct

material, labour, overhead and other components that are considered while doing evaluation

of cost as well as profit margin as per marginal costing method (Difference Between

Absorption Costing and Marginal Costing, 2017). Hence, referring the same, it can be

presented that in marginal costing method variable expenses are recognized as product cost,

whereas fixed expenditures considered a periodical. Marginal costing method aid in decision

making and grab the attention of management about the changes take place in results or cost

under consideration. By using such method, management team of Heath can assess the

contribution and profit margin associated with per unit of output. Hence, through undertaking

such method manager can present the effect of changes take place in activity. Further, in

marginal costing, closing stock, WIP and finished goods are valued at variable cost.

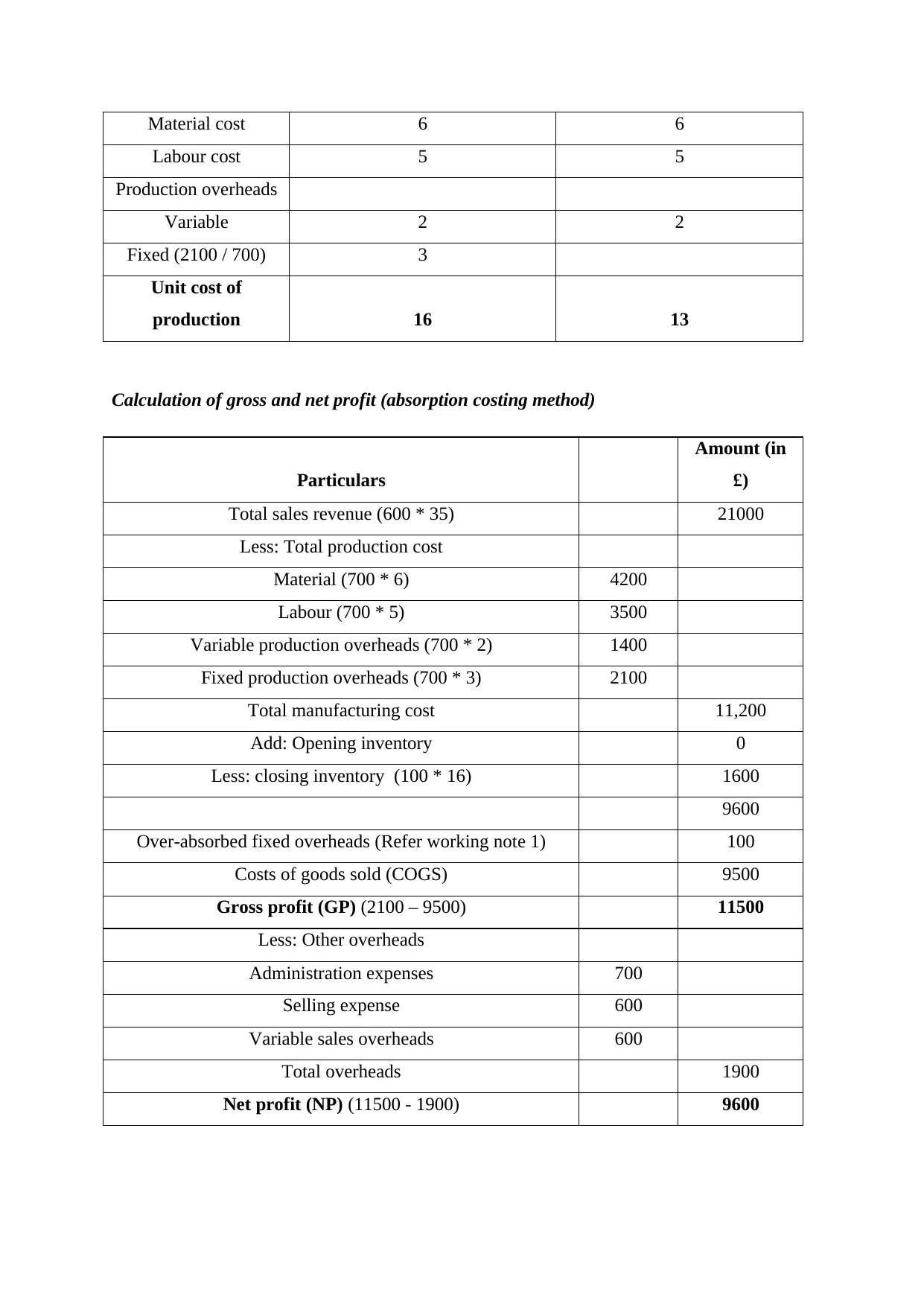

Unit cost assessment (absorption and marginal costing method)

Particulars

Absorption costing ( per unit)

in £

Marginal costing (per unit in

£)

evaluating debtors as well as inventory report firm can develop appropriate policy framework for

decision making.

Sincerely

Management Accountant

P3 Evaluation of cost and profit margin on the basis of absorption and marginal costing

method

Absorption costing: In the modern business context, now business units are making

focus on undertaking full costing method which is also known as absorption. Moreover, it

considers both fixed and variable cost while doing valuation of inventory as well as margin.

Under absorption costing method, value of inventory is higher because it valued at total

production cost. International Accounting standards 2 also exhibit that absorption costing is

the best method of inventory valuation as compared to others. Thus, by using such full

costing method manager of Heath can do valuation of stock and profit margin more

effectually. Moreover, such costing method assumes that fixed cost can be recovered by the

firm so it needs to be considered at the time stock as well as gross and net profit evaluation.

Marginal costing: This costing method helps manager in getting information about

the cost that needs to be incurred on the production of one additional unit. Hence, direct

material, labour, overhead and other components that are considered while doing evaluation

of cost as well as profit margin as per marginal costing method (Difference Between

Absorption Costing and Marginal Costing, 2017). Hence, referring the same, it can be

presented that in marginal costing method variable expenses are recognized as product cost,

whereas fixed expenditures considered a periodical. Marginal costing method aid in decision

making and grab the attention of management about the changes take place in results or cost

under consideration. By using such method, management team of Heath can assess the

contribution and profit margin associated with per unit of output. Hence, through undertaking

such method manager can present the effect of changes take place in activity. Further, in

marginal costing, closing stock, WIP and finished goods are valued at variable cost.

Unit cost assessment (absorption and marginal costing method)

Particulars

Absorption costing ( per unit)

in £

Marginal costing (per unit in

£)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material cost 6 6

Labour cost 5 5

Production overheads

Variable 2 2

Fixed (2100 / 700) 3

Unit cost of

production 16 13

Calculation of gross and net profit (absorption costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material (700 * 6) 4200

Labour (700 * 5) 3500

Variable production overheads (700 * 2) 1400

Fixed production overheads (700 * 3) 2100

Total manufacturing cost 11,200

Add: Opening inventory 0

Less: closing inventory (100 * 16) 1600

9600

Over-absorbed fixed overheads (Refer working note 1) 100

Costs of goods sold (COGS) 9500

Gross profit (GP) (2100 – 9500) 11500

Less: Other overheads

Administration expenses 700

Selling expense 600

Variable sales overheads 600

Total overheads 1900

Net profit (NP) (11500 - 1900) 9600

Labour cost 5 5

Production overheads

Variable 2 2

Fixed (2100 / 700) 3

Unit cost of

production 16 13

Calculation of gross and net profit (absorption costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material (700 * 6) 4200

Labour (700 * 5) 3500

Variable production overheads (700 * 2) 1400

Fixed production overheads (700 * 3) 2100

Total manufacturing cost 11,200

Add: Opening inventory 0

Less: closing inventory (100 * 16) 1600

9600

Over-absorbed fixed overheads (Refer working note 1) 100

Costs of goods sold (COGS) 9500

Gross profit (GP) (2100 – 9500) 11500

Less: Other overheads

Administration expenses 700

Selling expense 600

Variable sales overheads 600

Total overheads 1900

Net profit (NP) (11500 - 1900) 9600

Income statement (Marginal costing method)

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material cost (700 * 6) 4,200

Labour cost (700 * 5) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost (4200 + 3500) 9,100

Add: Inventory at the beginning of the year 0

Less: Stock at the end of year (100 * 13) 1300

Costs of goods sold (COGS) 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution 12,600

Less: Other overheads

Administration expenses 800

Selling and distribution expenditure 600

Fixed production cost 2000

Total overhead cost 3400

NP (12600 – 3400) 9,200

Reconciliation statement as per marginal and absorption costing is enumerated below:

Particulars Amount (in £)

NP (absorption costing method) 9,600

Less: Fixed production overhead on closing stock (100 * 3) 300

Less: Over-Absorbed overheads 100

Net profit on the basis of marginal costing method 9,200

Interpretation: The above depicted table shows that unit cost of production under

absorption and marginal costing method accounts for £16 & £13 respectively. The rationale

Particulars

Amount (in

£)

Total sales revenue (600 * 35) 21000

Less: Total production cost

Material cost (700 * 6) 4,200

Labour cost (700 * 5) 3,500

Variable production overheads (700 units @ 2 PU) 1,400

Total production cost (4200 + 3500) 9,100

Add: Inventory at the beginning of the year 0

Less: Stock at the end of year (100 * 13) 1300

Costs of goods sold (COGS) 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution 12,600

Less: Other overheads

Administration expenses 800

Selling and distribution expenditure 600

Fixed production cost 2000

Total overhead cost 3400

NP (12600 – 3400) 9,200

Reconciliation statement as per marginal and absorption costing is enumerated below:

Particulars Amount (in £)

NP (absorption costing method) 9,600

Less: Fixed production overhead on closing stock (100 * 3) 300

Less: Over-Absorbed overheads 100

Net profit on the basis of marginal costing method 9,200

Interpretation: The above depicted table shows that unit cost of production under

absorption and marginal costing method accounts for £16 & £13 respectively. The rationale

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

behind increasing cost as per absorption method is the inclusion of fixed production overhead

implies for £3 significantly. By doing assessment, it has found that gross and net profit

margin under absorption costing method accounts for £11500 & £9600. On the other side, as

per marginal costing method contribution of £12600 & net margin of £9200 has found.

Referring the overall evaluation, it can be said that due to the consideration of fixed

production overhead GP as per absorption costing method is lower as compared to

contribution determined through marginal technique. Thus, absorption costing presents

solution by taking into account both fixed as well as variable cost while determining gross

and net profit margin.

P4 Identifying planning tools associated with the field of MA

Financial planning and decision making is highly important for the business

organization to build or sustain competitive edge over others. Thus, by preparing competent

financial plan Heath can employ monetary resources in an appropriate manner. Hence, by

undertaking or considering below mentioned tool firm can do effectual planning such as:

Zero base budgeting (ZBB): By using ZBB, Heath can set suitable budgeting or

financial framework for the upcoming time period. Such modern technique of budgeting may

be served as a bottom-up approach and sustainable cost philosophy which in turn facilitates

optimum allocation of financial resources. It allows firm to save cost and reinvest the same in

the long term growth opportunities such as innovation and product development. Moreover,

in this, manager starts with zero bases and after justifying all the expenses set budgeting

framework (Zero-Based Budgeting, 2017). This method encourages manager to find cost

effective ways to perform business activities and functions. By taking into account all the

above depicted methods, it can be presented that such technique helps in developing

competent financial plan.

Advantages: Technique of ZBB is highly significant which in turn assists firm in

reducing cost and improving both efficiency as well as competitiveness. Such technique of

budgeting helps in preventing take over and assessing top performers. By using ZBB, firm

can indulge cost conscious culture within the firm.

Disadvantages: Sometimes, ZBB technique negatively affects employee morale and

motivation. Moreover, company that follows such technique take strict measure or action

who failed to perform as per the budgeted figures. Along with this, to prepare budget in

accordance with ZBB business unit requires more financial and human resources.

implies for £3 significantly. By doing assessment, it has found that gross and net profit

margin under absorption costing method accounts for £11500 & £9600. On the other side, as

per marginal costing method contribution of £12600 & net margin of £9200 has found.

Referring the overall evaluation, it can be said that due to the consideration of fixed

production overhead GP as per absorption costing method is lower as compared to

contribution determined through marginal technique. Thus, absorption costing presents

solution by taking into account both fixed as well as variable cost while determining gross

and net profit margin.

P4 Identifying planning tools associated with the field of MA

Financial planning and decision making is highly important for the business

organization to build or sustain competitive edge over others. Thus, by preparing competent

financial plan Heath can employ monetary resources in an appropriate manner. Hence, by

undertaking or considering below mentioned tool firm can do effectual planning such as:

Zero base budgeting (ZBB): By using ZBB, Heath can set suitable budgeting or

financial framework for the upcoming time period. Such modern technique of budgeting may

be served as a bottom-up approach and sustainable cost philosophy which in turn facilitates

optimum allocation of financial resources. It allows firm to save cost and reinvest the same in

the long term growth opportunities such as innovation and product development. Moreover,

in this, manager starts with zero bases and after justifying all the expenses set budgeting

framework (Zero-Based Budgeting, 2017). This method encourages manager to find cost

effective ways to perform business activities and functions. By taking into account all the

above depicted methods, it can be presented that such technique helps in developing

competent financial plan.

Advantages: Technique of ZBB is highly significant which in turn assists firm in

reducing cost and improving both efficiency as well as competitiveness. Such technique of

budgeting helps in preventing take over and assessing top performers. By using ZBB, firm

can indulge cost conscious culture within the firm.

Disadvantages: Sometimes, ZBB technique negatively affects employee morale and

motivation. Moreover, company that follows such technique take strict measure or action

who failed to perform as per the budgeted figures. Along with this, to prepare budget in

accordance with ZBB business unit requires more financial and human resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based budget: From assessment, it has identified that cost determination as

per ABBs highly accurate and reliable. Moreover, in this, on the basis of relevant cost driver

firm makes assessment and allocation of overhead expenses. Thus, in the modern business

arena, ABB may be served as the most effectual technique that helps business in developing

competent framework.

Advantages: It helps in determining cost and effect relationship between the concerned

activities. Along with this, by undertaking ABB Heath can set fair prices for multi-products

because in this allocation is based on relevant drivers (Advantages And Disadvantages Of

Activity-Based Costing (ABC), 2017). Further, by using ABB, Heath can take prominent

decision pertaining to the profitability of different product lines.

Disadvantages: In ABB, concerned authority faces difficulty in evaluating the activities that

have an impact on cost aspects. Along with this, in ABB, accountant also faces issue in

evaluating cost on the basis of activities (Disadvantages of Activity-Based Budgeting, 2017).

Further, it is suitable for only large sized manufacturing firms rather than small one.

Moreover, for setting budgeting framework as per ABB company has to organize training

session for personnel.

Responsibility budgeting: In the case of such budgeting, manager of different

departments are accountable to give report to supervisory head on routine basis. Hence,

reports which are presented by different responsibility centre’s such as sales, profit, expenses

etc contain information about operational results of the areas as well as items for which they

are responsible to control. Thus, management team of the firm can take timely input from the

managers and would become able to make suitable modifications in existing strategic as well

as policy framework.

Advantages: Responsibility budgeting system establishes sound control system within the

firm and thereby improves performance. By using such budgeting tool management team of

Heath can delegate roles and responsibilities of personnel. Promptness in reporting is

considered as major strengths or advantage of responsibility budgeting system.

Disadvantages: Under responsibility budgeting, way of expenses classification is the subject

of further analysis and highly difficult. Further, regular reporting system is considered as time

intensive activity or exercise.

per ABBs highly accurate and reliable. Moreover, in this, on the basis of relevant cost driver

firm makes assessment and allocation of overhead expenses. Thus, in the modern business

arena, ABB may be served as the most effectual technique that helps business in developing

competent framework.

Advantages: It helps in determining cost and effect relationship between the concerned

activities. Along with this, by undertaking ABB Heath can set fair prices for multi-products

because in this allocation is based on relevant drivers (Advantages And Disadvantages Of

Activity-Based Costing (ABC), 2017). Further, by using ABB, Heath can take prominent

decision pertaining to the profitability of different product lines.

Disadvantages: In ABB, concerned authority faces difficulty in evaluating the activities that

have an impact on cost aspects. Along with this, in ABB, accountant also faces issue in

evaluating cost on the basis of activities (Disadvantages of Activity-Based Budgeting, 2017).

Further, it is suitable for only large sized manufacturing firms rather than small one.

Moreover, for setting budgeting framework as per ABB company has to organize training

session for personnel.

Responsibility budgeting: In the case of such budgeting, manager of different

departments are accountable to give report to supervisory head on routine basis. Hence,

reports which are presented by different responsibility centre’s such as sales, profit, expenses

etc contain information about operational results of the areas as well as items for which they

are responsible to control. Thus, management team of the firm can take timely input from the

managers and would become able to make suitable modifications in existing strategic as well

as policy framework.

Advantages: Responsibility budgeting system establishes sound control system within the

firm and thereby improves performance. By using such budgeting tool management team of

Heath can delegate roles and responsibilities of personnel. Promptness in reporting is

considered as major strengths or advantage of responsibility budgeting system.

Disadvantages: Under responsibility budgeting, way of expenses classification is the subject

of further analysis and highly difficult. Further, regular reporting system is considered as time

intensive activity or exercise.

Standard costing: It may be presented as the powerful system that provides assistance

in controlling cost to the significant level. System of standard costing enables company to do

planning pertaining to budget more effectually. In this, manager makes estimation of the cost

pertaining to production process. Hence, before the initiation of new accounting period firm

sets standards regarding material, labour, overhead, sales and profit. Thus, on the basis of

such method, standards are used to set a plan or budget for the production process.

Considering the standards setting down as per such costing method firm performs the

evaluation of actual outcomes in against to the budgeted figures (Standard Costing -

Meaning, Advantages and Disadvantages, 2015). On the basis of such aspect, by identifying

deviations and taking corrective action for improvement firm can attain success. Hence,

Heath will get following benefits by undertaking such budgeting tool or method:

Advantages: Standard costing method helps in controlling cost through eliminating wastage

and inefficiency. It also helps in locating areas that demand for improvement and fixing the

accountability of personnel for each variance. In addition to this, standard costing method

assists in making improvement in the methods and operations through providing guidance in

relation to production as well as pricing policies.

Disadvantages: In this, when deviations are assessed then personnel entail that standards

which are setting down by Heath not realistic in nature (Kim and Schmidgall, 2017). Further,

sector where changes take place in the technological aspects standard costing method does

not give suitable outcome. In addition to this, for setting standards business entities require

technical skills.

Variance analysis: Contribution of such technique is vita in the planning as well as

decision making aspect of firm. Moreover, it provides management team with the information

about the reasons due to which firm failed to attain predetermined results. Hence, by

investigating the causes of deviations and taking appropriate measure firm can significantly

improve deficiencies. Hence, through undertaking this, Heath store can prepare plan and

become able to get favourable outcome or results.

P5 Presenting and evaluating ways of MA that assist in responding monetary problems or

issues

For the attainment of goals, it is highly required for the business unit to resolve

financial problems within the appropriate time frame. Hence, by adapting following aspect

Heath retail store avoid monetary issues in the best possible way such as:

in controlling cost to the significant level. System of standard costing enables company to do

planning pertaining to budget more effectually. In this, manager makes estimation of the cost

pertaining to production process. Hence, before the initiation of new accounting period firm

sets standards regarding material, labour, overhead, sales and profit. Thus, on the basis of

such method, standards are used to set a plan or budget for the production process.

Considering the standards setting down as per such costing method firm performs the

evaluation of actual outcomes in against to the budgeted figures (Standard Costing -

Meaning, Advantages and Disadvantages, 2015). On the basis of such aspect, by identifying

deviations and taking corrective action for improvement firm can attain success. Hence,

Heath will get following benefits by undertaking such budgeting tool or method:

Advantages: Standard costing method helps in controlling cost through eliminating wastage

and inefficiency. It also helps in locating areas that demand for improvement and fixing the

accountability of personnel for each variance. In addition to this, standard costing method

assists in making improvement in the methods and operations through providing guidance in

relation to production as well as pricing policies.

Disadvantages: In this, when deviations are assessed then personnel entail that standards

which are setting down by Heath not realistic in nature (Kim and Schmidgall, 2017). Further,

sector where changes take place in the technological aspects standard costing method does

not give suitable outcome. In addition to this, for setting standards business entities require

technical skills.

Variance analysis: Contribution of such technique is vita in the planning as well as

decision making aspect of firm. Moreover, it provides management team with the information

about the reasons due to which firm failed to attain predetermined results. Hence, by

investigating the causes of deviations and taking appropriate measure firm can significantly

improve deficiencies. Hence, through undertaking this, Heath store can prepare plan and

become able to get favourable outcome or results.

P5 Presenting and evaluating ways of MA that assist in responding monetary problems or

issues

For the attainment of goals, it is highly required for the business unit to resolve

financial problems within the appropriate time frame. Hence, by adapting following aspect

Heath retail store avoid monetary issues in the best possible way such as:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.